hsbc_org1

DESCRIPTION

Report on HSBCTRANSCRIPT

Chapter 1: An Overview

1.1 Report Origin

As a mandatory requirement of the Masters of the Business Administration (MBA)

program under Asian University, this report entitled - "HSBC Consumer Product,

Credit Operation & Collection Procedure in Bangladesh" - is a connived depiction of

the three months long internship program at Personal Financial Services – Consumer

Credit Risk (PFS CCR) in The Hongkong and Shanghai Banking Corporation Ltd.

The organization attachment started on February 15, 2000 and finished on April 15,

2000. My organization supervisor Mr. Kamruzzaman Mamun (Credit Manager,

Personal Financial Services, Anchor Tower, HSBC) assigned me the topic of the term

paper & my institution supervisor at Asian University Mr. Sirker, duly approved it.

1.2 Purpose

The purposes of this report cognates the internship purpose. The internship objective is

to gather practical knowledge and experiencing the corporate working environment

with the close approximation to the business firm and the experts who are leading and

making strategic decisions to enhance the growth of a financial institution. To this

regard this report is contemplating the knowledge and experience accumulated from

internship program. With the set guidelines and proposal by the Asian University and

with the kind advices of the organization and the internship supervisor, this report

comprise of an organization part and a project part.

The prime objective of organization part is:

To present an overview and brief introduction of HongKong and Shanghai

Banking Corporation Ltd.

The prime objectives of project part are:

Give a very brief overview of the risk analysis criteria for loan assessment.

Analysis the demography of the skip customers.

Find out if there is any relationship among the skip customers.

1.3 Scope

The scope of this report is limited to the overall description of the company, its services

and its financial performance analysis. The scope of the study is limited to

organizational setup, functions, and performances Since HSBC is still in its growth

stage in Bangladesh; it has still to go a long way to achieve its destination. The report

will mainly focus on what criteria HSBC Bangladesh is maintaining before approving

the loan facility. And if there is relationship among the customers who are defaulting to

pay the installments accordingly.

1.4 Methodology

Both the primary as well as the secondary form of information was used to prepare the

report. The details of these sources are highlighted below.

Primary Sources:

Customer database and historical data of delinquent customers.

Interviews with the approval officers as well as the sales and collection

teams.

Secondary Sources:

Internal Sources

► HSBC Collection Manual

► HSBC Bank's Annual Report

► Group Business Principal Manual

► Group Instruction Manual (GIM) & Business Instruction Manual

(BIM)

External Sources

► Different books and periodicals related to the banking sector

► Bangladesh Bank Circulars

► Newspapers

► Website information

Data collecting instruments:

In-depth interview

► During the exploratory research, in-depth interviews were conducted

with managers, approval officers, mobile sales officers (MSO) &

collection tea of HSBC.

1.5 Limitations

Being an intern of “Personal Financial Services – MIS department” of

HSBC Anchor Tower, it was difficult to stay in continuous contact with

other departments.

As per Bank’s compliance, as an intern I was unable to obtain indispensable

experiences of different departments.

Details of many aspects of the services of HSBC Bangladesh Limited have

been skipped in this report due to various constraints, including time and

space, security reason.

One of the main barriers in writing this report was the confidentiality of data. Though I

had access to lot of information regarding the performance of the bank, I am unable and

not authorized to use this information due to legal restrictions.

Chapter 2: Introduction to HSBC Group

HSBC Mission Statement:

“We aim to satisfy our customers with high quality service that reflects our global

image as the premier international bank”

Objectives of HSBC:

HSBC’s objectives are to provide innovative products supported by quality delivery of

systems and excellence customer services, to train and motivate staffs and to exercise

social responsibility. By combining regional strengths with group network HSBC’s aim

is to be the one of the leading banks in its principle markets. HSBC’s goal is to achieve

sustained earnings growth and to continue to enhance shareholders value.

2.1 An Overview of HSBC Group

The HSBC Group is named after its founding member, The Hongkong and Shanghai

Banking Corporation Limited, which was established in 1865 in Hong Kong and

Shanghai to finance the growing trade between China and Europe.

Thomas Sutherland, a Hong Kong Superintendent of the Peninsular and Oriental Steam

Navigation Company helped to establish this bank in March 1865. Throughout the late

nineteenth and the early twentieth centuries, the bank established a network of agencies

and branches based mainly in China and South East Asia but also with representation in

the Indian sub-continent, Japan, Europe and North America.

The post-war political and economic changes in the world forced the bank to analyze its

strategy for continued growth in the 1950s. The bank diversified both its business and

its geographical spread through acquisitions and alliances.

HSBC Holdings plc, the parent company of the HSBC Group, was established in 1991

with its shares quoted on both the London and Hong Kong stock exchanges. The HSBC

Group now comprises a unique range of banks and financial service providers around

the globe.

HSBC maintains one of the world’s largest private data communication networks and is

reconfiguring its business for the e-age. Its rapidly growing e-commerce capability

includes the use of the internet, PC banking over a private network, interactive TV, and

fixed and mobile, including wireless application protocol or WAP-enabled mobile,

telephones.

2.2 HSBC History

The HSBC Group has a history, which is unique. Many of its principal companies

opened for business over a century ago and they have a history rich in variety and

achievement.

Foundation and Growth:

The inspiration behind the founding of the bank was Thomas Sutherland, a Scot who

was then working as the Hong Kong Superintendent of the Peninsular and Oriental

Steam Navigation Company. Realizing the considerable demand for local banking

facilities both in Hong Kong and along the China coast and he helped to establish the

bank in March 1865. Then, as now, the bank's headquarters were at 1 Queen's Road

Central in Hong Kong and a branch was opened one month later in Shanghai.

Throughout the late nineteenth and the early twentieth centuries, the bank established a

network of agencies and branches based mainly in China and South East Asia but also

with representation in the Indian sub-continent, Japan, Europe and North America. In

many of its branches the bank was the pioneer of modern banking practices. From the

outset, trade finance was a strong feature of the bank's business with gold bars,

exchange and merchant banking also playing an important part. Additionally, the bank

issued notes in many countries throughout the Far East.

During the Second World War the bank was forced to close many branches and its head

office was temporarily moved to London. However, after the war the bank played a key

role in the reconstruction of the Hong Kong economy and began to further diversify the

geographical spread of the bank.

The Making of the modern HSBC Group:

The post-war political and economic changes in the world forced the bank to analyze its

strategy for continued growth in the 1950s. The bank diversified both its business and

its geographical spread through acquisitions and alliances. This strategy culminated in

1992 with one of the largest bank acquisitions in history when HSBC Holdings

acquired the UK’s Midland Bank plc (now called HSBC Bank plc). However, it

remained committed to its historical markets and played an important part in the

reconstruction of Hong Kong where its branch network continued to expand.

2.3 Banks under the HSBC Group

Many of the members have changed their name into HSBC, The Hongkong and

Shanghai Banking Corporation Limited to introduce the whole group under one brand

name.

Midland Bank HSBC Holdings acquired Midland Bank one of the principal UK

clearing banks in 1992. Headquartered in London, the bank has a

personal customer base of five and a half million, business customers of

over half a million, and a network of almost 1,700 branches in the

United Kingdom. Midland has offices in 28 countries and territories,

principally in continental Europe, with a number of offices in Latin

America.

Hang Seng Bank

Hang Seng Bank, in which Hongkong Bank has a 62.1% equity

interest, maintains a network of 146 branches in the Hong Kong SAR,

where it is the second largest locally incorporated bank after Hongkong

Bank. Hang Seng Bank also has a branch in Singapore and two branches

and two representative offices in China.

Marine Midland Bank

Marine Midland Bank headquartered in Buffalo, New York, has 380

banking locations statewide. The bank serves over two million personal

customers and 120,000 commercial and institutional customers in New

York State and, in selected businesses, throughout the United States.

Hongkong Bank of Canada

Hongkong Bank of Canada is the largest foreign-owned bank in

Canada and the country’s seventh-largest bank. With headquarters in

Vancouver, it has 116 branches across Canada and two branches in the

western United States.

Banco HSBC Bamerindus

Banco HSBC Bamerindus was established in Brazil in 1997. The bank

has network of some 1,900 branches and sub-branches, the second

largest in Brazil.

Hongkong Bank Malaysia

Hongkong Bank Malaysia is the largest foreign-owned bank in

Malaysia and the country’s fifth-largest bank, with 36 branches.

The British Bank of the Middle East (British Bank)

The British Bank of the Middle East (British Bank) is the largest and

most widely represented international bank in the Middle East, with 31

branches throughout the United Arab Emirates, Oman, Bahrain, Qatar,

Jordan, Lebanon and the Palestinian Autonomous Area, including an

offshore banking unit in Bahrain. The bank also has branches in

Mumbai and Trivandrum, India, and Baku, Azerbaijan, as well as

private banking operations in London and Geneva.

HSBC Banco Roberts

HSBC Banco Roberts was acquired in 1997. Based in Buenos Aires, it

is one of Argentina’s largest privately owned banks, with 60 branches

throughout the country.

Hongkong Bank of Australia

Hongkong Bank of Australia has 16 branches across Australia. It is

the flagship of the HSBC Group’s businesses there, operating under the

name HSBC Australia, and providing a complete range of financial

services.

The Saudi British Bank

The Saudi British Bank, a 40%-owned member of the HSBC Group,

has 63 branches throughout Saudi Arabia and a branch in London.

Figure 1: Banks under the HSBC Group

Other associated Group banks are British Arab Commercial Bank, The Cyprus

Popular Bank and Egyptian British Bank.

2.4 Customer Segments of HSBC Group

Personal

Financial Services

HSBC provides a full range of personal financial services, including

current and savings account, mortgages, insurance, credit cards, loans,

pensions and investments. In 2000, residential mortgages across the

Group – excluding Household – grew by 15%, while non-mortgage

personal lending increased by over 20%. Credit cards in issue grew by

20% worldwide. Sales of repayment protection insurance and deposit

growth reached record levels. Current account balances in the UK

exceeded £ 10 billion for the first time at year-end 2000. The number of

customers registered for e-banking services – via the internet and

telephone – more than trebled in 2000. The internet generated sales of

over 2.3 million products and 87 million transactions.

Consumer

Finance

Through Household International, Inc., HSBC is now a major provider

of consumer finance and a top 10 issuer of credit cards in the USA.

Household provides consumer loans, credit cards, vehicle finance,

mortgage financing and credit insurance to middle America. During

2004, Household achieved good organic loan growth, which it

supplemented with portfolio acquisitions. The strongest growth was in

the real estate portfolio and the mortgage services business, and also in

branch-based consumer lending. Synergy benefits with HSBC included

store cards and point-of-sale financing.

Commercial

Banking

The provision of services to small and medium-sized enterprises around

the world is core strength of HSBC. During 2000, HSBC increased its

leading position in the UK business start-up market to 21% and attracted

record levels of business current and deposit account balances. Business

internet banking was offered in 20 countries and territories, and the

number of registered users more than doubled to 600,000. Money

transmission revenues, trade finance fees, wealth, savings and insurance

products all showing growth during 2000.

Corporate,

Investment

Banking and

Markets

This customer group comprises four main business lines – Corporate

and Institutional Banking, Global Investment Banking, Global Markets

and Global Transaction Banking – which focus on long-term

relationships with major international corporations and institutions.

Record results were achieved in 2000. The Global Markets business

excelled, particularly in international debt issuance, risk management

and structured products, and foreign exchange. Global Investment

Banking was entrusted with a number of landmark deals in capital

restructuring, corporate reorganization and strategic advice.

Private Banking This customer group provides world-class financial services to high net

worth individuals and their families. In 2000, Private Banking posted

improved financial results in all regions, led by Asia, which had a

record year. New business initiatives and a general improvement in

investment markets led to increased client activity across a range of

products. An increase in discretionary mandates, together with a strong

demand for client-tailored structured products, contributed to higher fee

revenues and dealing income. Funds under management grew by 18%,

reflecting both net inflows of client assets and improving market

conditions.

2.5 HSBC’s International Network

Fig 2: HSBC’s International Networks

The HSBC Group's international network comprises of some 7,000 offices in 80

countries. A brief list is presented below:

2.6 Country Classifications

To ensure that the key resources (management time, capital, human resources and

information technology) are correctly allocated and that the exchange of best practice is

accelerated between entities, the group has classified the countries where it operates

into 3 categories: the large, the major and the international.

These classifications are a function of sustainable, attributable earnings, the number of

retail clients, balance sheet and size of operation. A brief presentation of this

classification is shown below:

Figure 3: Map of HSBC's Country Classifications

Large: United Kingdom, USA and Hong Kong SAR/Mainland China.

Definition

► More than one million personal clients

► Sustainable earnings greater than US$ 200 million

Business Focus

► Concentrated group resources on wealth management

► Be a top 10 player in any market or region served

► Develop cross selling, loyalty programs and value added

products.

Major: Argentina, Canada, Malaysia, India, Kingdom of Saudi Arabia, Singapore and

United Arab Emirates.

Definition

► Sustainable earnings between US$ 100 - 200 million

Business Focus

► Universal bank’s (personal, corporate, and investment

banking with domestic business)

► Platforms for international group business

► Next generation of large companies

► Stable self funding entities

► Onshore HQ

International: The rest of the world.

Definition

Earnings below US$ 100 million

Business Focus

► Platforms for international group business

► Limited domestic presence

► “Nursery” for developing management

► Tomorrow’s major businesses

► Supported by offshore HQ

2.7 International Brand

A key part of the Group’s business strategy, announced in 1998, is the creation of a

global brand featuring the HSBC name and hexagon symbol. The symbol is now a

familiar sight around the world. The Group has embarked on the next phase — making

the HSBC brand universally synonymous with its core values of integrity, trust and

excellent customer service.

HSBC Brand & Corporate Identity:

The Hexagon logo of HSBC derives from HSBC’s traditionally flag, a white rectangle

divided diagonally. The design of the flag was based on the cross of ST.Andrew, The

Patron Saint of Scotland.

HSBC brand & corporate identity represents what HSBC wants its brand to mean to its

customer. It is derived from the group:

Corporate Character:

HSBC is a prudent, cost conscious, ethically grounded, conservative, trustworthy

international builder of long-term customer relationships.

Basic Drives:

HSBC’s basic drives are Higher Productivity, Team Orientation, and Creative

Organization, & Customer Orientation.

The essence of HSBC brand is integrity, trust, and excellent customer service. It gives

confidence to customers, value to investors, & comfort to colleagues.

Through the process of listening to individuals needs and then acting in partnership to

deliver the right solutions, HSBC is committed to help the clients make the most of

their financial assets.

HSBC operate on a global basis, but also work on a local level to ensure the cross-

border differences are identified and any related benefits exploited. HSBC teams of

specialists ensure that whether you need solutions across the world, regionally, or

locally, and they have the skills, expertise, and resources to deliver them. They

automate as many functions as possible, even as ensuring retains control.

HSBC claims that they are the people to talk to if anyone wants the following: -

Global cash flow co-ordination

Enhanced risk management

Improved security and audit controls

Minimized costs and reduced operating expenses

Maximized liquidity, returns and interest benefits

2.8 Group Business Principles and Value

The HSBC Group is committed to Five Core Business Principles:

Outstanding customer service;

Effective and efficient operations;

Strong capital and liquidity;

Conservative lending policy;

Strict expense discipline;

HSBC Operates According to Certain Key Business Values:

The highest personal standards of integrity at all levels;

Commitment to truth and fair dealing;

Hand-on management at all levels;

Openly esteemed commitment to quality and competence;

A minimum of bureaucracy;

Fast decisions and implementation;

Putting the Group’s interests ahead of the individual’s;

The appropriate delegation of authority with accountability;

Fair and objective employer;

A merit approach to recruitment, selection, promotion;

Promotion of good environmental practice and sustainable development and

commitment to the welfare and development of each local community.

HSBC’s reputation is founded on adherence to these principles and values. All actions

taken by a member of HSBC or staff member on behalf of a Group company should

conform to them.

Chapter 3: Overview of HSBC Bangladesh

3.1 HSBC Bangladesh

The HSBC Group is represented in Bangladesh by its Head Office in Dhaka

(Sonargaon Road), a second full-service branch in Chittagong (Agrabad) and two

booths in Gulshan & Motijheel with a vision to satisfy its customer with high quality

service that reflects its global image as the premier International Bank. The Bank has

recently opened another branch in Dhanmondi. The Bank has been serving customers

in Bangladesh since 1996. It has also an Offshore Banking Unit, which provides

banking services for foreign companies based in the Export Processing Zones in Dhaka

and Chittagong. In September 1999, it introduced ATM and telephone banking for

Personal Banking. Five ATMs located at the five branches, there are five off-site ATMs

located in Uttara, Dhanmondi, Banani, Shantinagar and GEC (Chittagong).

3.2 HSBC Bangladesh Overview

Name of the

Organization

The Hong Kong Shanghai Banking Corporation

Bangladesh LTD

Year of Establishment 1996

Head Office Anchor Tower, 1/1-B Sonargaon Road Dhaka 1205,

Bangladesh

Nature of the

organization

Multinational company with subsidiary group in

Bangladesh

Shareholders HSBC group shareholders

Products Savings & deposit services

Loan products

Corporate and Institutional services

Trade services & Hexagon

Management Mr. Mark Humble

Chief Executive Officer

Mr. Joo Baknner

Head of Personal Financial Services

Mr. Adil Islam

Head of Corporate Banking

Mr. Syed Akhtar Hossain Uddin

Human Resource Manager

Mr. Munir Hussain

Marketing Manager

Mr. Wasim Adnan Wahed

Chief Operating Officer

Number of Offices 4 (Dhaka, Motijheel, Gulshan, Dhanmondi, &

Chittagong)

Number of ATM’s 06

Number of employees 250+

Technology Offers full online banking from branch to branch and

from Dhaka to Chittagong.

Service Coverage & Customers

Serves individual and corporate customers within

Dhaka & Chittagong.

HSBC Bangladesh currently provides services from two of its full service branches one

in Dhaka and the other one in Chittagong. Besides these offices there are two personal

banking Booth offices located at Gulshan & Motijheel, and a new branch opened at

Dhanmondi. There is currently nine ATM’s operating in Dhaka and 1 in Chittagong.

3.3 Different Activities in Bangladesh

As one of the largest international banks in Bangladesh, HSBC has a long-term

commitment to its customers and provides a comprehensive range of financial services:

personal, commercial and corporate banking; trade services; cash management;

treasury; consumer & business finance; and securities, and custody services.

Personal Banking Services:

The Hongkong and Shanghai Banking Corporation Limited offers a full range of

personal banking products and services designed to take care of its customers’ growing

needs and requirements. HSBC in Bangladesh has launched a number of loan products

during 2000. Personal Installment Loan is an unsecured loan that does not require any

personal guarantee or cash security; Car Loan, also, does not require any down

payment or personal guarantee. The Bank has already launched Phone banking, a

state-of-the-art automated telephone banking service available 24 hours a day, 7 days a

week, and 365 days a year, which allows customers to access their account from the

comfort of the office or home. HSBC is the market leader in the local Auto pay service

with which the company can initiate bulk Taka payments to, or Taka collections from,

any HSBC current or savings accounts of counterparts for a specified sum at a specified

date, regardless of the branch. HSBC also offers Power vantage, a unique all-in-one

package of products and services designed to give total financial control to the

customer; a unique savings account, which allows the customer to do any number of

transactions without any charges being incurred or credit interest lost. To satisfy the

growing needs of real estate HSBC Bangladesh recently launched Home Loan Scheme

and a special type of deposit product named “Bangladesh International” for non-

resident Bangladeshi.

Corporate Banking Services:

The Hongkong and Shanghai Banking Corporation Limited offers a wide range of cash

financing, working capital, short and medium-term loans and guarantee facilities from

its Head Office and Chittagong branch. The Offshore Banking Unit (OBU) provides

US Dollar denominated working capital as well as short-term finance for capital

imports to eligible businesses. Using high-speed communication links, HSBC connects

customers to international payment systems.

Trade Services:

As the leading provider of trade finance and related services to importers and exporters

in Asia, HSBC in Bangladesh operates a highly automated trade-processing network

and offer an Electronic Data Interchange (EDI) capability through Hexagon. The Bank

also uses SWIFT, an efficient and secure mechanism for bank-to-bank global

communications used for all trade related activities including fund transfers and

issuance of DC’s (Documentary Credit).

Financial Institutions:

HSBC provides global trade services and cash management services to local banks.

HSBC’s worldwide network strength, with over 7000 offices in 81 countries and

territories, coupled with a world class reputation in Trade Finance (“Best Trade

Documentation Bank” – Euro money) and an unparalleled presence in Asia (“Best

Bank in Asia” — Euro money), places HSBC in an ideal position to render unmatched

correspondent banking services.

HSBC’s commanding presence in the USA (5th largest USD clearing bank globally),

UK (largest GBP clearing bank globally), and the Euro land (largest Euro clearing bank

in the UK) both in terms of network strength and clearing ability allows the Bank to

provide first class cash management solutions in 3 major global currencies; US dollar,

Pound sterling, and the Euro.

Payments and Cash Management (PCM):

HSBC is the pioneer in introducing electronic cash management solutions in

Bangladesh, by introducing its state-of-the-art proprietary software, Hexagon, back in

1997. This was initially made available to corporate clients only but has since been

expanded to include banks and retail clients.

With Hexagon, the Bank’s proprietary cash management system, corporate customers

can access banking services from anywhere in the world to view account balances and

statements, make transfers and international payments, and to open documentary

credits, by using only a PC, a modem, and a telephone line.

Chapter 4: An Overview of Functional Departments

4.1 Management of HSBC Bangladesh

HSBC Bangladesh is such a company that has to overcome a lot of hurdles to reach the

position it now holds. At present, Mr. Mark Humble is the CEO; Mr. Adil Islam is the

chief of Corporate Banking; Mr. Adnan Wahed is COO, Mr. Joo baknner is the Chief

of Personal Banking or as known in HSBC, Personal Financial Services (PFS) Head,

and Mr. Syed Akhtar Hossain is the Human Resource Manager at HSBC Bangladesh.

These five men at the top carried out their management roles comprehensively and

systematically. They equally contributed to HSBC’s superior leadership, by carrying

out their unique roles. They worked well together, respecting each other’s abilities, &

arguing openly, & without any resentment when they disagreed.

To maintain a close touch with the organization each man works in separate area of

HSBC’s complex. Their offices are indistinguishable from all other cubicles where

HSBC’s junior executives & secretaries work in. There are no office walls in HSBC

and all the staff starting from the CEO to the lower operating level employees shares

the same premises under one roof. There are no specialized cabins for top management

and executives and also no executive dining rooms. This has created a management

team that is unified, cohesive, & energetic.

Each and every employee of HSBC takes pride of being an employee at HSBC and his

or her pride comes from the freedom of direct communication with the top

management. The management of HSBC is supportive in the sense that the top

management deliberately supports the suggestions, values, ideas, innovation, and hard

work of the employees and officers. Again high amount of employee participation is

encouraged in the management process. There are also systems for awards, incentives,

and status for innovative ideas and hard works. Again the management style can also be

termed as collegial as high amounts of teamwork and participation exists between the

top and bottom parts of HSBC.

HSBC follows a 4 layers management philosophy in Bangladesh. These are Managers,

Executives, Officers, and Assistant Officers. The CEO is the top most authority of all

the levels. Managers are the departmental heads who are responsible for the activities

of their departments. They are the heads of the department who formulate strategies for

that department. e.g. Human Resources Manager. Executives have the authority next to

managers. They are basically responsible for certain activities & organizational

functions. e.g. Admin Executive. These two layers represent the management level of

HSBC Bangladesh.

Officers are the next persons to stand in the hierarchy list. They are the typical mid-

level employees of HSBC organizational hierarchy. These officers are responsible for

managing the operational activities and operating level employees. The operating level

employees of HSBC who are ranked as Assistant Officer fill the last layer of this

hierarchy. They perform the day-to-day operational activities of HSBC. An

organizational hierarchy chart is shown below:

Figure 4: Organizational Hierarchy

4.2 Chief Executive Committee

Executives

Officers

Assistant Officers

Managers

Figure 5: Chief Executive Committee

The organizational structure of HSBC Bangladesh is designed according to the various

service and functional departments. The Chief Executive Officer (CEO) heads the chief

executive committee, which decides on all the strategic aspect of HSBC. The CEO is

the person who supervises the heads of all the departments and also is the ultimate

authority of HSBC Bangladesh. He is responsible for all the activities of HSBC

Bangladesh and all its consequences. He administers all the functional departments and

communicates with the department heads for smooth functioning of the organization.

The HSBC Chief Executive Committee is formed with the heads of all departments

along with the CEO. Besides the CEO the CEC is staffed with 6 more managers:

Manager of Human Resources, Manager of Services, and Manager of Financial

Control Department, Chief of Personal Banking, Chief of Corporate Banking, and

Manager of Marketing.

4.3 Functional Departments of HSBC

HSBC activities are performed through functional departmentalization. So, the

departments are separated according to the functions they perform (HR, Marketing,

Personal Banking, etc.). There are 6 major functional departments at HSBC: Human

Resources Department, Financial Control, Personal Banking, Corporate Banking and

Marketing. Within these major departments there are some other subsidiary

departments that allow smooth operation of their own major departmental function. A

graphical presentation of all the departments (Major & minor) is shown below. Brief

functional descriptions of these departments are-

Figure 6: Functional Departments of HSBC

4.4 Human Resource Department (HR)

The Human Resource Manager currently heads this department. The major functions of

this department are strategic planning and policy formulation for Compensation,

Recruitment, Promotion, Training, and Developments, Personnel Services, and

Security. The HR department is very much concerned with the discipline that is set up

Chief Executive Officer (CEO)

Human Resources

Financial Control

Personal Banking

Corporate Banking

MarketingServices

Administration Administration

Development IT

Internal Control (IC)

Network Service Center (NSC)

HUB

Foreign Correspondence

Payment

Treasury

PCM

DAK Branch

Chittagong Branch

Dhanmondi Branch

Motijheel Booth

Gulshan Booth

Credit Department

Bond, ATM & ATB

Trade Services

Institutional Banking

Hexagon

Direct Sales

Promotion

Marketing Administration

by the HSBC group. HSBC group has got strict rules and regulations for each and

every aspect of banking, even for non-banking purposes; i.e. the Dress Code. All these

major personnel functions are integrated in the best possible way at HSBC, which

results in its higher productivity. The Human resource officer monitors the employee

staffing and administration activities. The Training officer supervises training,

development, & rotation activities. The structure of the HR department is shown below:

Figure 7: Structure of Human Resource Department

HSBC activities are performed through functional departmentalization. So, the

departments are separated according to the functions they perform. Within the major

departments there are some other subsidiary departments that allow smooth operation

of their own major departmental functions.

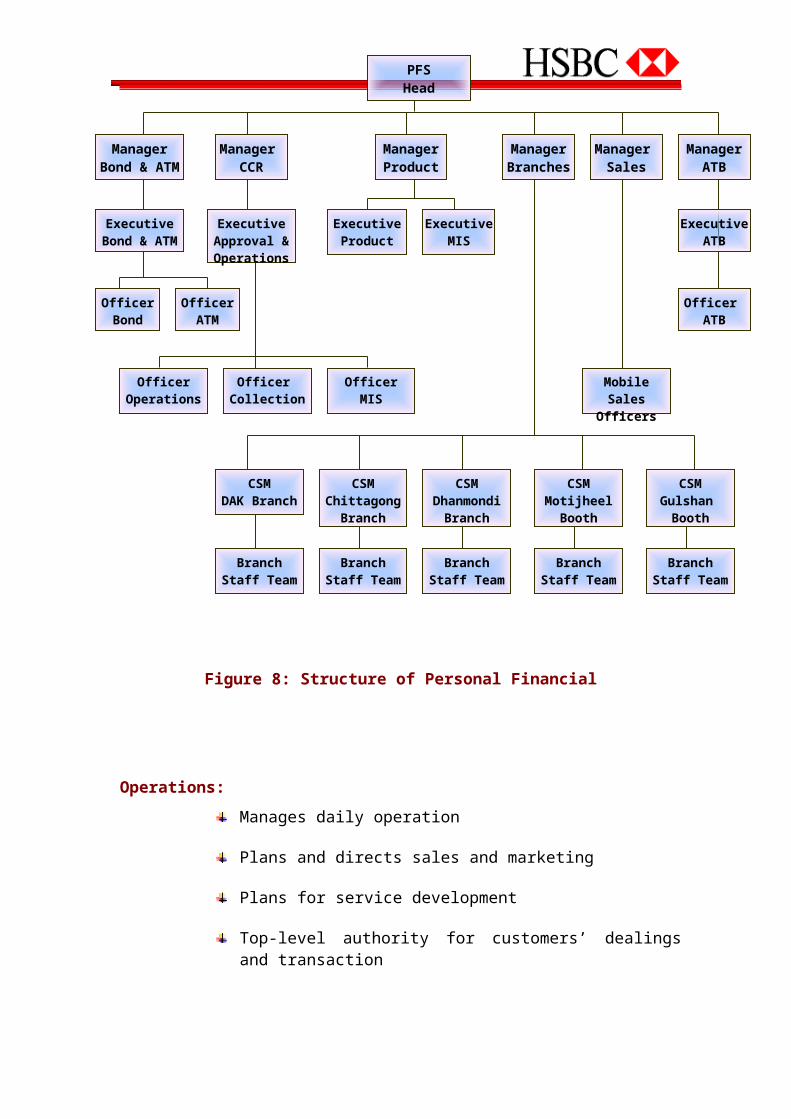

4.5 Personal Financial Services (PFS)

PFS is the most flourishing department of HSBC Bangladesh. This department

basically deals with the management of products and services offered to the individual

consumers. Within a span of only five year HSBC PFS has grown tremendously and is

still growing with its innovative products and service offerings. The 3 branches and 2

booths of HSBC basically deal with the personal banking activities and provide various

Human Resource Manager

Development Officer

Human Resource Officer

AO Staffing

AO Administration

AO Training

AO Appraisal

Figure 8: Structure of Personal Financial Services Department

accounts services to individual customers. The departments under PFS are shown in the

following diagram:

Operations:

Manages daily operation

Plans and directs sales and marketing

Plans for service development

Top-level authority for customers’ dealings and transaction

Provides required service to the customers directly

PFSHead

ManagerBond & ATM

ManagerProduct

Manager Sales

Manager ATB

Manager CCR

OfficerBond

OfficerMIS

OfficerOperations

Officer Collection

ExecutiveProduct

ExecutiveMIS

Mobile Sales Officers

Executive ATB

Officer ATB

OfficerATM

CSMDAK Branch

ExecutiveBond & ATM

ExecutiveApproval & Operations

ManagerBranches

Branch Staff Team

Branch Staff Team

CSMGulshan

Booth

Branch Staff Team

Branch Staff Team

Branch Staff Team

CSM Chittagong

Branch

CSMDhanmondi

Branch

CSMMotijheel Booth

Maintains documentation and report flow vary rapidly

Helps in planning at field level

Assists PFS Head in decision-making process and researches

Assists PFS Head day-to-day work

Keeps track and inform PFS Head in present condition of the

competition in the market

4.6 Branch Network

There are five branches of HSBC, four situated at different locations in Dhaka and one

at Chittagong. Only the Dhaka office (head office) & Chittagong branch deals with

both corporate and personal banking. Other three offices only deal with the personal

banking activities. Their functions are to provide various financial services to the

consumers. These include customer services, sale of various PFS products, opening

new accounts, providing cash, remittance, and other teller services, etc. The branches

are quite decentralized for better delivery of services to customer and have their own

premises and facilities. Branch managers head these branches. Each branch is staffed

with its own team of employees. A great deal of teamwork is seen within these

branches. ATM’s are situated with each branch premises.

CSMDAK Branch

Executive (CSO)Front Office

Executive (CSO)Back Office

OfficersFront Office

Officers Back Office

Figure 9: Branch Network

4.7 Credit Department

The personal banking credit department deals with the consumer credit schemes such as

the Personal loan, Car loan, Travel Loan, Personal Secured loan, etc. which are tailored

to meet the demand of individual customers. The manager of PFS credit who approves

and administers all the activities of this department. He is staffed with five approval

officers, four operations officers, and two MIS officers. The approval officers mainly

reject or approve the credit requests. After being checked by the approval officer, the

credit requests go to the operations for further processing of the application and

disbursement. This department is a member of ALCO (Asset Liability Management

Committee), which coordinates in preparation of lending analysis and data on

concentration of risk and identifies possible lending risks. This department is also

responsible for monitoring all necessary documents and securities related to loans.

4.8 ATM Center

The ATM center ensures smooth operation of the ATM machines that are located at

Dhaka and Chittagong. The ATM center is responsible for regular replenishment of the

off-site ATM’s and servicing of all the ATMs. Currently a total 10 ATMs are in

operation. The ATM center also deals with issuance, termination, and servicing of the

ATM cards. On a whole, the ATM center is the department that is solely responsible

for all the activities related to ATM and is the facilitating department that enables

customers 24 hours banking support.

4.9 Bond Department

This department is under the same manager as the ATM center. They basically deal

with all the buying and selling of government bonds and treasury bills as per customer

instruction, i.e. BSP, PSP, and TSP etc. This department keeps under its control the

transactions regarding USDB, USDIB, and WEDB.

4.10 ATB Center

ATB refers to Automated Tele Banking. This department deals with the back office

serving the HSBC phone banking services provided to customers. This department is

basically responsible for the activation of ATB, ATB pin generation, and ATB security

management, ATB blocking and troubleshooting of all ATB problems. This department

is fairly new and was constructed on January 2000. Currently this department is staffed

with two executive and two officers.

4.11 Corporate Banking

This division if HSBC provides financial services to organizational (corporate) clients.

HSBC is a worldwide leader in banking and financial services whose success is based

on its relationships with its corporate clients. Whether it is locally or around the world,

HSBC offers a comprehensive range of services that can be tailored to the individual

needs of the company. The Head of this department is the Chief of Corporate Banking.

He is also the Vice-CEO of HSBC Bangladesh. The chief of Corporate Banking

manages the activities of corporate banking of HSBC Bangladesh. Two offices of

HSBC Bangladesh offer corporate banking services to corporate clients. These are the

Dhaka Head Office and Chittagong office. Corporate Banking of HSBC Bangladesh

includes Corporate Institutional Banking (CIB), Trade Service (HTV), and Hexagon.

These sub-divisions are discussed briefly in the following sections.

4.12 Corporate Institutional Banking (CIB)

As their major customers operate internationally, HSBC services them internationally.

Operating through the major centers and in close liaison with HSBC Investment Bank,

Corporate and Institutional Banking provides the full range of the Group's capabilities

at local and global levels, with a particular focus on payments and cash management,

trade, and securities custody. HSBC also offers local financial institutions and banks

access to wide range of financial services available on an international basis. The

services are tailored to suit the needs of the companies. CIB has two separate wings:

Relationship management department and Hexagon. These are discussed below:

Relationship Management Department:

The RM department consists of various relationship managers who are assigned to

different corporate client to better satisfy their needs. These RM’s communicate with

the clients and are solely responsible for the companies they deal with. Any

information regarding a corporate client must be communicated through the respective

RM assigned to that corporate client. A relationship manager may be assigned more

than one company and this decision depends on the chief of Corporate Banking.

Hexagon:

The Hexagon department deals with all aspects related to HSBC’s unique banking

software product - Hexagon. It is the global Electronic Banking system of HSBC,

which offers the customers more convenient and efficient banking than ever before. It

is an innovative desktop banking system developed by the HSBC group, which

operates via the group’s proprietary worldwide communications network.

4.13 HSBC Trade Services (HTV)

Trade service is known by various names in other banks, e.g. Trade Finance Foreign

Exchange, Foreign Trade etc. However, the functions are the same. As the name

suggests, this department is involved in facilitating trade, both international & within

Bangladesh. HSBC is the leading provider of trade finance and related services to

importers and exporters in Asia. Trade is considered a core business of the group. The

group’s presence in 81 countries of the world gives a good opportunity to control both

ends of a trade transaction and keep the business within the Group. The various awards

it has won from the leading publications of the world acknowledge HSBC’s excellence

in trade. The trade service department has two separate subsidiaries: Credit

Administration & Foreign Exchange Division.

Credit Administration:

Credit Administration department basically deals with all the documentation,

processing, administration, and disbursement of the import-export services provided to

corporate clients. This department is known to be the heart of HSBC trade services that

administers and manages all the trade tools and facilities provided by HSBC Corporate

Banking. Some important aspects of this department are LC advising, documentation,

OD facilities, guarantees, etc.

Foreign Exchange Division:

The For-ex division of trade services is solely concerned with the management of

Foreign exchange inflow and outflow. The For-ex division of trade service in relation

with NSC and FCD manages the foreign currency traffic of HSBC that originates from

Corporate Banking and trade services.

4.14 Finance Department of HSBC Bangladesh

This is considered as the most powerful department of HSBC. It keeps tracks of each

and every transaction made within HSBC Bangladesh. Manager of FCD who ensures

that all the transactions are made according to rules and regulation of HSBC GROUP

heads it. Violation of such rules can bring serious consequences for the lawbreaker.

FCD is responsible for the preparation of the Annual Operating Plan (AOP),

monitoring treasury risk limits, profit exposure, and maintaining strong liquidity. FCD

is the key member of the Asset Liabilities Management Committee (ALCO), which

deals with how efficiently the bank’s assets and liabilities are managed. FCD also deals

with money market matters. FCD acts as a custodian of all vouchers. FCD as the name

implies does all the banks monitoring of the banks internal compliance and all local

regulatory requirements.

The functions of FCD are briefly discussed below along with an organogram of the

department:

ManagerFCD

Executive,FC

Executive, Treasury

Executive, Payments

Executive, Cash Management

Officer,Accounts

Officer, Financial Control

Officer,Fund Management

Officer Payments

Officer,Administration

Officer,In-house PCM

Officer,Out-ward OCM

Figure 10: Finance Department

4.15 Foreign Correspondence (FC)

FC keeps records of all the accounts of HSBC. All the vouchers, notes, advices and

transaction reports of the branches are sent to FC for record keeping purposes. FC also

prepares the financial statements for the banks and decided upon banks assets and

liabilities. It also deals with the returns that are submitted to the Central Bank on

regular interval.

4.16 Treasury

This department works under FCD. Their main job is to take decisions regarding

purchase and sell of foreign currency. The purpose of treasury's operations is to utilize

the funds effectively and arrange funds at a lowest possible rate of interest, through

maintaining effective relationship with other banks and following the Government rules

and foreign exchange regulations

4.17 Payment and Cash Management (PCM)

PCM deals with the inter-bank payment. PCM strategies are designed to ensure

efficiency, profitably, and comprehensive support.

4.18 Services Department of HSBC

This is an integral and vital part of the bank. The services department ensures smooth

operation and functioning within and between all the departments of HSBC. It also

provides continuous support to the core banking activities of HSBC. The Manager of

Services heads this department who formulates and manages various critical issues of

the services function of HSBC. He is followed by a group of executives who are the

heads of various subsidiary divisions that operate within the services department. The

services department is considered as the backbone of all other departments. The various

subsidiary divisions within this department are Administration, IT, Internal Control

(IC), Network Services Center (NSC), and HUB. A structure of the services

department is presented below followed by a briefing of the subsidiary divisions:

Figure 11: Services Department4.19 Administration

Like any other organizations, the Admin department of HSBC makes sure that the

organizations moves on with all its departments and staffs operating according to all the

rules and regulations of the company. It also prevents any bottlenecks within the work

process and ensures smooth functioning. The admin department has two divisions –

General Administration and Business Support Services.

The general admin division is pretty much similar to the admin departments of other

companies that ensure discipline and regulatory concerns. The business support

services provide supports to the departments during employee leaves and sudden

terminations so that the department can function without problems.

4.20 Information Technology (IT)

This department gives the software and hardware supports to different departments of

the bank. As HSBC is engaged in online banking, the role of IT is very crucial for the

bank. This department is the most active department of HSBC where employees always

Manager Services

ExecutiveAdministration

Executive, IT

Executive Internal Control

ExecutiveHUB

OfficerBSS

OfficerGeneral Admin

OfficerSystem Admin

OfficerSystem

OfficerInternal Control

OfficerRemittances

OfficerHUB

OfficerNetwork Services

Executive,NSC

stand by to solve any problems in the system. The managers and executives of IT

division work continuously to develop the total IT system of HSBC so that it can be

operated with ease, accuracy, and speed.

4.21 Internal Control

HSBC has internal auditors who visit on regular basis and submit the report to the

higher authority for audit purposes. This gives different departments the chance to

know their mistakes and take necessary corrective actions. Again, the Bank annually

administers a company wide audit program to evaluate the overall performance of the

bank in Bangladesh.

4.22 HSBC Universal Banking (HUB)

The HSBC banking system is called HUB. HSBC does the online banking and it is

HUB, which sets up the parameter for that. This HUB is linked with the HSBC group

via satellite and each and every transaction made by HSBC within Bangladesh is being

recorded at the HSBC Asia-pacific headquarters at Hong Kong via HUB. Thus the

HUB is the most powerful and important equipment of HSBC Bangladesh that

monitors and tracks any fraud and faults made with HSBC Bangladesh.

4.23 Network Services Center (NSC)

This department can be described as the ‘Power House’ of HSBC Bangladesh. NSC

does the back office job for the bank. The main four jobs that are performed by NSC

are Clearing, Scanning of signature cards, issuing checkbooks, and sending & receiving

Remittances. NSC looks after the clearing process of HSBC and makes necessary

contact with the central bank for maintaining account flows. All the customer

signatures are scanned in this department and are entered into the system. NSC also

issues checkbooks for new and old accounts based on requisition from various

branches. ‘Remittance’ is a banking term, which means ‘Transfer of funds through

banks’. When a bank remits on behalf of its customers, it is termed as outward

remittance. On the other hand, when the bank receives the remittance on behalf of the

bank, it is inward remittance. The following methods that NSC uses to remit money for

customers: Telegraphic Transfer (TT), Demand Draft (DD), & Cashier’s Order.

4.24 Marketing Department

The sixth major department of HSBC is the marketing department. The marketing

department of HSBC play a vital role in fostering the continuos growth HSBC in

Bangladesh. A manager is assigned to this department who looks after the overall

marketing operation of HSBC in Bangladesh. This department is basically concerned

about marketing the company’s products, services, and building a strong corporate

image. The marketing department of HSBC has three subdivisions: Direct Sales,

Promotion, & Marketing Administration.

Figure 12: Marketing Department

4.25 Amanah Finance Department

Amanah Finance is an ethical and indigenous form of community banking that is

compliant with the Shariah (Islamic law). It involves financing based on the sale

or lease of assets; i.e. the bank is a selling goods for use (trade) rather than

selling money itself. This facility is extended by the way of providing finance for

Manager Marketing

Executive, Direct Sales

Executive, Promotion

Executive,Marketing Administration

Officer,Sales Administration

HSBC Mobile Sales Team

Officer,Public Relations

Officer,Advertising

Officer, R & D

Officer, Billing & Admin

imports. The issuance of import documentary credits and the retirement of bills

are handled in compliance with the Shariah law.

The process of issuance of Amanah DCs (DCI) and handling of bills (IBR) is

very similar to the existing products, except for the exceptions detailed on the

following: Under this product the customer requests the Bank to buy goods

which the customer will buy from the Bank at a deferred sales price. The Bank

then appoints the customer as an agent (Wakala) for buying the goods so

specified. The Customer opens the DC as a buying agent, and when the goods

arrive, constructive delivery is made, buys it from the bank. The purchase price

for the Bank is the bill value and the Bank sells the goods at a profit in

consideration of the customer paying at a later date.

While the overall contract and the transaction are different, the DC itself does

not differ significantly from conventional DCs. A small number of clauses are

proposed to be mandatory in Bangladesh i.e. no TT reimbursement is allowed

and payment is made only upon receipt of documents at counter, the goods are

consigned to the order of the Bank, and the beneficiary has to notify the

applicant of the shipment. These are standard clauses in Bangladesh market and

are normal business practice and local norm.

Two additional documents are required for Amanah DC transaction compared to

the conventional DCs, the Purchase Transaction Notice and the Murabaha

Transaction Notice. In the Purchase Transaction notice the customer requests a

transaction whereby they will purchase goods as the bank agent and also

promises to buy the same goods from the Bank, which the Bank must accept to

go ahead with the transaction. In the Murabaha Transaction Notice, the customer

proposes to buy the goods on a deferred sales price, and agrees to pay a markup

over the purchase price of the goods, payable at a future date.

4.26 Overview of Process

Customer executes Master Murabaha and Wakala agreement,

the omnibus Trust Receipt and the Promise to Purchase

documents which sets the framework along with Facility Offer

Letter

Facility Set up

DC application along with Purchase Transaction Notice placed

to Bank

Bank opens DC with specific set of conditions

Exporter Prepares goods and notifies applicant

Customer submits the Murabaha Transaction Notice (MTN) to

Bank

Exporter ships goods and sends document to Bank

HSBC accepts MTN before or at least on the day the

documents are receives. Customer is advised that documents

are received.

Customer provides acceptance of documents after reviewing

them at the Banks counter. A New Bill advice is sent, and if

there are any discrepancies, customer must accept this or the

DC amended. If documents are in order but the customer does

not provide the MTN or does not wish to pay, the RM to be

referred and the conventional procedures to be followed.

HSBC retires bill by creating CLI or Customer Account Debit

and endorses documents in the name of the customer.

Customer retires the CLI by paying the pre agreed amount

equal to Bill Value + Profit.

4.27 Trade Services Operations

New Product Codes for HSBC Amanah Import Finance are:

Amanah Import Finance

Product Code Description

DCI Islamic Sight Doc Credit

DIG Islamic Usance Doc Credit

DIB Islamic Sight DC. (Back to Back)

IBR Islamic Bill Receivable

SIG Islamic Shipping Guarantees

AWI Islamic Airway Bill Release

CLI Islamic Clean Import Finance

Although the above will support a full range of DC and related products, we will

be using only DCI, IBR, SIG, AWI and CLI for the time being.

4.28 Important Notes

Discrepant Documents

Discrepant documents should be treated the same as with a discrepant document

for a conventional DC. All other Amanah procedures still apply.

Partial Shipments

For each DC, one DC application and one transaction notice are required. For

partial shipments, a separate ‘Murabaha Notification’ must cover each shipment.

Late payment

For late payment, the same charges will apply as with a conventional DC. These

are generated automatically by the system. No changes are necessary in the

system, however when talking to the customer interest should not be mentioned.

4.29 Communication with Customers

Never say “interest” or “loan” to an Amanah Customer

For “Interest” use “Profit”

For “Loan” use “Financing”

4.30 Glossary Agent

Under Shariah requirements the bank will have to purchase the goods before it is

allowed to sell them on cash or deferred payment basis. The bank is however

allowed to appoint an agent who can go in the market and source the goods for

the bank. Since it is recognized that the bank is not in a position to buy the goods

itself it will appoint the customer as its undisclosed agent (solely) for the

purpose of sourcing the required goods and purchase them on behalf of the bank.

This will also include negotiation with the seller or exporter. The bank after the

purchase can sell the goods to the customer.

Financing Requirements:

With the offer to buy or any time before receipt of the offer to buy, under

Shariah, the customer must inform the bank if they require any financing. If the

customer informs that they require any financing after the receipt of the Offer to

Buy, the transaction is not Shariah compliant. Bank still can provide financing

but the customer is aware that the transaction is not Shariah compliant.

Master Murabaha Agreement (MMA):

It is the equivalent to a general financing agreement or, in Trade Services case,

Trade Finance General Agreement (TFGA) that has stated terms and conditions

applicable to transaction under the overall agreement.

Murabaha:

It is an Islamic-financing tool based on the idea of selling goods at a stated

profit. The crucial element in Murabaha is that there must be an underlying asset

involved. In other words, the bank is selling goods for use (which would be

trade) rather than selling money itself (which would be interest).

Murabaha Notification:

MN is essentially a formal offer from the customer to purchase the goods from

the Bank. It will stipulate that the customer has obtained goods and offers to buy

the goods on "as it is" basis on the shipment date. This is again a Shariah

requirement.

Promise to Purchase:

It is a binding agreement on the customer to unconditionally and irrevocably

purchase the goods from the Bank. It is equivalent to a promissory note.

Shariah:

Refers to the Islamic legal tradition, which is sometimes called Islamic Law

(literally it means 'a path to life-giving water')-

Transaction Notice:

It is required by Shariah to have specific notice under each shipment. The MMA

will have a general agreement and will assume that transactions will be

conducted from time to time; however Transaction Notice will ensure that each

party is aware of the details. Without a Transaction notice the DC will not be

Shariah compliant. It should be received with the DC application.

Wakala

Islamic term for agency.

Chapter 5: Products & Services

HSBC Bangladesh carries out all traditional functions, which a commercial Bank

performs such as mobilization of deposit, disbursement of loan, investment of funds,

financing export & import business, trade & commerce & so on. Besides it also offers

some specialized services to its customers. Products & services offered by HSBC can

be categorized according to the customers they serve. Thus two major groups can be

identified. They are – individual customers or consumers & corporate customers or

organizations. An in-depth analysis of HSBC’s product and services in Bangladesh is

presented in this section. First of all, the liability products of the bank are discussed.

After that the various products and services of personal banking division will be

presented, followed by a brief discussion of the corporate banking services offered to

corporate clients. The summary of all the products and services of HSBC Bangladesh is

displayed in the following page.

5.1 Accounts

Savings Accounts:

Maximize wealth with daily interest-

Unlike other banks there is no ledger fee and any interest accrued is not

lost

Customers can issue any number of cheque or withdraw any amount

Interest is calculated on daily credit balance (not on average credit

balance) and paid half yearly

Only condition to earn interest is maintaining a minimum balance of BDT

25,000/-

Relationship fee is BDT 300/- per quarter if average relationship falls

below BDT 50,000/- for three months.

Current Account:

This is also a depository account basically designed for various customers. This is a

non- interest bearing accounts and the features of this account are as follows:

Opening balance TK 25,000

Average balance that should be maintained: TK 25,000

No restrictions on number of transactions

No yearly ledger fee

Non interest bearing

Free ATM card and phone banking service

Documentation: various kinds of documents are needed for the companies such

as memorandum of association, board resolution, etc. however the requirements

for individuals are same as the savings account.

Can be opened only by:

Individuals (joint or single)

Proprietorship companies

Partnership companies

Limited Companies

Liaison offices

NGO’s

5.2 ATM Card

Can be linked with Savings or Current Account or both

24 Hours a day from any one of the 11 HSBC ATM outlets –

DAK, DMO, DGU, DHA and CHG onsite & 5 offsite.

Maximum limit BDT 20,000/- per day per card. For PVA ATM card the

maximum limit is BDT 50,000/- per day.

You can withdraw or deposit money, inquire about your balance, check last

5 transactions, transfer funds between your accounts and make payments to

other accounts with HSBC

Minimum BDT 500/- can be withdrawn;

5.3 Power Vantage

For total financial control-

Average deposit balance should be BDT 2,00,000/-

Annual fee BDT 500/-

Penalty charge BDT 500/- half yearly, if the average deposit balance falls below

BDT 2,00,000/-

Free personal accident insurance coverage for BDT 1,00,000/-

Free endorsement of foreign currency against travel quota

Special Power Vantage ATM card with enhanced cash withdrawal facility of

BDT 50,000/- per day

An all-in-one composite statement of all your accounts under the Power

Vantage package

Special loan rages for the Personal Installment Loan

Lower processing fee for Car Loan

Fee waiver for setting up standing instructions at Auto Sweep

5.4 Time Deposit

Minimum amount to open a TMD is BDT 1,00,000/- (Individual and Joint both)

Interest is paid at maturity

Cumulative Time Deposits (Principal + Interest) is also available

Automatic roll over at prevailing rate

Time deposit is offered in Time Period (Minimum 1 month and Maximum 12

months)

Standing instruction can be given (like credit interest to other accounts)

Personal Secured Loan – a loan facility up to 90% of the value of the LCY

and 80% of FCY time deposit for a maximum period of 5 years

Personal Secured Credit – an overdraft facility up to 90% of the value LCY

and 80% of the time deposit.

Short Term Deposit (STD):

These accounts are opened mostly by the organizations. Organizations normally

maintain current accounts in the banks. They need to transact bulk amount regularly

that’s why, current account fits with their requirements. As current accounts do not

provide any interests and as the organizations cannot have savings account, they are

deprived of earning any interest even though having huge deposit in their accounts.

‘Short-term deposit’ accounts enable them to earn interests from their accounts. These

kinds of accounts share some properties of both current and savings accounts. The

account provides interests, which are like the savings accounts, and the holder can

withdraw any amount any time from his account that is a property of the current

account. Individuals especially, businessmen also maintain such accounts.

Fixed Deposit:

It is also known as term deposits. These deposits are made in the bank for a fixed

period of time. This period of time should be specified in advance. The bank needs not

to maintain cash reserves against these deposits & therefore, it offers interest rates that

are higher than the savings accounts.

Monthly Interest Bearing Time Deposit:

The simple, safe, and flexible way to enjoy guaranteed monthly return-

Minimum opening amount is BDT 5,00,000/- (Individual and Joint both)

Tenure: 1-2 years

Interest is paid at a monthly basis and is transferred to another nominated

account

Automatic roll over for the 2nd year at prevailing rate.

5.5 Expatriate Account

Expatriates can open normal BDT current a/c as well as FCY current a/c

Expatriates can open convertible account if entitled to and subject to restrictions

such as they can not deposit taka in convertible A/C

Free ATM card is provided to access to their accounts to withdraw Taka from

current accounts

Expatriates can not earn interest on their BDT or FCY accounts (Regulations of

Bangladesh Bank)

Expatriates can not get any credit facilities (Regulations of Bangladesh Bank)

5.6 Non-Resident Bangladeshi (NRB)

There are some other accounts for non- resident Bangladeshi

Foreign Currency Current Account

Foreign Currency Time Deposit Account

Resident Bangladeshi

Resident Foreign Currency Current Account:

Features-

Accounts opened from funds brought in when returning from abroad

If amount exceeds USD 3,000/- or equivalent then customer must fill up

declaration form FMJ at the customs.

To be opened within 30 days of return

Minimum opening balance is USD/GBP/EURO 1,000/-

An International ATM card giving access to their funds from 8,00,000/-

ATMs worldwide. Withdrawal in local currencies.

The balance of the account is freely remittable but no inward remittance is

allowed.

Non-chequeable account – chequebook will not be issued.

Can take out the money for further traveling without being subject to any

regulations.

Foreign Currency Time Deposit Account:

Features-

Accounts opened from funds brought in when returning from abroad or by

transferring from resident FCY account

To be opened within 30 days of return

Minimum opening balance is USD/GBP/EURO 1,000/-

Interest bearing time deposit account with maturities of 1, 3, 6 and 12

months

Personal Secured Credit / Personal Secured Loan – an overdraft facility up

to 80% of the value of the foreign currency time deposit.

Chapter 6: Loans & Credits

6.1 Personal Installment Loan (PIL)

Any purpose loan – no cash security

Minimum monthly income BDT 15,000/-, 2 years service in a well reputed,

stable company, minimum age 25 and maximum 56

Valid income proof documents must be furnished, unsecured loan, & no

personal guarantee required

Minimum loan amount is BDT 50,000/- and maximum loan amount is BDT

20,00,000/- or 4 times of salary

Interest rate will be 18% per annum

Maximum loan tenure is 36 months. If loan amount it BDT 4, 00,000/- or above

then maximum tenure is 48 months

Auto Pay customers will get discounted interest rate: 15.5% and loan amount: 6

times of salary or 2 million whichever is lower

CEPS customers will get discounted interest rate: 15.5% and loan amount: 10

times of salary or 2 million whichever is lower

Personal loans will be granted at discounted rates to employees of blue chip

companies against assignment of terminal benefits as per agreement with

employer. Loan tenure will be up to 5 years.

For salaried individuals additional income including rent will be considered,

provided these are substantiated with requisite documentation or evidence.

For businessmen the TIN certificate and CIB (Credit Information Bureau)

report will remain a mandatory document for income verification.

A current account needs to be opened by the customer before applying for

Personal Installment loan (PIL).

6.2 Travel Loan

Travel Loan is offered within the existing Personal Installment loan structure. The

purpose of launching this product is to attract and aid customers with their travel

related services.

Loan amount is minimum loan amount is BDT 50,000/- and maximum loan

amount is BDT 5,00,000/-

Interest rate: 15%

Tenure: Maximum loan tenure is 36 months. If loan amount is BDT 4,00,000/-

or above then maximum tenure is 48 months.

Loan processing fee: 1% of the loan amount or BDT 1,000/- whichever is

higher + stamps BDT 170/-

No personal guarantee is required

6.3 Car Loan

Eligibility- minimum monthly income BDT 20,000/-, 2 years service in a well

reputed, stable company, minimum age 25 and Maximum 56

Valid income proof documents must be furnished

No personal guarantee is required

Minimum loan amount is BDT 50,000/, maximum is 4,00,000/-

For both reconditioned car and new car loan amount will be maximum 70% of

the car value

Interest rate will be 14.5% per annum

Maximum loan tenure is 60 months

Loan processing fee is 1% of the loan amount or BDT 1,000/- whichever is

higher + stamps BDT 170/-

Car will be registered in Bank’s name (no joint registration)

Comprehensive insurance in discounted rate from selected insurance company

in Bank’s name is mandatory and automatically debited from customers account

every year.

CEPS salaried customers will get 0.5% discount in loan processing fee, i.e. 14%

6.4 Home Loan

It’s easier than ever to own a dream home-

Eligibility- minimum monthly income BDT 40,000/-, 2 years service in a well

reputed, stable company, minimum age 25. The loan must end before

borrower’s age reaching 57 years or retirement date, which ever is earlier.

This loan is provided for completed flats / apartments – less than 20 years of

age

No personal guarantee is required

Minimum loan amount is BDT 7,50,000/- and maximum loan amount is

100,00,000/-

Maximum loan tenure is 15 years, loan must be repaid prior to 57 years of age

A maximum loan amount of 70% of the total value of the apartment costing up

to BDT 50,00,000/- and 60% of the total value for the apartments over BDT

50,00,000/-. The total loan value is inclusive of the registration cost.

Interest rate is 14% per annum

Loan processing fee is 1.5% of the loan amount or BDT 20,000/- whichever is

higher + stamp charge

Security: Registered mortgage and original title deed

Insurance: Fire, earthquake, flood, cyclone

6.5 Personal Secured Loan

Personal Secured Loan is a simple stand by loan against the Time Deposit and NRB

Bonds and the loan is repayable in equal monthly installment.

Standby loan against TMD and NRB bonds (WEDB/USDB)

WEDB (Wage Earners Development Bond) or USDB (US Dollar Bond) issued

from HSBC and other multinational banks are considered.

Interest rate 12.5% for loan amount below BDT 5,00,000/- and 12% for loan

amount of BDT 5,00,000/- and above

Interest rate against LCY TMD is 13%

Minimum loan amount BDT 90,000/-

Maximum loan amount 90% of LCY TMD amount or WEDB and 80% of FCY

TMD or USDB

Processing fee against certificate issued from HSBC is BDT 1,000/- + stamps

BDT 170/-

6.6 Personal Secured Credit

Credit facility against the investments-

Personal Secured Credit is a credit facility against Time Deposits and NRB Bonds that

enables customers to have the flexibility to meet short-term commitments without

unlocking their long-term investments.

Customers can borrow up to 90% of their LCY TMD’s and WEDB value

WEDB and USDBs issued from HSBC and other multinational banks are

considered

Minimum loan amount is BDT 90,000/-

Maximum loan amount 90% of LCY TMD amount or WEDB and 80% of FCY

TMD or USDBs.

6.7 Credit Card

Increase the spending power-

Product Name: HSBC – Prime Co-branded Master Card Gold Card

Card Type: Local Master Card Gold Card

Card Limit: Staff Card: BDT 15,000/- to 1, 00,000/-

Master Card Gold Normal: BDT 50,000/- to 1, 00,000/-

Master Card VIP: BDT 1, 00,000/- to 2, 00,000/-

Eligibility:

Primary Eligibility: Minimum BDT 25,000/- gross income from regular

sources. Bangladeshi Citizen 21-65 years of age and has account with HSBC

For Supplementary card the person has to be at least 18 years of age

Card Life: By default 2 years for all cards new and renewed

Billing Cycle: 7th day of the month

Repayment Period: 26th day of every month. Maximum 50 days interest free

period

Minimum Payment Calculation

8% of the current balance shown on the statement or BDT 500/- which ever is

higher. If current balance is less than BDT 500/-, then full payment

For over limit account: 8% of the credit limit plus exceeded amount

6.8 Corporate Banking Services

HSBC offers wide range of cash financing, working capital, short, and medium-term

loans, and guarantee facilities to its corporate customers. Its offshore banking Unit

(OBU) provides US dollar denominated working capital as well as short tem finance

for capital imports to eligible businesses. HSBC is a worldwide leader in banking and

financial services whose success is based on its relationships with its clients. Whether

locally or around the world, HSBC offers a comprehensive range of services that can be

tailored to the company's needs. Some major services provided by HSBC corporate

division are Custody services, Global payment & cash management, Trade services, &

Hexagon.

6.9 Global Payments & Cash Management (PCM)

HSBC's Global Payments and Cash Management services are designed to help its

clients to operate efficiently, profitably and with comprehensive support. The aim is to

provide a service that takes full account of the customers’ local needs as well as

regional and international requirements using our expertise and global resources of the

HSBC Group. PCM provides the following services to its clients:

Accounts & transaction management services: Structuring of bank accounts

to optimize the management and flow of funds within or across national

borders.

Cash & Liquidity management services: Cash is a company's most volatile

asset and HSBC provides the best service to manage its client’s cash efficiently.

6.10 HSBC Trade Services (HTV)

HSBC is the leading provider of trade finance and related services to importers and

exporters in Asia. The bank operates a highly automated trade-processing network and

offers an electronic data interchange (EDI) capability through Hexagon. Some services

provided by HTV are as follows:

6.11 Import Services

A full range of import services handled by experienced staff is available, ensuring that

clients import documents are processed without delay. Some import related services

are- Import collection services, Import financing services, Import documentary

advising, Processing, and advising on shipping guarantees.

6.12 Export Services

HSBC provides advices on any aspect of export document preparation. It also provides

working capital finance to help the sourcing of raw materials. Some other export

services are- Pre-shipment Financing, Post shipment Financing, Purchase of Export

bills, Back-to-Back credit, and LC, Documentary credit advising, Documentary

checking.

6.13 Risk management

HSBC has developed a unique range of specialized products aimed specifically to