how to analyze how much to borrow from your banker

TRANSCRIPT

www.futurumcorfinan.com

Page 1

How to Analyze How Much to Borrow from Your

Banker?

Money has no royalty to one master, it is always going to the highest bidder.

Introduction

When faced with two alternatives for borrowing, it is normal to see that the corporate analyst will

see direct to the annual interest rate being quoted for each loan facility alternative. If the loan

proposal for each alternative has the same terms and conditions other than the quoted annual

interest rate, this practice might sound reasonable, that is just looking at the stated borrowing

interest rate. Yet, how about if one alternative, let’s say will make the company to borrow “more

funds” compared to the other alternative.

For example, a company has a plan to purchase a property project with a market value of IDR

100,000,000,000 (IDR 100 billion). The company might not have funds at company’s vault

sufficiently to execute the purchase. The company then considers going to obtain the loan

facility from the bank under mortgage scheme, meaning that the property purchased will be

used as a main collateral to the loan facility.

Sukarnen

DILARANG MENG-COPY, MENYALIN,

ATAU MENDISTRIBUSIKAN

SEBAGIAN ATAU SELURUH TULISAN

INI TANPA PERSETUJUAN TERTULIS

DARI PENULIS

Untuk pertanyaan atau komentar bisa

diposting melalui website

www.futurumcorfinan.com

www.futurumcorfinan.com

Page 2

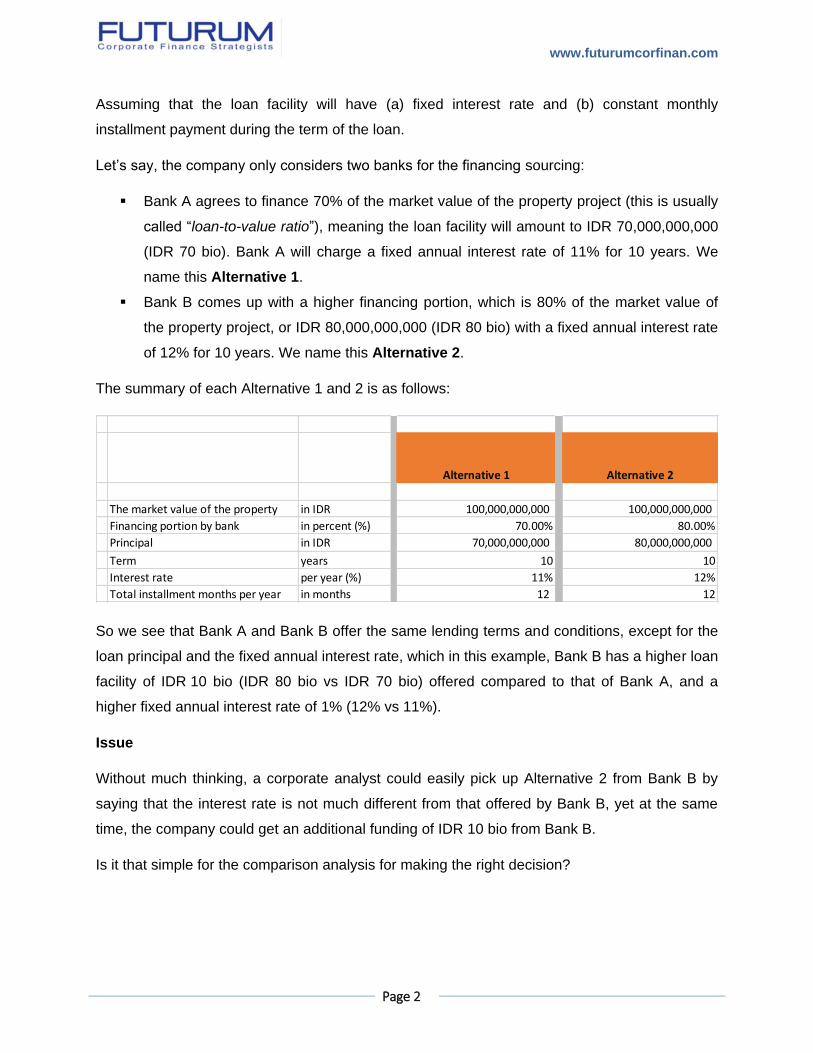

Assuming that the loan facility will have (a) fixed interest rate and (b) constant monthly

installment payment during the term of the loan.

Let’s say, the company only considers two banks for the financing sourcing:

Bank A agrees to finance 70% of the market value of the property project (this is usually

called “loan-to-value ratio”), meaning the loan facility will amount to IDR 70,000,000,000

(IDR 70 bio). Bank A will charge a fixed annual interest rate of 11% for 10 years. We

name this Alternative 1.

Bank B comes up with a higher financing portion, which is 80% of the market value of

the property project, or IDR 80,000,000,000 (IDR 80 bio) with a fixed annual interest rate

of 12% for 10 years. We name this Alternative 2.

The summary of each Alternative 1 and 2 is as follows:

So we see that Bank A and Bank B offer the same lending terms and conditions, except for the

loan principal and the fixed annual interest rate, which in this example, Bank B has a higher loan

facility of IDR 10 bio (IDR 80 bio vs IDR 70 bio) offered compared to that of Bank A, and a

higher fixed annual interest rate of 1% (12% vs 11%).

Issue

Without much thinking, a corporate analyst could easily pick up Alternative 2 from Bank B by

saying that the interest rate is not much different from that offered by Bank B, yet at the same

time, the company could get an additional funding of IDR 10 bio from Bank B.

Is it that simple for the comparison analysis for making the right decision?

Alternative 1 Alternative 2

The market value of the property in IDR 100,000,000,000 100,000,000,000

Financing portion by bank in percent (%) 70.00% 80.00%

Principal in IDR 70,000,000,000 80,000,000,000

Term years 10 10

Interest rate per year (%) 11% 12%

Total installment months per year in months 12 12

www.futurumcorfinan.com

Page 3

Analysis

Here we re-check the effective annual interest rate for Alternative 1 and Alternative 2 using

RATE formula (see cell G16 and I16 by using =Formulatext() in Excel 2013).

The answer to above question is NO.

We cannot use the fixed annual interest rate for Alternative A and Alternative B to decide which

loan facility that should be taken by the company.

If it is not the annual interest rate of both Alternative A and Alternative B, then how should we

compare these two Alternatives?

Here we are going to introduce the incremental or marginal cost of borrowing to be used in

such analysis.

Somehow we know that Alternative B will lend the company Rp 10 bio higher than that of

Alternative A, yet, for this higher loan facility of IDR 10 bio, the company should be willing to pay

a higher annual interest rate of 1%. Using the incremental or marginal cost of borrowing

concept, then we need to ask:

How much is the effective cost that the company should pay to get an additional or

incremental borrowing of IDR 10 bio from Bank B?

www.futurumcorfinan.com

Page 4

We might think quickly that it might be possible that the incremental or marginal cost of

borrowing more IDR 10 bio from Bank B is 12% per year since in “actual”, the company has to

disbursed more money to pay this higher interest per monthly installment and this 12% is

applied to the “whole” loan facility from Bank B, that is IDR 80 bio.

The logic by linking the incremental or marginal cost of borrowing to the interest cost that have

to be paid over the “whole” loan facility from Bank B, is correct, since:

If the company will only be willing to take the loan facility of IDR 70% from Bank A, the

annual interest to be paid is 11%, yet

By obtaining additional Rp 10 IDR with a higher loan facility of IDR 80 bio from Bank B,

the company will pay a 1% higher, not only on the additional IDR 10 bio, but also on the

IDR 70 bio that previously could be obtained by paying 11% annual interest rate.

Intuitively from the above paragraph, we could sense that the incremental or marginal cost of

borrowing more of IDR 10 bio cannot be 12% per year, but even higher.

The question, then, how much higher is it?

The term “incremental” or “marginal” cost of borrowing will require us to compare the “additional”

against the “additional”, in this case, the higher monthly payments versus the higher loan

principal from Alternative B.

The snapshot of the spreadsheet below indicated that the company will pay a higher monthly

installment payment of IDR 183.5 mio for a higher loan facility of IDR 10 bio, to Bank B.

www.futurumcorfinan.com

Page 5

Once we have a monthly installment payment of IDR 183.5 mio for 10 years and the “additional”

loan facility of IDR 10 bio, then we could use RATE function from Excel to obtain the annual

interest rate, in this case, the result is 18.52% (see cell Q10).

You might be surprised that the incremental or marginal cost of borrowing more of IDR 10 bio is

much higher than the stated or quoted annual interest rate from Bank B, 18.52% compared to

12%.

Then you might want to ask, then how about 12% annual interest rate quoted by Bank B?

Are they misleading you by giving you intentionally a lower quoted interest rate so that you

might be induced to take up that loan offering from Bank B, by thinking that it is not really

expensive by obtaining IDR 10 bio more yet the additional annual interest rate is 1% higher?

Not really, Bank B’s 12% annual interest rate is not wrong.

Bank financial calculator should always be right…as usual, money attracts brain, and there are

surely many smart persons inside Bank B.

Then you are asking further, how to link this considerably higher marginal rate of 18.52% with

the quoted 12% from Bank B?

Though Bank B financial calculator is correct, but Bank B doesn’t really tell you the whole

story…”silence is golden”.

This is the secret…

What Bank B doesn’t tell you is that the quoted or stated annual interest rate of 12% is in fact

calculated from the approximated weighted average of the loan interest rate of 11% (for

loan facility of IDR 70 bio, the same that is offered by Bank A) and 18.52% of lending an

additional IDR 10 bio more compared to that offered by Bank A to the company.

Here is the calculation….

www.futurumcorfinan.com

Page 6

From the above analysis, we obtain 11.94% or rounded to 12%, the annual interest rate that

Bank B is offering to the company with a loan-to-value ratio of 80%, 10% higher than that

offered by Bank A. By taking the loan facility from Bank B, implicitly, the company is willing to

pay 11% annual interest rate for the IDR 70 bio (the same as offered by Bank A) plus 18.52%

annual interest rate for the additional IDR 10 bio.

Now you are not really happy to know the fact that the instead of just paying 1% annual interest

rate more (12% vs 11%), you need to pay 18.52% annual interest rate for that additional IDR 10

bio, or

the spread is 18.52% - 11% or 7.52%, or approximately 7.52% / 11% = 68% considerably

higher.

I will say to you to cool down first instead of confronting this fact direct to your Bank B banker.

At the end of the day, Bank B doesn’t “force” you to accept its loan facility offering.

Then the next question is how to deal with this 18.52%?

www.futurumcorfinan.com

Page 7

I will say, well it depends:

i. whether you have money of IDR 10 bio in the company’s bank account and

ii. whether the company could get the additional IDR 10 bio from other financier with a

lower annual interest rate.

Let discuss the i) point first.

Let’s say, the company has IDR 10 bio in its bank account, that is not reserved for other fund

request within another 10 years (for example, to support capital expenditures which are needed

to drive EBITDA and growth, or financing working capital requirements), then the company

could use this IDR 10 bio to fund the property purchase. This will implicate that the company will

only accept a loan-to-value ratio of 70% from Bank A, paying IDR 30 bio as the down payment

and the rest to be covered by the loan facility. The reason driving this choice is that the

company is not willing to accept a relatively higher annual interest rate of 18.52% for that

additional loan amount of IDR 10 bio, to reach a loan-to-value ratio of 80%.

Is this reasoning correct?

Well, my answer, this again depends.

We do know from the above analysis that to obtain additional IDR 10 bio, Bank B will charge the

company with a rate of 18.52%. We could use this 18.52% as the minimum rate of return that

the company could utilize that IDR 10 bio that is now sitting “idly” in the company’s bank

account.

Suppose the company could have a new business project in its pipeline with an initial

investment of IDR 10 bio and with a comparably equal risk that could “guarantee” the annual

rate of return of more than 18.52%, then the company might be better off to consider to accept

Bank B loan facility, paying only IDR 20 bio (IDR 100 bio for property market price minus IDR 80

bio of funds from Bank B) as a down payment (instead of IDR 30 bio as a down payment if the

company chooses the loan facility from Bank A). This choice will leave the company with IDR 10

bio intact in its bank account, and could use this IDR 10 bio to fund the initial investment of that

new business prospect.

We could interpret this 18.52% as the “[minimum] opportunity cost of capital”. If the company

could invest this IDR 10 bio elsewhere that could earn the annual rate of return of more than

18.52%, then the company might be better off taking a higher loan facility that is from Bank B. If

not, then the company is better off with a smaller loan facility from Bank A.

www.futurumcorfinan.com

Page 8

Now we go to the ii) point above.

How about if the company doesn’t have an excess cash of IDR 10 bio that could be channeled

to fund the property purchase. So it might seem that the “only” road to go is by taking a higher

loan facility from Bank B, paying IDR 20 bio for the down payment using its own money and

leaving IDR 80 bio to be covered by Bank B loan facility.

Will the analysis be different even if the company doesn’t have IDR 10 bio?

Well, I would like to say again, it depends.

If the company doesn’t have money, it doesn’t mean that the company has no other option or

alternative to consider to make it better off.

How about if the company could go to other bank, let’s say, Bank C, which could extend a loan

facility of IDR 10 bio with the same terms and conditions of loan, including the loan term of 10

years.

So instead of borrowing IDR 80 bio from Bank B with its weighted average of 11% rate on the

IDR 70 bio and 18.52% rate on the additional IDR 10 bio, then the company could take a

smaller loan facility of IDR 70 bio from Bank A, and then cover the shortage of IDR 10 bio for a

down payment (assuming the company has an IDR 20 mio in its bank account ready for the

down payment) from Bank C.

The above option will be financially feasible if the company could negotiate with Bank C to have

the loan annual interest rate for that IDR 10 bio, lower than 18.52%.

So if under (i) we could interpret “18.52%” rate as the minimum rate of return that we should

earn from other alternative or option, yet under (ii), we could interpret “18.52%” rate as the

maximum cost of borrowing that we could pay to get the additional loan facility from other

bank.

Conclusion

In analyzing how much to borrow from the bank in financing a property project, then in the

financial modelling, the corporate analyst should use the incremental cost of borrowing on an

annual basis in comparing one alternative with another option(s).

Before I am closing this article, there are some caveats in my analysis, which is under this

analysis:

www.futurumcorfinan.com

Page 9

I do not factor the corporate income tax into the analysis. Corporate income tax could

reduce the interest rate effectively since by taking a higher loan facility, the interest

expense charged to the profit and loss statement will be higher, resulting in a lower

corporate income tax liability. If the company’s EBIT is higher than the interest expense,

we could say that the company could realize this interest tax shield, making the effective

after-income-tax interest cost lower than that paid to the bank.

In addition, the company in a higher corporate income tax bracket might enjoy higher

income tax reduction by taking a higher loan facility. Yet for Indonesia context, this is not

really applicable, as Indonesia tax regime applies one single rate of 25%, unless if the

company has a significant tax loss that could be carried forward to reduce the corporate

income tax liability.

I assume that the loan facility will not be repaid early. The loan repaid early than

scheduled in the analysis will affect the incremental cost of borrowing, which in general,

we could say, it will increase the incremental cost of borrowing.

I don’t consider all costs that could be charged by bank, such as loan provision,

insurance, administration/notary charge, that in most cases, could be collected by bank

at the beginning of the loan term, which could add several points to the effective

borrowing cost. Here, I assume that other than the loan principal amount and interest

rate, the terms and conditions of the loan facility from different banks are the same.

~~~~~~ ####### ~~~~~~

www.futurumcorfinan.com

Page 10

Disclaimer

This material was produced by and the opinions expressed are those of FUTURUM as of the date of

writing and are subject to change. The information and analysis contained in this publication have been

compiled or arrived at from sources believed to be reliable but FUTURUM does not make any

representation as to their accuracy or completeness and does not accept liability for any loss arising from

the use hereof. This material has been prepared for general informational purposes only and is not

intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors

for specific advice.

This document may not be reproduced either in whole, or in part, without the written permission of the

authors and FUTURUM. For any questions or comments, please post it at www.futurumcorfinan.com

© FUTURUM. All Rights Reserved