hm sultan qaboos bin said, sultan of oman€¦ · mr. hani bin dawood bin hamdan al baharani mr....

TRANSCRIPT

HM Sultan Qaboos Bin Said, Sultan of Oman

Oman Fisheries Co. S.A.O.G

Twentyfirst Annual Report2009 - 2010

INDEX Page

Members of the Board of Directors, Executive Committee and Internal Audit Committee i

Chairman’s Report ii-iii

Report of the Shareholders of Factual Findings iv

Report on Corporate Governance v-x

Report of the auditors 1

Consolidated and parent company income statement 2

Consolidated and parent company financial position 3

Consolidated and parent company statement of changes in equity 4

Consolidated and parent company cash flow statement 5

Notes to the consolidated financial statements 6 – 32

Oman Fisheries Co. S.A.O.G

i

Oman Fisheries Co. S.A.O.G

Members of the Board of DirectorsSheikh Mohammed bin Hamad bin Ali al Masrouri Chairman

Mr. Saleh bin Nasser bin Juma al Araimi Deputy Chairman

Mr. Abdul Ameer bin Said bin Mohammed Director

Sheikh. Salah bin Hilal bin Naser al Mawali Director

Mr. Hani bin Dawood bin Hamdan al Baharani Director

Dr. Saud bin Hamood bin Ahmed al Habsi Director

Mr. Qais bin Mahmood bin Abdalla al Khonji Director

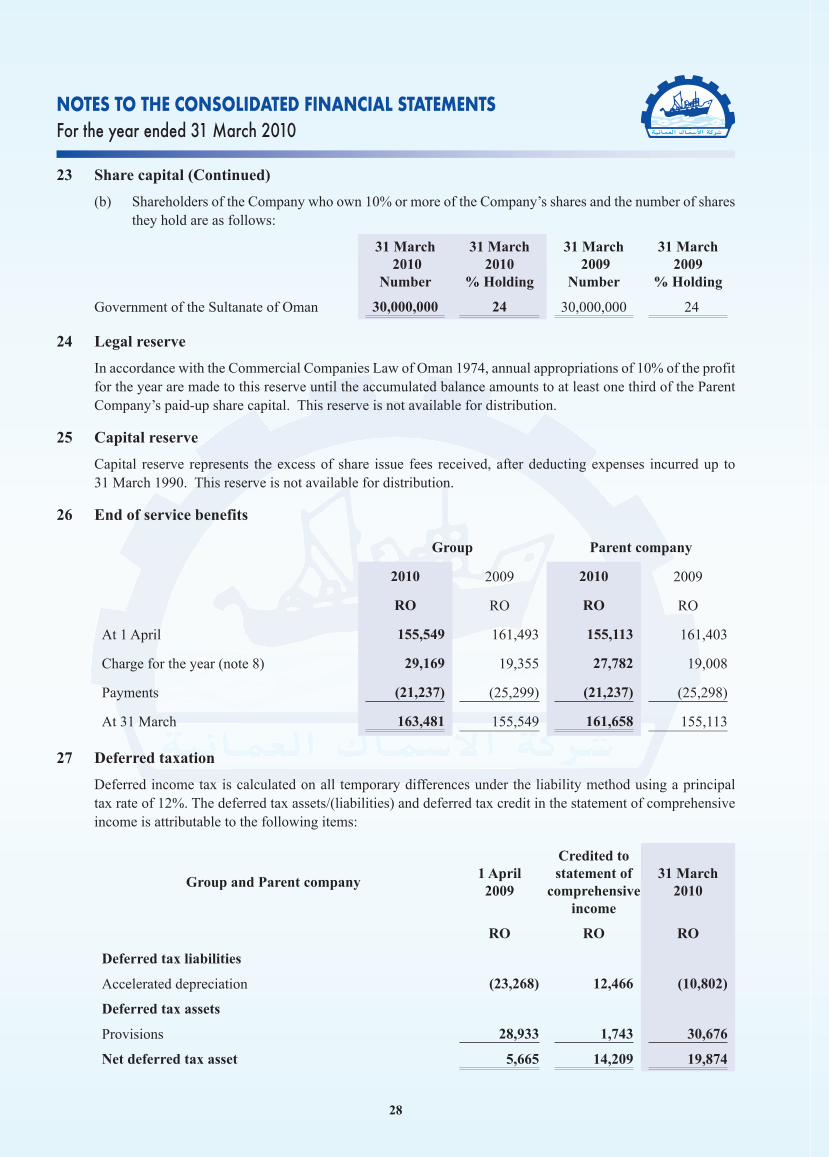

Mr. Musalam Amer al Ammri Director

Executive CommitteeMr. Saleh bin Nasser bin Juma al Araimi Chairman

Sheikh Salah bin Hilal bin Naser al Mawali Director

Mr. Hani bin Dawood bin Hamdan al Baharani Director

Dr. Saud bin Hamood bin Ahmed al Habsi Director

Mr. Qais bin Mahmood bin Abdalla al Khonji Director

Internal Audit CommitteeMr. Abdul Amir bin Said bin Mohammed Chairman

Sheikh Salah bin Hilal bin Naser al Mawali Member

Mr. Hani bin Dawood bin Hamdan al Baharani Member

Mr. Said Al Rashid Al Rawahi General Manager

Company Address P.O. Box 2900, Code : 112

Auditors PricewaterhouseCoopers

ii

CHAIRMAN REPORT

Dear Shareholders,

On behalf of myself and Board of Directors of Oman Fisheries Co. SAOG on occasion of Annual General Meeting I have pleasure to present Annual Report of your company for the financial year ended 31st March, 2010 along with Corporate Governance report. The summary of the financial result of the company is as follows:

1. Financial Results:

This year company had achieved total sales of RO 11.830 Million as compared to RO 10.856 Million of previous year which is more by 9%.

As a result of the improvement in the Company’s operation and controlling the expenses, the Company had achieved operational profit of RO 447,225 compared with operational loss of RO 274,486 of previous year.

We had achieved net profit during the financial year 2009 – 2010 of RO 1.485 Million as compared to the net loss of RO 1.634 of the previous year.

As a result of efforts of the Management during this financial year your company had achieved turnover of 16,029 MT as compared to the last year turnover of 14,185 MT which is more by 13%.

Muscat Security Market index at the beginning of the year was 4,628 and it increased to 6,697 at the end of the year. Because of this growth, portfolio of the company which was managed by Bank Muscat and Vision Investment Services had also gone up. During this financial year company had achieved gain of RO 644,512 through investment in Muscat Security Market.

The Management of the company is trying their level best to distribute dividend to Shareholders during this financial year. As per the rules and regulations of Capital Market Authority first company has to set off previous year losses, only after that if any balance is remaining then Company can able to distribute dividend to Shareholders. After setting off losses the remaining balance is not enough to distribute dividend hence during this year your company is unable to declare any dividend.

2. Future Outlook:

The company is searching new ways for catching fish to subsidize the banned of Trawler. The company had purchased 4 coastal fishing boats which had started operation from May 2010, and in the case of succession of those boats, the company will do its role in promoting these types of boats to local fishermen.

Moreover the Company had prepared 5 year’s plan for purchasing and operating coastal fishing boats, which will enable it - God willing - from the exploitation of quota granted under the concession agreement and will seek during the ten-year plan, deliberate Omanisation fleet for fishing vessels. Company had planned to sell maximum catch from these boats in the local market either through direct sales or through company’s vehicles or through opening fish shops in all the regions of Sultanate mainly to support Government effort’s to make fish available in the interior region.

Oman Fisheries Co. S.A.O.G

iii

The company is about to finish feasibility study for some projects and we hope that we are going to implement them during this financial year. The projects are as follows:

Buying and operating coastal fishing boats in Oman as per the approval of Ministry of Fisheries.

Supporting local fishermen by signing medium term agreements with the company.

Expansion of Value Added Plant of Buraimi.

5 year’s Business Plan for accelerated growth of the company; Management had already prepared Business

Plan and it will be reviewed by Executive Committee very soon then it will be presented to the Board of Directors for their approval. We hope that we will implement this from October 2010.

Acknowledgement and Appreciation:

I take this opportunity to thank all the Ministers and Government sectors for their support to the activities of the company in particular, I would thank Ministry of Fisheries Wealth headed by H.E. Sheikh Mohammed bin Ali al Qathabi for his continuous support for the company in fisheries sectors.

On behalf of the Board of Directors and Management of the Company, I wish to acknowledge and express the sincere gratitude to His Majesty Sultan Qaboos Bin Said for his wise leadership and in support of the economic development and prosperity of the Country.

May Allah guide us all to keep steps on the right path and crown our efforts with success.

Mohammed bin Hamad bin Ali al Masrouri

Chairman

v

REPORT ON CORPORATE GOVERNANCE

The Company has implemented the code of Corporate Governance during the financial year issued by the Capital Market Authorities.

1. Company Philosophy on Code of Corporate Governance

The Company has always believed in fair business and corporate practices while dealing with Shareholders,

Employees, Customers, Creditors and Others. The Company is prompt in discharging its statutory obligations

and duties. The Company is maintaining policies, procedures and systems for the purposes to ensure the fair

and timely release of information about the Company.

The Board of Directors (“the Board”) has had adequate representation of the qualified, Non-executive and

Independent Directors. The Board has constituted various Committees of directors from time to time for the

matters which require special attention. The Board has adequately empowered the Executive Management on

all day-to-day matters, subject to the overall authority vested in the Board. The Directors attending the Board

and Committee meetings and actively participate in their proceedings. The Company lays strong emphasis on

audit and internal controls, having regard to the nature of the company’s business and has introduced suitable

checks and balances to ensure sound integrity of the operations. The Company also lays a very high emphasis

on total compliance with the various laws and regulations of the Country.

2. Board of Directors

As per the Article 19 of Articles of Association of the Company the strength of the Board is eight Directors,

and all of them are Non executive and Independent among them 6 Directors are elected by shareholders during

the AGM and 2 directors are appointed by resolution from the Cabinet.

The primary functions of the Company’s Board of directors in general include amongst others the following:

To approve business and financial policies to meet the objectives of the Company and enhance shareholders

value.

Review and approve the Company’s annual budget / plans and monitoring corporate performance against

the budget.

Approve and implement the disclosure policy in compliance with regulatory requirements.

Ensure compliance with regulatory requirements, policies, procedures and laws.

Nominating members of subcommittees and defining their roles, responsibilities and authorities.

Evaluate and appoint senior management executives.

Review effectiveness of systems and procedure of internal controls.

Constantly monitor and oversee the Corporation’s financial position, adherence to reporting standards and

policy of public disclosure of material information.

To facilitate proper governance, the Company’s management places before the Board, at least, the minimum

information as required by Article 4 of the Code of Corporate Governance.

The current Board of directors as on 31st March 2010 consists of 8 members, six of them were elected on 23rd

June 2009 and other two were appointed by the Cabinet and the details of them is as follows:

vi

REPORT ON CORPORATE GOVERNANCE

Composition of the Board of Directors:

Name of the Director DesignateCategory, basis & Capacity of

Membership

Sheikh Mohammed bin Hamad bin Ali al Masrouri ChairmanNon – Executive, Independent & In

Personal Capacity

Mr. Saleh bin Nasser bin Juma al Araimi Deputy ChairmanNon – Executive, Independent & In

Personal Capacity

Sheikh Salah bin Hilal bin Naser al Mawali DirectorNon – Executive, Independent & In

Personal Capacity

Mr. Abdul Ameer bin Said bin Mohammed DirectorNon – Executive, Independent & In

Personal Capacity

Mr. Hani Bin Dawood Bin Hamdan Al Baharani DirectorNon – Executive, Independent &

Nominee of Ministry of Finance.

Dr. Saud Bin Hamood Bin Ahmed Al-Habsi DirectorNon – Executive, Independent &

Nominee of Ministry of Fisheries Wealth.

Mr. Qais bin Mahmood bin Abdalla al Khonji DirectorNon – Executive, Independent & In

Personal Capacity

Mr. Musalam Amer Al - Ammri DirectorNon – Executive, Independent & In

Personal Capacity

Number of Meetings held and Dates of the meeting:

Meeting

DescriptionName of Directors / Members Designation Date of holding Meeting

Board of Directors

Meeting

All Directors 25th May 2009

23rd June 2009

14th September 2009

31st October 2009

24th January 2010

15th March, 2010.

Internal Audit

Committee

Meeting

Mr. Abdul Amir bin Said Mohammed

Sheikh Salah Bin Hilal Bin Naser Al Mawali

Mr. Qais bin Mahmood bin Abdalla al Khonji #

Mr. Hani Bin Dawood Bin Hamdan Al Baharani #

– Chairman

– Deputy

Chairman

26th April, 2009

23rd May 2009

28th July 2009

20th October 2009

17th January 2010.

Executive

Committee

Meeting

Mr. Saleh bin Nasser bin Juma al Araimi

Sheikh Salah bin Hilal bin Naser al Mawali

Dr. Saud Bin Hamood Bin Ahmed Al-Habsi

Mr. Hani Bin Dawood Bin Hamdan Al Baharani

Mr. Qais bin Mahmood bin Abdalla al Khonji

Mr. Musalam Amer Al - Ammri

– Chairman 17th August 2009

18th October 2009

15th November 2009

8th March 2010.

# Mr. Qais bin Mahmood bin Abdalla al Khonji is transferred from Audit Committee to the Executive Committee from 23rd June 2009 and Mr. Hani bin Dawood bin Hamdan Al Baharani is appointed in his place.

vii

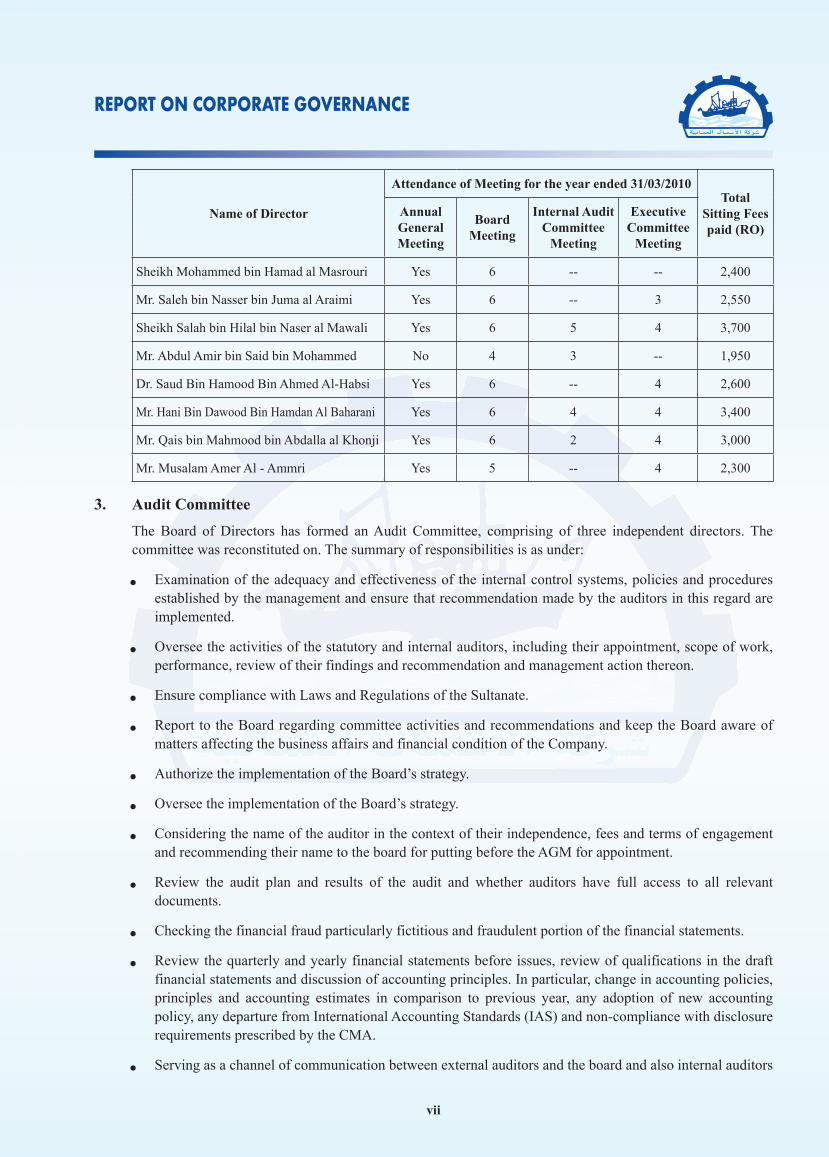

REPORT ON CORPORATE GOVERNANCE

Name of Director

Attendance of Meeting for the year ended 31/03/2010Total

Sitting Fees paid (RO)

Annual General Meeting

Board Meeting

Internal Audit Committee

Meeting

Executive Committee

Meeting

Sheikh Mohammed bin Hamad al Masrouri Yes 6 -- -- 2,400

Mr. Saleh bin Nasser bin Juma al Araimi Yes 6 -- 3 2,550

Sheikh Salah bin Hilal bin Naser al Mawali Yes 6 5 4 3,700

Mr. Abdul Amir bin Said bin Mohammed No 4 3 -- 1,950

Dr. Saud Bin Hamood Bin Ahmed Al-Habsi Yes 6 -- 4 2,600

Mr. Hani Bin Dawood Bin Hamdan Al Baharani Yes 6 4 4 3,400

Mr. Qais bin Mahmood bin Abdalla al Khonji Yes 6 2 4 3,000

Mr. Musalam Amer Al - Ammri Yes 5 -- 4 2,300

3. Audit Committee

The Board of Directors has formed an Audit Committee, comprising of three independent directors. The committee was reconstituted on. The summary of responsibilities is as under:

Examination of the adequacy and effectiveness of the internal control systems, policies and procedures

established by the management and ensure that recommendation made by the auditors in this regard are implemented.

Oversee the activities of the statutory and internal auditors, including their appointment, scope of work,

performance, review of their findings and recommendation and management action thereon.

Ensure compliance with Laws and Regulations of the Sultanate.

Report to the Board regarding committee activities and recommendations and keep the Board aware of

matters affecting the business affairs and financial condition of the Company.

Authorize the implementation of the Board’s strategy.

Oversee the implementation of the Board’s strategy.

Considering the name of the auditor in the context of their independence, fees and terms of engagement

and recommending their name to the board for putting before the AGM for appointment.

Review the audit plan and results of the audit and whether auditors have full access to all relevant

documents.

Checking the financial fraud particularly fictitious and fraudulent portion of the financial statements.

Review the quarterly and yearly financial statements before issues, review of qualifications in the draft

financial statements and discussion of accounting principles. In particular, change in accounting policies, principles and accounting estimates in comparison to previous year, any adoption of new accounting policy, any departure from International Accounting Standards (IAS) and non-compliance with disclosure requirements prescribed by the CMA.

Serving as a channel of communication between external auditors and the board and also internal auditors

viii

REPORT ON CORPORATE GOVERNANCE

and the board.

Reviewing risk management policies and looking into the reasons of defaults in payment obligations of

the company.

Reviewing the specific transactions with related parties for making suitable recommendations to the board

and setting rules for entering the small values transactions with related parties without obtaining the prior approval of audit committee and the board.

4. Executive Committee

The Board Executive Committee, which comprises of 6 directors, is chaired by the Dy. Chairman to the Board of Directors and meets as and when required. The objective of the Executive Committee is to discharge responsibilities on behalf of the board in deciding on specific and any other matters. The Executive Committee also reviews and recommends to the Board of Directors the annual budget of the Company.

5. Appointment of General Manager

Further to the news published in the Muscat Securities Market site on 25th January 2010 regarding the appointment of General Manager of the company, the Board of Directors decided on 24th January 2010 to appoint Mr. Said Rashid Al Rawahi as General Manager of the company.

6. Remuneration Matters

a) Sitting Fees of RO 21,900 was paid to the directors during the year. The Board of Directors has proposed R.O. 13,994 (P.Y RO. NIL) as Directors remuneration.

The top six senior executives of the Company have received a total amount of R.O. 101,020.

The above includes salary, benefits, bonuses, gratuity, etc.

b) There are no incentives payable to the above based on performance criteria.

c) Consolidated audit fees payable for the financial year 2009-2010 will be RO. 8500.

7. Details of Non-Compliance by the Company.

The company fails to publish initial un audited results for the year 2007 – 08 and because of that Capital Market Authority had charged fine of RO 1250/- which was duly paid by the company. During this year company had already published initial unaudited financial result.

8. Means of Communication with the Shareholders

a) Quarterly results are published in Arabic and English local newspaper and the Shareholders are notified that the detailed accounts will be sent to any Shareholder who requests the same.

b) Annual Reports containing the audited financial statements together with the Chairman’s Report, Related Party Transactions and invitation to attend the AGM are sent by registered post to all shareholders.

c) Management Discussion and Analysis Report is a part of this Annual Report.

d) The company has its own website and the information relating to the Company products and facilities are posted on the website for all interested parties. The company’s website is www.omanfisheries.com

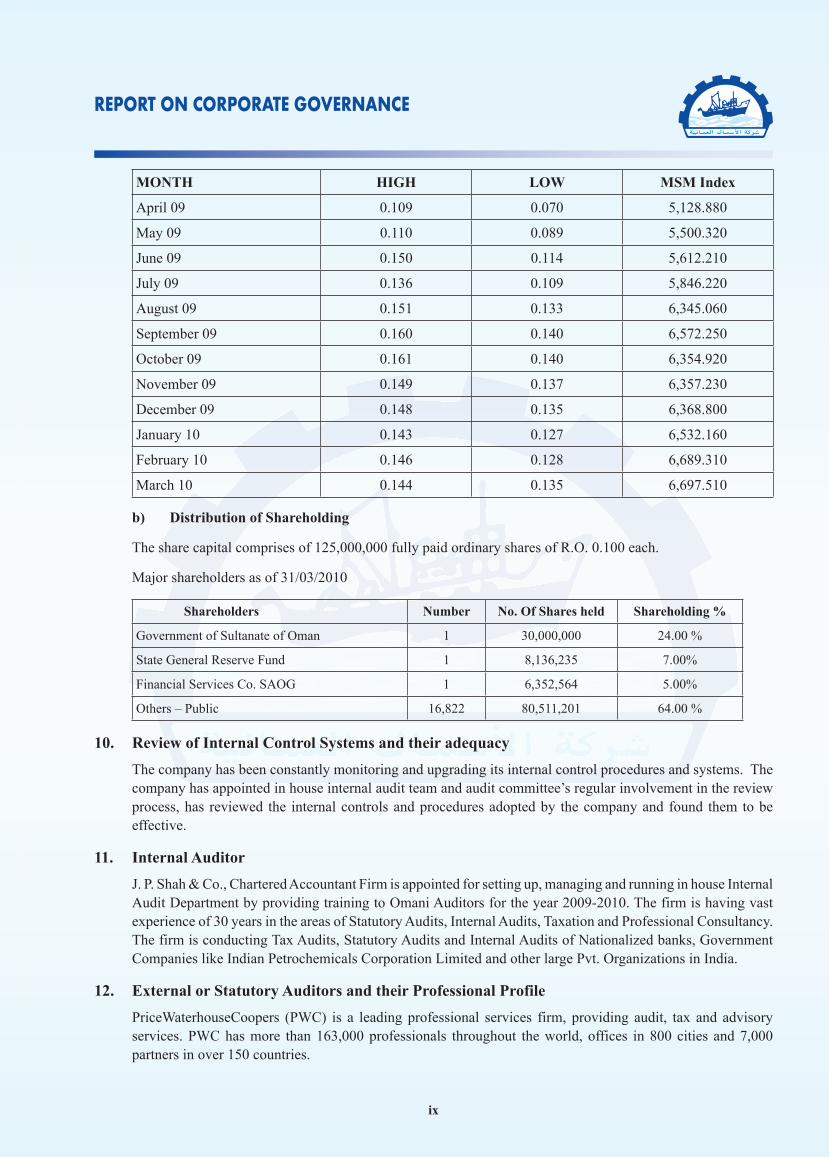

9. Market Data

a) The following table depicts the high, and low of company’s share traded during the financial year ended 31st March 2010 with month end general index.

ix

REPORT ON CORPORATE GOVERNANCE

MONTH HIGH LOW MSM Index

April 09 0.109 0.070 5,128.880

May 09 0.110 0.089 5,500.320

June 09 0.150 0.114 5,612.210

July 09 0.136 0.109 5,846.220

August 09 0.151 0.133 6,345.060

September 09 0.160 0.140 6,572.250

October 09 0.161 0.140 6,354.920

November 09 0.149 0.137 6,357.230

December 09 0.148 0.135 6,368.800

January 10 0.143 0.127 6,532.160

February 10 0.146 0.128 6,689.310

March 10 0.144 0.135 6,697.510

b) Distribution of Shareholding

The share capital comprises of 125,000,000 fully paid ordinary shares of R.O. 0.100 each.

Major shareholders as of 31/03/2010

Shareholders Number No. Of Shares held Shareholding %

Government of Sultanate of Oman 1 30,000,000 24.00 %

State General Reserve Fund 1 8,136,235 7.00%

Financial Services Co. SAOG 1 6,352,564 5.00%

Others – Public 16,822 80,511,201 64.00 %

10. Review of Internal Control Systems and their adequacy

The company has been constantly monitoring and upgrading its internal control procedures and systems. The company has appointed in house internal audit team and audit committee’s regular involvement in the review process, has reviewed the internal controls and procedures adopted by the company and found them to be effective.

11. Internal Auditor

J. P. Shah & Co., Chartered Accountant Firm is appointed for setting up, managing and running in house Internal Audit Department by providing training to Omani Auditors for the year 2009-2010. The firm is having vast experience of 30 years in the areas of Statutory Audits, Internal Audits, Taxation and Professional Consultancy. The firm is conducting Tax Audits, Statutory Audits and Internal Audits of Nationalized banks, Government Companies like Indian Petrochemicals Corporation Limited and other large Pvt. Organizations in India.

12. External or Statutory Auditors and their Professional Profile

PriceWaterhouseCoopers (PWC) is a leading professional services firm, providing audit, tax and advisory services. PWC has more than 163,000 professionals throughout the world, offices in 800 cities and 7,000 partners in over 150 countries.

x

REPORT ON CORPORATE GOVERNANCE

PWC in the Middle East and South Asia employs more than 4,000 professional and have offices in 15 countries.

The Oman practices of PWC were established in 1974. PWC Oman currently has a staff compliment in audit, tax and advisory services in excess of 100, including 5 partners. PWC Oman is accredited by the Capital Market Authorities to audit Omani listed companies.

13. Legal consultant

M/s Yassir Al Salami & Associates is a noted local legal consultant who employs qualified professional lawyers and was appointed as our retainer legal consultants for pursuing the company’s legal matters.

14. Acknowledgment

The Board of Directors acknowledges confirmation of:

Its responsibility for the preparation of the financial statements in accordance with the applicable standards

and rules.

Review of the efficiency and adequacy of internal control systems of the Company and that it compliance

with internal rules and regulations

There are no material matters effects the continuation of the Company and its ability to continue its

operation during the next financial year.

For OMAN FISHERIES CO SAOG For OMAN FISHERIES CO SAOG

AUTHORISED SIGNATORY AUTHORISED SIGNATORY

2

CONSOLIDATED AND PARENT COMPANY STATEMENT OF

COMPREHENSIVE INCOME

For the year ended 31 March 2010

Group Parent company

2010 2009 2010 2009

Note RO RO RO RO

Sales 6 11,829,840 10,855,668 11,812,729 10,846,329

Insurance claims for property, plant and equipment

4 199,440 146,935 199,440 146,935

Loss on sale of property, plant and equipment

4 (120,355) (1,427) (120,355) (1,427)

Other income 49,317 70,068 46,630 70,068

11,958,242 11,071,244 11,938,444 11,061,905

Cost of goods sold 7 (7,662,259) (7,553,191) (7,662,259) (7,553,191)

Staff costs 8 (1,185,611) (1,173,724) (1,171,624) (1,170,449)

Other operating expenses 9 (1,979,910) (1,924,964) (1,979,049) (1,897,730)

Fishing levy (405,607) (247,481) (405,607) (247,481)

Depreciation 15 (226,888) (267,874) (226,845) (267,811)

Contribution to Fisheries Research Fund

(50,712) (30,935) (50,712) (30,935)

Impairment of property, plant and equipment

15 - (147,561) - (147,561)

Operating profit/(loss) 447,255 (274,486) 442,348 (253,253)

Investment income/(loss) 10 644,512 (1,770,501) 644,512 (1,770,501)

Foreign exchange gain 11 33,293 788 33,293 788

Interest expense 12 (2,568) (8,233) (2,568) (8,233)

Interest income 12 469,102 435,638 469,102 435,638

Finance income - net 466,534 427,405 466,534 427,405

Profit/(loss) before taxation 1,591,594 (1,616,794) 1,586,687 (1,595,561)

Taxation 13 (106,921) (17,393) (106,921) (17,393)

Profit/(loss) and total comprehensive income/(loss) for the year

1,484,673 (1,634,187) 1,479,766 (1,612,954)

Earning/(loss) per share 14 0.012 (0.013) 0.012 (0.013)

The notes on pages 6 to 33 form an integral part of these financial statements.

Report of the Auditors - Page 1

3

CONSOLIDATED AND PARENT COMPANY STATEMENT OF

FINANCIAL POSITION

At 31 March 2009

Group Parent company2010 2009 2010 2009

Note RO RO RO ROASSETSNon-current assetsProperty, plant and equipment 15 863,317 824,879 863,291 824,810Investment in subsidiary 16 - - 15,750 15,750Due from subsidiary 31(b) - - 54,382 -Held to maturity financial assets 17 1,105,073 1,637,581 1,105,073 1,637,581Fixed deposits 22 6,981,947 5,666,027 6,981,947 5,666,027Deferred tax asset 27 19,874 5,665 19,874 5,665

8,970,211 8,134,152 9,040,317 8,149,833Current assets Held to maturity financial assets 17 1,502,141 - 1,502,141 -Inventories 18 1,377,144 1,656,633 1,377,144 1,656,633Trade and other receivables 20 1,694,510 1,579,565 1,745,875 1,682,303Financial assets at fair value through profit or loss 21 2,109,378 1,389,100 2,109,378 1,389,100Short term deposits 22 500,000 1,538,104 500,000 1,538,104Cash and cash equivalents 22 576,644 792,007 554,308 775,844

7,759,817 6,955,409 7,788,846 7,041,984Total assets 16,730,028 15,089,561 16,829,163 15,191,817

EQUITY Capital and reserves Share capital 23 12,500,000 12,500,000 12,500,000 12,500,000Legal reserve 24 3,008,442 2,859,975 3,007,952 2,859,975Capital reserve 25 29,269 29,269 29,269 29,269Retained earnings/(accumulated losses) 87,037 (1,249,169) 189,587 (1,142,202)Total equity 15,624,748 14,140,075 15,726,808 14,247,042

LIABILITIES Non-current liabilities End of service benefits 26 163,481 155,549 161,658 155,113

Current liabilities Trade and other payables 28 786,926 729,466 785,824 725,191Taxation 13 154,873 64,471 154,873 64,471

941,799 793,937 940,697 789,662Total liabilities 1,105,280 949,486 1,102,355 944,775Total equity and liabilities 16,730,028 15,089,561 16,829,163 15,191,817Net assets per share 29 0.125 0.113 0.126 0.114

The financial statements were approved and authorized for issue by the Board of Directors on 22 May 2010 and were signed on their behalf by:

MOHAMMED BIN HAMAD AL MASROURI SALEH BIN NASSER BIN JUMA Al ARAIMI

CHAIRMAN DEPUTY CHAIRMAN

Report of the Auditors – page 1

4

CONSOLIDATED AND PARENT COMPANY STATEMENT OF CHANGES IN EQUITY

For the year ended 31 March 2010

Group

NoteShare capital

RO

Legal reserve

RO

Capitalreserve

RO

Retained earnings/

(accumulated losses)

RO

TotalRO

Balance at 1 April 2008 12,500,000 2,859,975 29,269 1,635,028 17,024,272

Comprehensive income

Loss for the year - - - (1,634,187) (1,634,187)

Transaction with owners:

Dividend paid - - - (1,250,010) (1,250,010)

Balance at 31 March 2009 12,500,000 2,859,975 29,269 (1,249,169) 14,140,075

Balance at 1 April 2009 12,500,000 2,859,975 29,269 (1,249,169) 14,140,075

Comprehensive income

Profit for the year - - - 1,484,673 1,484,673

Transaction with owners:

Transfer to legal reserve 24 - 148,467 - (148,467) -

Balance at 31 March 2010 12,500,000 3,008,442 29,269 87,037 15,624,748

Parent Company

Note

Share capital

RO

Legal reserve

RO

Capitalreserve

RO

Retained earnings/

(accumulated losses)

ROTotalRO

Balance at 1 April 2008 12,500,000 2,859,975 29,269 1,720,762 17,110,006

Comprehensive income

Loss for the year - - - (1,612,954) (1,612,954)

Transaction with owners:

Dividend paid - - - (1,250,010) (1,250,010)

Balance at 31 March 2009 12,500,000 2,859,975 29,269 (1,142,202) 14,247,042

Balance at 1 April 2009 12,500,000 2,859,975 29,269 (1,142,202) 14,247,042

Comprehensive income

Profit for the year - - - 1,479,766 1,479,766

Transaction with owners:

Transfer to legal reserve 24 - 147,977 - (147,977) -

Balance at 31 March 2010 12,500,000 3,007,952 29,269 189,587 15,726,808

The notes on pages 6 to 33 form an integral part of these financial statements.

Report of the Auditors – page 1

5

Note Group Parent company

2010 2009 2010 2009

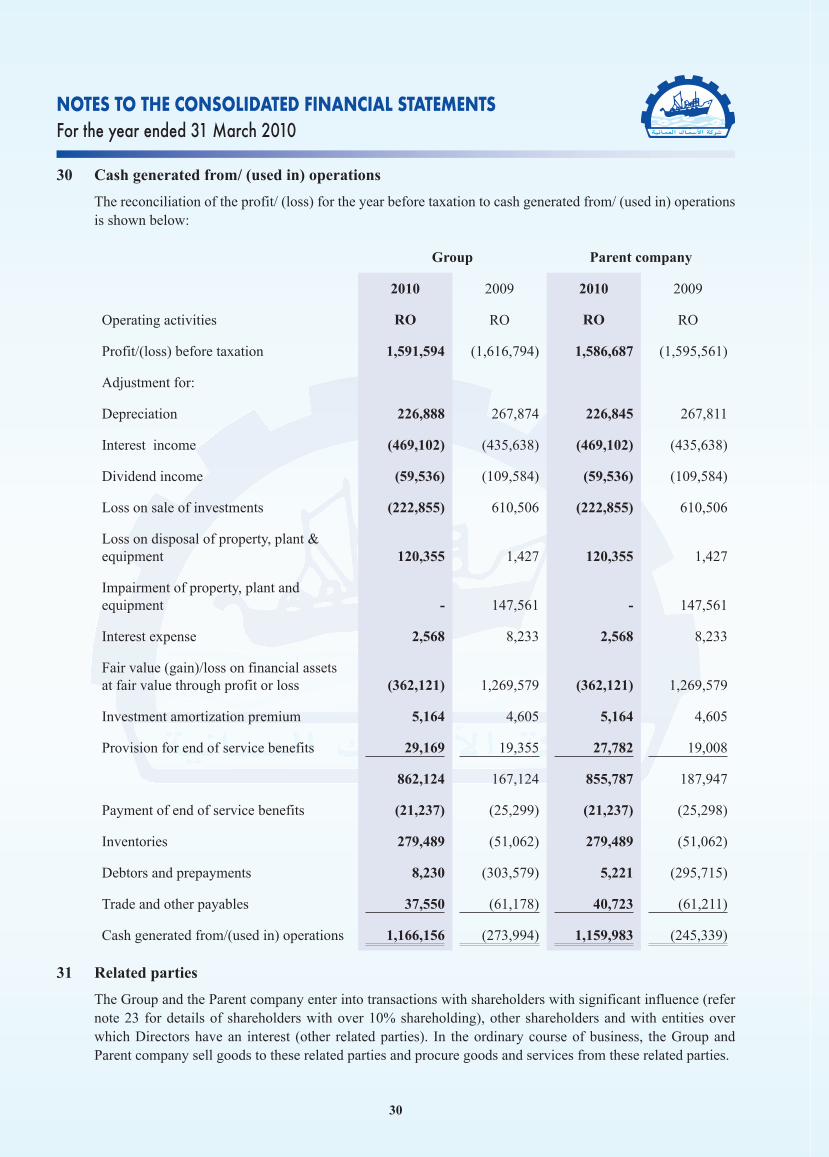

Operating activities RO RO RO RO

Cash generated from/(used in) operations 30 1,166,156 (273,994) 1,159,983 (245,339)

Interest paid (2,568) (8,233) (2,568) (8,233)

Interest received 345,927 432,827 345,927 432,827

Tax paid (30,728) - (30,728) -

Net cash from operating activities 1,478,787 150,600 1,472,614 179,255

Investing activities

Purchase of property, plant and equipment 15 (395,771) (79,309) (395,771) (79,309)

Proceeds from disposal of property, plant and equipment 30,000 - 30,000 -

Purchase of investments (1,744,680) (1,825,120) (1,744,680) (1,825,120)

Proceeds from sale of investments 1,609,378 907,177 1,609,378 907,177

Dividend received 59,536 109,584 59,536 109,584

(Decrease)/ increase in bank deposits (277,816) 1,898,232 (277,816) 1,898,232

Investment in held to maturity financial assets (974,797) - (974,797) -

Held to maturity financial assets matured - 500,000 - 500,000

Net cash (used in)/from investing activities (1,694,150) 1,510,564 (1,694,150) 1,510,564

Financing activities

Dividend paid - (1,250,010) - (1,250,010)

Net change in cash and cash equivalents (215,363) 411,154 (221,536) 439,809

Cash and cash equivalents at beginning of year 792,007 380,853 775,844 336,035

Cash and cash equivalents at end of year 576,644 792,007 554,308 775,844

The notes on pages 6 to 33 form an integral part of these financial statements.

Report of the Auditors – page 1.

CONSOLIDATED AND PARENT COMPANY STATEMENT

OF CASH FLOWS

For the year ended 31 March 2010

6

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

1 Legal status and principal activities

Oman Fisheries CO. SAOG (“the company” or “the Parent Company”) is an Omani Joint Stock Company registered under the Commercial Companies Law of Oman. The principal activities of the Company are the procurement, processing and sale of fresh, frozen and coated fish, fishing and the sale of fishing rights.

On 27 August 2005, the company incorporated a company in UAE, Oman Fisheries Co. FZE with an initial registered share capital of RO 15,750. Oman Fisheries Co. FZE (“the Subsidiary”) registered in United Arab Emirates as a free zone company, is a wholly owned subsidiary of the company. The subsidiary company is engaged in the business of distribution of the products of the Parent Company and it started its operations on 1 February 2006. The consolidated financial statements comprise of the Parent Company and its subsidiary, collectively “the Group”.

2 Summary of significant accounting policies

The principal accounting policies are summarised below. These policies have been consistently applied to each of the years presented, unless otherwise stated.

2.1 Basis of preparation

(a) These financial statements are prepared on the historical cost basis, as modified by the revaluation of investments held as financial assets at fair value through profit or loss and in accordance with International Financial Reporting Standards (IFRS), the requirements of the Commercial Companies Law of the Sultanate of Oman, 1974 (as amended) and comply with the disclosure requirements set out in the “Rules and Guidelines on Disclosure by issuer of Securities and Insider Trading” issued by the Capital Market Authority (CMA) of the Sultanate of Oman.

(b) The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Group’s accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in Note 4.

(c) New and amended standards adopted by the group:

IFRS 7 ‘Financial instruments – Disclosures’ (amendment) - effective 1 January 2009. The amendment requires enhanced disclosures about fair value measurement and liquidity risk. In particular, the amendment requires disclosure of fair value measurements by level of a fair value measurement hierarchy. As the change in accounting policy only results in additional disclosures, there is no impact on earnings per share;

IAS 1 (revised), ‘Presentation of financial statements’ – effective 1 January 2009. The revised standard prohibits the presentation of items of income and expenses (that is, ‘non-owner changes in equity’) in the statement of changes in equity, requiring ‘non-owner changes in equity’ to be presented separately from owner changes in equity in a statement of comprehensive income. As a result the company presents in the statement of changes in equity all owner changes in equity, whereas all non-owner changes in equity are presented in the statement of comprehensive income. Comparative information has been re-presented so that it also is in conformity with the revised standard. The change in accounting policy only impacts presentation aspects, there is no impact on earnings per share;

IFRS 8, Operating segments (effective 1 January 2009).

IAS 27 (Revised), ‘Consolidated and separate financial statements’ (effective from 1 July 2009);

7

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

2 Summary of significant accounting policies (continued)2.2 Consolidation

(a) Subsidiaries

Subsidiaries are all entities (including special purpose entities) over which the Group has the power to govern the financial and operating policies generally accompanying a shareholding of more than one half of the voting rights. The existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing whether the Group controls another entity. Subsidiaries are fully consolidated from the date on which control is transferred to the Group. They are de-consolidated from the date that control ceases.

The purchase method of accounting is used to account for the acquisition of subsidiaries by the Group. The cost of an acquisition is measured as the fair value of the assets given, equity instruments issued and liabilities incurred or assumed at the date of exchange, plus costs directly attributable to the acquisition. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date, irrespective of the extent of any minority interest. The excess of the cost of acquisition over the fair value of the Group’s share of the identifiable net assets acquired is recorded as goodwill.

Inter-company transactions, balances and unrealised gains on transactions between Group companies are eliminated. Unrealised losses are also eliminated. Accounting policies of subsidiaries have been changed where necessary to ensure consistency with the policies adopted by the Group.

2.3 Revenue recognitionRevenue from the sale of goods is stated at the fair value of the consideration received or receivable, net of returns and allowances, trade discounts and volume rebates. Revenue is recognised when the significant risks and rewards of ownership have been transferred to the buyer, recovery of the consideration is probable, the associated costs and possible return of goods can be estimated reliably, and there is no continuing management involvement with the goods.

Sales represent the invoiced value of fish supplied by the Group during the year. Sale of fishing rights is recognised on an accrual basis.

2.4 Foreign currency translation

(a) Functional and presentation currency

Items included in the financial statements of each of the Group’s entities are measured using the currency of the primary economic environment in which the entity operates (‘the functional currency’). The consolidated financial statements are presented in ‘Rial Omani’, which is the Parent company’s functional and the Group’s presentation currency.

(b) Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions or valuation where items are re-measured. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in the statement of comprehensive income.

(c) Group companies

The accounting records of the subsidiary, Oman Fisheries Co. FZE are maintained in UAE Dirhams (AED). The Rial Omani amounts included in the consolidated financial statements have been translated at an exchange rate of 0.105 Omani Rial to each AED for the statement of comprehensive income and the statement of financial position items, as the AED to RO exchange rate has effectively remained fixed during the year, both currencies being pegged to the US Dollar.

8

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

2.5 Finance costs and income

Finance cost comprises of interest payable on overdraft facility and finance income comprises of interest income from deposits and held to maturity financial assets. Finance income and cost are accounted on accrual basis using the effective interest rate method.

2.6 Operating leases

Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments made under operating leases are included in “other operating expense” in the statement of comprehensive income on a straight-line basis over the period of the lease.

2.7 Taxation

Income tax on the results for the year comprises current and deferred tax.

Current tax is recognised in the statement of comprehensive income as the expected tax payable on the taxable income for the year, using tax rates enacted or substantially enacted at the reporting date, and any adjustment to tax payable in respect of previous years.

Deferred income tax is provided, using the liability method, for all temporary differences arising between the tax bases of assets and liabilities and their carrying values for financial reporting purposes. Currently enacted tax rates are used to determine deferred tax. Deferred income tax assets and liabilities are offset as there is a legally enforceable right to offset these in Oman.

The principal temporary differences arise from depreciation on property, plant and equipment, provision for doubtful debts and provision for slow moving inventories.

2.8 Property, plant and equipment

Property, plant and equipment are stated at historical cost less accumulated depreciation. The cost of property, plant and equipment is their purchase price together with any incidental expenses that are directly attributable to the acquisition of the item. Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the establishment and the cost of the item can be measured reliably. All other repairs and maintenance are charged to the statement of comprehensive income during the financial year in which they are incurred.

The cost of property, plant and equipment is written down to residual value in equal installments over the estimated useful lives of the assets. The estimated useful lives are:

YearsBuildings and cabins 5 - 25Plant and equipment 3 - 10Boats and trawlers 5 - 15Motor vehicles 3 - 5Furniture, fixtures and office equipment 3 - 10

Land is not depreciated as it is deemed to have an indefinite life.

Capital work-in-progress is not depreciated until it is transferred into one of the above categories at the time when it is ready for use.

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at each reporting date.

Where the carrying amount of an asset is greater than its estimated recoverable amount it is written down immediately to its recoverable amount.

Gains and losses on disposals of property and equipment are determined by reference to their carrying amounts, and are taken into account in determining operating profit.

9

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

2.9 Investment in subsidiary

Classification

A company is a subsidiary company, if Oman Fisheries Co (SAOG) has the power to govern the financial and operating policies generally accompanying a shareholding of more than one half of the voting rights so as to obtain benefits from the investee company’s activities.

Valuation

Investment in a subsidiary company is stated at cost less any diminution in the value of specific investment, which is other than temporary by the Parent company. Investment income is accounted for in the year in which entitlement is established.

2.10 Financial assets

The Group classifies its financial assets in the following categories: at fair value through profit or loss, held to maturity and loans and receivables. The classification depends on the purpose for which the financial assets were acquired. Management determines the classification of its financial assets at initial recognition.

(a) Financial assets at fair value through profit or loss

Classification

A financial asset is classified in this category if acquired principally for the purpose of selling in the short term or if so designated by management.

Valuation

Financial assets carried at fair value through profit or loss are initially recognised at fair value and transaction costs are expensed in the statement of comprehensive income. Financial assets at fair value through profit or loss are subsequently carried at fair value.

The fair values of quoted investments are based on current market bid prices. Gains or losses arising from changes in the fair value are presented in the statement of comprehensive income in the period in which they arise.

Investments are derecognised when the rights to receive cash flows from the investments have expired or have been transferred and the Group has transferred subsequently all risks and rewards of ownership.

All purchases and sales of investments are recognised on the trade date, which is the date that the Group commits to purchase or sell the asset.

(b) Held to maturity investments

Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturities that the Group’s management has the positive intent and ability to hold to maturity.

Held-to-maturity investments are initially recognized at cost and subsequently re-measured at amortized cost using the effective yield method less any provision for impairment.

Interest receivable from held to maturity is accounted for on the accruals basis.

(c) Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are included in current assets, except for maturities greater than 12 months after the reporting date. These are classified as non-current assets. The Group’s loans and receivables comprise deposits, trade and other receivables and cash and cash equivalents in the statement of financial position (notes 2.12 and 2.13).

10

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

2.11 Inventories

Inventories are valued at the lower of cost and net realisable value. Cost is determined on the weighted average cost method. The cost of inventories comprises of direct cost of materials and related expenses. Net realisable value is the price at which inventories can be sold in the normal course of business after allowing for the costs of realisation. Provision is made where necessary for obsolete, slow moving and defective items.

2.12 Trade and other receivables

Trade debtors and other receivables are initially recognised at their fair value and subsequently stated at amortised cost using effective interest rate method, less provision for impairment. A provision for impairment of trade receivables is established when there is objective evidence that the Group will not be able to collect all amounts due according to the original terms of receivables. Significant financial difficulties of the debtor, probability that the debtor will enter bankruptcy or financial reorganisation, and default or delinquency in payments are considered indicators that the trade receivable is impaired. The amount of the provision is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the effective interest rate. The amount of any provision is recognised in the statement of comprehensive income within “other operating expenses”. Subsequent recoveries of amounts previously written off are credited against “other operating expenses” in the statement of comprehensive income.

2.13 Cash and cash equivalents

For the purpose of the cash flow statement the Group considers all bank balances, including short term deposits with a maturity of three months or less from the date of placement, to be cash equivalents.

2.14 End of service benefits and leave entitlements

End of service benefits are accrued in accordance with the terms of employment of the Group’s employees at the reporting date, having regard to the requirements of the Oman Labour Law 2003 as amended and UAE Labour Law. Employee entitlements to annual leave and leave passage are recognised when they accrue to employees and an accrual is made for the estimated liability as a result of services rendered by employees up to the reporting date. These accruals are included in current liabilities, while that relating to end of service benefits is disclosed as a non-current liability.

Contributions to a defined contribution retirement plan and occupational hazard insurance for Omani employees in accordance with the Omani Social Insurances Law of 1991 are recognised as an expense in the statement of comprehensive income as incurred.

2.15 Trade and other payables

Trade payables are recognized initially at fair value and subsequently measured at amortized cost using the effective interest method.

Liabilities are recognised for amounts to be paid for goods and services received, whether or not billed to the Group.

2.16 Earning per share

The Group presents basic earnings per share (EPS) data for its ordinary shares. Basic EPS is calculated by dividing the profit or loss attributable to ordinary shareholders of the Parent company/Group by the weighted average number of ordinary shares outstanding during the period.

2.17 Directors’ remuneration

The Directors’ remuneration is governed as set out by the Commercial Companies Law and the rules prescribed by the Capital Market Authority.

11

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

2.17 Directors’ remuneration (continued)

The Annual General Meeting shall approve the remuneration and the sitting fees for the Board of Directors and its sub-committees provided that such fees shall not exceed a minimum of 5% of the annual net profit after deduction of the legal reserve and the optional reserve as distribution of dividends to the shareholders. Such fees shall not exceed RO 200,000 in one year. The sitting fees for each Director shall not exceed RO 10,000 in one year.

2.18 Dividend distribution

Dividend distribution to the company’s shareholders is recognised as a liability in the company’s financial statements in the period in which the dividends are approved by the Parent company’s shareholders.

2.19 Segment reporting

Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision-maker. The chief operating decision maker, who is responsible for allocating resources and assessing performance of the operating segments, make strategic decisions and has been identified as the Board of Directors.

3 Financial risk management

3.1 Financial risk factors

The Group’s activities expose it to a variety of financial risks: market risk (including currency risk, price risk and interest rate risk), credit risk and liquidity risk. The Group’s overall risk management program focuses on the unpredictability of financial markets and seeks to minimize potential adverse effects on the financial performance of the Group. Risk management is carried out by the management under policies approved by the Board of Directors.

(a) Market risk

(i) Foreign exchange risk

Foreign exchange risk arises when future commercial transactions or recognised assets or liabilities are denominated in a currency that is not the entity’s functional currency. The Group is exposed to foreign currency risk arising from currency exposures with respect to US Dollars, UAE Dirham, Saudi Riyal and Euro. In respect of the Group’s transactions denominated in US Dollars, Saudi Riyals and UAE Dirham, the Group is not exposed to currency risk as the Rial Omani, Saudi Riyals and UAE Dirham are pegged to the US Dollar.

At 31 March 2010, if the Rial Omani had weakened/strengthened by 5% against the Euro with all other variables held constant, post-tax profit for the year would have been RO 5,022 (2009 - nil) higher/lower primarily as a result of monetary assets.

(ii) Price risk

Price risk is the risk that the value of a financial instrument will fluctuate as a result of changes in market prices, whether these changes are caused by factors specific to the individual security, or its issuer, or factors affecting all securities in the market.

The Group is exposed to equity price risk because of investment in certain publicly listed companies at the Muscat Securities Market (MSM) which have been classified as financial assets at fair value through profit or loss. The Group limits market risk by maintaining a selective and strategic portfolio and by regular monitoring of the market. In addition the Group monitors actively the key factors that effect stock market movements.

12

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

3.1 Financial risk factors (continued)

The table below summarises the impact of increase/(decreases) of the MSM Index on the gains/losses on equity securities on the assumption that the equity index had increased/decreased by 5% with all other variables held constant:

Index GroupParent

company GroupParent

company

2010 2010 2009 2009

RO RO RO RO

MSM 105,469 105,469 69,455 69,455

(iii) Interest rate risk

Interest rate risk arises from the possibility of changes in interest rates and mismatches or gaps in the amount of assets and liabilities that mature or re-price in a given period.

The Group is exposed to fair value interest rate risk on its held to maturity financial assets and fixed deposits placed with the commercial banks as these carry fixed interest rates.

At 31 March 2010, if the interest rate were to shift by 0.5%, there would be a maximum increase or decrease in the interest income by RO 85,356 (2009 - RO 72,539).

(b) Credit risk

Credit risk is the risk of financial loss if a customer or counterparty to a financial instrument fails to meet its contractual obligations.

Credit risk arises from cash and cash equivalents, long term fixed deposits, trade receivables and credit exposures to customers through outstanding debtors including outstanding amounts due from related parties (refer to note 19 for credit quality of banks and financial institutions).

The Group’s exposure to credit risk is influenced mainly by the individual characteristics of each customer. The demographics of the Group’s large customer base, including the default risk of the industry in the country of operation, which customers operate, has an influence on credit risk. Exposure to credit risk is monitored on an ongoing basis. Credit evaluations are performed on all customers requiring credit. All export customers risks are either covered by letter of credit, insurance or by way of a bank guarantee.

The Group categorizes its customers as hypermarkets, private entities and other retail customers.

The Group has significant concentrations of credit risk, details of which are provided in note 20. The Group manages concentration of its credit risk by monitoring collections within the credit period.

The maximum exposure to credit risk for trade receivables at the reporting date for the Group and the Parent company by geographical region was:

Group Parent company

2010 2009 2010 2009

RO RO RO RO

Local customers 361,852 237,268 331,879 237,268

Foreign customers 546,582 679,776 546,582 661,829

908,434 917,044 878,461 899,097

13

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

3.1 Financial risk factors (continued)

The maximum exposure to credit risk for trade receivables at the reporting date for the Group and Parent company by type of customer was:

Group Parent company2010 2009 2010 2009RO RO RO RO

Hypermarkets 29,260 30,999 27,429 29,291Private entities 715,974 717,800 687,832 703,732Other retail customers 163,200 168,245 163,200 166,074

908,434 917,044 878,461 899,097

Management does not expect any losses from non-performances by these counterparties.

(c) Liquidity risk

Liquidity risk is the risk that the Group will not be able to meet its financial obligations as they fall due. The Group’s approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damages to the Group’s reputation.

The Group’s financial liabilities consisting of trade and other payables for Group of RO 786,926 (2009 - RO 729,466) and for Parent company of RO 785,824 (2009 - RO 725,191) are the contractual undiscounted cash flows which are due within twelve months from the reporting date.

3.2 Fair value estimation

Effectively 1 January 2009, the Group adopted the amendments to IFRS 7 for financial instruments that are measured in the statement of financial position at fair value. Level 1 – quoted market prices; Level -2, inputs other that quoted prices included within level 1 that are observable for the asset or liability directly or indirectly; Level -3, inputs for the asset or liability that are not based on the observable market data. The Group’s entire financial assets at fair value through profit or loss are valued using Level 1 fair value techniques.

The face value less any estimated credit adjustments for financial assets and liabilities with a maturity of less than one year are assumed to approximate to their fair values. The fair values of quoted securities are based on market bid prices at the reporting date. The fair values of non-current fixed deposits are considered to approximate to their carrying amounts as these carry interest rates which are believed to be the commercial interest rates.

The table below summarises the carrying amounts and their fair values of the financial assets not presented in the statement of financial position at their fair value.

2010 2009Carrying

valueFair value Carrying

valueFair value

RO RO RO ROFinancial assets Held-to-maturity investments 1,105,073 1,153,755 1,637,581 1,630,700

3.3 Capital risk management

The capital of the Group comprises of paid-up share capital, retained earnings, legal reserves and special reserves. Summary of quantitative data as to what it manages as the capital and any changes therein from the previous year are given in statement of changes in equity. The Group’s objectives when managing capital are to safeguard the Group’s ability to continue as a going concern in order to provide returns for shareholders and to maintain an optimal capital structure to reduce the cost of capital.

14

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

4 Critical accounting estimates

The Group makes estimates and assumptions concerning the future. Estimates are regularly evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are set out below:

Insurance claim/loss on sale of boats

During the year, the parent company disposed two boats (Asmak 1 and Asmak 2) included in the fixed assets as approved by the board of directors during 2009. Asmak 1 and Asmak 2 were sold at a loss of RO 68,431 and RO 51,924 respectively. During the year as against Asmak 2, an amount of RO 199,440 was agreed and received as insurance claim settlement and accordingly recognised as income. In respect of Asmak 1 during 2009, an amount of RO 146,935 was recognised as income towards insurance claim based on agreed settlement with the insurer in 2009.

Impairment of trade receivables

An estimate of the collectible amount of trade receivables is made when collection of the full amount is no longer probable. For individually significant amounts, this estimation is performed on an individual basis. Amounts which are not individually significant, but which are past due, are assessed collectively and a provision applied according to the length of time past due, based on historical recovery rates.

Impairment of inventories

Inventories are held at the lower of cost and net realisable value. When inventories become old or obsolete, an estimate is made of their net realisable value. For individually significant amounts this estimation is performed on an individual basis. Amounts which are not individually significant, but which are old or obsolete, are assessed collectively and a provision applied according to the inventory type and the degree of ageing or obsolescence, based on historical selling prices.

5 Segment information

Management has determined the operating segments based on the reports reviewed by the Board of Directors that are used to make strategic decisions. The Board considers the business from a group level as the group is principally engaged in one segment which is fishing, procurement, processing and sale of fish. The Board also considers the geographical segments. The directors review monthly analysis of these geographical segments by monitoring volume and value and the related debtors. As the directors effectively look at only one group level segment, all relevant details are as set out in the statement of comprehensive income and statement of financial position. The geographical distribution of revenue and receivables, based on the reports reviewed by the directors are set out as follows

Geographical segments

The geographical analysis relating to the primary segment based on the location of the Group’s customers is as follows:

SalesGroup Parent company

2010 2009 2010 2009RO RO RO RO

Far East 4,749,431 4,411,136 4,749,431 4,411,136GCC and Middle East 4,492,243 4,128,369 4,475,132 4,119,030Europe 854,383 1,160,433 854,383 1,160,433Others 1,733,783 1,155,730 1,733,783 1,155,730

11,829,840 10,855,668 11,812,729 10,846,329

15

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

5 Segment information (continued)

Trade debtors

Group Parent company

2010 2009 2010 2009

RO RO RO RO

Far East 384,186 223,852 384,186 223,852

GCC and Middle East 377,937 349,398 347,964 331,451

Europe 55,341 240,669 55,341 240,669

Others 61,160 87,839 61,160 87,839

878,624 901,758 848,651 883,811

6 Sales

Group Parent company

2010 2009 2010 2009

RO RO RO RO

Procured from fishermen 7,320,764 5,794,379 7,320,764 5,794,379

Purchased from Yemen centre 1,758,102 2,479,407 1,758,102 2,479,407

Received from trawler companies under fishing rights 958,373 714,133 958,373 714,133

Breaded products 811,122 795,002 794,011 785,663

Purchased from Saudi Arabia centre 541,443 703,948 541,443 703,948

Frozen fish purchased from other suppliers and trawlers operating outside Oman 401,578 343,216 401,578 343,216

Purchased from Bahrain center 37,425 - 37,425 -

Received from operation of own boats 723 - 723 -

Purchased from India centre 310 25,337 310 25,337

Purchased from Somalia centre - 246 - 246

11,829,840 10,855,668 11,812,729 10,846,329

7 Cost of goods sold

Group Parent company

2010 2009 2010 2009

RO RO RO RO

Opening stock of fish 1,526,621 1,460,317 1,526,621 1,460,317

Purchases 6,757,975 6,906,945 6,757,975 6,906,945

Packing material consumed 308,974 302,941 308,974 302,941

Processing charges 304,496 409,609 304,496 409,609

Closing stock of fish (1,235,807) (1,526,621) (1,235,807) (1,526,621)

7,662,259 7,553,191 7,662,259 7,553,191

16

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

8 Staff costs

Group Parent company

2010 2009 2010 2009

RO RO RO RO

Salaries and wages 871,627 850,531 860,090 848,433

Air passage and leave salary 89,265 94,693 88,945 94,585

Housing expenses 70,645 62,951 70,645 62,951

End of service benefits (note 26) 29,169 19,355 27,782 19,008

Staff insurance 29,439 18,626 29,439 18,626

Social security costs 24,649 24,512 24,648 24,512

Others 70,817 103,056 70,075 102,334

1,185,611 1,173,724 1,171,624 1,170,449

9 Other operating expenses

Group Parent company

2010 2009 2010 2009

RO RO RO RO

Freight 760,624 675,973 760,624 675,972

Agency fee 114,053 14,141 121,549 14,141

Vehicle expenses 223,972 182,230 222,733 177,829

Repairs and maintenance 187,897 302,792 187,897 302,760

Electricity, water and fuel 157,780 161,525 157,780 161,524

Export related expenses 82,827 134,763 82,827 134,763

Ice charges 58,559 51,605 58,559 51,605

Professional fees 49,198 44,759 49,198 43,611

Insurance costs 47,313 64,028 47,135 63,852

Advertisement and sales promotion expenses 42,506 49,076 42,506 33,986

Traveling and entertainment 33,068 53,423 33,036 53,413

Communication expenses 29,250 43,275 28,906 42,968

Rent 24,341 14,978 20,403 10,765

Directors’ sitting fees 21,900 16,500 21,900 16,500

Printing and stationery 16,152 21,659 16,063 21,626

Provision for doubtful debts (note 20) 14,524 15,286 14,524 15,286

Directors’ remuneration 13,994 - 13,994 -

Bank charges 8,889 312 8,889 312

Sundry expenses 93,063 78,639 90,526 76,817

1,979,910 1,924,964 1,979,049 1,897,730

17

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

10 Investment income

Group and Parent company

2010 2009

RO RO

Financial assets at fair value through profit or loss

Dividend income 59,536 109,584

Gain/(loss) on sale of investments 222,855 (610,506)

Fair value gain/(loss) (note 21) 362,121 (1,269,579)

644,512 (1,770,501)

11 Foreign exchange gains - net

Profit before taxation is arrived at after crediting RO 33,293 (2009 - RO 788) on account of foreign exchange gains on year-end translation of foreign currency assets and liabilities.

12 Finance income - net

Group and Parent company

2010 2009

RO RO

Finance costs

Interest expenses on overdraft (2,568) (8,233)

Finance income

Interest income on deposits (note 22) 318,152 333,607

Interest income on held to maturity financial assets (note 17) 150,950 102,031

469,102 435,638

Finance income - net 466,534 427,405

13 Taxation

(a) The tax charge/(credit) for the year is analysed as follows:

Group and Parent company

2010 2009

RO RO

Current tax

In respect of current year 123,670 33,268

In respect of prior year (2,540) -

121,130 33,268

Deferred tax (note 27) (14,209) (15,875)

106,921 17,393

(b) The company is subject to income tax at the rate of 12% of taxable profits in excess of RO 30,000 (2009 - 12%) in accordance with the income tax laws of the Sultanate of Oman. The following is reconciliation between income taxes calculated on accounting profits at the applicable tax rates with the income tax expense for the year:

18

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

13 Taxation (Continued)

Group and Parent company2010 2009RO RO

Tax expense/(benefit) on accounting profit/(loss) 186,802 (191,467)Add/(less) tax effect of:Income not subject to tax (77,341) (13,150)Expenses not deductible - 225,610Reversal of excess tax provision in prior year (2,540) -Tax rate difference - (3,600)Tax charge for the year 106,921 17,393

(c) Gains and losses on sales of securities through the Muscat Securities Market are exempt from taxation from 2003.

(d) The tax assessments for the year ended 31 March 2006 to 2009 have not yet been agreed with the Oman Taxation Authorities. Board of Directors is of the opinion that any additional taxes that may be assessed would not be significant to the financial position of the Parent Company at 31 March 2010. The Parent Company was not subject to tax prior to 22 October 1999.

Oman Fisheries Co. FZE (The subsidiary)

Oman Fisheries Co. FZE is registered in Free Zone Establishment with limited liability at Sharjah Airport International Free Zone (SAIF Zone) in the Emirate of Sharjah and is not subject to taxation in the UAE.

(e) The movement in current tax liability is as follows:

Group and Parent company 2010 2009

RO ROAt 1 April 64,471 31,203Charge for the year 123,670 33,268Reversal in respect of prior year (2,540) -Paid during the year (30,728) -At 31 March 154,873 64,471

14 Earnings/(loss) per share

The earnings/(loss) per share has been derived by dividing the net profit/(loss) for the year attributable to shareholders by the weighted average number of shares outstanding. As there are no dilutive potential shares, the diluted earnings/(loss) per share is identical to the basic earnings/(loss) per share.

Group GroupParent

companyParent

Company

2010 2009 2010 2009

Profit/(loss) attributable to shareholders (RO) 1,484,673 (1,634,187) 1,479,766 (1,612,954)

Weighted average number of shares outstanding 125,000,000 125,000,000 125,000,000 125,000,000

Earnings/(loss) per share (RO) 0.012 (0.013) 0.012 (0.013)

19

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

15 Property, plant and equipment

Group

Land, buildings

and cabinsPlant and equipment

Boats and trawlers

Motor vehicles

Furniture, fixtures

and office equipment

Capital work in progress Total

RO RO RO RO RO RO RO

Cost

1 April 2009 1,396,630 1,801,161 477,107 191,796 238,245 - 4,104,939

Additions 56,877 78,246 1,050 14,960 29,032 235,516 415,681

Disposals - - (474,890) - (2,770) - (477,660)

31 March 2010 1,453,507 1,879,407 3,267 206,756 264,507 235,516 4,042,960

Depreciation

1 April 2009 1,184,761 1,433,522 299,642 165,197 196,938 - 3,280,060

Charge for the year 50,369 111,576 28,207 16,141 20,595 - 226,888

Disposals - - (324,583) - (2,722) - (327,305)

31 March 2010 1,235,130 1,545,098 3,266 181,338 214,811 - 3,179,643

Net book value

31 March 2010 218,377 334,309 1 25,418 49,696 235,516 863,317

Land, buildings

and cabinsPlant and equipment

Boats and trawlers

Motor Vehicles

Furniture, fixtures and

office Equipment Total

RO RO RO RO RO RO

Cost

1 April 2008 1,380,910 1,791,174 631,794 179,146 261,705 4,244,729

Additions 16,445 62,267 - 12,650 13,553 104,915

Disposals (725) (52,280) (7,126) - (37,013) (97,144)

Impairment - - (147,561) - - (147,561)

31 March 2009 1,396,630 1,801,161 477,107 191,796 238,245 4,104,939

Depreciation

1 April 2008 1,120,403 1,373,383 251,223 149,423 213,471 3,107,903

Charge for the year 64,776 111,320 55,545 15,774 20,459 267,874

Disposals (418) (51,181) (7,126) - (36,992) (95,717)

31 March 2009 1,184,761 1,433,522 299,642 165,197 196,938 3,280,060

Net book value

31 March 2009 211,869 367,639 177,465 26,599 41,307 824,879

20

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

15 Property, plant and equipment (continued)

Parent Company

Land, buildings

and cabinsPlant and equipment

Boats and trawlers

MotorVehicles

Furniture, fixtures

and office equipment

Capital work in progress Total

RO RO RO RO RO RO RO

Cost

1 April 2009 1,396,630 1,801,161 477,107 191,796 237,978 - 4,104,672

Additions 56,877 78,246 1,050 14,960 29,032 235,516 415,681

Disposals - - (474,890) - (2,770) - (477,660)

31 March 2010 1,453,507 1,879,407 3,267 206,756 264,240 235,516 4,042,693

Depreciation

1 April 2009 1,184,761 1,433,522 299,642 165,197 196,740 - 3,279,862

Charge for the year 50,369 111,576 28,207 16,141 20,552 - 226,845

Disposals - - (324,583) - (2,722) - (327,305)

31 March 2010 1,235,130 1,545,098 3,266 181,338 214,570 - 3,179,402

Net book value

31 March 2010 218,377 334,309 1 25,418 49,670 235,516 863,291

Land, buildings

and cabinsPlant and equipment

Boats and trawlers

Motorvehicles

Furniture, fixtures and

officeequipment Total

RO RO RO RO RO RO

Cost

1 April 2008 1,380,910 1,791,174 631,794 179,146 261,438 4,244,462

Additions 16,445 62,267 - 12,650 13,553 104,915

Disposals (725) (52,280) (7,126) - (37,013) (97,144)

Impairment - - (147,561) - - (147,561)

31 March 2009 1,396,630 1,801,161 477,107 191,796 237,978 4,104,672

Depreciation

1 April 2008 1,120,403 1,373,383 251,223 149,423 213,336 3,107,768

Charge for the year 64,776 111,320 55,545 15,774 20,396 267,811

Disposals (418) (51,181) (7,126) - (36,992) (95,717)

31 March 2009 1,184,761 1,433,522 299,642 165,197 196,740 3,279,862

Net book value

31 March 2009 211,869 367,639 177,465 26,599 41,238 824,810

Included above at a net book value of RO 13,557 (2009 - RO 7,724) are buildings and cabins constructed on leasehold land. The lease agreement will expire on 28 February 2011 and is renewable annually. The annual rental of this land is RO 10,288 (2009 - RO 9,615).

21

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

16 Investment in subsidiary

Details regarding the Parent company’s subsidiary are set out below:

Company nameCountry of

incorporation Year endPercentage held

Principal activities

2010 2009

Oman Fisheries Co. FZE UAE 31 March 100% 100% Procurement and sale of fish and fish products

17. Held to maturity financial assets

Group and Parent company

2010 2009

RO RO

At 1 April 1,637,581 2,142,186

Investment during the year 974,797 -

Matured during the year - (500,000)

Premium amortized during the year (5,164) (4,605)

At 31 March 2,607,214 1,637,581

Less: current portion included in current assets (1,502,141) -

1,105,073 1,637,581

Held to maturity financial assets comprise of Oman Government Development Bonds of RO 1,502,141 which earn interest at a rate of 5.25% per annum with maturity on 1 November 2010 and bonds issued by a commercial bank of RO 131,540 which earn interest at the rate of 7% per annum with maturity on 18 June 2013 and of RO 973,533 which earns interest at the rate of 8% per annum with maturity on 7 May 2016.

18 Inventories

Group and Parent company

2010 2009

RO RO

Fish 1,235,807 1,526,621

Maintenance spares 46,500 51,307

Packing materials 108,707 94,237

Others 6,130 4,468

1,397,144 1,676,633

Less: provision for slow moving and obsolete maintenance spares (20,000) (20,000)

1,377,144 1,656,633

(a) Fish stocks at 31 March 2010 represent 45 days (31 March 2009 - 55 days) of sales.

(b) Cost of stock directly written off to cost of sales amounted to RO 9,551 (2009 - RO 117)

22

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

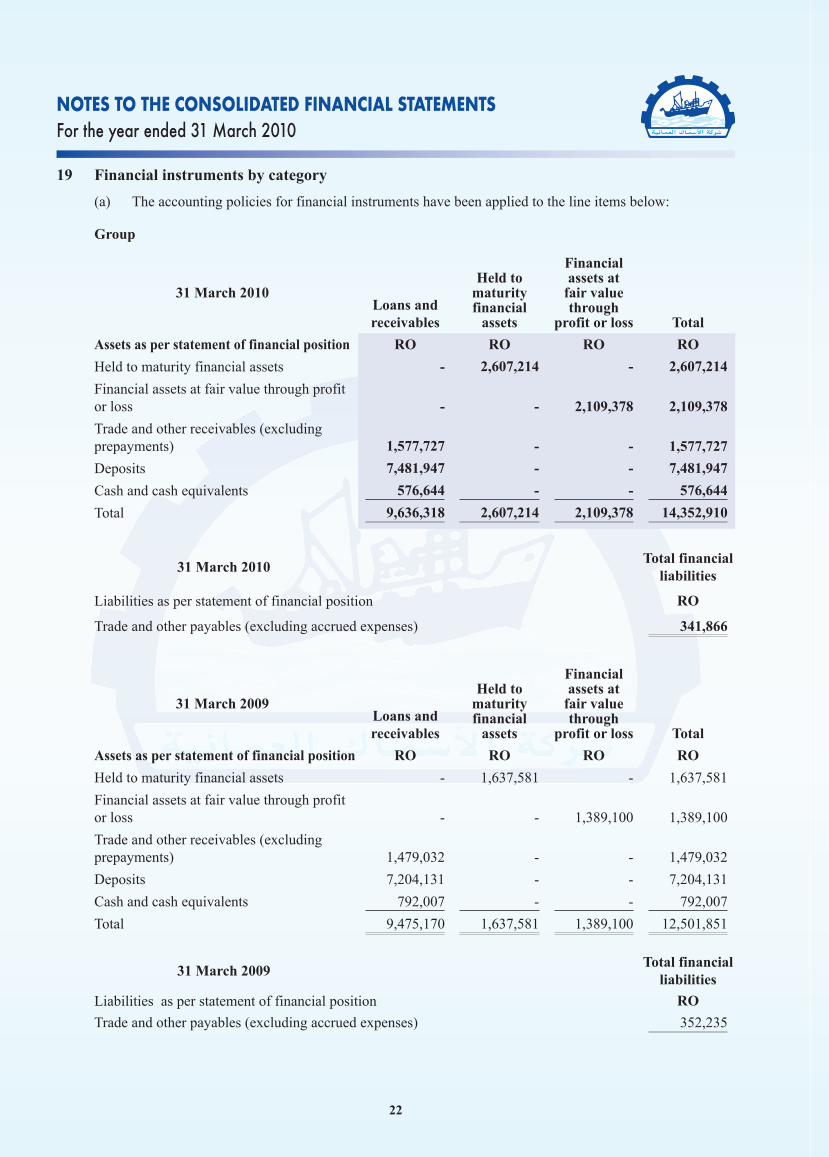

19 Financial instruments by category

(a) The accounting policies for financial instruments have been applied to the line items below:

Group

31 March 2010Loans and receivables

Held to maturity financial

assets

Financial assets at

fair value through

profit or loss Total

Assets as per statement of financial position RO RO RO RO

Held to maturity financial assets - 2,607,214 - 2,607,214

Financial assets at fair value through profit or loss - - 2,109,378 2,109,378

Trade and other receivables (excluding prepayments) 1,577,727 - - 1,577,727

Deposits 7,481,947 - - 7,481,947

Cash and cash equivalents 576,644 - - 576,644

Total 9,636,318 2,607,214 2,109,378 14,352,910

31 March 2010 Total financial

liabilities

Liabilities as per statement of financial position RO

Trade and other payables (excluding accrued expenses) 341,866

31 March 2009Loans and receivables

Held to maturity financial

assets

Financial assets at

fair value through

profit or loss Total

Assets as per statement of financial position RO RO RO RO

Held to maturity financial assets - 1,637,581 - 1,637,581

Financial assets at fair value through profit or loss - - 1,389,100 1,389,100

Trade and other receivables (excluding prepayments) 1,479,032 - - 1,479,032

Deposits 7,204,131 - - 7,204,131

Cash and cash equivalents 792,007 - - 792,007

Total 9,475,170 1,637,581 1,389,100 12,501,851

31 March 2009Total financial

liabilities

Liabilities as per statement of financial position RO

Trade and other payables (excluding accrued expenses) 352,235

23

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

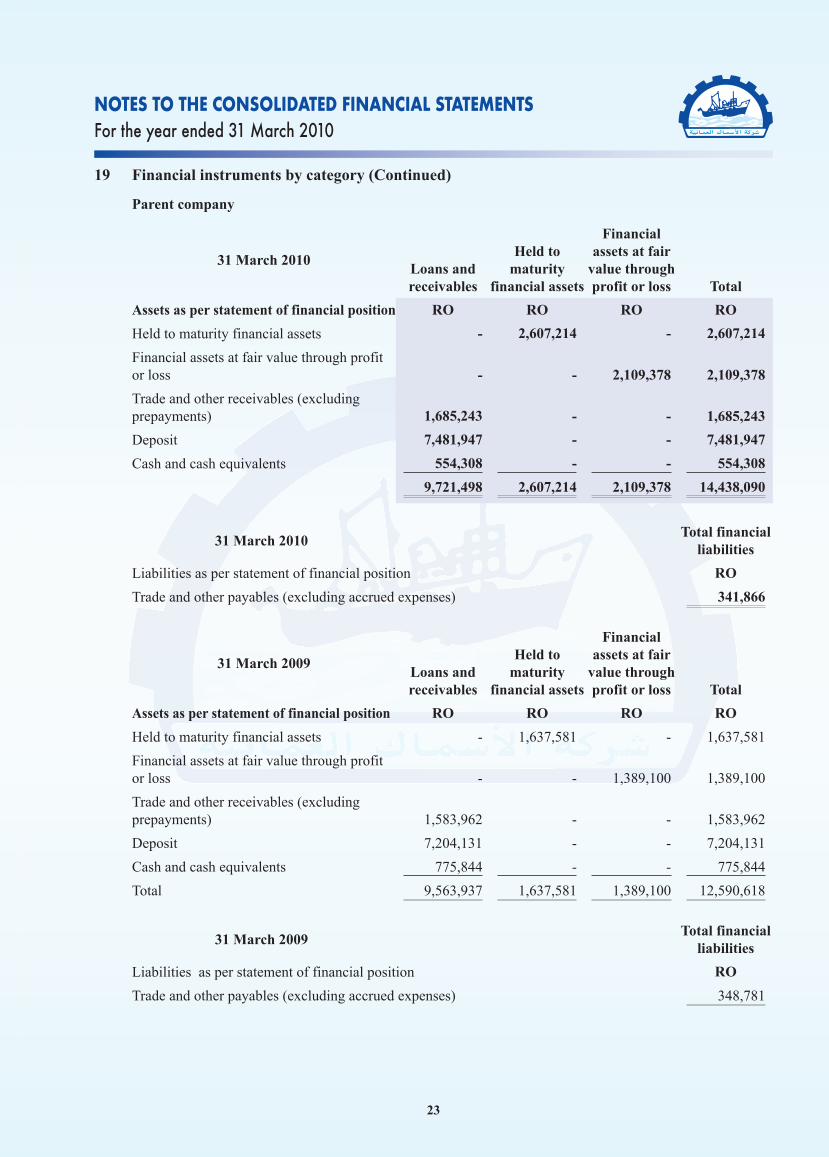

19 Financial instruments by category (Continued)

Parent company

31 March 2010Loans and receivables

Held to maturity

financial assets

Financial assets at fair

value through profit or loss Total

Assets as per statement of financial position RO RO RO RO

Held to maturity financial assets - 2,607,214 - 2,607,214

Financial assets at fair value through profit or loss - - 2,109,378 2,109,378

Trade and other receivables (excluding prepayments) 1,685,243 - - 1,685,243

Deposit 7,481,947 - - 7,481,947

Cash and cash equivalents 554,308 - - 554,308

9,721,498 2,607,214 2,109,378 14,438,090

31 March 2010Total financial

liabilities

Liabilities as per statement of financial position RO

Trade and other payables (excluding accrued expenses) 341,866

31 March 2009Loans and receivables

Held to maturity

financial assets

Financial assets at fair

value through profit or loss Total

Assets as per statement of financial position RO RO RO RO

Held to maturity financial assets - 1,637,581 - 1,637,581

Financial assets at fair value through profit or loss - - 1,389,100 1,389,100

Trade and other receivables (excluding prepayments) 1,583,962 - - 1,583,962

Deposit 7,204,131 - - 7,204,131

Cash and cash equivalents 775,844 - - 775,844

Total 9,563,937 1,637,581 1,389,100 12,590,618

31 March 2009Total financial

liabilities

Liabilities as per statement of financial position RO

Trade and other payables (excluding accrued expenses) 348,781

24

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

19 Financial instruments by category (Continued)

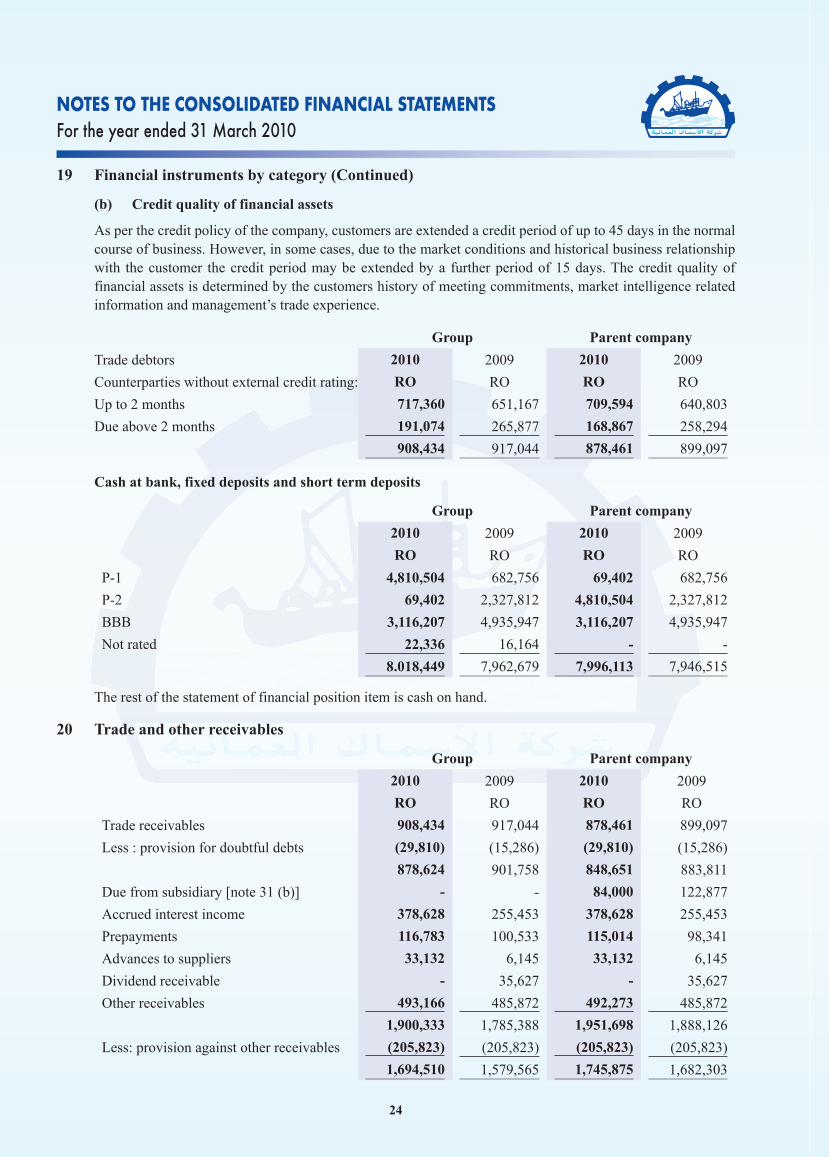

(b) Credit quality of financial assets

As per the credit policy of the company, customers are extended a credit period of up to 45 days in the normal course of business. However, in some cases, due to the market conditions and historical business relationship with the customer the credit period may be extended by a further period of 15 days. The credit quality of financial assets is determined by the customers history of meeting commitments, market intelligence related information and management’s trade experience.

Group Parent company

Trade debtors 2010 2009 2010 2009

Counterparties without external credit rating: RO RO RO RO

Up to 2 months 717,360 651,167 709,594 640,803

Due above 2 months 191,074 265,877 168,867 258,294

908,434 917,044 878,461 899,097

Cash at bank, fixed deposits and short term deposits

Group Parent company

2010 2009 2010 2009

RO RO RO RO

P-1 4,810,504 682,756 69,402 682,756

P-2 69,402 2,327,812 4,810,504 2,327,812

BBB 3,116,207 4,935,947 3,116,207 4,935,947

Not rated 22,336 16,164 - -

8.018,449 7,962,679 7,996,113 7,946,515

The rest of the statement of financial position item is cash on hand.

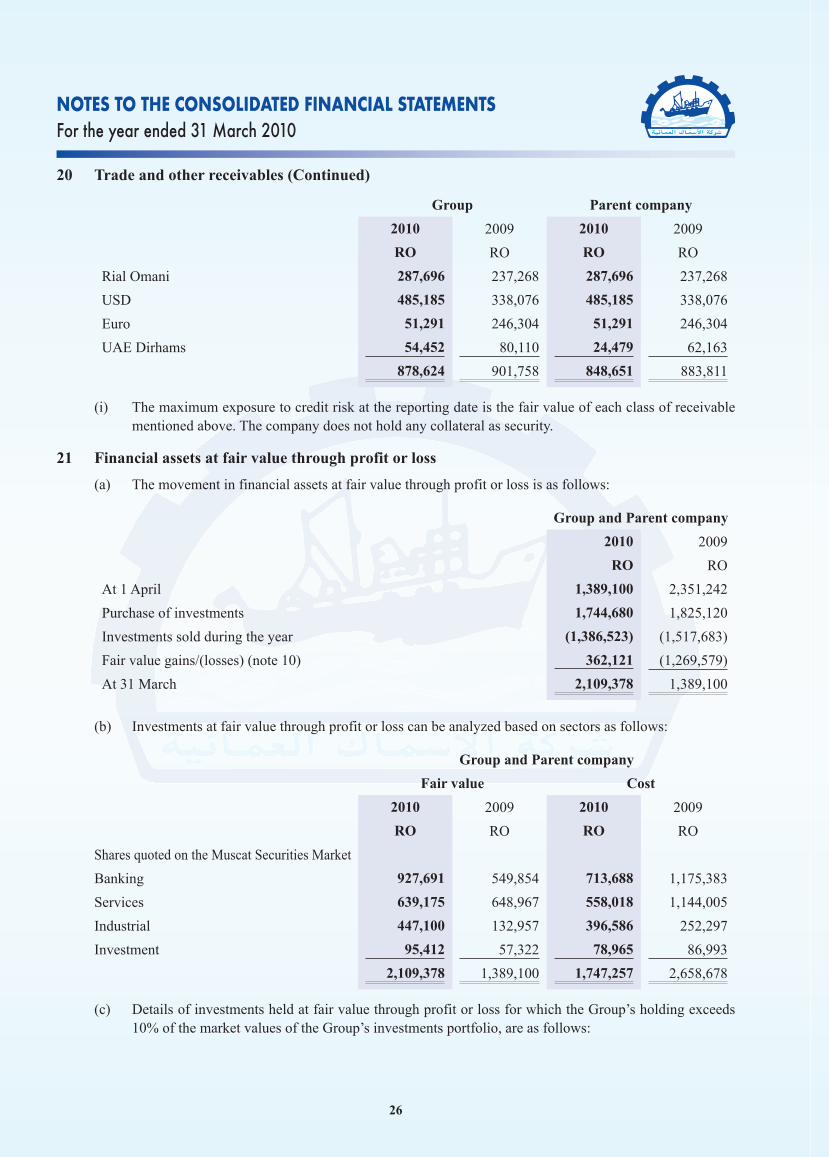

20 Trade and other receivables

Group Parent company

2010 2009 2010 2009

RO RO RO RO

Trade receivables 908,434 917,044 878,461 899,097

Less : provision for doubtful debts (29,810) (15,286) (29,810) (15,286)

878,624 901,758 848,651 883,811

Due from subsidiary [note 31 (b)] - - 84,000 122,877

Accrued interest income 378,628 255,453 378,628 255,453

Prepayments 116,783 100,533 115,014 98,341

Advances to suppliers 33,132 6,145 33,132 6,145

Dividend receivable - 35,627 - 35,627

Other receivables 493,166 485,872 492,273 485,872

1,900,333 1,785,388 1,951,698 1,888,126

Less: provision against other receivables (205,823) (205,823) (205,823) (205,823)

1,694,510 1,579,565 1,745,875 1,682,303

25

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 March 2010

20 Trade and other receivables (Continued)

(a) At the reporting date 16% of trade debtors are receivable from one party (2009 - 18% from one party) in the sultanate of Oman.

(b) The fair values of trade and other debtors are assumed to be the same as their carrying amounts above.

(c) Details of gross exposure of trade debtors are set out below:

Group Parent company

2010 2009 2010 2009

RO RO RO RO

Not due 717,360 651,167 709,594 640,803

Past due not impaired 161,264 250,591 139,057 243,008

Past due and impaired 29,810 15,286 29,810 15,286

908,434 917,044 878,461 899,097

(d) As of 31 March 2010, trade debtors of Group RO 161,264 (2009 - RO 250,591), Parent company RO 139,057 (2009 - RO 243,008) were past due but not impaired. These relate to a number of independent customers for whom there is no recent history of default. The ageing analysis of these past due trade debtors is as follows: