hl overview 2-13-13

TRANSCRIPT

Philadelphia London Hong Kong Rio de Janeiro San Francisco San Diego New York Fort Lauderdale Tel Aviv Tokyo Las Vegas Singapore

Private Equity Investment ManagementGlobal Reach - Personal Touch®

Hamilton Lane Overview

Proprietary and Confidential | Page 2

Hamilton Lane

Who We Are• Independent firm dedicated to private equity for 20+ years• 12 offices around the world• More than 190 global employees and significant employee ownership• Approximately $24 billion of discretionary assets under management1• More than $123 million committed alongside our clients since 19971

What We Offer• Separate accounts• Specialized funds• Advisory services• Full service back office support

Benefits of Working with Hamilton Lane• Global Access: Global team that sees the market• Influence: Seat at the table with GPs• Realized Performance: 1,000+ basis point outperformance versus S&P 500 PME for the 10-year composite history2

• Customized Approach: Ability to create a customized relationship• Comprehensive Offering: Complete, full service option

1 As of December 31, 20122 As illustrated in our track record on page 18

“Best Places to Work in Money Management” – Pensions & Investments, 2012

“The 2012 Inc. 5000: America’s Fastest Growing Private Companies” – Inc. 5000, 2012

“Best Places to Work in PA” – Best Companies Group, 2012

“The 100 Most Influential of the Decade” – Private Equity International, 2011

“European Gatekeeper of the Year” – Private Equity News, 2010 and 2006

“Private Equity Hall of Fame Inductee” – PEAC, 2009

“Best Places to Work” – Philadelphia Business Journal, 2007

Awards & Recognitions’

Hamilton Lane

Proprietary and Confidential | Page 3

Global Reach

* Representative clients by type. The identification of these clients does not serve as an endorsement of Hamilton Lane or the services provided.

Who We Are

Sovereign Funds/Financial Institutions

Endowments/Foundations

Public/Private Pension Funds

Taft-Hartley

Corporate Pension Funds

Amitim

Proprietary and Confidential | Page 4

Global presence is reflected in the languages we speak

Global Presence

San Francisco

San Diego

Las Vegas

Fort Lauderdale

PhiladelphiaNew York

Rio de Janeiro

London

Tel Aviv

Hong Kong

Tokyo

Singapore

Who We Are

Global presence is reflected in the languages we speak: Arabic, Cantonese, Croatian, Danish, Dutch, French, German, Gujarati, Hebrew, Hindi, Italian, Japanese, Korean, Malayalam, Mandarin, Moroccan, Norwegian, Portuguese, Punjabi, Russian, Spanish, Swedish, Ukrainian and Urdu

Proprietary and Confidential | Page 5

Hands-on Investment Committee provides perspective and insight

• All investment decisions made by Investment Committee• Members average more than 22 years of investment experience and 18 years experience in private equity• Members average more than 12 years working together as a team

Professionals with Deep Experience

Erik Hirsch | Chief Investment Officer

• Prior experience: Investment banking at Brown Brothers Harriman/ public finance at PFM

• B.A. from the University of Virginia

• Serves on several advisory boards including Apollo, Blackstone, Gores and Leonard Green

Hartley Rogers | Chairman

• Prior experience: Co-Head of CSFB Equity Partners

• M.B.A. from Harvard Business School and an A.B. from Harvard College

• Managing Director at Morgan Stanley where he was President of Princes Gate Investors family of private equity funds

Juan Delgado-Moreira | Managing Director

• Prior Experience: Investment Associate at Baring Private Equity Partners

• Chartered Financial Analyst, Fulbright Scholar at Stanford University

• Ph.D. in Research Methods/Statistics and a B.A. in Political Science and Sociology from the Universidad Complutense de Madrid, Spain

Tara A. Blackburn | Managing Director

• Prior Experience: Managing Director at Pacific Corporate Group

• She began her private equity career in 1993 and has experience in manager due diligence, portfolio development, account management, and business development

• B.A. from Colorado College

Mario Giannini | Chief Executive Officer

• Prior experience: More than 24 years in financial services industry

• J.D. from Boston College, Master of Laws degree from University of Virginia and a B.A. from California State University

• Serves on several advisory boards, including Providence, Blum and TPG

Andrea Kramer | Managing Director

• Prior Experience: General Partner at Exelon Capital Partners

• Senior Business Development Manager for Philadelphia Gas Works

• Fund Manager for Murex Corporation

• M.B.A. in Finance from Temple University, B.A. in Economics from Franklin and Marshall College.

Mike Kelly | Managing Director

• Prior Experience: Financial Analyst for InterMountain Canola Company

• Financial Analyst for DNA Plant Technology

• M.B.A. from the College of William and Mary, B.S. from Trenton State College

Paul Yett | Managing Director

• Prior Experience: Four years with StonePine Asset Management, LLC

• Lease Accountant with Bramalea U.S. Properties in Denver

• B.S. in Finance from San Diego State University

Who We Are

Proprietary and Confidential | Page 6

Hamilton Lane Offers

Customized Strategies Specialized Strategies Due Diligence / Research / Analytics Back office/services

• Broad mandate (core)

• Focused mandates (spoke)

• Examples include:

• Small/mid market buyout

• Europe

• Venture

• Asia

• Co-Investments

• Secondaries

• Funds-of-Funds

• Robust databases

• 32-year history

• More than 5,000 funds analyzed

• Proprietary systems and models

• Horizon model

• Fund rating system

• Portfolio benchmarking

• Portfolio allocation system

• SMRRT (Simulated Market Risk Return Tool)

• Market Research

• Web-based reporting

• Performance reporting

• Cash flow reconciliation

• Portfolio company data

• View, analyze and download portfolio information

• 24/7 access

Private Equity Solutions

What We Offer

What We Offer

Proprietary and Confidential | Page 7

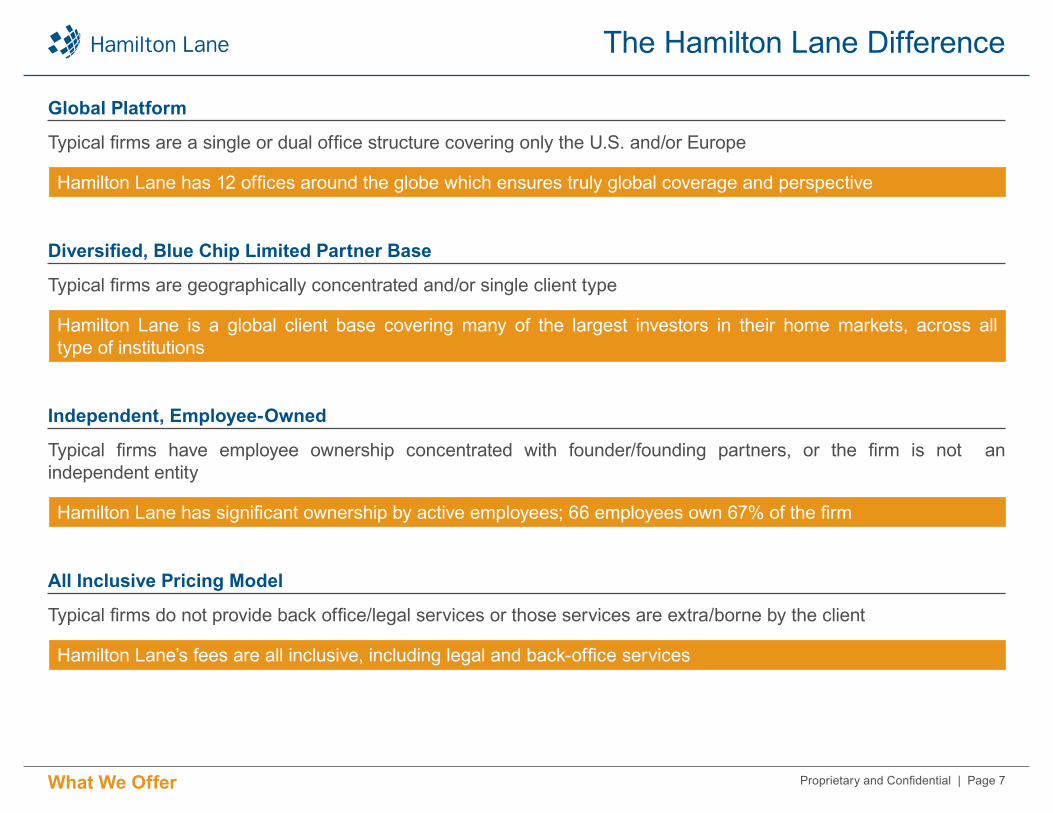

Global Platform

Typical firms are a single or dual office structure covering only the U.S. and/or Europe

Hamilton Lane has 12 offices around the globe which ensures truly global coverage and perspective

Diversified, Blue Chip Limited Partner Base

Typical firms are geographically concentrated and/or single client type

Hamilton Lane is a global client base covering many of the largest investors in their home markets, across all type of institutions

Independent, Employee-Owned

Typical firms have employee ownership concentrated with founder/founding partners, or the firm is not an independent entity

Hamilton Lane has significant ownership by active employees; 66 employees own 67% of the firm

All Inclusive Pricing Model

Typical firms do not provide back office/legal services or those services are extra/borne by the client

Hamilton Lane’s fees are all inclusive, including legal and back-office services

The Hamilton Lane Difference

What We Offer

Proprietary and Confidential | Page 8

Separate Account

Full Service Back Office Support

Specialized Products

Advisory

What We Offer

Specialized Products

Monitoring &ReportingInvestments Legal Private Equity

Strategic Planning

Hamilton Lane Private Equity Client

Example 1Europe

Small/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

Example 2Europe

Small/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

Example 3Europe

Small/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

Example 4Europe

Small/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

P R I V A T E P L A C E M E N T M E M O R A N D U M

Hamilton LaneCapital Opportunities Fund, L.P.Con�dential Book No. 001

P R I V A T E P L A C E M E N T M E M O R A N D U M

Hamilton LaneSecondary Fund IIICon�dential Book No. 001

P R I V A T E P L A C E M E N T M E M O R A N D U M

Hamilton LaneCo-Investment Fund IIICon�dential Book No. 001

P R I V A T E P L A C E M E N T M E M O R A N D U M

Hamilton LanePrivate Equity Fund VIII, L.P.Con�dential Book No. 001

What We Offer

Hamilton Lane Private Equity Fund VIII, L.P. | Hamilton Lane Co-Investment Fund III | Hamilton Lane Secondary Fund III | Hamilton Lane Capital Opportunities Fund, L.P.

Proprietary and Confidential | Page 9

Example 1

Example 2

Example 3

Example 4

Examples of Customized Strategy

What We Offer

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

EuropeSmall/Mid

AsiaSmall/Mid

Secondaries

U.S.Small/Mid

EmergingManagers

VentureCapital

Co-Investment

Core

LegalMonitoring & Reporting

Proprietary and Confidential | Page 10

Separate Account Structure

Structure: Flexible to address client’s needs (risk/return, geographic focus, strategic targets)ResponsibilitiesStrategic Plan and Guidelines: CollaborationInvestment Selection: Hamilton LaneLegal Negotiations: Hamilton LaneMonitoring and Reporting: Hamilton LaneDiscretion: Hamilton LaneClient/HL Interaction: Customized to client’s requirements

A customized separate account offers significant benefits:• Custom-tailored to meet your investment needs (risk/return profile, pacing, investment restrictions, diversification)• You control your level of involvement• Full transparency of investment decisions and ongoing monitoring• All-inclusive structure offers ease of use, as well as a cost-efficient solution• Discretion allows for Hamilton Lane to operate efficiently, creating an increased ability to access top-tier

General Partners• Interaction with General Partners• Training sessions with Hamilton Lane• Further alignment through a capital commitment by Hamilton Lane

Hamilton Lane ClientSeparate Account

What We Offer

Proprietary and Confidential | Page 11

Specialized Funds

Funds-of-Funds Secondary Funds Co-Investment Funds

• Fund-of-funds manager since 1998

• Thoughtful portfolio construction• Multi-year investment period• Exposure to all subsets of

private equity• Diversified across geography,

type, funding level and vintage year

• Focus on J-curve mitigation• Customized Taft-Hartley funds

• Secondary investor since 2000• Thoughtful portfolio construction

• Multi-year investment period• Disciplined approach to

pacing/pricing• Global Fund• Leverage our size and scale with

General Partners to generate deal flow• 490 GP meetings in 2012• Vast database of GP

information (more than 1,900 active funds)*

• GPs eager to work with us

• Co-investor since 1996• Exposure to leading GPs in their

areas of demonstrated expertise• Global Fund• Leverage our size and scale with

General Partners• Dedicated pool of capital• Attractive partner• Dedicated team

• Diversified across GPs, geography, industry and deal size

• Attractive fee structure

Raising Private Equity Fund VIIIRaising Carpenters Fund III

Raising HL Brazil FundRaising HL Real Estate Fund

Raising Secondary Fund III Investing $1.2 billion fund

* As of December 31, 2012

What We Offer

Proprietary and Confidential | Page 12

ClientLink®

• Web-based document warehouse and reporting system allows the client to view, analyze, and download up-to-date information on private equity portfolio

• Accessible 24 hours a day, seven days a week• Cash flows updated daily• Password-protected and secure platform technology• Point and click access to partnership and portfolio company information • Excel exporting capabilities

What We Offer

Proprietary and Confidential | Page 13

• Dedicated to the negotiation of private equity terms for the benefit of Hamilton Lane clients• Team of attorneys with extensive private equity experience, including paralegal support staff

• Legal team, on average, reviews and assists with negotiating more than 250 amendments and more than 60 funds annually

Legal Services

Document Review Discuss Issues With Investment Team

Negotiate Terms With GP and Counsel

Coordinate Comments With Client’s Counsel

E X E C U T I O N V E R S I O N

Amended and RestatedLimited Partnership Agreement

Sample Fund L.P.

THE LIMITED PARTNER INTERESTS (THE “INTERESTS”) OF NEW MOUNTAIN PARTNERS III, L.P. HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), THE SECURITIES LAWS OF ANY STATE OR ANY OTHER APPLICABLE SECURITIES LAWS IN RELIANCE UPON EXEMPTIONS FROM THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND SUCH LAWS. INTERESTS MUST BE ACQUIRED FOR INVESTMENT ONLY AND MAY NOT BE OFFERED FOR SALE, PLEDGED, HYPOTHECATED, SOLD, ASSIGNED OR TRANSFERRED AT ANY TIME EXCEPT IN COMPLIANCE WITH THE SECURITIES ACT, ANY APPLICABLE U.S. STATE SECURITIES LAWS AND ANY OTHER APPLICABLE SECURITIES LAWS AND THE TERMS AND CONDITIONS OF THIS AMENDED AND RESTATED LIMITED PARTNERSHIP AGREEMENT. THE INTERESTS MAY NOT BE TRANSFERRED OF RECORD EXCEPT IN COMPLIANCE WITH SUCH LAWS AND THIS AMENDED AND RESTATED LIMITED PARTNERSHIP AGREEMENT. THEREFORE, PURCHASERS OF INTERESTS WILL BE REQUIRED TO BEAR THE RISK OF THEIR INVESTMENT FOR AN INDEFINITE PERIOD OF TIME.

Benefits:

• Cost savings• Increased negotiating power• Efficiency - Aggregation coupled with experience

What We Offer

Proprietary and Confidential | Page 14

Why Private Equity and Why Now?

Benefits of working with HL: Global Access

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

1987 1990 1993 1996 1999 2002 2005 2008 2011

GD

P

Inte

rnal

Rat

e of

Ret

urn

(IRR

%)

Vintage Year

PE Performance vs. GDP

Pooled Avg GDPSource: U.S. Bureau of Economic Analysis / ThomsonOne PE Data as of 9/30/2011, Data pulled on 2/13/2012.

Why Now?

• Capital is scarce. Those who have it will be rewarded• Values and multiples continue to contract• Troubled companies need outside investors• History has shown strong private equity performance

post market downturns

Why Private Equity?

• Return Enhancement• Private Equity top quartile has historically

outperformed public indices• Portfolio Diversification• Access private companies across strategy, size,

industry and geography

Proprietary and Confidential | Page 15

The Reality of PE

• Fund access and selection are crucial to performance in this asset class

• The performance gap between top and bottom quartile returns is wider in private equity than any other asset class

• Most managers do not beat the public markets

Benefits of working with HL: Global Access

-60%-40%-20%

0%20%40%60%80%

100%120%

1995 1997 1999 2001 2003 2005 2007 2009 2011

Inte

rnal

Rat

e of

Ret

urn

(IRR

)

Vintage Year ReturnsAs of June 30, 2012

Upper Med Lower

Note: Time weighted returns using periodic IRRsSource: ThomsonOne (Venture Economics Data)

-30%

-20%

-10%

0%

10%

20%

30%

1995 1997 1999 2001 2003 2005 2007 2009 2011

Inte

rnal

Rat

e of

Ret

urn

(IRR

)

SPTR vs. U.S. Private Equity Rolling One Year AverageAs of June 30, 2012

S&P 500 Quarterly Returns PE Upper Quartile PE MedianSource: ThomsonOne (Venture Econmics Data), Bloomberg

-20% -15% -10% -5% 0% 5%

10% 15% 20% 25%

U.S. Private Equity

EuropeanPrivate Equity

U.S.Stock Funds

EuropeanStock Funds

Ten

Year

Ret

urn

Dispersion of Returns for Public vs. Private Ten Year Annualized as of June 30, 2012

Upper Median Bottom

Source: ThomsonOne (Venture Economics Data), MorningstarU.S. and European private equity returns represent 10-year annualized returns for the U.S. All Private Equity and European All Private Equity universes, as presented by Venture Economics, as of 12/31/11. Source: ThomsonReuters, run date 06/30/12U.S. and European Stock Funds Returns represent 10-year annualized returns for all U.S. Equity and European equity funds as of 12/31/11. Source: Morningstar

Proprietary and Confidential | Page 16

Seeing The Market - 2012

Site Visits by Strategy

Buyout41%

Venture Capital22%

Special Situation4%

Real Estate9%

Mezzanine3%

Distressed Debt9%

Growth Equity11%

Secondaries1%

2012 in Detail

Selection is Everything634 PPMs Screened

271 GP Meetings Taken*

74 Manager Site Visits

Site Visits by Region

North America53%

Europe22%

Global10%

Asia Pacific11%

Middle East3%

South America2%

Site Visits by Fund Sizes

$0-$100M4%

$100-$500M32%

$500-$2B35%

$2-$5B20%

> $5B8%

* Includes only new fund presentations and does not include fund update meetings, which totaled 185 in 2011.

Consistency: Every PPM is captured, screened and reviewed

PPMs are not enough. To know the market, you must meet the market.

Meet the full team in its offices.

• More than: • $6.9B of capital allocated in 2012**• $1.3B to U.S. Small/Mid market funds• $1B to Credit funds• $568M to Europe funds• $382M to Venture/Growth funds

• Cumulative “cutbacks” equaled $143M (2.1% of total allocated dollars)

Benefits of working with HL: Global Access

* Includes only new fund presentations and does not include fund update meetings, which totaled 220 in 2012.** The 2012 capital allocated includes all commitments for which Hamilton Lane retains a level of discretion for the investment decisions and Advisory client commitments to Hamilton Lane broadly recommended funds. This amount excludes commitments made by Hamilton Lane’s secondary and co-investment commingled funds.

Proprietary and Confidential | Page 17

A Seat At The Table

Advisory seats are afforded due to our size and market presence(More than 130 seats)

Sample, not whole list. As of 1/17/13( ) Multiple of funds with same General Partners* Khosla’s seat is on the conflict committee

• 3i Europartners

• Advent (3)

• American Securities Partners (5)

• Apollo (6)

• Blackstone Capital Partners (5)

• Bridgepoint Europe (2)

• Carlyle Group

• Charterhouse Capital Partners (3)

• Clessidra Capital Partners

• CVC European Equity Partners (3)

• Energy Capital Partners

• Enhanced Equity (2)

• Ethos

• Falcon Partners (3)

• FIMI (2)

• First Reserve (2)

• Gilde Buy Out Partners

• Giza Venture Fund

• Gores Capital Partners (4)

• Green Equity Investors (2)

• H2 Equity Partners

• High Road Capital Partners

• ICG (2)

• J.H. Whitney (2)

• JVP Media V

• KKR

• Kohlberg Investors (4)

• KPS Special Situations (3)

• Linden Capital Partners

• Lindsay Goldberg & Bessemer (3)

• Merit Capital Partners

• Montreux Equity Partners

• NG Capital Partners

• Oak Investment Partners (3)

• Odyssey Investment Partners

• OHA Strategic Credit Fund

• Pátria Investimentos

• Platinum Equity Capital Partners (3)

• Providence Equity Partners (4)

• Quad-C Partners

• Roark Capital Partners (3)

• SAIF Partners

• Saw Mill Capital Partners

• Spark Capital

• Thomas H. Lee Company (2)

• TPG Partners (7)

• Veritas Capital

• Westbury Investment Partners

Benefits of working with HL: Global Access

Proprietary and Confidential | Page 18

Discretionary Track Record

Benefits of working with HL: Global Access

Please refer to endnotes in the the Appendix

Hamilton Lane Discretionary Track Record1

As of September 30, 2012

Vintage Year PerformanceVintage Year6 Hamilton Lane IRR2 Spread vs. S&P 500 PME (bps)5 Spread vs. MSCI World PME (bps)5

1997-2001 10.76% 752 bps 575 bps2002 21.49% 1,382 bps 1,127 bps2003 20.57% 1,622 bps 1,547 bps2004 14.71% 1,166 bps 1,157 bps2005 9.44% 643 bps 761 bps2006 3.93% 26 bps 248 bps2007 8.36% 143 bps 408 bps2008 12.11% 135 bps 515 bps2009 16.13% 104 bps 602 bps2010 9.84% -550 bps 3 bps2011 9.92% -689 bps -133 bps

Composite Performance5-Year 7-Year 10-Year

Hamilton Lane Realized IRR3 7.88% 16.90% 20.13%Spread vs. S&P 500 PME (bps)5 755 bps 1,179 bps 1,064 bpsSpread vs. MSCI World PME (bps)5 947 bps 1,176 bps 876 bps

Hamilton Lane Total IRR4 7.87% 10.52% 12.63%Spread vs. S&P 500 PME (bps)5 204 bps 325 bps 383 bpsSpread vs. MSCI World PME (bps)5 502 bps 547 bps 524 bps

Proprietary and Confidential | Page 19

Our Strengths

Consistent Results

• Significant history of outperformance1

Leading Asset Manager

• Global presence with both offices and clients• Private firm with more than 190 employees dedicated to private equity• Service provider for many of the most sophisticated investors around the world• Approximately $24 billion of discretionary assets under management2

Global Investment Team

• Deep, senior team• Hands-on Investment Committee provides perspective and insight• Market presence and tenure enables access to “top-tier” funds

Intelligent Portfolio Design

• Carefully planned allocations tailored to market opportunities• Highly selective investing approach• Use of managers as building blocks

1 As illustrated in our track record on the previous page2 As of December 31, 2012

Benefits of working with HL: Global Access

Appendix

Proprietary and Confidential | Page 22

Biographies

Investment Committee

Hartley RogersChairman

As Chairman, Hartley focuses on the firm’s investment activities, client relationships, and strategic initiatives. He is the Co- Head of Hamilton Lane’s co-investment businesses and participates on the firm’s Investment Committees. He joined Hamilton Lane in 2003 and was formerly a Managing Director in the Private Equity Division and Co-Head of the U.S. and Canadian Private Equity Department of Credit Suisse First Boston. He continues to serve as Co- Head of CSFB Equity Partners, a $2.74 billion private equity fund, which is nearing the end of its term, and served as a senior partner and Investment Committee member of DLJ Merchant Banking Partners Ill, a $5.3 billion private equity fund. Prior to joining CSFB in 1997, Hartley was a Managing Director of Morgan Stanley & Co. where he was president of the general partners of the Princes Gate Investors family of private equity funds.

Hartley received an M.B.A. from Harvard Business School, where he was designated a Baker Scholar, and an A.B. from Harvard College.

Mario GianniniCEO

Mario is the Chief Executive Officer of Hamilton Lane and sits on the firm’s Investment Committee. He is responsible for the firm’s strategic direction and oversees the development of the firm’s management structure and process. Mario also plays a significant role in providing client services to the firm’s numerous clients and in marketing the firm’s products and services. In addition, Mario serves on several advisory boards on behalf of Hamilton Lane and its clients, including Thomas H. Lee, TPG Partners and Providence Equity Partners.

Mario received a J.D. from Boston College, a Master of Laws degree from the University of Virginia, and a B.A. from California State University. He is a member of the state bars of California and Illinois.

Erik HirschCIO

Erik is the Chief Investment Officer of Hamilton Lane. At Hamilton Lane, Erik is responsible for managing all of the firm’s investment and research activities, as well as chairing the firm’s Investment Committee.

Erik is a frequently quoted expert on the private equity industry, both in the print and broadcast media. He also serves on the advisory boards of several leading fund managers on behalf of Hamilton Lane and its clients.

Further, Erik serves on the board of iLevel Solutions, Inc., representing Hamilton Lane’s strategic interest in the company.

Prior to joining Hamilton Lane, Erik was a corporate investment banker in the Mergers & Acquisitions department of Brown Brothers Harriman & Co. He began his career as a municipal financial consultant with Public Financial Management (PFM). At PFM, Erik specialized in asset securitization, strategic consulting and sport stadium financings.

Erik currently serves on the board of Philadelphia’s Mural Arts Program.

Erik has a B.A. from the University of Virginia.

Andrea KramerManaging Director

Andrea is a Managing Director at Hamilton Lane where she is responsible for the oversight and management of the firm’s global Fund Investment Group. Andrea is a member of the Investment Committee and also serves on a number of fund advisory boards.

Prior to joining Hamilton Lane in 2005, Andrea worked as a General Partner at Exelon Capital Partners where she managed investments in the energy technology and enterprise application areas; as a Senior Business Development Manager for Philadelphia Gas Works; and as a Fund Manager for Murex Corporation.

Andrea received an M.B.A. in Finance from Temple University and a B.A. in Economics from Franklin and Marshall College.

Proprietary and Confidential | Page 23

Biographies

Investment Committee

Juan Delgado-MoreiraManaging Director

Juan is a Managing Director and Head of International at Hamilton Lane, based in the firm’s Hong Kong office, where he oversees the firm’s Asian and European investment activities and client relationships.

Prior to joining Hamilton Lane in 2005, Juan was an Investment Manager at Baring Private Equity Partners Ltd. in London, where he focused on mid-market private equity in Europe. Previously, Juan held senior research positions at UK institutions such as the University of Essex and was a lecturer and Fulbright Scholar at Stanford University. Juan began his career as an analyst in Madrid at the SEPI (formerly known as lnstituto Nacional de Industria).

Juan received a Ph.D. in Research Methods/statistics and a B.A. in Political Science and Sociology from the Universidad Complutense de Madrid, Spain. He is a Chartered Financial Analyst, a member of the CFA Institute and the Securities Institute.

Tara BlackburnManaging Director

Tara is a Managing Director at Hamilton Lane, based in the firm’s San Diego office, where she is involved in both the firm’s investment activities and client relationships. She began her private equity career in 1993 and has experience in manager due diligence, portfolio development, account management, and business development. Tara is a member of Hamilton Lane’s Investment Committee and manages a number of the firm’s client relationships.

Prior to joining Hamilton Lane in 2007, Tara was a Managing Director at Pacific Corporate Group where she headed the firm’s global Portfolio Management activities, was an active member of the investment committee, and served on various fund advisory boards on behalf of PCG and its clients. Prior to joining PCG, Tara worked with the media research firm Paul Kagan Associates covering the cable and cellular markets, including the firm’s expansion into Latin America. Tara began her career with Arthur Andersen, where she worked with the litigation consulting division.

Tara received a B.A. from Colorado College.

Mike KellyManaging Director

Mike is a Managing Director at Hamilton Lane where he is responsible for due diligence of primary fund investment opportunities. Mike began his career at Hamilton Lane in 1994 and previously was responsible for managing the client relationship and reporting activities of the firm, as well as the analysis of venture investment opportunities. Mike is a member of Hamilton Lane’s Investment Committee and also serves on a number of fund advisory boards.

Prior to joining Hamilton Lane in 1994, Mike was a Financial Analyst for InterMountain Canola Company and a Financial Analyst for DNA Plant Technology.

Mike received an M.B.A. from the College of William and Mary and a B.S. from Trenton State College.

Paul YettManaging Director

Paul is a Managing Director at Hamilton Lane, based in the firm’s San Francisco office, where he is involved in both the firm’s investment activities and client relationships. Paul began his career with Hamilton Lane in 1998 in the Due Diligence Department, where he managed the firm’s global venture capital practice and real estate. Paul is a member of Hamilton Lane’s Investment Committee and manages a number of the firm’s client relationships.

Prior to joining Hamilton Lane, Paul spent four years with Stone Pine Asset Management, LLC, a Denver-based private equity firm, where he was part of a team that managed a direct private equity mezzanine fund under the parent company, FCM Fiduciary Capital Management Company. Paul began his career in Denver as a Lease Accountant with Bramalea U.S. Properties where he covered several of the firm’s U.S. commercial retail properties.

Paul received a B.S. in Finance from San Diego State University.

Proprietary and Confidential | Page 24

Hamilton Lane Organization

Hartley Rogers & Erik Hirsch

Co-Investment Team

Thomas KerrSecondary Team

Andrea KramerFund Investment Team

Jerome GatesReal Estate

Michael RyanResearch

Jeffrey MeekerProduct Management

Alice LindenauerHuman Resources

Napoleon StephensonBusiness Development

Kevin LuceyRelationship Management

Frederick ShawCompliance

Olin HonoreIT

Michael DonohueCorporate Finance

Matthew BarbatoFinancial Reporting

Randy StilmanCFO

Robert ClevelandGeneral Counsel

Legal

Kevin LuceyCOO

Juan Delgado-MoreiraManaging Director

Erik HirschCIO

Mario GianniniCEO

Hartley RogersChairman

Mario Giannini, CEO | Erik Hirsch, CIO | Hartley Rogers, Chairman | Paul Yett, Managing Director | Tara Blackburn, Managing Director | Michael Kelly, Managing Director | Juan Delgado-Moreira, Managing Director | Andrea Kramer, Managing Director

Investment Committee

Proprietary and Confidential | Page 25

Endnotes

Page 181 The Discretionary Track Record includes all commingled funds-of-funds and separate accounts managed by Hamilton Lane for which Hamilton Lane retains a level of discretion for the investment

decisions, as of September 30, 2012. The results herein include all secondary fund investments (except as noted below), as well as primary fund investments where a commingled fund-of-funds or multiple accounts participated in an investment. This presentation does not include co-investments or investments made on behalf of two accounts which Hamilton Lane no longer manages. As of September 30, 2012 this presentation represents commitments of $20.7 billion; in total Hamilton Lane had $25.2 billion in commitments for all discretionary accounts, of which $2.0 billion represents co-investments.

2 Hamilton Lane IRR represents the pooled IRR for all Discretionary Track Record investments within the relevant vintage year for the period from inception to September 30, 2012. The returns are net of management fees, carried interest and expenses charged by the underlying fund managers, but do not include Hamilton Lane management fees, carried interest or expenses. The Hamilton Lane IRR would decrease with the inclusion of these fees, carried interest and expenses. Hamilton Lane has calculated and presented these returns on a pooled basis using daily cash flows. Performance results for the most recent vintage years are considered less meaningful due to the short measurement period, the incurrence of fees and expenses and the absence of significant distributions.

3 Hamilton Lane Realized IRR represents the pooled IRR for those Discretionary Track Record investments that Hamilton Lane considers realized for purposes of its Discretionary Track Record, which are investments where the underlying investment fund or direct investment has been fully liquidated, has generated a DPI greater than or equal to 1.0 or has an RVPI less than or equal to 0.2 and is older than 6 years. DPI represents total distributions divided by total invested capital. RVPI represents the remaining market value divided by total invested capital. These realized investments represent $3.2 billion of the $20.7 billion of total commitments included in the overall Discretionary Track Record. The Hamilton Lane Realized IRR is measured for the 5-, 7- and 10-year periods ending September 30, 2012. The returns are net of management fees, carried interest and expenses charged by the underlying fund managers, but do not include Hamilton Lane management fees, carried interest or expenses. The Hamilton Lane Realized IRR would decrease with the inclusion of these fees, carried interest and expenses. Hamilton Lane has calculated and presented these returns on a pooled basis using daily cash flows, where vintage years with larger amounts committed to investment have a proportionately larger impact on returns.

4 The Hamilton Lane Total IRR represents the pooled IRR for all Discretionary Track Record investments and is measured for the 5-, 7- and 10-year periods ending September 30, 2012. These returns are net of management fees, carried interest and expenses charged by the underlying fund managers, but do not include Hamilton Lane management fees, carried interest or expenses. The Hamilton Lane Total IRR would decrease with the inclusion of these fees, carried interest and expenses. Hamilton Lane has calculated and presented these returns on a pooled basis using daily cash flows, where vintage years with larger amounts committed to investment have a proportionately larger impact on returns.

5 The indices presented for comparison are the S&P 500 and the MSCI World, calculated on a Public Market Equivalent (PME) basis. The PME calculation methodology assumes that capital is being invested in, or withdrawn from, the index on the days the capital was called and distributed from the underlying fund managers. Contributions were scaled by a factor such that the ending portfolio balance would be equal to the private equity net asset value. The scaling factor is found by taking the sum of all shares sold (SS), the sum of all shares purchased (SP) and calculating the number of shares the ending value is worth (SEV). Dividing SEV + SS by SP solves for the PME scaling factor. The scaling of contributions prevents shorting of the public market equivalent portfolio in order to match the performance of an outperforming private equity portfolio. Realized and unrealized amounts were not scaled by this factor. The S&P 500 Total Return Index is a capitalization weighted index that measures the performance of 500 U.S. large cap stocks. The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The indices are presented merely to show general trends in the markets for the relevant periods shown. The comparison between Hamilton Lane performance and the index is not intended to imply that a fund’s or separate account’s portfolio is benchmarked to the index either in composition or level of risk. The index is unmanaged, has no expenses and reflects the reinvestment of dividends and distributions. The spreads are provided for comparative purposes only. A variety of factors may cause an index to be an inaccurate benchmark for any particular fund or separate account and the indices do not necessarily reflect the actual investment strategy of a fund or separate account.

6 The Hamilton Lane IRR for the 2012 Vintage Year, calculated on a non-annualized basis in a manner consistent with the CFA Institute’s standards for private equity performance reporting, as well as on a pooled basis using daily cash flows, is 26.08%. Hamilton Lane does not consider this performance metric meaningful due to the very short measurement period.

Past performance of the investments presented herein is not indicative of future results and should not be used as the basis for an investment decision. The information included has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot be guaranteed.

Proprietary and Confidential | Page 26

Disclosures

As of February 13, 2013

This presentation has been prepared solely for informational purposes and contains confidential and proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this presentation are requested to maintain the confidentiality of the information contained herein. This presentation may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

The information contained in this presentation may include forward-looking statements regarding returns, performance, opinions, the fund presented or its portfolio companies, or other events contained herein. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control, or the control of the fund or the portfolio companies, which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts of future performance or other events contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. Past performance of the investments described herein is not indicative of future results. In addition, nothing contained herein shall be deemed to be a prediction of future performance. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The results shown herein are compared to the performance of the S&P 500 and MSCI World since institutional investors often use such indices for comparative purposes for private equity portfolio performance.

The investment volatility of the S&P 500 and MSCI World may differ from the funds or strategies reflected.

Certain of the performance results included herein do not reflect the deduction of any applicable advisory or management fees, since it is not possible to allocate such fees accurately in a vintage year presentation or in a composite measured at different points in time. A client’s rate of return will be reduced by any applicable advisory or management fees, carried interest and any expenses incurred. Hamilton Lane’s fees are described in Part 2 of our Form ADV, a copy of which is available upon request.

The following hypothetical example illustrates the effect of fees on earned returns for both separate accounts and fund of funds investment vehicles. The example is solely for illustration purposes and is not intended as a guarantee or prediction of the actual returns that would be earned by similar investment vehicles having comparable features. The example is as follows: The hypothetical separate account or fund of funds consisted of $100 million in commitments with a fee structure of 1.0% on committed capital during the first four years of the term of the investment and then declining by 10% per year thereafter for the 12-year life of the account. The commitments were made during the first three years in relatively equal increments and the assumption of returns was based on cash flow assumptions derived from a historical database of actual private equity cash flows. Hamilton Lane modeled the impact of fees on four different return streams over a 12-year time period. In these examples, the effect of the fees reduced returns by approximately 2%. This does not include performance fees, since the performance of the account would determine the effect such fees would have on returns. Expenses also vary based on the particular investment vehicle and, therefore, were not included in this hypothetical example. Both performance fees and expenses would further decrease the return.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Services Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FSA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Any tables, graphs or charts relating to past performance included in this presentation are intended only to illustrate the performance of the indices, composites, specific accounts or funds referred to for the historical periods shown. Such tables, graphs and charts are not intended to predict future performance and should not be used as the basis for an investment decision.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein..