health care reform 101 - black, gould

TRANSCRIPT

Health Care Reform 101

U P D A T E D N O V E M B E R 2 0 1 4

U P D A T E D N O V E M B E R 2 0 1 4

P A G E 2

This guide will review:

Overview The Affordable Care Act (ACA) includes several provisions to extend

greater access to health insurance benefits to more people. Beginning in

2014, most Americans must purchase a minimum amount of health insur-

ance or be taxed by the government.

While there is a lot to be done when ACA is fully implemented, this useful

guide provides important information to help you understand the imple-

mentation of the ACA in Arizona.

The ways to purchase health insurance in Arizona have expanded

Changes to health plan benefits Essential health benefits Actuarial value Rating

What Individual consumers need to know Health insurance options for individuals and families Options outside open enrollment; plan renewals Cost sharing potential and premium tax credits Income requirements for federal tax credits and cost-

sharing reductions Penalties for uninsured individuals

What Businesses need to know Health Insurance options for small group employers Health Insurance options for large group employers Taxes and fees for businesses

H E A L T H C A R E R E F O R M 1 0 1

The ways to purchase health insurance in Arizona have expanded

P A G E 3

The ACA requires each state to operate a Health Insurance Marketplace, also known as an Exchange, where people can purchase

coverage. The health insurance marketplace is an online site where consumers can compare plans of participating insurers and pur-

chase health insurance. The U.S Department of Health and Human Services (HHS) runs the marketplace in states that choose not to

create one, such as the case in Arizona. The Marketplace in Arizona is known as the Federally Facilitated Marketplace (FFM) for

individuals and families, and the Small business Health Plan Federally Facilitated Marketplace (SHOP-FFM) for small group

(small group is defined as 2-50 employees).

The Open Enrollment Period (OEP) for the 2015 plan year is November 15, 2014 to February 15, 2015.

Options Outside of Open Enrollment

When Enrollment Selection is Received Date Health Insurance Coverage Begins

Enrollments received between Nov 15, 2014 and Dec 15, 2014 January 1, 2015

December 16, 2014 to January 15, 2015 February 1, 2015

January 16, 2015 to February 15, 2015 March 1, 2015

Outside of Open Enrollment, you can buy a health insurance plan or change from one plan to another only if you qualify for a Special Enrollment Period. This is true for plans available both on the Marketplace and off the Marketplace. For most qualify-ing events the Special Enrollment Period lasts 60 days from the date of the qualifying event. The following is a list of the most common qualifying events. Please see www.healthcare.gov for a complete list of qualifying events including Special Enrollment Periods for complex issues.

Loss of eligibility for other coverage (for example, if you quit your job, were laid off, if your hours were reduced, if you lose student health coverage when you graduate). Note that loss of eligibility for other coverage because you didn't pay premiums, voluntarily ended coverage, or lost coverage that is not minimum essential coverage does not trigger a SEP

Gaining a dependent (for example, if you get married or give birth to or adopt a child). Note that pregnancy does NOT trigger a SEP

Divorce or legal separation

Loss of dependent status (for example, "aging off" a parents' plan when you turn 26)

Moving to another state, or within a state if you move outside of your health plan service area

Exhaustion of COBRA coverage

Losing eligibility for Medicaid, or the Children's Health Insurance Program

For people enrolled in a Marketplace plan, income increases or decreases enough to change your eligibility for subsidies

Change in immigration status

Enrollment or eligibility error made by the Marketplace or another government agency, or somebody such as an assist-er, acting on their behalf.

P A G E 4

Individual Health plan Renewals - Marketplace

All 2014 Marketplace health plans will come up for renewal January 1, 2015. Your insurance company will send you information this fall about updated premiums and benefits. Review your plan’s 2015 changes to see if the plan still meets your needs. Call your broker or visit the plan’s web-site to make sure your doctor and other health care provid-ers will be in the plan network next year. Also make sure any prescriptions you take will be covered. If you’re happy with your renewal changes and you want to keep your plan, and your income or household size haven’t changed, you don’t need to do anything. However, your insurance will auto-enroll you in the same plan for 2015. If your income or household size have changed, you’ll need to report that to the Marketplace so you get the right premium tax credit. If you don’t update this information, you’ll get the same premium tax credit you got in 2014. If your income has gone up or your household size changes and you don’t report these changes to the Marketplace, you may owe money at the end of 2015 when you file your tax return. If you want to change plans you can:

Choose any other Marketplace health plan your company offers in your service area if you want to stay with your current insurance company.

Choose a new health plan from a different insurance company through the Marketplace.

Buy a new private health plan outside of the Marketplace. If you do this, you won’t be eligible for premium tax credits and cost-sharing reductions offered through the Marketplace.

In some cases, your current Marketplace plan won’t be offered in 2015. If that’s the case, the Marketplace will automatically enroll you in a similar plan so you don’t have a gap in coverage, unless you choose another plan and enroll. Because your plan is ending, you’ll qualify for a Special Enrollment Period that lets you enroll in an individual plan outside of Open Enrollment.

Individual Health plan Renewals - Outside the Marketplace

All plans purchased outside the Marketplace with an effective date in 2014 will renew January 1, 2015. Grandfathered plans and Grandmothered plans (non-ACA, non-grandfathered) may renew at different times during the year. Your insurance company will send you information this fall about updated premiums and benefits. If you’re happy with your renewal changes and the plan still fits your needs, in most cases, you don’t need to do anything. However, your insurance company will notify you if any action needs to be taken. Be sure to contact your broker with any questions. In some cases your plan may no longer be offered in 2015. If that is the case your insurance company will notify you regard-ing the change and may automatically move you to another plan or require you to select a new plan to continue coverage.

P A G E 5

INDIVIDUALS 1. Direct purchase through a broker or insurance pro-

vider.

2. Those who are eligible and wish to obtain a federal subsidy or premium tax credit may purchase health insurance in the FFM.

3. Those who do not qualify for a federal subsidy or premium tax credit, still have the option to pur-chase health insurance in the FFM.

BUSINESSES 1. Direct purchase through a broker or insurance pro-

vider.

2. Employers may use a broker to access the Small business Health Options Program (SHOP-FFM) to purchase a health plan online, or shop direct for plans.

3. Direct purchase through a private marketplace option.

Individuals and businesses now have more ways to purchase health insurance.

The FFM/SHOP-FFM will not replace private health insurance; it is

simply a new place for qualified individuals and employers to shop for

and purchase health insurance.

Brokers and navigators* will work with individuals and small group

employers looking for coverage on the FFM/SHOP-FFM. The FFM/

SHOP-FFM will allow brokers and navigators to help people enroll in

Qualified Health Plans (QHPs), or help them with their application for

premium tax credits and cost sharing reductions. As more guidance is

shared about these roles, more information will be provided.

* A navigator cannot receive compensation from any health plan in

connection with enrolling someone in a plan offered through the FFM/

SHOP-FFM.

Special Enrollment Period for small Employers (2-50)

November 15 – December 15 is a Special Enrollment Period for small employers (2–50) who don’t meet participation or contribution requirements. This little known part of the Affordable Care Act requires health insurance companies to offer an annual one month Special Enrollment Period (From 11/15 to 12/15 for January effective dates.) This means employers do not have to meet the normal 75% participation requirement, or 50% premium contribution rule. So if you have 30 employees and only 2 want it, that’s okay. It doesn’t matter. And the contribution amount, well, you set it up how you want to, but it can be way lower than 50%, and it does need to be the same for each employee.

Changes to health plan benefits In order to sell on the FFM/SHOP-FFM, carriers must offer Qualified Health Plans (QHPs) in the individual

and small group markets. This means plans must be certified by the FFM/SHOP-FFM and meet a number of

coverage and other requirements, including a specific set of services and items called Essential Health Benefits

(EHB).

Additionally, the ACA requires QHPs offered off the FFM/SHOP-FFM to offer standardized benefit packages

in the individual and small group markets.

These packages represent four levels of value which make it easier to compare options. (See page 7 for levels.)

ACA requirements for QHPs on the FFM/SHOP-FFM.

“Essential Health Benefits” are key components of coverage

Whatever the level of coverage, each of the benefit plans has to include “Essential Health Benefits.” According to the

ACA, an essential health benefits package must include services and items in these 10 broad categories of care:

1. Ambulatory patient services

2. Emergency services

3. Hospitalization

4. Maternity and newborn care

5. Mental Health and substance use disorder services, including behavioral health treatment

6. Prescription drugs

7. Rehabilitative and habilitative services and devices

8. Laboratory services

9. Preventive and wellness services and chronic disease management

10. Pediatric services including oral and vision care

(Insurance policies must cover these benefits in order to be certified and offered in the FFM/SHOP-FFM, and all Medicaid state plans must cover these ser-

vices by 2014. For more information visit: healthcare.gov)

Rather than establish premiums based on health status, rates for these individual and small group plans will be based on variables that include: Family status Age Geographic area Tobacco use (1.5%) In addition, the federal healthcare law requires QHPs to use 3-to-1 age-rating bands. As a result, the highest premium cannot be more than three times the lowest premium for the same plan.

Beginning January I, 2014, the small group and individual insurance market will offer QHPs. Under the ACA, all ACA-qualified plans must follow new coverage and benefit rules with requirements based on: Whether the plan is offered in or outside the FFM/

SHOP-FFM Whether the plan is fully insured or self-insured Group size Not only does the ACA mandate that nearly all Americans must purchase health care, the law also requires health insurance to be “Guaranteed Issue.” This means a person (or family) can’t be denied coverage or charged more be-cause of a pre-existing health condition.

P A G E 6

P A G E 7 Sometimes referred to as “metal plans,” or “metallic plans” the different tiers are

defined by the percentage each plan will pay toward healthcare expenses for an

average person (known as the actuarial value.) Here’s how the metal or metallic

levels break down:

Standard benefits package - 5 Levels of Coverage

Bronze

Silver

Gold

Platinum

Plans provide 60% coverage

Plans provide 70% coverage

Plans provide 80% coverage

Plans provide 90% coverage

Example:

As an example, a Bronze plan will generally

have the lowest monthly premium and pay

60% of healthcare services; enrollees are

responsible to pay 40% for healthcare ser-

vices through some combination of cost

shares. Although cost shares will be just

10% for Platinum plans, this level will also

have the highest monthly premium.

Mixing the metals Health Insurers offering QHPs must offer at least one plan at the Silver level,

and one plan at the Gold level on and off the FFM/SHOP-FFM. Although

not a requirement, they also have the option to offer a choice of Bronze, Plat-

inum or Catastrophic plans. Under each metal level there can be several

plans available, which will vary according to the deductibles, coinsurance

and copays offered.

At-a-Glance Coverage & Essential Health Benefits

Note: The healthcare re-form law does not re-quire carriers to offer plans with at least a 60% actuarial value, nor does it require employers to provide health coverage. However, it imposes pen-alties on employers with 50+ FTEs that do not pro-vide minimum coverage if an employee purchases coverage on the SHOP-FFM and received a pre-mium tax credit or cost sharing reduction.

Inside FFM/SHOP-

FFM

Outside FFM/SHOP-

FFM - Fully insured

small group and

individual

Outside FFM/SHOP-

FFM - Fully insured

large group and self-

insured

Include essential health benefits

Provide 60% actuarial value min-

imum

Adhere to deductible and

out-of-pocket maximum limits

Comply with “metal levels”

benefits (actuarial values-60, 70,

80, 90 percent)

Be certified by the marketplace

through which the plan is offered

Out-of-pocket maximum

requirements

Catastrophic Plans

Catastrophic plans provide affordable cov-

erage options for young adults and people

for who coverage would otherwise be unaf-

fordable. These plans have higher deducti-

bles than the Bronze, Silver, Gold or Plati-

num plans. The benefits of a Catastrophic

plan is that the premiums will be lower

than the metallic plans. They offer protec-

tion against out-of-pocket costs above the

$6,600 for an individual, and $13,200 for a

family. Preventive services (as long as

recommended) will be covered without

cost sharing. The eligibility for Cata-

strophic plans is limited to: individuals

under the age of 30, OR individuals who

otherwise do not have an affordable cover-

age option, or who otherwise qualify for a

hardship exemption to the minimum essen-

tial coverage rule.

P A G E 7

P A G E 8

What individual consumers need to know

Health Insurance options for Individuals and families Consumers purchasing insurance in the individual market will be guaranteed coverage for pre-

existing conditions and their premiums cannot vary based on their gender or medical history. Here

are some options, benefits and criteria for individuals and families purchasing health insurance in

2014.

Keep their grandfathered plan

Buy a plan through either:

The FFM using a broker

Direct through broker or an

insurer outside of the FFM.

Go uninsured and pay a

penalty, unless exempt

The online marketplace allows consumers to: Shop for and compare a variety of private health plans

Get answers to questions about health coverage options

Find out if they’re eligible for health programs like Medicaid and the Children’s Health Insurance

Program (CHIP)

Receive premium tax credits

Cost-sharing reductions

Enroll in a health plan that meets their needs

Premium Assistance People who purchase coverage in the FFM may be eligible for a premium tax credit as long as their

household income is between 100%- 400% of federal poverty guidelines. Those below 100% of federal

poverty level will be directed to apply through their state Medicaid program. Figures based on January

2014 federal poverty guidelines:

For an individual, that equals $11,670 to $46,680

For a family of four, that equals $23,850 to $95,400

The assistance amount that a person can receive varies with income. The tax credit may be applied to

Bronze, Silver, Gold, or Platinum. Tax credits cannot be applied to catastrophic plans.

Cost Sharing reductions and premium tax credits for individuals To address the needs of those who fall in certain income levels and cannot afford minimum essential

health benefits, the law includes provisions for federal subsidies to reduce the cost of premiums, with a

cost-sharing reduction.

OR OR

P A G E 9

Income requirements for cost-sharing reductions Those who earn up to 250% of federal poverty guidelines and enroll at the Silver level only may also be eli-

gible for reduced cost sharing. Again, the subsidy amount will vary according to income. Examples of cost

sharing that may be reduced include deductibles, co-insurance, co-payments or similar charges and do not

include balance billing for non-network providers or spending on non-covered services.

Penalties for uninsured individuals In 2015, legal U.S. citizens who do not carry a minimum amount of health coverage will receive a penalty of

$325 or 2% of their taxable income, whichever is greater. Penalties will increase each year through 2016;

and annually thereafter.

Penalty Timeline

2014 Greater of $95 or 1%

of taxable income

2015 Greater of $325 or 2%

of taxable income

2016 Greater of $695 or

2.5% of taxable income

2017 And beyond, annual

adjustments

Who is subject to a penalty under the Individual Mandate?

Part of a religious group with an exception

Incarcerated Undocumented resident American Indian Pay more than 8% of take-home

pay for employer coverage Such low-income, you don’t pay

federal income taxes Someone who falls into a Medi-

caid expansion coverage hole Some other hardship exemption

Coverage through a job Coverage through an ex-

change Medicaid, Medicare,

CHIP Tricare or VA Care Student Health Plan Grandfathered plan

No Penalty

Penalty OR

YES

NO

CRITERIA: DO YOU HAVE:

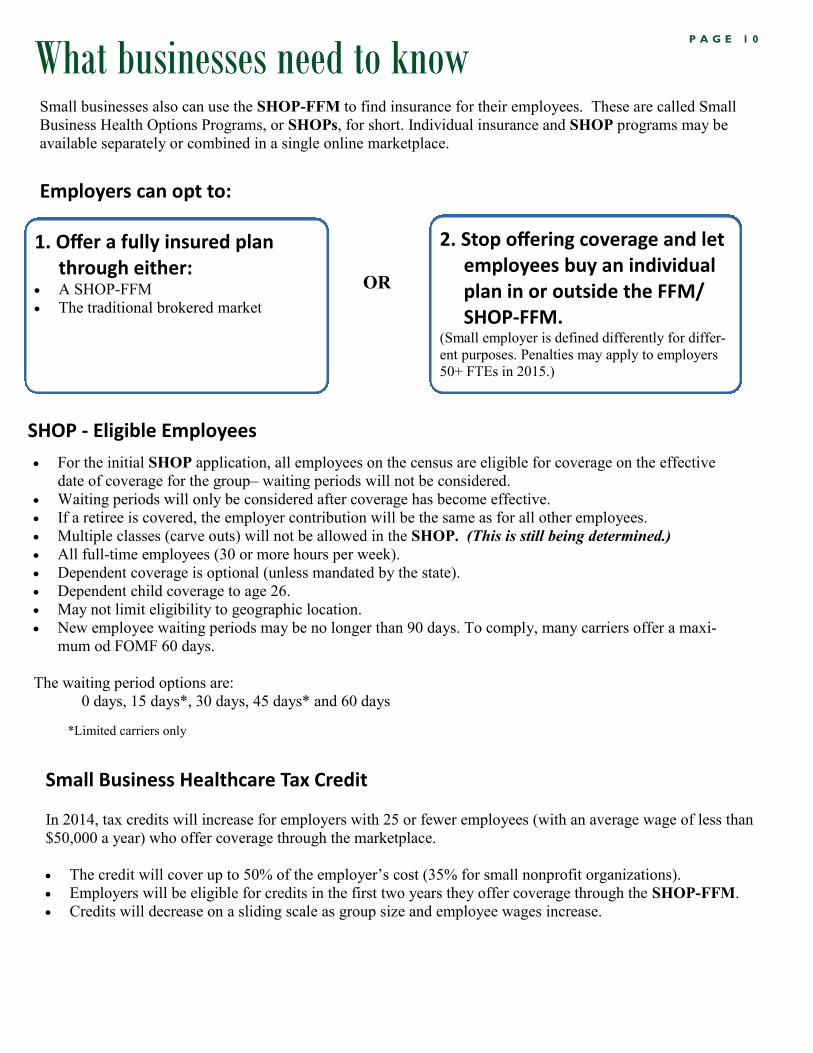

What businesses need to know Small businesses also can use the SHOP-FFM to find insurance for their employees. These are called Small

Business Health Options Programs, or SHOPs, for short. Individual insurance and SHOP programs may be

available separately or combined in a single online marketplace.

Employers can opt to:

2. Stop offering coverage and let employees buy an individual plan in or outside the FFM/SHOP-FFM.

(Small employer is defined differently for differ-

ent purposes. Penalties may apply to employers

50+ FTEs in 2015.)

1. Offer a fully insured plan through either:

A SHOP-FFM

The traditional brokered market

P A G E 1 0

OR

Small Business Healthcare Tax Credit

In 2014, tax credits will increase for employers with 25 or fewer employees (with an average wage of less than

$50,000 a year) who offer coverage through the marketplace.

The credit will cover up to 50% of the employer’s cost (35% for small nonprofit organizations).

Employers will be eligible for credits in the first two years they offer coverage through the SHOP-FFM.

Credits will decrease on a sliding scale as group size and employee wages increase.

SHOP - Eligible Employees

For the initial SHOP application, all employees on the census are eligible for coverage on the effective

date of coverage for the group– waiting periods will not be considered.

Waiting periods will only be considered after coverage has become effective.

If a retiree is covered, the employer contribution will be the same as for all other employees.

Multiple classes (carve outs) will not be allowed in the SHOP. (This is still being determined.)

All full-time employees (30 or more hours per week).

Dependent coverage is optional (unless mandated by the state).

Dependent child coverage to age 26.

May not limit eligibility to geographic location.

New employee waiting periods may be no longer than 90 days. To comply, many carriers offer a maxi-

mum od FOMF 60 days.

The waiting period options are:

0 days, 15 days*, 30 days, 45 days* and 60 days

*Limited carriers only

P A G E 1 1

Penalties for large group employers (50+)

Large group employers

Health insurance options for large group employers

1. Offer health insurance (either fully insured or a self-insured plan) that meets the mini-mum coverage defini-tion and is affordable.

2. Offer some level of cov-erage that does not meet minimum require-ments and risk the em-ployer penalty.

3. Stop offering coverage and let employees buy insurance through the FFM, and risk the em-ployer penalty (which is not tax deductible).

OR OR

If minimum coverage is not offered to full-time employees, and at least one employee gets

subsidized coverage through the FFM/SHOP-FFM, then a $2,000 penalty is assessed for each

employee (after the first 30).

If minimum coverage is offered to full-time employees but is not affordable for an employee

or does not meet minimum value requirements and that employee gets subsidized coverage

through the FFM/SHOP-FFM, then a $3,000 penalty is assessed for each employee who re-

ceives subsidized coverage.

Note: the Employer Mandate has been delayed until 2015; the fines for not offering coverage will apply then. It is essential to start preparing now to avoid any fees or penalties.

Large employers may be subject to an excise tax if at least one full-time employee whose household income is between 100-400% of FPL level received a premium tax credit on the FFM/SHOP-FFM and the em-ployer either:

Basic Coverage Rules for Large Employers

Fails to offer minimum essential coverage to full-time employees and their dependents.

Offers coverage to full-time em-ployees that does not meet the law’s affordability or minimum value standards.

P A G E 1 1

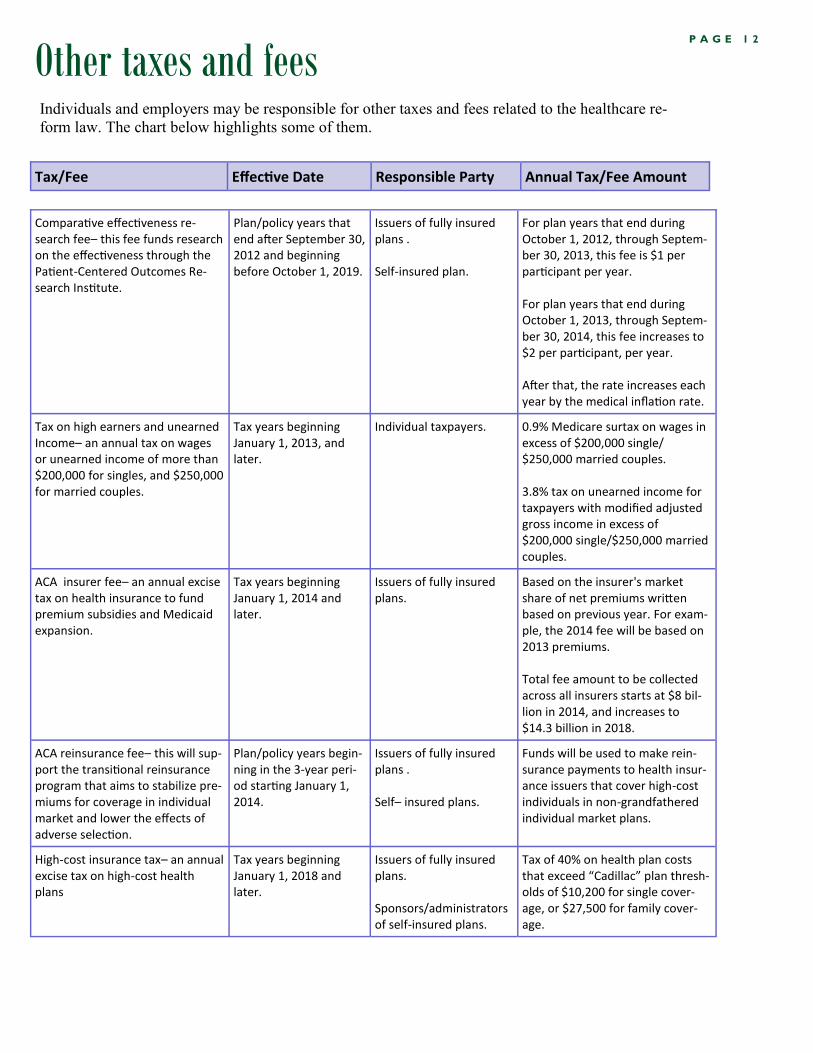

Other taxes and fees P A G E 1 2

Individuals and employers may be responsible for other taxes and fees related to the healthcare re-

form law. The chart below highlights some of them.

Comparative effectiveness re-search fee– this fee funds research on the effectiveness through the Patient-Centered Outcomes Re-search Institute.

Plan/policy years that end after September 30, 2012 and beginning before October 1, 2019.

Issuers of fully insured plans . Self-insured plan.

For plan years that end during October 1, 2012, through Septem-ber 30, 2013, this fee is $1 per participant per year. For plan years that end during October 1, 2013, through Septem-ber 30, 2014, this fee increases to $2 per participant, per year. After that, the rate increases each year by the medical inflation rate.

Tax on high earners and unearned Income– an annual tax on wages or unearned income of more than $200,000 for singles, and $250,000 for married couples.

Tax years beginning January 1, 2013, and later.

Individual taxpayers. 0.9% Medicare surtax on wages in excess of $200,000 single/ $250,000 married couples. 3.8% tax on unearned income for taxpayers with modified adjusted gross income in excess of $200,000 single/$250,000 married couples.

ACA insurer fee– an annual excise tax on health insurance to fund premium subsidies and Medicaid expansion.

Tax years beginning January 1, 2014 and later.

Issuers of fully insured plans.

Based on the insurer's market share of net premiums written based on previous year. For exam-ple, the 2014 fee will be based on 2013 premiums. Total fee amount to be collected across all insurers starts at $8 bil-lion in 2014, and increases to $14.3 billion in 2018.

ACA reinsurance fee– this will sup-port the transitional reinsurance program that aims to stabilize pre-miums for coverage in individual market and lower the effects of adverse selection.

Plan/policy years begin-ning in the 3-year peri-od starting January 1, 2014.

Issuers of fully insured plans . Self– insured plans.

Funds will be used to make rein-surance payments to health insur-ance issuers that cover high-cost individuals in non-grandfathered individual market plans.

High-cost insurance tax– an annual excise tax on high-cost health plans

Tax years beginning January 1, 2018 and later.

Issuers of fully insured plans. Sponsors/administrators of self-insured plans.

Tax of 40% on health plan costs that exceed “Cadillac” plan thresh-olds of $10,200 for single cover-age, or $27,500 for family cover-age.

Tax/Fee Effective Date Responsible Party Annual Tax/Fee Amount

Healthcare.gov https://www.healthcare.gov/

Healthcare.gov--small-businesses https://www.healthcare.gov/small-businesses/

CCIIO Webpage for agents and brokers: http://www.cms.gov/CCIIO/Programs-and-Initiatives/Health-Insurance-Marketplaces/a-b-resources.html

Role of Agents and Brokers: http://www.cms.gov/CCIIO/Resources/Regulations-and-Guidance/Downloads/agent-broker-5-1-2013.pdf

General CCIIO Resources: http://www.cms.gov/CCIIO/Resources/Fact-Sheets-and-FAQs/index.html

Not covered in this publication, but very important: Employers will have to pro-vide notices to employees no later than October 1, 2013 whether they offer cover-age or not. This is an employers responsibility. For more information please visit: Model Exchange Notices http://www.dol.gov/ebsa/newsroom/tr13-02.html

Disclaimer: Health Care Reform legislation is subject to ongoing guidelines interpretations, and safe

harbors from the Department of Health and Human Services, Treasury Labor. The information and

statistics provided at this time may change with additional guidance.

Additional helpful Resources:

For any additional questions that may not have been covered under “additional helpful resources” contact your Account Executive or email BGA at

P A G E 1 3