health and wellness trends - manitoba · health and wellness trends ... halls cadbury schweppes plc...

TRANSCRIPT

International

Markets

Bureau

MARKET INDICATOR REPORT | APRIL 2010

Health and Wellness Trends

In Mexico

EXECUTIVE SUMMARY

INSIDE THIS ISSUE

DID YOU KNOW

PAGE 2

Health and Wellness in Mexico

Executive Summary 2

Market Data 3

FortifiedFunctional 4-6

Better-For-You 7-10

Neutraceuticals 10-13

Organics 13-16

Middle-aged adults compose

the largest portion of the

Mexican population and will

continue to be the largest part

of the market

Total spending on health

goods and medical services

increased by nearly 50 from

2000-2007

Supermarkets hypermarkets

are the most popular

distribution model for health

and wellness food and

beverages

This report uses definitions for Fortifiedfunctional better-for-you nutraceutical and organic foods as defined in Annex ldquoArdquo Consumer spend ing in Me xi co has continued to increase moderately as the country has enjoyed a decade of continuous economic growth fully recovering from the Tequila Crisis of 1995 However the current global economic crisis combined with the devalued peso has had some bearing on all consumer purchases Nonethe less

increased spending has been observed by consumers on health products and services and can be attributed to both the aging population and increased health awareness in the general population Total spending on health goods and medical services increased by nearly 50 from 2000 to 2007

In Mexico the majority of the population falls within the 15 to 64 years of age demographic and has a projected population growth of 113 for 2009 In 2007 the number of people over the age of 55 is one-fourth that of the United States

Mexicans constitute the second most obese nation in the world after the United States Consumption of so-called junk food particularly among youth is a problem It is cheap easily accessi-ble and for those with lower incomes it is a frequent replacement for whole meals The weight problem in Mexico has prompted various national campaigns public and private to raise health awareness and promote illness prevention In general Mexicans value their health and seek to improve it but lower income segment perceive it to be too expensive either because of the financial cost or the time and effort required Better-educated higher-earning Mexican consumers tend to look for products to reduce the effects of aging These trends are leading to increased demand for food perceived as healthy natural and nutritious

The most significant consumer segment

is the urban segment particularly within the

main metropolitan zones

ldquo

rdquo

PAGE 3

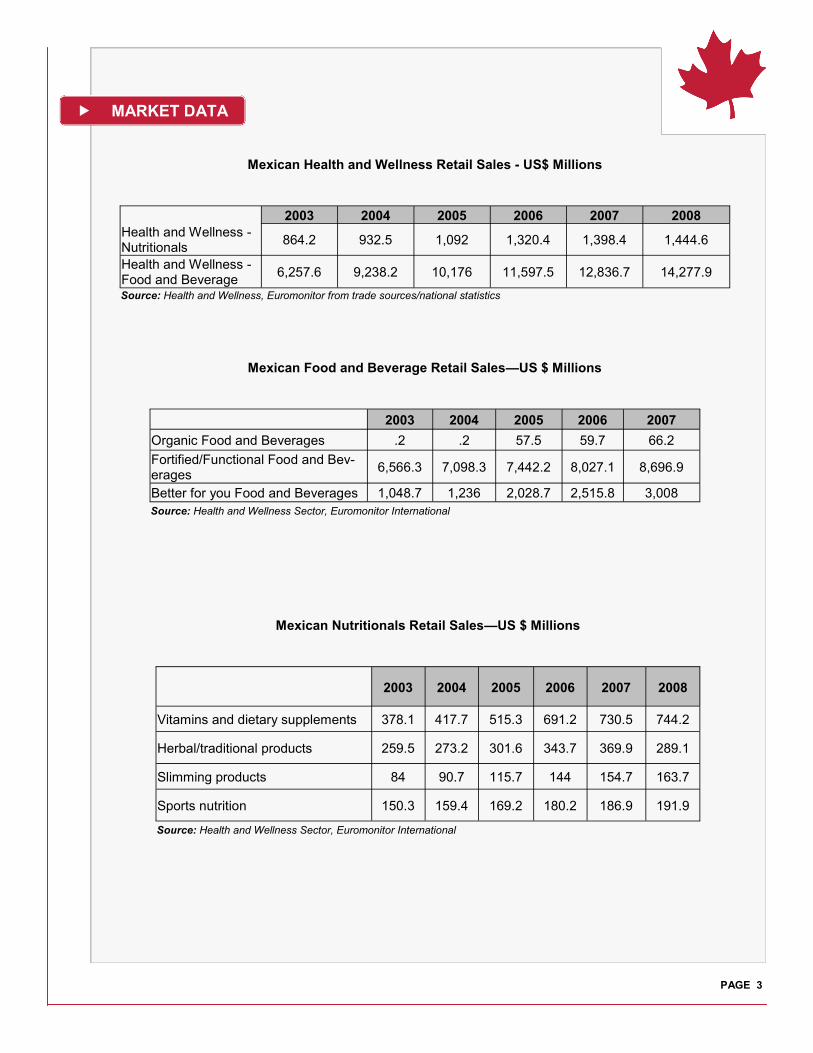

Mexican Food and Beverage Retail SalesmdashUS $ Millions

2003 2004 2005 2006 2007

Organic Food and Beverages 2 2 575 597 662

FortifiedFunctional Food and Bev-erages

65663 70983 74422 80271 86969

Better for you Food and Beverages 10487 1236 20287 25158 3008

Source Health and Wellness Sector Euromonitor International

Mexican Nutritionals Retail SalesmdashUS $ Millions

2003 2004 2005 2006 2007 2008

Vitamins and dietary supplements 3781 4177 5153 6912 7305 7442

Herbaltraditional products 2595 2732 3016 3437 3699 2891

Slimming products 84 907 1157 144 1547 1637

Sports nutrition 1503 1594 1692 1802 1869 1919

Source Health and Wellness Sector Euromonitor International

Mexican Health and Wellness Retail Sales - US$ Millions

2003 2004 2005 2006 2007 2008

Health and Wellness - Nutritionals

8642 9325 1092 13204 13984 14446

Health and Wellness - Food and Beverage

62576 92382 10176 115975 128367 142779

Source Health and Wellness Euromonitor from trade sourcesnational statistics

MARKET DATA

FORTIFIEDFUNCTIONAL FOODS

PAGE 4

Consumer Trends

The Mexican fortifiedfunctional market retail sales were US$8696 million in 2007 up from US$8027 million in

2006 the positioning of fortifiedfunctional products remained stable from 2006 to 2007 with the exception of those

in the cholesterol-lowering category which saw sales double from 15 in 2006 to 3 in 2007

The power of brands and brand loyalty in Mexico has been historically strong

Rural lower-income consumers will choose ldquocheaperrdquo soft drinks while urban higher-income consumers tend to

choose the more expensive healthier vitamin water

Distribution

While supermarkets hypermarkets are the most popular mode of distribution for health and wellness food and

beverages their share has been gradually declining from 98 in 2003 to 90 in 2007 Independent small grocer

sources are growing and ranked second in popularity at 69 The non-grocery retailers share is also growing

slowly capturing 31 market share in 2007

48 of fortified functional food and beverage products were distributed through supermarketshypermarkets in

2007

Source Health and Wellness Euromonitor International

Functional Food Sales Distribution breakdown by Retail Outlet

2002 2003 2004 2005 2006 2007

Store-Based Retailing 100 100 100 995 99 985

SupermarketsHypermarkets 48 475 47 475 48 48

Discounters 17 17 17 175 18 185

Small Grocery Retailers 32 32 33 31 295 28

Convenience Stores 3 3 5 7 7 8

Independent Small Grocers 28 28 27 22 195 17

Forecourt Retailers 1 1 1 2 3 3

Other store-based retailing 3 35 3 35 35 4

Other Grocery Retailers 3 35 3 35 35 4

Non-Grocery Retailers - - - - - -

Non-Store Retailing - - - 05 1 15

Vending - - - 05 1 15

Homeshopping - - - - - -

Internet Retailing - - - - - -

Direct Selling - - - - - -

PAGE 5

Companies and Brands

Source Health and Wellness Food and Beverages Euromonitor International

Brand Shares (by Global Brand Name) - Retail Sales breakdown

Brand Company name (GBO) 2005 2006 2007

Lala Industrial Lala SA de CV Grupo 13 126 124

Alpura Ganaderos Productores de Leche Pura SA de CV

99 95 94

Yakult Yakult Honsha Co Ltd 35 35 33

Leche Liconsa Liconsa SA de CV 36 34 3

Sello Rojo Lechera Guadalajara SA de CV 28 27 27

Boreal Industrial Lala SA de CV Grupo 31 28 26

Nido Nestleacute SA 18 19 21

Boing Sociedad Cooperativa Trabajadores de Pascual SCL

17 19 2

Kelloggs Coco Pops Kellogg Co 19 19 19

Sveltesse Nestleacute SA 16 17 18

Kelloggs Frosties Kellogg Co 15 15 15

Pau Pau Jumex SA de CV Grupo 13 14 15

Halls Cadbury Schweppes Plc 16 15 15

Kelloggs Special K Kellogg Co 13 14 15

Frutsi Administracioacuten SAPI SA de CV - - 14

Danonino Danone Groupe 13 13 13

Nutri Leche Industrial Lala SA de CV Grupo 15 13 12

La Moderna La Moderna SA de CV Grupo 16 13 12

Chiquitin Nestleacute SA 13 12 12

Kelloggs Corn Flakes Kellogg Co 14 13 11

Choco Milk Bristol-Myers Squibb Co 14 13 11

Kelloggs Froot Loops Kellogg Co 1 1 1

San Marcos Pasteurizada Aguascalientes SA de CV 1 1 09

Santa Clara Santa Clara Productos Lacteos SA de CV 09 09 09

Nesquik Nestleacute SA 1 09 08

Cal-C-Tose Bristol-Myers Squibb Co 1 09 08

Fitness Cereal Partners Worldwide SA 08 08 08

Saladitas PepsiCo Inc 08 08 08

Yopli Sodiaal SA (Socieacuteteacute de Diffusion Internationale Agro-alimentaire)

08 08 07

Activia Danone Groupe 06 08 07

Emperador PepsiCo Inc 07 07 07

Nestleacute Corn Flakes Cereal Partners Worldwide SA 07 07 06

Barritas Bimbo SA de CV Grupo 06 06 06

Tang Kraft Foods Inc 06 06 06

PAGE 6

New Products

For 2009 there were 46 new functional foods products launched in Mexico Top new product

introductions are as follows

Under the functionalndashimmune system category 15 new products were launched The most new launch activity

was in the drinking yogurts and liquid cultured milk sub-category with five new products The flavored milk sub-

category saw three new product launches Baby juices and drinks had two new product launches followed by

growing-up milk (1-4 yrs) baby formula (6-12 months) baby formula (0-6 mths) white milk and hot cereals sub-

categories which each had one new product introduction

Thirty-one new functional-cardiovascular products were launched Both hot and cold cereals sub-categories

topped the list with the most new product launches at five each Following behind the sweet biscuitscookies sub-

category had four new product introductions Both chocolate tablets and bread amp bread products tied with three

new product launches each Two sauces and seasonings and two processed fish meat and egg products were

introduced under the ldquootherrdquo sub-category Margarine and other blends soy based drinks white milk dry soup and

nuts sub-categories each had one new product launch

Source Mintel

FortifiedFunctional Foods and Beverages New

Products Health Claims Breakdown for 2007

36

17

41

33 Cholesterol-lowering

Digestiveintestinal

health

Energy

General health and

wellbeing

Others

PAGE 7

BETTER FOR YOU FOODS

Consumer Trends

Overall the Mexican better-for-you food marketrsquos retail sales were US$3073 million in 2007 While Mexicos sales of better-for-you food sales remained relatively constant the better-for-you beverage sales dropped 7 from 2006 to 2007 The downturn in beverage sales could be attributed to a number of factors such as positive or negative changes in customer awareness reduction in consumer overall spending or a re-prioritizing of health-related expenditures

Reduced-fat and reduced-sugar became the most sought-after products by consumers concerned with their weight

Mexico is a domestic producer of all

sorts of fruit which are accessible to all

income segments

The fastest-growing products over the

past few years were fish and seafood

meat oils and fats milk cheese and

eggs Source Health and Wellness Food and Beverages Euromonitor International Note 2009 data is provisional and based on part-year estimates

Distribution

72 of naturally healthy

f o o d a n d b e v e r a g e s

p r e shy d o m i n a n t l y s o l d

through supermarkets

hypermarkets in 2007 a

steady decline since 2002

Source Health and Wellness Food and Beverages Euromonitor International

Better-For-You Sales Distribution breakdown

by Retail Outlet

2002 2003 2004 2005 2006 2007

Store-Based Retailing 100 100 100 100 100 100

SupermarketsHypermarkets 84 80 78 76 74 72

Discounters 12 13 14 15 16 16

Small Grocery Retailers 2 5 6 7 8 98

Convenience Stores 2 5 4 5 55 7

Independent Small Grocers - - 2 2 2 2

Forecourt Retailers - - - - 05 08

Other store-based retailing 2 2 2 2 2 23

Other Grocery Retailers 2 2 2 2 2 23

Non-Grocery Retailers - - - - - -

Non-Store Retailing - - - - - -

Vending - - - - - -

Homeshopping - - - - - -

Internet Retailing - - - - - -

Direct Selling - - - - - -

Mexico Better-For-You Market Sales

Growth for 2006-2007

126 125

405333

0

10

20

30

40

50

2006 2007

Year

Perc

en

tag

e Better-for-you

Packaged Food

Better-for-you

Beverages

PAGE 8

Companies and Brands

Of better-for-you food and beverages Coca Cola Co owned the largest company market share for 2007 at 21 The Danone Group held a good part of the business with 16 share as well as Pepsi Co which captured 152 of the Mexico market

The naturally healthy food and beverages category is dominated by Nestle SA with a 175 company share in 2007 Bimbo SA in second with 173 followed by Pepsi Co with 134 market share

Brand Shares (by Global Brand Name) Retail Sales breakdown

Brand Company name

(GBO) 2005 2006 2007

Diet Coke Coca-Cola Co The 158 143 145

Trident Cadbury Schweppes Plc

121 11 108

Leviteacute Danone Groupe 53 87 105

Be-light PepsiCo Inc 42 65 84

VitalineaVitasnellaTaillefine Danone Groupe

65 61 52

Ciel Coca-Cola Co The 16 34 45

Douglas PepsiCo Inc 34 37 38

Clight Kraft Foods Inc 41 37 37

Sveltesse Nestleacute SA 35 32 29

San Rafael Sigma Alimentos SA 37 32 28

Carnation Nestleacute SA 33 28 27

Zwan Sara Lee Corp 25 22 19

Noche Buena Sigma Alimentos SA de CV

19 17 16

Nescafeacute Nestleacute SA 19 17 15

Diet Pepsi PepsiCo Inc 19 15 13

Sprite Zero Coca-Cola Co The 12 14 12

Sabori Grupo Bafar 14 12 11

Pentildearanda Empacadora Campo Friacuteo SA de CV

14 12 11

Coca-Cola Zero Coca-Cola Co The - - 1

McCormick McCormick amp Co Inc 13 12 1

Bernina Empacadora Bernina SA de CV

13 11 1

Source Health and Wellness Sector Euromonitor International

PAGE 9

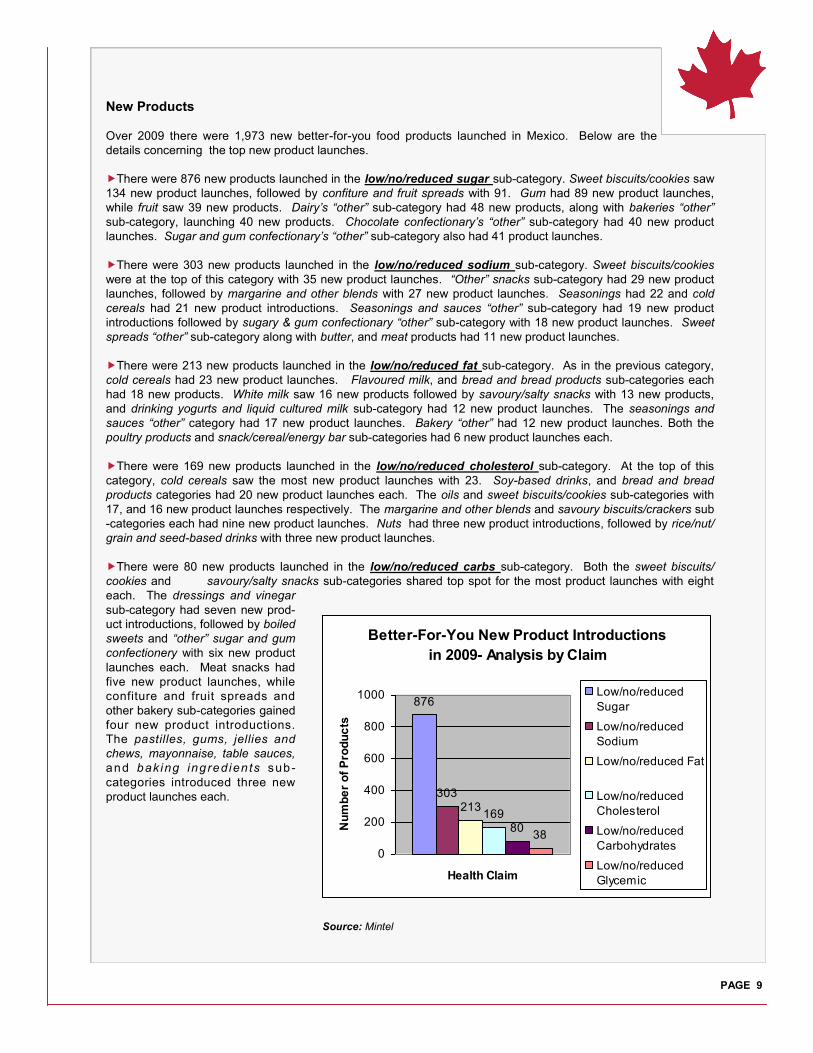

New Products

Over 2009 there were 1973 new better-for-you food products launched in Mexico Below are the

details concerning the top new product launches

There were 876 new products launched in the lownoreduced sugar sub-category Sweet biscuitscookies saw

134 new product launches followed by confiture and fruit spreads with 91 Gum had 89 new product launches

while fruit saw 39 new products Dairyrsquos ldquootherrdquo sub-category had 48 new products along with bakeries ldquootherrdquo

sub-category launching 40 new products Chocolate confectionaryrsquos ldquootherrdquo sub-category had 40 new product

launches Sugar and gum confectionaryrsquos ldquootherrdquo sub-category also had 41 product launches

There were 303 new products launched in the lownoreduced sodium sub-category Sweet biscuitscookies

were at the top of this category with 35 new product launches ldquoOtherrdquo snacks sub-category had 29 new product

launches followed by margarine and other blends with 27 new product launches Seasonings had 22 and cold

cereals had 21 new product introductions Seasonings and sauces ldquootherrdquo sub-category had 19 new product

introductions followed by sugary amp gum confectionary ldquootherrdquo sub-category with 18 new product launches Sweet

spreads ldquootherrdquo sub-category along with butter and meat products had 11 new product launches

There were 213 new products launched in the lownoreduced fat sub-category As in the previous category

cold cereals had 23 new product launches Flavoured milk and bread and bread products sub-categories each

had 18 new products White milk saw 16 new products followed by savourysalty snacks with 13 new products

and drinking yogurts and liquid cultured milk sub-category had 12 new product launches The seasonings and

sauces ldquootherrdquo category had 17 new product launches Bakery ldquootherrdquo had 12 new product launches Both the

poultry products and snackcerealenergy bar sub-categories had 6 new product launches each

There were 169 new products launched in the lownoreduced cholesterol sub-category At the top of this

category cold cereals saw the most new product launches with 23 Soy-based drinks and bread and bread

products categories had 20 new product launches each The oils and sweet biscuitscookies sub-categories with

17 and 16 new product launches respectively The margarine and other blends and savoury biscuitscrackers sub

-categories each had nine new product launches Nuts had three new product introductions followed by ricenut

grain and seed-based drinks with three new product launches

There were 80 new products launched in the lownoreduced carbs sub-category Both the sweet biscuits

cookies and savourysalty snacks sub-categories shared top spot for the most product launches with eight

each The dressings and vinegar

sub-category had seven new prod-

uct introductions followed by boiled

sweets and ldquootherrdquo sugar and gum

confectionery with six new product

launches each Meat snacks had

five new product launches while

confiture and fruit spreads and

other bakery sub-categories gained

four new product introductions

The pastilles gums jellies and

chews mayonnaise table sauces

and baking ingredien ts sub-

categories introduced three new

product launches each

Source Mintel

Better-For-You New Product Introductions

in 2009- Analysis by Claim

876

303213

16980

38

0

200

400

600

800

1000

Health Claim

Nu

mb

er

of

Pro

du

cts

Lownoreduced

Sugar

Lownoreduced

Sodium

Lownoreduced Fat

Lownoreduced

Cholesterol

Lownoreduced

Carbohydrates

Lownoreduced

Glycemic

PAGE 10

There were 38 new products launched in the lownoreduced glycemic sub-category Syrups saw

11 new product launches followed by sweet biscuitscookies sub-category had nine new product

launches The non-individually wrapped chocolate pieces boiled sweets and sweeteners and sugars

sub-categories had two product launches each Honey confiture and fruit spreads chocolate pastilles gums

jellies and chews and bakery ldquootherrdquo sub-categories each had one product launch

Consumer Trends

Meal replacementslimming products and herbal and traditional products were the most popular nutraceutical

purchases by the Mexican consumer in 2009 The Mexican meal replacementslimming products market has

grown from US$671 million in 2005 to over US$1024 million in 2009 The typical group of consumers interested in

meal replacementslimming products are high-income earners who make up a fraction of the total population

Powder versions of meal replacementslimming products are the most popular but are losing share to bars and

ready-to-drink types which are typically found in six packs

Vitamins and dietary supplements retail sales reached US$6389 million in 2009 and are expected to grow by

13 in constant value terms over the next few years In a comparative analysis of herbaltraditional supplements

versus standard supplements the herbaltraditional products are outselling slightly with approximately 1 growth

per year since 2005 Of the dietary supplements calcium was the top seller in 2008 however cod liver oil was the

fastest growing in popularity Multivitamins aimed at consumers in the lower income segments will remain the most

popular products

Sports nutrition product sales value remained relatively constant from 2006 to 2009 reaching US$1528 million in

2009 Of the various items that make up this category protein powder dominates with 72 of sales followed by

protein bars with 23 of sales

Interestingly nutraceuticals saw a drop in sales volume as opposed to sales value across the board in 2009 This may be attributed to the global economic downturn which affected consumers worldwide during this time frame

NUTRACEUTICALS

59

88

40

91

54

26

38

34

-22

57

64

18

Mexico Nutraceuticals Market Growth from 2007 to 2009

Vitamins and Dietary Supplements

Sports Nutrition

Meal ReplacementSlimming Products

Herbal and Traditional Products

Note 2009 data is provisional and based on part-year estimates

Source Health and Wellness Sector Euromonitor Internaitonal

PAGE 11

Distribution

136 of herbaltraditional products were sold in grocery retail and 673 were sold in nonshygrocery retail such as pharmacies 26 of vitamins and dietary supplements were sold in grocery retail while 461 sold in non-grocery retail settings

465 of sports nutrition products were purchased through non-grocery retail Direct selling contributed to the remaining volume with 40 of sales

In the slimming products category direct sale was the most popular purchasing option with 45 of sales in 2008 followed by Internet retail with 26 of sales

Companies and Brands

Unilever Groups Slim Fast product has been the dominant product brand in the slimming products category with 405 share in 2008 Herbalife Ltds Herbalife Thermosjetics is in second place with 10 of brand share in 2008 but has been in a slight decline since 2007

In the sports nutrition category Pro Winner from Pronat SA is the leading brand seizing 197 of market share in 2008 Nutrisa Sport from Nutrisa SA is second with 167 This is slightly above Universal by Universal which has 158 share It is important to note that two of the three leading brands have lost market share which appears to be cascading down to lesser players in this category

In the slimming products category the dominant supplier in 2008 was Unilever with 405 of the market followed by

Herbalife with a 139 share

In the vitamin and dietary supplements category the top brand share belongs to Dr Simi from Farmacias Similares SA at 82 surpassing its closest competitor Herbalilfe at 79 in 2008

Medications like Asenlix Xenical and Raductil are being considered by a growing number of Mexicans as alternative

methods for weight loss

Mexico Neutraceutical Sales Distribution breakdown by Retail Outlet

2003 2004 2005 2006 2007 2008

Store-Based Retailing 758 762 724 671 673 665

Grocery Retailers 136 136 144 159 17 172

Non-Grocery Retailers 622 626 579 512 503 493

ChemistsPharmacies 161 163 135 116 104 134

Parapharmacies148 152 144 131 128 94

Healthfood shops 258 256 246 223 223 22

Mass Merchandisers - - - - - -

Other Non-Grocery Retailers

55 55 54 43 48 46

Non-Store Retailing 242 238 276 329 327 335

Vending - - - - - -

Homeshopping - - 01 02 02 02

Internet Retailing 19 22 31 37 42 5

Direct Selling 223 216 244 29 282 283

Source Health and Wellness Sector Euromonitor International

PAGE 12

Company and Brand Market Share Retail Sales breakdown

Brand Company name (GBO) 2004 2005 2006 2007 2008

Slim Fast Unilever Group 32 35 4 42 46

Dr Simi Farmacias Similares SA de CV

48 48 44 42 42

Herbalife Herbalife Ltd 18 31 44 42 41

Pharmaton Boehringer Sohn CH 5 45 4 29 28

ProWinner Pronat SA de CV 0 32 28 27 26

Bedoyecta Laboratorios Grossman SA de CV

13 26 25 26 24

Herbalife ShapeWorks Herbalife Ltd 11 19 26 25 24

Nutrisa Sport Nutrisa SA de CV - 27 23 22 22

Universal Universal Nutrition Inc - 26 25 24 21

Biometrix Schering-Plough Corp 18 19 17 18 19

Aderogyl Sanofi-Aventis 23 21 19 18 18

Omnilife Omnilife SA de CV Grupo

05 11 14 16 16

OGSS Sport Nutrition OGSS SA de CV Grupo - 19 13 12 16

Diabion Merck KGaA 06 08 07 14 13

Centrum Wyeth 23 2 19 14 13

Herbalife Thermojetics Herbalife Ltd 06 09 12 12 11

Rocaltrol Bayer AG 13 13 11 1 11

Weider Weider Global Nutrition LLC

- 12 11 1 1

Caltrate Wyeth 15 12 1 1 1

Cell Activator Herbalife Ltd - - 11 1 1

New Products

Over 2009 there were 176 new nutraceutical products launched in Mexico Below are the details concerning the top

new products launches

There were 83 new products launched in the vitamin category Botanicalherbal products saw the most new

product releases with 16 followed by lowreducedno sugar all natural weight control and childrens (5-12) vitamins

There were 66 new products launched in the herbal supplements category The most product launches were

those claiming to be natural (no preservatives) and geared to specific demographics

There were 18 new products launched in the sports products category The most popular product claim within this

category was lownoreduced caloriesmdashas seen by 10 of the 18 new products Following in popularity were three

product claims of vitaminmineral fortification lownoreduced sodium and lownoreduced fat Apple grape and

lemon-lime were the popular flavours

There were six new products launched in the meal replacement category Of these all were in liquid form and all

claimed to be vitaminmineral fortified

There were only three new products launched in the slimming products category Two of these products are in

capsule form and one in liquid form

Source Health and Wellness Sector Euromonitor International

PAGE 13

Consumer Trends

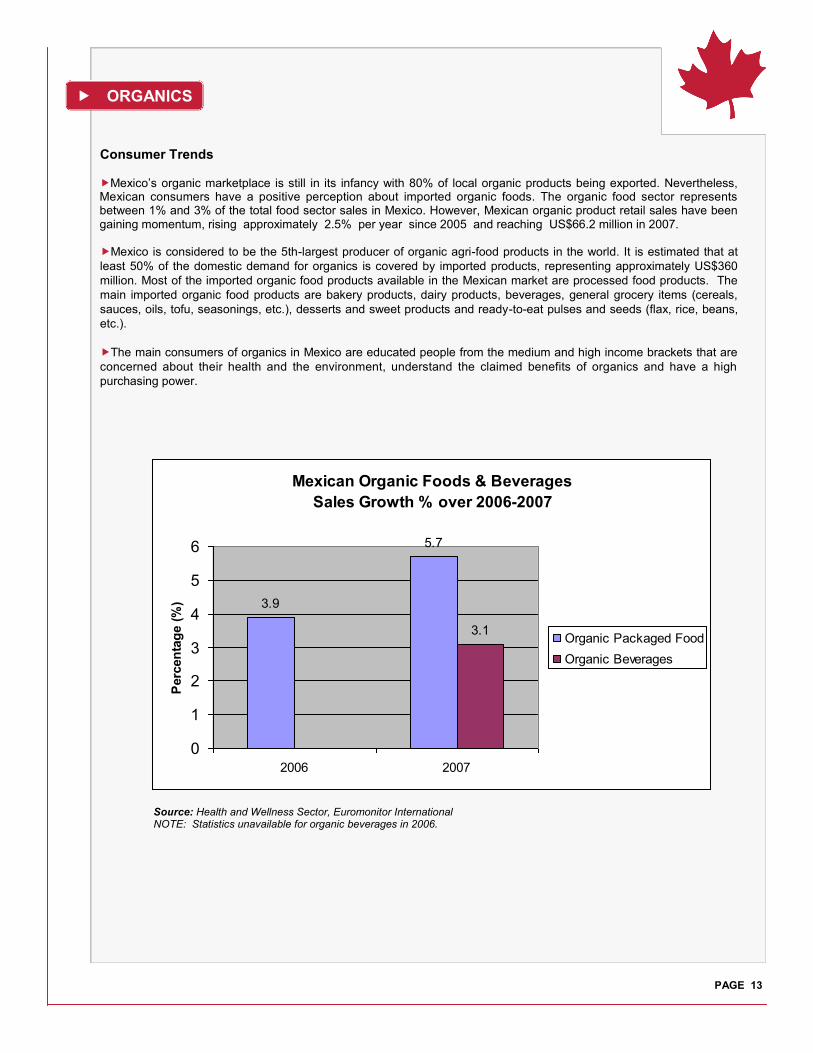

Mexicorsquos organic marketplace is still in its infancy with 80 of local organic products being exported Nevertheless Mexican consumers have a positive perception about imported organic foods The organic food sector represents between 1 and 3 of the total food sector sales in Mexico However Mexican organic product retail sales have been gaining momentum rising approximately 25 per year since 2005 and reaching US$662 million in 2007

Mexico is considered to be the 5th-largest producer of organic agri-food products in the world It is estimated that at

least 50 of the domestic demand for organics is covered by imported products representing approximately US$360

million Most of the imported organic food products available in the Mexican market are processed food products The

main imported organic food products are bakery products dairy products beverages general grocery items (cereals

sauces oils tofu seasonings etc) desserts and sweet products and ready-to-eat pulses and seeds (flax rice beans

etc)

The main consumers of organics in Mexico are educated people from the medium and high income brackets that are

concerned about their health and the environment understand the claimed benefits of organics and have a high

purchasing power

ORGANICS

Source Health and Wellness Sector Euromonitor International NOTE Statistics unavailable for organic beverages in 2006

Mexican Organic Foods amp Beverages

Sales Growth over 2006-2007

39

57

31

0

1

2

3

4

5

6

2006 2007

Perc

en

tag

e (

)

Organic Packaged Food

Organic Beverages

PAGE 14

Distribution

The largest importerdistributor of organic food products in Mexico is Aires de Campo which handles over 600 imported and domestic products This company also has its own brand and store that sells directly to the public Other importerdisbributors are Distribuidora Promesa Smart Holding Mexico Marinter and Tendencia to name a few

Of the five main Mexican store chains that specialize in organics the Green Corner chain is the main one The

remaining are Yerbabuenamarket Origenes Organicos Ki-An and Purorganiko

Source Health and Wellness Euromonitor International

Organics Sales Distribution Analysis by Retail breakdown

2002 2003 2004 2005 2006 2007

Store-Based Retailing 100 100 100 100 100 100

SupermarketsHypermarkets 99 98 97 95 93 90

Discounters - - - - - -

Small Grocery Retailers 1 15 19 36 55 69

Convenience Stores - - - - - -

Independent Small Grocers 1 15 19 36 55 69

Forecourt Retailers - - - - - -

Other store-based retailing - 05 11 14 15 31

Other Grocery Retailers - - - - - -

Non-Grocery Retailers - 05 11 14 15 31

Non-Store Retailing - - - - - -

Vending - - - - - -

Homeshopping - - - - - -

Internet Retailing - - - - - -

Direct Selling - - - - - -

PAGE 15

Companies and Brands

New Products

Over 2009 there were 105 new organic food products launched in Mexico Below are the products listed by category

There were 32 new products launched in the sauces and seasonings category The seasonings sub-category launched 21

new products followed by the ldquootherrdquo sub category with 11 new product launches

There were 13 new products launched in the chocolate confectionery category The chocolate tablets sub-category

launched nine new products and the non-individually wrapped chocolate pieces sub-category saw four new products

introduced

There were 12 new products launched in the fruits and vegetables category The vegetable sub-category saw eight new

products introduced and the fruits sub-category saw four new product launches

There were 10 new products launched in the sweet spreads category The confiture and fruit spreads sub-category saw four

new product launches the honey sub-category saw three new products launched as did the ldquootherrdquo sub-category

There were nine new products launched in the snacks category The snackcerealenergy bars sub-category introduced four

new products the ldquootherrdquo sub-category launched five new snacks

Company and Brand Shares Retail Sales breakdown

Brand Company name (GBO) 2005 2006 2007

Del Rancho Unifoods SA de CV

617 633 643

Biorganic Unifoods SA de CV 165 17 168

Silk Dean Foods Co 56 58 88

Aires de Campo Aires de Campo SA de CV 88 61 12

Avaacutendaro Agrocultivos de Valle de Bravo SA de CV 08 09 1

St Dalfour St Dalfour Fregraveres - - 07

Pasa Organico Panamericana Abarrotera SA de CV - - 07

Blasoacuten Intercafeacute SA de CV - - 02

Tierra Grande Desarrollo Agropecuario Bravo SA de CV 02 02 02

Others Others 64 66 62 Source Health and Wellness Food and Beverages Euromonitor International

PAGE 18

There were eight new products launched in the dairy category The white milk sub-category introduced

three new products and the ldquootherrdquo sub-category launched five new products

There were seven new products launched in the breakfast cereal category The cold cereals sub-

category had six new product introductions and the ldquootherrdquo sub-category had one new breakfast cereal new product intro-

duction

There were 6 new products launched in the bakery category The other sub-category was the sole sub-category with new

product introductions

The soup category and the savoury spreads category each had two product launches in the ldquootherrdquo sub-category

Source Mintel

Mexico Organic Foods

Number of New Product Introductions for 2009

32

13

12

9

6

10

8

7

Sauces and Seasonings

Chocolate confectionary

Fruits and Vegetables

Snacks

Bakery

Sw eet Spreads

Dairy

Breakfast Cereal

PAGE 19

This report analyses the market for health and wellness food and beverages in Mexico For the purposes of this

study the market has been defined as follows

Functional FoodsmdashItems to which health ingredients have been added These functional foods and beverages

should have a specific physiological function andor are enhanced with added ingredients not normally found in the

product providing health benefits beyond their nutritional value The categories covered in this segment are

added calcium functional digestive functional immune system functional bone health and vitaminmineral

fortified

Better-For-You FoodsmdashThe category includes packaged food and beverage products where the amount of a

substance considered to be less healthy (fat sugar salt carbohydrates) has been actively reduced during pro-

duction To qualify for inclusion in this category the ldquoless healthyrdquo element of the food stuff needs to have been

actively removed or substituted during the processing This should form part of the positioningmarketing of the

product Products which are naturally fatsugarcarbohydrate-free are not included The categories covered in this

segment are lownoreduced fat lownoreduced sugar lownoreduced sodium lownoreduced glycemic and

nolowreduced cholesterol

NutraceuticalsmdashNatural substances are found in food which have medicinal properties to treat or prevent certain

diseases These natural substances can be added to the diet by increasing consumption of certain foods or can

be taken as nutritional supplements Products typically claim to prevent chronic diseases improve health delay

the aging process and increase life expectancy The categories covered in this segment are vitamins sports

products herbal supplements and meal replacement slimming products

OrganicmdashProducts that are certified organic by an approved certification body Depending on the country such

products are called ldquoorganicrdquo ldquobiologicalrdquo or ldquoecologicalrdquo

The usage of the above categories are taken from both Euromonitor International and Mintel These groupings

represent globally accepted classification and product identification for the purpose of data collection

ANNEX ldquoArdquo DEFINITIONS

Health and Wellness in Mexico copy Her Majesty the Queen in Right of Canada 2010 ISSN 1920-6593 Market Indicator Report AAFC No 11204E Photo Credits All Photographs reproduced in this publication are used by permission of the rights holders All images unless otherwise noted are copyright Her Majesty the Queen in Right of Canada

For additional copies of this publication or to request an alternate format please contact Agriculture and Agri-Food Canada 1341 Baseline Road Tower 5 4th floor Ottawa ON Canada K1A 0C5 E-mail infoserviceagrgcca

Aussi disponible en franccedilais sous le titre Les produits de santeacute et de mieux-ecirctre au Mexique

The Government of Canada has prepared this report based on primary and secondary sources of information Although every effort has been made to ensure that the information is accurate Agriculture and Agri-Food Canada assumes no liability for any actions taken based on the information contained herein

EXECUTIVE SUMMARY

INSIDE THIS ISSUE

DID YOU KNOW

PAGE 2

Health and Wellness in Mexico

Executive Summary 2

Market Data 3

FortifiedFunctional 4-6

Better-For-You 7-10

Neutraceuticals 10-13

Organics 13-16

Middle-aged adults compose

the largest portion of the

Mexican population and will

continue to be the largest part

of the market

Total spending on health

goods and medical services

increased by nearly 50 from

2000-2007

Supermarkets hypermarkets

are the most popular

distribution model for health

and wellness food and

beverages

This report uses definitions for Fortifiedfunctional better-for-you nutraceutical and organic foods as defined in Annex ldquoArdquo Consumer spend ing in Me xi co has continued to increase moderately as the country has enjoyed a decade of continuous economic growth fully recovering from the Tequila Crisis of 1995 However the current global economic crisis combined with the devalued peso has had some bearing on all consumer purchases Nonethe less

increased spending has been observed by consumers on health products and services and can be attributed to both the aging population and increased health awareness in the general population Total spending on health goods and medical services increased by nearly 50 from 2000 to 2007

In Mexico the majority of the population falls within the 15 to 64 years of age demographic and has a projected population growth of 113 for 2009 In 2007 the number of people over the age of 55 is one-fourth that of the United States

Mexicans constitute the second most obese nation in the world after the United States Consumption of so-called junk food particularly among youth is a problem It is cheap easily accessi-ble and for those with lower incomes it is a frequent replacement for whole meals The weight problem in Mexico has prompted various national campaigns public and private to raise health awareness and promote illness prevention In general Mexicans value their health and seek to improve it but lower income segment perceive it to be too expensive either because of the financial cost or the time and effort required Better-educated higher-earning Mexican consumers tend to look for products to reduce the effects of aging These trends are leading to increased demand for food perceived as healthy natural and nutritious

The most significant consumer segment

is the urban segment particularly within the

main metropolitan zones

ldquo

rdquo

PAGE 3

Mexican Food and Beverage Retail SalesmdashUS $ Millions

2003 2004 2005 2006 2007

Organic Food and Beverages 2 2 575 597 662

FortifiedFunctional Food and Bev-erages

65663 70983 74422 80271 86969

Better for you Food and Beverages 10487 1236 20287 25158 3008

Source Health and Wellness Sector Euromonitor International

Mexican Nutritionals Retail SalesmdashUS $ Millions

2003 2004 2005 2006 2007 2008

Vitamins and dietary supplements 3781 4177 5153 6912 7305 7442

Herbaltraditional products 2595 2732 3016 3437 3699 2891

Slimming products 84 907 1157 144 1547 1637

Sports nutrition 1503 1594 1692 1802 1869 1919

Source Health and Wellness Sector Euromonitor International

Mexican Health and Wellness Retail Sales - US$ Millions

2003 2004 2005 2006 2007 2008

Health and Wellness - Nutritionals

8642 9325 1092 13204 13984 14446

Health and Wellness - Food and Beverage

62576 92382 10176 115975 128367 142779

Source Health and Wellness Euromonitor from trade sourcesnational statistics

MARKET DATA

FORTIFIEDFUNCTIONAL FOODS

PAGE 4

Consumer Trends

The Mexican fortifiedfunctional market retail sales were US$8696 million in 2007 up from US$8027 million in

2006 the positioning of fortifiedfunctional products remained stable from 2006 to 2007 with the exception of those

in the cholesterol-lowering category which saw sales double from 15 in 2006 to 3 in 2007

The power of brands and brand loyalty in Mexico has been historically strong

Rural lower-income consumers will choose ldquocheaperrdquo soft drinks while urban higher-income consumers tend to

choose the more expensive healthier vitamin water

Distribution

While supermarkets hypermarkets are the most popular mode of distribution for health and wellness food and

beverages their share has been gradually declining from 98 in 2003 to 90 in 2007 Independent small grocer

sources are growing and ranked second in popularity at 69 The non-grocery retailers share is also growing

slowly capturing 31 market share in 2007

48 of fortified functional food and beverage products were distributed through supermarketshypermarkets in

2007

Source Health and Wellness Euromonitor International

Functional Food Sales Distribution breakdown by Retail Outlet

2002 2003 2004 2005 2006 2007

Store-Based Retailing 100 100 100 995 99 985

SupermarketsHypermarkets 48 475 47 475 48 48

Discounters 17 17 17 175 18 185

Small Grocery Retailers 32 32 33 31 295 28

Convenience Stores 3 3 5 7 7 8

Independent Small Grocers 28 28 27 22 195 17

Forecourt Retailers 1 1 1 2 3 3

Other store-based retailing 3 35 3 35 35 4

Other Grocery Retailers 3 35 3 35 35 4

Non-Grocery Retailers - - - - - -

Non-Store Retailing - - - 05 1 15

Vending - - - 05 1 15

Homeshopping - - - - - -

Internet Retailing - - - - - -

Direct Selling - - - - - -

PAGE 5

Companies and Brands

Source Health and Wellness Food and Beverages Euromonitor International

Brand Shares (by Global Brand Name) - Retail Sales breakdown

Brand Company name (GBO) 2005 2006 2007

Lala Industrial Lala SA de CV Grupo 13 126 124

Alpura Ganaderos Productores de Leche Pura SA de CV

99 95 94

Yakult Yakult Honsha Co Ltd 35 35 33

Leche Liconsa Liconsa SA de CV 36 34 3

Sello Rojo Lechera Guadalajara SA de CV 28 27 27

Boreal Industrial Lala SA de CV Grupo 31 28 26

Nido Nestleacute SA 18 19 21

Boing Sociedad Cooperativa Trabajadores de Pascual SCL

17 19 2

Kelloggs Coco Pops Kellogg Co 19 19 19

Sveltesse Nestleacute SA 16 17 18

Kelloggs Frosties Kellogg Co 15 15 15

Pau Pau Jumex SA de CV Grupo 13 14 15

Halls Cadbury Schweppes Plc 16 15 15

Kelloggs Special K Kellogg Co 13 14 15

Frutsi Administracioacuten SAPI SA de CV - - 14

Danonino Danone Groupe 13 13 13

Nutri Leche Industrial Lala SA de CV Grupo 15 13 12

La Moderna La Moderna SA de CV Grupo 16 13 12

Chiquitin Nestleacute SA 13 12 12

Kelloggs Corn Flakes Kellogg Co 14 13 11

Choco Milk Bristol-Myers Squibb Co 14 13 11

Kelloggs Froot Loops Kellogg Co 1 1 1

San Marcos Pasteurizada Aguascalientes SA de CV 1 1 09

Santa Clara Santa Clara Productos Lacteos SA de CV 09 09 09

Nesquik Nestleacute SA 1 09 08

Cal-C-Tose Bristol-Myers Squibb Co 1 09 08

Fitness Cereal Partners Worldwide SA 08 08 08

Saladitas PepsiCo Inc 08 08 08

Yopli Sodiaal SA (Socieacuteteacute de Diffusion Internationale Agro-alimentaire)

08 08 07

Activia Danone Groupe 06 08 07

Emperador PepsiCo Inc 07 07 07

Nestleacute Corn Flakes Cereal Partners Worldwide SA 07 07 06

Barritas Bimbo SA de CV Grupo 06 06 06

Tang Kraft Foods Inc 06 06 06

PAGE 6

New Products

For 2009 there were 46 new functional foods products launched in Mexico Top new product

introductions are as follows

Under the functionalndashimmune system category 15 new products were launched The most new launch activity

was in the drinking yogurts and liquid cultured milk sub-category with five new products The flavored milk sub-

category saw three new product launches Baby juices and drinks had two new product launches followed by

growing-up milk (1-4 yrs) baby formula (6-12 months) baby formula (0-6 mths) white milk and hot cereals sub-

categories which each had one new product introduction

Thirty-one new functional-cardiovascular products were launched Both hot and cold cereals sub-categories

topped the list with the most new product launches at five each Following behind the sweet biscuitscookies sub-

category had four new product introductions Both chocolate tablets and bread amp bread products tied with three

new product launches each Two sauces and seasonings and two processed fish meat and egg products were

introduced under the ldquootherrdquo sub-category Margarine and other blends soy based drinks white milk dry soup and

nuts sub-categories each had one new product launch

Source Mintel

FortifiedFunctional Foods and Beverages New

Products Health Claims Breakdown for 2007

36

17

41

33 Cholesterol-lowering

Digestiveintestinal

health

Energy

General health and

wellbeing

Others

PAGE 7

BETTER FOR YOU FOODS

Consumer Trends

Overall the Mexican better-for-you food marketrsquos retail sales were US$3073 million in 2007 While Mexicos sales of better-for-you food sales remained relatively constant the better-for-you beverage sales dropped 7 from 2006 to 2007 The downturn in beverage sales could be attributed to a number of factors such as positive or negative changes in customer awareness reduction in consumer overall spending or a re-prioritizing of health-related expenditures

Reduced-fat and reduced-sugar became the most sought-after products by consumers concerned with their weight

Mexico is a domestic producer of all

sorts of fruit which are accessible to all

income segments

The fastest-growing products over the

past few years were fish and seafood

meat oils and fats milk cheese and

eggs Source Health and Wellness Food and Beverages Euromonitor International Note 2009 data is provisional and based on part-year estimates

Distribution

72 of naturally healthy

f o o d a n d b e v e r a g e s

p r e shy d o m i n a n t l y s o l d

through supermarkets

hypermarkets in 2007 a

steady decline since 2002

Source Health and Wellness Food and Beverages Euromonitor International

Better-For-You Sales Distribution breakdown

by Retail Outlet

2002 2003 2004 2005 2006 2007

Store-Based Retailing 100 100 100 100 100 100

SupermarketsHypermarkets 84 80 78 76 74 72

Discounters 12 13 14 15 16 16

Small Grocery Retailers 2 5 6 7 8 98

Convenience Stores 2 5 4 5 55 7

Independent Small Grocers - - 2 2 2 2

Forecourt Retailers - - - - 05 08

Other store-based retailing 2 2 2 2 2 23

Other Grocery Retailers 2 2 2 2 2 23

Non-Grocery Retailers - - - - - -

Non-Store Retailing - - - - - -

Vending - - - - - -

Homeshopping - - - - - -

Internet Retailing - - - - - -

Direct Selling - - - - - -

Mexico Better-For-You Market Sales

Growth for 2006-2007

126 125

405333

0

10

20

30

40

50

2006 2007

Year

Perc

en

tag

e Better-for-you

Packaged Food

Better-for-you

Beverages

PAGE 8

Companies and Brands

Of better-for-you food and beverages Coca Cola Co owned the largest company market share for 2007 at 21 The Danone Group held a good part of the business with 16 share as well as Pepsi Co which captured 152 of the Mexico market

The naturally healthy food and beverages category is dominated by Nestle SA with a 175 company share in 2007 Bimbo SA in second with 173 followed by Pepsi Co with 134 market share

Brand Shares (by Global Brand Name) Retail Sales breakdown

Brand Company name

(GBO) 2005 2006 2007

Diet Coke Coca-Cola Co The 158 143 145

Trident Cadbury Schweppes Plc

121 11 108

Leviteacute Danone Groupe 53 87 105

Be-light PepsiCo Inc 42 65 84

VitalineaVitasnellaTaillefine Danone Groupe

65 61 52

Ciel Coca-Cola Co The 16 34 45

Douglas PepsiCo Inc 34 37 38

Clight Kraft Foods Inc 41 37 37

Sveltesse Nestleacute SA 35 32 29

San Rafael Sigma Alimentos SA 37 32 28

Carnation Nestleacute SA 33 28 27

Zwan Sara Lee Corp 25 22 19

Noche Buena Sigma Alimentos SA de CV

19 17 16

Nescafeacute Nestleacute SA 19 17 15

Diet Pepsi PepsiCo Inc 19 15 13

Sprite Zero Coca-Cola Co The 12 14 12

Sabori Grupo Bafar 14 12 11

Pentildearanda Empacadora Campo Friacuteo SA de CV

14 12 11

Coca-Cola Zero Coca-Cola Co The - - 1

McCormick McCormick amp Co Inc 13 12 1

Bernina Empacadora Bernina SA de CV

13 11 1

Source Health and Wellness Sector Euromonitor International

PAGE 9

New Products

Over 2009 there were 1973 new better-for-you food products launched in Mexico Below are the

details concerning the top new product launches

There were 876 new products launched in the lownoreduced sugar sub-category Sweet biscuitscookies saw

134 new product launches followed by confiture and fruit spreads with 91 Gum had 89 new product launches

while fruit saw 39 new products Dairyrsquos ldquootherrdquo sub-category had 48 new products along with bakeries ldquootherrdquo

sub-category launching 40 new products Chocolate confectionaryrsquos ldquootherrdquo sub-category had 40 new product

launches Sugar and gum confectionaryrsquos ldquootherrdquo sub-category also had 41 product launches

There were 303 new products launched in the lownoreduced sodium sub-category Sweet biscuitscookies

were at the top of this category with 35 new product launches ldquoOtherrdquo snacks sub-category had 29 new product

launches followed by margarine and other blends with 27 new product launches Seasonings had 22 and cold

cereals had 21 new product introductions Seasonings and sauces ldquootherrdquo sub-category had 19 new product

introductions followed by sugary amp gum confectionary ldquootherrdquo sub-category with 18 new product launches Sweet

spreads ldquootherrdquo sub-category along with butter and meat products had 11 new product launches

There were 213 new products launched in the lownoreduced fat sub-category As in the previous category

cold cereals had 23 new product launches Flavoured milk and bread and bread products sub-categories each

had 18 new products White milk saw 16 new products followed by savourysalty snacks with 13 new products

and drinking yogurts and liquid cultured milk sub-category had 12 new product launches The seasonings and

sauces ldquootherrdquo category had 17 new product launches Bakery ldquootherrdquo had 12 new product launches Both the

poultry products and snackcerealenergy bar sub-categories had 6 new product launches each

There were 169 new products launched in the lownoreduced cholesterol sub-category At the top of this

category cold cereals saw the most new product launches with 23 Soy-based drinks and bread and bread

products categories had 20 new product launches each The oils and sweet biscuitscookies sub-categories with

17 and 16 new product launches respectively The margarine and other blends and savoury biscuitscrackers sub

-categories each had nine new product launches Nuts had three new product introductions followed by ricenut

grain and seed-based drinks with three new product launches

There were 80 new products launched in the lownoreduced carbs sub-category Both the sweet biscuits

cookies and savourysalty snacks sub-categories shared top spot for the most product launches with eight

each The dressings and vinegar

sub-category had seven new prod-

uct introductions followed by boiled

sweets and ldquootherrdquo sugar and gum

confectionery with six new product

launches each Meat snacks had

five new product launches while

confiture and fruit spreads and

other bakery sub-categories gained

four new product introductions

The pastilles gums jellies and

chews mayonnaise table sauces

and baking ingredien ts sub-

categories introduced three new

product launches each

Source Mintel

Better-For-You New Product Introductions

in 2009- Analysis by Claim

876

303213

16980

38

0

200

400

600

800

1000

Health Claim

Nu

mb

er

of

Pro

du

cts

Lownoreduced

Sugar

Lownoreduced

Sodium

Lownoreduced Fat

Lownoreduced

Cholesterol

Lownoreduced

Carbohydrates

Lownoreduced

Glycemic

PAGE 10

There were 38 new products launched in the lownoreduced glycemic sub-category Syrups saw

11 new product launches followed by sweet biscuitscookies sub-category had nine new product

launches The non-individually wrapped chocolate pieces boiled sweets and sweeteners and sugars

sub-categories had two product launches each Honey confiture and fruit spreads chocolate pastilles gums

jellies and chews and bakery ldquootherrdquo sub-categories each had one product launch

Consumer Trends

Meal replacementslimming products and herbal and traditional products were the most popular nutraceutical

purchases by the Mexican consumer in 2009 The Mexican meal replacementslimming products market has

grown from US$671 million in 2005 to over US$1024 million in 2009 The typical group of consumers interested in

meal replacementslimming products are high-income earners who make up a fraction of the total population

Powder versions of meal replacementslimming products are the most popular but are losing share to bars and

ready-to-drink types which are typically found in six packs

Vitamins and dietary supplements retail sales reached US$6389 million in 2009 and are expected to grow by

13 in constant value terms over the next few years In a comparative analysis of herbaltraditional supplements

versus standard supplements the herbaltraditional products are outselling slightly with approximately 1 growth

per year since 2005 Of the dietary supplements calcium was the top seller in 2008 however cod liver oil was the

fastest growing in popularity Multivitamins aimed at consumers in the lower income segments will remain the most

popular products

Sports nutrition product sales value remained relatively constant from 2006 to 2009 reaching US$1528 million in

2009 Of the various items that make up this category protein powder dominates with 72 of sales followed by

protein bars with 23 of sales

Interestingly nutraceuticals saw a drop in sales volume as opposed to sales value across the board in 2009 This may be attributed to the global economic downturn which affected consumers worldwide during this time frame

NUTRACEUTICALS

59

88

40

91

54

26

38

34

-22

57

64

18

Mexico Nutraceuticals Market Growth from 2007 to 2009

Vitamins and Dietary Supplements

Sports Nutrition

Meal ReplacementSlimming Products

Herbal and Traditional Products

Note 2009 data is provisional and based on part-year estimates

Source Health and Wellness Sector Euromonitor Internaitonal

PAGE 11

Distribution

136 of herbaltraditional products were sold in grocery retail and 673 were sold in nonshygrocery retail such as pharmacies 26 of vitamins and dietary supplements were sold in grocery retail while 461 sold in non-grocery retail settings

465 of sports nutrition products were purchased through non-grocery retail Direct selling contributed to the remaining volume with 40 of sales

In the slimming products category direct sale was the most popular purchasing option with 45 of sales in 2008 followed by Internet retail with 26 of sales

Companies and Brands

Unilever Groups Slim Fast product has been the dominant product brand in the slimming products category with 405 share in 2008 Herbalife Ltds Herbalife Thermosjetics is in second place with 10 of brand share in 2008 but has been in a slight decline since 2007

In the sports nutrition category Pro Winner from Pronat SA is the leading brand seizing 197 of market share in 2008 Nutrisa Sport from Nutrisa SA is second with 167 This is slightly above Universal by Universal which has 158 share It is important to note that two of the three leading brands have lost market share which appears to be cascading down to lesser players in this category

In the slimming products category the dominant supplier in 2008 was Unilever with 405 of the market followed by

Herbalife with a 139 share

In the vitamin and dietary supplements category the top brand share belongs to Dr Simi from Farmacias Similares SA at 82 surpassing its closest competitor Herbalilfe at 79 in 2008

Medications like Asenlix Xenical and Raductil are being considered by a growing number of Mexicans as alternative

methods for weight loss

Mexico Neutraceutical Sales Distribution breakdown by Retail Outlet

2003 2004 2005 2006 2007 2008

Store-Based Retailing 758 762 724 671 673 665

Grocery Retailers 136 136 144 159 17 172

Non-Grocery Retailers 622 626 579 512 503 493

ChemistsPharmacies 161 163 135 116 104 134

Parapharmacies148 152 144 131 128 94

Healthfood shops 258 256 246 223 223 22

Mass Merchandisers - - - - - -

Other Non-Grocery Retailers

55 55 54 43 48 46

Non-Store Retailing 242 238 276 329 327 335

Vending - - - - - -

Homeshopping - - 01 02 02 02

Internet Retailing 19 22 31 37 42 5

Direct Selling 223 216 244 29 282 283

Source Health and Wellness Sector Euromonitor International

PAGE 12

Company and Brand Market Share Retail Sales breakdown

Brand Company name (GBO) 2004 2005 2006 2007 2008

Slim Fast Unilever Group 32 35 4 42 46

Dr Simi Farmacias Similares SA de CV

48 48 44 42 42

Herbalife Herbalife Ltd 18 31 44 42 41

Pharmaton Boehringer Sohn CH 5 45 4 29 28

ProWinner Pronat SA de CV 0 32 28 27 26

Bedoyecta Laboratorios Grossman SA de CV

13 26 25 26 24

Herbalife ShapeWorks Herbalife Ltd 11 19 26 25 24

Nutrisa Sport Nutrisa SA de CV - 27 23 22 22

Universal Universal Nutrition Inc - 26 25 24 21

Biometrix Schering-Plough Corp 18 19 17 18 19

Aderogyl Sanofi-Aventis 23 21 19 18 18

Omnilife Omnilife SA de CV Grupo

05 11 14 16 16

OGSS Sport Nutrition OGSS SA de CV Grupo - 19 13 12 16

Diabion Merck KGaA 06 08 07 14 13

Centrum Wyeth 23 2 19 14 13

Herbalife Thermojetics Herbalife Ltd 06 09 12 12 11

Rocaltrol Bayer AG 13 13 11 1 11

Weider Weider Global Nutrition LLC

- 12 11 1 1

Caltrate Wyeth 15 12 1 1 1

Cell Activator Herbalife Ltd - - 11 1 1

New Products

Over 2009 there were 176 new nutraceutical products launched in Mexico Below are the details concerning the top

new products launches

There were 83 new products launched in the vitamin category Botanicalherbal products saw the most new

product releases with 16 followed by lowreducedno sugar all natural weight control and childrens (5-12) vitamins

There were 66 new products launched in the herbal supplements category The most product launches were

those claiming to be natural (no preservatives) and geared to specific demographics

There were 18 new products launched in the sports products category The most popular product claim within this

category was lownoreduced caloriesmdashas seen by 10 of the 18 new products Following in popularity were three

product claims of vitaminmineral fortification lownoreduced sodium and lownoreduced fat Apple grape and

lemon-lime were the popular flavours

There were six new products launched in the meal replacement category Of these all were in liquid form and all

claimed to be vitaminmineral fortified

There were only three new products launched in the slimming products category Two of these products are in

capsule form and one in liquid form

Source Health and Wellness Sector Euromonitor International

PAGE 13

Consumer Trends

Mexicorsquos organic marketplace is still in its infancy with 80 of local organic products being exported Nevertheless Mexican consumers have a positive perception about imported organic foods The organic food sector represents between 1 and 3 of the total food sector sales in Mexico However Mexican organic product retail sales have been gaining momentum rising approximately 25 per year since 2005 and reaching US$662 million in 2007

Mexico is considered to be the 5th-largest producer of organic agri-food products in the world It is estimated that at

least 50 of the domestic demand for organics is covered by imported products representing approximately US$360

million Most of the imported organic food products available in the Mexican market are processed food products The

main imported organic food products are bakery products dairy products beverages general grocery items (cereals

sauces oils tofu seasonings etc) desserts and sweet products and ready-to-eat pulses and seeds (flax rice beans

etc)

The main consumers of organics in Mexico are educated people from the medium and high income brackets that are

concerned about their health and the environment understand the claimed benefits of organics and have a high

purchasing power

ORGANICS

Source Health and Wellness Sector Euromonitor International NOTE Statistics unavailable for organic beverages in 2006

Mexican Organic Foods amp Beverages

Sales Growth over 2006-2007

39

57

31

0

1

2

3

4

5

6

2006 2007

Perc

en

tag

e (

)

Organic Packaged Food

Organic Beverages

PAGE 14

Distribution

The largest importerdistributor of organic food products in Mexico is Aires de Campo which handles over 600 imported and domestic products This company also has its own brand and store that sells directly to the public Other importerdisbributors are Distribuidora Promesa Smart Holding Mexico Marinter and Tendencia to name a few

Of the five main Mexican store chains that specialize in organics the Green Corner chain is the main one The

remaining are Yerbabuenamarket Origenes Organicos Ki-An and Purorganiko

Source Health and Wellness Euromonitor International

Organics Sales Distribution Analysis by Retail breakdown

2002 2003 2004 2005 2006 2007

Store-Based Retailing 100 100 100 100 100 100

SupermarketsHypermarkets 99 98 97 95 93 90

Discounters - - - - - -

Small Grocery Retailers 1 15 19 36 55 69

Convenience Stores - - - - - -

Independent Small Grocers 1 15 19 36 55 69

Forecourt Retailers - - - - - -

Other store-based retailing - 05 11 14 15 31

Other Grocery Retailers - - - - - -

Non-Grocery Retailers - 05 11 14 15 31

Non-Store Retailing - - - - - -

Vending - - - - - -

Homeshopping - - - - - -

Internet Retailing - - - - - -

Direct Selling - - - - - -

PAGE 15

Companies and Brands

New Products

Over 2009 there were 105 new organic food products launched in Mexico Below are the products listed by category

There were 32 new products launched in the sauces and seasonings category The seasonings sub-category launched 21

new products followed by the ldquootherrdquo sub category with 11 new product launches

There were 13 new products launched in the chocolate confectionery category The chocolate tablets sub-category

launched nine new products and the non-individually wrapped chocolate pieces sub-category saw four new products

introduced

There were 12 new products launched in the fruits and vegetables category The vegetable sub-category saw eight new

products introduced and the fruits sub-category saw four new product launches

There were 10 new products launched in the sweet spreads category The confiture and fruit spreads sub-category saw four

new product launches the honey sub-category saw three new products launched as did the ldquootherrdquo sub-category

There were nine new products launched in the snacks category The snackcerealenergy bars sub-category introduced four

new products the ldquootherrdquo sub-category launched five new snacks

Company and Brand Shares Retail Sales breakdown

Brand Company name (GBO) 2005 2006 2007

Del Rancho Unifoods SA de CV

617 633 643

Biorganic Unifoods SA de CV 165 17 168

Silk Dean Foods Co 56 58 88

Aires de Campo Aires de Campo SA de CV 88 61 12

Avaacutendaro Agrocultivos de Valle de Bravo SA de CV 08 09 1

St Dalfour St Dalfour Fregraveres - - 07

Pasa Organico Panamericana Abarrotera SA de CV - - 07

Blasoacuten Intercafeacute SA de CV - - 02

Tierra Grande Desarrollo Agropecuario Bravo SA de CV 02 02 02

Others Others 64 66 62 Source Health and Wellness Food and Beverages Euromonitor International

PAGE 18

There were eight new products launched in the dairy category The white milk sub-category introduced

three new products and the ldquootherrdquo sub-category launched five new products

There were seven new products launched in the breakfast cereal category The cold cereals sub-

category had six new product introductions and the ldquootherrdquo sub-category had one new breakfast cereal new product intro-

duction

There were 6 new products launched in the bakery category The other sub-category was the sole sub-category with new

product introductions

The soup category and the savoury spreads category each had two product launches in the ldquootherrdquo sub-category

Source Mintel

Mexico Organic Foods

Number of New Product Introductions for 2009

32

13

12

9

6

10

8

7

Sauces and Seasonings

Chocolate confectionary

Fruits and Vegetables

Snacks

Bakery

Sw eet Spreads

Dairy

Breakfast Cereal

PAGE 19

This report analyses the market for health and wellness food and beverages in Mexico For the purposes of this

study the market has been defined as follows

Functional FoodsmdashItems to which health ingredients have been added These functional foods and beverages

should have a specific physiological function andor are enhanced with added ingredients not normally found in the

product providing health benefits beyond their nutritional value The categories covered in this segment are

added calcium functional digestive functional immune system functional bone health and vitaminmineral

fortified

Better-For-You FoodsmdashThe category includes packaged food and beverage products where the amount of a

substance considered to be less healthy (fat sugar salt carbohydrates) has been actively reduced during pro-

duction To qualify for inclusion in this category the ldquoless healthyrdquo element of the food stuff needs to have been

actively removed or substituted during the processing This should form part of the positioningmarketing of the

product Products which are naturally fatsugarcarbohydrate-free are not included The categories covered in this

segment are lownoreduced fat lownoreduced sugar lownoreduced sodium lownoreduced glycemic and

nolowreduced cholesterol

NutraceuticalsmdashNatural substances are found in food which have medicinal properties to treat or prevent certain

diseases These natural substances can be added to the diet by increasing consumption of certain foods or can

be taken as nutritional supplements Products typically claim to prevent chronic diseases improve health delay

the aging process and increase life expectancy The categories covered in this segment are vitamins sports

products herbal supplements and meal replacement slimming products

OrganicmdashProducts that are certified organic by an approved certification body Depending on the country such

products are called ldquoorganicrdquo ldquobiologicalrdquo or ldquoecologicalrdquo

The usage of the above categories are taken from both Euromonitor International and Mintel These groupings

represent globally accepted classification and product identification for the purpose of data collection

ANNEX ldquoArdquo DEFINITIONS

Health and Wellness in Mexico copy Her Majesty the Queen in Right of Canada 2010 ISSN 1920-6593 Market Indicator Report AAFC No 11204E Photo Credits All Photographs reproduced in this publication are used by permission of the rights holders All images unless otherwise noted are copyright Her Majesty the Queen in Right of Canada

For additional copies of this publication or to request an alternate format please contact Agriculture and Agri-Food Canada 1341 Baseline Road Tower 5 4th floor Ottawa ON Canada K1A 0C5 E-mail infoserviceagrgcca

Aussi disponible en franccedilais sous le titre Les produits de santeacute et de mieux-ecirctre au Mexique

The Government of Canada has prepared this report based on primary and secondary sources of information Although every effort has been made to ensure that the information is accurate Agriculture and Agri-Food Canada assumes no liability for any actions taken based on the information contained herein

PAGE 3

Mexican Food and Beverage Retail SalesmdashUS $ Millions

2003 2004 2005 2006 2007

Organic Food and Beverages 2 2 575 597 662

FortifiedFunctional Food and Bev-erages

65663 70983 74422 80271 86969

Better for you Food and Beverages 10487 1236 20287 25158 3008

Source Health and Wellness Sector Euromonitor International

Mexican Nutritionals Retail SalesmdashUS $ Millions

2003 2004 2005 2006 2007 2008

Vitamins and dietary supplements 3781 4177 5153 6912 7305 7442

Herbaltraditional products 2595 2732 3016 3437 3699 2891

Slimming products 84 907 1157 144 1547 1637

Sports nutrition 1503 1594 1692 1802 1869 1919

Source Health and Wellness Sector Euromonitor International

Mexican Health and Wellness Retail Sales - US$ Millions

2003 2004 2005 2006 2007 2008

Health and Wellness - Nutritionals

8642 9325 1092 13204 13984 14446

Health and Wellness - Food and Beverage

62576 92382 10176 115975 128367 142779

Source Health and Wellness Euromonitor from trade sourcesnational statistics

MARKET DATA

FORTIFIEDFUNCTIONAL FOODS

PAGE 4

Consumer Trends

The Mexican fortifiedfunctional market retail sales were US$8696 million in 2007 up from US$8027 million in

2006 the positioning of fortifiedfunctional products remained stable from 2006 to 2007 with the exception of those

in the cholesterol-lowering category which saw sales double from 15 in 2006 to 3 in 2007

The power of brands and brand loyalty in Mexico has been historically strong

Rural lower-income consumers will choose ldquocheaperrdquo soft drinks while urban higher-income consumers tend to

choose the more expensive healthier vitamin water

Distribution

While supermarkets hypermarkets are the most popular mode of distribution for health and wellness food and

beverages their share has been gradually declining from 98 in 2003 to 90 in 2007 Independent small grocer

sources are growing and ranked second in popularity at 69 The non-grocery retailers share is also growing

slowly capturing 31 market share in 2007

48 of fortified functional food and beverage products were distributed through supermarketshypermarkets in

2007

Source Health and Wellness Euromonitor International

Functional Food Sales Distribution breakdown by Retail Outlet

2002 2003 2004 2005 2006 2007

Store-Based Retailing 100 100 100 995 99 985

SupermarketsHypermarkets 48 475 47 475 48 48

Discounters 17 17 17 175 18 185

Small Grocery Retailers 32 32 33 31 295 28

Convenience Stores 3 3 5 7 7 8

Independent Small Grocers 28 28 27 22 195 17

Forecourt Retailers 1 1 1 2 3 3

Other store-based retailing 3 35 3 35 35 4

Other Grocery Retailers 3 35 3 35 35 4

Non-Grocery Retailers - - - - - -

Non-Store Retailing - - - 05 1 15

Vending - - - 05 1 15

Homeshopping - - - - - -

Internet Retailing - - - - - -

Direct Selling - - - - - -

PAGE 5

Companies and Brands

Source Health and Wellness Food and Beverages Euromonitor International

Brand Shares (by Global Brand Name) - Retail Sales breakdown

Brand Company name (GBO) 2005 2006 2007

Lala Industrial Lala SA de CV Grupo 13 126 124

Alpura Ganaderos Productores de Leche Pura SA de CV

99 95 94

Yakult Yakult Honsha Co Ltd 35 35 33

Leche Liconsa Liconsa SA de CV 36 34 3

Sello Rojo Lechera Guadalajara SA de CV 28 27 27

Boreal Industrial Lala SA de CV Grupo 31 28 26

Nido Nestleacute SA 18 19 21

Boing Sociedad Cooperativa Trabajadores de Pascual SCL

17 19 2

Kelloggs Coco Pops Kellogg Co 19 19 19

Sveltesse Nestleacute SA 16 17 18

Kelloggs Frosties Kellogg Co 15 15 15

Pau Pau Jumex SA de CV Grupo 13 14 15

Halls Cadbury Schweppes Plc 16 15 15

Kelloggs Special K Kellogg Co 13 14 15

Frutsi Administracioacuten SAPI SA de CV - - 14

Danonino Danone Groupe 13 13 13

Nutri Leche Industrial Lala SA de CV Grupo 15 13 12

La Moderna La Moderna SA de CV Grupo 16 13 12

Chiquitin Nestleacute SA 13 12 12

Kelloggs Corn Flakes Kellogg Co 14 13 11

Choco Milk Bristol-Myers Squibb Co 14 13 11

Kelloggs Froot Loops Kellogg Co 1 1 1

San Marcos Pasteurizada Aguascalientes SA de CV 1 1 09

Santa Clara Santa Clara Productos Lacteos SA de CV 09 09 09

Nesquik Nestleacute SA 1 09 08

Cal-C-Tose Bristol-Myers Squibb Co 1 09 08

Fitness Cereal Partners Worldwide SA 08 08 08

Saladitas PepsiCo Inc 08 08 08

Yopli Sodiaal SA (Socieacuteteacute de Diffusion Internationale Agro-alimentaire)

08 08 07

Activia Danone Groupe 06 08 07

Emperador PepsiCo Inc 07 07 07

Nestleacute Corn Flakes Cereal Partners Worldwide SA 07 07 06

Barritas Bimbo SA de CV Grupo 06 06 06

Tang Kraft Foods Inc 06 06 06

PAGE 6

New Products

For 2009 there were 46 new functional foods products launched in Mexico Top new product

introductions are as follows

Under the functionalndashimmune system category 15 new products were launched The most new launch activity

was in the drinking yogurts and liquid cultured milk sub-category with five new products The flavored milk sub-

category saw three new product launches Baby juices and drinks had two new product launches followed by

growing-up milk (1-4 yrs) baby formula (6-12 months) baby formula (0-6 mths) white milk and hot cereals sub-

categories which each had one new product introduction

Thirty-one new functional-cardiovascular products were launched Both hot and cold cereals sub-categories

topped the list with the most new product launches at five each Following behind the sweet biscuitscookies sub-

category had four new product introductions Both chocolate tablets and bread amp bread products tied with three

new product launches each Two sauces and seasonings and two processed fish meat and egg products were

introduced under the ldquootherrdquo sub-category Margarine and other blends soy based drinks white milk dry soup and

nuts sub-categories each had one new product launch

Source Mintel

FortifiedFunctional Foods and Beverages New

Products Health Claims Breakdown for 2007

36

17

41

33 Cholesterol-lowering

Digestiveintestinal

health

Energy

General health and

wellbeing

Others

PAGE 7

BETTER FOR YOU FOODS

Consumer Trends

Overall the Mexican better-for-you food marketrsquos retail sales were US$3073 million in 2007 While Mexicos sales of better-for-you food sales remained relatively constant the better-for-you beverage sales dropped 7 from 2006 to 2007 The downturn in beverage sales could be attributed to a number of factors such as positive or negative changes in customer awareness reduction in consumer overall spending or a re-prioritizing of health-related expenditures

Reduced-fat and reduced-sugar became the most sought-after products by consumers concerned with their weight

Mexico is a domestic producer of all

sorts of fruit which are accessible to all

income segments

The fastest-growing products over the

past few years were fish and seafood

meat oils and fats milk cheese and

eggs Source Health and Wellness Food and Beverages Euromonitor International Note 2009 data is provisional and based on part-year estimates

Distribution

72 of naturally healthy

f o o d a n d b e v e r a g e s

p r e shy d o m i n a n t l y s o l d

through supermarkets

hypermarkets in 2007 a

steady decline since 2002

Source Health and Wellness Food and Beverages Euromonitor International

Better-For-You Sales Distribution breakdown

by Retail Outlet

2002 2003 2004 2005 2006 2007

Store-Based Retailing 100 100 100 100 100 100

SupermarketsHypermarkets 84 80 78 76 74 72

Discounters 12 13 14 15 16 16

Small Grocery Retailers 2 5 6 7 8 98

Convenience Stores 2 5 4 5 55 7

Independent Small Grocers - - 2 2 2 2

Forecourt Retailers - - - - 05 08

Other store-based retailing 2 2 2 2 2 23

Other Grocery Retailers 2 2 2 2 2 23

Non-Grocery Retailers - - - - - -

Non-Store Retailing - - - - - -

Vending - - - - - -

Homeshopping - - - - - -

Internet Retailing - - - - - -

Direct Selling - - - - - -

Mexico Better-For-You Market Sales

Growth for 2006-2007

126 125

405333

0

10

20

30

40

50

2006 2007

Year

Perc

en

tag

e Better-for-you

Packaged Food

Better-for-you

Beverages

PAGE 8

Companies and Brands

Of better-for-you food and beverages Coca Cola Co owned the largest company market share for 2007 at 21 The Danone Group held a good part of the business with 16 share as well as Pepsi Co which captured 152 of the Mexico market

The naturally healthy food and beverages category is dominated by Nestle SA with a 175 company share in 2007 Bimbo SA in second with 173 followed by Pepsi Co with 134 market share

Brand Shares (by Global Brand Name) Retail Sales breakdown

Brand Company name

(GBO) 2005 2006 2007

Diet Coke Coca-Cola Co The 158 143 145

Trident Cadbury Schweppes Plc

121 11 108

Leviteacute Danone Groupe 53 87 105

Be-light PepsiCo Inc 42 65 84

VitalineaVitasnellaTaillefine Danone Groupe

65 61 52

Ciel Coca-Cola Co The 16 34 45

Douglas PepsiCo Inc 34 37 38

Clight Kraft Foods Inc 41 37 37

Sveltesse Nestleacute SA 35 32 29

San Rafael Sigma Alimentos SA 37 32 28

Carnation Nestleacute SA 33 28 27

Zwan Sara Lee Corp 25 22 19

Noche Buena Sigma Alimentos SA de CV

19 17 16

Nescafeacute Nestleacute SA 19 17 15

Diet Pepsi PepsiCo Inc 19 15 13

Sprite Zero Coca-Cola Co The 12 14 12

Sabori Grupo Bafar 14 12 11

Pentildearanda Empacadora Campo Friacuteo SA de CV

14 12 11

Coca-Cola Zero Coca-Cola Co The - - 1

McCormick McCormick amp Co Inc 13 12 1

Bernina Empacadora Bernina SA de CV

13 11 1

Source Health and Wellness Sector Euromonitor International

PAGE 9

New Products

Over 2009 there were 1973 new better-for-you food products launched in Mexico Below are the