head office - capexil · head office “vanijya bhavan” international trade facilitation centre,...

TRANSCRIPT

1

2012February - March

HEAD OFFICE“Vanijya Bhavan” International TradeFacilitation Centre, 1/1, Wood Street, Kolkata - 700 016Tel : 91-33-2289-0524/25, to 23/1725Fax : 033-2289 1724Email : [email protected] / [email protected] : www.capexil.com

REGIONAL OFFICESWestern Region :‘Commerce Centre’, 4th Floor, Block No.D-17, Tardeo Road,Mumbai - 400 034 l IndiaTel : 91-22-2352 3410, 2352 0084 l Fax : 91-22-2351 6665Email : [email protected] / [email protected]

Eastern Region :“Vanijya Bhavan”, International Trade Facilitation Centre,1/1, Wood Street, 3rd Floor, Kolkata - 700 016 l IndiaTel : 91 - 33 - 2289-0524/25, 2289 - 1721 to 231/1725Fax : 033-2289 0537/1724Email : [email protected] / [email protected]

Northern Region :‘Vandana Building’, 11, Tolstoy Marg, 4th Floor,Flat No.4B, New Delhi - 110 001 l IndiaTel : 91-11-2335 6703, 2371 1479, 2376 2282Fax : 91-11-4486 l Email : [email protected]

Edited & Published byExecutive DirectorCAPEXIL, Vanijya Bhavan, Kolkata

Designed & Printed by :Timir Printing Works Pvt. Ltd.,Tel : 94333 63966 / 98301 65883

2 From Chairman’s Desk

3 Bilateral Trade & Business Environment in Nepal

4 Senior Expert, SES, Bonn, Germany VisitsCapexil’s Office at Kolkata

5 Seminar on “Export Market Challanges for IndianTimber Products”

9 Payment of Cheques/Drafts/Pay Orders/Banker’sCheques

10 India-Israel Bilateral Trade Statistics

12 New Restrictions on Imports to Argentina

13 Seminar on “Books Beyond the Borders”

15 Highlights of Union Budget 2012-13

16 Brazilian Calendar of Exhibitions and Fairs 2012

17 The New Delhi World Book Fair 2012

18 Agreement on Anti Dumping - Frequently askedquestions

22 Overseas Enquiries (February 2012)

26 Overseas Enquiries (March 2012)

30 New Members (February 2012)

31 New Members (March 2012)

CONTENTSFEBRUARY-MARCH 2012

2

Friends,

The year 2011-12 has just passedand we have now entered into anew fiscal year 2012-13 with newhopes and aspirations. The year2011-12 was somewhat difficult fortrade & industry as we noticeddecline in industrial expansion as

well as fall in export growth. The Indian economy hadto face constraints arising out of debt crisis inEuro Zone, rise in crude oil price, political turmoil inMiddle East and Earthquake in Japan and somedomestic factors. According to the economic survey ofthe Govt. of India, the country’s economy is expectedto grow at 6.9% in 2011-12 as compared to a growthof 8.4% in preceding two years. This slow down isattributed largely to weakening industrial growth.Agriculture and service sectors continued to performwell in 2011-12. As per the economic survey, despitethe low growth figure, India remains one of the fastestgrowing economies of the world as all major countriesincluding the fast growing emerging economies areseeing a significant slow down.

The preceding year also noticed high rate of inflationand as a result monetary policy was tightened byReserve Bank of India to control inflation and curbinflationary pressure. There was slowdown in inflationduring end of the year. Food inflation in particular hascome down to around zero. Headline inflation is expectedto moderate further in the next few months and remainstable thereafter. The Union Budget for 2012-13 hasalready been presented in the Parliament where stresshas been given to strengthen infrastructure and industrialdevelopment, attract Foreign Direct Investment. Stresshas also been given to improve the power sector andfor that matter customs duty on steam coal has beenremoved. The Finance Minister has also mentioned thatfrom August 2012, GST may come into force and DTCbill (Direct Tax Code) is likely to be enacted after dueconsultations. In the external trade, the country’sperformance was encouraging in the first half of theyear.

Gloomy economic scenario in major buying countriesof Europe, USA, deceleration in industrial growth hadsome effect on India’s export and as a result growth in

FROM CHAIRMAN’s DESK

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

export had declined to 3.87% in dollar terms duringNovember 2011. In fact, the country’s export growthwas high at 40.5% during 1st half of 2011-12 butthereafter seen deceleration in export growth.

Growth in export during February 2012 was only 4.28%in Dollar terms. Cumulative value of India’s exportduring April 2011 – February 2012 was US$ 267409.89million (Rs.1274839.70 crore) ) as against US$220241.12 million (Rs.1003784.83 crore), reflecting agrowth of 21.42% in Dollar terms and 27.0% in rupeeterms over the same period of last year. The aboveperiod’s export was quite satisfactory when we look atthe overall business scenario in our major buyingcountries.

On the other hand, during April – February 2011-12,India’s import was US$ 434159.81 mil l ion(Rs.2069642.80 crore) as against US$ 335502.15million (Rs.1529295.07 crore), registering a growth of29.41% in Dollar terms and 35.33% in rupee termsover the same period of last year. In fact, India’s tradedeficit during April – February 2011-12 was estimatedat US$ 166749.92 million as against the deficit of US$115261.03 million during April – February 2010-11.This increased trade deficit is a matter of concern.

Indian Rupee was under pressure during the year andas a result import intensive industries faced difficulty.As far as CAPEXIL is concerned, we are hopeful toachieve the target of US$ 17.09 billion fixed for 2011-12 and I request our members to take appropriatesteps to further raise their exports of CAPEXIL’s productline during 2012-13. The Council has already takenthe initiative to issue online RCMCs to its membersand I request our members to take advantage of onlineRCMCs, if not already taken and furnish export returnsonline to enable the Council draw up realistic exportestimates and export projections. Members are alsorequested to take part in CAPEXIL’s export promotionevents abroad with a view to diversify market baseand enlarge exports. Let us hope for a better businessin 2012-13 so that we may see higher export growth.

With warm regards,

C K Somany(Chairman, CAPEXIL)

3

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

I) Trade Volume : India is Nepal’s largest trade partner and source of foreign investment. India is also the onlytransit providing country for Nepal. The contribution of India in total Nepalese import was 66.3% amount toNRs.261631.2 million in the year 2010-11. Its total foreign trade with India in the same financial year stands tothe tune of NRs.304977.2 million which is 66.2% of the total foreign trade of Nepal. India has provided 15 specifiedland routes for transit trade and an additional 12 routes for bilateral trade. Majority of trade is however mainlycatered through five check posts viz. Raxaul – Birgunj, Jogbani – Biratnagar, Sunauli – Bhairhwa, TribhuvanInternational Airport – Kathmandu and also through Raxaul – ICD Birgunj which is the only rail linked ICD (InlandClearance Depot) in Nepal for both bilateral as well as third country goods. Out of this, Raxaul – Birgunj andRaxaul – ICD together constitutes almost 60% of bilateral trade.

Birgunj which is situated at the head of most industrialized hinterlands of Nepal because of its proximity to Raxaul– Birgunj trade route, availability of sufficient land, cheap labour from both India and Nepal and vibrant communityof entrepreneurs settled in this part. Many domestic and Indian joint ventures have their factory established inBirgunj – Pathlaiya Corridor. Pharmaceuticals, cement, iron & steel products, synaptic yarn, plastic, juices & foodproducts are some of the major items being manufactured in this part.

The trends of Indo – Nepal merchandize trade is as under :-

( in million US$ )

Nepal’s 2008-09 2009-10 2010-11

Export to India 536.09 536.54 599.77

Import from India 2123.64 2912.72 3620.19

Total trade with India 2659.73 3449.26 4219.96

(2008/09 = US$ 1 = NRs.76.49, 2009/10 = US$ 1 = NRs.74.54, 2010/11 = US$ 1 = NRs.72.27)

Over the years, Nepal’s trade with India has been continuously growing.

India’s share in Nepal’s foreign trade is as under :-

(in percentage )

India’s share : inNepal’s 2008-09 2009-10 2010-11

Export 60.6 65.8 67.1

Import 57.1 58.0 66.3

Total trade 57.8 59.1 66.4

Trade balance 56.0 56.5 66.1

BILATERAL TRADE & BUSINESS ENVIRONMENT IN NEPAL

4

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

II) Preferential Rates of Duties : The bilateral tradebetween India and Nepal is primarily governed byrevised treaty of trade signed in October 2009. Nepalesemanufactured products are allowed access to the Indianmarket, free of basic customs duty, on the basis ofCertificate of Origin issued by a Govt. of Nepaldesignated authority – FNCCI, if the goods aremanufactured in Nepal with Nepalese and/or Indianinputs ; or, with at least 30% local value addition, if thirdcountry inputs are used; and, involves substantialmanufacturing process leading to change in HSclassification at four- digit level.

Nepal provides a small rebate of 7% in the customsduty for imports from India upto a duty rate of 25% andrebate of 5% for duty rates above 25%. The treaty alsoprovides duty free access to primary products, but Nepallevies an Agriculture Development Fee (ADF) of 5% onimports from India.

Almost all goods are OGL (Open General Licence) andthe customs duty is calculated on CIF (Cost, Insurance

and Freight) basis on import. An amount of NRs.500/- as customs service fee is charged as per CustomsDeclaration Form (Pragyapan Patra) at Customs pointson import.

Bilateral trade takes place either in Indian Rupee orconvertible currency. Nepal’s Central Bank (NepalRashtra Bank) maintains a list of items that can beimported from India in convertible currency. Currently,136 items are in the list. Since 1993, the Nepal RashtraBank maintains a fixed exchange rate with IndianRupee (1 INR = 1.6 NPR). All other items are importedas per DRP (Duty Refund Procedure) specified in thetreaty of trade. This procedure is however, beingabolished w.e.f. 1st March, 2012. After that date allexports from India to Nepal will be eligible for exportincentives irrespective of the currency involved in thetrade. Scrapping of DRP is likely to substantially boostIndian export to Nepal.

Source: Consulate General of India, Birgunj, Nepal

Mr.Michael Blodig, Senior Expert of SES (SeniorExperten Service), BuschstraBe 2 53113 Bonn,Germany had visited CAPEXIL’s office at Kolkata on24th February, 2012 along with Mr. T. K. Hore, IndiaRepresentative of the said organization. Mr Blodig isa technical expert in the field of ceramics, refractories,clay bricks, etc. and he can extend technical assistance/guidance to such industries for development. Membersof the industry interested to seek his advice may sendmail to him at [email protected] and proposalsfor technical assistance may be sent direct to SES(Senior Experten Service),

BuschstraBe 2 53113 Bonn, Germany, Tel: +49 22826090-0, Fax: +49 228 26090-77, e-mail: [email protected], website: www.ses-bonn.de with a copy toMr. T K Hore, India representative, SES, SundaramBuilding, 46F, Rafi Ahmed Kidwai Road, 6th floor,Room 6C, Kolkata – 700 016, Phone : 033-2226-2866,Fax: 033-2226-2867, Mobile: +91-98300-23030, e-mail: [email protected] , website: www.ses-bonn.de .Mr. T K Hore, India Representative of the aboveorganization may also be contacted for preliminaryinformation on the services available from SES, Bonn,Germany.

SENIOR EXPERT, SES, BONN, GERMANY VISITSCAPEXIL’S OFFICE AT KOLKATA

SPEECH ON “EXPORT MARKET CHALLENGES FOR INDIAN TIMBER PRODUCTS”BY MR. B.H. PATEL, CHAIRMAN - PLYWOOD & ALLIED PRODUCTS PANEL, CAPEXIL

19TH ILLEGAL LOGGING STAKEHOLDER UPDATE, 10TH FEBRUARY 2012,CHATHAM HOUSE, 10 ST JAMES’S SQUARE, LONDON

5

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

Ladies and Gentlemen,

I consider it an honour & privilege to address this augustgathering of 19th Illegal Logging Stakeholder Updatein London on export market challenges for India’sTimber Products. I am keenly aware of the vastknowledge and experience embedded in the audienceand I am looking forward to a meaningful exchange ofideas.

Before we start, let us have a look at India’s EconomyParameters:-

India’s GDP Growth

In 2007-08 India’s GDP grew by 9.3%. Due to the globalfinancial crisis our growth rate in 2008-09 had sloweddown to 6.8 per cent. However, India was among thefew nations to recover earlier from the crisis. Our growthrate rose to 8.0% in 2009-10 and to 8.5 per cent in2010-11. Unfortunately, dark clouds have gathered inthe global skies once again, and these are casting ashadow on us. The Indian economy grew by 7.7 percent during April-June 2011. Agriculture, industry andservices registered growth rates of 3.9, 5.1 and 10 percent, respectively, in the first quarter.

Wood & Wood Based Industries in India

It may be noted here that the Wood and Wood basedIndustry play a very vital role in shaping the robustgrowth of the Indian Economy. This industry has truepotential to grow manifolds from the existing levels andis poised for a sustainable growth annually. The lastdecade has seen India fast become the manufacturinghub for the global markets. The Wood, Plywood & AlliedProducts Industry is one of the key sectors havingimmense potential for gaining from these developmentsas India is one of the major wood-users in the Asiapacific region. Asia Pacific region has over 4500 varietiesof wood-yielding species & has some of the best knownand most highly prized tropical hardwoods.

Indian plywood industry is as big as Rs.5,000 croreequivalent to USD 1 billion. The industry is growing atrapid pace of 10-20% per annum. Approximately 600units are currently functioning all over the country.There is tremendous growth potential as the playersare yet to penetrate majority of the international market.

Panel and plywood products are the main woodproducts in India. Product categories include veneersheets, particle board (composite wood core withplastic laminate finish), panel products (fiber board),plywood made from both hard and softwood (veneeredpanels and laminated woods), and medium densityfiber board. Indian particle board and plywood industryaccounts for 15% of the total production, producing,some 30 million sqm of plywood and block boards.

At present, the Indian wood & furniture sector ispredominantly in the hands of unorganized small units.Fortunately, large corporate houses have started takinginterest in production of modern furniture. The furnituremarket is the second largest wood processing segmentafter timber & logs, making India a fast emergingmarket for high-end, value-added imported products. The manufacture of pre-fabricated doors and windowsis relatively new and the current market is growing at10% per annum. The total annual market for timber &furniture in India is estimated to be US$ 1.25 billionabout 90% of which is for wooden products. Thebranded (higher quality) wooden furniture industry isgrowing at 15% annually.

Wood, Plywood and Panel Industry - US$157.97billion global opportunity

Let me inform you & you all may be aware that globalimports of Wood, Plywood and Panel Industry reachedto US $ 157.97 billion during 2010. The broad groupof the products exported globally under Wood, Plywoodand Panel Industry are Furniture and Parts (41%),Sawn Wood (19%), Plywood (7%), Builders’ joineryand carpentary of wood (7%), Fibre board of Wood

6

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

(5%), balance in Cork & Cork Products, Hard board ofwood fibre, other articles of wood, Parquet Panel andSandal wood Chips etc., as detailed below:-

Products Value in 2010 % Share(US$ Million)

Furniture and parts 63648 41

Sawn Wood 29761 19

Plywood 11343 7

Joinery & Carpentary of Wood 11140 7

Fibre board 8183 5

Others 33899 21

TOTAL 157973

Source: ITC Trade Map

Global Importers of Wood and Wood Articles(Chapter 44)

The main importing countries for Wood and Woodarticles into globally are USA (11%), China (10%),Japan (9.5%), Germany (6.1%), United Kingdom (4.6%),Italy (4.5%), France (4.2%), Netherlands (3.2%), Canada

Exports of Plywood and Wood Products from India

Value: Rs. Million

Products 2009-2010 2010-2011 % Change Export Destinations

Wooden furniture 11220.45 16207.13 44.44 USA, Germany & France

Other articles of wood 3546.03 4560.69 28.61 USA, UK & Canada

Sawn timber 687.34 831.15 20.92 UAE, Italy & Oman

Veneer 925.47 717.52 -22.47 Turkey, UAE & USA

Other plywood 674.00 566.16 -16.00 Turkey, UAE & Netherlands

Hard board of wood fibre 583.46 486.17 -16.68 UAE, Saudi Arabia & Qatar

Cork and cork products 53.98 116.23 115.34 USA, UAE & Russia

Sandalwood chips 50.57 92.84 83.58 UAE, Malaysia & Saudi Arabia

Decorative plywood 152.92 33.50 -78.10 Nepal, Canada & Turkey

Tea chest panel 1.34 0.98 -26.51 Nepal, Germany & Japan

Grand Total 17895.55 23612.36 31.95

Source: MoC Export Import Data Bank

(2.8%), Belgium (2.6%), Netherlands (2.5%), Austria(2.4%) and Rep. of Korea (2.1%).

The major markets for Indian furniture’s (Bedroom,Kitchen and Office furniture’s) in the world are USA,UK, France, Switzerland, Canada and Netherlands. China, USA, Japan, UK, Italy, Germany and Franceare the leading importers for Sawn wood. France,USA, Spain, Italy, Germany, Russian Federation, Chile,China and Japan are the leading importers for Corkand Cork Products in the world.

Exports of Plywood, Wood and Panel productsfrom India

I am happy to inform you that the exports of wood andwood products from India has reached to all time highof US $ 453 million during 2010-11 showing a growthof 20% compared to previous year. For the past 4years, exports of timber products growing an averageof Compounded Annual Growth Rate (CAGR) of over7% from India. The major export destinations for IndianPlywood and Wood Products are USA (23%), Germany(10%), UK (9%), France (7%), UAE (7%), Italy (4%),Netherlands (3%), Australia (3%), Belgium (3%) andSpain (2%), as per the table given below :-

7

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

Now I would briefly address the Export MarketChal lenges for India’s Timber Products

a. Globalization

With the globalization & opening of economy, there areentry of very well known multinational brands in India,many products and services are now delivered toconsumers in a similar way across the world andconsumers are now aware of trends, tastes and fashionsas in other parts of the world. These developmentspresent opportunities to increase efficiency in the deliveryof products and services across a much larger globalmarketplace as well as they also enable firms to gaincompetitive advantage through overseas marketknowledge, product differentiation and the developmentof local market niches. This globalization is posing bigchallenges for exports of timber products from India toacross the globe. Consumers expect high qualitymaterials at par with international standards particularlywith various certifications in place.

b. Forest product certification

Forest product certification was developed during the1990s as a mechanism to identify forest products thatcome from sustainably managed forests. Four mainelements of the certification process are: thedevelopment of agreed standards defining sustainableforest management; auditing of forest operations andissuance of certificates to companies that meet thosestandards; auditing of the chain-of-custody to ensurethat a company’s products come from certified forests;and the use of product labels so that certified productscan be identified in the marketplace. There are presentlymore than 50 certification programmes in differentcountries around the world, many of which fall underthe two largest umbrella organizations: the ForestStewardship Council (FSC) and the Programme for theEndorsement of Forest Certification (PEFC). The areaof certified forests covered by the two main organizationshas steadily increased since the 1990s to reach about350 million hectares in 2010.

Globally a number of barriers to more widespreadadoption of certification have been identified. Two ofthe most important of these are the costs of certification(especially for small forest owners) and the lack of aprice premium for certified forest products in themarketplace. Although the latter has been noted in

almost all developed country markets for forest products,one benefit of certification is that it facilitates entry tothose markets, where prices generally may be higherthan in countries where there is no demand for certifiedforest products.

Although forest certification has so far failed to stimulatewidespread changes in forest management andharvesting practices in all parts of the world, it remainsan important tool for companies in the forest industryto demonstrate their commitment to meeting high socialand environmental performance standards. Indeed,many of the largest forest products companies arecertified and can use this to gain competitive advantageby differentiating their products and communicatingtheir superior performance to consumers. The majorexporting countries of logs are still to get the forestcertification & hence it is difficult to get certified logs.

Due to this, Indian exporters cannot supply certifiedwood products. Further, this certification adds to thecost of production to a great extent which stands alone,will not be competitive internationally.

c. Understanding and meeting customers’ needs

Making the wood and wood products more customer-focused and responsive to changing needs is one ofour biggest challenges. The wood and wood industryremains very conservative in comparison with manyother consumer product markets and it’s essential thatmanufacturers and merchants become more dynamicand attuned to market trends and customerrequirements. Globally, the price-conscious customersadopting a more cautious approach to committing tosignificant home improvement projects. This shift indemand means that quality becomes even moreimportant, as customers purchasing premium woodand wood products have higher expectations of design,finish and durability, as well as service and after-salessupport.

d. Increasing competition from other Asiancountries

Indian producers are facing increasingly higher amountof competition particularly from other Asian countriesof China and Vietnam and wooden furniture in particular. Since the manufacturing of plywood, furniture/veneersetc. are labour intensive processes in India and whereas

8

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

a good number of jobs are being created for export ofthese products. Industries in India are still to beorganized & need huge investment & technical supportin the form of technology, plant & machineries, education& training. There is substantial quality difference ininternational products compared to domestic products.This is also a big challenge for Indian Exporters toimprove as per international market demand &standards.

e. Use of Alternative materials to Wood

Perhaps the biggest challenge for the wood and woodindustry as a whole is to position the material ascomplementary to modern homes, were alternativematerials such as metal and glass are nowcommonplace within shelves, storage units, tables,chairs and other furniture. Customers are including awhole range of different materials, finishes and textureswithin their homes, and wood and wooden manufacturersand merchants need to innovate to either integratethese materials within their ranges or design wood andwood products to complement them. The wood andwood products industry in India need to understandand respond to these changing needs if it is to growand compete with other consumer product suppliers.

f. Increasing labour costs and Automation

In India, both wood raw materials and skilled labour arenow in short supply. Because labour was cheap inIndia the wood and wood industry developed usinglabour intensive production processes. Today however,the situation is different and because of low cost labouris no longer readily available many factories are runningat around only 60% of their capacity. To overcome thispersistent problem the industry now prefers to have asmuch automation as possible and is retooling productionplant accordingly. This change is driving up demandfor high tech wood processing equipment.

g. Social trends & Domestic Market Scenario

Social trends changes public opinions, attitudes andlifestyles that occur when income rises. For example,as income increases, people move beyond basic needsand start to seek new products and services that willimprove their quality of life, according to their tastesand preferences. Other wealth related factors also affectconsumption, such as increases in home ownership

(including second homes), trends towards larger homesand greater leisure time, as well as changes in theamount of time spent at home. This creates anadditional demand for the domestic market & thus thesurplus available for the export reduces. There are lotsof pressure on forest land & resources as demand forconstruction for new homes increases.

Secondly, India is experiencing a rapid phase ofurbanization with a change in lifestyles, a growingdemand for engineered wood panel products, and ahigh infrastructure, industry sources expect positivegrowth for wood products such as plywood,particleboard, medium density fiberboard, oriented-strand board and laminated veneer lumber in nearfuture. Therefore manufacturers are not really willingto export when they have readymade domestic marketto cater. There is huge young population aging between18 – 40 years in India adopting high quality of lifestandards with high income group & having morespending power. Therefore, the domestic market isquite strong & housing sector & other relevant industriesare booming. This affects exporters to decide betweendomestic market & export market.

h. Lack of Market Information

In India, there is no proper market information systemto provide the prevailing price on wood on a day-to-day basis, nor is there any support price fixed by theGovernment as has been the case in agriculturalproducts. Indian exporters need to participate in everypossible wood fairs & exhibitions to get first handinformation on market & recent trends. This also helpsin upgrading plant & machinery & brings about latesttechnology in wood industry.

The other major challenges for the Indian exporterscan be summarized as under:-

l There has been acute shortage of good rawmaterial as wood is the natural commodity. Thecustomers demand for high quality of productsat higher rate for which the exporters need toprocure best quality of raw material to ensurequality specification & to meet customersexpectation.

l For technology upgradation & modernization,huge capital & resources are required which is

9

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

difficult for small & medium size exporters.

l Shipping has become critical aspect as most ofthe raw materials are imported from Africancountries where container facility is not available& the cargo has to come in break bulk whichinvolves huge finance & forex risk & alsoincreases transaction cost.

l India is still lacking in developing propermarketing strategies to penetrate theinternational market & to sustain against cutthroat competition, as exporters need to haveunited efforts to meet ever-changing marketchallenges.

Conclusion

It may be recalled here that Asia is one of the mostinteresting dynamic and fastest growing markets in theindustry, and China in particular, thanks to its incredibleeconomic prosperity. The region is becoming one of

the most important areas in the world for furnituremanufacturing. The development of demanding, qualityorientated industries such as furniture manufacturingand interior decoration will ensure a steady andpromising flow of business among India and otherAsian countries for years to come.

Before concluding my speech, I would also like tohighlight that there has been very strict legal framework, rules & regulations for fair trade of timber productsin India. The Indian entrepreneurs are required tomaintain complete records, to fulfill all the formalitiesas well as to ensure full chain of custody from forestto final delivery of finished products to overseascustomers. Thus there is no scope of illegal trading oftimber products in India. The experience of concernedauthorities to implement FSC & other certificationprocess in India, has been quite satisfactory & theyare impressed with the transparent & straightforwardway of doing the business by Indian exporters.

PAYMENT OF CHEQUES/DRAFTS/PAY ORDERS/BANKER’S CHEQUES

1. In India, it has been the usual practice amongbankers to make payment of only such chequesand drafts as are presented for payment within aperiod of six months from the date of the instrument.

2. It has been brought to the notice of ReserveBank by Government of India that some personsare taking undue advantage of the said practiceof banks of making payment of cheques/drafts/payorders/ banker's cheques presented within a periodof six months from the date of the instrument asthese instruments are being circulated in the marketlike cash for six months. Reserve Bank is satisfiedthat in public interest and in the interest of bankingpolicy it is necessary to reduce the period withinwhich cheques/drafts/pay orders/ banker's chequesare presented for payment from six months tothree months from the date of such instrument.

Accordingly, in exercise of the powers conferredby Section 35A of the Banking Regulation Act,1949, Reserve Bank hereby directs that with effectfrom April 1, 2012, banks should not make paymentof cheques/drafts/pay orders/banker's chequesbearing that date or any subsequent date, if theyare presented beyond the period of three monthsfrom the date of such instrument.

3. Banks should ensure strict compliance of thesedirections and notify the holders of such instrumentsof the change in practice by printing or stamping onthe cheque leaves, drafts, pay orders and banker'scheques issued on or after April 1, 2012, by issuingsuitable instruction for presentment within the periodof three months from the date of the instrument.

Source : RBI, Mumbai Circular No.RBI/2011-12/251(DBOD.AML BC No.47/14.01.001/2011-12)

dated 4.11.2011

10

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

Bilateral Trade in December 2011 (in US$ millions)

India’s Exports Israel’s Exports Total Bilateral trade % change **

169.4 341.7 511.1 + 30.58% ( from $ 391.4 )

* Source: Israel Central Bureau of Statistics (CBS). * *Compared to Dec 2010.

Bilateral Trade during January- December 2011 (in US$ millions)

India’s Exports Israel’s Exports Total Bilateral trade % change **

2154.5 2998.5 5153 + 8.8% (from $ 4736)

* Source: Israel Central Bureau of Statistics (CBS). ** Compared to Jan-Dec 2010.

Analysis of Trade Figures

(A) In 2011 Balance of trade between Israel and India, was in Israel’s favor by US$ 844 Million.

(B) In 2011, India was ranked the 8th largest trade partner of Israel in the world, and the 3rd largest trade partnerin Asia following China and Hong Kong (*Trade data includes diamonds. ** CBS gives separate trade data forHong Kong although it is part of China).

(C) India’s share in Israel’s two way global trade decreased from 4.02% (in 2010) to 3.66% (in 2011).

In 2011:

- India is ranked 5th largest export destination of Israel (including diamonds) and 7th when excluding diamonds.

- India is ranked 11th largest import source of Israel including diamonds, and 16th largest import source excludingdiamonds.

In the month of December 2011:

- Israel’s two-way global trade increased by 1.57% from US$ 10974.2 million in December 2010 to US$ 11,114.2million in December 2011. India’s share in Israel’s two-way global trade increased from 3.56% in December2010 to 4.65% in December 2011.

(D) Israel’s top trade partners in Jan- Dec 2011

Israel’s top trade partners in Jan- Dec 2011 (in US$ billions)

USA Belgium China Hong Kong Germany Switzerland UK India Netherlands Italy

28.069 8.217 8.157 7.189 6.506 5.407 6.154 5.153 4.428 4.889

* Source: Israel Central Bureau of Statistics ** Trade data including diamonds.

INDIA-ISRAEL BILATERAL TRADE STATISTICS

11

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

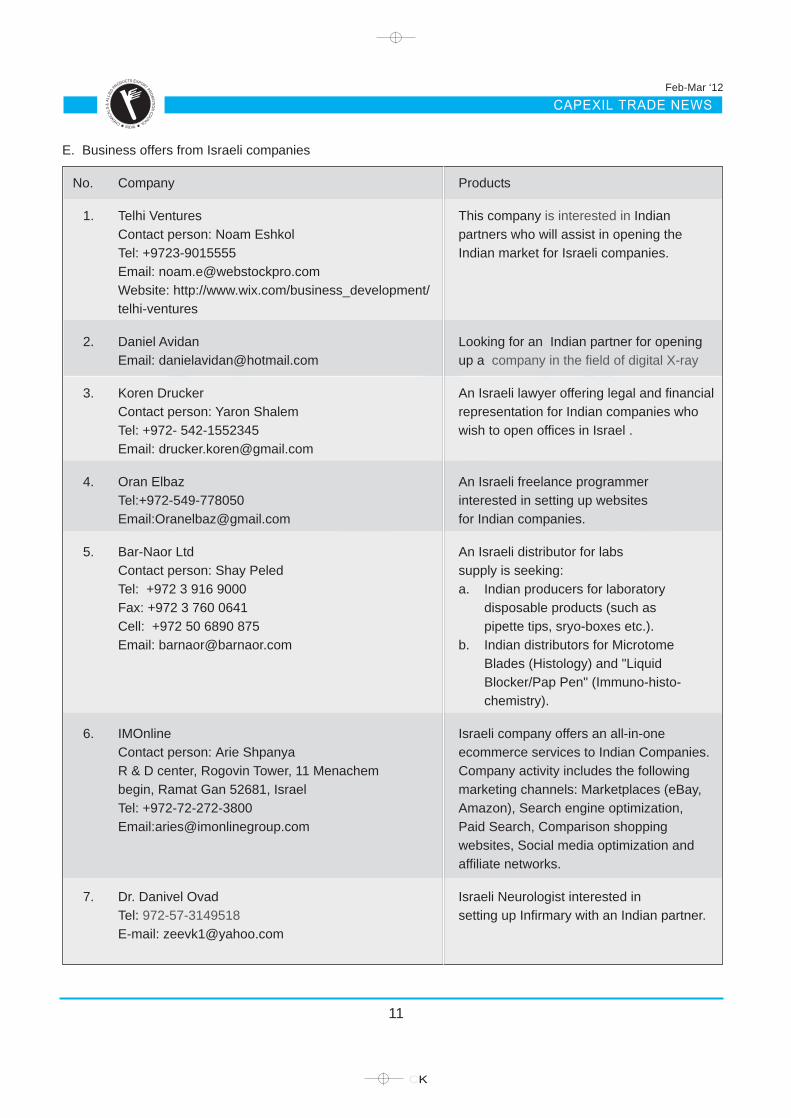

E. Business offers from Israeli companies

No. Company Products

1. Telhi Ventures This company is interested in IndianContact person: Noam Eshkol partners who will assist in opening theTel: +9723-9015555 Indian market for Israeli companies.Email: [email protected]: http://www.wix.com/business_development/telhi-ventures

2. Daniel Avidan Looking for an Indian partner for openingEmail: [email protected] up a company in the field of digital X-ray

3. Koren Drucker An Israeli lawyer offering legal and financialContact person: Yaron Shalem representation for Indian companies whoTel: +972- 542-1552345 wish to open offices in Israel .Email: [email protected]

4. Oran Elbaz An Israeli freelance programmerTel:+972-549-778050 interested in setting up websitesEmail:[email protected] for Indian companies.

5. Bar-Naor Ltd An Israeli distributor for labsContact person: Shay Peled supply is seeking:Tel: +972 3 916 9000 a. Indian producers for laboratoryFax: +972 3 760 0641 disposable products (such asCell: +972 50 6890 875 pipette tips, sryo-boxes etc.).Email: [email protected] b. Indian distributors for Microtome

Blades (Histology) and "LiquidBlocker/Pap Pen" (Immuno-histo-chemistry).

6. IMOnline Israeli company offers an all-in-oneContact person: Arie Shpanya ecommerce services to Indian Companies.R & D center, Rogovin Tower, 11 Menachem Company activity includes the followingbegin, Ramat Gan 52681, Israel marketing channels: Marketplaces (eBay,Tel: +972-72-272-3800 Amazon), Search engine optimization,Email:[email protected] Paid Search, Comparison shopping

websites, Social media optimization andaffiliate networks.

7. Dr. Danivel Ovad Israeli Neurologist interested inTel: 972-57-3149518 setting up Infirmary with an Indian partner.E-mail: [email protected]

12

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

Major bilalteral economic and commercialdevelopments :

1. The Israeli Ports Company and the Indian CompanyCargo Motors won an international tender for constructionof a new container port in the state of Gujarat , for atotal of $600 Million. The port will be constructed 150Km North of Mumbai. HANI (The Israeli Ports Company)will hold 26% of its stocks. This is a B.O.T project wherethe concessionaire who will construct the port, willoperate the port for 30 years, in return for different tolls.Upon the end of this period, the concessionaire will

handover the port to the state for an agreed amount,as per the contract. The concessionaire is requestedto complete financial aspects of the project within 18months.

2. Government of India has given approval to the Stateof Israel to open a new Consulate of the state of Israelin the city of Bangalore , India 's Silicon Valley tostrengthen ongoing Hi-tech cooperation. This wasannounced during the visit to Israel of Mr. S.M. Krishna,India's Minister of External Affairs, during January 2012.

The Resolution 3252 from Federal Public TaxAdministration (AFIP), published in Boletin Oficial(Official Gazette) on January 10, 2012 states that allArgentine importers registered at the Argentine Customswill have to comply with the new import guidelines thathave come into effect from February 1st 2012. Thesemainly deal with the with the information regimeregarding the destination of the imports of goods intothe country.

Prior to placing any order or any other operationregarding purchase of goods from overseas, the importerwill have to file a Declaracion Jurada Anticipada deImportacion (Anticipated Import Affidavit.) with theSecretariat of Foreign Trade. This will be examined forapproval or rejection.

Later the Federal Public Tax Administration AFIP willcommunicate to the applicant importer through thesystem online MOA Mis Operaciones Aduaneras (MyCustoms Operations) the result of their petition.

In case of rejection, the importer will be informed thereasons and will have the opportunity to make thecorrections indicated by the Secretary of Foreign Tradein order to be able to get the approval.

NEW RESTRICTIONS ON IMPORTS TO ARGENTINA

In case of approval, the importer will be able to preparethe documents for the final import, quoting the numberof his Anticipated Import Affidavit. At the same time hewill have to furnish to the Central Bank through theSystem of Control of Exchange Operations the numberof his approved Anticipated Import Affidavit so he canmake the money in foreign exchange transfer to theexporter.

With these the Argentine import restrictions havebecome even more stringent as part of the governmentpolicy to save foreign exchange and to promotedomestic manufacturing in these times of globaluncertainty. These restrictions apply to imports of allgoods and from all the countries including Mercosurpartners and they are not are not country specificnor product specific.

While the restrictions are arbitrary and non transparent,the same are being implemented through persuasionand reportedly indirect threats to importers. The approvalof any request filed for import of any good from anycountry would fully depend on the importers abilityto satisfy the conditions put forward by the Secretariatof Foreign Trade.

13

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

SEMINAR ON “BOOKS BEYOND THE BORDERS” ORGANIZED BY CAPEXIL BOOKDIVISION IN ASSOCIATION WITH PUBLISHERS & BOOKSELLERS GUILD, KOLKATAON 3RD FEBRUARY, 2012 AT UNITED BANK AUDITORIUM, MILAN MELA COMPLEX,

KOLKATA BOOK FAIR GROUND, KOLKATA

CAPEXIL Book Division in association with Publishers& Booksellers Guild, Kolkata had organized a seminaron “Books Beyond the Borders” on 3rd February, 2012at the United Bank Auditorium, Milan Mela Complex,Kolkata Book Fair ground, Kolkata. The subject mattersdealt in this seminar were book trade with Latin Americancountries by Dr. Dibyajyoti Mukhopadhyay, export ofbooks, publications and printing in SAARC and SouthEast Asia by Mr. Amitabha Sen, Member - EasternRegional Committee of CAPEXIL, print exports fromIndia by Mr. Ranjan Kothari, President of All IndiaFederation of Master Printers and CAPEXIL and itsservices to books, publications & printing industry byMr. J K Bagchi, Director, CAPEXIL (Eastern Region),Kolkata. The export awareness seminar was inauguratedby Mr. Ramesh K Mittal, Chairman – Books, Publications& Printing Panel of CAPEXIL. In his welcome addressMr. Mittal touched upon the areas to be covered in thisawareness programme for the benefit of book publishingtrade. He thereafter introduced the speakers before theaudience and thereafter the seminar started withpresentation by Dr. Dibyajyoti Mukhopadhyay on thetopic of Book Trade with Latin American Countries.

Dr. Dibyajyoti Mukhopadhyay mentioned about sharpincrease in export of books & publications to LatinAmerican countries during 2009-10 to 2010-11. Heindicated about good scope for developing export ofbooks & publications to Mexico particularly translationrights. He also mentioned that Latin America beingmostly Spanish speaking area except Brazil offers gooddemand for Indian text books.

Mr. Amitabha Sen in his presentation mentioned aboutscope of export of books & publications to SAARCcountries with special reference to Maldives, Sri Lanka,Bangladesh and Pakistan. Mr. Sen mentioned aboutvery high rate of literacy in Maldives though theirpopulation is very small as compared to other SAARCcountries. In Sri Lanka also, literacy rate is high andour text books are in good demand there. In the case

of Pakistan and Bangladesh, there is a problem ofpiracy and as such our exporters should work out pricingfor their books & publications in a manner which shouldnot influence or encourage local trade in those countriesto go in for pirated version. In the case of Pakistan thecustoms procedure for export of books is cumbersomeand he cautioned the members to be careful on thecontents of published material to exclude any sensitivematter related to religion, culture, obscene, etc. He alsosuggested our book publishing trade to considerparticipation in 2/3 major book fairs in Pakistan viz.Karachi Book Fair and Lahore Book Fair. The localpeople in the country have interest for Indian booksand our book publishing trade may get good resultsout of participation in the said two fairs. According toMr. Sen, it is very difficult to get advance payment fromPakistan for supply of goods from India. Urdu andPunjabi books have large market in Pakistan and Indiahas advantage in this area because no other countriesare producing books in these languages.

As regards Bangladesh, our export has increased fromUS$ 2.1 million in 2006-07 to US$ 2.3 million in 2008-09. There is problem in realization of payment fromBangladesh because books are considered as lowpriority items. There is shortage of text books in thecountry and piracy is also rampant. Our exporters maytherefore take adequate safeguard measures forrecovery of payment. Eastern India has an addedadvantage of being able to export Bengali languagebooks to Bangladesh since it is their national language.

Mr. Ranjan Kothari in his address highlighted that notebooks & diaries have good export growth potential.Scope also exists for expanding business on supply ofprinted materials as also getting printing works donein the overseas countries to meet short time schedulefor execution of bulk printing orders. For instance, inAfghanistan, it is possible to get large volume printorders for delivery within such short time which is rathertoo difficult for our printers to maintain delivery schedule.

14CHEMIC

ALS

&A

LLIE

D

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

In this situation setting up of a printing unit in Afghanistanmay be useful to service such large volume orders atshort notice. Another potential area identified byMr Kothari is printing of credit cards, scratch card,lottery tickets, hologram, etc.

Mr. J K Bagchi, Director, Capexil through power pointpresentation narrated about “CAPEXIL and its activities”.Mr. Bagchi mentioned that CAPEXIL, a trade promotionbody under the aegis of Ministry of Commerce &Industry, Govt. of India is the registering authority forexport of chemical based & allied products includingminerals & ores. Set up in 1958, CAPEXIL has todayemerged as a mega trade promotion body in the country.He mentioned about categories of membership, feesstructure, etc. as well as the type of services offeredto Indian exporters as well as overseas importers. Onthe other hand, export of CAPEXIL's product line during2009-10 & 2010-11 was US$ 13.13 billion and US$16.41 billion respectively. In fact, growth in export indollar terms was 25%. Export of books, publicationsand printing including printed materials during 2009-10 & 2010-11 was Rs.9444.5 million and Rs.10532.6million respectively. In fact, growth in export of books,publications and printing during 2010-11 was 16% indollar term and 12% in rupee term. In his address,Mr. Bagchi also mentioned that out of the total exportof books & publications panel, the major share of exportduring 2010-11 was books & pamphlets nearly 77.8%and printed material 17.45%. He also highlighted theexport trend of the panel from Rs.80.76 million in 1980-81 to Rs.10532.6 million in 2010-11.

In the promotional front, CAPEXIL organize exportpromotion events in specific regions abroad includingFocus regions viz. Latin America, Africa, CIS countriesand ASEAN +2 under MDA related activities of theMinistry of Commerce & Industry, Govt. of India. TheCouncil also takes part in major international fairsabroad as well as some domestic fairs. Mr. Bagchiexplained about the quantum of assistance availableunder MDA scheme for participation in above types ofevents abroad. He also mentioned about Market AccessInitiative scheme of the Ministry of Commerce & industry,Govt. of India where 65% subsidy on stand rentalcharges may be available to the members participatingin an international event organized by CAPEXIL.Financial support is also available for inviting foreignbuyers in reverse buyer seller meets organized by

CAPEXIL within the country. Mr. Bagchi mentioned thata member can undertake maximum five overseas tripsin a financial year covering four Focus regions and oneGeneral Area Country subject to fulfilment of theconditions as laid down in the MDA scheme. In thisarea, assistance is available on stand rental/ participationfee and economy excursion class air fare.

As for 2012-13, the Council has ambitious plan toorganize participation of its members indexed to books& publications panel in the following six internationalfairs and for that matter the Council has requestedDepartment of Commerce, Govt. of India for givingapproval under MDA related activity :-

1. London Book Fair 2012.

2. Nigeria International Book Fair 2012

3. Singapore Book Fair 2012

4. Cape Town Book Fair 2012

5. Frankfurt Book Fair 2012

6. Guadalajara International Book Fair 2012

At the close of the seminar, members raised a fewquestions on Foreign Trade Policy issues. Mr. Mittalsuggested for enhancement or removal of value CAPunder duty drawback scheme in respect of books whichis at present 1% with a value cap of Rs.5/- per Kg.Mr. Mittal informed the members that CAPEXIL isorganizing 3rd Reverse Buyer-Seller Meet on 22nd &23rd February, 2012 at Jaipur for members of bookdivision by inviting at least 15 plus importers from Focuscountries like Africa, Association of South East AsianNations (ASEAN+2) and LAC under the MAI Schemeof Ministry of Commerce & Industry, Govt. of India forone to one interaction with our members. The Councilhas already issued circular among all members of thepanel inviting their participation in this RBSM for oneto one discussion with overseas buyers/customers.

Before close of the awareness seminar, Mr. RameshK. Mittal, Chairman – Books, Publications and PrintingPanel of CAPEXIL proposed vote of thanks to themembers present in the seminar, Publishers &Booksellers Guild for their co-operation and associationin this programme. He specially thanked the speakersfor their valued presentation which has enriched themembers. He also mentioned about the importance ofKolkata Book Fair for the book publishing trade andappreciated the overwhelming response by the commonpeople of this region.

15

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

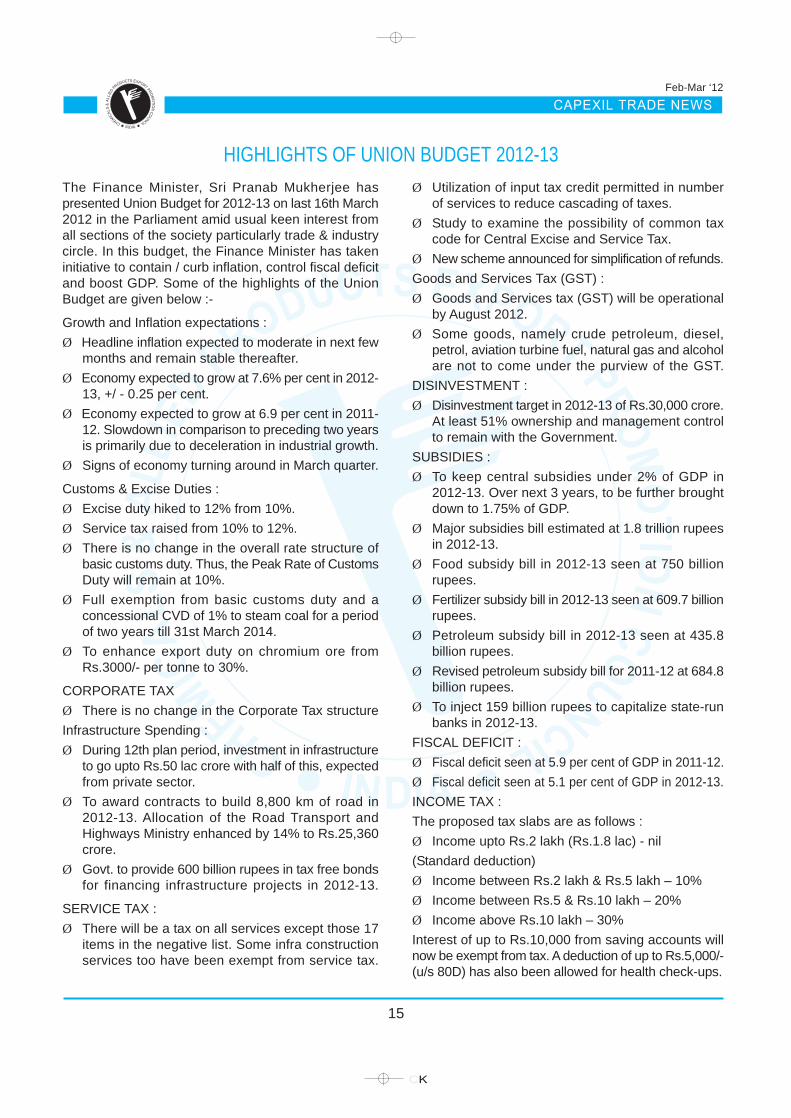

The Finance Minister, Sri Pranab Mukherjee haspresented Union Budget for 2012-13 on last 16th March2012 in the Parliament amid usual keen interest fromall sections of the society particularly trade & industrycircle. In this budget, the Finance Minister has takeninitiative to contain / curb inflation, control fiscal deficitand boost GDP. Some of the highlights of the UnionBudget are given below :-

Growth and Inflation expectations :Ø Headline inflation expected to moderate in next few

months and remain stable thereafter.Ø Economy expected to grow at 7.6% per cent in 2012-

13, +/ - 0.25 per cent.Ø Economy expected to grow at 6.9 per cent in 2011-

12. Slowdown in comparison to preceding two yearsis primarily due to deceleration in industrial growth.

Ø Signs of economy turning around in March quarter.

Customs & Excise Duties :Ø Excise duty hiked to 12% from 10%.Ø Service tax raised from 10% to 12%.Ø There is no change in the overall rate structure of

basic customs duty. Thus, the Peak Rate of CustomsDuty will remain at 10%.

Ø Full exemption from basic customs duty and aconcessional CVD of 1% to steam coal for a periodof two years till 31st March 2014.

Ø To enhance export duty on chromium ore fromRs.3000/- per tonne to 30%.

CORPORATE TAXØ There is no change in the Corporate Tax structureInfrastructure Spending :Ø During 12th plan period, investment in infrastructure

to go upto Rs.50 lac crore with half of this, expectedfrom private sector.

Ø To award contracts to build 8,800 km of road in2012-13. Allocation of the Road Transport andHighways Ministry enhanced by 14% to Rs.25,360crore.

Ø Govt. to provide 600 billion rupees in tax free bondsfor financing infrastructure projects in 2012-13.

SERVICE TAX :Ø There will be a tax on all services except those 17

items in the negative list. Some infra constructionservices too have been exempt from service tax.

Ø Utilization of input tax credit permitted in numberof services to reduce cascading of taxes.

Ø Study to examine the possibility of common taxcode for Central Excise and Service Tax.

Ø New scheme announced for simplification of refunds.Goods and Services Tax (GST) :Ø Goods and Services tax (GST) will be operational

by August 2012.Ø Some goods, namely crude petroleum, diesel,

petrol, aviation turbine fuel, natural gas and alcoholare not to come under the purview of the GST.

DISINVESTMENT :Ø Disinvestment target in 2012-13 of Rs.30,000 crore.

At least 51% ownership and management controlto remain with the Government.

SUBSIDIES :Ø To keep central subsidies under 2% of GDP in

2012-13. Over next 3 years, to be further broughtdown to 1.75% of GDP.

Ø Major subsidies bill estimated at 1.8 trillion rupeesin 2012-13.

Ø Food subsidy bill in 2012-13 seen at 750 billionrupees.

Ø Fertilizer subsidy bill in 2012-13 seen at 609.7 billionrupees.

Ø Petroleum subsidy bill in 2012-13 seen at 435.8billion rupees.

Ø Revised petroleum subsidy bill for 2011-12 at 684.8billion rupees.

Ø To inject 159 billion rupees to capitalize state-runbanks in 2012-13.

FISCAL DEFICIT :Ø Fiscal deficit seen at 5.9 per cent of GDP in 2011-12.Ø Fiscal deficit seen at 5.1 per cent of GDP in 2012-13.INCOME TAX :The proposed tax slabs are as follows :Ø Income upto Rs.2 lakh (Rs.1.8 lac) - nil(Standard deduction)Ø Income between Rs.2 lakh & Rs.5 lakh – 10%Ø Income between Rs.5 & Rs.10 lakh – 20%Ø Income above Rs.10 lakh – 30%Interest of up to Rs.10,000 from saving accounts willnow be exempt from tax. A deduction of up to Rs.5,000/-(u/s 80D) has also been allowed for health check-ups.

HIGHLIGHTS OF UNION BUDGET 2012-13

16

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

The Brazilian Calendar of Exhibition and Fairs is a jointpublication of the Department for Trade and ServicesPolicies (DECOS) of the Secretariat of Trade andServices (SCS), Ministry of Development, Industry, andForeign Trade (MDIC), and the Trade and InvestmentPromotion Department (DPR) of the Undersecretary-General for Cooperation, Culture, and Trade Promotion(SGEC), Ministry of External Relations (MRE). Thepartnership between the two Ministries was launchedthrough creation of the Standing Inter-Ministerial WorkingGroup provided for under Directive No. 5 of January11, 2008. The Calendar does not constitute acomprehensive list of all the companies or entitiespromoting events in Brazil, nor does it encompass thefull range of events organized in the country. Indeed,many others of equal excellence in terms of organization,quality, and reliability are sponsored throughout Brazilevery year. The events listed in this publications weresubmitted by the respective organizers and sponsors.The information provided in these pages is the sole andexclusive responsibility of the organizing companiesand entities. Additional information may be obtainedthrough the official Web sites of the events and/ororganizing companies or entities, the addresses andtelephones for which are provided at the end of thispublication This publication is distributed free of charge.The information in these pages is also available atwww.mdic.gov.br and www.brasilglobalnet.gov.br.

Ministry of Development, Industry,and Foreign Trade

Secretariat of Trade and ServicesDepartment of Trade and Services Policy

Esplanada dos Ministé'erios, bloco J, sala 30070053-900 - Brasília-DF

Telephone: +55 (61) 2027-7604 / 2027-7605www.mdic.gov.br

Ministry of External RelationsUnder Secretariat-General for Cooperation, Culture,

and Trade Promotion and Investment PromotionDepartment

Esplanada dos Ministé'erios, bloco H, Anexo 1, sala523

70170-900 - Brasília-DFTelephone: +55 (61) 3411-8960

INTRODUCTIONThe Brazilian Calendar of Exhibitions and Fairs is anofficial publication of the Brazilian Government.Published annually since 1969, this year’s editionincludes 365 events, more than in any previous edition,reflecting the rich diversity of the country’s economy,extending over a broad range of productive activitiesfrom arts and crafts production to information technology.A joint effort of the private initiative and the publicsector, the Calendar is organized and distributed freeof charge in Brazil and abroad by the Ministry ofDevelopment, Industry, and Foreign Trade (MDIC) andthe Ministry of External Relations (MRE). The 2012 edition was compiled using the MDIC’s Fairsand Exhibition System as well as the MRE’s tradepromotion portal, BrasilGlobalNet. Companies andevent organizers registered voluntarily on the two sitesand inserted the information on the events listed in the2012 Edition. In addition to the English version, theCalendar has been translated into a number oflanguages, including Arabic, Spanish, French, Mandarin,and Russian.The print version of the Catalogue is distributedthroughout Brazil to event promoters, companies, localgovernments, hotels, chambers of commerce, privatesector trade associations, public organizations,convention centers, consulates, embassies, and anyindividual or legal entity with an interest in receiving acopy. Outside Brazil, the Catalogue is distributedprimarily by the Trade Promotion Offices of Brazil’sEmbassies and Consulates and by representatives ofthe Brazilian Government at international events.The publication is also available online at www.mdic.gov.br and www.brasilglobalnet.gov.br. Through thesesites, specific events may be located using a range offilters, including “date,” “event name,” “industry,” and/or“venue.”The Calendar serves as a valuable tool for Brazilianand foreign entrepreneurs, providing a multiplicity ofevents with the potential to create new businessopportunities. The fairs offer the chance to learn aboutnew technologies, develop commercial strategies,enhance competitiveness in an increasingly demandingglobal market, in addition to promoting business tourismand contributing to economic growth across the country.Success in your research and business!

Source : Ministry of Comemrce & Industry,Foreign Trade (LAC), Govt. of India.

BRAZILIAN CALENDAR OF EXHIBITIONS AND FAIRS 2012

17

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

The 20th edition of the New Delhi World Book Fair (25February – 4 March 2012) was organized by NationalBook Trust, India at Pragati Maidan, New Delhi. It’s amajor calendar event for book lovers. Beside otherthings it showcased the diversity of one of the largestpublishing industry in the world.

This event celebrated two important occasions: 150years of Rabindranath Tagore and 100 years of Delhias the Capital of India.

The fair was inaugurated by the Hon’ble Minister ofHRD Shri Kapil Sibal. Shri Ramesh K. Mittal, Chairman,Books, Publications and Printing Panel, CAPEXIL washonoured to grace the occasion as a Special Guest.

The theme of the fair was “Books on Indian Cinema”.1300 Exhibitors and 1200 publishers displayed theirpublications in more than 20 languages. Countries fromEurope, Asia and America participated with pomp andshow.

To facilitate trade negotiations, NBT provided the RightsTables in association with GBO – a forum of Indianpublishers to exchange copyright of books where Indianand International publishers exchanged notes for twodays.

Most attractive event at the Fair was Children’s Pavilionwhich was humming with activities and programmes forand by children i.e. seminars, panel discussions,workshops, plays and special exhibit of books.

A daily issue of fair news in English and Hindi wasbrought out and circulated among the participants andvisitors to keep everybody updated on the eventshappening and programmes at the fair.

Capexil was a partner to this mega show by way ofsupporting and promoting it at the domestic andinternational level. Moreso, Council invited fair authoritiesand trade associations related to books and publishingof major countries with free stand provided for their

activities as authorized by NBT. Fair Authority ofThailand took advantage of this offer. Activities ofCouncil promoted through its stand at Hall No. 7B-Cspecially dedicated for foreign participants. Goodnumber of contacts were developed for newmemberships.

Seminar on E-publishing held on 1st and 2nd March2012 at the fair ground was organized by Federationof Indian Publishers and W3C India, managed by SPAConsultancy Services Pvt.Ltd. and S-Media wassupported by CAPEXIL. Shri Ramesh K. Mittal,Chairman, Books, Publications and Printing Panel,CAPEXIL offered vote of thanks at the seminar on 1stMarch 2012.

A meeting was held at Capexil’s stand between Mr.Randy Kiefer of CLOCKSS, USA and Mr. Ramesh K.Mittal, Chairman, Books, Publications and PrintingPanel. Both had a discussion on how Indian E-publishing industry could store their e-publications withCLOCKSS database to ensure the clients worldovera perpetual access to their products. CLOCKSS planto come forward and conduct seminars in India on thisservice in association with Capexil.

Capexil in association with NBT organized apresentation on publishing industry of Poland at thefair ground on 26th February 2012.

This time NBT took several new initiatives and one ofsuch is associating CAPEXIL with its endeavour andauthorized Council to invite foreign participants andmaking the occasion an annual event.

The New Delhi World Book Fair could be a premiumfair among the book fairs around the world if we couldbe involved as a co-organiser with responsibility toindependently organize seminar/reverse buyer-sellermeet etc. as concurrent event of the Show.

THE NEW DELHI WORLD BOOK FAIR 2012— A Report

18

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

I. Anti dumping - Meaning and concept

QI. What is anti dumping duty? What is its purposein international trade?

AI. Dumping is said to occur when the goods areexported by a country to another country at aprice lower than its normal value and this causesinjury to domestic industry. This is an unfair tradepractice which can have a distortive effect oninternational trade as it keeps competitors out ofa particular market. Anti dumping measures rectifythe situation arising out of the dumping of goodsand its trade distortive effect. The use of antidumping measure as an instrument of faircompetition is permitted by the WTO. Anti dumpingduty is recognised as an instrument for ensuringfair trade and is not a measure of protection perse for the domestic industry. It provides relief tothe domestic industry against the injury causedby dumping.

Q2. Does dumping mean cheap or low pricedimports?

A2. Often, dumping is mistaken and simplified to meancheap or low priced imports. However, it is amisunderstanding of the term. Dumping, in itslegal sense, means export of goods by a countryto another country at a price lower than its normalvalue. Thus, dumping implies low priced importsonly in the relative sense (relative to the normalvalue), and not in absolute sense. In simpleparlance, the normal value is the selling price ofthe product in the exporting country.

Import of undervalued products to evade customsduty or through megal trade channels likesmuggling does not fall within the purview of anti-dumping measures.

Q3. What is the difference between anti dumpingduty and Normal Customs duty? Is the antidumping duty over and above the NormalCustoms duty chargeable on the import of anitem?

A3. Although anti dumping duty is levied and collectedby the Customs Authorities, it is entirely differentfrom the Customs duties not only in concept and

substance, but also in purpose and operation.The following are the main differences betweenthe two: -

l Conceptually, anti dumping and the like measuresin their essence are linked to the notion of fairtrade. The object of these duties is to guardagainst the situation arising out of unfair tradepractices while customs duties are levied as ameans of raising revenue and for overalldevelopment of the economy.

l Customs duties fall in the realm of trade and fiscalpolicies of the Government while anti dumpingmeasures are trade remedial measures.

l The object of anti dumping is to offset the injuriouseffect of international price discrimination whilecustoms duties have implications for thegovernment revenue and for overall developmentof the economy.

l Anti dumping duties are not necessarily in thenature of a tax measure inasmuch as the Authorityis empowered to suspend these duties in caseof an exporter offering a price undertaking. Thussuch measures are not always in the form ofduties / tax.

l Anti dumping duties are levied against exporter/ country inasmuch as they are country specificand exporter specific as against the customsduties which are general and universallyapplicable to all imports irrespective of the countryof origin and the exporter.

The anti dumping duty is levied over and abovethe normal customs duty chargeable on the importof goods in question.

II. WTO Agreement and legal framework in Indiafor anti dumping investigations

Q4. Is there a WTO Agreement on anti dumping?

A4. There is a WTO Agreement on Implementationof Article VI of the General Agreement on Tariffsand Trade (GATT) 1994 which is commonly knownas the Anti dumping Agreement.

AGREEMENT ON ANTI DUMPING - FREQUENTLY ASKED QUESTIONS

19

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

Q5. What is the legal framework for Anti dumpingmeasures in India?

A5. Sections 9A, 9B and 9C of the Customs Tariff Act,1975 as amended in 1995 and the Customs Tariff(Identification, Assessment and Collection of Anti-dumping Duty on Dumped Articles and forDetermination of Injury) Rules, 1995 framed thereunder form the legal basis for anti-dumpinginvestigations and for the levy of anti-dumpingduties in India.

III. Institutional arrangement for anti-dumpingmeasures in India

Q6. What is the institutional arrangement in Indiafor anti dumping measures against unfair tradepractices?

A6. Anti dumping (as also anti subsidies &countervailing measures) in India are administeredby the Directorate General of Anti dumping andAllied Duties (DGAD) functioning in the Departmentof Commerce in the Ministry of Commerce andIndustry and the same is headed by the"Designated Authority". The Designated Authority'sfunction, however, is only to conduct the antidumping / anti subsidy and countervailing dutyinvestigation and make recommendation to theGovernment for imposition of anti dumping or antisubsidy measures. Such duty is finally imposed/levied by a Notification of the Ministry of Finance.Thus, while the Directorate General of Anti dumpingand Allied Duties (DGAD) recommend the Anti-dumping duty, it is the Ministry of Finance, whichlevies such duty.

IV. Some important concepts and practices of Antidumping Agreement

Q7. What are the parameters used to assessdumping of goods from a country?

A7. Dumping means export of goods by one country/ territory to the market of another country / territoryat a price lower than the normal value. If the exportprice is lower than the normal value, it constitutesdumping. Thus, there are two fundamentalparameters used for determination of dumping,namely, the normal value and the export price.Both these elements have to be compared at thesame level of trade, generally at ex-factory level,for assessment of dumping.

Q8. How are the following terms defined?l Normal Valuel Export price andl Dumping margin

A8. Normal Value: Normal value is the comparableprice at which the goods under complaint aresold, in the ordinary course of trade, in thedomestic market of the exporting country.

If the normal value can not be determined bymeans of the domestic sales, the following twoalternative methods may be employed todetermine the normal value:-l Comparable representative export price to an

appropriate third country.l Constructed normal value, i.e. the cost of

production in the country of origin withreasonable addition for administrative, sellingand general costs and reasonable profits.

Export price: The Export price of the allegedlydumped goods means the price at which it isexported to the complaining country. It is generallythe CIF value minus the adjustments on accountof ocean freight, insurance, commission, etc. soas to arrive at the value at ex-factory level.

Dumping Margin: The margin of dumping is thedifference between the Normal value and theexport price of the goods under complaint. It isgenerally expressed as a percentage of the exportprice.

Illustration: Normal value US$110 per kg.

Export price US$100 per kg.

There is dumping in this case as export price islower than normal value and dumping margin inthis case is US$ 10 per kg., i.e.10% of the exportprice.

Dumping is a function of two variables, namelyNormal Value and Export Price, which must becompared at the same level of trade, normallyat the ex-factory level.

NORMAL VALUE

l Comparable price of the like article at the samelevel of trade in the domestic market of theexporting country

l In the ordinary course of trade

20

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

WHAT IS DUMPING?

Difference between Normal Value and Export Price isknown as 'Margin of dumping'

Q9. What is understood by the term' domesticindustry'?

A9. The term "domestic industry" means the domesticproducers as a whole engaged in the manufactureof the like article or those whose collective outputof the said article constitutes a major proportionof the total domestic production of that article. Theproducers who are related to the exporters orimporters of the alleged dumped article or arethemselves importers thereof are excluded fromthe purview of 'domestic industry' in certainsituations.

Q10. What is the meaning of the term 'like product'?

A10. Like product means a product which is identicali.e. alike in all respects to the product underconsideration, or in the absence of such a product,another product which, although not alike in allrespects, has characteristics closely resemblingthose of the product under consideration.

Q11. What are the methods of calculating dumpingmargin?

A11. The dumping margin is normally to be established:

a) on the basis of comparison of a weightedaverage normal value with a weighted averageof prices of all comparable export transactions,or

b) by comparison of normal value and exportprices on a transaction-to-transaction basis.

A normal value established on a weighted averagebasis may be compared to the prices of theindividual export transactions if it is found that thepatterns of export prices differ significantly amongdifferent purchasers, regions or time periods andif an explanation is provided as to why suchdifferences cannot be taken into accountappropriately by the use of weighted average-to-weighted average or transaction-to-transactioncomparison.

Q12. Under what circumstances can domestic salesin the market of the exporting country bedisregarded for determining normal value?

A12. In case the sales of the like product in the domesticmarket of the exporting country is less than 5%of the quantity of the export sale of the productunder consideration to the importing country, suchdomestic sales in the market of the exportingcountry can be disregarded for determining normalvalue on account of being not sufficient in quantityfor a proper comparison.

Q13. Under what circumstances can sales of the likeproduct in the domestic market of the exportingcountry may be treated as not being in the ordinarycourse of trade by reason of price and disregardedin determining normal value?

A13. When the weighted average selling price of thetransactions under consideration for determinationof the normal value is below the weighted averageper unit costs, or the volume of sales below perunit costs are 20% or more of the volume sold intransactions under consideration, then such lossmaking transactions have to be disregarded fordetermining normal value.

Q14. What is the method of calculation of dumpingmargin when goods are exported from anintermediate country, i.e. from a country otherthan the country of manufacture?

A14. Normally the export price of the product from thecountry of export is to be compared with thecomparable domestic price of the product in thecountry of export for arriving at the dumpingmargin. However if the product is not producedin the country of export, then comparison of exportprice may be made with the price in the countryof origin.

Q15. What is meant by zeroing?

A15. While making comparison of normal value andexport price either on a weighted average basisor on a transaction-to-transaction basis, somecomparisons at intermediate stage may result innegative dumping margin i.e. where export priceis more than the normal value. In the finalcalculation of dumping margin if such negativedumping margins are not taken into account,such practice is called zeroing.

Q16. How is dumping margin determined from exportsfrom countries which are characterised as Non-Market Economy?

21

CHEMICAL

S&

ALLI

ED

PRODUCTS EXPORT PROMO

TION

COUNCIL

INDIA

Feb-Mar ‘12

A16. The term ‘non-market economy’ country meansany country which the designated authoritydetermines as not operating on market principlesof cost or pricing structures, so that sales ofmerchandize in such country do not reflect the fairvalue of the merchandize, in accordance with thecriteria specified in sub-paragraph (3) of paragraph8 of Annexure I of the Anti dumping Rules of India.

Paragraph 7 and 8 of Annexure I of Anti dumpingRules of India lays down the procedure fordetermination of normal value in case of importsfrom non-market economy countries.

Q17. What are the types of injury to the domestic industryin an Anti dumping investigation?

A17. The WTO Agreement on implementation of ArticleVI of GATT (Anti dumping Agreement) lays downthe injury can be material injury to a domesticindustry, threat of material injury or materialretardation of the establishment of such an industry.

Q18. What are the parameters of material injury to thedomestic industry?

A18. Broadly, injury may be analysed in terms of thevolume effect and price effect of the dumpedimports.

The volume effect of dumping relates to the marketshare of the domestic industry vis-a-vis the dumpedimports from the subject country/ies while withregard to the price effect, the Designated authorityshall consider whether there has been a significantprice under cutting by the dumped imports ascompared with the price of the like product in thedomestic market, or whether the effect of suchimports is otherwise to depress prices to asignificant degree or prevent price increase whichotherwise would have occurred to a significantdegree.

INJURY EVALUATION OF ECONOMICINDICATIORS

ACTUAL/POTENTIAL DECLINE IN

SalesOutputProfitsMarket shareProductivityReturn on InvestmentCapacity Utilization

Factors affecting domestic prices;EmploymentInventory/StocksWages, effects on cash flow, growthAbility to raise capital or investment etc.

The parameters by which injury to the domesticindustry is to be assessed in the anti dumpingproceedings are such economic indicators havinga bearing upon the state of industry as the magnitudeof dumping, and the decline in sales, selling price,profits, market share, production, utilisation ofcapacity, etc.

Q19. On what basis is threat of material injuryestablished?

A19. A determination of a threat of material injury hasto be based on facts and not merely on allegation,conjecture or remote possibility. The change incircumstances which would create a situation inwhich the dumping would cause injury must beclearly foreseen and imminent. In making adetermination regarding the existence of a threatof material injury, the designated authority has toconsider, inter alia, such factors as :

(a) a significant rate of increase of dumpedimports into domestic market indicating thelikelihood of substantially increasedimportation;

(b) sufficient freely disposable, or an imminent,substantial increase in, capacity of theexporter indicating the likelihood ofsubstantially increased dumped exports todomestic markets, taking into account theavauilability of other export markets to absorbany additional exports;

(c) whether imports are entering at prices thatwill have a significant depressing orsuppressing effect on domestic prices, andwould likely increase demand for furtherimports; and

(d) inventories of the article being investigated.

(Source : Centre for WTO Studies,

Indian Institute of Foreign Trade)

to be contd...

22

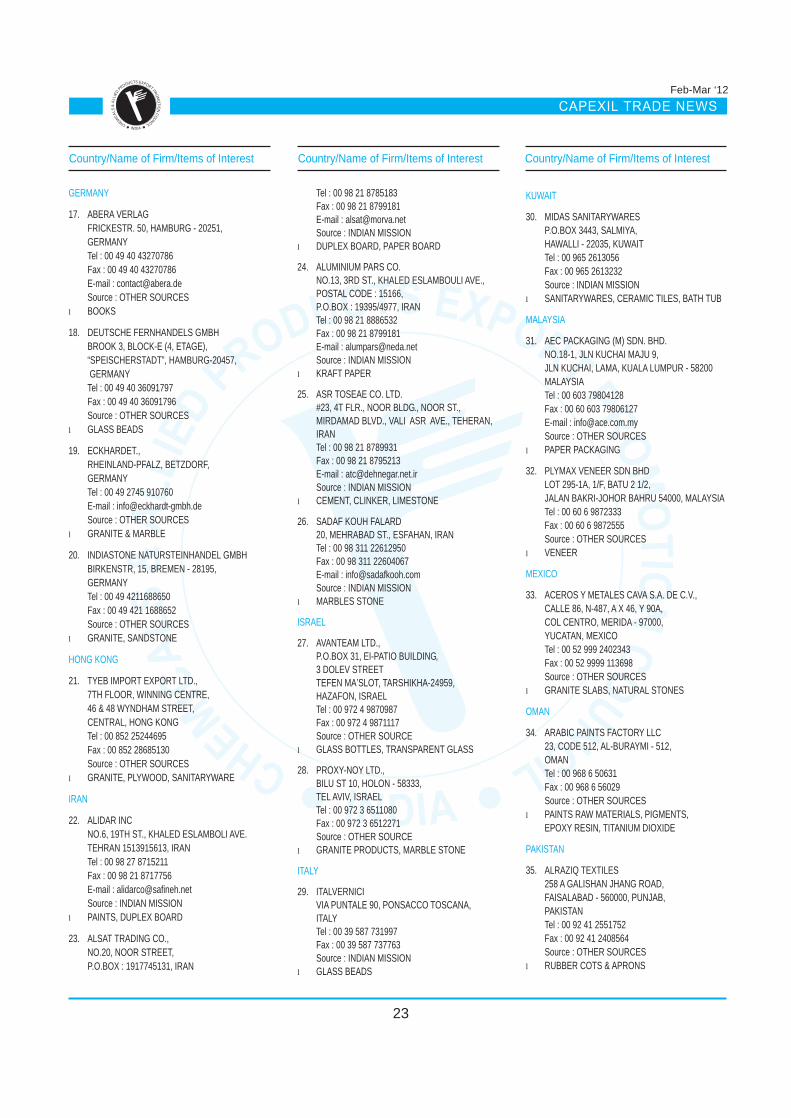

OVERSEAS ENQUIRIES (FEBRUARY 2012)

Country/Name of Firm/Items of Interest Country/Name of Firm/Items of Interest Country/Name of Firm/Items of Interest

CHEMICAL

S&

ALL

IED

PRODUCTS EXPORT PROM

OTIO

NCOUNCIL

INDIA

Feb-Mar ‘12

AUSTRALIA

1. BEAD BARN AUSTRALIA PI.P.O.BOX 96, HALL, CANBERRA - 2618,AUSTRALIAN CAPITAL TERRITORY,AUSTRALIATel : 00 61 2 62275017Fax : 00 61 2 62425551Source : OTHER SOURCES

l GLASS BEADS

2. DOGLION TRADING43 OLSEN ROAD, ILKLEY,SUNSHINE COAST-4554,QUEENSLAND, AUSTRALIATel : 00 61 7 54788631Fax : 00 61 7 54788631Source : OTHER SOURCES

l GRANITE & MARBLE, LIME STONE

3. DALSKI STONEUNIT 5, 743-745 THE HORSLEY DRIVE,SMITHFIELD - 2164, NEW SOUTH WALES,AUSTRALIATel : 00 61 2 97292532Fax : 00 61 2 97292832E-mail : [email protected] : OTHER SOURCES

l GRANITE & MARBLE, LIME STONE

4. HOT DOT DESIGNS BY CAROL YNE BRENNAN10 BIARA STREET, CHESTER HILL - 2162,NEW SOUTH WALES, AUSTRALIATel : 00 61 2 97438300Fax : 00 61 2 94438300Source : OTHER SOURCES

l GLASS BEADS

5. JILL BOND10, RINTOUL LOOP, BOORAGOON,AUSTRALIATel : 00 61 8 93172771Fax : 00 61 8 93172771Source : OTHER SOURCES

l GLASS BEADS

BAHARAIN

5. CASTLE ROCK INDUSTRIES W.L.LP.O.BOX : 5707, MANAMA,AL-MANAMAH-5707,BAHARAINTel : 00 973 3 9184577Fax : 00 973 17 830824E-mail : [email protected] : OTHER SOURCES

l GRANITE ROUGH BLOCKS

BANGLADESH

6. AKIN ENTERPRISEBAITUSH SHARAF COMPLEX,1ST FLOOR, D.T. ROAD,CHITTAGONG - 4100, BANGLADESHTel : 00 880 21 2520847Fax : 00 880 31 710832Source : OTHER SOURCES

l LABORATORY GLASSWARE

7. ALVE PAINTS & CHEMICAL WORKS6, MOHUDDIN LANE, IMAMAGONG,Dhaka-1211, BANGLADESHTel : 00 880 2 7310593Fax : 00 880 2 7319754Source : OTHER SOURCES

l PAINTS, RAW MATERIALS

8. BOILER & PNEUMATIC223, NAWABPUR ROAD,DHAKA - 1100,BANGLADESHTel : 00 880 2 7175648Fax : 00 880 2 7160379Source : OTHER SOURCES

l TISSUE PAPER

9. RH INTERNATIONAL AGENCIESMOTIJHEEL C/A,DHAKA - 1000,BANGLADESHTel : 00 880 1611 333351E-mail : [email protected] : OTHER SOURCES

l NEWS PRINT, DUPLEX BOARD,STICKER PAPER

BELGIUM

10. BSTWALGOEDSTRAAT 12, TEMSE - 9140,OOST-VLAANDEREN, BELGIUMTel : 00 32 474 895466Fax : 00 32 3 7113320Source : OTHER SOURCES

l GLAZED CERAMIC TILES,PORCELAIN TILES

CANADA

11. INCAS CANADA INC.,606 RIVERMEDE ROAD #7,CONCORD - L4K 2H6, ONTARIO,CANADATel : 00 1 905 7381606Fax : 00 1 905 7381606

Source : OTHER SOURCESl TITANIUM DIOXIDE

CYPRUS

12. A FINIRIS CO23-B, KYRIAKOU MATSI AVENUE,CYPRUSTel : 00 357 22 454858Fax : 00 357 22 316602E-mail : [email protected] : OTHER SOURCES

l PRINTING & WRITING PAPER

ECUADOR

13. LISLOPAVE PAUCARBAMBA 455,AND LUIS, ECUADORTel : 00 593 72 882692Fax : 00 593 72 814913Source : OTHER SOURCES

l GRANITE, SLATE TILES, PORCELAIN TILES,CERAMIC TILES

EGYPT

14. ELSHAMY CO16 SIDI GABER STREET, ON TRAM,BESIDE THE CHURCH OF THE ADVANTIST,ELSABTEYEEN, CLEOPATRA,SIXTH FLOOR, FLAT #13, ALEXANDRIA,AL-ISKANDARIYAH-21533, EGYPTFax : 00 20 3 4835115Source : OTHER SOURCES

l GLASS BEADS

15. GRANISER TILE KITCHEN BATH5650 GENERAL WASHINGTON DRIVE,ALEXANDRIA - 22312-2415,VIRGINIA, EGYPTTel : 00 1 703 2565650Fax : 00 1 703 2568878Source : OTHER SOURCES

l CERAMIC & PORCELAIN TILES

16. NEEASAECANAL MAHMOUDIA ST., ELBAR-EL-KABLY,EL-NOZHA, ALEXANDRIA - 21523,MUHAFAZAT, AL ISKANDARLYAH,EGYPTTel : 00 20 3 3814103Fax : 00 20 3 3815522Source : OTHER SOURCES

l GLASS TUBES

23

Country/Name of Firm/Items of Interest Country/Name of Firm/Items of Interest Country/Name of Firm/Items of Interest

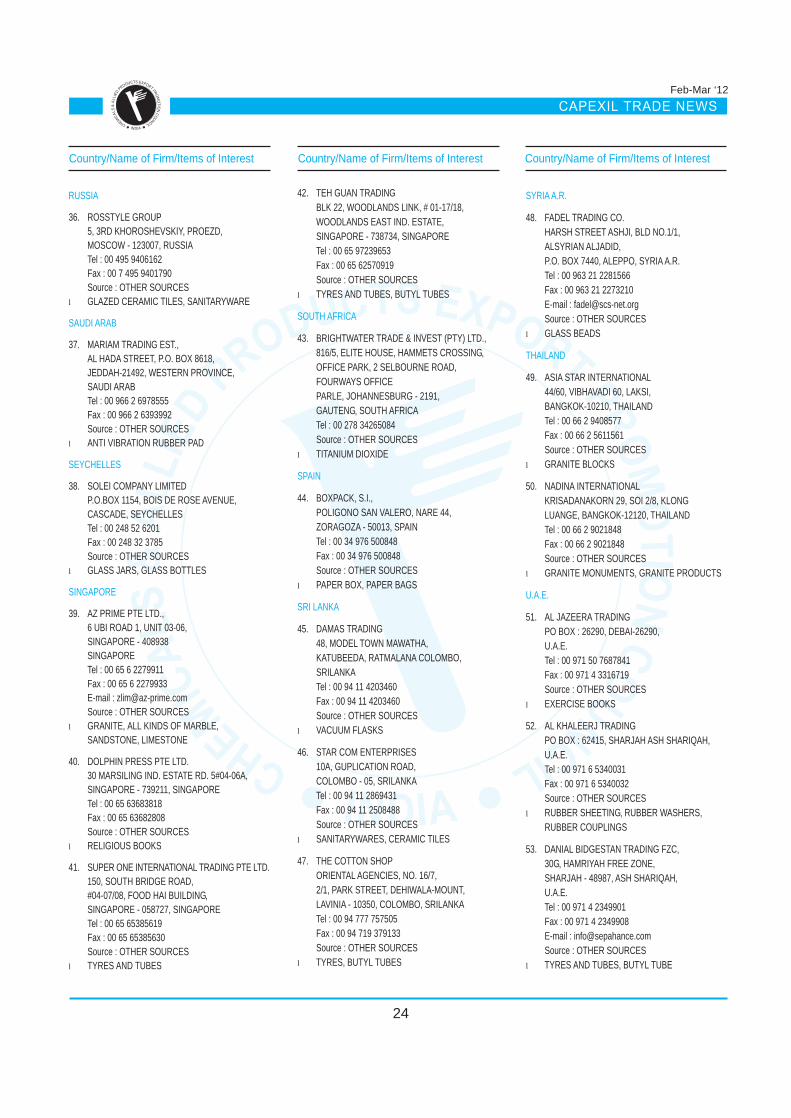

CHEMICAL

S&