guaranteed income solutions - stan the … new york life: built for times like these new york life...

TRANSCRIPT

NEW YORK LIFE LIFETIME INCOME ANNUITY

G U A R A N T E E D I N C O M E S O L U T I O N S

2

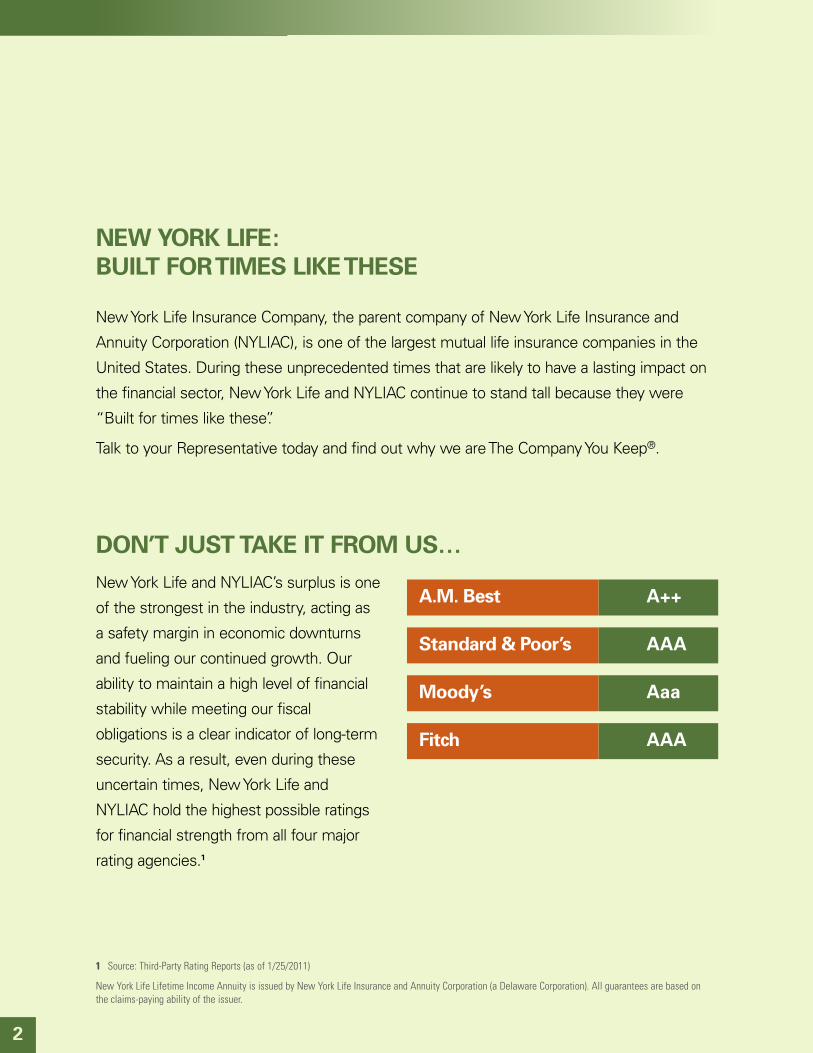

NEW YORK LIFE:BUILT FOR TIMES LIKE THESE

New York Life Insurance Company, the parent company of New York Life Insurance and

Annuity Corporation (NYLIAC), is one of the largest mutual life insurance companies in the

United States. During these unprecedented times that are likely to have a lasting impact on

the financial sector, New York Life and NYLIAC continue to stand tall because they were

“Built for times like these”.

Talk to your Representative today and find out why we are The Company You Keep®.

DON’T JUSTTAKE IT FROM US…New York Life and NYLIAC’s surplus is one

of the strongest in the industry, acting as

a safety margin in economic downturns

and fueling our continued growth. Our

ability to maintain a high level of financial

stability while meeting our fiscal

obligations is a clear indicator of long-term

security. As a result, even during these

uncertain times, New York Life and

NYLIAC hold the highest possible ratings

for financial strength from all four major

rating agencies.1

A++A.M. Best

AAAStandard & Poor’s

AaaMoody’s

AAAFitch

1 Source: Third-Party Rating Reports (as of 1/25/2011)

New York Life Lifetime Income Annuity is issued by New York Life Insurance and Annuity Corporation (a Delaware Corporation). All guarantees are based onthe claims-paying ability of the issuer.

3

As you embark on your retirement, keep in mind that you may face unforeseen risks including:

Longevity RiskWith the average life expectancy increasing, there is a veryreal risk of outliving your money in retirement.

Market VolatilityInvestments are subject to ups and downs of the market. As you get older, you have less time to recover lossescaused by market volatility.

Healthcare ExpensesHealthcare costs have continued to rise, and may becomemore expensive. This is a major financial concern for manyAmericans.2

At New York Life Insurance and Annuity Corporation (NYLIAC), we believe that when it comes to your retirement, the decisions you make today will impact the lifestyle you’ll have tomorrow.

2 Source: The Rising Cost of Healthcare: The Causes. Updated January 2009.

4

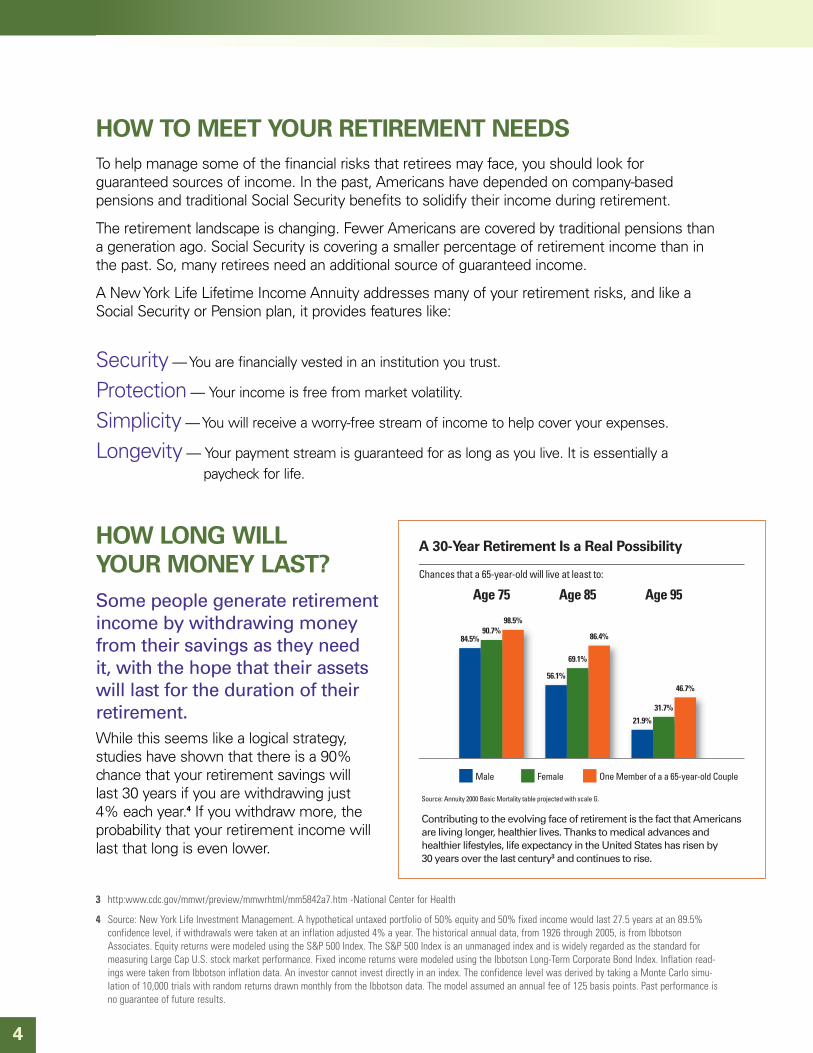

HOW TO MEET YOUR RETIREMENT NEEDSTo help manage some of the financial risks that retirees may face, you should look for guaranteed sources of income. In the past, Americans have depended on company-based pensions and traditional Social Security benefits to solidify their income during retirement.

The retirement landscape is changing. Fewer Americans are covered by traditional pensions thana generation ago. Social Security is covering a smaller percentage of retirement income than inthe past. So, many retirees need an additional source of guaranteed income.

A New York Life Lifetime Income Annuity addresses many of your retirement risks, and like aSocial Security or Pension plan, it provides features like:

Security— You are financially vested in an institution you trust.

Protection— Your income is free from market volatility.

Simplicity— You will receive a worry-free stream of income to help cover your expenses.

Longevity— Your payment stream is guaranteed for as long as you live. It is essentially a paycheck for life.

HOW LONG WILL YOUR MONEY LAST?Some people generate retirementincome by withdrawing moneyfrom their savings as they need it, with the hope that their assetswill last for the duration of theirretirement.While this seems like a logical strategy,studies have shown that there is a 90%chance that your retirement savings will last 30 years if you are withdrawing just 4% each year.4 If you withdraw more, theprobability that your retirement income willlast that long is even lower.

One Member of a a 65-year-old Couple

Contributing to the evolving face of retirement is the fact that Americansare living longer, healthier lives. Thanks to medical advances and healthier lifestyles, life expectancy in the United States has risen by 30 years over the last century3 and continues to rise.

3 http:www.cdc.gov/mmwr/preview/mmwrhtml/mm5842a7.htm -National Center for Health

4 Source: New York Life Investment Management. A hypothetical untaxed portfolio of 50% equity and 50% fixed income would last 27.5 years at an 89.5%confidence level, if withdrawals were taken at an inflation adjusted 4% a year. The historical annual data, from 1926 through 2005, is from IbbotsonAssociates. Equity returns were modeled using the S&P 500 Index. The S&P 500 Index is an unmanaged index and is widely regarded as the standard formeasuring Large Cap U.S. stock market performance. Fixed income returns were modeled using the Ibbotson Long-Term Corporate Bond Index. Inflation read-ings were taken from Ibbotson inflation data. An investor cannot invest directly in an index. The confidence level was derived by taking a Monte Carlo simu-lation of 10,000 trials with random returns drawn monthly from the Ibbotson data. The model assumed an annual fee of 125 basis points. Past performance isno guarantee of future results.

5

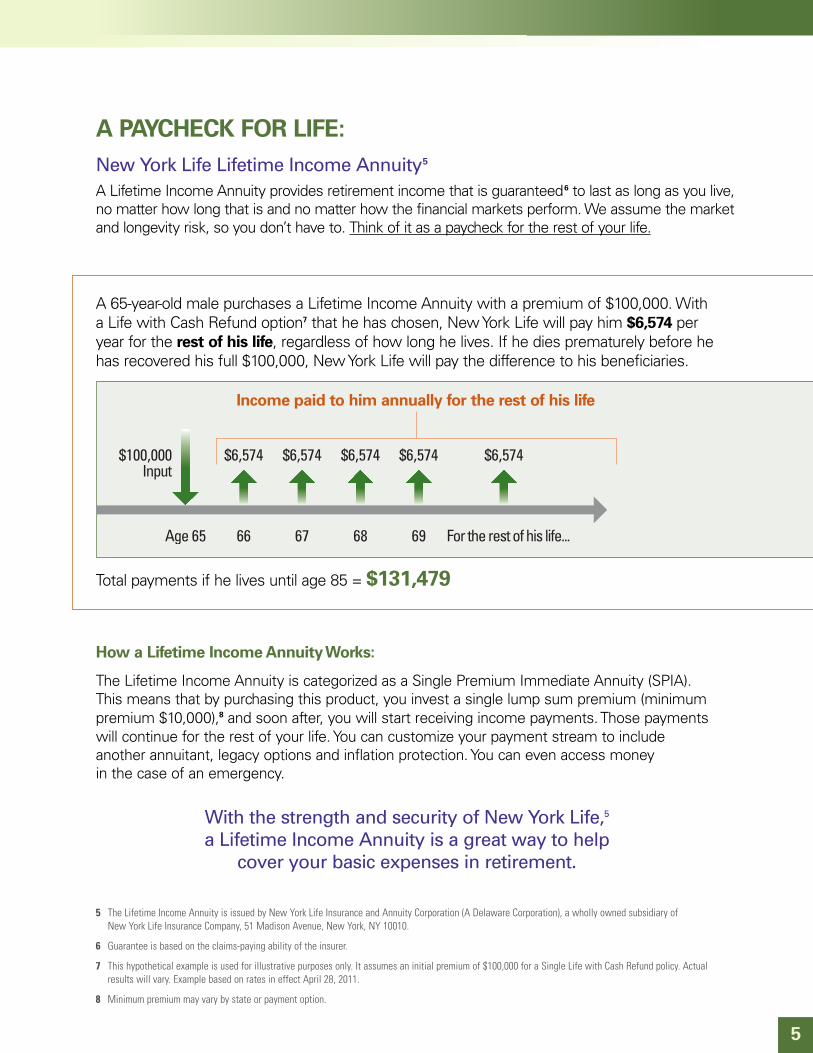

A 65-year-old male purchases a Lifetime Income Annuity with a premium of $100,000. Witha Life with Cash Refund option7 that he has chosen, New York Life will pay him $6,574 peryear for the rest of his life, regardless of how long he lives. If he dies prematurely before hehas recovered his full $100,000, New York Life will pay the difference to his beneficiaries.

Total payments if he lives until age 85 = $131,479

A PAYCHECK FOR LIFE: New York Life Lifetime Income Annuity5

A Lifetime Income Annuity provides retirement income that is guaranteed6 to last as long as you live,no matter how long that is and no matter how the financial markets perform. We assume the marketand longevity risk, so you don’t have to. Think of it as a paycheck for the rest of your life.

How a Lifetime Income Annuity Works:

The Lifetime Income Annuity is categorized as a Single Premium Immediate Annuity (SPIA).This means that by purchasing this product, you invest a single lump sum premium (minimumpremium $10,000),8 and soon after, you will start receiving income payments. Those paymentswill continue for the rest of your life. You can customize your payment stream to include another annuitant, legacy options and inflation protection. You can even access money in the case of an emergency.

With the strength and security of New York Life,5

a Lifetime Income Annuity is a great way to help cover your basic expenses in retirement.

5 The Lifetime Income Annuity is issued by New York Life Insurance and Annuity Corporation (A Delaware Corporation), a wholly owned subsidiary of New York Life Insurance Company, 51 Madison Avenue, New York, NY 10010.

6 Guarantee is based on the claims-paying ability of the insurer.

7 This hypothetical example is used for illustrative purposes only. It assumes an initial premium of $100,000 for a Single Life with Cash Refund policy. Actualresults will vary. Example based on rates in effect April 28, 2011.

8 Minimum premium may vary by state or payment option.

$6,574$6,574$6,574$6,574$6,574

Income paid to him annually for the rest of his life

WHAT ARE YOUR QUESTIONS CONCERNING RETIREMENT? We can help answer them.“I want to make sure my spouse is taken care of, should anything happen to me.”

By choosing a Joint Life policy, covering you and your spouse, the LifetimeIncome Annuity payout stream will continue as long as either of you is alive.

“How can I maximize the legacy I leave to my loved ones?”

New York Life offers many payout options designed to provide income for you,but also help make sure that your heirs are taken care of after you’re gone.

6

7

A STREAM OF INCOME FOR TODAY, TOMORROW AND BEYONDThe Lifetime Income Annuity offers a combination of cutting-edge features9 that can help address your retirement income needs.

You can choose from the following options:10

Highest Amount of Income (Single or Joint Life Only)

The Single Life Only option provides income to you for the duration of your lifetime, regardless of how long you live. This option generally provides the highest income benefit for any given pre-mium. However, payments will stop at your death.

A Joint Life Only option makes payments to you for your lifetime and the lifetime of one otherperson. If one of you were to die, the payments would continue to the survivor for the rest ofhis or her life. All else being equal, a given premium amount will provide lower income over jointlives than for a single life policy. Payments stop at the death of both annuitants.

Guaranteed Payment for a Period of Time(Single or Joint Life with Period Certain)

This option pays income for your lifetime, or a guaranteed period of time (you may choose from5 to 30 years), whichever is longer. If you (or both of you for a Joint Life policy) were to livebeyond that period, payments would continue for your lifetime. If you (or both of you for a JointLife policy) were to die prior to the guaranteed period ending, payments would continue to yourbeneficiaries for the remainder of the guarantee period.11,12

Guaranteed Return of Your Principal as a Lump Sum(Single or Joint Life with Cash Refund)

This option pays income for your lifetime (and the lifetime of one other person, with a Joint Lifepolicy). However, this option guarantees that if you die (or both of you for a Joint Life policy), yourbeneficiaries will receive a lump sum equaling your premium less all payments made. For a JointLife, the policy pays income as long as both of you are alive.13

9 Some features are not available on qualified policies, and some are not available in all jurisdictions.

10 The payout option you choose, as well as your age and gender, will affect the amount of each income payment, so be sure to discuss these factors with yourinsurance professional. Not all payment options are available for all ages.

11 If your Joint Life with Period Certain policy includes a survivor income that is less than 100% of the income while both of you are alive, the reduction inincome will not take place until the first annuitant’s death or at the end of the guaranteed payment period, whichever is later.

12 Upon death of the annuitant (or both annuitants for a Joint Life policy), remaining guaranteed payments can be commuted into a lump sum if the policyownerselected this option at issue.

13 If the total payments you receive prior to your death equal or exceed the initial premium you paid for your policy, then no further payments will be made tobeneficiaries upon death.

8

14 The Percent of Premium Death Benefit payout option is not available on qualified policies. It is not available in New York or Washington.15 Please consult with your professional tax advisor.16 Reduction of benefits is not available on Joint Life with Cash Refund policies, Joint Life with Installment Refund policies, Joint Life policies with the

Changing Needs Option or the Income Enhancement Option.17 Income payments generally begin one payment period after the policy date. If you choose to receive a monthly income, your payments will begin one month

after the policy date, whereas if you choose to receive quarterly income, payments will begin three months after the policy date. You may select the startdate for receiving payments, but payments must begin within one year of the policy issue date.

Guaranteed Return of Your Principal in Installments (Single or Joint Life with Installment Refund)

This option pays income for your lifetime (and the lifetime of one other person if a Joint Lifepolicy). However, this option guarantees that if you die (or both of you for a Joint Life policy),your beneficiaries will continue to receive the annuity payments until the premium is fullyrecovered. The Installment Refund provision entitles your beneficiaries to receive the total ofthe premium less all payments made on a scheduled installment basis.13

Death Benefits for Your Loved Ones (Single or Joint Life with Percent of Premium Death Benefit)14

This option offers income for your lifetime (and the lifetime of one other person with a Joint Lifepolicy). It also guarantees that when you die (or both annuitants for a Joint Life policy) your bene-ficiaries will receive a death benefit totaling 25% or 50% of your original premium. This alterna-tive pays a lower income for the same premium than one that does not provide a guaranteeddeath benefit, but it ensures a legacy for your heirs. Furthermore, in many cases the amountyour heirs receive will be a non-taxable return of your investment in the contract.15

Additional Flexibility for You and Your Loved One(Reduction of Benefits for Joint Life Policies)

Most of the Joint Life policies16 we offer also allow you to reduce the income amount by 40% to99% after one of the annuitants dies. By reducing the survivor’s income payments, you are ableto enjoy a higher income while both annuitants are still alive.

You might decide, for example, that if one of you were to die, the survivor would need only 80%of the income that both of you previously required. Choosing this lower percentage may bettermeet your needs, because a Joint Life policy that pays a smaller income to the survivor will provide a higher income while both of you are alive.

The factors that determine the amount of payments you will receive include:n The amount of your premium and the interest rate environment when you purchase

your policyn The number of lives the policy covers (either one or two)n Your age and gender (and those of the other person for Joint Life policies)n Any guaranteed minimum payment, inflation protection, change in income schedule,

or legacy options you selectn The frequency with which you choose to receive your income payments

(monthly, quarterly, semi-annually or annually); andn How soon your payments are scheduled to begin17

9

SOME TAX BENEFITS OF A LIFETIME INCOME ANNUITYPerfect for Required Minimum Distribution (RMD)You can set up a qualified annuity which may automatically satisfy your RMDs each year underthe current federal income tax law.18 The IRS generally requires that people begin withdrawingmoney each year from their tax-qualified accounts after age 701/2. A Lifetime Income Annuitymay help you avoid penalties and free you of the burden of having to figure out and withdrawthe correct distribution amount on your own each year.

No tax penalty for early withdrawals:If you are younger than age 591/2 and you would like to withdraw funds from any of your tax-qualified accounts, a 10% penalty tax will apply in most cases. However, if you were to roll thatmoney into a qualified Lifetime Income Annuity the income payments from the Lifetime IncomeAnnuity would generally be penalty tax-free.

A WELLSPRING OF ADVANTAGES If you fund your annuitywith funds from a qualifiedplan, rather than withdraw-ing your qualified funds in alump sum, your incomepayments may allow you tospread your tax liability overyour lifetime. As a result,this can offer you significanttax benefits.

An income annuity funded with IRA or qualified planassets must meet certain Internal Revenue Service (IRS)RMD requirements. Clients who are considering purchas-ing an income annuity with IRA or qualified plan fundsshould consult their own professional tax advisors to dis-cuss these RMD requirements and how they apply to theirparticular situation. New York Life, its subsidiaries, agentsand employees do not provide tax or legal advice.

18

FUNDING YOUR ANNUITYNon-qualified annuities are purchased using “after-tax” dollars you may have accumulated inother savings vehicles. Each annuity income payment consists of a taxable income portion, anda return of premium portion, which is not taxable. The division between the taxable and “tax-free” portions of your payments is determined by IRS rules based on several factors, includingyour life expectancy, the premium you paid for your policy (“cost basis” or original investment),and any guarantees chosen. Once the “tax-free” payments you receive equal your policy’s “costbasis” all future payments you receive are 100% taxable as ordinary income.

Qualified annuities are purchased using “pre-tax” dollars you may have accumulated in anIndividual Retirement Account (IRA), 401(k), Keogh, or other employer-sponsored retirement plan.However, by rolling funds from a qualified plan into a Lifetime Income Annuity rather than takinga lump-sum distribution, you will spread your tax liability over many years, which may reduceyour total tax liability. Qualified annuity payments generally are fully taxable as ordinary income inthe year they are received.

Perfect for RolloversWhen retiring, you may need to decide what to do with your IRA, 401(k), 403(b), governmentalsection 457 plan or other employer sponsored retirement plans. You have several options ofcourse, including purchasing CDs, bonds, or stocks. Rolling some, or all, of your retirement planassets into a Lifetime Income Annuity can turn that money into a steady stream of income thatyou can enjoy for the rest of your life.

Lifetime Income Annuity Roth IRA (Single Life Only)Roth IRAs are funded with “after-tax” dollars. These funds can come from either converting traditional IRAs or qualified retirement plans, such as 401(k)s and other Roth IRAs (provided youmeet applicable requirements).

The Lifetime Income Annuity Roth IRA payments and death benefit amount are tax free. To purchase the Lifetime Income Annuity, you must:

n Have a Roth IRA in place for at least five (5) calendar years before the calendar year inwhich income payments start (this Roth IRA does not have to be used to fund the RothIRA income annuity), AND

n Be at least age 591/2 by the time income payments start

The Internal Revenue Code provides a Roth IRA is not subject to the required minimum distribution(“RMD”) rules during the life of the Roth IRA owner, but is subject to the RMD rulesafter the owner’s death. Accordingly, the Lifetime Income Annuity Roth IRA provides that anyamounts payable to a beneficiary after the owner’s death must be made in accordance with theRMD rules, not withstanding any inconsistent provision in the contract. This may affect theamount otherwise payable to a beneficiary.19

Consult your professional tax advisor to understand fully how a Lifetime Income Annuitywill impact your personal tax situation.

10

19 If, at the time of the owner’s death, the remaining guaranteed period under a Life with Period Certain is longer than the beneficiary’s life expectancy (determinedunder the IRS Single Life Table), NYLIAC will commute all of the future guaranteed payments. This commuted value will be calculated as specified in the policy.

11

ADJUST YOUR INCOME FOR LIFE’S CHANGING NEEDSWe understand that individuals may have their own specific needs interms of retirement income. With our many different features, you havethe flexibility and control to help address your particular retirement needs.

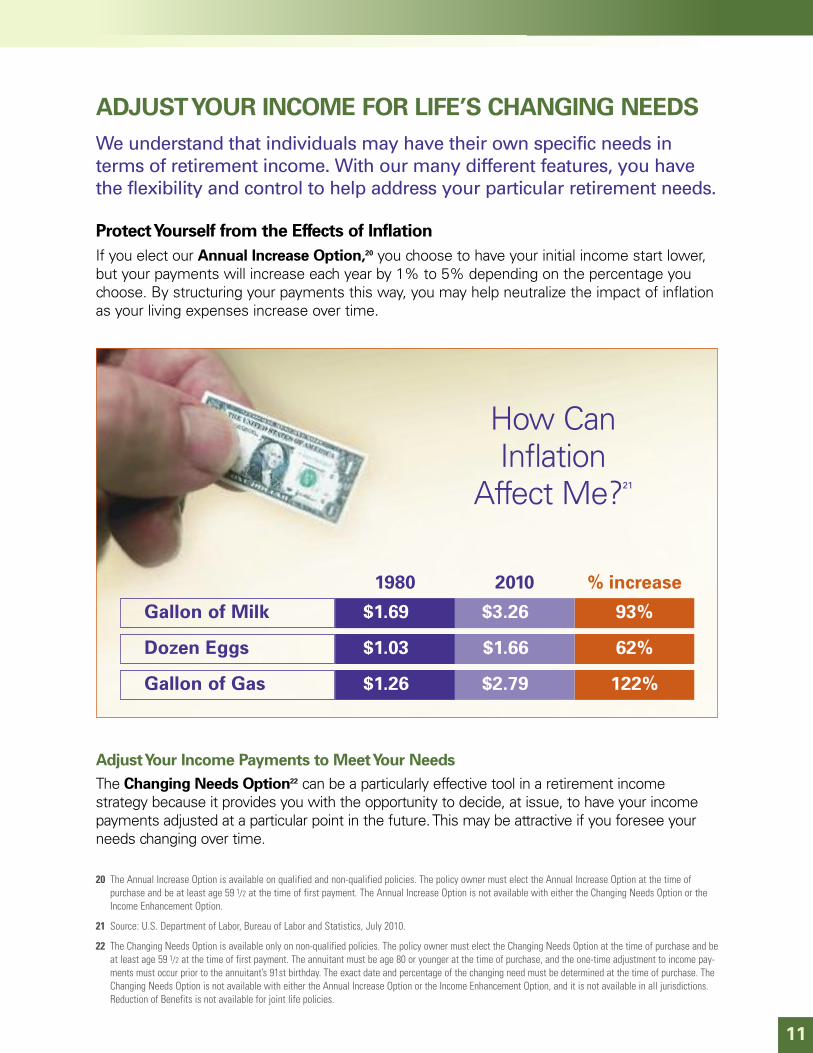

Protect Yourself from the Effects of InflationIf you elect our Annual Increase Option,20 you choose to have your initial income start lower,but your payments will increase each year by 1% to 5% depending on the percentage youchoose. By structuring your payments this way, you may help neutralize the impact of inflationas your living expenses increase over time.

20 The Annual Increase Option is available on qualified and non-qualified policies. The policy owner must elect the Annual Increase Option at the time of purchase and be at least age 59 1/2 at the time of first payment. The Annual Increase Option is not available with either the Changing Needs Option or theIncome Enhancement Option.

21 Source: U.S. Department of Labor, Bureau of Labor and Statistics, July 2010.

22 The Changing Needs Option is available only on non-qualified policies. The policy owner must elect the Changing Needs Option at the time of purchase and beat least age 59 1/2 at the time of first payment. The annuitant must be age 80 or younger at the time of purchase, and the one-time adjustment to income pay-ments must occur prior to the annuitant’s 91st birthday. The exact date and percentage of the changing need must be determined at the time of purchase. TheChanging Needs Option is not available with either the Annual Increase Option or the Income Enhancement Option, and it is not available in all jurisdictions.Reduction of Benefits is not available for joint life policies.

% increase

93%Gallon of Milk

62%Dozen Eggs

122%Gallon of Gas

How Can Inflation

Affect Me?21

2010

$3.26

$1.66

$2.79

1980

$1.69

$1.03

$1.26

Adjust Your Income Payments to Meet Your NeedsThe Changing Needs Option22 can be a particularly effective tool in a retirement income strategy because it provides you with the opportunity to decide, at issue, to have your incomepayments adjusted at a particular point in the future. This may be attractive if you foresee yourneeds changing over time.

23 The Income Enhancement Option is available only on non-qualified policies. The policy owner must elect the Income Enhancement Option at the time of purchase and be at least 59 1/2 at the time of first payment. The annuitant must be age 75 or younger at the time the policy is issued. The IncomeEnhancement Option is not available with either the Changing Needs Option or the Annual Increase Option.

24 The higher income benefit will be paid if the 10-Year Constant Maturity Treasury (CMT) Index in the third full week of the calendar month immediately preceding the fifth policy anniversary is at least two percentage points (2%) higher than the 10-Year CMT Index in the third full week of the calendar monthimmediately preceding the policy date. The higher income benefit would begin on the first scheduled payment after the fifth policy anniversary.

25 If, on the fifth policy anniversary, the benchmark index has not increased sufficiently, you will not receive the increase in your payments, but will continue toreceive the original, guaranteed income payment amount.

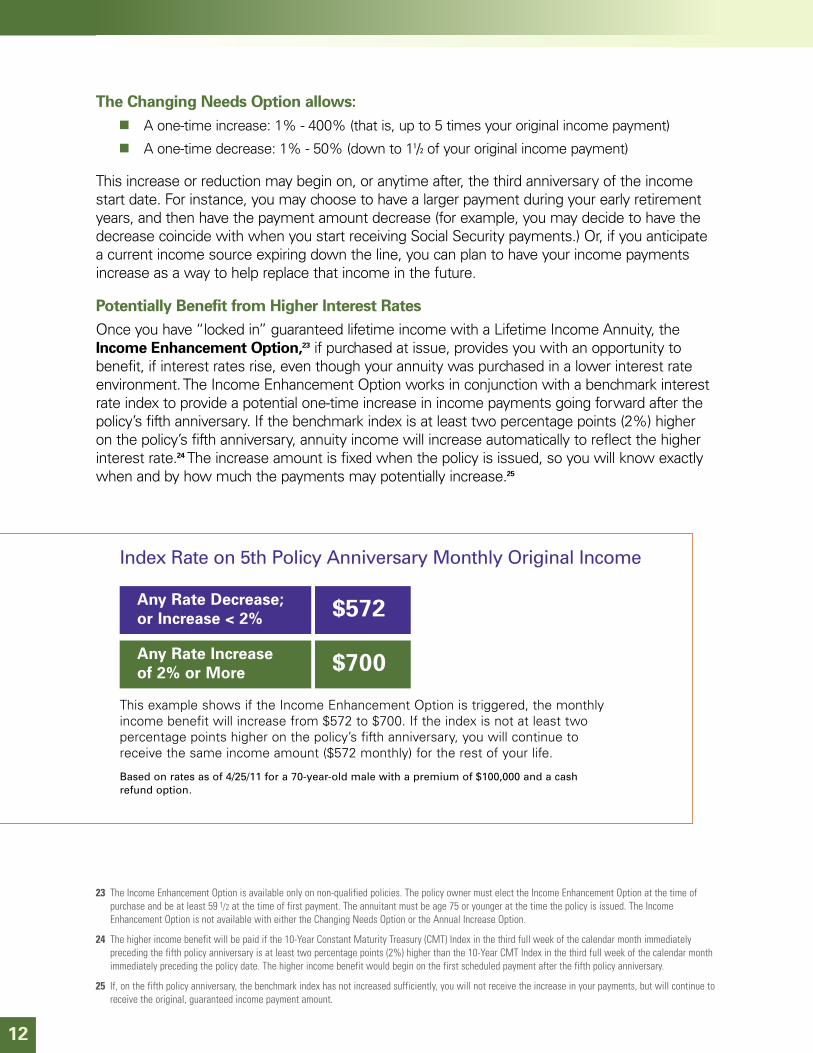

Index Rate on 5th Policy Anniversary Monthly Original Income

This example shows if the Income Enhancement Option is triggered, the monthlyincome benefit will increase from $572 to $700. If the index is not at least two percentage points higher on the policy’s fifth anniversary, you will continue toreceive the same income amount ($572 monthly) for the rest of your life.

Based on rates as of 4/25/11 for a 70-year-old male with a premium of $100,000 and a cashrefund option.

Any Rate Decrease; or Increase < 2%

Any Rate Increase of 2% or More

$572

$700

12

The Changing Needs Option allows:n A one-time increase: 1% - 400% (that is, up to 5 times your original income payment)n A one-time decrease: 1% - 50% (down to 11/2 of your original income payment)

This increase or reduction may begin on, or anytime after, the third anniversary of the incomestart date. For instance, you may choose to have a larger payment during your early retirementyears, and then have the payment amount decrease (for example, you may decide to have thedecrease coincide with when you start receiving Social Security payments.) Or, if you anticipatea current income source expiring down the line, you can plan to have your income paymentsincrease as a way to help replace that income in the future.

Potentially Benefit from Higher Interest RatesOnce you have “locked in” guaranteed lifetime income with a Lifetime Income Annuity, theIncome Enhancement Option,23 if purchased at issue, provides you with an opportunity to benefit, if interest rates rise, even though your annuity was purchased in a lower interest rateenvironment. The Income Enhancement Option works in conjunction with a benchmark interestrate index to provide a potential one-time increase in income payments going forward after thepolicy’s fifth anniversary. If the benchmark index is at least two percentage points (2%) higher on the policy’s fifth anniversary, annuity income will increase automatically to reflect the higherinterest rate.24The increase amount is fixed when the policy is issued, so you will know exactlywhen and by how much the payments may potentially increase.25

13

What if something should happen, and you need money all at once? These situations could occur, but fortunately, we have measures in place

to provide you with…

• Up to 100% CashWithdrawal

• 30% Cash Withdrawal

What Withdrawal Options Are Available With Your Policy?

ACCESS TO CASH SHOULD YOU HIT ROUGHWATERS

Cash WithdrawalFeature

• Life with Cash Refund

• Life with InstallmentRefund

• Life with 5 to 30 Years

• Life Only

• Life with Percent ofPremium DeathBenefit (25% or 50%)

Non-QualifiedPolicies

• Not Available

• Life Only

• Life with Cash Refund

• Life with InstallmentRefund

• Life with 5 to 30 Years

Qualified Policies

• Life with Cash Refund

• Life with InstallmentRefund

• Life with 5 to 30 Years

• Life Only

Roth IRA*

* Single life only, unless otherwise indicated.

FLEXIBILITY AND CONTROLThe Lifetime Income Annuity gives you control of your money by providing you access to funds beyond the scheduled income payments, in the event you need additional cash due to unexpected circumstances.Each policy includes withdrawal features that provide you access to cashin an emergency after you are at least age 591/2.

Payment Acceleration (For Non-Qualified Annuities with Monthly Payments)This feature enables you to receive your next scheduled monthly payment, along with five subsequent payments — for a total of six months of income payments paid to you all at once.When you exercise this option, your income payments will not be paid for the next five months.You may use this feature twice during the life of your policy.

Cash Withdrawal Provides a one-time opportunity to receive the discounted value of future payments.26 Dependingon your policy, you will have access to cash through one of two Cash Withdrawal features.27

Up to 100% Cash Withdrawal28

This feature allows you to withdraw up to 100% of the discounted value of the remaining guaranteed payments at anytime within the guaranteed payment period. Once this optionis exercised, future income payments through the end of the guaranteed payment periodwill be reduced by the withdrawal percentage you elected. If the annuitant is alive at theend of the guaranteed payment period, full annuity payments will then resume for the lifeof the policy.29

30% Cash Withdrawal

This feature allows you to withdraw 30% of the discounted value of the remaining paymentsexpected to be paid to you based on your life expectancy when you purchased your policy.You may exercise this option on the 5th, 10th or 15th anniversary of your first income payment, or upon proof of a significant non-medical financial loss,30 as specified by the policy. Once this option is exercised, future income payments will be reduced by 30% forthe life of the policy.

Taxation of Withdrawals (Fully Taxable)Withdrawals made using the Payment Acceleration feature and the Cash Withdrawal feature willbe reported to the Internal Revenue Service (IRS) as fully taxable.31 In addition, penalty taxes mayapply in certain circumstances as a result of exercising a withdrawal feature under an immediateannuity.32 Please consult with your professional tax advisor.

Not all options are available on all contracts, in all jurisdictions, or to annuitants of all ages.Ask your insurance professional for details.

14

26 The cash withdrawal amount is subject to an Interest Rate Change Adjustment that will increase or decrease the withdrawal amount based on the change ininterest rates, as measured by the 10-Year CMT, between the time you purchase your policy and the time you elect to receive the cash withdrawal. The 30% CashWithdrawal feature is not available after the annuitant’s life expectancy.

27 Policies either offer the “Up to 100%” Cash Withdrawal feature or the 30% Cash Withdrawal feature, but not both.

28 The Up to 100% Cash Withdrawal is not 100% of the original purchase payment and is generally less than this value. Instead, it is based on the presentvalue of the future guaranteed payments on the policy at the time of withdrawal. The guaranteed payment period for the Life with Cash Refund or the Lifewith Installment Refund payment option is determined by dividing the premium paid for the policy by the annualized income benefit amount.

29 For Joint Life policies, full annuity payments will resume for the life of the policy at the end of the guaranteed payment period if at least one of the annuitants is alive at that time.

30 The non-medical financial loss provision is not available in all jurisdictions. Ask your insurance professional for details.

31 The federal income tax treatment of an immediate annuity that contains a withdrawal feature, such as the Payment Acceleration and the Cash Withdrawalfeatures, is uncertain and the IRS may determine that the taxable amount of the annuity payments and/or withdrawals received for any year is differentthan the amount reported by New York Life. For non-qualified policies, the exercising of a withdrawal feature may extend the period over which a policyowner may recover the investment in the contract and may limit the policy owner’s ability to fully recover the investment in the contract over the annuitypayment period because of the reduction or elimination of future annuity payments. The policy owner should consult with his or her own tax advisor prior to exercising a withdrawal feature under an immediate annuity.

32 If the policy owner purchases a policy with a withdrawal feature, such as the Payment Acceleration and the Cash Withdrawal features, before age 59 1/2and exercises the features within five years from the date of the first annuity payment (and after the policy owner has attained age 59 1/2), then a 10%penalty tax (plus interest) may be imposed retroactively on any annuity payments received before the policy owner attained age 59 1/2. The 10% penalty taxwould be in addition to the ordinary income tax on the taxable amount of the lump sum withdrawal. The policy owner should consult with his or her owntax advisor prior to exercising a withdrawal feature under an immediate annuity.

For most jurisdictions, the policy form numbers for the New York Lifetime Income Annuity are: 203-169 for the Life Only Annuity;203-170 for the Primary and Secondary Joint Life Annuity; 203-171 for the Life Annuity With Percent of Premium Death Benefits;203-172 for the Life Annuity With Cash Refund; 203-173 for the Life Annuity With Guaranteed Period Certain; 203-174 for thePrimary and Secondary Joint Life Annuity With Guaranteed Period Certain; and 210-195 for the Life Annuity with Installment Refund.

For most jurisdictions, rider form numbers are 205-300 for the Changing Needs Rider; 206-300 for the Income Enhancement Rider;206-308 and 206-309 for the 30% Cash Withdrawal Rider; and 206-310 for the Up to 100% Cash Withdrawal Rider.

New York Life Insurance Company

New York Life Insurance and AnnuityCorporation (A Delaware Corporation)51 Madison AvenueNew York, NY 10010

www.newyorklifeannuities.com

The Company You Keep®

LIA-1077 (4/11) 421866 (Exp. 5/18/2013)