guano, credible commitments, and state finances in ... · guano, credible commitments, and state...

TRANSCRIPT

Guano, Credible Commitments, and State Finances in Nineteenth-Century Peru September 2006 Catalina Vizcarra Assistant Professor Department of Economics University of Vermont Tel: (802) 656-0694 Fax: (802) 656-8405 [email protected] Abstract A main result in the literature on credible commitments and sovereign finance in the modern period is that financial credibility and political stability go hand-in-hand. Peruvian public finance in the nineteenth-century is an exception. This paper explains how, in spite of Peru’s chronic political instability, the unique characteristics of the guano trade and a web of contracts linking guano export revenues to interest and sinking fund payments made the establishment of credible contractual relations with foreign interests possible. The paper demonstrates that a sufficiently large penalty for default can produce an equilibrium with positive lending, even in highly unstable polities. JEL classification: N26, N46, N56, 017 Keywords: Institutions; Development; Latin America; Resource Curse; Sovereign Debt; Credible Commitments.

Guano, Credible Commitments and State Finances

Introduction

Chronic political instability can hamper economic development if it interferes with

establishment of consistent rules that firms and individuals need in order to have the

confidence to invest. Political instability can also wreck havoc with public finance. A

recent dramatic example was that the Mexican peso crisis in the early 1990s was affected

in no small measure by the assassination of a presidential candidate and the Zapatista

rebellion. The capital flight that ensued was only stemmed when an international lender

of last resort restored confidence.

In the 19th century there was no such creditor country cooperation to assure

investors in the sovereign debt of unstable countries. Much of Latin America spent the

first sixty to eighty years of the 19th century in a cycle of dictatorships and civil wars.

Nearly all had issued debt in the years immediately following their independence, and all

but Brazil defaulted almost immediately after issuing the debt. Most of those countries

could not regain access to international credit markets until they had achieved some

degree of stability. Peru was an exception. Although it was plagued by civil wars like

the rest, it settled its debt in 1849 and for the next quarter century was one of the most

prolific sovereign borrowers in the world. Massive per capita foreign obligations were

obtained by hypothecating returns from the state monopoly of guano, a valuable natural

fertilizer in large demand in world markets.

This paper examines how Peruvian governments persuaded foreign creditors of

their willingness and ability to service their debt faithfully. A central issue in the

literature on sovereign debt is the incentives that a sovereign government has to fulfill its

2

Guano, Credible Commitments and State Finances

debtor obligations. This can be explained in the context of a simple game. Imagine in

stage one, a potential creditor decides whether or not to make a loan to a sovereign

government, and the size of the loan. In stage two, the sovereign decides whether or not

to repay the loan. If the sovereign repudiates the loan, in stage three the lender can

decide whether or not to retaliate, as well as the scope of the retaliation. It is clear that in

a game that is not repeated, any sub-game perfect equilibrium in which lending actually

occurs must involve a credible threat by the creditor to levy a penalty of sufficient size as

to induce the sovereign not to default. This is true because a simple promise not to

default by the borrower is no more than cheap talk.

The literature contains a number of variations of this basic framework, including

different information structures, and dynamic repeated games versus one-shot games.

Following seminal papers by Eaton and Gersovitz, and Bulow and Rogoff, a vigorous

debate has emerged about whether reputation effects or sanctions are more important for

the functioning of the sovereign debt market.1 Reputation effects imply that a default is

penalized either through a future credit boycott, strict limits on future credit, or higher

interest rates on future loans reflecting a default risk premium. Sanctions could imply the

seizure of government assets, impediments to trade credits that could seriously hamper

foreign commerce, or the actual removal of the sovereign if he should violate his

agreements. Sanctions could also take the form of foreign (creditor) government

diplomatic or military pressure.

Surprisingly, little research has been done on the impact of political instability on

sovereign debt contracts. When referred to at all, it is typically taken for granted that

instability contributes to debt repudiation and “zero credit” equilibrium because it 1 Eaton and Gersovitz, “Debt with Potential Repudiation,” and Bulow and Rogoff, “Sovereign Debt.”

3

Guano, Credible Commitments and State Finances

shortens the time horizon of the government. Any government facing a violent threat to

its survival has extraordinarily powerful incentives to abrogate property rights and default

on his financial obligations. Short-sighted governments generally do not care about

building a reputation because the threat of a credit boycott in the distant future is unlikely

to suffice as a deterrent.

The Peruvian experience constitutes, in this sense, an exceptional episode for

expanding our knowledge of sovereign debt. Contrary to the existing literature, Peru’s

re-access to financial markets was not reliant on political stability. Financial credibility

in the British case heavily depended on the stability of political institutions and the

Whigs’ dominance in parliament.2 The expansion of credit in the case of Hapsburg

Spain, Imperial Brazil, and nineteenth-century Mexico was also achieved under the spell

of a stable ruler.3 In contrast, Peru’s early republican period was marked by the

dominance of caudillos (military leaders). The guano windfall had transformative effects

on the Peruvian economy and society but it did not result in the formation of a stable

polity. Guano revenues allowed the central government to buy off rivals through

patronage by maintaining a bloated military and bureaucracy. Paradoxically, the promise

of such power also offered an incentive for ambitious rivals to seek control of the central

government in Lima at all costs. Thus, nineteenth-century Peru remained highly

unstable. How could the bonds of a chronically unstable government like Peru find a

ready market in Europe? How could foreign investors trust such a government to honor

its financial obligations?

2 North and Weingast, “Evolution of Institutional Governing,” Stasavage, Public Debt. 3 Conklin, “Theory of Sovereign Debt,” Maurer, “Internal Consequences,” Maurer and Gomberg, “When the State is Untrustworthy,” Marichal, “Construction of Credibility,” Summerhill, Inglorious Revolution.

4

Guano, Credible Commitments and State Finances

The paper explores how the unique characteristics of the guano trade and a web of

contracts linking guano export revenues to interest payments due to foreign bondholders

made the establishment of credible contractual relations possible. In my argument, the

government’s credibility rested on a web of self-enforcing contracts involving the

Peruvian government, the guano consignees and the bondholders. The link between

guano revenues and debt service was simple and effective. Peru relied on a reputable

British merchant house for the commercialization of guano. Consignees, in particular

Gibbs & Sons, who dominated the trade for two decades, were appointed as the state’s

financial agent and were responsible for withholding a large portion of government’s

guano income (originally 50% of proceeds from the British market) for debt servicing.

Guano revenues were collected by Gibbs in Britain and distributed shortly thereafter to

the bondholders. The operation was clean and did not involve the meddling of the

Peruvian government. Peruvian governments, irrespective of their origin, respected the

guano-debt contracts because default would interrupt the foreign trade in guano, their

lifeline. Impatient “myopic” Peruvian governments could not afford losing such a vital

source of income (between 70 and 80% of government revenues) for that could

jeopardize their grip on power.

The paper proceeds as follows. In the next section I describe the conditions that

determined Peru’s poor financial standing prior to the guano boom. Then I present

evidence on the scale of the guano deposits and the revenues that they generated so as to

demonstrate the immense improvement in the Peruvian government’s financial

capabilities. The economic pre-requisites for debt settlement and lending resumption

were in place, but there remained the issue of the government’s credibility as a good faith

5

Guano, Credible Commitments and State Finances

borrower. In section five I review the theoretical literature on sovereign debt lending that

highlights the credible commitment problem and discuss how to interpret the Peruvian

experience in this context. In sections six and seven, I discuss the settlement and lending

resumption process and show how the unique characteristics of the guano export trade

made it possible to construct contractual relationships that persuaded creditors that the

Peruvian government was committed to paying off its current and any future loans. The

nature of the loan security and the contractual terms meant that the risk associated with

internal political instability could be largely overcome. Section eight presents

quantitative evidence in support of these arguments through a statistical analysis of a

newly collected series of bond prices. The final section concludes.

2. Peru before Guano: Weak and Unstable

During the late colonial period, Peru’s economy was dominated by mineral extraction,

primarily for export, and agriculture, which was largely for domestic consumption. By

the time of its independence in 1825, mining, although still important relative to other

industries was a shadow of its former self.4 The new republic had a population of

approximately two million, but the majority of the population consisted of Indian

peasants who lived in the highlands and relied on subsistence agriculture. A small elite

resided primarily on the coast, particularly in the capital, Lima. The elite specialized in

plantation agriculture, mining and commerce. There was no banking system, and credit

markets were thin, and dominated by personal connections. Foreign commerce consisted

of the exchange of minerals for luxury manufactures with Europe, and agricultural trade

with Chile and Bolivia. 4 Peru declared independence in 1821 but became effectively independent only in 1825.

6

Guano, Credible Commitments and State Finances

There are few quantitative estimates of the size of the Peruvian economy at the

time. An often cited metric of economic activity is Paul Gootenberg’s estimate of

business revenues and prices in the province of Lima.5 According to his estimates, real

business revenues in Lima in the mid 1840s were 15% below levels in 1830.6 More is

known about foreign commerce. Shane Hunt’s estimates of export quantum are widely

considered the best available. Here the picture is slightly better -exports grew at an

average annual rate of about nine percent during the 1830s, principally driven by the

rejuvenation of silver mining and the rapid growth of wool exports. But export growth

slowed considerably during the early 1840s. The general view in the historiography is

that the period preceding the guano boom was one in which the economy was weak and

unstable.7

The economic conditions were mirrored by a high degree of political instability.

Despite the early adoption of a written constitution blending elements of American and

French models, the early republican period was marked by the dominance of caudillos.8

From 1821 until 1845, Peru had 50 changes in government, five constitutions, countless

internal rebellions, and five foreign wars, including wars with each of its neighbors

except Brazil.9

The economic and political environment was hardly conducive to the

development of sound government finance. In addition, Peru at independence was

5 Lima, the richest region, included the major Peruvian port (Callao) and concentrated not only the most important fraction of the local elite, but also a large artisanal sector. 6 Paul Gootenberg, Between Silver and Guano, p.166. 7 For an overview of the Peruvian economy at the time see Carlos Contreras, “La economía peruana,” pp. 277-309. 8 See Aljovín, Caudillos y constituciones. 9 The most severe conflicts were in the late 1830s when a Peruvian-Bolivian confederation was defeated by Chile, and an exceptionally violent period of civil war from 1841-1845 in which the presidency changed hands nine times.

7

Guano, Credible Commitments and State Finances

burdened with large foreign and domestic debt contracted to finance its five-year long

revolutionary war. The lion’s share of the debt consisted of two large external bond

issues, totaling £1.816 million pounds sterling. As described by Carlos Marichal, British

financiers made a series of loans to the newly independent states and revolutionary

governments of South and Central America in the years 1822-1825. Virtually all of these

governments defaulted by 1826, with the exception of Brazil.10

Reflecting the turbulent political atmosphere, statistics on government revenue

and expenditures are scarce. Customs revenue and an Indian head tax – a holdover from

the colonial era – were the two largest sources of revenue. Expenditures exceeded

revenues throughout the period.11 In particular, military expenditures of the government

of the moment could run into £450,000 of pounds sterling a year.12 According to

Gootenberg, however, budget deficits were often covered through “emergency loans”

from domestic merchants. Although these were promised to be repaid from future

customs and other revenue, many of these loans remained unpaid until the 1860s. The

exact amount of this credit will probably never be known, but estimates have put them at

around $3 million pesos (£600,000 pounds) between 1821 and 1845.13 It was against this

backdrop of political chaos and financial ruin that guano emerged as an unlikely savior.

10 Marichal, Century of Debt Crisis, and Neal, “Financial Crisis,”discuss possible reasons for this early “debt crisis.” 11 For a discussion of the ruinous state of government finances in the period see Gootenberg, Between Silver and Guano, and his “Merchants, Foreigners and the State.” 12 There are no systematic data available on such expenses until the first public budget was issued under Castilla in 1845. Military expenditures in his first year in office was around $2.239 million pesos (£450,000), the lowest of the guano era. 13 Gootenberg Between Silver and Guano, pp. 169-171.

8

Guano, Credible Commitments and State Finances

3. The Growth of Peruvian Guano Exports

The existence of deposits of guano on islands near the Peruvian coast had been noted by

travelers for some time. Agricultural chemists conducted experiments with Peruvian

guano and found it contained significant quantities of nitrogen and phosphorus that made

it an especially useful fertilizer, with major advantages over other manures, as well as

bone and dried blood.14 Large deposits were found on the Chincha islands, a group of

three uninhabited islands about 20 kilometers off the coast of Peru, and less than 200

kilometers from Callao, the main port of Lima. Under Peruvian law, they were property

of the state, and because of their isolated location, with a modicum of naval presence they

were not difficult to protect from poachers. Thus, legal tradition and geography made the

enforcement of a government monopoly possible.

The extraction of guano required very little capital investment. It mainly involved

digging the guano and transporting it to chutes that led from the island’s cliffs into the

holds of ships that were anchored nearby. However, it could take over one month to load

a ship, and during the heyday of the trade in the 1850s and 1860s, there were often more

than fifty ships loading at any given point in time. The length of loading time and the

voyage meant that the cost of transport was substantial.15 Procurement of vessels and

coordination of sales, foreign warehousing and marketing were also costly and demanded

a certain degree of expertise that the Peruvian government lacked.

14 Mathew, “Peru and the British Guano Market,” p.113. 15 Transport of guano to foreign markets was estimated at about £4 17s per ton, around 70% of total costs. See Mathew, House of Gibbs, p.29 and “Primitive Export Sector.” See also Levin, Export Economies.

9

Guano, Credible Commitments and State Finances

As a consequence, the state contracted with “consignees” who managed the

export to and marketing in the various foreign markets.16 The largest and most lucrative

contract was for the British market, and the consignee was a highly reputable British

merchant house, Anthony Gibbs and Sons, until 1862. Gibbs earned commissions as well

as a cost-plus arrangement for freight, loading and storage.17 After 1862, the

consignment system was modified so as to permit Peruvian nationals to enjoy more of the

rents, but the key role in Britain remained in the hands of a U.K. firm of high standing,

this time Thomson, Bonar and Co., which had connections to Prime Minister Gladstone.18

As stated above, the principal foreign market for guano was Great Britain, but the

United States, and France were also important markets. Figure 1 shows Peruvian guano

exports between 1845 and 1878. The erratic nature of the data series is deceptive – the

flow of revenues to the Peruvian government was much less variable because of the

holding of stocks by consignees in the importing countries. Unfortunately, outside of

some data for Britain, little direct evidence exists on actual guano sales.

The value of Peruvian guano exports to Britain, which was the destination for

between 1/2 and 2/3 of all Peruvian guano exports, rose dramatically between 1847 and

1860, and it routinely exceeded two million pounds sterling per year. There was a high

degree of price stability. The Peruvian government set a minimum sales price that was

usually binding.19 As a consequence, fluctuations in guano export revenues mirrored

fluctuations in the quantity exported. Because Peru did not publish trade statistics

16 A summary of the main terms of all Peruvian guano export contracts during the guano age is available in Rodríguez “Historia de los contratos.” The actual contracts are available in Dancuart, Anales, various volumes. 17 See Levin, Export Economies, and Mathew, House of Gibbs. 18 Thomson & Bonar remained in the trade until the expiration of their contract in the early 1870s. 19 For most of the period guano was priced at around 12 £ per ton. See Mathew, “The guano trade and the Peruvian government,” p.359 and “The House of Gibbs,” p.29.

10

Guano, Credible Commitments and State Finances

between 1847 and 1877, the value and relative importance of guano exports can only be

estimated. Charles Fenn estimated Peru’s total exports at 2.92 million pounds sterling, of

which 1.56 was estimated as guano. Estimates based upon United Kingdom trade

statistics indicate that between 1854 and 1871, the height of the guano boom, guano

constituted on average sixty percent of the value of all Peruvian exports to Britain.20

4. The Significance of Guano for State Finances

The Peruvian state’s guano monopoly was a revolution for government finance. As is

shown in Table 1, guano exceeded customs revenue beginning in the early 1850s, from

then until the late 1860s it accounted for two-thirds or more of total government revenue.

In the mid 1850s, when guano income was well over two million pounds sterling per

year, Peru reduced import tariffs and abolished the Indian head tax. Tariff revenue still

grew because imports were growing rapidly during the period. Real government

revenues nearly doubled between 1847 and 1852, and doubled again by the early 1860s.

Peruvian government expenditures expanded in tandem with guano income. The

chronic instability led Peruvian leaders to spend freely. There were large increases in

military, naval and bureaucratic expenditures. The lion’s share of the budget was

directed to the armed forces, which excluding debt service represented an average of

between 50 and 75% of the central government budget from the mid 1840s to the late

1860s.21 In the 1870s, railroad construction was a massive expense. Overly optimistic

and/or corrupt railroad investments were a major cause of the catastrophe that marked the

20 United Kingdom trade statistics with Peru were taken from various volumes of Fenn’s compendium, citing U.K. Board of Trade figures. 21 The most reliable source on government expenditures is in Hunt, “Growth and Guano.” Hunt series only covers selected years between 1846 and 1877.

11

Guano, Credible Commitments and State Finances

end of the guano boom. In sum, the guano boom fueled the growth of government so that

Peru still rarely had a budget surplus.

Guano also made possible the settlement of Peru’s revolutionary war debt, and

enabled successive Peruvian governments to tap into credit markets for a variety of

purposes –debt conversion, general expenses, war finance and railway construction.

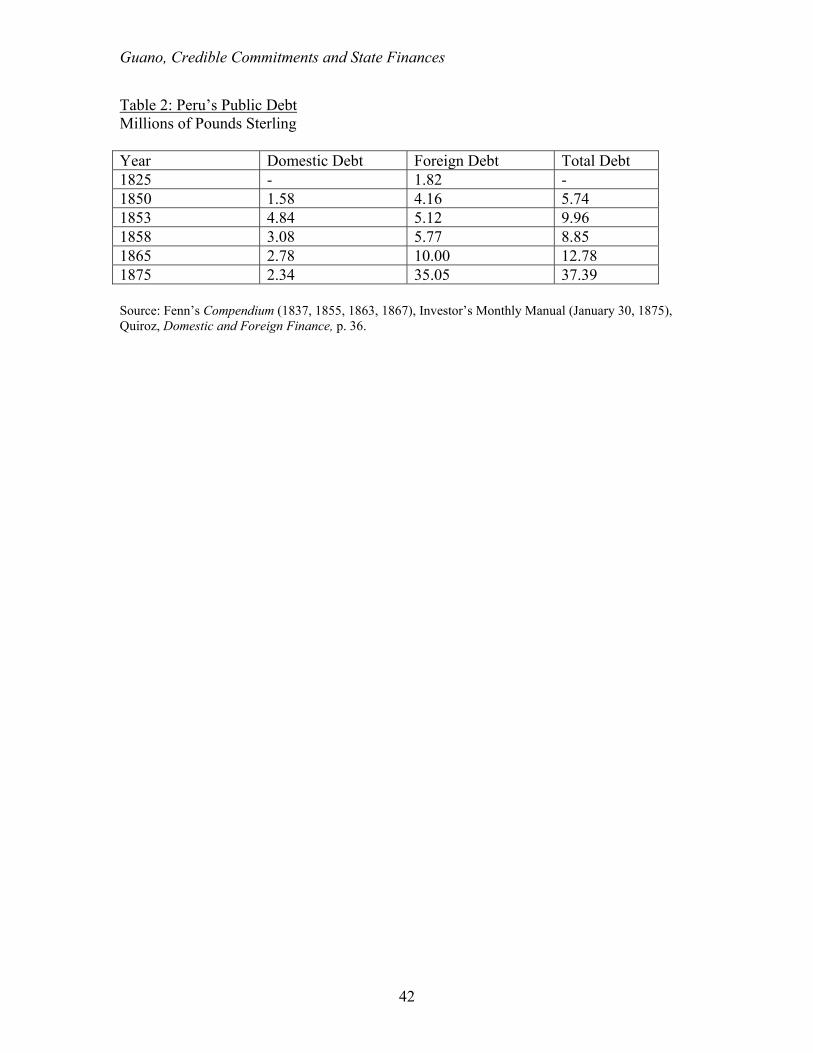

Table 2 shows the total public debt for selected years between 1825 and 1875. During

the entire guano period, foreign loans comprised the majority of the debt. The increase in

domestic obligations was the result of the consolidation process which recognized old

debts generated during the Independence Wars and forced loans of the early caudillo

period. No further domestic debt was contracted until the 1870s, when the government

intervened in the banking system and nationalized the nitrate industry.22

An analysis of foreign debt issues is covered in subsequent sections, but an

overview of their characteristics is given in Table 3. As mentioned earlier, the initial

loans amounted to 1.8 million pounds sterling. Because Peru had been in default for

nearly a quarter-century, significant arrears of interest accumulated. In January 1849 the

Peruvian government reached a settlement with British bondholders. Under the scheme,

the principal of the old loans was converted into new bonds for a total of £1,759,100,

25% of the interest was written off, and the remainder of the accumulated interests for

£1,854,700 pounds was floated as “passive” bonds, which would not begin to pay interest

until April 1852.23 Both issues were secured by up to fifty percent of government

revenue from the guano monopoly.

22 See Quiroz Domestic and Foreign Finances, and Deuda defraudada,on the corruption scandals associated with the consolidation process. 23 Dancuart, Anales, vol 4, p.43. Casa Murieta was in charge of the conversion for a 0.5% interest charge over the total. Dancuart, Ibid. vol 5, chp. 5, p. 33-36. The active bonds yielded a 4% interest since April 1,

12

Guano, Credible Commitments and State Finances

In 1853, Peru borrowed on four separate occasions. The first was a conversion

operation on the 1849 bond representing the principal of the 1822 loan, which also

produced a significant inflow. Two others were issued a few months later, one placed in

Paris and the other in England. They effected a conversion of domestic debt into external

debt. These loans were for a total of approximately 2.4 million pounds, and as is

subsequently discussed, were highly unpopular with the bondholders of the main British

loan of February 1853. A fourth loan was also issued for the construction of a railroad in

southern Peru in the amount of 403,000 pounds. In each case the loans were formally

guaranteed with guano revenues. Charles Fenn, commenting on these loans in 1855,

calculated total debt service at 267,000 pounds sterling per year, and stated that “...should

the consumption of guano in this country (the U.K.) continue at the same rate, and the

terms of the debt remain unaltered, the liabilities of the Peruvian Government will only

amount to a little more than one-third of the proceeds of the guano [sold in the United

Kingdom].”24

Another conversion was undertaken in 1862, which also yielded more than two

million pounds sterling to the government. Later, during war with Spain in 1865, Peru

was able to place a loan in Europe for ten million pounds and another in the U.S. in 1866.

In the late 1860s Peru, like many other countries around the same time, began a major

campaign of railway construction. Three loans were issued, in 1869, 1870 and finally, in

1849. The interest rate on these bonds, however, was scheduled to increase by 0.5% points annually until reaching a ceiling of 6% in April, 1853. The passive bonds, on the other hand, had interests of 1% a year starting in April, 1852. This rate was scheduled to rise by 0.5% annually up to 3% in April, 1856. In addition, sinking funds for both bonds were scheduled to start only in April, 1856. The latter was established at 1% for the active bonds and 0.5% for passives. 24 Fenn’s Compendium, 1855, pp. 206-207.

13

Guano, Credible Commitments and State Finances

1872, which paid off the 1865 loan but added enormously to the foreign debt. These last

loans were earmarked primarily for railroads.

Peru secured those loans with guano as well as the planned railroads, but it was

strongly suspected that the deposits of the Chincha Islands were nearly exhausted. Peru

publicized the surveys of vast new deposits at Pabellón de Pica, Penita de Lobos and Las

Huanillas. A British Parliamentary report in 1874 confirmed the near-exhaustion of the

Chinchas and questioned the veracity of Peru’s new claims, but the news came too late

for Peru’s unfortunate creditors. Further, farmers began complaining about the inferior

quality of the recent Peruvian guano exports. To make matters worse, guano began to

face increased competition from nitrate of soda, a mineral, and ammonium sulfate, a by-

product of coke production. Under the weight of this new debt, and with the decline of

guano, Peru defaulted on its foreign debt in December, 1875.

The foregoing discussion illustrates that the very significant increase in

government revenue due to the guano windfall coincided with Peru’s resumed access to

international capital markets. Guano had transformative effects on the Peruvian

economy, state finances and sovereign debt. It also transformed Peruvian politics and

society, but it did not result in the formation of a stable polity. On the contrary, Peru

continued to be dogged by infighting, civil conflict, coup d'etats, and foreign wars. How

could the bonds of such a country find a ready market in Europe? How could foreign

investors trust such a government to pay its debt? The answers to these questions require

an analytical framework.

14

Guano, Credible Commitments and State Finances

5. The Enforcement of Sovereign Debt Contracts

The problems confronted by governments in establishing credible commitments with

creditors are well known. Sovereign contracts are not subject to third-party enforcement.

Thus, unless lenders (often in combination with the sovereign) orchestrate a credible

threat to levy a sufficiently large penalty in case of government default, the promise to

repay is not credible.

Theoretically, a sovereign can commit to honor his financial obligations in two

ways. One is by building a reputation so he can access credit in the future. Reputation

effects imply that a default is penalized either through a future credit boycott, strict limits

on future credit, or higher interest rates on future loans reflecting a default risk premium.

Alternatively, the government can commit by orchestrating an increased penalty for

default over and above the threat of credit restrictions. Those penalties (or sanctions) can

take several forms. They can emanate from domestic political institutions that punish the

ruler if he should repudiate the debt, like in the emblematic case of Great Britain; from

ad-hoc contracts that explicitly link debt repayment to sanctions radiating from a

complementary (nonlending) relationship, like in Hapsburg Spain, or from foreign

government diplomatic or military pressure as with regard to U.S. imperialism in the

Caribbean in the early 20th century.25

Reputation effects heavily rely on the ability of creditors to deny future credit to a

defaulting sovereign. The effectiveness of such a threat, however, will depend upon the

cost to creditors of imposing the penalty, as well as the unity of all creditors undertaking

25 North and Weingast, “Evolution of Institutional Governing,” Conklin, “Theory of Sovereign Debt,” Mitchener and Weidenmier, “Supersanctions.”

15

Guano, Credible Commitments and State Finances

the punishment in response to a default on some subset of creditors.26 In the extreme

case when the creditor is a monopoly, this unity may be trivial. When there are many

potential creditors, however, the problem is more severe. The literature has shown that

banking syndicates, bondholders’ committees, and regulations of creditor country

governments or stock exchanges, and political institutions can all play roles in cementing

that unity.27 Even a credible threat of a credit boycott would fall short of persuading a

sovereign not to default, if, for example, the debtor country is able to save in financial

assets.28 Moreover, it is unlikely that reputation effects would be effective under political

instability. Any government facing a violent threat to its survival has extraordinarily

powerful incentives to default on their financial obligations. Short-sighted governments

generally do not care about building a reputation because the threat of a credit boycott in

the distant future is unlikely to suffice as a deterrent.29

If the literature with respect to reputation effects seems disparate, it is also true

that there is no consensus about the importance of sanctions. Particularly important is the

role of political institutions, potential trade embargos, and military and diplomatic threats.

Douglass North and Barry Weingast explored the role of domestic political institutions in

building government credibility in their seminal work on British sovereign debt. The

establishment of representative political institutions in the aftermath of the Glorious 26 Weingast, “Political Foundations.” 27 With respect to the unity of potential creditors, see Bond and Krishnamurthy, “Regulating Exclusion,” Conklin, “The Theory of Sovereign Debt,” Johnson, “Banking on the King,” Mauro and Yafeh, “Corporation of Foreign Bondholders,” and Weingast, “Political Foundations.” Even a monopoly creditor needs to make credible its threat of a credit boycott. This problem bears some similarities to models of predatory pricing and “tit-for-tat” strategies that maintain cooperation. Credit boycotts could occur in a repeated game in which the creditor gains by establishing its own reputation as being tough on delinquent debtors. 28 See Bulow and Rogoff, “Sovereign Debt.” 29 One exception is Amador, who presents a model in which political uncertainty generate an equilibrium with positive lending. His model, however, assumes a democratic regime, where parties alternate in power. Incumbents have an incentive to honor their debts because they can benefit from access to financial markets in the future. See Amador, “Political Economy.”

16

Guano, Credible Commitments and State Finances

Revolution gave Parliament substantial prerogatives in the area of public finance, setting

effective boundaries on the sovereign’s ability to renege on her financial obligations.30

Setting the “right” political institutions, however, is neither a necessary nor a sufficient

condition for the expansion of credit. As Stasavage has shown, the role of veto players is

critical in establishing such credibility. The Whigs’ predominance in Parliament was

essential to reassure lenders of the government’s commitment.31

In contrast to the British case, Peru’s early republican period was marked by the

dominance of caudillos. The guano windfall had transformative effects on the Peruvian

economy and society but it did not result in the formation of a stable polity. As discussed

above, Peru’s political atmosphere was not conducive to the establishment of sound and

stable political institutions. Throughout the guano age, Peru continued to be dogged by

infighting and civil wars. Table 4 describes all Peruvian chief-executives and the manner

in which they were selected during the guano age. As the table illustrates, in the lapse of

thirty years (from 1845 to 1876) Peru had sixteen presidents, of which ten accessed

power through violent means, usually after a major rebellion or civil war.

But, what of the threat of trade embargoes and military sanctions? Some argue

that such pressures on behalf of bondholders were not decisive,32 while others are more

sympathetic.33 The evidence suggests that on some occasions such pressure was

important, for example with regard to U.S. imperialism in the Caribbean in the early 20th

century, or the foreign operation of Chinese customs in the 19th century. More relevant

for our discussion is the extensive scholarly examination of British Foreign Office

30 North and Weingast, “Evolution of Institutional Governing.” 31 Stasavage, Public Debt. 32 Platt, Finance,Trade and Politics, and Tomz, “How do reputations form?” 33 Finnemore, Purpose of Intervention, and Mitchener and Weidenmeier, “Supersanctions.”

17

Guano, Credible Commitments and State Finances

archives, which suggests that there was no consistent policy on the part of the British

government of backing up bondholders with military, economic or diplomatic threats.34

In particular, the records suggest that the British government did not issue any

commercial, diplomatic or military threats to the Peruvian government in behalf of the

bondholders –more on this later.

Thus, why and how did Peru resume payment on its debt in 1849? Why did

foreign creditors grant large new loans in 1853? After twenty-seven years in default, it

was not enough to show the ability to pay by publishing reports of official surveys on the

size of guano deposits. Peru, unlike Britain after the Glorious Revolution, lacked stable

political institutions with real veto power that could allow credit to expand. Peruvian

politics continued to be plagued by autocrats, frequent changes in government, internal

rebellions, and foreign wars. What the country needed was to find an alternative

mechanism to raise the penalty that creditors could impose on it if it defaulted again. The

penalty had to be sufficiently large, direct and imminent so as to persuade even short-

sighted governments of the benefits of repayment. As I discuss in the subsequent

sections, Peru was able to find such a mechanism by securitizing its guano deposits. This

was possible because the special characteristics of the guano deposits and the collection

of revenues from its export made it feasible to design a series of contracts that

bondholders would trust.

6. Debt Settlement: The Carrot and the Stick

In January 1849 the Peruvian government reached a settlement with British bondholders.

As described earlier, the principal of the old loans was converted into new bonds for a 34 Platt, Finance Trade and Politics, pp. 34-53.

18

Guano, Credible Commitments and State Finances

total of £1,759,100, 25% of the interest was written off, and the remainder of the

accumulated interests for £1,854,700 pounds was floated as “passive” bonds, which

would not begin to pay interest until April 1852. Both issues were secured by up to fifty

percent of government revenue from the guano monopoly.

The 1849 settlement was a necessary pre-requisite for regaining access to

international credit markets. At the time, British and Continental bondholders were able

to exert pressure on delinquent debtors through a simple institutional device: the leading

European stock exchanges would not list any new issue proposed by a defaulting state.35

Peru issued new debt only in 1853, after four years of “good behavior.” Peruvian guano

exports had only begun to exceed 50,000 tons in 1847. Unless guano exports remained at

high levels, Peru would have to cut spending or raise taxes in order to meet its

obligations. No Peruvian government in the early republican period had demonstrated its

ability to accomplish that.36

The ability of Peru to maintain high levels of export revenues depended on the

extent of its guano deposits and whether or not it faced serious competition from abroad,

as it did from Africa in the mid 1840s.37 Surveys of the Chincha Islands were conducted

in the 1850s, and the surveys included foreign observers. In 1851, for example, it was

estimated that the guano deposits were of around 26 million tons, which would last –at

current export rates- until the year 2112. In 1853 the deposits were estimated at a total of

35 Borchard, State Insolvency, p.xxiv. 36 The most recent attempt to resume payment on the foreign debt occurred in January 1842 when the Peruvian government approved a decree that promised half of guano proceeds to the British bondholders. The terms of the decree were never followed. Exigent circumstances existed – the Peruvian government fell and there were numerous changes of government in the next few years, and the guano revenues were nowhere near the level that initially had been forecasted. The 1842 decree can be found in Dancuart, Anales, vol. 3, chp. 2, p.155. See also the letter of G.R. Robinson, chair of the Committee of Spanish-American Bondholders, to The Times, dated February 26, 1847. The Times, 13 March, 1847. 37 The guano deposits, found off the west coast of Africa, were depleted in the course of four years. It was much cheaper than Peruvian guano, and as a result captured a good size of the market in the mid 1840s.

19

Guano, Credible Commitments and State Finances

around 12.5 million tons. A member of the British government wrote in 1854 that it

would take about four decades to exhaust the deposits of the Chincha islands alone –

which had the best quality deposits, and that considering the other deposits, guano was

possibly inexhaustible. In 1859 an American trade journal suggested a figure of 27

million tons for the Chincha islands and others. The grimmest view calculated the

Chincha deposits at about 6-8 million tons, which still implied a long life span for guano

deposits.38

Insofar as outside competition, the most significant new discoveries, the Lobos

Islands, were also claimed by Peru. No comparable guano deposits were found, nor were

they likely to be. The exceedingly arid climate and the nutrient-rich Humboldt current

made the Peruvian coast an ideal location where guano could accumulate. Many

locations had one of those two key characteristics, but not the other.

Peru remained politically unstable, however, and the investment of guano

revenues in an uncertain scheme to regain access to international capital at some future

date does not seem to gibe for a government with a high discount rate. Notwithstanding,

there are mitigating circumstances. First, Ramón Castilla, Peru’s president at the time,

had been in power for more than three years when the settlement was reached, making his

government the longest in the republic’s brief history. According to the portrait of

Castilla advanced by one of Peru’s most eminent historians, he cared more about the

future financial condition of the state than previous rulers.39 Perhaps he was sufficiently

self-confident that he believed his government would last.

38 See for example, The Times, 17 October 1853; Statement of E. Escobar de Bedoya, Attaché to the Legation of Peru in Paris, New York, The Times, 23 November 1853. Also see Dancuart, Anales vol. 5, p.18, and Mathew, House of Gibbs, p. 146. 39 Basadre, Historia de la República, vol.3, pp.87-89.

20

Guano, Credible Commitments and State Finances

Notwithstanding, Castilla was succeeded by Rufino Echenique in 1851. Three

years later, however, he overthrew the latter and regained power. After fending off a

series of revolts, he finally relinquished power again in 1862, only to attempt two other

coups before his death. Given his personal history, it seems entirely possible that Castilla

had a lower discount rate than other Peruvian rulers. A careful account of flows of guano

revenues from 1849 to the end of his period in office shows that he received net flows (in

the form of cash advances from the consignees) for as much as £344,400 pounds.40 The

government commitment with the bondholders on the other hand, for the same period,

summed up to around £202,768 pounds.41 That is, settlement did not pose a negative

flow and no additional risk to losing power. The government continued to receive large

positive balances.

What of the threat of sanctions? Is there any evidence that Castilla, or other

decision-makers in his government, settled the foreign debt due to fears that the British

government might intervene by either seizing guano cargos abroad, or affecting guano

trade? Alternatively, did continued growth in exports to Britain depend on settlement

with the bondholders? It was certainly the case that after the relatively high levels of

exports in 1847 and 1848, the bondholders felt that Peru had the ability to pay, but not the

will. The bondholders had been pressing the British government for assistance for years,

40 From the December 1847 contract with Gibbs, £90,000 pounds. From the October 1849 contract, with the same house, £94,400 pounds. And from the May 1850 contract, again with Gibbs, £160,000 pounds. See the contracts in Dancuart, Anales, vol 4, chp. 5, with the exception of the 1850 one which was never published. See Mathew, House of Gibbs, for details on the 1850 contract, pp. 104-105. 41 It could be decomposed in the following way: 50% of guano revenues produced from January 1850 to April 1851. Sales in that period were of around 135,068 tons. Considering costs of around £6 pounds per ton, total net revenues would have amounted to around £405,204 pounds (price per ton was around £9), substracting consignees commissions, which were of around £71,666, we end up with a net total of £333,537 pounds. From the latter, 50% belonged to the bondholders £166,768 + £36,000 from interests in year 1849, totaling £202,768 pounds. The estimation of consignees’ commissions is derived from Mathew, House of Gibbs, p.104.

21

Guano, Credible Commitments and State Finances

and the increase in guano exports beginning in 1847 led them to renew their campaign.

They passed a series of resolutions in July of that year, including a formal request to the

British government for aid, and they resolved “…that it appears abundantly evident to

this meeting...that there exist within the territories of [Peru] ample resources in the

article of guano alone to provide for the liquidation of its foreign debt; and that

consequently the Government is bound by every principle of public faith and national

honour to proceed to that stipulation without further delay.” 42

Studies on this precise issue concluded that the Foreign Office communicated its

displeasure to the Peruvian Government, but that no threats were issued.43 In particular, a

famous circular signed by Lord Palmerston in January 1848 stated that the British

Government had absolutely no obligation to make delinquent sovereign debts a matter of

even diplomatic negotiations, not to mention military intervention. Palmerston, however,

left the door open to possible diplomatic action if the “loss occasioned by the non-

payment of interest...might become so great that it would be too high a price for the

nation to pay.”44

But, what of Peruvian perceptions? The possibility of British intervention – even

seizure of the islands – was openly discussed in Peru. Peruvian Finance Minister Del Río

in his Memoria in 1847, expressed the government fears that “…until the foreign debt is

settled, the remission of guano abroad…could bring major complications that we must

avoid”.45 One can not disentangle the precise motivation for such an announcement.

42 The Times, 24 July 1847. 43 For a comprehensive and exhaustive analysis of this point see Mathew, “First Anglo-Peruvian Debt.” See also Platt, Finance, Trade and Politics. For an alternative (but not as well documented) view see Levin, Export Economies, and Palacios Moreyra, Deuda anglo-peruana. 44 Parliamentary Papers, 1849 (1049), LVI, reprinted in Platt, Ibid., pp. 398-399. 45 Del Ríos’ Memoria is reproduced in Dancuart, Anales, vol. 4, p.107.

22

Guano, Credible Commitments and State Finances

From a game-theoretic perspective, it is more important what the Peruvian decision-

makers actually perceived than what the British intended. Moreover, to obtain credit,

Peru might have wanted to convince potential foreign creditors that the Peruvian

government feared intervention so that they would repay. Actual repayment would be

consistent with that belief being held. Similarly, if bondholders believed that their

government would enforce payment, they would loan freely. As stated above, however,

the literature suggests that no serious threats either diplomatic or military were issued,

making it unlikely that the threat of sanctions was a decisive factor in the settlement

process.46

7. Establishing a Credible Commitment: The Guano Export Contracts In 1852 the Peruvian Congress authorized its representative in London to negotiate the

terms of a new debt issue. An agreement was reached in early 1853, and the prospectus

for the debt issue was advertised February 26. The loan, as discussed earlier, would

redeem the outstanding bonds from 1849 that were scheduled to take on an interest of six

percent in April 1853, and still yield a net capital inflow of over 600,000 pounds sterling.

The issue, priced at 85, came at a lower rate of interest (4.5%), and annual sinking fund

payments of two percent were committed.47

Yet the 1853 bonds represented new debt. So why did bondholders believe Peru’s

promise to repay? In other words, how could they be sure that the guano proceeds would

be used as stipulated in the terms of the bond contract? As discussed above, the literature

46 See Platt, Finance, Trade and Politics, Mathew, “First Anglo-Peruvian Debt,” and Tomz, “Finance and Trade.” 47 The Times, February 26, 1853. The interest rate charged Peru was the same as that on a smaller Brazilian issue in 1852, and less than the six percent three million pound Ottoman loan of 1854 – the first of a long series by that country. The Brazilian loan was priced at 95 and the Ottoman loan at 80. The figures are from Clarke, “Debts of Sovereign,” pp. 314-315.

23

Guano, Credible Commitments and State Finances

suggests that a higher penalty for default can generate increased access to credit. In our

case, the penalty does not appear to have come from the threat of military or diplomatic

sanctions. I argue that the increased penalty was the potential major loss in government

income due to the disruption of the guano trade in case of government default.

It was not uncommon for governments to pledge government revenues – usually

customs revenues – for the payment of interest and sinking fund obligations. The

original Peruvian loans were “secured” by such a promise. In a number of Latin

American cases, such pledges were ignored at the government’s convenience.48 Guano

had the potential to be superior collateral because revenue from it was collected at the

point of sale abroad. A bondholder quoted in the Times in April 1857 said exactly as

much. “The security of the guano is unquestionable, and from its local situation is

beyond the reach of any Government in Peru to control...and it must be borne in mind

that the proceeds are received in England and not in Peru.”49 In assessing the history of

Peru’s credit, Fenn, the publisher of Britain’s most important manual of stocks and

bonds, observed that, “Above all, in distinction from other securities hypothecated by

foreign states, the transfer was so easy, the Peruvian revenue being, as it were, collected

in Europe – that Peru grew in favour with European capitalists.”50 Fenn’s reference to

the same argument advanced twenty years earlier suggests that this perspective was

probably held by a large number of bondholders, and contributed greatly to confidence of

lenders and investors alike.

48 See Fenn for such repudiations in the case of Colombia, Ecuador, Mexico and Venezuela during the 1840s and 1850s. 49 The Times, 23 April 1857. 50 Fenn, Compendium, 1876, p. 387.

24

Guano, Credible Commitments and State Finances

The practical linkage of the guano trade to the debt service was simple and

effective. Recall that because Peru did not possess the expertise and connections for

selling guano in European markets, they relied on consignees –Gibbs for Britain until

1862, and later Thomson, Bonar and Co.51 In the consignee contract of 1849 Peru

specified the consignee as the financial agent for the service of the debt. The terms of the

debt settlement in 1849 were agreed upon the same day that the Gibbs contract was

renegotiated.52 According to the contract, Gibbs were responsible for withholding a large

portion of guano income (originally 50% of proceeds from the British market at the time)

for debt servicing. The export revenues were collected by Gibbs in Britain and

distributed shortly after to the bondholders. The operation was clean and did not involve

the meddling of the Peruvian government.

Still, the bondholders needed to have confidence in that the consignee-agent

would not collude with Peru to defraud them. Thus, Peru needed to specify a firm that

would lose a lot by taking such action. A firm with substantial reputational capital would

be less likely to collude with a foreign government because it could cost them their

network. Mathew, in his monumental work on Gibbs and the guano trade, stresses

precisely this point: “Gibbs’ base was the London money market and therein they were

attempting, with substantial long-run success, to build up a large acceptance business.

Progress in this field had to do with the marketability of ones name and reputation.”53

51 After the expiration of the contract with Thomson, Bonar and Co, a new contract was signed with the House of Dreyfus. Dreyfus was appointed financial agent and received monopoly rights to sell guano in all of Europe and its colonies with the exception of Cuba and Puerto Rico. 52 Both contracts were negotiated on 4 January 1849. The contracts can be found in Dancuart, Anales, vol.4, pp. 33-39. 53 Mathew, House of Gibbs, p. 242.

25

Guano, Credible Commitments and State Finances

Perhaps the best illustration of the significance of this arrangement is expressed in

Castilla’s confession to the British Charge d’Affaires in October 1849, that his main

reason for persisting with Gibbs was his wish to establish Peru’s credit on a firm basis.

Mathew (1981) adds “… the fact that the funds due to them came from a reputable

London merchant house and not from exposed government coffers in Lima gave them

great confidence in Peruvian paper.”54 Further, because the consignee-agent was a legal

entity in Britain, it could reasonably fear a lawsuit, as later occurred when Peru defaulted

in 1875.55 The costs of litigation and the risk of liability, even if a relatively low

probability outcome, could ruin even a large merchant house because of the funds at

stake.

But, what would have been the consequences if Peru reneged on its consignee

contract because Gibbs refused to collude in defrauding the bondholders?56 Such an

action would have implied a sudden interruption in the flow of guano income, which in

the context of political instability could topple the government because of Peru’s

enormous dependence on guano and its complete inability to save.57

At the onset of the guano boom in the early 1850s, Presidents Echenique and

Castilla radically reformed the tax system. Some of the key changes included massive

54 Idem. p. 233. 55 For a brief introduction to the legal battles between bondholders and guano consignees see Wynne, State Insolvency, vol.2, pp. 127-136. 56 The latter would have entailed finding another consignee willing to enter into business with Peru, and that possessed the capacity for raising the capital for transportation and storage, as well as the skills in marketing the guano. By their experience, Gibbs had developed a considerable advantage in these departments and finding an equally adept export consignee willing to risk their reputation would be difficult. On these points, see Mathew, House of Gibbs, p. 243. 57 The issue is further complicated by the consignee’s practice of advancing future guano revenues to the state. These short-term loans were quite substantial and the main source of regular government income at the time. For much of the period regular stipends in the form of cash advances were of around £300,000 pounds per year – a sizable sum in relation to annual debt service on the bonds. In the event that Peru reneged on Gibbs, Gibbs might have seek a legal remedy to cover its advances if not against the Peruvian government itself, against any future consignees. Gootenberg Between Silver and Guano, p. 130.

26

Guano, Credible Commitments and State Finances

reduction in tariffs, commercial treaties with foreign countries, and the abolition of the

tribute (Indian head tax). The reduction of tariffs and abolition of the head tax comprised

close to 70 percent of government income in the pre-guano era. Re-imposition of the

head tax or raising tariffs would entail political negotiations that could be time-

consuming and perhaps have unintended political consequences. There is well

documented evidence of major resistance to any tax reforms (re-imposition of these

measures) in the period.58 Furthermore, a fall in guano exports would cut into imports, so

that even with an increase in tariff rates, positive effects on revenue would be uncertain.

This meant that, at least in the short term, there was no alternative to guano –see

Table 1 for a description of the relative importance of different sources of revenue

throughout the period. This raises the penalty from default because the opportunity cost

is very large. Historians have typically interpreted Peru’s tax reforms of the 1850s as

motivated by domestic political considerations, but the problem of credible commitments

offers another possible explanation. By increasing dependence on guano, Peru made its

commitment to the bondholders more credible because it could not risk interrupting the

guano trade. Any Peruvian government could not take the risk. Thus, Peru’s notorious

political instability was not an impediment to the credible commitment to repay loans.

Because of the nature of the guano security, the identity of the government was of

secondary concern.

8. Evidence from Financial Markets Peru’s commitment to repay had to meet some threshold of credibility simply to be able

to resume borrowing. But how credible was Peru relative to other debtors? And were

58 For a succinct overview of the political economy of tax reforms see Pike, Modern History.

27

Guano, Credible Commitments and State Finances

investors rattled by Peruvian internal political events? There are two types of evidence

that I examine to answer these questions. First, I compare Peru’s access to foreign credit

with that of different Latin American countries at the time by displaying some statistics

on debt to export and debt to population ratios. Second, I examine the performance of

bond prices and yields, and their sensitivity to events that transmitted information about

the adequacy of guano revenues for debt service -the size of the guano deposits, the

government’s control over the guano islands, changes in the amount of debt outstanding,

and sinking fund payments- and those that do not transmit information about the

adequacy of the guano deposits –internal rebellions and wars that did not involve the

security of the guano islands. Through this analysis I wish to gain insight as to whether

or not investors were concerned about Peruvian politics or if, as I argue in preceding

sections, they perceived that the nature of their contractual relationship with the Peruvian

government did not depend on the structure or stability of Peruvian political institutions.

Table 5 provides a basis for comparing the relative debt burdens of Latin

American countries in the early 1850s. Note that only Peru, Brazil and Chile were

solvent at the time, and of those three countries Peru’s debt to export and debt to

population ratio were substantially higher. This suggests that Peru might have been

closer to its credit limit. If Peru were closer to its credit limit than the other two

countries, then the yield on its bonds would likely reflect a higher default risk premium.

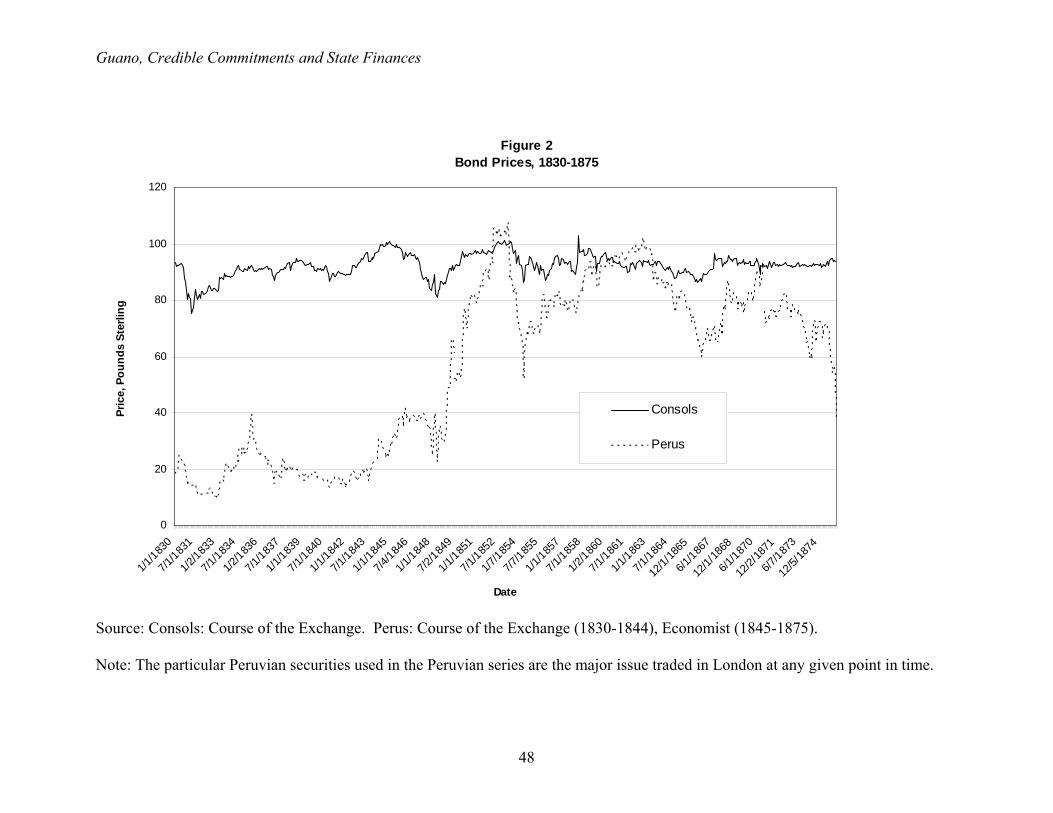

In Figure 2 I show the price of the major Peruvian bond of the moment and that of

the British consol, as a low-risk comparison, for the years 1830 to 1875. Figure 3

compares the Peruvian yield spread versus the consol to the yield spreads of Brazilian

28

Guano, Credible Commitments and State Finances

and Chilean bonds for 1830 to 1875.59 The first two decades of the series in Figure 3 are

not true yield spreads, because Peru was in default and there were no interest payments

(Chile was also in default until 1842). The salient feature in the figures is the dramatic

increase in the price of Peruvian bonds and decrease in the spread coinciding with the

resumption of debt service under the guano-debt contracts of 1849. The price of

Peruvian bonds rose by more than 33 percent between December 1848 and January 1849,

and the sharp rise continued over the next several months. The Peruvian-British consol

yield spread decreased to 2%, which was lower than those of Brazil and Chile -the most

stable countries in the region.60 This result is remarkable considering that Brazil was the

only country in Latin America that maintained an impeccable record of interest and

sinking fund payments since the early loans of the 1820s.61

The next major movement in the graphs occurred in 1853-54. The prices of

Peruvian bonds fell and the yield spread increased. This corresponds to significant

uncertainty about the adequacy of the guano revenues to cover a sudden increase in the

debt burden. As discussed earlier, in February 1853 Peru floated new debt. This loan, a

4.5% per cent issue for £2,600,000 was created for the conversion and/or redemption of

various liabilities that were carrying higher interest charges. The latter included the

active bonds of 1849, which at this point yielded a 6% interest rate. As shown in Figure

2, there was a precipitous decline in Peruvian bond prices in that year. Also, in Figure 3

we observe an increase in the spread from 2% in May of 1853 to a spread as large as

5.1% by April 1854. Interpretation of 1853-54 is complicated by the fact that the consol

59 The data presented on Peruvian and Latin American bonds have been taken from The Economist and the Course of the Exchange. Monthly prices of British consols, a low-risk security used for comparison, were taken from the Course of the Exchange. 60 Brazil was a monarchy and Chile was close to a functioning democracy. 61 For a discussion see Summerhill, The Inglorious Revolution.

29

Guano, Credible Commitments and State Finances

also suffered a marked decline. Notwithstanding, the exceedingly strong fall in Peruvian

notes coincides with the controversy over the consolidation of the internal debt and its

unexpected conversion to external debt through the Uribarren and Montané loans of mid

1853. Bondholders complained that the issues were diluting the value of their

investments, even if guano was available in sufficient quantities to secure the loan.62 The

conversion of the domestic debt was highly controversial not only in London but also in

Lima, where it was seen by many as a massive scheme to defraud the nation by

recognizing some highly questionable debt claims of those politically connected with the

Echenique government. Dissatisfaction with this operation was a major impetus for

Castilla to wage a war against Echenique, driving him from power in January 1855.

The next large price movements occurred in 1855 and in 1858, which correspond

with increases in sinking fund payments. The sinking fund on the February 1853 loan

increased from 2% to 5% by the end of 1854, and from 5% to 8% in 1858. Increasing the

sinking fund effectively shortened the term of the loan, reducing the risk that guano

supplies would run out or that some other unforeseen event would cause a default. After

the first increase Peru’s yield spread approached that of Chile’s. After the second the

yield spread on Peruvian bonds was comparable to Brazil’s.

Figures 2 and 3 also illustrate an important decline in Peruvian bond prices and

increase in the yield spread during the Spanish-Peruvian conflict (1864-1866). There are

strong reasons to believe that the war was responsible for the unusually poor performance

of Peruvian bonds during this period. The conflict originated in 1864 when the Spanish

ordered a naval expedition to seize the guano-rich Chincha Islands.63 The islands were

62 The Times, 6 August 1855. 63 See Pike, Modern History, p.115, for a brief description of the events that provoked the Spanish invasion.

30

Guano, Credible Commitments and State Finances

seized between April 1864 and January 1865. In January 1865 Peru and Spain signed the

Vivanco-Pareja treaty. Under the terms of the treaty Spain withdrew from the islands in

exchange for an indemnification. Many considered the treaty as an affront to national

honor and shortly after, in January 1866, President Prado declared war on Spain.64

Importantly, throughout these years the perception in Britain was that the Chincha islands

were under serious threat.65 After Peruvian victory was secured, by mid 1866, bond

prices began to recover and the yield spread initiated a downward trend.

The final feature is the movement toward default in the 1870s, as the crushing

railway debt Peru took on in 1870 and 1872 required too great a burden for guano

revenues to meet. The yields on these new bonds were considerably higher than previous

ones. The sudden jumps in the yield in 1870 and 1872 observable in Figure 3 occur when

those bonds are issued.

Not only was the debt burden immense, but, as mentioned earlier, a sudden

decline in the guano market coincided with the increase in debt. Ironically, a contributing

factor was increased competition from nitrate of soda as a fertilizer, which was also

found in great quantities on Peruvian territory. The Government took measures to

establish a monopoly that would protect its guano revenues and supplement them, but the

cost of expropriation proved immense and it was only carried out by virtually stripping

the local banks of liquidity. Suspension of convertibility followed closely thereafter, and

the state’s finances collapsed. This is well put in President Pardo’s message to Congress

in 1874, “My predecessor, Balta, formed the idea to convert our guano into railways. In

two years he contracted for nine railways to cost 125 million dollars – say 24 million

64 Building on such discontent, Castilla and Prado led an insurrection that placed the latter in power in November of 1865. 65 See for example, The Times, 4 March 1865.

31

Guano, Credible Commitments and State Finances

pounds sterling, which money being raised by foreign loans, the Dreyfus guano contract

for 8 ½ million dollars per year would pay the interest. Such enormous loans soon

crippled us, as the railways were unproductive. At the same time the sudden influx of

twenty millions sterling in two years upset our equilibrium. Everything ran up to

fabulous prices...then came failures and suspensions and all the troubles that have

reduced Peru to her present wretched condition.”66

What is most remarkable about the data is the relative unimportance of internal

politics. Of all of the major price movements in Peruvian securities from 1849-1875,

none can be associated with Peruvian political instability. In Table 6 we see the

correlation between major rebellions and wars and the Peruvian yield spread. The data

show that the only two conflicts that are associated with any increase in the spread are

precisely the ones that involved the occupation of the guano islands: the rebellion against

the Vivanco-Pareja treaty and Vivanco’s rebellion of 1856, which affected the shipment

of guano. In Vivanco’s 1856 rebellion, the rise in the spread was still of a small enough

magnitude as to make the Peruvian bond look like that of Chile. Except for these two

episodes other conflicts were either insignificant or associated with a reduction in the

spread of the two bonds. Perhaps the best way to illustrate the irrelevance of political

instability is to cite a letter from a British bondholder to The Times: “With respect to the

[disturbed] internal state of Peru…It is not of the slightest importance to the English

bondholders. Did their security rest upon no other foundation than the internal

resources of Peru and the honesty of her government I do not believe there is a single

holder of the stock who would value it at 10 per cent (…) but the security of the guano is

66 The Economist, 24 April 1875, pp. 483-484.

32

Guano, Credible Commitments and State Finances

unquestionable, and from its local situation is beyond the reach of any Government in

Peru to control.”67

Cumulative Abnormal Returns

Although a preliminary evaluation of the evolution of bond prices and yields strongly

suggests that the factors associated with the adequacy of guano revenues drove much of

the evolution in bond prices (as opposed to those factors that did not transmit information

about the adequacy of the guano deposits like internal rebellions and wars), I further

examine the data through an econometric analysis. The objective of this section is to

establish with greater precision whether political and economic events coincide with

anomalous returns on Peruvian bonds. Following the work of Mitchener and

Weidenmier, I develop a market model in which the return on Peruvian bonds is

regressed against the returns of an indicator of the sovereign debt market.68 The model

can be stated as follows:

Rt = ao + βXt + εt (1)

where Rt is the return on Peruvian bonds, ao is a constant, β is the beta coefficient, Xt is

the market return at time period t, and εt is an error term. The beta coefficient measures

the correlation of the returns on Peruvian bonds with an index of the market return.

I estimate two versions of the equation, one employing the return on the British

consol as the market indicator and another with the average return on Brazilian and

Chilean debt.69 The errors resulting from these estimations are interpreted as the

67 The Times, 23 April 1857. 68 Mitchener and Weidenmier, “Empire,” pp. 671-672. 69 Note that the equation I estimate is not technically a market model, in which the return on Peruvian bonds is compared to the return on a market portfolio. Instead, the model is a single-factor model in which either the return on the British consol or on the Chilean/Brazilian bonds is used to provide a base for comparison with the return on Peruvian debt. Returns in period t are computed by taking the natural logarithm of the bond price at time t divided by the bond price at time t-1. The data employed are monthly.

33

Guano, Credible Commitments and State Finances

abnormal returns on Peruvian bonds. Examining the path of cumulative abnormal returns

(CARs) permits one to identify periods of time during which Peruvian bonds consistently

over-performed or under-performed relative to the market indicator.70 Figure 4 shows the

CARs for Peruvian bonds from 1830 to 1875. The figure confirms the basic patterns

observable in the graphs of bond prices and yields. First, the onset of the guano-debt

contracts coincides with a period of large positive abnormal returns for Peruvian bonds

with respect to both the British consol and the Latin index. Second, there are substantial

negative abnormal returns both during the financial scandals of 1853-54 and during the

conflict with Spain in 1864-66. Finally, the last years before default are ones in which

Peruvian securities under-performed relative to the consol and the Chilean and Brazilian

bonds. Besides those episodes, the most striking feature of the graph is the remarkable

stability of returns over much of the guano period.

The evidence from financial markets strongly supports the hypothesis that Peru’s

contractual commitment to repay debt from guano revenues was credible. The analysis

of market reactions to major political and financial events suggests that through much of

the guano period, investors cared much about Peru’s ability to pay – control of guano

deposits and debt burdens were important. But they were indifferent to much of the

internal instability that historians argue held back Peru’s broader development.

Conclusions

Peru’s 19th century guano boom signified the country’s emergence from the bankrupt

and relatively stagnant state of affairs that had existed in the twenty years following

For a discussion of the market model see Sharpe, Alexander and Bailey, “Investments,” pp. 258-260. I apply the Newey-West methodology to correct for autocorrelation. 70 CARs are calculated by taking the partial sum of the residuals in equation 1.

34

Guano, Credible Commitments and State Finances

independence. The country possessed a natural resource that had the potential to

revolutionize Peruvian government finances. But arranging for the export of the

commodity and the return to international capital markets was not a foregone conclusion.

Both were accomplished through the linkage of guano export consignee contracts to the

financial agency role of debt service. These measures were effective in convincing

investors that Peru was creditworthy because they understood Peru’s extreme dependence

on the guano trade made them highly unlikely to risk losing it. The Peruvian

government’s experience with guano-based borrowing provides support for the view that

even in the context of highly unstable polities a sufficiently large penalty for default can

support an equilibrium with positive lending.

The guano windfall ushered in an era of relative prosperity for many in Peru,

particularly those among the elite. It also created a flow of capital that facilitated the

creation of Peru’s first banks, and of investment in cotton, nitrates and sugar. The guano

boom did not markedly improve Peru’s political institutions, however. There continued to

be a struggle between liberals and conservatives that more often than not took place

outside the realm of the law, which explains the largely unproductive use of the guano

resources. Much of the guano income that entered the state’s coffers (approximately 90

million pounds by Hunt’s calculations) was directed to military and bureaucratic expenses.

The guano boom finally came to an end in the early 1870s. The dramatic decrease

in guano income due to the exhaustion of the best guano deposits and the competition of

new fertilizers, led Peru into a period of abysmal public finance and default, and the

weakened state fell easy prey to Chilean territorial ambitions in the disastrous War of the

Pacific.

35

Guano, Credible Commitments and State Finances

References

Contemporary Sources and Official Documents Collections:

Course of Exchange. London. Dancuart, P. Emilio, comp. Anales de la Hacienda Pública del Perú: historia y legislación fiscal de la República, 24 vols. Lima: Imprenta Gil, 1902-26. Fenn, Charles. Fenn’s Compendium of the English and Foreign Funds. London: Effingham Wilson. Varios Issues. The Economist. London. The Times. London. Secondary Sources: Aljovín de Losada, Cristóbal. Caudillos y constituciones: Perú 1821-1845. Lima: Fondo de Cultura Económica, Instituto Riva Agüero, 2000. _______________. and Eduardo Araya L. “Prácticas políticas y formación ciudadana,” in Perú-Chile/Chile-Perú 1820-1920. Desarrollos políticos, económicos y sociales, edited by Eduardo Cavieres and Cristóbal Aljovín de Losada. Lima: Fondo Editorial de la Universidad Nacional Mayor de San Marcos, 2006. Amador, Manuel. “A Political Economy Model of Sovereign Debt Repayment,” Unpublished Manuscript. September 2003. Basadre, Jorge. Historia de la República del Perú. Rev. 7th ed. 11 vols. Lima: Editorial Universitaria, 1983. Bond, Philip and Arvind Krishnamurthy. “Regulating Exclusion from financial Markets,” Review of Economic Studies, vol 71, no. 4 (2004), pp.681-707. Borchard, Edwin. State Insolvency and Foreign Bondholders. General Principles. Vol 1. New Haven: Yale University, 1951. Bortz, Jeffrey and Stephen Haber. The Mexican Economy, 1870-1930. Essays on the Economic History of Institutions, Revolution, and Growth. Stanford: Stanford University Press, 2002.

36

Guano, Credible Commitments and State Finances

Bulmer-Thomas, Victor. The Economic History of Latin America since Independence. Cambridge: Cambridge University Press, 1994. Bulow, Jeremy and Kenneth Rogoff. “Sovereign Debt: Is to Forgive to Forget?” American Economic Review vol. 79, no.1 (1989), pp. 43-50. Cavieres, Eduardo F. and Cristóbal Aljovín de Losada, eds. Perú-Chile/Chile-Perú 1820-1920. Desarrollos políticos, económicos y sociales. Lima: Fondo Editorial de la Universidad Nacional Mayor de San Marcos, 2006. Clarke, Hyde. “On the Debts of Sovereign and Quasi-Sovereign States, Owing by Foreign Countries.” Journal of the Statistical Society of London, vol. 41, no. 2 (1878), pp. 299-347. Cole, Harold, James Dow and William English. “Default, Settlement, and Signalling: Lending Resumption in a Reputational Model of Sovereign Debt.” International Economic Review, vol. 36, no.2 (1995), pp. 365-385. Conklin, James. “The Theory of Sovereign Debt and Spain ander Phillip II,” Journal of Political Economy, vol. 106, no.3 (1998), pp. 483-513. Contreras, Carlos. “La economía peruana en su primera centuria: mercado interno e inserción internacional,” in Perú-Chile/Chile-Perú 1820-1920. Desarrollos políticos, económicos y sociales, edited by Eduardo Cavieres and Cristóbal Aljovín de Losada. Lima: Fondo Editorial de la Universidad Nacional Mayor de San Marcos, 2006. Eaton, Jonathan and Mark Gersovitz. “Debt with Potential Repudiation: Theoretical and Empirical Analysis.” Review of Economic Studies, vol.48 (1981), pp. 289-309. Finnemore, Martha. The Purpose of Intervention: Changing Beliefs about the Use of Force. Ithaca: Cornell University Press, 2003. Gootenberg, Paul. Between Silver and Guano. Commercial Policy and the State in Postindependence Peru. Princeton: Princeton University Press, 1989.