gst a broad overview

TRANSCRIPT

Page 1 of 8

Good Morning, Respected chairman, ICAI members & my dear

friends. Today I, Mukesh kumar sah is here to present my paper

on the topic “GST-a broad overview” i.e. Goods & Service Tax in

India.

India is a diverse country in terms of religion, caste, color, biodiversity, then how can

taxes be an exception. That’s why have sales tax, excise duty, customs laws, service tax

and many more. To avoid various taxes levied on goods & service, we thought of

introducing GST in India.

Page 2 of 8

We have been talking about GST since 2004 when Dr. Vijay Kelkar mooted the idea of

national GST. During 2006-07, the then Finance Minister Mr. P. Chidambaram set 1st

April,2010 as the date for introducing GST and asked the Empowered Committee of

state Finance Ministers to prepare a road map and work with central Government for

this purpose and in March 2011, Finance Minister Mr. P. Chidambaram had introduced

in Parliament 115th Constitutional Amendment Bill i.e. GST Bill. But, on account of lack

of adequate preparedness the implementation of GST further postponed and finally, In

May 2014 due to change of Government at center 115th Constitutional Amendment Bill

was lapsed.

But, after changing of Government at center, the new Finance Minister Mr. Arun Jetley

has introduced 122nd Constitutional Amendment Bill in Dec-2014 and finally, in May

2015 122nd Constitutional Amendment Bill was passed in Lok Sabha and proposes to

introduced on 1st April,2016 but pending in Rajya Sabha.

Today, even an Astrologer can’t answer the question on date of introduction of GST.

Having said the above, following important steps show government is actively working

on GST.

122nd Constitutional Amendment Bill for GST is already passed by Lok Sabha

and pending in Rajya Sabha.

Contract to manage IT infrastructure already awarded to Infosys

GST law is already drafted and available in public domain.

Our Prime Minister Shri Narendra Modi and Finance Minister Mr. Arun Jetley have

repeatedly assured that the new proposed date i.e. 1st april 2016 will be followed.

Page 3 of 8

What is GST? GST i.e. Goods & Service Tax is a comprehensive tax levy on manufacture, sale and consumption of goods and service at a National level. Under GST, the taxation burden will be divided equitably between manufacturing and services, through a lower tax rate by increasing the tax base and minimizing exemptions. It is expected to help build a transparent and corruption free tax administration. GST

will be levied only at the destination point and not various points.

Taxes that will be subsumed in GST GST would be levied on all the transactions of goods and service made for a consideration. This new levy would replace almost all of the indirect taxes. In particulars, it would replace the following indirect taxes :-

Central Taxes to Subsumed

Central Excise duty (CENVAT)

Additional duties of excise

Excise duty levied under Medicinal

& Toiletries Preparation Act

Additional duties of customs (CVD &

SAD)

Service Tax

Surcharges & Cess

State Taxes to subsumed

State VAT / Sales Tax Central Sales Tax

Purchase Tax

Entertainment Tax (not levied by the

local bodies)

Luxury Tax

Entry Tax ( All forms)

Taxes on lottery, betting & gambling Surcharges & Cess

However, certain items/Sectors would be outside the GST regime. Products such as

alcohol, petroleum products would remain outside the GST regime. Further, land &

Properties may remain outside since they are neither goods nor services.

GST in India India is proposing to implement “Dual GST”. In dual GST regime, all the transactions of Goods and Service made for a consideration would attract two levies i.e Central GST (CGST) and State GST (SGST).

Introduction

Page 4 of 8

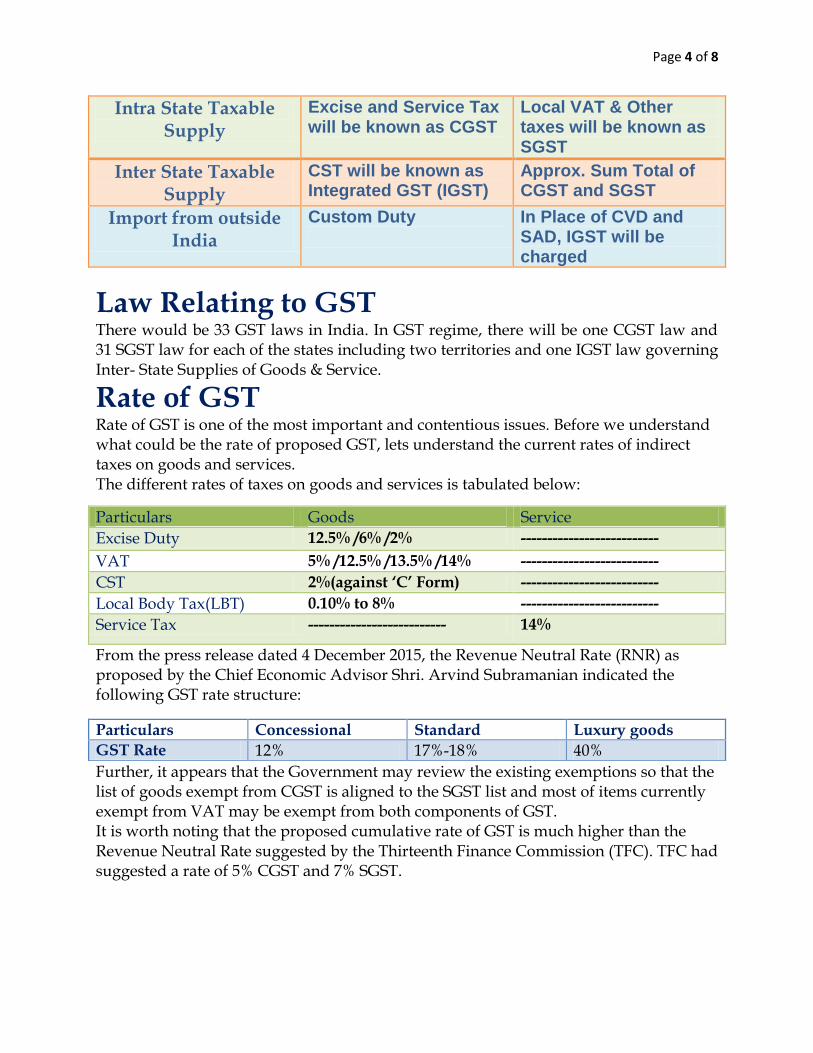

Intra State Taxable Supply

Excise and Service Tax will be known as CGST

Local VAT & Other taxes will be known as SGST

Inter State Taxable Supply

CST will be known as Integrated GST (IGST)

Approx. Sum Total of CGST and SGST

Import from outside India

Custom Duty

In Place of CVD and SAD, IGST will be charged

Law Relating to GST There would be 33 GST laws in India. In GST regime, there will be one CGST law and 31 SGST law for each of the states including two territories and one IGST law governing Inter- State Supplies of Goods & Service.

Rate of GST Rate of GST is one of the most important and contentious issues. Before we understand what could be the rate of proposed GST, lets understand the current rates of indirect taxes on goods and services. The different rates of taxes on goods and services is tabulated below:

From the press release dated 4 December 2015, the Revenue Neutral Rate (RNR) as proposed by the Chief Economic Advisor Shri. Arvind Subramanian indicated the following GST rate structure:

Further, it appears that the Government may review the existing exemptions so that the list of goods exempt from CGST is aligned to the SGST list and most of items currently exempt from VAT may be exempt from both components of GST. It is worth noting that the proposed cumulative rate of GST is much higher than the Revenue Neutral Rate suggested by the Thirteenth Finance Commission (TFC). TFC had suggested a rate of 5% CGST and 7% SGST.

Particulars Goods Service

Excise Duty 12.5% /6% /2% --------------------------

VAT 5% /12.5% /13.5% /14% --------------------------

CST 2%(against „C‟ Form) --------------------------

Local Body Tax(LBT) 0.10% to 8% --------------------------

Service Tax -------------------------- 14%

Particulars Concessional Standard Luxury goods

GST Rate 12% 17%-18% 40%

Page 5 of 8

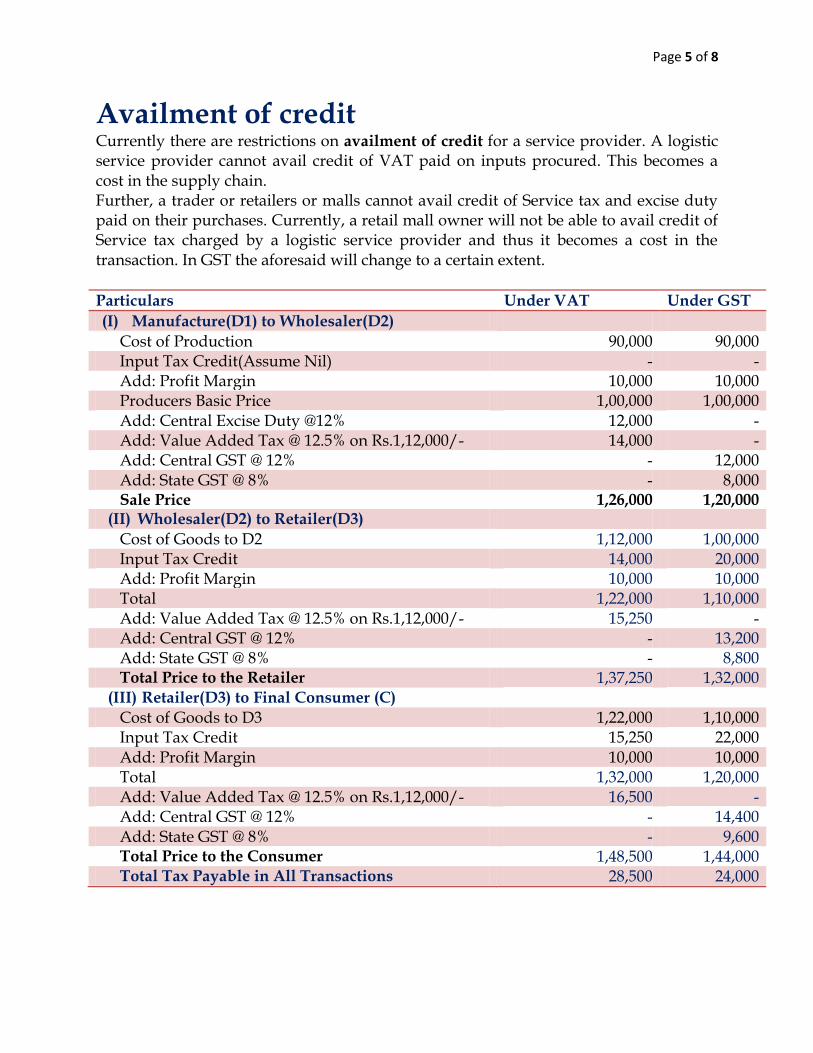

Availment of credit Currently there are restrictions on availment of credit for a service provider. A logistic service provider cannot avail credit of VAT paid on inputs procured. This becomes a cost in the supply chain. Further, a trader or retailers or malls cannot avail credit of Service tax and excise duty paid on their purchases. Currently, a retail mall owner will not be able to avail credit of Service tax charged by a logistic service provider and thus it becomes a cost in the transaction. In GST the aforesaid will change to a certain extent.

Particulars Under VAT Under GST

(I) Manufacture(D1) to Wholesaler(D2) Cost of Production 90,000 90,000 Input Tax Credit(Assume Nil) - - Add: Profit Margin 10,000 10,000 Producers Basic Price 1,00,000 1,00,000 Add: Central Excise Duty @12% 12,000 - Add: Value Added Tax @ 12.5% on Rs.1,12,000/- 14,000 - Add: Central GST @ 12% - 12,000 Add: State GST @ 8% - 8,000 Sale Price 1,26,000 1,20,000

(II) Wholesaler(D2) to Retailer(D3) Cost of Goods to D2 1,12,000 1,00,000 Input Tax Credit 14,000 20,000 Add: Profit Margin 10,000 10,000 Total 1,22,000 1,10,000 Add: Value Added Tax @ 12.5% on Rs.1,12,000/- 15,250 - Add: Central GST @ 12% - 13,200 Add: State GST @ 8% - 8,800 Total Price to the Retailer 1,37,250 1,32,000

(III) Retailer(D3) to Final Consumer (C) Cost of Goods to D3 1,22,000 1,10,000 Input Tax Credit 15,250 22,000 Add: Profit Margin 10,000 10,000 Total 1,32,000 1,20,000 Add: Value Added Tax @ 12.5% on Rs.1,12,000/- 16,500 - Add: Central GST @ 12% - 14,400 Add: State GST @ 8% - 9,600 Total Price to the Consumer 1,48,500 1,44,000 Total Tax Payable in All Transactions 28,500 24,000

Page 6 of 8

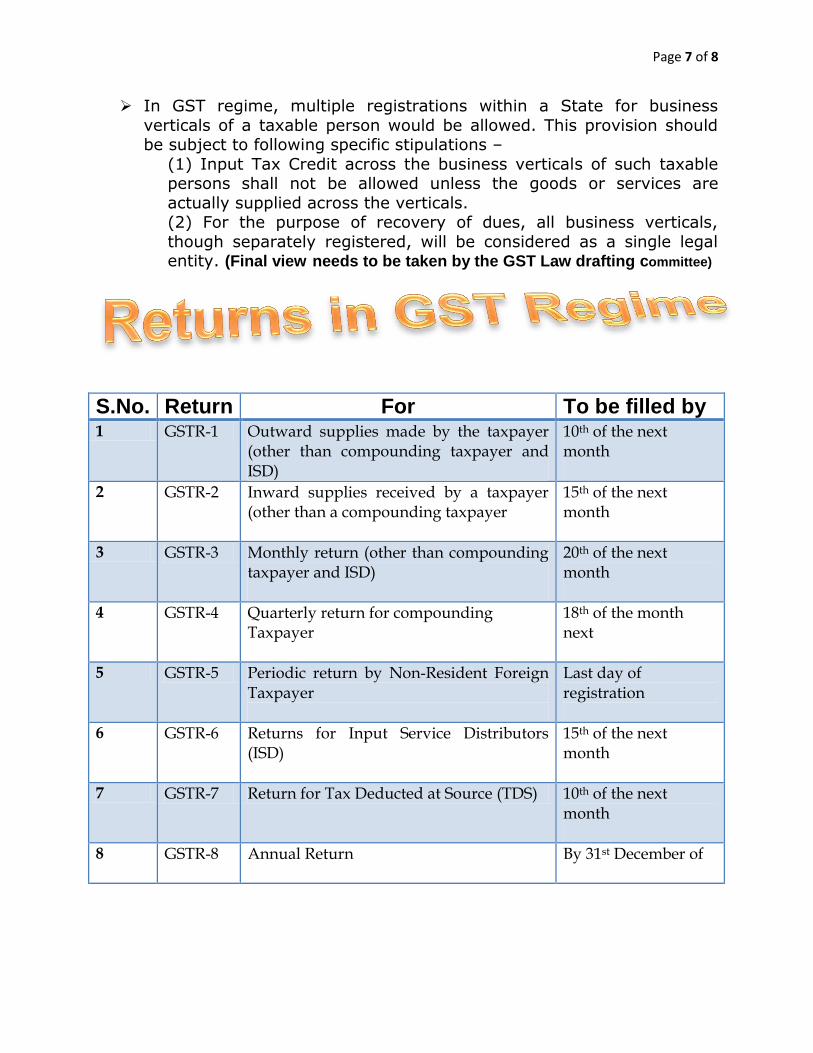

Mechanism of input tax credit in GST Input tax credit of CGST would be available for payment of CGST and input tax credit of SGST would be available for payment of SGST. However, cross utilization of tax credit between the Central GST and the State GST would be allowed in the case of inter-State supply of goods and services under the IGST model. Structure of registration number

State Code

PAN

Entity Code

BLANK

Check Digit

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Each taxpayer will be allotted a State wise PAN-based 15-digit Goods and Services Taxpayer Identification Number (GSTIN).

In the GSTIN, the State Code as defined under the Indian Census 2011

would be adopted. In terms of the Indian Census 2011, each State has been allotted a unique two digit code e.g. „09‟ for the State of Uttar

Pradesh and „27‟ for the State of Maharashtra.

13th digit would be alpha-numeric (1-9 and then A-Z) and would be assigned depending on the number of registrations a legal entity

(having the same PAN) has within one State. For example, a legal entity with single registration within a State would have „1‟ as 13th

digit of the GSTIN. If the same legal entity goes for a second

registration for a second business vertical in the same State, the13th digit of GSTIN assigned to this second entity would be „2‟.This way 35

business verticals of the same legal entity can be registered within a State.

14th digit of GSTIN would be kept BLANK for future use.

Page 7 of 8

In GST regime, multiple registrations within a State for business

verticals of a taxable person would be allowed. This provision should be subject to following specific stipulations –

(1) Input Tax Credit across the business verticals of such taxable persons shall not be allowed unless the goods or services are

actually supplied across the verticals. (2) For the purpose of recovery of dues, all business verticals,

though separately registered, will be considered as a single legal entity. (Final view needs to be taken by the GST Law drafting committee)

S.No. Return For To be filled by 1 GSTR-1 Outward supplies made by the taxpayer

(other than compounding taxpayer and ISD)

10th of the next month

2 GSTR-2 Inward supplies received by a taxpayer (other than a compounding taxpayer

15th of the next month

3 GSTR-3 Monthly return (other than compounding taxpayer and ISD)

20th of the next month

4 GSTR-4 Quarterly return for compounding Taxpayer

18th of the month next

5 GSTR-5 Periodic return by Non-Resident Foreign Taxpayer

Last day of registration

6 GSTR-6 Returns for Input Service Distributors (ISD)

15th of the next month

7 GSTR-7 Return for Tax Deducted at Source (TDS) 10th of the next month

8 GSTR-8 Annual Return By 31st December of

Page 8 of 8

Every registered assessee will be required to file returns (including NIL returns). However, persons exclusively dealing in exempted / Nin-rated or non-GST goods or services would neither obtain registration nor file returns. It is pertinent to note that there could be 8 GST returns as under: - 3 returns - Outward supplies (GSTR 1), Inward supplies (GSTR 2) and Monthly return (GSTR 3) - Return for compounding dealers (GSTR 4) - Return by non-resident tax payer (GSTR 5) - Input Service Distributor (ISD) return (GSTR 6) - Tax deducted at Source (GSTR 7) - Annual return (GSTR 8) It is pertinent to note that GSTR-3 would be entirely auto-populated through GSTR-1 (of counterparty suppliers), own GSTR-2, ISD return (GSTR-6) (of Input Service Distributor), TDS return (GSTR-7) (of counterparty deductor), own ITC Ledger, own cash ledger, own Tax Liability ledger. However, the taxpayer may fill the missing details to begin with. As there are multiple returns, for most of the organisations, in GST regime, compliances are expected to increase dramatically. Take example of a service tax assessee, who currently files 2 returns on an annual basis. Now, in GST regime, Service tax assessee could be required to file as many as 61 returns (5 returns per month plus 1 annual return)!!! Thus, in Human Resource(HR) department and Chartered Accountants will have to anticipate the increase (and decrease in certain cases) in the manpower and plan accordingly. A legal thanks to one and all….!!