globalserve moscow seminar september 2013 by phani schiza antoniou the netherlands and luxembourg:...

TRANSCRIPT

Globalserve Moscow SeminarSeptember 2013

By Phani Schiza Antoniou

The Netherlands and Luxembourg:

The high profile players in the Russian market

Netherlands, the country

EU memberHighly strategic commercial location that makes

it the “Gateway to Europe”Natural hub for logistics and headquarter

functions High educated, multi cultural and multi-lingual

workforceHigh level of infrastructureGood economic and financial climate

Netherlands, the country

One of the major and reputable international Business centers

Extensive Network of double Tax Treaties; 90!!Good Banking systemTax Rulings possible

Question

The Netherlands is the X largest investor in Russia

50th?17th?

2nd?

The Netherlands is the X largest investor in Russia

2nd

The Netherlands is the second largest foreign investor in Russia

Question

A Dutch B.V

BV=Private company with limited liability Set up by a notary (make up of their articles) Official Permission of Minister of Justice Minimum share capital is €1 Registered in the Chamber of Commerce Director can be also legal entity Min director/ shareholder 1 Director can be non Dutch resident but for management

and control purposes Dutch director is advisable

Summary of Dutch Tax RatesCorporate Income Tax upto € 200000 Corporate Income T above € 200000

20%25%

Tax on Dividends received 0% if participation exemption applies i.e 5% minimum shareholding in the subsidiary held as participation not as an investment

Royalty income 5 %

Capital gains tax in the case of disposal of participation

0% if participation exemption applies i.e 5% minimum shareholding in the subsidiary, held as participation not as investment

Profit from the trading in securities 20-25%

Withholding tax on dividends other than EU or Treaty countries

15%

Withholding taxes on interest, royalties 0%

Summary of the Dutch tax system

GENERALCorporate Income Tax rate=25%Taxable income EUR 200,000=20%≦Innovation box income taxed at 5%

Average ETR of Dutch multinational: Between 8% and 20%

Summary of the Dutch tax system

No withholding tax on interest and royalty payments

Dividend withholding tax =maximum 15%Qualifying dividends to EU or 0% treaty

country=0%No capital taxes

Summary of the Dutch tax system

CORPORATE INCOME TAX SPECIFICSTax loss carry forward: 9 yearsTax loss carry back:1 Thin cap: 3 to 1 or the group’s debt-to-equity

ratioInterest deduction limitations when eroding the

Dutch taxable basis of operating subsidiariesThese rules do not affect international

structuring

Summary of the Dutch tax system

INNOVATION BOX Offers attractive opportunities to lower the ETR for income

allocable to intangible assets to 5% if: The intangible assets are self developed, which includes contract

research for the risk and benefit of the tax payer and participation in R&D activities by means of cost-contribution arrangements (but excludes marketing intangibles created by the tax payer, such as brand names, logos and assets alike)

The intangible assets are purchased, provided the purchased intangible asset loses its independence and is merged into a new self developed intangible asset.

At least 30% of expected income can be attribute to patents/registrations obtained for the intangible asset

Summary of the Dutch tax system

Test per intangible asset, to be met at the end of the first year of applying for the Innovation Box for an intangible asset

No upfront approval of Dutch tax authorities is required, so Innovation Box can be applied for by ticking a box in the Dutch corporate Income tax return. However, in order to determine income to be allocated to Innovation Box, consultation with Dutch tax authorities upfront is highly recommended.

Summary of the Dutch tax system

PARTICIPATION EXEMPTION

100% income (dividend income and capital gains)exempt from Dutch corporate income tax if it concerns an investment in shares of at least 5% of the nominal paid-in capital, unless it concerns a portfolio investment company(no minimum holding period)

Summary of the Dutch tax system SUBSTANCE REQUIREMENTSFocus should be on substance requirements set by the jurisdiction that pays to a Dutch holding company;

Presence of local operations Key executives 'agenda for travel to the holding company jurisdiction

The Dutch tax authorities published the following list with minimum substance requirements that should be met by so-called financing flow-through ruling companies:

At least 50% of the Board of Directors(BOD) MEMEBRS SHOULD BE Dutch residents(live and work there)and of a certain professional level and the company has adequate staff (itself or from 3rd parties)for performing the functions

All key strategic/material decisions of the BOD should be taken in the Netherlands, such as the entering into contracts and signing of documents

The main bank account should be held in the Netherlands The bookkeeping is maintained in the Netherlands The address of the company should be in the Netherlands and the company is not

considered a resident in another state on the basis of a tax treaty The company has sufficient equity considering its activities and the risks to be

absorbed by the company.

DOUBLE TAX TREATY WITH RUSSIA

DIVIDEND

•If 25% ownership in the subsidiary Russian company and minimum investment of •€ 75000

5*%/15%

INTEREST 0%

ROYALTIES 0%

Why Luxembourg?

• Providing a platform to the EU: a founding member of the EU with many EU institutions located on is land

• Population & Workforce: Multicultural and multilingual population becoming the source of highly trained working force

• High standards of living and safety • Business friendly tax framework (large number of double tax

treaties (64), the lowest VAT in Europe etc.)• Enable flexibility and transparency in doing business• Solid legal and regulatory framework• Internationally established financial and investment fund centre:

with more than USD 2.5 trillion in assets (2nd as an investment fund centre in the world and 1st in Europe)

Why Luxembourg? •Politically and socially stable•Established in the fund management market: Easy access to fund management groups and decision makers with long-standing experience in attracting international companies; USD 300 billion assets under management; A market leader in product innovation for UCIT and non-UCIT funds•Outstandingly developed banking system:•Strategic location in Europe•Transport: Highly efficient infrastructure and logistical network (e.g. airport, railway); •Known for pro-business legislation and administration with government encouraging business•Sound macroeconomic fundamentals. It is the richest country in Europe and second richest in the world as per per capita income, one of the 11 AAA rated countries•The international market in a single place: access to a market of over 100 million consumers within a 250 km radius•A base for Islamic products•Wide range of double tax treaties 64!

Types of Luxembourgish vehicles

Regulated by CSSF (Commission de Surveillance du Secteur Financier) vehicles:

SIF (Specialised Investment Fund)SICAR (Risk Capital Investment Company)

Unregulated by CSSF vehicles:SOPARFI (Société de Participation Financière)SPF (Private Wealth Management Company)SPV (Securitisation Vehicle)

Types of legal forms of investment vehicles

Public Limited Liability Company- (S.A)Private Limited Liability Company- (SARL)Partnerships-(S.N.C.)Limited partnerships- (S.C.S.)Partnerships Limited by Shares or Cooperative companies- (S.C.A.)Cooperative Company Organised as a public Limited - (COOPSA) European Company (SE)

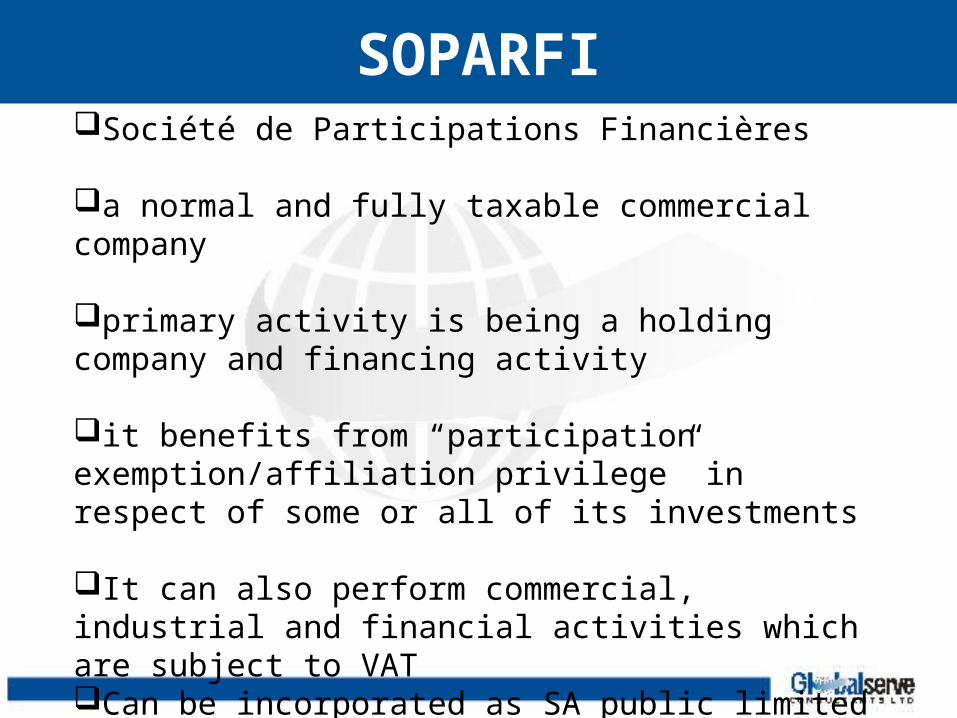

SOPARFI

Société de Participations Financières

a normal and fully taxable commercial company

primary activity is being a holding company and financing activity it benefits from “participation exemption/affiliation privilege” in respect of some or all of its investments

It can also perform commercial, industrial and financial activities which are subject to VATCan be incorporated as SA public limited co or as SARL the limited liability company or as limited partnership by shares SCA

Characteristics of SOPARFI

Registered office or central administration in Luxembourg Registered and bearer shares of various classesMinimum Share Capital (in any currrency): depends on the form of the business (S.A./S.C.A. vs S.à R.L)Directors: minimum of 1 for SARL; a minimum of 1 for SA but only if the shreholder is also 1, otherwise 3 directors are needed; they an be natural persons or corporate bodies; of any nationality

BUT even if they do not have to be residents of Luxembourg the majority is recommended to be so in order to comply with the rules of “permanent establishment”

No need of a company secretaryShareholders minimum of 1 Reporting: Annual audit is compulsory and the abbreviated accounts are filed and accessible to he general public

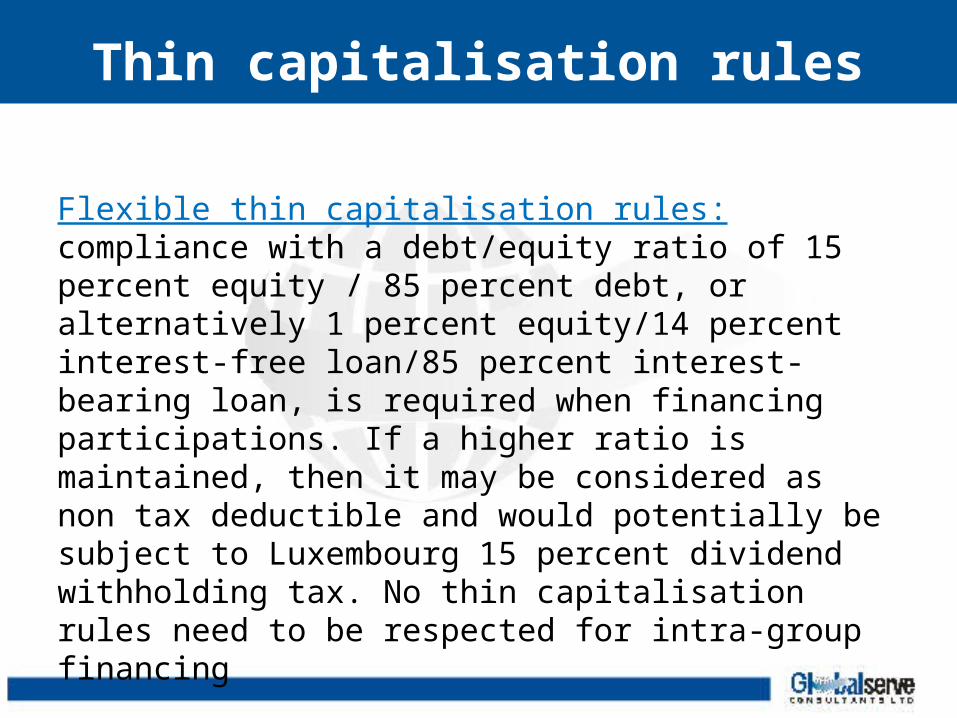

Thin capitalisation rules

Flexible thin capitalisation rules: compliance with a debt/equity ratio of 15 percent equity / 85 percent debt, or alternatively 1 percent equity/14 percent interest-free loan/85 percent interest-bearing loan, is required when financing participations. If a higher ratio is maintained, then it may be considered as non tax deductible and would potentially be subject to Luxembourg 15 percent dividend withholding tax. No thin capitalisation rules need to be respected for intra-group financing

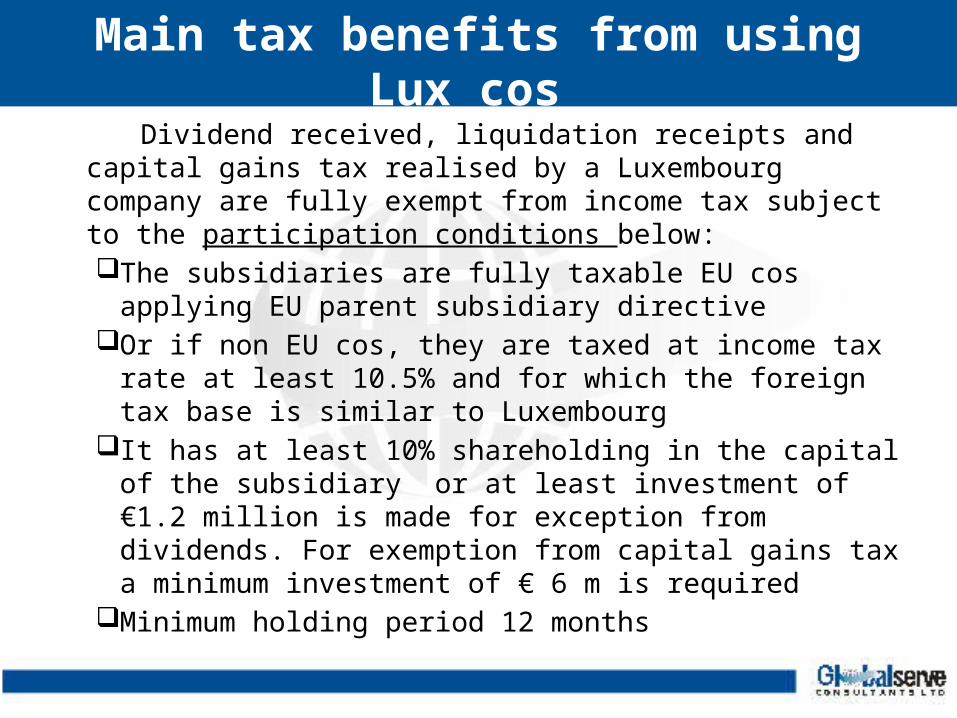

Main tax benefits from using Lux cos

Dividend received, liquidation receipts and capital gains tax realised by a Luxembourg company are fully exempt from income tax subject to the participation conditions below:The subsidiaries are fully taxable EU cos applying EU

parent subsidiary directiveOr if non EU cos, they are taxed at income tax rate at least

10.5% and for which the foreign tax base is similar to Luxembourg

It has at least 10% shareholding in the capital of the subsidiary or at least investment of €1.2 million is made for exception from dividends. For exemption from capital gains tax a minimum investment of € 6 m is required

Minimum holding period 12 months

New Double Tax Treaty between Luxembourg and Russia in effect as from 2014

DIVIDEND

•If 10% ownership in the subsidiary Russian company and minimum investment of •€ 80.000

5*%/15%The new treaty which is to be put in effect as from 2014 has reduced the WHT on dividend from 10% to 5% under conditions like Cyprus and Nertherlands

INTEREST 0%

ROYALTIES 0%

Main tax benefits from using Lux cos

No withholding tax on interest payments Benefit from EU interest, royalty and dividend DirectiveWithholding tax of 15% for dividend paid to non EU cos and non

Treaty cos which do not meet the participation exemption criteria Favourable IP regime for royalties at the effective tax rate of

5.85% through 80% income exception from tax arising either from royalty income or capital gains from the sale of Intellectual property rights, copyrights patents

Flexible thin capitalisation rules #Corporate tax rate at 28.8% consisting of 20 % or 21% corporate

tax if above € 15000 net profit plus surcharge to the employment fund plus municipal tax . Minimum flat tax € 3210

Net wealth tax 0.5%on worldwide net assets but there are exemptions

Losses are carried forward indefinitely

Comparison of Luxembourg and Dutch Tax Rates

Luxembourg company Dutch company Capital It has minimum amount and has to

be paid in advance according to the type of company

No minimum

Corporate tax 28.8% 20 % upto € 20000025% above € 200000

Tax on Dividends received O% if participation exemption applies i.e •10% minimum shareholding or a minimum of € 1.2 m investment•For at least 12 months•EU co or if non EU to be taxed at tax rate at least equal to 10.5%

0% if participation exemption applies i.e •5% minimum shareholding in the subsidiary •held as participation not as an investment

Royalty income 5.85% 5 %

Comparison of Luxembourg and Dutch Tax Rates

Luxembourg company Dutch company

Capital gains tax in the case of disposal of participation

O% if participation exemption applies i.e •10% minimum shareholding or a minimum of € 6 m investment•For at least 12 months•EU co or if non EU to be taxed at tax rate at least equal to 10.5%

0% if participation exemption applies i.e •5% minimum shareholding in the subsidiary,• held as participation not as an investment

Profit from the trading in securities

28.8% 20-25%

Thin capitalisation rules 15:85 equity /debt 1:3 equity /debt

Withholding tax on dividends other than EU or Treaty countries

15% 15%

Comparison of Luxembourg and Dutch Tax RatesLuxembourg company Dutch company

Tax loss carried forward indefinite 9 years

EU dividend , interest and royalty directives

Yes Yes

Extensive network of DTT 64 90

DTT with Russia :WHT on dividend

5%*/15% *10% participation And € 80000 investment

5%*/15%*25% participationAnd € 75000 investment

WHT on royalty and interest 0% 0%

Exchange of information Yes Yes

Limitation of treaty benefits Will not apply provided substansive business in one of the states

Will not apply provided substansive business in one of the states

Who is going to be the winner in the race for the Russian market???

Are Cyprus and Netherlands going to maintain their positions as 1st and 2nd investor in Russia

or is Malta and Luxembourg equipped with the new DTTs going to successfully compete

and overcome them

???????Time will show but.........

Who is going to be the winner in the race for the Russian market???

Cyprus , Malta, Netherlands or Luxembourg ??

However Malta ‘s DTT with the 5% withholding tax on interest and royalties as against the 0% WHT of Netherlands, Cyprus and Luxembourg put her in a disadvantageous position in this race.

The inexperience of the maltese banks in international transactions and slowness / ineffectiveness as well as their unwillingness to expand banking among the Russians puts Malta in a less advantageous position as against Cyprus.

Of course the new DTT in combination with the special regimes that it already has with respect to gaming, yachting , shipping and aviation will assist it in increasing its share in the Russian market, although not considerably

Who is going to be the winner in the race for the Russian market???

Cyprus, Malta,Netherlands or Luxembourg ? With respect to Cyprus, the banking crisis has shattered the

Russian confidence since a lot of Russian deposits were lost

But despite the crisis which has tested the stability of the tax regime, the favourable tax system has remained unchanged with respect to the international business companies with the blessings of the Europeans

After the first shock, the demand for the Cyprus companies is picking up recognising the advantages of the island, not found in the competitive jurisdictions :

Who is going to be the winner in the race for the Russian market???

Cyprus, Malta, Netherlands, Luxembourg ?? Reasonable costs combined with high value of services Experienced with positive attitude in commercial banking Simple, uncomplicated system without conditions for the participation exemption

for dividends received and capital gains from the sale of securities Trading in securities is tax exempt which cannot be found in any other jurisdiction No withholding tax on dividends if paid to non residents even if they are offshore

companies, unlike all the other competitive jurisdictions with DTT with 5% withholding tax on dividends

And perhaps the biggest advantage of the Cyprus treaty is that the limitation of the treaty benefits is only in case it is not registered in Cyprus while with all the other treaties benefits may be limited if there is no substance

Who is going to be the winner in the race for the Russian market???

Cyprus, Malta, Netherlands, Luxembourg ?? Luxembourg has definitely a big advantage over the other competing

jurisdictions with respect to the sophisticated and complete legislation, its outstanding developed banking system its leading position in fund management industry But it is very expensive and has high income tax rate at 28.8% for financing

operations Tax exemption of capital gains from the sale of the shares has conditions which

are not easily met The banks are mainly private banks and cannot cater for the clients’ commercial

needs Applies withholding tax on dividend to non EU with low tax rates such as the

classical offshore. For this reason both the Luxembourg cos and the Dutch have to be combined with low cost EU companies which do not apply WHT like Cyprus

Who is going to be the winner in the race for the Russian market???

Cyprus, Malta, Netherlands, Luxembourg ??

With respect to Netherlands, it will have to compete with Luxembourg’s fund management and banking industry to attract the big Russian groups

Still its tax regime is more flexible and its participation conditions easily achievable

Its main defect the withholding tax on dividends to non EU and non Treaty companies which is overcome using a Cyprus/ Irish company to exit