globalised financial flows - university of nigeria

TRANSCRIPT

University of Nigeria Research Publications

Aut

hor

AGU, Reuben Amaechi PG/MSC/02/33751

Title

Globalised Financial Flows, Capital Market

Deepening, and Economic Growth: the Nigerian Experience

Facu

lty

Social Sciences

Dep

artm

ent

Economics

Dat

e

August, 2007

Sign

atur

e

TITLE PAGE

GLOBALSED FINANCIAL FLOWS, CAPITAL MARKET DEEPENING, AND

ECONOMIC GROWTH: THE NIGERIAN EXPERIENCE.

AGU, REUBEN AMAECHI

PGIM.ScIO213375 1

DEPARTMENT OF ECONOMICS

UNIVERSITY OF NIGERIA,

NSUKKA

AUGUST 2 0 0 7

I

This work has been read and approved for the award of M.Sc Degree in I

the Department of Economics, University of Nigeria Nsukka. I I -

~ e a d of Department

--.---.--------------------____________________________ Date

Dean, Faculty of Social Sciences

CERTIFICATION

AGU, REUBEN AMAECHI, a postgraduate student in the Department of Economics with Reg.

No. PG/M.Sc/02/33751 has satisfactorily completed the requirements for course and

research work for M.Sc Degree in Economics.

The work embodied in this dissertation i s original and has not been submitted in part or full

for any other diploma or degree of this or any other University.

AGU, RE EN AMAECHI I?

H? OF DEPARTMENT

P DEDICATION

This i s dedicated with warmth and love to my parents: Alexander Agu-Ugwu, my father;

and Victoria Morenike Agu-Ugwu, my late mother; for their love and foresight in laying

the basic foundation of this project many years ago - in my formative years.

And also to my loving and wonderful wife - Victoria, whose show of love, understanding

and care has been a source of inspiration. And mostly to God who i s the actual owner of

the knowledge and energy expended on this project.

ACKNOWLEDGEMENT

In the course of carrying out this study, I received helps, in one way or the other, from many

people. As such it would seem invidious of me to select just a few of them for mention here,

since mentioning al l of them would create a rather long l i s t . However, even at the risk of

appearing so (invidious) some individuals must necessarily be mentioned for the very special

helps they offered to me.

Firstly I wish to express my thanks to Moses Oduh (Chairman), who helped me with his data

bank and for his useful remarks and advice on the methodology used. I equally wish to

express my appreciation to my senior research friend, Dr. Patterson Ekeocha (Papa), for his

witty comments and advice on the empirical literature. I am also fu l l of appreciation for Dr.

F.I. Njoku, of Mathematics Department, for his useful suggestions regarding some of the

mathematical derivations used in this work. My thanks also go t o Rev. Fr. Dr. lchioku and Dr. '. Fonta for their useful advice during the period of this work. I equally received help and

encouragement from some of my classmates: Richard Ojike, Charles Manasseh, and Victor

Malolu, therefore my thanks also go to them.

I found the library of the Nigerian Stock Exchange (NSE) very useful, and their staffs were

really helpful; I am therefore immensely grateful to them.

I am highly appreciative of members of my family - my wife, Victoria; Ikechukwu;

Nwanneka; and my father, Elder Alexander Agu - Ugwu - for their encouragement and

prayers.

I owe the greatest debt of thanks to Prof. F.E. Onah, my project supervisor, who

incidentally i s instrumental to my developing interest i n International Economics, (and who 4

equally, i s the Head of Department of Economics) -for his fatherly disposition and patience

i n guiding me throughout the period of this work.

However, I remain solely responsible for the views and accuracy of information contained in

this work.

Agu, Reuben Amaechi

Postgraduate School of Economics

University of Nigeria, Nsukka

August, 2007

TABLE OF CONTENTS

Title Page

Approval Page

Certification

Dedication

Acknowledgement

Table of Contents

Abstract

List of Tables

List of Charts

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

1.2 Statement of the Problem

1.3 Objectives of the Study

1.4 Statement of Hypothesis

1.5 Importance of the Study

1.6 Scope and Limitations of the Study

CHAPTER TWO

LITERATURE REVIEW

2.1 Globalisation Finance and Economic Growth

2.2 Foreign Capital Flows to Nigeria: Nature, Trend and Impact

On the Capital Market

2.3 Determinants of Foreign Portfolio Investment (FPI) in Nigeria

2.4 The Nigerian Capital Market: Developments and Reforms

2.4.1 The Capital Market and i t s Institutions

7.4.7 D e v d o n r n ~ n t z and R ~ f o r r n z i n the N i w r i a n Canital Market

Page

i . . 11

iii

i v

v

vi

vii

i x

X

CHAPTER THREE RESEARCH METHODOLOGY

3.1 Theoretical Model Specification

3.2 Derivation of the Theoretical Model

3.3 Choice of Proxies for GFF and Financial Deepening of the

Capital Market 3.3.1 Other Proxies

3.3.2 Capital Market Deepening and Financial Deepening of The External Segment of the Nigerian Capital Market (IFD)

3.4 Functional Model Specifications

3.4.1 Modeling Impact of Globalization on FPI

. 3.4.2 Model 2: Modeling the financial Deepening of ESNCM (IFD)

3.4.3 Model 3: Modeling the Financial Deepening of the Nigeria Capital Market (NCM)

3.4.4 Model 4: Modeling the Impact of Globalized Financial flows (GFF) on the Growth rate

3.5 Justification of the Model

3.6 Data Required and sources1 software for Estimation

CHAPTER FOUR ANALYSIS AND ESTIMATION OF REUSULTS 4.1 Results of Econometric Tests 4.2 Interpretation of Results 4.3 Granger Causality Tests 4.4 Other Econometric Tests

CHAPTER FIVE SUMMARY, CONCLUSION AND RECOMMENDATION 5.1 iummary of Findings

5.2 Conclusion ' 5.3 Recommendations

REFERENCES

CHARTS

Econometric Result Print Out

Of the whole complexion of globalized financial flows (GFF), Foreign Portfolio lnvestment (FPI)

stands out uniquely on account of i t s dual characterization of being distinct and essential. It i s

distinct in the sense that it i s the only type of GFF that must necessarily util ize the framework of

capital markets t o transmit from one country to another. I t s essential feature derives from i t s

potential to excite economic growth positively. Literature shows that GFF, of the FPI type, can foster

financial development through capital market deepening, which then engenders economic growth.

Opposing views posit that GFF in the form of FPI i s of "foot loose" nature and thus can lead to crisis

and contagion and as such should not be relied on for purposes of strategizing for economic growth.

Since 1998, the rise i n the volume of FPI inflow has been so impressive that it can no longer be

ignored. In fact by 2005, the inflow of FPI has surpassed that of Foreign Direct lnvestment (FDI).

This study therefore sets out t o find whether GFF flow (of the FPI type) into Nigeria has improved

under the policy financial globalization and financial integration (financial openness). And also

confirm whether this policy has impacted positively on economic growth. The relevance of this study

derives from the fact that available studies on FPI inflow are just a handful and recent, and there is

no country specific study regarding the effect of foreign portfolio investment on financial sector

development and economic growth. This study hopes contribute t o the literature in this gray area

using Nigerian data.

The study applied the dynamic distr ibuted lag model, w i th error correction, on a set of relevant

t ime series data and finds that FPI inflow has improved under the policy of financial openness. It was

also confirmed that the policy of financial openness i s positively related to capital market deepening

and hence financial sector development. Finally, it was discovered that the inflow of FPI within the

policy context of financial openness i s positively related to economic growth via capital market

deepening. Granger causality tests reveal that: financial openness, and market size, does not

granger cause FPI inflow; real rate of return (RRR) of investments granger causes FPI inflow; while

market size granger causes capital market deepening. Finally the tests revealed that there i s a bi-

directional causality relationship between capital market deepening and economic growth.

It was therefore concluded that the lure for superior rate of return causes FPI inflow, while the

policy of financial openness facilitates it. Financial openness facilitated deepening of the capital

market which led to economic growth.

Based on the results, it is recommended that there i s need that the present reforms going on in the

capital market, and the financial sector in general, be sustained given the fact that the Nigerian

financial sector has a prominent role t o play in channeling resources for investment and productive

purposes. Again, government should put i n place appropriate policies that wi l l boost continuous

inflow of foreign portfolio investment in Nigeria.

viii

> LIST OF TABLES

4.2 Table 1: Foreign Direct lnvestment and Foreign Portfolio lnvestment Inflow in Nigeria (1 996-2005).

4.1 Table 4.1 Model 1 : ADF Unit Root Test on the Quarterly series

4.1 Table 4.2 Results from Co Integration Test on Model I Estimation

4.1 Table 4.3 Result Summary for Model 1

4.1 Table 4.4 Model 2 ADF Unit Root Test on the Quarterly Series

4.1 Table 4.5 Results from Co integration Test on model 2

4.1 Table 4.6 Estimation Result Summary for model 2

4.1 Table 4.7 Model 3 ADF Unit Root Test on the Quarterly Series

4.1 Table 4.8 Co integration Results Test on Model 3

4.1 Table 4.9 Estimation Result Summary for Model 3

4.1 Table 4.10 Model 4 ADF Unit Root Test on the Quarterly Series

4.1 Table 4.11 Co integration Result Test on Model 4

4.1 Table 4.12 Estimation Result Summary for Model 4

4.3 Table 4.3.1 Direction of Causality between FPI and FG proxied by (GFR)

4.3 Table 4.3.2 Direction of Causality between FPI and RRR 60

4.3 Table 4.3.3 Direction of Causality between FPI and Map 60

4.3 Table 4.3.4 Direction of Causality IFD and RGDP 60

% 4.3 Table 4.3.5 Direction of Causality between FD and RGDP 6 1

4.3 Table 4.3.6 Direction of Causality between IFD and Mcap 6 1

4.3 Table 4.3.7 Direction of Causality between FD and IFD 6 1

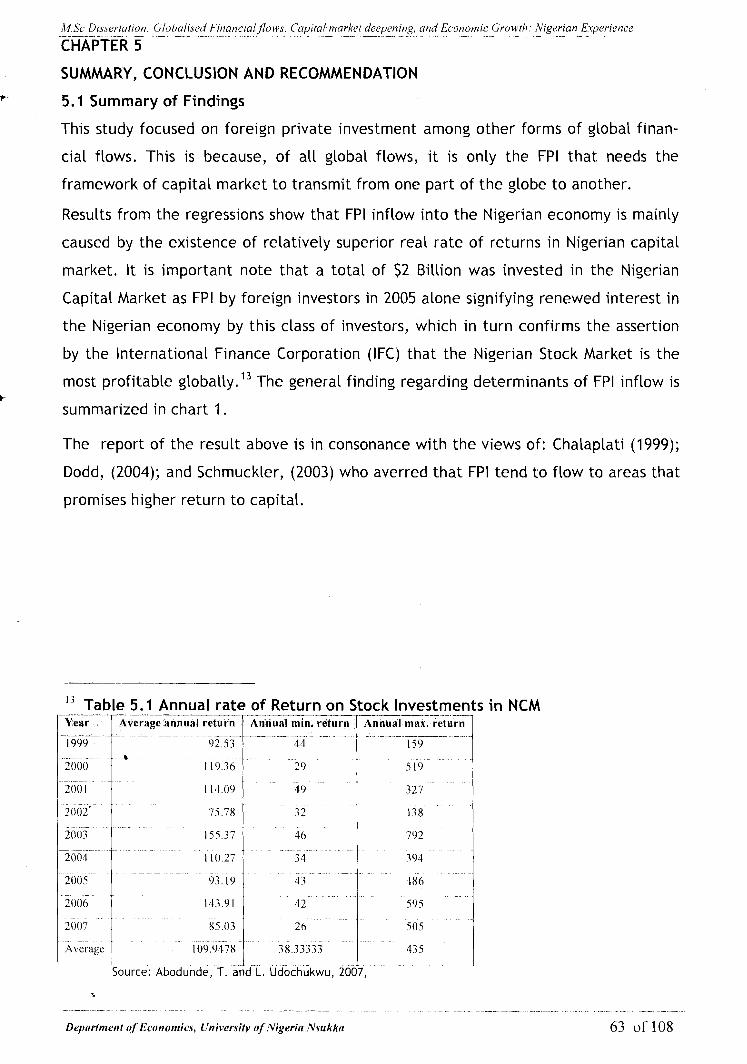

5.1 Table 5.1 Annual Rates of Return on Stock Investments in NCM (A Foot Note) 63

LIST OF CAHRTS -

1.1 Chart 1 : World Export of Goods and Series

1.1 Chart 2: Foreign Direct lnvestment

1 .I Chart 3: Annual Rate of Return on lnvestment at the Nigeria Capital Market

1.1 Chart 4: Global FPI Compared to ODA (Footnote)

5.1 Chart 5.1: Determinants of FPI in flow in Nigeria

5.1 Chart 5.2: Effect of Factors changes on Financial Depending of ESNCM

5.1 Chart 5.3: Effects of factor changes on capital Market deepening

7 5.1 Chart 5.4: Effects of factor changes on the growth rate of real GDP

5.2 Chart 5.1: Globalized flow (GFF), Transmission channels and Impacts

CHAPTER 1

b INTRODUCTION

1.1 Background of t he Study

A consensus seems to have emerged amongst economists that economic growth is

inextricably tied to globalised financial flows (GFF). This GFF - growth nexus is

implicitly implicated in the relation showing domestic savings and net capital inflows

as the main sources of financing domestic investment and budget deficit*. On

exploring the equality relationship between current account balance (CAB) and the

capital account balance (CAP) of a country, it becomes obvious that a deficit on the

CAB implicitly measures the financial inflows into the country's economy and there-

fore measures the resources coming into a country to finance investment demand in

excess of national savings, i.e. savings - investment gap - 51 gap (Diwivedi, 2006; T

Okojie, 2005; Roubini and Watchel, 1997). Since globalised financial flows into a

country indicate the resources flowing into the country, an inference could be made

motivated by the fact that i f GFF equals CAB which also equals CAP, then GFF is an

alternative for financing the SI gap when confronted with difficult domestic con-

straints". Economic theory based on: Harrod-Domar; Neoclassical; and Endogenous

Growth models, recognizes SI gap as being correlated with growth, therefore GFF is

intrinsically tied to growth (Hakkio, 1995; Ayhan et al, 2003; Calvo and Reinhart,

1999; and Smith e t al, 2003).

GFF needs the framework of financial globalization (FG) and financial integration (FI).

FG and FI are in principle different concepts. FG is an aggregate concept that refers f

to rising global linkages through cross - border financial flows. FI on the other hand

refers to an individual country's linkages to international capital markets. Obviously

the two concepts are intimately related. For instance, increasing FG is perforce

associated with FI on average and together they. imply increasing GFF (Ayhan e t al,

* Recall that Uses = Sources. Uses are usually for Investment (I) and Budget Deficit (BD), while Sources are

domestic Savings (S) and Net Capital Inflow (i.e. net of GFF) Hence: I + RD - S + GFF , 'd Domestic uses >

Domestic Sources, GFF > 0, GFF = I + BD - S

* CAD 2 CAP - GFF, but ?

CAP = CAD + AR = FDI + FPI + ODA but GFF = CAD + AX

i.2 GFF = FDI + FPI t- ODA .. . - -. .. -. ~- .- ~ . . ... . .. ..-.- .- . -- ..- .

Depczrtment yf Economics, Universify ryf Nigeria Nsukkn 1 of 108

~. .~ . -~ ~ . . . . --p--.----.-.--....---.-....-...--

2003). In this study, these terms are looseiy used, i n te r~hangeab~~ , without loss of

rigor in the pursuance of the central theme.

By definition GFF includes: official development assistance (ODA) and other official

development flows (ODF) -. i.e. grants or soft loans from government and mulhtilat-

eral institutions; export credit (EC) - i.e. all forms of international trade credits by

individuals or banks; and foreign private flows international bank loans and bond

issues, foreign direct investment (FDI), and foreign portfolio investment (FPI) - which

could be debt or equity (Obadan, 2004; and Okojie, 2006).

The GFF - economic growth relation i s usually explained in mainly two ways. One way

considers the relation to crystallize through two main channels: the direct and

indirect channels. The direct channels' GFF - growth link i s brought about by:

augmentation of domestic savings; lower cost of capital due to better risk allocation;

transfer of technology; and financial sector development of the capital market. The

indirect channels' categorization rationalizes the link on the ground that GFF:

promotes specialization; induces better policies; and enhances capital inflows by

signaling better policies (Ayhan et al, 2003). The other way sees GFF as being trans-

mitted through quantity and quality effects (Abiad et al, 2006).

ODA, EC, and FDI can be transmitted without the aid of the capital market, but FPI

necessarily requires the capital market to be transmitted to any nation. Capital

markets promote economic efficiency and productive investment by channeling funds

from surplus units to deficit units who have immediate productive use for it (Woep-

king, 2004). Therefore, GFF transmitted through the international capital market into

any nations capital market (ESCM) i s strictly of FPI type. The fact that FPI i s transmit-

ted through the capital market implies that it flows to those investments that

guarantee the highest rate of return (Dodd, 2004), thereby ensuring strict allocative

efficiency in the use of FPI (Chalapati,, 1999). Thus it promotes efficiency and aids

productive investment. Some countries, especially in Asia and Latin America have

been able to utilize it (FPI) for growth, even though there are reversals in the

aftermath of the 1982 debt crisis and in the middle 1990s respectively in Latin

America and Asia (Halac, 2005) . FPI comes with some benefits which includes the

following: spreadsldiversifies risk for foreign; provides an opportunity, for other

nations, to share the fruits of growth of developing countries; provides investment

T- outlet for foreign investors that promises a better return on investment - especially

.. for pension funds; it supplements foreign exchange availability and domestic savings;

l)epar/tnen/ of'Econoniics, Univer.~i/y of' Nigeria Nsukkrr 2 of 108

M.Sc Dissertation: Globdised Financinl,flows, C ~ ~ p i t a l mar.liet deepening, and Econonzic Growth: Nigerian Erperience ~ ~ . .. . . .... .... ~ ~. ~ .... - . .. .- .

it i s non debt creating; i f involved in primary issues provides critical risk capital for

new projects; expectedly, it could help to achieve a higher degree of liquidity at > capital markets; thereby causing an increase in the price - earning (PE) ratios and

consequently reduce the cost of capital for investment; and it helps to improve the

functioning of the financial system through increased availability of funds and

improvement of the financial infrastructure thereby reducing adverse selection and

moral hazard (Chalapati, e t al, 1999; Schmukler, 2003).

I t is probable that increasing confidence in the FPI - growth nexus inspired policy

makers world over - mainly encouraged by multilateral agencies - to opt for liberali-

zation of both the financial and commodity markets and also the capital account of

their respective countries. Under this policy of trade and financial liberalization,

there was a gradual dismantling of official controls on trade and capital. Conse-

T

quently, there has been a rapid growth in international trade and services, and also

in cross border financial flows. A trend catalysed by gradual removal of official

controls on trade and capital. Statistics show that between 1970 and 2000, the value

of world exports of goods of goods and services increased by 25 percent, while

foreign direct investment (FDI) increased by 50 percent (Rybinski, 2006; Dodd, 2000

(See charts 1, 2)). At the same time private flows (debt plus equity (FPI)) surpassed

official flows (aid plus debt (ODA)) by more than seven fold by 1997 and maintained

dominance till 2003 (Rybinski, 2006)*.

In this regard, Ayhan Kose e t al, (2003) and Woepking (2004) had noted that one of

the most important developments over the past three decades has been the interna-

tionalization, and now globalization, of capital markets which gave rise to the

International Capital Market (ICM) that is composed of a number of closely integrated

markets with an international dimension. ICM allows the possibility of fund mobiliza-

tion from all over the world for subsequent investment at any point on the globe.

Source: World -. Bank's Global Development - Finance. ~ - - .. ~

Depnrtnwnt of Econonzics, Universi[v of Nigeria Nsukka 3 of 108

Al.Sc Dissertation: Glol~crlised Financinl,fTows, Capitol nlarltet deepening, and Econon~ic Growth: Nigerian Experience -.-- -- ~~ . .... .. . . - .- .. - In 1993, the Federal Government of Nigeria liberalized the Nigerian Capital Market

(NCM) and subsequently internationalized it in 1995 with the abolition of the laws

that constrained foreign participation in the NCM. Specifically, the Exchange Control

Act, 1962 was abrogated together with the Nigerian Enterprises Promotion Act, 1989

(NigeriaBusinessinfo.com, 2001). Also a lot of improvements have been made on the

operational fundamentals of the stock exchange. For instance: it operates a comput-

erized clearing and delivery system for transaction in securities listed on The Nigerian

Stock Exchange; and settlement cycle i s now T + 3. These developments paved the

way for foreigners to participate in the NCM both as operators and investors (Nigeri-

aBusinessinfo.com, 2001). In fact the International Finance Corporation, in the year

2005, rated the Nigerian Stock Market as the best in terms of returns on investment

universally (Abodunde e t al, 2007 -See chart 3). Nigeria was, as a result of al l these

development, placed on a vantage point for reaping the inherent benefits in both FI

and FG even as GFF increases with more FPI flowing in to the Nigerian capital market.

With increased inflow of FPI into Nigeria, it i s expected that: the capital market's

liquidity would improve; and there wi l l be enhanced capital market efficiency, and

reduced information asymmetry. Simply put, there would be deepening of the capital

market and, filling of SI gap' in the domestic economy which has been characterized

by inadequate savings, these would bring about economic growth.

Available literature reveal that finance matter in engendering growth, as such, since

GFF i s part of the financial flows critical for financing investment, it equally matters.

Arising from this backdrop, what i s the relationship between GFF and economic

growth in Nigeria? Particularly, does the inflow of FPI contribute to financial sector

development and through that means associated with growth?

1.2 *STATEMENT OF THE PROBLEM

The NEEDS document (NPC, 2004) has indicated a savings - investment (SI) gap of

about 20 percent for Nigeria, with the consequence that the annual average invest-

ment rate was about 16 percent of the GDP, clearly below the minimum investment

rate of about 30 percent needed to unleash a poverty - reduction growth rate of at

least 7 - 8 percent per year (NPC, 2004). The sovereign risk premium for Nigeria i s

In the National Economic, Empowerment and Development Strategy (NEEDS) document it has been

estimated that Nigeria has a savings investment gap of 7 percent. Note also that capital market

elopment. . - . .... ~... . .- . . . . .. . - -. ..

Dep~rtmerrt of Economics, University qf Nigerirr Nsukkrr 4 of 108

M S c Dissertation: Globalised Financial,flows, Capital n~orliet deepening, and Econoniic Growth: Nigerian E.xperierm --pppppp--.--.--.p--p ~ ~p~ ...............................................

perceived to be high. Equally the cost of doing business i s also high, thus private

business agents kept the bulk of their money abroad (NPC, 2004). In view of these,

coupled with the fact of wide spread mass poverty, it i s substantially difficult to raise

national aggregate savings rate to cover the SI gap. Measures to f i l l 51 gap have to be

provided i f Nigeria i s to be placed back on the path of economic prosperity.

Received theory from the Harrod -- Domar growth model shows that a basic growth

strategy i s to reduce the 51 gap by increasing the proportion of national income

saved, and this can be done through general consumption sacrifices. Recourse could

also be made to GFF (Smith et al, 2003). In other words, growth can take place if,

among other things, observed 51 gap is filled. Plethoras of literature exist to show

that foreign capital inflows could play critical roles in the filling 51 gap (Hakkio, 1995;

Okojie, 2005). Indeed, Capital flows have contributed in fi l l ing the resource gap in

countries where domestic savings are inadequate to finance investment (Mailafia, -?

2005). Therefore it i s envisaged that capital inflow would help Nigeria fast track

higher production levels and hence attain the Millennium Development Goals (MDGs)

and the objectives of NEEDS (Mailafia, 2005). FPI i s also expected to have a positive

impact on the levels of savings and investment, efficiency of investment, and also

enhance best practice, hence leading to higher productivity.

Recent works have shown some causal relationships between GFF and positive

quantity effects', the works of McKinnon (1973), Shaw (1973), Obstfeld (1994), and

Ueda (2000) generally show that increases in GFF positively impact output growth

through quantity effects. However, some economists have cautioned that it might not

be correct to always expect quantity effects under libralisation (Devereux and smith 1

1994; Bandiera and others 2000; Jayaratne and Strahan, 1996; and Sancak, 2000).

Quality effects2 due to GFF have been established by the works of many scholars.

Abiad'et al (2004) showed that financial libralisation (FL) brings about improved

allocative efficiency of the capital market. Corroborating this, King and Levine (1993)

have argued in their work that FD results i n economic growth. De Gregorio (2004)

showed that FD brought about increases i n GDP by increasing the efficiency of

investment. The works of Rajan and Zingales (1998); Wurgler (2000); Beck, Levine,

I Quantity effect refers to increase in the magnitude of savings and investments as a result of financial globalization.

-v ' Quality effect refers to increases in efficiency levels as a result of financial globalization. (See Abiad, et al, 2004.

The Quality Effect: Does Financial 1,ibralization Improve the Allocation of Capital'? IMF working paper

wp/04/1 12. . - ~.

Dqnr tn tmt qf Econonlics, University ofNigerin Nsukko 5 of 108

A1 Sc Dr wertcrtron Globalrwd Flnuncd flow^, Cnprtcd niurltet deepenrng, ond Econonllc Growth Nrgenun Experience .- -- - - - - - - . . - -- -- - - - - - - - .. - - . - - - -

and-loayza (2000); and Love (2001); argue: that industries which are more dependent

on external finance grow more slowly than other industries in countries with less A. developed financial markets (whether measured by financial depth or improved

accounting standards); and that in countries with deeper financial sectors, capital i s

better allocated in the sense that it tends to flow to growing industries. FPI leads to

FD which then affects GDP growth through increases in total factor productivity,

rather than through factor accumulation. FD i s associated with a drop in the sensitiv-

i ty of investment to the availability of internal funds (Abiad et al, 2006).

Thus, as the beam of globalisation settles on Nigeria, the following questions are apt

to be asked:

a. Has globalisation brought about increased flow of FPI into Nigeria?

b. Has financial globalisation brought about capital market deepening in Nige-

ria?

c. Has the deepening of the capital market engendered economic growth in

Nigeria?

1.3 OBJECTIVES OF THE STUDY

Generally, this research work seeks to confirm i f the inflow of FPI engendered by GFF

has impacted Nigeria's economic growth positively. However, the following particular

objectives wi l l be pursued:

a. To determine whether increased globalisation 1 financial liberalization has

positive relationship with increased inflow of FPI into Nigeria.

b. To ascertain whether globalised financial flows has engendered capital

market deepening in Nigeria.

' c. To find out i f the stock market deepening precipitated by globalised finan-

cial flows has brought about economic growth in Nigeria.

1.4 STATEMENT OF HYPOTHESES

In line with the preceding objectives, the following hypotheses are formulated:

a. Globalisation has not facilitated increased inflow of FPI into Nigeria.

b. Financial globalisation has not contributed to capital market deepening

in Nigeria.

Drynrtment of l:'cononlics, University yf Nigrrirr Nsukkrr 6 of 108

h1.S~ Dissertation: Clobnlised Fit~uncial,flows, Capital marltet deepening, and Economic Growth: Nigerian Experience ~ ~ .... ~~~ ~.. -

c. Capital market deepening as a result of globalised financial flows has

not brought economic growth in Nigeria.

1.5 IMPORTANCE OF THE STUDY

Some studies have been carried out to show the relationship between financial

deepeningjfinancial development and economic growth (Wallich, 1969; Schmidt -

Hebble, 1994; McKinnon, 1973; King and Levine, 1994; Levine and Zervous, 1998;

Montiel, 1994; De Gregorio, 1998; Schmuckler, 2003; Adiad et al, 2006; and Ndebbio,

2004). One way in which this study is essentially different from them is that it

particularizes on capital market deepening as an aspect of financial sector develop-

ment.

Particularly, the works of Wallich, 1969; De Gregorio (1994); and Ndebbio (2004)

share certain similar features with this study. For instance, the cross country study by

De Gregorio (1998) used indicators based on: lnternational Arbitrage Pricing Model - lAPM - as developed by Levine and Zervous in 1995; lnternational Capital Asset Pricing

Model - ICAPM - also as developed by Levine and Zervous (1998); Gross Capital Flows

Ratio - GFR - developed by Montiel in 1994, but transformed into discrete values; as

proxies for financial integration - FI - (i.e. globalisation), while variables such as:

Bank Credit; Market Capitalization; Total value of Shares Traded in a year; and Stock

Market Volatility were used as proxies for financial deepening (FD). He showed that FI

(FG or GFF) leads to FD of the domestic financial market, and through that channel

foster economic growth.

Though a part of this study investigates the relationship between FI and FD, it differs

from the work of De Gregorio in the sense that it typifies the Nigeria experience

under financial Globalization. Another difference is that this study avoided the use

IAPM and ICAPM as they have some shortcomings. This derives from the observation

that tests of any sort using IAPM require the identification of an adequate interna-

tional factor model, and since such a model is lacking at present, it is not possible to

say whether or not arbitrage pricing relationships hold internationally (Sharpe, 1985).

Also, if international capital markets are completely integrated, a type of ICAPM

might hold, while i f the markets are completely separated different Capital Asset

Pricing Models (CAPM) might hold for each country, but recent researches were

inconclusive on whether international markets are completely integrated or com-

pletely separated (Sharpe, 1985). Hence, IAPM and ICAPM were not used in this work.

. ~ ... - ~ - .. - .

Depprrrmtrnt of Ecoaotnics, Universiv of Nigeria Nsukkn 7 of 108

M S c Dlssertntroii Global~sed F ~ n n n c ~ a l j l o w ~ . Cnp~tol imrXet deepenlng, ond E c o n o i n ~ ~ Growth Niger~an Experience . --A --- - . -- - . -- -

Equally, GFR transformed into discrete flow was considered inferior to GFR in the

continuous mode for the purpose conducting impact analysis. Hence, unlike the work b De Gregorio, this study used GFR in continuous flow to proxy globalisation, and as

such expects a more robust result. Finally, it differs from the work of De Gregorio in

the sense that he (De Gregorio) related GFF to FD, and through that means to growth

- this study first relates GFF to the financial deepening of the external (international)

segment of the nation's capital market (IFD) and from there it i s linked to growth

through capital market deepening (FD).

Similarly, this work can be likened to Ndebbio's work (Ndebbio, 2004) in the sense

that they both analysed the relationship between financial development and eco-

nomic growth. Particularly, Ndebbio (2004) has shown for Sub Saharan African (SSA)

countries that FD leads to economic growth and development. He proxied FD in SSA

M .r countries by the degree of financial intermediation - measured as---", and the

Y

growth rate of per capita real money balances (GPRMB). In this vein also, De Gregorio

used: Credit by the Banking sector to the private sector; market capitalization as a

fraction of GDP - MCAP; total value of shares traded as a fraction of GDP - TVT;

volatility index for the stock market - VOL. to proxy FD. Clearly, these proxies do not

clearly show FD due to GFF; of FPI type equally these proxies are affected by internal

factors and hence would not show FD mainly due to GFF. However this study

uses - FPI

- - , i.e. the ratio of foreign portfolio investment in the external Re a1 Non GDP

segment of the Nigerian capital market to real non oil GDP (IFD) as a proxy for the

+ capital market deepening of the international segment of the Nigerian capital

market. This allows the liberty to specifically look at financial deepening 1 develop-

ment from the perspective of developments in the offshorelinternational segment of

the Nigerian capital market or due to GFF. Also Ndebbio's work was interested in

fineancia( development3 in general while this work particularizes on the effects of

deepening of both the domestic and external segments of the capital market. In

these ways, this study i s different from the works of Ndebbio (2004) and De Gregorio

(1998). It i s equally the first of i t s kind to use stylized facts to link GFF of the FPI

type, to economic growth in Nigeria.

' There is a strict difference between financial sector development (FSD) and capital market deepening (FD). FD is

in fict a subset of FSD. - - -

Department 01 Econonricr. Univer5ify of Nigeria Nsukkn 8 of108

A4.Sc Dissertation: Globalised Financialjlows, Capital market deepening, and Economic Growth: Nigerian Experience ~

Presently, there i s dearth of empirical literature linking FPI to economic growth in

Nigeria; therefore this study would add to empirical literature in this gray area.

1.6 Scope and Limitations o f the Study.

This study i s restricted to analyzing the impact of GFF of the FPI type on, firstly,

capital market deepening in Nigeria and ultimately, on economic growth. In doing

this, our main interest i s mainly the foreign portfolio investment flows to Nigeria.

This means that even though FDI, foreign commercial bank loans, ODA (whether

multilateral or bilateral) were al l mentioned in this study, our analysis mainly

centered on FPI and i t s effects on the capital market and economic growth in Nigeria.

This study i s also limited to some extent due to lack of data. For instance, in model-

ing the impact globalization on FPI flows to Nigeria, available literature show that

Nigerian Sovereign Risk Premium ought to be included as one of the explanatory

variables, but this was not possible due to non availability of data. Use was therefore

made of the size of sovereign national debt. Equally, the non availability of data on

FPI flows into Nigeria for the period 1986 downwards constrained this study to work

from I986 upwards.

~ . ....

Depnrtmenl @Economics, University of Nigerirr Nsrrkkn 9 of 108

M Sc D~ss~.rtutrovr Globnlrred F~nunclal flows Cnpltal 17znrket deepening, and Econonzic Growth Nlgerian Experience - --- - . . - - - -- - - - - --- -

CHAPTER TWO r

LITERATURE REVIEW

2.1. Globalization Finance and Economic Growth.

The ultimate yardstick of a country's economic success i s i t s ability to generate a

high level of production of goods and services for i t s population (Oduh, 2006). In

other words, productivity i s central to societal welfare. Therefore sustained increase

in productivity, i.e. economic growth, i s arguably an issue of primary concern to

economists in both developed and developing countries (Turnovsky, 2000). In fact,

economic theory shows that economic growth can be realized in two ways: increase

in the amount of factors of production; or increase in the efficiency with which those

factors are used. Thus, growth i s induced by the increases in investments (i.e. capital

accumulation) and the efficiency of investments (De - Gregorio, 1998).

There i s growing awareness among economists that capital accumulation plays a vital

role in economic growth. This can be discerned from the Harod - Domar, neo classical

and endogenous growth models (Smith et al, 2003; Aysit and Nil - Demet, 1997; and

Turnovsky, 2000). Therefore in economies where capital i s deficient, economic

growth is most likely to be hampered. In situations where it i s not possible to raise

investment levels due to deficient savings, recourse could be made to foreign inflows

(Baye et al, 2006; Hakkio, 1995). In fact, investment in an open economy i s equal to

the sum of domestic savings, capital inflow and budget deficit. The relation between

investment, capital inflows and domestic savings i s positive, while it i s negatively

related to budget deficits. Therefore, i f there i s no budget deficits and domestic

savings are inadequate, then capital inflows become critical to investment and by

externion to economic growth (Hakkio, 1995).

Thus foreign sources could be a good alternative of filling observed savings - invest-

ment gap in any given economy (Schmuckler, 2003). In this regard, it has also been

observed that foreign inflows can bring about capital formation, and also lower the

cost of capital to firms, especially those with access to the capital market (Schmuck-

ler, 2003; De - Gregorio, 1998). In fact, when international financial flows are

allowed into a country, it helps the functioning of the financial system through:

increased availability of funds; and improvement in the financial infrastructure

/Schmuckler, 2003). Simply put, financial globalization brings about financial sector

MSc Dissertntiori: Globtrlised Firiarzcia/,f~o~:s. Capital nzarlcet deepening, a d dcorzonzic Growth: Nigerian Experience . . .. . ... .- ~~ ~~

~ .. , - ~ -

development (De Gregorio, 1998; Schmuckler, 2003), while financial sector develop-

ment brings about growth (Ardic, Oya Pinar and Damar, H. Evren, 2006). Oks (2001 )

argued that existing finance - growth nexus literature which started with Bagehot

(1873), Schumpeter (191 1 ), Hicks (1969), and Mckinnon (1973) showed that there is a

positive relationship between financial development and growth. This conforms to

later studies on the finance growth nexus by Levine (2005), De Gregorio (1998), and

Levine and King (1994).

International financial flows have its surges closely linked to financial globalisation.

Financial globalisation, besides engendering improvements in the financial sector

infrastructure, brings about the maximization of the benefits of credits; it catalyses

competition in the provision of funds - thereby generating efficiency gains; i t makes

way for the adoption of international accounting standards, thereby increasing

transparency and good corporate governance - brought about by the introduction of

international financial intermediaries and new shareholders who now monitor the

management, which results in pushing the financial sector towards the international

frontier; i t allows the increase in the technical capabilities for engaging in precision

financing to be passed on to local and global markets; stringent market discipline

imposed by financial globalization has consequences not only on the macro-economy,

but also on the business environment and other institutional factors (Stulz, 1999;

Crockett, 2000; and Stiglitz, 2000). Financial globalization brings about financial

development which has a dual effect on economic growth. On the one hand, the

development of domestic financial markets may enhance the efficiency of capital

accumulation. On the other hand, financial intermediation may contribute to raising

the savings rate and, thus, the investment rate. The former effect was first empha-

sized by Goldsmith (1969), who also finds some positive correlation between financial

development and the level of real per capita GNP. In addition, Goldsmith (1969) also

argues that the process of growth has feedback effects on financial markets by

.creating incentives for further financial development.

Nevertheless, it is not deterministic that financial globalization must bring about

economic growth. This i s because of the existence of some puzzles i n international

financial economics - the home bias puzzle i n portfolio investment and the high

correlation between saving and investment within an economy with no or limited

barriers to cross-border financial flows. The home bias puzzle was identified by

French and Poterba (1991), who noted the low proportion of foreign stocks in

--

Depnrtntent o f Economics, University of Nigerin Nsri kkn 1 1 of 108

MSc Dissertation: Globalised Financialjlows, Capital market deepening, and Economic Growth: Nigerian Experience - - portfolio investment compared with the optimal levels suggested by the trade-off.

between risk and return. Investors seem to totally or partly ignore the benefits > associated with the diversification of the sources of risks, as may be achieved through

a wider geographical coverage. As emphasised for example by Obstfeld and Rogoff

(2000) in lssing (2000)) a possible explanation for home bias is the existence of

various forms of transaction costs for cross-border purchases and sales of financial

instruments. However, Tesar, L., and I. Werner (1995) point out that such transaction

costs are unlikely to be very high since turnover in foreign stocks is larger than for

domestic stocks. Hasan and Simaan (2000) focus on information asymmetries. They

show that home bias in portfolios of stocks can be reconciled with theory in the

presence of uncertainty regarding the estimation of returns and risks on foreign

stocks, provided such uncertainty i s higher than for domestic stocks. In some

countries, a further explanation for home bias i s the existence of restrictions on the f

range of instruments which can be held by certain categories of investors, such as

quotas on foreign country exposures of investment funds for example.

Feldstein and Horioka (1980) identified another puzzle. They remarked that, over the

long run, developments in domestic saving and investment rates were highly related

than theory would suggest. Thus, by implication, the financing of investment and the

placement of savings seem not to take ful l advantage of international financing and

placement opportunities. Plethora of explanations have been proffered to clarify the

Feldstein- Horioka puzzle, many are similar to the explanations envisaged for the

home bias puzzle. For instance, Obstfeld and Rogoff (2000) posit that transaction

costs can help explain not only the home bias puzzle, but also the Feldstein-Horioka C puzzle as well as other puzzles i n international economics such as the low cross-

country correlation of growth rates in consumption.

As poir~ted by several authors, however, there i s evidence that, although they s t i l l

exist, the puzzles have become less pronounced over recent years, as net cross-

border financial flows have increased. Specifically, international banking activity has

increased steadily i n recent decades as large banking institutions developed activities

at the global level. In addition, both the amount outstanding of securities issued in

foreign currencies and the amount outstanding of securities held by foreign investors

increased rapidly over recent years. As a result of these developments, there seems

t o be a progressive shift in the average composition of portfolios by currency and

issuer, towards patterns more in line with those suggested by the theory.

- . .

Departnzent of Ecotionzics. U11iversi1~- qf Nigeria Nsukka 12 of 108

MSc Dissertation: Globalised Finuncial~flows, Cup&~l market deepening, and Econonzic Growth: Nigerian Experience -. - -- - - - .- -. -- -

Some economists have gone beyond how the puzzles play out themselves to actually

say that there is a negative relationship between globalization and economic growth.

For instance, Oks (2001) has pointed out the work of Jappelli and Pagano as

emphasizing the possibility that the relation between financial intermediaries'

development and economic growth can be negative.

Today the endogenous growth theory i s prevailing and the existence of the

relationship between financial sector development and economic growth i s set

beyond doubt by the scientists. The matters of direction, robustness and, of course,

causation s t i l l provoke interest (Oks, 2001).

Finally, five views regarding finance growth nexus debate have been identified by

Levine (1997): first, one of the views attributable to Hamilton, Bagehot, and

Schumpeter, argues that finance ignites growth; a second view traceable to Adam

Smith opines that finance hurts growth; a third view due to Robinson is that finance i s

growth led; a fourth view credited to Lucas avers that growth is finance neutral; and

a f i f th view, mainly canvassed by World Bank and IMF emphasize that finance matter

because there is financial crisis.

Finally, we conclude by deducing that i f finance matters, then GFF being a part of

the financial flows, needed to finance investments, equally matters.

2.2 FOREIGN CAPITAL FLOWS T O NIGERIA: NATURE, TREND AND IMPACT ON THE

CAPITAL MARKET.

Of al l the foreign capital flowing into Nigeria, which comprises of: Official develop-

ment assistance - which could be either multilateral flow or bilateral flow; commer-

cial bank loans; commercial credits - which could be either buyers' credit or suppli-

ers' credit; foreign direct investment; and foreign portfolio investment, foreign

portfolio is totally distinct from the others in the sense that it i s the only type of

foreign capital inflow that passes through the capital market.

L)eprirtnzeat of Ecoaonzics, University of Nigerin Nsukka 13 of 108

MSc Dissertcrtion: Globnlised Finnncial,flows, Capital nzar.ltet deepening, and Econonlic Growth: Nigerian Experience -. -- .... -- ............ .. - .................... .....................

Table 1 - - - -- -

FPI -.-......- - . I -- - -- - - - - --- . . 7 FDI

Table 1 reveals that from 1986 FPI started featuring in the nation's balance of

payment account. From this time to 1997, the volatility of FPI flows has been

high as FPI hovers between positive and negative values. I t is worthy to note

that the period coincide with when the country was characterized by political

instability occasioned by unending transition programme of the Babangida re-

gime, the annulment of the June 12 election in 1993. The short lived Interim Na-

tional Government headed by Chief Ernest Shonekan, the 1993 coup by Abacha

and the draconian style of leadership that characterized Abacha' regime. Within

these periods, net FPI was mostly negative. I t could be argued that the sovereign

risk premium was high for the country. This most likely disturbed the investment

activities of foreign investors. By 1998, with the return of democratic govern-

ance, FPI flow into the country (Nigeria) improved from negative to positive. I t

(FPI) had kept improving that by 2005 the value of FPI has surpassed FDI flow

........ . . . - . . . . . -. . - .... ..-..... - - .. ...

L)epnrlnzenl of Econonlics, University of Nigerin Nsrrkkn 14 of 108

MSc Dissertation: Globalised Financialjlows, Capital madcet deepening, and Econonzir Growth: N~gerian Experience p--...-.--p.p--. -. .. . . . -.. . -.-.--- ~. - -~.. ..

into the country.

The relative importance of Portfolio investment to a small emerging market like

Nigeria has risen in recent years and this has led to the libralisation and internation-

alization of the capital market. Since the internationalization of the Nigerian stock

exchange, which i s a part of the financial liberalization policy of Nigeria, there has

been increased inflow of foreign portfolio investment into the Nigerian economy

through the capital market (Obadan, 2004). Thus, for Nigeria, the increase in foreign

portfolio investment has been fueled, partly by the process of globalization and the

ensuing deregulation of the capital market. A fact that i s hard to ignore i s that the

stock market i s getting good attention from foreign investors and fund managers with

its exceptionally good returns becoming too good to ignore (Uzor, 2007).

The increase in private capital flows especially foreign portfolio investment has

stimulated an intense debate about the impact of such on an emerging market like

Nigeria. Proponents emphasize the positive impacts of such flows on growth and

financial sector development, while critics express concern about i ts volatile nature.

A common concern however is that economic growth resulting from such volatile

flows is unsustainable and adversely affects the financial sector of the economy.

However, the potential contribution that FPI can make to financial sector develop-

ment and economic growth especially when regulated is enormous.

2.3 DETERMINANTS OF FOREIGN PORTFOLIO INVESTMENT (FPI)

Portfolio investment flow into Nigeria is quite a recent phenomenon. Up to the mid

1980s, Nigeria did not record any figures on Foreign Portfolio investmenred inflow in

her balance payment accounts (Okojie, 2005; Soludo, 2006). The reason for non

participation of foreign investors derives from the non- iberalization and internation-

alization of the country's money and capital markets (NSE, 2006). Thus the interna-

tionalization of the Nigeria Capital Market in 1995 is one of the reasons for enhanced

'in flow of FPI (NSE, 2006).

In Nigeria, the composition of Foreign Portfolio Investment are: Transactions in

bonds, debentures and notes as well as non-direct investor equity, preferred stocks,

mutual funds and investment trusts, also are transactions in money market instru-

ments like treasuring bills (Olisadebe, 1995). Many nations have taken steps to lure

foreign investors by tinkering with their fiscal and monetary policies to create an

.economic climate that is conducive. This is because reformed markets and increased

Ueprtnzent qf Bmnomics, University qf Nigerin Nsrikk(1 15 of 108

AbSc Dissertation: Globalised Fin~~ncial flows, Capital nzarlcet deepening, and Economic Growth: Nigeritm Experience ~ ~

legal protection for foreign investors are very necessary in attracting NPI (Macdonald

e t al, 2006; and Levine, 1995). > Reforms are facilitative of FPI in flow while the pursuit of higher rates of returns is

central to FPI inflow (Dodd, 2004). High rates of return are indicative of enhanced

economic growth. Increasing marginal efficiency of capital leads to increases in

economic growth (Jhingan, 2003). This derives from the Passinette's Profit- growth

model which stipulates that growth could be accounted for by sustained profitability

of economic activities. Thus sustained increases in growth rate can spur inflow of FPI.

Equally a surge of capital inflows into a developing country can be triggered by the

lift ing of restrictions on the capital account, know as capital account liberalization,

and by a policy to privatize what were formerly publicly owned assets such as the

telephone or rail way system (Dodd, 2005; Uzor, 2006). The policy of privatization

opens up avenues of investment for FPI, and availability of such investments could a-

course a surge of capital inflows in a developing country.

Foreign portfolio investment flow is also affected by the risk of changes in exchange

rates and interest rate, otherwise known as market risks (Hackio, 1995). Loss of

investors' confidence triggered by rising external debt, political instability and

extreme instability in macro economic fundamentals could make foreign investors

shun investing in a country (Hackio, 1995; Fitch Soveriegn Rating, 2005; and Dodd,

2004). The size of the sovereign external debt captures these risks and therefore

could be used as a proxy for sovereign risk. When the sovereign risk premium of

nation is high, it becomes difficult to attract FPI and even where it i s attracted; it

would be on unfavouarble terms (Hakkio, 2005).

+ In the view of Mundell (2000), deregulation, privatization and advances in technology

can be the reason for foreign direct investment and equity investment in emerging

markets by firms and household from developed countries. Another factor that cannot

be igtored in attracting FPI i s institutional quality. Foreign investors demand and

extract a high level of discipline on firms, and this i s essential in forming their

decision to invest (Levine, 1999; Schmukler, 2003).

To foster the level of economic growth required to create jobs, raise living standards,

and hasten development, sub Saharan African (SSA) nations need to attract more

foreign capital (McDonald, e t al., 2006). Along this line, many nations have taken

steps to lure foreign investors. They have changed fiscal and momentary policies to

create a more stable economic climate. They have reformed their national markets

and increased legal protection for investment (MacDonald e t a/. , 2006). . . . ~ .. - ..- ... -. . ..... . - . . . . ... . - - . .. -. -. .

l)epcrrtnier~t oj'l:'cononiics, University qf'Nigericr Nsukkn 16 of 108

M Sc Dmermtron Globalrsed F~nancral~7ows, Capital market deepenrng, and Economrc Growth Nrgerran Experrence - - - . - - - - -- --

Besides the twin factors of higher rate of return and policy incentives, other drivers

of FPI inflow exist. Soludo (2006) has identified other factors which attract capital

inflows as macroeconomic stability (especially price and exchange rate stability),

openness and competitiveness of the economy as well as stable political environment

and good infrastructure. UNCTAD (2003) also points to favourable rates of return of

nations as another factor that attracts FPI.

2.4 THE NIGERIAN CAPITAL MARKET: DEVELOPMENT AND REFORMS

2.4.1THE CAPITAL MARKET AND ITS INSTITUTIONS

The capital market is the long term end of the financial market. I t specializes in the

mobilization of medium to long-term funds for investment and development pur-

poses. Transactionary activities in the capital market revolve around issuance and

marketing of shares, bounds and debenture (CBN, 2000). The markets that make up

the capital market are the primary market; and the secondary market.

The Primary Market

In this market are traded new issues of securities. The mode of offer of securities

traded here consists of: offer for subscription: right issues; offer for sale; and private

placements. Most of the dominant mode of issues is equity offer which accounted for

59% of the market i n 1999. Others are: rights issue, which constitute 36.7%; deben-

tures, which make up 3.1%; private placements constitute about 0% of the transac-

tions in the primary market (CBN, 2000).

The Secondary Market

This is the market where existing securities are re-traded. This is made up of stock

exchanges and over the counter markets where securities are bought and sold. CBN

(2000) has noted that secondary market activities have increased over the years. This

'was attributed to the opening of trading floor in more parts of the

Nigerian Stock Exchange (NSE), and the elimination of institutional

impediments to operational efficiency, including foreign investment

also dominates i n this market

The Nigerian Stock Exchange

country by the

and regulatory

flows. Equities

The Nigerian stock exchange evolved from the Lagos Stock Exchange which was

=incorporated in 1960. I t became the Nigerian Stock Exchange (NSE) in 1977 (CBN, .- .. . - - -. - .. - - - .. . .. .

Deyartntent o f Ecortoniics, U~tiversify of' Nigeria Nsukkn 17 of 108

M Sc D~sserlallon Glolx~l~sed Frnuncml flows, Capital mar/cet doepenlng, and Econo~nrc: Growth N~ge twn Experwnce - -- - . - - . - . - - -. -- - - - .- - . - - - - - . - - -

2000, and NSE, 1998). Since its inception, the NSE has grown to have many trading

floors across the country. These trading floors are i n Lagos; Kaduna; Port Harcourt;

). Kano; Onitsha; Ibadan; Abuja; and Yola. The head office of the exchange is in Lagos

(NSE, 2006). NSE commenced trading with only 19 securities on its floor, however, at

present there over 300 securities being traded on the floor of the exchange (Monye,

2007).

In 1995, the NSE was internationalized with the result that quoted companies can

now access funds from international markets through Global Depository Receipt (GDR)

or American Depository Receipt (ADRs) etc using their shares as the covering securi-

ties (Nigeriabusinessinfo.com, 2001 ).

At present, the NSE has over one 1.5 million individual investors and hundreds of institutional

investors (including foreigners who own 40% - 60% of the quoted companies (NSE, 2006). The

.... NSE is the fastest growing exchange in the world today, with a market capitalization of $61.3 16

billion as at the end of June 2007. Analysts' project that is has the capaeity to hit $100 billion

mark by the end of 2007 (Monye, 2007). Furthermore, the NSE is the most profitable in the

whole world (Abodunde, 2007, and Monye, 2007).

2.4.2 Developments i n the Nigerian Capital Market

Uzor (2007) has noted that some significant developments in the business and

economic environment have led to greater attention and reliance on the capital

market.

Reforms induced by Privatization Policies

Ever since government policy started shifting in the direction of limiting the role of

the state in business activities the reform of the capital market has been a crucial

requirement for creating a viable private sector (Uzor, 2007) some of these require-

ment are in the form of more accounting information disclosure, improved capital

. market infrastructure and product offerings like e-bonus, e-dividend, e-IPOs, and e-

POS. These reforms led to and reinforced further reform in the market.

Universal Banking policy triggered reform in the capital market:

The CBN announced the Universal Banking policy of the Government i n 2000. This

policy initiative was the main starting point of sustaining rapid growth and discarding

institutional distinctions in the banking sector. The policy opened the doors of capital

market business to commercial banks. The result is that the rapid growth in the

Departmettt of Economics, University of Nigerin Nsukkn 18 of 108

MSc Dissertation: Clobnlised Fintmcitrljlows, Capital nzarket deepening, and Econonzic Growth: Nigerian Experience ~

financial se rv i ce~ indus t r~ found an expression i r i a market set for explosive growth

(Uzor, 2007).

Introduction of the Emerging Market

The Emerging Markets was introduced in April 1985~. NSE in i ts "presentation notes"

states that Emerging Market (formerly second Tier Securities) are the small compa-

nies (upstarts) that are yet to meet all the listing requirements of the NSE. The main

purpose of the Emerging Market is to encourage indigenous entrepreneurs to access

the stock market. In the Emerging market, a company may not be allowed to raise an

amount in excess of W100 million. Under the Emerging market rules; an individual can

own up to 90% of the shares. This adds flexibility to the restriction of an individual

not allowed to own shares in a company in excess of 5% of the company (NSE, 1999).

Thus the Emerging market architecture in the capital market makes it possible to

raise funds for business whose potentials are not immediately known to the public.

Establishment of the Indigenous Quoted group (IQG)

The IQG was formed and established in 1997 by indigenous quoted companies on the

Nigerian stock exchange as a platform for indigenous quoted companies to discuss

issues of common interest (NSE, 2006). Thus it forms a forum for the critique of issues

and developments in the capital market and juxtaposing them against the realities of

the times with the interest of the Nigerian quoted companies paramount. I t is hoped

that this development wi l l lead to synergy and subsequent fine tuning of capital

market policies i n a way that wi l l move our industries forward.

Automated Trading System (ATS) and Electronic processing of share issues.

The ATS is a security arrangement whereby transactions on the stock Exchange are

carrigd out through a network of computers. The ATS was launched in April 27 1999.

I t has facility for remote trading and surveillance (NSE, 2006). The ATM makes it

.possible for dealing members to trade on-line-real-time from their offices. The ATS is

tightly coupled with the CSCS (Central Securities Clearing System). In view of this,

when brokers enter their orders for buy, for instance, the system goes into the CSCS

system to verify i f the account numbers entered by the broker exist and i f the stocks

4 NSE in its 'Presentation Notes' states that Emerging markets (formally Second Tier Securities) are for the small

companies (Upstarts) that are yet to meet all the listing requirements of the NSE. The main purpose of the Emerging

Market is to . encourage - .. indioenous . ._a entrepreneur., . ... .. to . access . . - the stock market. .- ~

~ . .. . . -. - .. . -- .. . .. -. -. . .. ..

Deprrrlnzent of Econonrics, Universily qf Nigerin Nsirkkn 19 of 108

M S c I~isser~tatiot~: Glol~ulised Fiwuncinl,flows. Cnpitcrl~~~rrrliet deepenirzg, and Lconomic Growth: Nigeriur~ hperierzce ~ - ~ " ~ .- ~ ~

are available in the client's accounts. The introduction of the ATS made it possible to

transit from the old system of transacting business in the capital market which i s

t manual (the call over system), to a new system of transacting business which i s

electronic (Nigeriabusinessinformation.com, 2001; NSE, 2006). The electronic system

of transaction made possible by the ATS made it possible for SEC to approve the e-

bonus system in 2004 to replace the issuance of physical certificates for scrip issues

(NSE, 2006, Uzor, 2007).

Introduction of t+3 transaction circle

The establishment of the CSCS made possible the introduction of T+5 on the lSt

March, 2000. T+5 means transaction day plus 5 working days. This was the initial

transaction cycle when the Nigerian Stock Exchange launched the CSCS Limited

(Central securities Clearing System). This has been reduced to 4 days with the

introduction of the T+3 (i.e. Transaction day plus 3 working days). With the estab- *

lishment and introduction of CSCS and T+3 respectively, NSE (2006) notes that the

following benefits stand to be reaped.

1. Reduced settlement cycle; increased liquidity and reduced risk

2. Efficiency i s increased by eliminating errors, and lowering costs

3. The automated system i s able to handle surges in demand

4. Reduction of risk through shortened transaction circle that eliminates

errorslfrauds which could occur as a result of long processing time.

5. Centralization of depository functions, reduces costs and increases effi-

ciency

6. Information can be retrieved and verified at a faster pace

lnvestprs can take advantage of capital appreciation because of the T+3 or same day

settlement cycle.

Introduction of the Trade-Alert Systems

The trade alert i s an automated stockholder alert system that notifies an investor of

transactions in his stocks-usually through a GSM mobiles phone. I t was introduced on

March 24, 2005 (NSE, 2006). The NSE noted that the introduction of the Trade Alert

Systems has brought about the following benefits. !

1) Empowers Investors with a tool for independent monitoring of their in- -

Depnrtnzent of Emnomics, University of Nigeria Nsukka 20 of 108

AlSc Drrset-tczt~on Glolmll~rd Flnancralflows, Capital nzarLet deepen~ng, and Econonzrc Growth A1~grt.run bxpcwence - --- - - -. - - - -- - - - - - . . - --- - - - -

vestment accounts at the CSCS

2) Eliminates chances of unauthorized transactions in investors' account

3) Reports of stock market activities- Notices of AGMs, quarterly financial

highlights of quoted companies, weekly price movement of stocks, etc.

4) Enhances trading in e-IPOs (electronic initial public offers), e-pos (elec-

tronic public offers) and e-bonus (electronic bonus shares).

5) Improved investors' confidence in the market.

The Big Banking Bang:

A very critical event in the growth process of the capital market happened in

2004/2005. This was as a result of the Banking sector Consolidation exercise. During

this exercise the banks pumped in billions of equities into the capital market. This

created investment opportunities in the capital market. The inflow of new money

from both foreign and domestic investors within the period of banking consolidation

improved the ranking of the Nigeria Capital market as the fastest growins equities

market (Uzor, 2006).

Re-entry of government bonds:

In the 1 9 8 0 ~ ~ issuance of long dated government instruments was suspended. These

long term instruments were re-introduced, and this made the capital market to be

deeper and broader in its range of products.

Support as a Result of Monetary Policy Spill Over

In recent times monetary Policy has achieved a great deal of stability. Monetary

authority's low interest rate policy and the accompanying stability in the liquidity of

the economy resulted in large flows of funds to the capital market as investors move

from money market to capital market.

The return of flight capital

The use of two major regulatory tools has brought about increased the retentive

ability of the capital market in terms of capital flow. For the first time, the economy

in about three decades i s retaining an increased proportion of Nigerian originated

M.Sc Disseriation: Globalised Financiuljlows, Capital nzcrrlcet deepening and Economic Growth: h'igerinn Experience ~ ~ .. ... . .-- ."

financial capital. The first of the policy tools has to do with government effort

against money laundering, which has recorded an appreciable success in stemming

capital flight (Okereke, 2005; and Uzor, 2007).

The second policy tool i s the high level of exchange rate stability achieved over the

past two years. That has closed the opportunity to profit from holding dollar denomi-

nated assets and reconverting to the naira later at depreciated exchange rate. The

developments have added to the stability of financial markets and made available

large sums of capital for investment in the stock market (Uzor, 2007).

This i s a big victory for the Nigerian economy, which i s happening at a time of

sustained rapid economic growth. Government revenue has been a t an exceptionally

high level in the past several years and reasonable stimulatory spending has happened

to raise the level of business activity generally.

A new strength from pension reform

The introduction of a new pension scheme has created a strong flow of investment

capital from retires to the capital market. Retirees leaving the public sector are for

the first time in Nigerian history able to get their retirement benefits within a

reasonable time. The number of such people has increases over the past two years, as

the government privatization machinery gained speed.

The pension reform itself created a new window in capital market operation for

pension funds managers. An estimated 10 million employees are expected to register

with the National Pension Commission [PENCOM] for retirement accounts. This has

- created a huge market for pension funds administrators [PFAs] key actor in a stock

market that have since been virtually absent in the Nigerian market.

Definitely, the presence the PFAs wi l l boost the availability of longer-term invest- *

ment capital in the market and positively impact on institutional investing and

trading in securities. According to Stock Market Guide (2007) an estimated 44300

billion contributed by the public and private sectors are estimated to be currently

under the management of PFAs.

Contributions are estimated at N8-10 billion monthly. Nigeria hasn't had such a long-

term stable fund for a long time. The inflow of huge funds for investment i s clearly

tasking the capital market i n terms of absorptive capacity. The market i s yet to

develop the depth and investment options needed in response to the demand for

D~pcrrtnrer~t of Lcononlio, Utliver~ity of Nigerici N\ukkrr 22 of 108

A1 Sc D I Y S ~ T I L I ~ I O N Globrrl~\ed F117nnc1rrl /lows, C'npltnl ~nurltet deepen~ng, and Economic Growth Vrgermn Expwrence . . - - - - - - - - - - - - - -".-- financial assets under the pension reform. How much of pension funds the capital

market can attract depends on how fast it can create the needed investment charac-

teristics (Stock Market Guide, 2007; and Uzor, 2007).

Investments and securities Act No. 45, of 1999fd

In 1999, the law with which the apex regulatory body in the capital market would

operate was enacted. The law - Act No. 45 of 1999 clearly stipulated the functions

and powers of the Securities and Exchange Commission (Aigbekaen, 2007). Laws are

listed below.

To regulate investment and securities business in Nigeria.

To register and regulate securities exchange, capital trade points futures, op-

tions and derivatives exchange, commodity exchanges and any other recog-

nized investment exchange.

To register securities to be offered for subscription or sale to the public.

To render assistance in all aspects including funding as may be deemed neces-

sary to promote an investor wishing to establish securities exchanse and capi-

tal trade points.

To prepare adequate guidelines and organize training programmes and dis-

seminate information necessary for the establishment of securities exchange

and capital trade points.

To register and regulate corporate and individual capital operators as defined

in section 30 of the Act.

To register and regulate the working of ventures capital funds and collective

investment scheme including mutual funds.

To facilitate the linking of al l markets in securities through modern communi-

cation and data processing facilities in order to foster efficiency, enhance

competition and increase the information available to brokers and investors.

To act in the public interest having regard to the protection of investors and

the maintenance of fair and orderly markets and to this end establish a na-

tionwide trust scheme to compensate investors whose losses are not covered

under the investors protection funds administered by securities exchanges and

. capital trade points.

A 1 Sc D~ssr i~i~tron Globulrsed Ftnirnocll flows, Cap~lal ~izrrrlwt cJ(v,uenrng, and Econonrrc Groii,tll Nrget'rrczn Expet rence . . - - -- - -- -- - - - - - - . - . ?. - .- - - - -

TO keep and maintain separate registers of foreign direct investment and for-

eign portfolio investments. ).

To register and regulate central depository companies and clearing and set-

tlement companies, custodians of securities, credit rating agencies and such

other agencies and intermediaries.

To protect the integrity of the securities market against abuses from the prac-

tices of insider trading.

To act as a regulatory apex organization for Nigeria capital market including

the promotion and registration of self regulatory organizations and capital

market trade associations in which it may delegate it's powers.

To review, approve and regulate mergers, acquisition and all forms of business

combination.

To promote investors education and the training of al l categories intermediar-

ies in the securities industry.

To call for information from an undertake inspection conduct inquiries and

audits of the security exchange unit trusts, mutual funds, capital trade points,

futures, options and derivatives exchanges as well as other intermediaries and

self-regulatory organization in the securities industry.

To call for and furnish to any agency such information discharge of i t s func-

tions.

To levy fees or other charges on any person for carrying out investment and

securities business in Nigeria.

To conduct research into al l or any aspect of the securities industry. b

To prevent fraudulent and unfair traded practices relating to securities indus-

try.

To advice the minister on all matters relating to securities industry.

To disqualify unfit individuals from being employed anywhere in the securities

industry.

To liaise effectively with the regulators and supervisors of other financial insti-

tutions locally and over seas and

- - . - . .

Department of l:'cononrics, lJniversi()~ of Nigeria N t r ~ k h ~ 24 of 108

h./Sc D1wr~tar1o17 Glohtrlr~ed F ~ t i o n c ~ ~ l jlniss Coprtrrl nzarltrt deepening, and Ecanonzrc Growth Nlgerlan Experrence - . - -- - - - - --- - - - - . - - - To perform such other functions and exercise such other powers not inconsis-

tent with the decree as are necessary or expedient for giving full effect to the

provisions of this decree.

M S c Dissertation: Glohnlised I;inancial,flows, Cupital market deepening, and Econon7ic Growth: Nigeritrn Experience --- --- -.. . ... .- . -- -. -. - ..~ - . -. . -. - . . . . - - .- .. .- - -- -. -. . - ... ~ ~ . .~

2.5 Empirical Literature

Empirical findings are as divergent as theoretical views on the growth -- finance

nexus. Many researches come out with different views. Essentially, the discussion

focuses on the link between different aspects of financial development and growth.

For instance, focus could be on different measures of financial intermediately

improvements and growth, or between any of: credit to private sector; different

measures of money supply; and, or the different forms of capital market develop-

ment (Schmuckler, 2003; De - Gregorio, 1998; Ndebbio, 2004). In the context that

capital flows, arising from financial globalisation and integration contribute to

financial development, views are currently being expressed regarding growth and the

various forms of ~lobalised financial flows.

De Gregorio (1998) contributing to the debate in his work on the relationship between

international financial integration and economic growth opines that most recent

literature on the theme emphasize the role of financial deepening on economic

growth, while neglecting the role of international financial integration in

promoting a deep domestic financial market and through that channel fostering

economic growth. Financial integration also permits portfolio diversification,

allowing higher profitability on investment and, hence higher rate of economic

growth. Other empirical findings exist and discussed below:

Schmuckler (2003) i n his work - Financial globalization: Gain and Pain for Develop-

ing Countries - discusses the benefits and risks that financial globalization entails for

developing countries. He opines that financial globalization can lead to large bene-

. fits, particularly to the development of the financial system. But financial globaliza-

tion can also come with crises and contagion. The net effect of financial globalization

is likely positive in the long run, with risks being more prevalent right after countries

liberalize.,So far, only some countries, sectors, and firms, have taken advantage of

globalization. As financial systems turn global, governments lose policy instruments,

so there i s an increasing scope for some form of international financial policy coop-

eration.

Issing, (2000), in his study on "the globalization of financial markets" posits that

globalization i s a process which is not yet finalized and wi l l lead to a world in which

countries and economic areas become more and more interdependent. In some

quarters, the unfolding of the process of globalization has given rise to the view that

central banks are becoming increasingly "powerless". ... the challenges posed to - --

Drprrrtnzent of Ecorlontic\, L'niverri[)l of Nigerin N w h k o 26 of 108