global value chains – a panacea for development?

TRANSCRIPT

Institute for International Political Economy Berlin

Global Value Chains – a Panacea for Development?

Author: Petra Dünhaupt & Hansjörg Herr

Working Paper, No. 165/2021

Editors: Sigrid Betzelt, Eckhard Hein (lead editor), Martina Metzger, Martina Sproll, Christina Teipen, Markus Wissen, Jennifer Pédussel Wu, Reingard Zimmer

Global Value Chains – a Panacea for Development?

Petra Dünhaupt & Hansjörg Herr•

Berlin School of Economics and Law, Institute for International Political Economy (IPE)

Abstract:

In the last decades in particular, national governments as well as development agencies and international organizations have increasingly turned to participation in global value chains (GVCs) as a development strategy. However, whether the positive development effects of integration are large enough to warrant trade liberalization cannot be answered in a straightforward manner. In this article, we show how development recommendations by international institutions and Western governments have changed since World War II and now ultimately recommend integration into GVCs.

Deregulation and liberalization of international trade and capital flows have fueled two opposing trends, which also affect GVCs: on the one hand, there is increasing concentration at the corporate level. On the other hand, globalization has resulted in more countries participating in international trade including via industrial production. Both developments have led to multinationals being able to expand their rent-seeking opportunities while also reducing production costs, especially for simple manufactured goods. Today, it is no longer sufficient for a country to industrialize in order to catch up with the rest of the world, as the prices for industrial goods and quality of productions have fallen tremendously in some cases, at least in comparison to developed countries. Integration into GVCs seems to provide only minimal macroeconomic benefits beyond the positive effects for individual companies and sectors. Industrial policy therefore seems indispensable for catch-up development.

JEL Classification Code: B27, F13, F63

Keywords: Global Value Chains, economic development, industrial policy, export market share concentration, import price development

Contact: [email protected]

• A revised version will be published in Teipen, C., Dünhaupt, P., Herr, H. and Mehl, F. (Eds.), Economic and Social Upgrading in Global Value Chains: Comparative Analyses, Macroeconomic Effects, the Role of Institutions and Strategies for the Global South, Palgrave. Forthcoming. For helpful comments and suggestions, we would like to thank Clare Hollins, Fabian Mehl and Christina Teipen.

1

1 Introduction

Development policy discourse has changed tremendously in recent decades, as have

economic policy recommendations in general. The spectrum ranges from a policy of import

substitution in the 1950s to radical market liberalization in the 1980s and 1990s. Whereas in

the post-World War II era developing countries relied heavily on industrial policy to achieve

post-colonial independence and also social development, the mere word and especially the

strategy of industrial policy was frowned upon by the 1980s (Andreoni and Chang 2019).

Ironically, developed countries have always practiced far-reaching industrial policy in areas

allowed by international treatises1. The financial and economic crisis of 2008-09 then opened

the way for a comeback of industrial policy (Chang and Andreoni 2016). The rapid

development of China, which has become a serious competitor to the U.S. and Europe in many

sectors and has made massive use of industrial policy for catching up, certainly also plays a

role for the renewed interest in industrial policy in the Global North.

During the last decades in particular, national governments as well as development agencies

and international organizations have increasingly turned to participation in global value chains

(GVCs) as a development strategy (Gereffi 2013; Werner et al. 2014).2 What makes this

concept so appealing is the oft-mentioned argument that, compared to the past, an entire

industry does not have to be built up; rather, countries can specialize in the production of

individual tasks or assembly activities in order to integrate themselves into international trade

(Baldwin 2011). These tasks can be simple from the perspective of the needed qualification of

the workforce and can be produced in big quantities for one or more companies in subsidiaries

of multinational enterprises (MNEs) or legally independent subcontractors. This allows the

MNEs at the top of the value chain, also known as ‘lead firms’, to exploit economies of scale

and cut costs in addition to benefiting from the low wages and in many cases low ecological

and social standards found in the Global South.

The World Bank enthuses about GVCs, including in its World Development Report 2020.

Among other things, GVCs are credited with enabling “an unprecedented convergence: poor

countries grew faster and began to catch up with richer countries. Poverty fell sharply” (World

1 For the case of Germany, refer to Dünhaupt and Herr (2020a and 2020b). 2 When we speak about integration of countries in the Global South in GVCs we speak of vertical value chains which are driven by cost advantages of countries in the Global South and not specific knowledge and capabilities of suppliers which can also be a motivation of lead firms which organize GVCs to outsource. Also, when we speak of Global South and Global North this is not a strictly geographical concept. Countries in the Global South can in certain industries have own lead firms which outsource to other countries. China is here the showcase.

2

Bank 2020, p. 1). The World Bank also attributes many other positive effects to GVCs, and

therefore recommends trade liberalization, not only for manufactured goods, but also for

services and agriculture.

Other authors, such as Rodrik (2018, p. 14), are less optimistic about the role of GVCs as a

development panacea, since:

“The affected sectors and activities remain a very small part of the domestic economy. New capabilities and productive employment remain limited to a tiny sliver of globally integrated firms.”

Hence, the question that arises is: are the development effects of integration into GVCs large

enough to warrant trade liberalization, as recommended by the World Bank? Or should

countries – as Rodrik (2018) recommends – rather focus on domestic integration and thus

concentrate on domestic-oriented industrialization?

In order to answer this question, this article is structured as follows: in the second part, we

show how development policy recommendations and strategies have changed since World

War II, and now favor integration into GVCs. In the third part, we move away from a firm focus

and examine whether countries have succeeded in industrializing and how increased global

competition affects terms of trade. In the fourth part, we examine whether there is a

relationship between participation in GVCs and macroeconomic indicators. The last part

concludes.

2 Shifting development strategies – from import substitution to export orientation to

global value chains

Import substitution development strategy

With the end of colonial rule after World War II and the striking disparities in income and

development between the Global North and Global South, many developing countries began

to practice one or another variant of import substitution policies. Latin American countries

were at the center of this development strategy. The main goal was to transform the structure

of the economy away from a backward (agrarian) economy and dependence on the export of

mineral resources towards an industry capable of producing industrial goods. The

development strategy popular after World War II assumed that unregulated markets will not

lead to catching up, as it was widely believed that “the market was an instrument that kept

poor countries poor and rich countries rich” (Bruton 1998, p. 905). Three strands of thinking

were decisive in this development strategy (see for details Bruton 1998).

3

First, based on Prebisch (1950) and Singer’s (1949) research, it was found that during the

decades before the 1940s the terms of trade for developing countries showed a secular

decline. The widely accepted explanation was that high productivity increases in the Global

North’s manufacturing sector did not lead to falling prices for manufactured goods, as the

monopoly power of firms and strong trade unions kept wages and profits, and thus prices,

high. In other words, the expected mechanism – that high productivity increases in countries’

export sector leads to falling prices and falling terms of trade – would not work. At the same

time, developing countries experienced low productivity increases in their export sectors,

mainly agriculture and minerals, while surplus labor from the big traditional subsistence sector

and weak trade unions also kept wages very low (Lewis 1954). Further, it was believed that

the income elasticity of demand for agricultural and mineral products was lower than for

manufactured goods. The expected consequence was that developing countries would run

current account deficits. As the efficiency of exchange rate adjustments were doubted from

this effect, low growth in developing countries was expected. The solution was seen in

building up an own manufacturing sector, by violating the market mechanism in order to

support the domestic manufacturing sector and its protection via tariffs and quotas, especially

in the field of durable consumption goods import.

Second, capital formation was understood to be particularly important as the source of

increasing productivity and thus as a trigger for growth. It was assumed that technology

embodied in capital goods could simply be imported and applied as it was in the country of

origin (Shapiro 2007). Export growth or even current account surpluses for the stimulation of

demand and output were not part of the import substitution strategy. Lack of domestic saving

and thus inadequate capital formation was seen as the problem. Foreign aid was therefore

welcomed as an instrument to stimulate domestic capital formation, and was very much

pushed by the World Bank in the 1960s (for a critique of the savings-gap approach, see

Easterly 1999). Of course, the huge private capital inflows and current account deficits that

would later emerge from the 1970s onwards in some of the countries in the Global South

could not be imagined at that time.

Third, there was the idea of replicating the Global North. Instead of continuing to import

manufactured goods and export primary commodities, countries should industrialize

themselves. Inspired by Lewis (1954), there was the belief that one day, by promoting a

modern capitalist sector with high growth, the latter would be able to absorb the surplus labor

4

from the subsistence sector, which would one day disappear and be replaced by the capitalist

sector3.

Although none of the countries practicing import substitution industrialization has ever

reached a stage of full convergence where a modern productive capitalist sector replaced the

traditional backward sector, some countries were able to achieve remarkable productivity and

growth rates until the 1970s. This together with social policies allowed countries to increase

life expectancy, decrease child mortality, and achieve other positive social effects (Bruton

1989). However, in 1979 the U.S. implemented very restrictive monetary policy to combat

inflation, triggering a severe worldwide recession. As a result, most countries in Latin America,

after deregulation of international capital flows and only one decade of high private capital

inflows, experienced deep balance of payments crises; the debt crisis of the 1980s was then

the final nail in the coffin of the strategy of import substitution industrialization (Shapiro

2007).

By contrast, East Asian countries pursued a dual strategy after World War II, since they not

only supported domestic industrialization via import substitution policies and comprehensive

industrial policy, but also massively promoted exports starting with simple manufactured

goods. Export promotion in these countries, and in many cases export surpluses, not only

stimulated domestic demand; rather, the export successes of sectors and companies also

became a criterium for successful industrial policy and government support. East Asian

countries supported the internationally competitive and, in many cases, newly created

industries whereas Latin America in many cases did the opposite (Stiglitz 1996). Based on their

low wages, East Asian countries also benefited from a new trend already starting in the late

1960s, when major retailers and brand-name manufacturers in the U.S. and Europe began

withdrawing from own production and sourcing from independent manufacturing suppliers

in overseas developing countries (Milberg et al. 2014).

The 1980s and the paradigm shift to export-oriented industrialization

Before we discuss the paradigm shift to export-oriented industrialization, let us look more

closely at how trade and foreign direct investment (FDI) developed from 1970 to 2019. From

the 1970s onwards, international trade in percent of GDP substantially increased worldwide.

3 According to Lewis (1954), workers from the subsistence sector come from diverse backgrounds, which include subsistence agriculture, casual labor, petty trade, domestic services, but also women in households. The capitalist sector is characterized among other things by profit-oriented firms with employees, an organized market for labor, capital and credit and the accumulation of reproducible capital goods.

5

Figure 1 shows the importance of goods exports as a share of GDP for various world regions

for these years. There was a first wave of increasing trade integration in the 1970s and a

second much stronger wave during the decade before the financial crisis of 2008-09 and the

subsequent Great Recession. Then there was a general break in the trend, with trade no longer

increasing faster than GDP. Exports-to-GDP ratios even dropped substantially in Africa and

Asia, indicating the poor economic development of the former and the intensifying trade war

between the U.S. and China in the latter. Latin American development during this period

reflects the “lost decade” of the 1980s, with massive opening up of trade following their

departure from import substitution strategies. From the mid-1990s until the Great Recession,

their export-to-GDP shares again increased sharply. North America had relatively low export

shares, mainly because of the U.S.’s size, whereas Europe had a high share because of the

many relatively small countries and the market result that, as a rule, small countries tend to

be deeper integrated into international trade than big countries. But also, for these regions

stagnating or falling export-to-GDP ratios can be observed. For the world as a whole between

1990 and 2008, real GDP expanded at an annual rate of 3.2 percent, while world trade volume

increased at an annual rate of 6 percent. After 2008 world trade did not grow faster that world

GDP (Davies 2013). Two reasons seem to be important to explain this break in international

trade dynamics. First, many countries gave up aggressive export-led growth strategies (see

below); second, since the financial crisis more and more protectionist tendencies and

especially a trade war between the U.S. and China developed.4

4 Global Trade Alert (2021) reports that after 2008, a sharp increase of worldwide government interventions which have negative economic consequences for other countries can be observed – a total of 21170 interventions between 2008 and 2021, from annually 1477 in 2009 to 2550 in 2020.

6

Figure 1: Goods exports in percent of GDP, various world regions, 1970-2019

Source: UNCTAD Statistics

To secure access to raw materials, companies from the Global North have already maintained

enterprises around the world since the 19th century. By the mid-20th century, it was the policy

of import substitution, accompanied by high import tariffs and import quotas, that led to

industrial manufacturing MNEs establishing production facilities in all parts of the world

through FDI, thereby controlling the entire production process (Milberg et al. 2014). However,

FDI flows in the 1950s and 1960s were small. Figure 2 displays FDI inflows in percent of GDP

for various world regions for the years 1970 until 2019. It shows that even until the early

1990s, FDI inflows as a share of GDP were relatively small in all world regions, at less than 1

percent of GDP. However, the liberalization and deregulation of international capital flows

gaining speed in the 1980s and step-for-step for most countries in the Global South by the

1990s led to a massive increase in the level of FDI inflows. It also becomes apparent that FDI

flows are very volatile and pro-cyclical, increasing in boom periods and shrinking during global

downturns. The enormous spikes shown in the figure can be explained by mergers and

acquisitions (M&As) rather than by greenfield investment5. Volatility and level of FDI flows

also remained high after the 2008-09 financial crisis.

5 The hostile takeover of Mannesmann by Vodafone in 2000, for example, is – at 180 billion euros – still considered the most expensive takeover of all times (Spinnler 2020).

0

5

10

15

20

25

30

35

40

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Africa Asia Europe Latin America North Amercia

7

Figure 2: Foreign direct investment inflows in percent of GDP, various world regions, 1970-2019

Source: UNCTAD Statistics

The paradigm of export-oriented industrialization prevailed in the late 1970s and in the 1980s,

many developing countries shifted strategy away from import substitution policies. Successful

Asian countries (first Japan, and then especially the ‘Asian Tigers’ Hong Kong, Singapore, South

Korea and Taiwan) utilized export-oriented development policy from the beginning for their

very effective catching-up strategy. But these countries also combined export orientation with

import substitution and massive industrial policy, supporting own national champions,

establishing completely new industries and developing new comparative advantages with the

aim of increasing domestic value creation and international competitiveness (Wade 2003).

The new export orientation thus followed a different philosophy. It was understood that

existing comparative advantages should be used and supported by foreign capital. To develop

national champions and new comparative advantages in the framework, comprehensive, but

also industry-specific, industrial policy disappeared. Politically this rethinking took place

together with the victory of neoliberalism (Gereffi 2013), which started with the election of

Margaret Thatcher (1979) in Great Britain and Ronald Reagan (1980) in the U.S. International

organizations embraced the idea of the Washington Consensus, which stressed privatization,

deregulation and liberalization of markets as well as the important role of FDI for development

(Williamson 1989). Due to the debt crisis of the 1980s, many developing countries, especially

-1

0

1

2

3

4

5

6

7

8

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Africa Asia Europe Latin Amercia and the Caribbean Northern America

8

in Latin America (and after the Asian crisis in 1997 also a number of Asian countries) had to

turn to the International Monetary Fund (IMF) and the World Bank. Both institutions began

linking the provision of help in form of loans to the implementation of structural adjustment

programs. These programs included the liberalization of trade, financial markets, the opening

for FDI, as well as cuts in public spending (Chang 2006; Summers and Pritchett 1993; Herr and

Priewe 2005).

The benefits of economic openness and the new export strategy were underpinned by three

strands of argument (Palley 2011). The first line of argument relates to the Heckscher-Ohlin

theory of comparative advantage, which states that countries with the same technological

knowledge, but different factor endowments can benefit from free trade, if they concentrate

on the production of the good which uses their abundant factor extensively. Compared to the

approach of David Ricardo, who stressed the importance of different technical and

educational development stages as the basis of comparative advantages, the reliance on this

theory is revealing. By using Heckscher-Ohlin the main problem of development, i.e., reaching

the technological and skill-level of advanced countries, is excluded by definition. The second

line of argument relates to the problem of rent-seeking by companies in the Global South,

which was closely associated with the strategy of import substitution and import licenses and

thus protection from foreign competition, and which could be wiped out by free trade

(Krueger 1974). Rent-seeking by companies in the Global North via technological leadership

and patent law was (again, revealingly) not a point in the debate. A third line of argument

pointed to a positive link between free trade and economic growth. In the neoclassical

paradigm any increase in efficiency as a result of better supply conditions leads to higher

growth. The demand side of economic growth and development becomes completely

neglected in this framework. In addition, in an influential paper in the early 1990s, Grossmann

and Helpman (1991) argued that integration in global trade would lead to productivity growth

through technology diffusion and knowledge spillovers. Empirically, advocates of export-

oriented industrialization seemed to be proven right by the success of the East Asian Tiger

countries. But these countries, as mentioned, not only relied on export-driven growth, but

also made massive use of industrial policy instruments, which has often been overlooked in

the debate (Amsden 1989; Stiglitz 1996; Chang 2003).

9

The 1990s and the acceleration of trade fragmentation in the form of GVCs

While companies and retailers initially outsourced entire production operations, by the early

1990s trade started to become increasingly fragmented. Instead of trading only finished

products, trade in components and intermediate products increased significantly. It was also

no longer just simple goods such as clothing and toys that were outsourced to countries in the

Global South, as it had been in the beginning. The range of industries involved increased and

simple tasks for high-tech goods, for example in the production of mobile phones, as well as

services were targeted by outsourcing activities (Gereffi 2013). The trend was spurred by two

further developments: innovation in transportation and information technology, leading to a

sharp drop in these costs, as well as international trade and capital flow liberalization,

including the creation of the World Trade Organization (WTO) in 1994. Today, the majority of

global trade - estimates vary between 50 and 65 percent - takes place through GVCs (Dollar

2019; World Bank 2020).

GVCs vary from industry to industry. The GVC literature has put the spotlight on firm

relationships - between the so-called lead companies, in most cases MNEs, that establish

governance relationships6 with foreign suppliers (Dallas 2014). A lead company usually has a

lot of power vis-à-vis suppliers. It decides which companies get access to a GVC in the first

place and it also massively influences suppliers’ chances for ‘economic upgrading’, which

refers to the ability to either realize more value added within one’s own chain - be it through

process, product or even functional upgrading - or even move to a new industry where more

added value can be achieved (Humphrey and Schmitz 2002).

Since the late 1990s, GVCs have also started to play a role in development policies via

international organizations and foreign donors’ national development agencies. GVC

participation was considered an important element of national development strategies, but

the main aspects of GVCs that were adopted are very market-friendly and focus on the export

sector. It was hoped that GVCs would not only create market access for firms in global markets

and support upgrading (Staritz 2012), but also that GVCs would, starting from the microlevel,

transform whole industries and countries (Dallas 2014). This idea is also stressed by Gereffi et

al. (2005, p. 79):

6 The governance in GVCs represents the “authority and power relationships that determine how financial, material, and human resources are allocated and flow within a chain” (Gereffi 1994, p. 97).

10

“The evolution of global-scale industrial organization affects not only the fortunes of firms and the structure of industries, but also how and why countries advance – or fail to advance – in the global economy.”

Macroeconomic effects have been studied only more recently (Carballa Smichowski et al.

2020), whereas if the focus is only on individual firms and sectors, conclusions for

macroeconomic developments are not possible. Baldwin (2011) argues that while

industrialization became easier in times of GVCs, because countries only have to join a supply

chain instead of building a whole industry, it also became less meaningful. Gereffi (2013, p.

10), not only stressing the positive effects of GVCs, argues in the same direction and points

out that export-oriented industrialization (EOI) is no guarantee for successful development:

“If countries are only engaged in the simplest forms of EOI, such as assembling imported parts for overseas markets in export-processing zones, then they would develop neither the institutions, nor the know-how, nor the consumer markets needed to create and sustain entire industries.”

It is, of course, possible that individual firms that manufacture for export will become more

productive. However, whether these firms or sectors will remain isolated and create "enclave

industrialization" without many positive spillovers to the rest the economy remains an open

question.

3 Economic development related to GVCs

In this section we will discuss macroeconomic effects of GVCs further. First, the question is

asked whether GVCs led to industrialization in the Global South. Second, development of

market concentration and connected with this the possibilities of rent-seeking are analyzed.

Third, it is shown how terms of trade for different product categories developed.

Global value chains and industrialization

At first glance, developing countries seem to have succeeded in industrializing, integrating

into the international distribution of labor in the manufacturing sector, and also in breaking

away from the sole dependence on primary goods exports. The aim of the import substitution

period, i.e. industrialization, seems to have been – at least to a large extent – realized after

the 1990s. In 1995, one quarter of all exported manufactured goods originated in developing

countries (Figure 3). In 2019, developing countries’ share of world exports of manufactured

goods even amounted to 45 percent. However, what also becomes apparent from the figure

is the fact that this tremendous increase is mainly attributable to China – “the world’s factory”.

Excluding China, the increase was far less impressive. Developing countries’ share still

11

accounted for approximately 27 percent of all manufacturing goods exports in 2019, and

hence was almost the same as in 1995.

Figure 3: Developing countries' share of world exports of manufactured goods, 1995-2019

Source: UNCTADSTAT (2021)

Note: Manufactured goods (Standard International Trade Classification (SITC) 5 to 8 less 667 and 68)

Table 1 gives a more detailed picture of the development and importance of the

manufacturing sector for economies in different world regions. At the world level,

manufacturing value added (MVA) as a share of domestic GDP almost did not change and

increased only slightly from 17 percent in 1970 to 18 percent in 2013. However, the

development differs in the various parts of the world. In the U.S., the share of MVA as a

percent of GDP was 13 percent in 1970, and remained almost the same in 2013. In the same

period, the share of MVA in GDP deceased in Western Europe from 22 percent in 1970 to 18

percent in 2013, in Latin America and the Caribbean from 20 percent to 16 percent and in Sub-

Saharan Africa from 14 percent to 11 percent. In Asia without China, the MVA shares increased

from 16 percent in 1970 to 20 percent in 2013. Only China experienced a tremendous increase

from 9 percent in 1970 to 36 percent in 2013 (Rodrik 2015). Rodrik also shows that in 2013,

the U.S. had a share of world MVA of 19 percent, Western Europe 13 percent, Latin America

and the Caribbean 6 percent, Sub-Saharan Africa 1 percent, China 18 percent and the rest of

Asia 26 percent. Hence, Africa never managed to industrialize to any relevant extent; indeed

0

5

10

15

20

25

30

35

40

45

50

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Developing countries Developing countries without China

12

in Latin America and the Caribbean, as well as in Africa, there was even deindustrialization.

Only Asian countries managed to industrialize to a relevant extent and the U.S., in contrast to

widespread perception, actually remained relatively industrialized. Also, the countries not

covered by the groups mentioned in Table 1, mainly countries of the former Soviet Union,

deindustrialized substantially and in 2013 only realized a share of world MVA of 17 percent.

This means the concerns of economists like Prebisch and Singer, that developing countries

would not be able to industrialize to levels comparable with developed countries for many

parts in the world, could not be removed.

Table 1: Manufacturing Value Added (MVA) in percent of domestic GDP; various world regions, 1970-2013

WORLD UNITED

STATES

WESTERN

EUROPE

LATIN

AMERICA

AND

CARIBBEAN

ASIA

(WITHOUT

CHINA)

CHINA SUB-

SAHARAN

AFRICA

1970 17 13 22 20 16 9 14 1980 16 12 20 20 16 16 15 1990 16 12 19 19 19 18 15 2000 17 13 18 19 19 29 13 2010 28 13 18 17 21 36 11 2013 18 13 18 16 20 36 11

Source: Rodrik (2015)

There appear to be major regional differences in how countries in different regions of the

world are integrated into GVCs: according to the World Bank (2020), countries in East Asia,

North America, and Western Europe produce sophisticated industrial goods and services, and

are integrated into complex GVCs with their innovative activities, while countries in Africa,

Latin America, and Central Asia specialize mainly in extracting commodities, and some in

limited manufacturing. This distribution is reminiscent of the “smile curve”, the image that is

frequently used when describing who takes on which tasks within a value chain, and which

shows that the tasks with high value-added take place in the Global North, while tasks with

low value-added are outsourced to the Global South.

Figure 2 shows that FDI inflows to the Global South, especially Africa and Latin America,

increased in the 1990s – pushed by the Washington Consensus which stressed opening up for

FDI inflows as a key development policy. Yet despite high FDI inflows, successful

industrialization did not take place. To understand this, it should be made clear that not all

FDI adds to industrialization in the host country. High FDI inflows should not be mixed up with

high gross capital formation. In case of M&As there may be only a change in ownership not

13

leading to new investment in machines or new technologies. Also, FDI can crowd out relatively

high value adding domestic investment. So while FDI inflow to Latin America was high in the

1990s, gross capital formation was low or stagnated (Akyüz 2017, p. 178ff.). Last but not least

the structure of FDI inflows plays a role. There is evidence that FDI inflows in the

manufacturing sector has higher effects on productivity development than FDI inflows in the

real estate sector, the financial sector, the retail sector or the service sector in general. In

addition, investment in the service sector is less export-oriented (Alfaro and Charlton 2007;

Mencinger 2003; Peărić et al. 2021). This is highly plausible. FDI in the real estate sector is

often speculative and increases asset bubbles with negative effects for long-term economic

development. FDI in the retail sector can lead to a stimulation of imports as big retail

companies source worldwide rather than locally. Moreover, the dominance of foreign

financial institutions in domestic markets does not stimulate domestic credit expansions as

foreign financial institutions lack the necessary knowledge of the domestic market or may shy

away from risk and tend to channel domestic monetary wealth to financial markets they know

in developed countries (Stiglitz and Greenwald 2003).

Between 2010 and 2019 the value of worldwide annually announced greenfield FDI fluctuated

around USD 800 billion. The net value of annually announced net cross-border M&As from

2010 to 2014 was around USD 400 billion, jumped to around USD 800 billion, and dropped in

2019 to USD 500 (UNCTAD 2020, p.16). As these data show, a substantial portion of FDI flows

are minimally beneficial M&As. From the greenfield investments, the average of the years

2018 and 2019 went first of all USD 445 billion to the service sector, followed by the

manufacturing sector with USD 435 billion and the primary sector with USD 33 billion. Among

the top 10 industries for greenfield investment in 2018 and 2019 were construction,

accommodation and food service activities, information and communication, or financial and

insurance activities, sectors which are not in the centre of manufacturing (UNCTAD 2020, p.

16).7

Concentration trends in selling markets of lead companies

Rent-seeking capacities of lead firms in GVCs depend, beside monopsony constellations on

their supply side, on the market constellation in the markets they sell their products. In case

7 The other sectors were electricity, gas, steam and air-conditioning supply, coke and refined petroleum products, motor vehicles and other transport equipment, computer, electronic, optical products and electrical equipment, chemicals and chemical products and transportation and storage.

14

of a monopoly position in a big market the power of a lead company for rent-seeking is the

highest. In case of pure and monopolistic competition the big number of firms and the easy

entry and exit of firms in the market prevents any rent-seeking. Between very competitive

markets and a monopoly there are various degrees of oligopolistic markets which can be

measured by concentration indicators.

Deregulation and liberalization of international trade and capital flows have fueled two

opposing trends, which also affect GVCs. On the one hand, there is increasing consolidation

at the corporate level. A giant takeover wave through M&As has contributed to a rise in global

market concentration. Nolan et al. (2008) demonstrate for the example of four sectors

(aerospace, automobiles, telecommunications, beverages) that not only has the degree of

concentration at the level of lead firms risen sharply, but that this effect extends throughout

the entire supplier network. The increasing monopolization trend is particularly pronounced

in the U.S. Stiglitz (2019, p. 55) reports that the number of competitors in U.S. markets has

been falling and the market share of the top two or three firms has been increasing. Between

1997 and 2012 in 75 percent of industries such concentration processes in the U.S. took place

with the effect of a concentration of profits in the most powerful companies.

Concentration processes in final consumer markets such as the U.S. does not mean that

concentration in general has increased. The liberalization of trade and capital flows and the

intensification of globalization gives grounds to expect more competition in many markets. To

determine how the global level of concentration has changed around the world, we follow

Mayer et al. (2002) and Milberg and Winkler (2013) and measure market share concentration

in world exports for several industries with a modified Herfindahl-Hirschmann Index (HHI).

While the HHI usually takes into account the number of firms in an industry, the number of

countries exporting a certain product is considered here.8 Evaluations by government

agencies are helpful for judging the index, even if they refer to the degree of concentration at

8 We calculate the modified HHI for each product by taking the sum of the squared values of the market shares of all countries that export a particular product, and by multiplying the sum by 10,000:

!!"! =$%&'"!&'#!($∗ 10,000

"

where EX represents the export of product i of country c as a share of world w exports EX of product i. The HHI ranges between 10,000/n – which would indicate that each country (n = number of countries) has the same export market share in product i’s total exports, and 10,000, meaning that only one country exports product i.

15

the firm level. In the U.S., the competition authorities consider an HHI of 2,500 already

presenting a highly concentrated market (Milberg and Winkler 2013).

Table 2 displays the development for export market share concentration for a selection of

industries, designated at the three-digit sector level using the Standard International Trade

Classification (SITC) for the years 1980, 1990, 2010 and 2018. As can be expected, the degree

of concentration of exporting countries of a good has declined over the observation period,

i.e., for 79 percent of products in all sectors, which means that a greater number of countries

are now exporting these goods. This development can be attributed to increasing trade

integration, triggered among other things by lower transport costs. The trend towards a

decline in export market share concentration runs through all sectors’ product categories,

from primary goods to low-technology manufacturing goods to high-technology

manufacturing goods. But a further development is striking: even if there was an overall

decline in the degree of concentration between 1980 and 2018, the degree of concentration

in some – mostly low-technology manufacturing sectors – intensified (again) after 1990.

Conventional wisdom suggests that when barriers to entry are low and competition

intensifies, prices tend to fall. However, prices can also fall in cases of increasing

concentration. If one country or producer can achieve high economies of scale and average

costs and prices continuously fall, other suppliers have little chance of entering the market or

are kicked out of the market, because they can no longer compete. This is what happened

after China's accession to the WTO in 2001 and China taking over the role as "world’s factory".

Let us take the case of the garment sector (compare SITC Code 842 and 844) as an example.

The global garment industry was for a long time highly regulated.9 The final liberalization of

the sector in 2005 led to significant shifts in production and a high concentration of production

in fewer countries, most notably China, where in 2018 almost 32 percent of all garments

exported worldwide were produced. Many countries could not withstand the low-cost

competition from China based on economies of scale and superior technology and were

forced out of the market. This was particularly the case in Latin America. However, the "China

effect" is not only seen in the apparel sector. In 2018, in 22 percent of all sectors, China is

responsible for more than 20 percent of all exports.

9 The famous Multi-Fiber Agreement (MFA), in force from 1974 until 1994, gave quotas for exports of garment and textiles producing countries in the Global South. It was replaced by the Agreement on Textiles and Clothing (ATC), in force until 2005, which phased out all quotas.

16

Table 2: Export-market share concentration by Standard International Trade Classification, 1980-2018*

SITC

CODE**

INDUSTRY 1980 1990 2010 2018

1 Beverages and Tobacco 111 Non-alcoholic beverages 1063 1083 644 592 112 Beverages 1756 1788 1201 1135 121 Tobacco, unmanufactured 3089 1415 887 712 2 Crude Materials, inedible, except fuels 261 Silk 3163 7131 6614 4532 262 Cotton 4843 1822 2100 2173 266 Synthetic fibers suitable for spinning 1328 910 791 793 4 Animal and Vegetable oils, fats and waxes 411 Animal oils and fats 2648 1511 786 685 5 Chemical and Related Products 541 Medicinal and pharmaceutical products 972 868 986 1057 582 Condensation, polycondensation and polyaddition products 1387 1092 654 601 6 Manufactured Goods Classified Chiefly by Material 611 Leather 813 839 827 676 625 Rubber tires 1094 836 612 625 651 Textile Yarn 796 600 718 900 652 Cotton fabrics, woven 700 597 1793 2346 633 Cork manufactures 4702 4602 3647 3436 672 Ingots and other primary forms, of iron or steel 1265 795 585 501 673 Iron and steel bars, rods, angles, shapes and sections 1035 605 519 512 7 Machinery and Transport Equipment 721 Agricultural machinery 1165 947 908 825 722 Tractors 1671 1358 873 907 736 Metal cutting machines tools 1431 1235 1098 1050 751 Office Machines 1951 1664 1651 978

752 Automatic data processing machines 1814 1117 2519 1938 761 Television receivers (Monitors and projectors) 1684 761 1156 1541 764 Telecommunication equipment 1110 1132 1358 1944 771 Electric power machinery 1028 773 991 983 773 Equipment for distributing electricity 995 698 556 583 775 Household type, electrical and non-electrical equipment 1059 972 1229 1401 781 Passenger motor cars 1702 1537 1074 870 785 Motorcycles 4179 1839 1121 1745 791 Railway vehicles & associated equipment 1065 838 966 861 792 Aircraft & associated equipment, and parts thereof 3206 2723 1850 1563 793 Ships, boats and floating structures 1375 1115 1438 912 8 Miscellaneous Manufactured Articles 831 Travel goods, handbags and similar containers 1305 1046 2470 1793 842 Outer garments, men’s and boy’ s of textile fabrics 729 497 1290 1141 844 Under garments of textile fabrics 1258 615 1218 1192 851 Footwear 1995 1110 1794 1333 873 Optical instruments and apparatus 1353 1341 746 955 894 Baby carriages, toys, games and sporting goods 958 749 1823 1876

*Value of 10,000 is the highest value in case only one country is exporting the good. ** SITC Classification Revision 2 was chosen to allow comparison of a time period as long as possible. The dataset contains 236 sectors. Source: Data: UN Comtrade via World Integrated Trade Solutions (WiTS).

The conclusion is that globalization increased competition in most of the markets, but there

are strong tendencies towards concentration of exporting countries of a good in some markets

mainly because of the China effect. Overall, intensified global competition goes along with

17

increasing concentration, for example in the U.S. This very much supports the theoretical

conclusion that in GVCs lead firms, usually MNEs, are in a double-rent-seeking position – an

oligopoly constellation on the selling side and intensive competition or even monopsony

constellation on the supply side.

Terms of trade effects of different groups of goods

For the U.S., Milberg (2008) showed that import price deflation over the period 1986-2006

was very pronounced in sectors that show both fast technological development and in which

GVCs play an important role. In fact, he found that over this period, real import prices in these

sectors declined for the U.S. by 40 percent. These calculations also correspond with recent

calculations by Mark Anner (forthcoming), who has shown that real import prices of apparel

items into the U.S. have fallen by 60 percent over the past 30 years.

Table 3 shows real import price changes between 2000 and 2018 for goods imports from the

rest of the world to the European Union for selected industries. Particularly in the case of

manufactured goods, there was a considerable decline in prices in some industries. The

decline in prices was especially pronounced for machinery of all kinds, where real import

prices fell by more than 40 percent during the period under observation. However, we can

also observe a sharp drop in prices for low-technology goods such as textiles (-32 percent),

apparel (-28 percent), footwear (-10 percent) and miscellaneous manufactured articles (-4

percent), which includes toys. Also noteworthy is the substantial decrease in the prices of

electronic goods (-57 percent) and computers (-47 percent).

On the other hand, real import prices of primary products increased during the period under

investigation, as for example in the case of coffee10, tea, cocoa (+16 percent), vegetables and

fruit (+34 percent), iron and steel (+38 percent), gas (+59 percent) and petroleum (+62).

This development between 2000 and 2018 is certainly in contrast to what Prebisch and Singer

predicted in the 1950s, namely that prices for primary products would relatively fall and prices

for manufacturing products would relatively rise.

10 In the case of coffee, however, it must be mentioned that coffee prices were already in crisis and extremely low in the early 2000s, the starting period of our study (for an overview about the development of coffee prices, compare Amrouk 2018).

18

Table 3: Real Import price changes between 2000-2018, European Union

SITC CODE

INDUSTRY PRICE CHANGE

IN % 73 Metalworking machinery -58.48 77 Electrical machinery, apparatus and appliances. n.e.s., and electrical parts thereof

(including non-electrical counterparts, n.e.s., of electrical household-type equipment)

-57.06

75 Office machines and automatic data-processing machines -47.95 72 Machinery specialized for particular industries -46.08 87 Professional, scientific and controlling instruments and apparatus, n.e.s. -43.84 65 Textile yarn, fabrics, made-up articles, n.e.s., and related products -31.96 93 Special transactions and commodities not classified according to kind -31.78 59 Chemical materials and products, n.e.s. -31.48 25 Pulp and waste paper -29.08 74 General industrial machinery and equipment, n.e.s., and machine parts, n.e.s. -28.75 84 Articles of apparel and clothing accessories -27.69 58 Plastics in non-primary forms -25.90 71 Power-generating machinery and equipment -25.60 24 Cork and wood -20.56 12 Tobacco and tobacco manufactures -20.55 78 Road vehicles (including air-cushion vehicles) -13.34 27 Crude fertilizers, other than those of division 56, and crude minerals (excluding coal,

petroleum and precious stones) -11.77

85 Footwear -10.18 63 Cork and wood manufactures (excluding furniture) -10.04 62 Rubber manufactures, n.e.s. -8.11 26 Textile fibers (other than wool tops and other combed wool) and their wastes (not

manufactured into yarn or fabric) -7.64

61 Leather, leather manufactures, n.e.s., and dressed fur skins -7.32 89 Miscellaneous manufactured articles, n.e.s. -4.15 57 Plastics in primary forms -2.68 64 Paper, paperboard and articles of paper pulp, of paper or of paperboard 0.56 66 Non-metallic mineral manufactures, n.e.s. 6.38 69 Manufactures of metals, n.e.s. 8.18 83 Travel goods, handbags and similar containers 8.58 07 Coffee, tea, cocoa, spices, and manufactures thereof 15.89 05 Vegetables and fruit 34.18 67 Iron and steel 37.93 76 Telecommunications and sound-recording and reproducing apparatus and

equipment 43.14

54 Medicinal and pharmaceutical products 48.06 34 Gas, natural and manufactured 58.80 33 Petroleum, petroleum products and related materials 62.16 11 Beverages 82.96 97 Gold, non-monetary (excluding gold. ores and concentrates) 88.89 28 Metalliferous ores and metal scrap 94.19 32 Coal, coke and briquettes 95.00 96 Coin (other than gold coin), not being legal tender 133.40 41 Animal oils and fats 193.57 79 Other transport equipment 391.85

Source: Import data derived from Eurostat; GDP deflator Federal Reserve Bank of St. Louis Note: GDP deflator for the European Union; index 2015=100; n.e.s. = not elsewhere specified; SITC classification revision 4, two-digit-level

19

The explanation for the relative price increase of primary products is manifold. In general,

prices for primary goods are relatively volatile because supply is inelastic in the short term and

demand as well. Thus, shocks like bad harvests lead to price hikes. In addition, some

commodities have become objects of speculation. Moreover, for some primary products, the

relative increase in prices can be found in the scarcity of some natural resources and the

establishment of supplier cartels, the most famous being the Organization of the Petroleum

Exporting Countries (OPEC). These countries were able to exploit the gifts of nature. However,

a different question is who gets the rents from natural resources. In many cases the companies

realizing rents are MNEs, as for example in the oil sector of Nigeria. Or as the United Nations

Economic Commission for Africa (UNECA 2016) reports, 90 percent of the income derived

from coffee goes to the countries where MNEs have their headquarters, rather than to the

countries where the coffee is produced and exported.

There are various theoretically possible explanations for the enormous drop in relative import

prices that can be observed in certain manufacturing sectors. First, better technology and

exploiting economies scale increased productivity; second, lower costs caused by factors

other than productivity increases, for example lower wage costs; third, higher competition.

The last two points are linked to GVCs. Shifting manufacturing tasks to the Global South

substantially reduces wage and other costs. And monopsony power of lead companies

increases competition and bring prices down to a minimum. For low technology manufactured

goods, we can assume that all three price-reducing factors mentioned above play a role, with

the result that countries in the Global South only reap relatively small benefits from

integrating in GVCs. UNECA (2016, p. 151) makes exactly this point:

“… developing countries are likely to suffer from a ‘fallacy’ of composition’ – many of them entering the production of low-technology manufacturing goods in the belief that it will significantly boost their export earnings, only to find out that the earnings are nowhere as high as expected, as the prices of those goods have fallen exactly because so many countries have started to producing them.”

What we find here is that in extreme cases, the productivity increases achieved in producing

export goods and respective tasks in GVCs can lead to very low welfare effects for the

exporting countries and even to immiserizing growth, which means growth which does not

lead to more domestically available goods and services (Bhagwati 1958).

In the following, to test the terms-of-trade hypothesis by Prebisch and Singer for the period

from 2000 to 2018, we look at terms of trade development for country groups in the Global

South mainly exporting primary goods or simple manufacturing goods. Figure 4 shows the

20

terms of trade index for various countries whose exports are heavily dependent on natural

resources.11 These countries have partly benefited from very favorable terms of trade.

However, the focus on raw materials has also favored another rather negative development,

in the form of poor industrial development or even tendencies of deindustrialization. Very

often, resource rich countries suffer from a persistent overvaluation of their exchange rates

for the industrial sector and a shrinking industrial base, even if they realize current account

surpluses. In addition, the relatively low-price elasticities of natural resources lead to high

price volatility, which is reinforced by speculation in futures markets. Finally, natural resource

wealth stimulates rent-seeking of domestic elites and foreign companies and can lead to the

so-called ‘resource curse’ (Humphreys et al. 2007). 12

Figure 4: Terms of trade index (2000=100); various commodity exporting countries; 2000-2019

Source: World Bank 2021; World Development Indicators. Note:

Note: Net barter terms of trade index is calculated as the percentage ratio of the export unit value indexes to

the import unit value indexes, measured relative to the base.

11 In 2018, 55.7 percent of all Argentine exports were agricultural products, and 4.6 percent were fuels and mining products. In Brazil, agricultural products accounted for 38.9 percent and fuels and mining products for 24.6 percent of all exports in 2018. In Chile, agricultural products accounted for 32 percent, and fuels and mining products for as much as 54 percent of all exports in 2018, while in Colombia they accounted for 17.5 and 59.2 percent, respectively (WTO 2021). 12 We do not look at the group of countries which in an extreme way depend on the export of natural resources, like for example the Arab countries, Russia or Nigeria. For this group of countries terms of trade effects and deindustrialization are even more extreme.

0

50

100

150

200

250

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Argentina Brazil South Africa Colombia Chile

21

Figure 5 shows the terms of trade index for various countries whose exports are heavily

dependent on low-technology manufacturing goods, in some countries especially on apparel.

As can be seen in the figure, the terms of trade of these countries have deteriorated, in some

cases tremendously, especially Pakistan, Bangladesh, Cambodia, but also China. These

countries had to export increasing quantities to get the same quantity of imported goods.

Whether the negative terms of trade effects led to immiserizing growth in some of the

countries cannot be tested here, but as UNECA (2016) argues, expanding exports in these

countries did not stimulate the domestic welfare effects that were probably expected. To this

story also fits the fact that after the creation of the North American Free Trade Agreement

(NAFTA) in 1994, Mexico’s share of world manufactured exports increased significantly while

its share in world manufacturing value-added dropped. “This happened because as high-

export, low-value-added firms in maquiladoras expanded, the traditional industries with high

value-added but low exports withered” (Akyüz 2017, p. 191).

Figure 5: Terms of trade index (2000=100); various Asian countries; 2000-2019

Source: World Bank 2021; World Development Indicators.

Note: Net barter terms of trade index is calculated as the percentage ratio of the export unit value indexes to the import unit value indexes. measured relative to the base.

It is worthwhile mentioning that China managed significant upgrading in GVCs in comparison

to many other countries. The share of foreign value-added in China’s processing exports fell

even from 79 percent in 1997 to 62.7 percent in 2007 and in total manufactured exports from

0

20

40

60

80

100

120

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Bangladesh Cambodia China India Pakistan

22

50 to 40 percent (Akyüz 2017, p. 195; Koopman et al. 2012). Obviously, China could in the

classification of Humphrey and Schmitz (2002) not only manage to achieve product and

process upgrading, but also substantial functional upgrading.

4 Productivity and employment effects of integration in GVCs

In order to examine whether participation in GVCs has positive macroeconomic effects that

go beyond a positive development for individual firms or sectors and could therefore

represent a development strategy, we will first explain how we measure participation in GVCs

and then show whether there is a correlation between participation in GVCs and

macroeconomic variables such as productivity and employment.

Ever since Hummel et al. (2001)'s seminal article, participation in GVCs has typically been

defined and measured in terms of vertical specialization. According to this definition, in a GVC

a good must be produced in different production steps, in which at least two countries are

involved, crossing at least two borders. A distinction is made between backward and forward

participation. Backward participation measures the foreign value-added content of exports.

Here, the exporting country takes the role of the buyer of inputs. For example, the backward

participation rate is very high if a country functions as an assembly platform where imported

components are only assembled for export. Forward participation, on the other hand,

represents the role of the seller. Here, the domestic value added contained in exports of third

countries is measured. Both values taken together as a share of exports express the level of

participation in GVCs. Based on this definition, it is frequently said that half of global trade

today takes place within GVCs (World Bank 2020).

However, in the present study we do not consider this indicator. We instead follow Carballa

Smichowski et al. (2020), and measure GVC participation as the sum of the non-primary

product portion of domestic value-added in exports plus intermediate imports both together

as a share of GDP13. This indicator is characterized by three features14, which we consider

beneficial for our work: first, it excludes primary products, which often exhibit very volatile

prices and do not add substantially to industrialization. Second, imports of finished products

13 The formal definition is (&'())∗(,-..&)/!.0∗(,-..0)1'2 , where XDVA is domestic value added in gross exports, ppX is the share of primary products in total exports, ipM is gross imports of intermediate products and ppM the share of primary products in total imports. 14 For a detailed introduction and discussion of the indicator, its measurement and differentiation from the common indicator, compare Carballa Smichowski et al. (2018).

23

for domestic use are also excluded. Third, the denominator is GDP instead of gross exports.

Thus, the value generated in the context of GVCs is put in relation to the value generated in

the domestic economy, and not just in relation to a country’s exports. Another plus point, in

our opinion, is the fact that not only trade which has crossed at least two borders counts as

GVC-related. The two border rule overlooks, for example, the fact that imported inputs can

also be processed into final products that are sold in the country and are not intended for

export. For example, Brazil is a country where electronic goods are assembled with imported

components primarily for sale in the domestic market. In the usual definition of the GVC

participation rate, this important sector would not be counted because the assembled final

products are predominantly not destined for export. However, not declaring this important

production as GVC participation is misleading.

Figure 6 shows the GVC participation rate according to our definition for 63 OECD and non-

OECD countries for 2005 and 2015. In the ranking of countries, it is striking that at the bottom

end, with little GVC participation, there are mainly countries that are rich in natural resources

and focus on the export of raw materials which is not part GVCs in our measure. In the

comparison period, the participation of these resource-rich countries in GVCs has decreased

remarkably. In fact, participation in GVCs has declined for almost all countries (in more than

85 percent of all countries in Figure 6, including a strong decline in China) over the observation

period. These figures support the trend shown in Figure 1, i.e., stagnation or decline of the

importance of goods exports as a share of GDP since 2008. Especially in small countries like

Luxembourg, Ireland, Singapore, Malta, and even Hong Kong, GVC trading plays a major role.

However, this is not surprising as smaller countries are usually deeper integrated into

international trade than big countries like the U.S.

24

Figure 6: Global Value Chain Participation excluding primary products, 2005 and 2015

Source: OECD TiVA Database. Version 2018; Data on primary products and total imports and exports: UNCTAD Statistics; GDP: World Development Indicators Sorted ascending by 2015

In the rest of this section, we turn to analyzing several relations between GVC participation

and key macroeconomic variables.

Global value chains and productivity

One major factor on the road to economic development is an increase in labor productivity,

shifting workers from less to more productive activities. The eminent importance of labor

productivity is aptly expressed by Paul Krugman (1992, p. 9):

“Productivity isn’t everything, but in the long run it is almost everything. A country’s ability to improve its standard of living over time depends almost entirely on its ability

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6

LuxembourgIreland

Viet NamSingapore

MaltaHungary

Slovak RepublicCzech Republic

ThailandMalaysia

Hong Kong, ChinaSlovenia

CambodiaEstonia

BelgiumKorea

BulgariaAustr ia

SwitzerlandCyprusPoland

LithuaniaDenmarkGermany

NetherlandsRomania

TunisiaSwedenMexico

Phil ippinesLatvia

PortugalFinlandCroatia

MoroccoCosta Rica

SpainIsraelItaly

FranceChina (People's…

United KingdomCanadaTurkey

South AfricaIceland

JapanIndia

IndonesiaNorway

Saudi ArabiaUnited States

GreeceChile

New ZealandPeru

Russian FederationAustralia

ArgentinaKazakhstan

ColombiaBrazil

Brunei Darussalam

2005 2015

25

to raise its output per worker. [In the U.S.] World War II veterans came home to an economy that doubled its productivity over the next 25 years; as a result, they found themselves achieving living standards their parents had never imagined. Vietnam veterans came home to an economy that raised its productivity less than 10 percent in 15 years; as a result, they found themselves living no better – and in many cases worse – than their parents.”

Current research on the relationship between participation in GVCs and productivity points

out various channels via which GVC participation can stimulate productivity growth. It is

assumed that the benefits arise at the firm level through specialization in core business and

offshoring other tasks, importing foreign inputs that may be cheaper or of better quality, pro-

competitive effects in domestic input markets, and knowledge spillover effects from MNEs

(Criscuolo and Timmis 2017). Recently, empirical studies have been conducted that examine

the impact of participation in GVCs on productivity. For example, Constantinescu et al. (2017),

for a panel of 13 industries in 40 countries covering the years 1995-2009, show that GVC

participation – measured as the share of foreign value added in gross exports of goods and

services – is a significant driver of labor productivity. Pahl and Timmer (2020) find a statistically

significant effect of GVC participation for a panel of 58 countries for the years 1970-2008 –

measured as the imported input content in exports as a share of exports – on labor

productivity growth in the export sector. Urata and Baek (2020) also present empirical findings

for a panel of 47 countries and 13 manufacturing sectors covering the years 1995 until 2011

that show that both backward and forward GVC participation contribute to an increase in the

productivity of countries involved in GVCs15. Moreover, they find that the productivity-

enhancing effect is largest for developing countries that import intermediate goods from

developed countries.

However, the finding that participation in GVCs increases the productivity of firms operating

in the export sector is not particularly surprising. Lead firms work with suppliers that have to

meet their quality standards and new technology is transferred to subsidiaries or even

subcontractors. A different question is whether functional upgrading and inter-sectoral

upgrading takes place which is of key importance for higher value adding and catching up with

productivity levels and the innovative power of developed countries. Case studies have also

consistently shown that product and process upgrading takes place in GVCs, but functional

upgrading usually not (Dünhaupt et al. 2020; Dünhaupt et al. forthcoming). Especially in cases

of captive and vertical governance in the form of FDI, functional and even less inter-sectoral

15 The authors measure productivity by total factor productivity growth, computed as the Solow residual.

26

upgrading is unlikely. Humphrey and Schmitz (2000, p. 23) write about “quasi-hierarchical

chain[s] ….: in such chains, functional upgrading is limited. Local firms move into new non-

strategic functions, but refrain from or are prevented from occupying the strategic functions

of the chain which tend to lie in product definition (design, branding, marketing) and chain co-

ordination.”

The other side of the coin of Humphrey and Schmitz’s convincing argument is that a

domination of key sectors of the economy by foreign firms prevents functional and inter-

sectoral upgrading and keeps a country always second class. Preventing the dominance of

foreign firms is an important element in a catching-up process and can help to explain the

relatively poor development in Latin America compared with Asia. In a nutshell, as Amsden

(2009, p. 413) puts it:

“If all industry were foreign-owned, a developing country would never develop top skills and highest-paying jobs (CEO, CFO, Regional Manager, Lead Scientist) that rocket the modern corporation. The developing country would never become advanced enough to earn the entrepreneurial rents that tacit technology and associated brand names earn.”

A further crucial question is whether companies integrated in GVCs are industrial enclaves, or

whether there are spillover effects and intensive links to the rest of the economy. For

example, if all inputs for a production are imported and the output exported, in substance

only labor is delivered by the host country. In such cases the positive effects for a country are

relatively small. Already Hirschman (1958) stressed that internal forward and backward

linkages are of key importance to increase domestic value added and to create high

technology and qualification spillovers. Hence, in order to make a real contribution to

development, other sectors and industries in the country would also have to benefit from

integration in GVCs through linkages and spillover effects, so that overall labor productivity in

the country increases. Singer (1950) noted that underdeveloped countries often have a dual

economic structure: on the one hand, there is a relatively productive sector producing for

export; on the other hand, a sector producing for the domestic economy, with low

productivity. In such a dual structure it can be argued that the relatively productive sectors

integrated in GVCs are not a real part of the domestic economy, and the technological spillover

effects are only small.

27

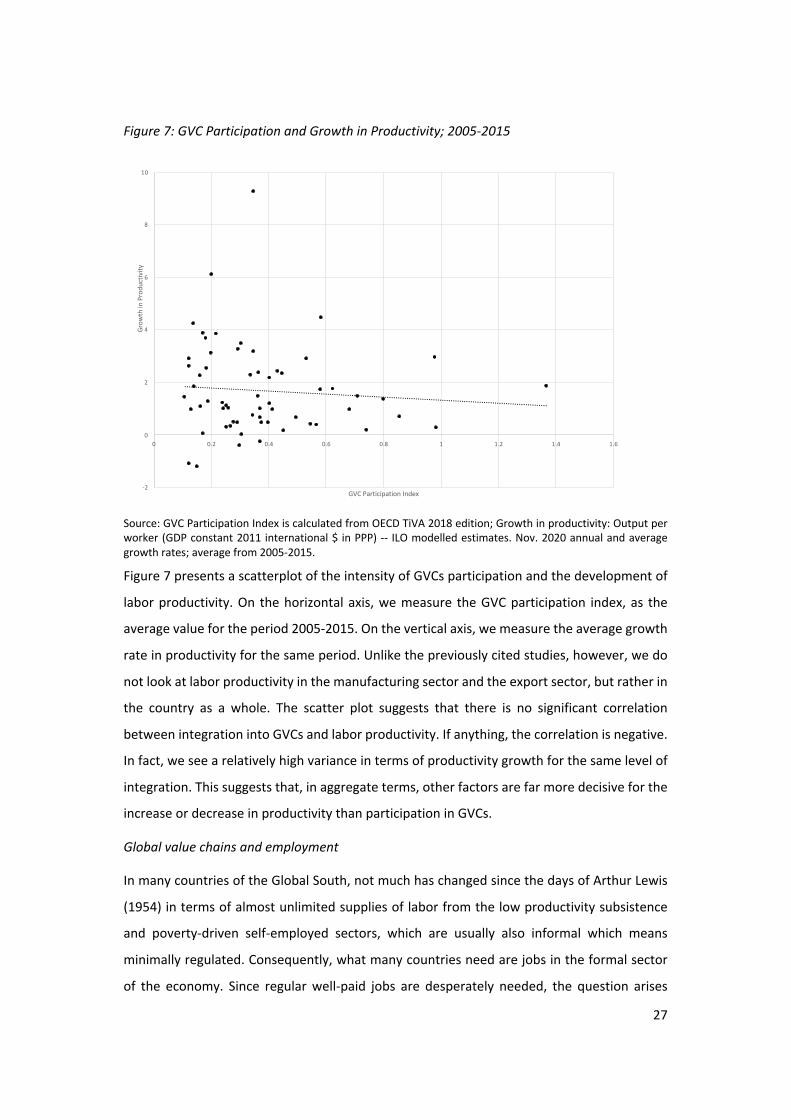

Figure 7: GVC Participation and Growth in Productivity; 2005-2015

Source: GVC Participation Index is calculated from OECD TiVA 2018 edition; Growth in productivity: Output per worker (GDP constant 2011 international $ in PPP) -- ILO modelled estimates. Nov. 2020 annual and average growth rates; average from 2005-2015.

Figure 7 presents a scatterplot of the intensity of GVCs participation and the development of

labor productivity. On the horizontal axis, we measure the GVC participation index, as the

average value for the period 2005-2015. On the vertical axis, we measure the average growth

rate in productivity for the same period. Unlike the previously cited studies, however, we do

not look at labor productivity in the manufacturing sector and the export sector, but rather in

the country as a whole. The scatter plot suggests that there is no significant correlation

between integration into GVCs and labor productivity. If anything, the correlation is negative.

In fact, we see a relatively high variance in terms of productivity growth for the same level of

integration. This suggests that, in aggregate terms, other factors are far more decisive for the

increase or decrease in productivity than participation in GVCs.

Global value chains and employment

In many countries of the Global South, not much has changed since the days of Arthur Lewis

(1954) in terms of almost unlimited supplies of labor from the low productivity subsistence

and poverty-driven self-employed sectors, which are usually also informal which means

minimally regulated. Consequently, what many countries need are jobs in the formal sector

of the economy. Since regular well-paid jobs are desperately needed, the question arises

-2

0

2

4

6

8

10

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6

Grow

th in

Pro

duct

ivity

GVC Participation Index

28

whether participation in GVCs contributes to employment growth. However, empirical studies

that analyze the relationship between GVC participation and employment indicate a negative

relationship. A study by Cali et al. (2016), which covers the years 1995-2011, shows that since

2001 the job intensity of exports has declined in both high- and low-income countries. The

novelty of this study is that it took into account not only direct export jobs, but also indirect

jobs., i.e., jobs in industries that serve the export sector. The result of this study is not

surprising; the explanation is that productivity increased. The result for developing countries

is a double-edged sword. Productivity increases are, as mentioned, of key importance for

development and catching up. But, as mentioned as well, the welfare effects for developing

countries are probably small and productivity increases reduce the employment effects of

increasing output (see also Rodrik 2018). Pahl and Timmer (2020) find no positive correlation

between GVC participation and employment growth in their panel estimation which covers

the period 1970-2008. The authors conclude that GVC participation is “a mixed blessing at

best” (Pahl and Timmer 2020, p. 1699). They also identify a bias in technological development

against unskilled workers as a possible explanation. Since MNEs often demand and employ

relatively high-skilled workers in a country, unskilled workers fall behind – apparently in all

parts of the world. Farole (2016) shows that almost no positive relationship exists between

the GVC participation index and the employment share of adult population, using average

values between 2008 and 2013. In fact, in his investigation a higher level of GVC participation

is actually related to a slightly lower employment share.

Figure 8 plots the GVC participation index and the employment share for averaged values from

2005-2015. As can be seen in the figure, there exists almost no relationship between both

variables. This is in line with the findings reported above.

29

Figure 8: Global Value Chain Participation and Employment Share of Adult Population*; 2005-2015

Source: GVC Participation Index is calculated from OECD TiVA 2018 edition; Employment Share from World Bank World Development Indicators; average from 2005-2015.

Note: Employment to population ratio. 15+ total (%) (national estimate)

This result should not be a surprise. Even if exports related to GVCs and employment in the

affected sectors increase, other sectors may – due to higher imports – shrink. Deeper

integration into world markets is not an engine of growth and employment per se. A country

can be very successful in offshoring certain tasks in GVCs and at the same time realize big

trade deficits which destroy domestic jobs. Or efficiency gains can lead to unemployment

when aggregate demand is not increasing sufficiently. It is the combination of increasing

foreign trade and simultaneously increasing foreign trade surpluses that usually stimulates

macroeconomic growth and employment. However, such mercantilist strategies are not

possible for all countries.

Rodrik (2018, p. 5) writes:

“It appears that exports are creating fewer and fewer jobs, and GVCs are certainly not helping. This is disappointing from a number of perspectives. It puts a damper on the idea of trade as an engine of growth. It suggests that the technological and organizational benefits associated with exports are not being disseminated throughout the economy. And since exports tend to be associated with better-paying jobs, it raises concerns about wage levels and inclusion.”

0

10

20

30

40

50

60

70

80

90

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6

Empl

oym

ent t

o po

pula

tion

ratio

(%)

GVC Participation Index

30

Overall, integration in global trade and GVCs does not, in the typical developing country,

create sufficient jobs to lead to inclusive growth and the absorption of traditional sectors.

5 Conclusion

The increasing importance of GVCs including the high levels of FDI from the 1990s onwards is

often considered to be one of the key pillars to support development in the Global South.

There is no doubt that GVCs can trigger positive developments in the form of growth and

economic upgrading of firms and sectors, but there is neither a guarantee that this will happen

nor a guarantee that, even in the positive case, only industrial enclaves will emerge that have

no positive spillover effects on the rest of the country, and “remain a tiny sliver of globally

integrated firms” (Rodrik 2018, p. 14). Moreover, there are also cases in which integration in

the world economy under a regime of free trade led to economic downgrading of sectors. And

in general, the effects of GVCs may be too weak to have positive macroeconomic impacts.

In this article we have argued that, on the one hand, there has been consolidation on the part

of the MNEs towards more oligopolistic markets and, on the other hand, globalization since

the 1980s has led to more and more countries entering into the production of simple

manufacturing goods; this has led, among other things, to more intensive competition and a

massive drop in the real import prices for manufactured goods over the same period.

Integration into GVCs facilitates industrialization, but because tasks in GVCs became so simple

and thus in spite of increasing productivity in export sectors, industrialization as such is now

less useful as a development strategy than it was 40 years ago. And there is an enormous

power imbalance between MNEs and their suppliers, which pushes the prices and profits of

many suppliers of MNEs to a minimum.

There are strong signs that integration into GVCs by countries in the Global South triggers

product and process upgrading for supplying firms. But it is very unlikely that lead firms

support their suppliers in functional or inter-sectoral upgrading, because it is not in their

interest to nurture potential competitors. Suppliers are instead positioned in GVCs by lead

firms to fulfil relatively simple tasks in a good and stable way. Thus, the conclusion is that while

integration into GVCs can bring productivity increases, catching-up of firms or sectors in the