global financial systems chapter 20 european crisis financial systems © 2017 jon danielsson, page...

TRANSCRIPT

Global Financial Systems © 2017 Jon Danielsson, page 1 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Global Financial Systems

Chapter 20

European Crisis

Jon Danielsson London School of Economics© 2017

To accompanyGlobal Financial Systems: Stability and Risk

http://www.globalfinancialsystems.org/

Published by Pearson 2013

Version 3.0, August 2016

Global Financial Systems © 2017 Jon Danielsson, page 2 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Book and slides

• The tables and graphs arethe same as in the book

• See the book forreferences to original datasources

• Updated versions of theslides can be downloadedfrom the book web pagewww.globalfinancialsystems.org

Global Financial Systems © 2017 Jon Danielsson, page 3 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

• The first part of these slides uses content from Chapter19 of the printed book, “sovereign debt crisis”

• The second part of the slides draws on Chapter 20,“European Crisis” published on–line

Global Financial Systems © 2017 Jon Danielsson, page 4 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

European Crisis

Global Financial Systems © 2017 Jon Danielsson, page 5 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Successful monetary unions

• Single nation state

• Free movement of people

• Economic rules and regulations mostly harmonized

• Economic development in sync

• Transfer union

• Or junior member much much smaller (Luxembourg,Panama)

Global Financial Systems © 2017 Jon Danielsson, page 6 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

EU attempts

• Snake in the tunnel in the 1970s

• European monetary system with ECU in 1980s (recall theERM crisis)

• Euro agreed on in 1995, implemented from 1999

Global Financial Systems © 2017 Jon Danielsson, page 7 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

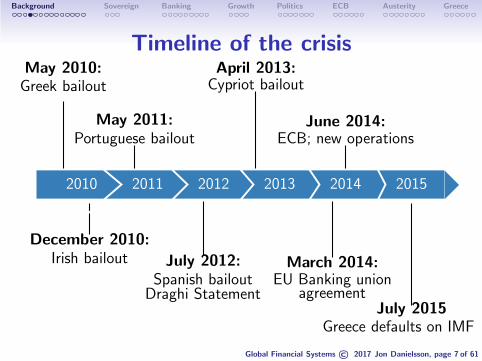

Timeline of the crisisMay 2010:Greek bailout

December 2010:Irish bailout

May 2011:Portuguese bailout

July 2012:Spanish bailout

Draghi Statement

April 2013:Cypriot bailout

March 2014:EU Banking union

agreement

June 2014:ECB; new operations

July 2015Greece defaults on IMF

2010 2011 2012 2013 2014 2015

Global Financial Systems © 2017 Jon Danielsson, page 8 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Role of the euro

• Several EU but not euro zone members have suffered aserious crisis and received bailouts

• Hungary, Latvia, Romania

• No impact on anybody else

• Tiny Cyprus had a huge impact

Global Financial Systems © 2017 Jon Danielsson, page 9 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Convergence of interest rates

• Before the crisis, market participants believed bonds tosovereigns were backed by all members

• Regardless of structural issues, sovereign bonds ended upcarrying the same interest rate

Global Financial Systems © 2017 Jon Danielsson, page 10 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Selected European long–term bond rates

(annual max) to August 2016

Germany

Greece

Ireland

Portugal

Spain

France

1985 1989 1993 1997 2001 2005 2009 2013

5%

10%

15%

20%

25%

30%

Global Financial Systems © 2017 Jon Danielsson, page 11 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

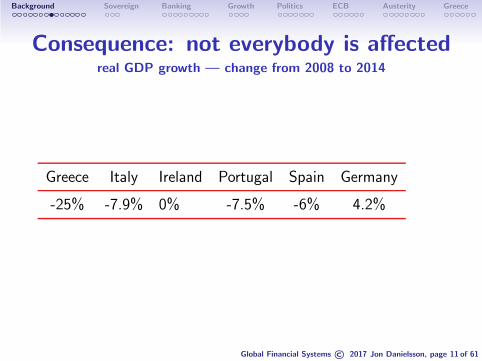

Consequence: not everybody is affectedreal GDP growth — change from 2008 to 2014

Greece Italy Ireland Portugal Spain Germany

-25% -7.9% 0% -7.5% -6% 4.2%

Global Financial Systems © 2017 Jon Danielsson, page 12 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Liquidity or solvency crisis

• Initial justification for support by ECB was that it is aliquidity crisis

• Then a “shock and awe” support was needed

• The amount of money is eye–catching, close to e800billion supposedly available

• But it is illusionary, as there are many restrictions onhow the funds can be used

• It therefore fails the test of effective liquidity support

• The inability to do so contributed to the crisis

• It now seems that it is much more of a solvency orstructural crisis

Global Financial Systems © 2017 Jon Danielsson, page 13 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

The European Crisis is Really

Multiple Crises in One

1. Banking

2. Debt

3. Growth

4. Political crisis

Global Financial Systems © 2017 Jon Danielsson, page 14 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Interactions

• Banks in difficulty may require bailouts and drag downgrowth

• Sovereign debt burdens banks’ balance sheets

• A country in a sovereign debt crisis, and hence austerity,cuts back on government demand, adversely affectinggrowth

• Negative growth means companies have difficultiesrepaying loans

• It also causes a decrease in tax revenues

Global Financial Systems © 2017 Jon Danielsson, page 15 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

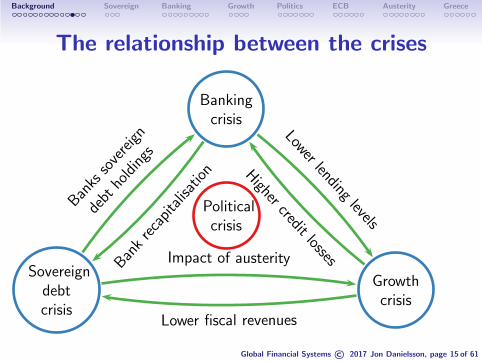

The relationship between the crises

Bankingcrisis

Sovereigndebtcrisis

Growthcrisis

Politicalcrisis

Bankrecapitalisation

Bankssovereign

debtholdings

Impact of austerity

Lower fiscal revenues

Higher credit losses

Lower lendinglevels

Global Financial Systems © 2017 Jon Danielsson, page 16 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

The crisis countries

• Structural problems

• Greece and Portugal

• Banking problems

• Ireland

• Structural and banking problems

• Spain and Cyprus

Global Financial Systems © 2017 Jon Danielsson, page 17 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

The business and credit cycles

• Rapid credit growth is an indicator of an upcomingfinancial crises

• Euro zone crises no different

• Prior, periphery borrowed large amounts

• In Spain and Ireland these funds went largely into the realestate bubble

• When these new investments became unprofitable, thebanks were hit by a large amount of non–performingloans, thus facing deteriorated capital levels

• The correlation between prior domestic money supplygrowth and the gravity of the recession is quite strong

Global Financial Systems © 2017 Jon Danielsson, page 18 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Sovereign Debt Crisis

Global Financial Systems © 2017 Jon Danielsson, page 19 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Sovereign debt crisis

• A country may seem to have sustainable debt levels whenthings are good, but can quickly get into a crisis

• The start was the Greek crisis which then spread to othercountries

• Some countries came into the crisis with very high debtlevels (e.g. Greece)

• Others has very little debt which quickly exploded, likeIreland and Spain

Global Financial Systems © 2017 Jon Danielsson, page 20 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Is the EU really excessively indebted?Gross debt of selected countries and global rank out of 173 countries

Estonia 168China 100Korea 123

Slovenia 28Finland 62

India 49Germany 42

Spain 15Canada 22Cyprus 10France 17

United States 12Singapore 16

Ireland 18Italy 4

Jamaica 7Greece 2Japan 1

0% 25% 75% 125% 175% 225%

2007

2015

Global Financial Systems © 2017 Jon Danielsson, page 21 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Banking Crisis

Global Financial Systems © 2017 Jon Danielsson, page 22 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

European banks

• Europe has more than its fair share of banks

• With the common market, banks aggressively expandedacross Europe

• Net foreign liabilities of the Irish banking systemincreased from around 10% of GDP in 2003, to 55% in2007

• Corresponding number for Spain grew from 35 to 65%

• Regulations failed to keep up (banking union discussedlater meant to solve this)

Global Financial Systems © 2017 Jon Danielsson, page 23 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Two explanations for banking crisis

• Banks were the culprit

• For example, excessively expanding without adequateoversight

• Ireland, Spain, Belgium, Germany, France (Portugal andItaly have some elements)

• Banks are the victims

• More or less prudently run but failing because of thecountry they are in

• Greece (some elements of Italy, Cyprus, Portugal)

Global Financial Systems © 2017 Jon Danielsson, page 24 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

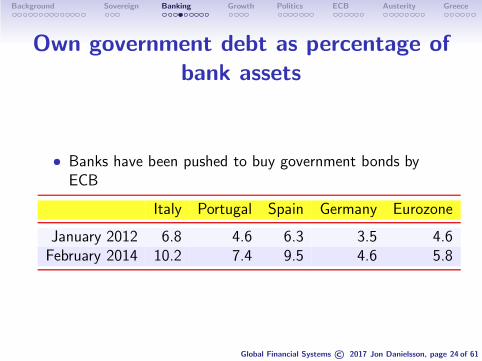

Own government debt as percentage of

bank assets

• Banks have been pushed to buy government bonds byECB

Italy Portugal Spain Germany Eurozone

January 2012 6.8 4.6 6.3 3.5 4.6February 2014 10.2 7.4 9.5 4.6 5.8

Global Financial Systems © 2017 Jon Danielsson, page 25 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Bank resolution in the EU

• In the beginning of the crisis taxpayers bore losses

• Expectation that amounts were small• Worries about the types of creditors (like pension funds

and vulnerable banks)• Worries about financial stability (it started in the fall of

2008)

• With time the banks’ creditors took over

• Banco Espırito Santo split into a good bank and badbank, equity holders and junior creditors wiped out,senior management was replaced

• The sovereign is providing close to e5 billion

• We discuss the Italian banks in the next Chapter

Global Financial Systems © 2017 Jon Danielsson, page 26 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Bail–ins

• Creditors participate in resolution

• EU law now demands a bail in by creditors andshareholders before the national state is allowed to bailout its banks

• Can be problematic because of the composition of thecreditors (like Cyprus and Italy, we come back to this)

Global Financial Systems © 2017 Jon Danielsson, page 27 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Deposits

• The run on Northern Rock was early in the crisis

• Maintaining confidence in the banking system was a firstorder priority in 2008

• Deposit insurance was hence unimpeachable

• Until Cyprus (next slide)

Global Financial Systems © 2017 Jon Danielsson, page 28 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Cyprus

• Status as an offshore haven

• Its largest banks were heavily exposed to Greek sovereigns

• Fine, because “European sovereign debt is riskless”

• With second Greek bailout in March 2012, it becameclear that the banks were bankrupt

• The government refused to recognize the problem, andthe EU/ECB did not press the issue

• A slow run on the Cypriot banks ensued

• A new government recognized the problem, and the EUentered into bailout discussions in April 2013

• Capital controls have now been lifted

Global Financial Systems © 2017 Jon Danielsson, page 29 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Cypriot bailout mistakes

• Very few bondholders, most debt is deposits

• Government insisted on hitting insured (below e100K)depositors, EU agreed

• Perhaps the biggest policy blunder in the whole crisis

• Now European deposits are no longer sacrosanct,consequently its financial system is more vulnerable

• The authorities quickly backtracked and only hituninsured depositors

• Given that the nature of the problem was known for ayear, it is incomprehensible that no authority prepared forwhat was an entirely foreseeable and unavoidable crisis

Global Financial Systems © 2017 Jon Danielsson, page 30 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Growth Crisis

Global Financial Systems © 2017 Jon Danielsson, page 31 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

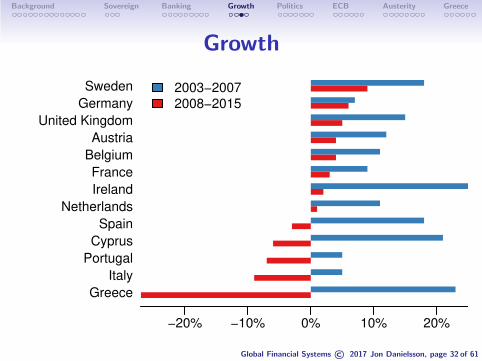

Importance of growth

• If all countries in Europe enjoyed similar economicgrowth, a crisis would be unlikely

• Problem is divergence in economic fortunes

• Some European countries increasingly uncompetitive

• If growth is negative and the growth prospects are poor, acountry can enter a vicious cycle

• Meanwhile it is shunned by foreign investors

• This affects other countries in the Union

• Feedback 2 slides down

Global Financial Systems © 2017 Jon Danielsson, page 32 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Growth

Greece

Italy

Portugal

Cyprus

Spain

Netherlands

Ireland

France

Belgium

Austria

United Kingdom

Germany

Sweden

−20% −10% 0% 10% 20%

2003−2007

2008−2015

Global Financial Systems © 2017 Jon Danielsson, page 33 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Growth problem — Negative feedback loop

• Production decreases, then tax revenues

• Deficit grows, increased debt levels, unless offset by adecrease in expenditure

• Growth prospects negative, investors become more wary— ask for higher interest rates

• Country with current account deficit accumulates debtand becomes increasingly vulnerable to changes in capitalflows

• Large — and even small if over a long period of time —

differences in growth patterns can therefore create

instabilities

Global Financial Systems © 2017 Jon Danielsson, page 34 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

European Politics and theCrisis

Global Financial Systems © 2017 Jon Danielsson, page 35 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Thomas Sargent (2011)

“There are no new issues in economic theory with Europe andthe Euro [...] the difficult thing is the politics.”

Global Financial Systems © 2017 Jon Danielsson, page 36 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Motivation for integration

• The motivation for European integration was politics, noteconomics

• Economic considerations swept under the table

• Creation of the euro and common market in bankingservices only later in the European Union’s history

Global Financial Systems © 2017 Jon Danielsson, page 37 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

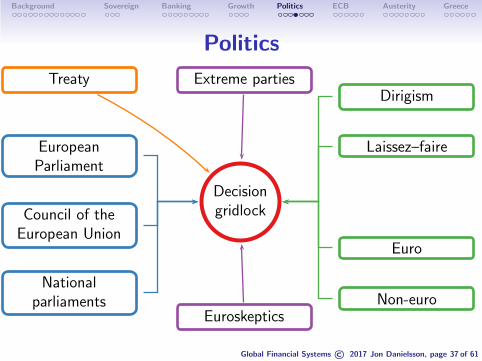

Politics

Decisiongridlock

EuropeanParliament

Council of theEuropean Union

Nationalparliaments

TreatyDirigism

Laissez–faire

Euro

Non-euroEuroskeptics

Extreme parties

Global Financial Systems © 2017 Jon Danielsson, page 38 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Balance of powers

• Non-crisis countries: Germany, Belgium, the Netherlands,Luxembourg, Finland and Austria

• Crisis countries: Greece, Italy, Ireland, Spain, Portugaland Cyprus

• Now Ireland, Spain (and perhaps Portugal) have changedpositions — Why?

• If the crisis countries refuse the conditions, risk notreceiving financial aid

• If non–crisis countries failed to reach an agreement, theyare impacted by these failures and face possibility of EUfailing

Global Financial Systems © 2017 Jon Danielsson, page 39 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Balance in favor of the non–crisis countries

1. As providers of the loans, a failure to reach an agreementwould have a less severe impact on their economies thanon the economies of the recipients

2. The way the crisis was seen by the electorate of therespective countries

• Greece’s fiscal mismanagement and misreporting of theirbudget deficits made the Southern countries appeareconomically irresponsible to non–crisis voters

3. For the elites of the indebted countries “good” financialmanagement consists of paying ones debts where thereputational costs of not doing so will be severe

4. The same elites see joining the EU as having been verybeneficial and consequently they fear being kicked out

Global Financial Systems © 2017 Jon Danielsson, page 40 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Decision lags

• A single country can make very rapid decisions, involvingthe government, the central bank and the parliament

• In the EU, there are multiple layers of decision–making

• A law is submitted to both the European Parliament andthe Council of Europe, meaning 27 governments startnegotiating

• A treaty requires all members to unanimously agree, eithervia parliament or referenda, a long and uncertain process

• A treaty is the equivalent of a constitutional change, butaddresses much more minute issues than a constitutionalchange in nation states (e.g. banking union)

Global Financial Systems © 2017 Jon Danielsson, page 41 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

The position of the ECB in thecrisis

Global Financial Systems © 2017 Jon Danielsson, page 42 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

“Within our mandate, the ECB

is ready to do whatever it takes

to preserve the Euro. And

believe me, it will be enough”

Mario Draghi

Global Financial Systems © 2017 Jon Danielsson, page 43 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

The ECB: an ambiguous position in the

political crisis

• When a crisis happens, governments quickly implement amixture of fiscal, legal, regulatory and monetaryoperations

• The central bank plays a key role

• In the EU, this is not possible: decision lags andopposition among member countries make the ECB’s taskmore difficult

• The ECB was not allowed to monetize the debt ofmember countries

• The QE program was launched in January 2015 only

• So the ECB has been accused of reacting “too little, too

late”

Global Financial Systems © 2017 Jon Danielsson, page 44 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Has the ECB gone too far?

• Some countries have accused the ECB of expanding itsmandate too far

• It was part of the Troika in the Greek crisis

• It has new supervisory functions in the banking union

• This raises issues regarding the independence and theaccoutability of the ECB

Global Financial Systems © 2017 Jon Danielsson, page 45 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

New role of ECB

• Accepting distressed sovereign securities as collateral

• Convincing the market of its willingness to do so towhatever extent was required

• Managed to convince the market that it had removed thecredit risk associated with holding EU sovereigns

Global Financial Systems © 2017 Jon Danielsson, page 46 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Risk

• Assets remain risky — backed by member governments,notably Germany

• ECB not willing to accept losses, because of strongNorthern European opposition, since that would imply themutualization of losses

• Strident denials that any such transfer has taken placeindicate the sensitivity of this topic and its unacceptabilityto the electorate

• Hard to explain where else the risk may have gone

• The pragmatic ECB approach is sufficiently obscure thatit may remain for many years a de–facto lender of lastresort despite the tenuous political support for this role

Global Financial Systems © 2017 Jon Danielsson, page 47 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Structural reforms and theausterity debate

Global Financial Systems © 2017 Jon Danielsson, page 48 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

The crisis debate (1): irrational panic?

• The pre–crisis convergence is the norm

• Market panicked

• Spread on a country’s bond highly correlated with thedegree of austerity programs implemented

• Negative impact on GDP growth — counter–productive

• Unlimited support via OMT in 2012 was necessary tocalm panicking markets

Global Financial Systems © 2017 Jon Danielsson, page 49 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

The crisis debate (2): rationality?

• Spreads are correlated with the underlying fundamentals

• The fact that the OMT led to lower bond yields does notimply that the austerity was not necessary

• If governments would credibly implement fiscaladjustments, yields would have decreased regardlessly

• OMT announcement did not improve fundamentals andbonds are underpriced

• As yields converge, pressure to adjustment weakens —imbalances build up again

• Risk of moral hazard — benefit felt by the worstperforming countries

Global Financial Systems © 2017 Jon Danielsson, page 50 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Internal devaluation

• A country with an overvalued currency can just devalueits currency to become competitive

• With the euro this is impossible, but a country can do aninternal devaluation

• Aim: lowering factor costs (e.g. wages)

• Germany did this successfully in the early 2000’s (Hartzplan)

• So have the Baltic countries and Ireland

• Even Spain has had some success

• But this is very inefficient

Global Financial Systems © 2017 Jon Danielsson, page 51 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Structural reforms

• Some European countries became increasinglyuncompetitive

• For example, Italy which will be discussed in nextChapter

• Countries providing bailouts demand structural reforms

• So the recipients become more competitive

• Will not need more bailouts

• Will pay the money back

Global Financial Systems © 2017 Jon Danielsson, page 52 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Obstacles to structural reforms

• Liberalization of services and utility sectors

• The periphery countries are more heavily regulated andless productive

• The labour market is often singled out as being especiallyin need of reform that are strongly resisted by vestedinterests

• Reforms are often painful in the short–run — beneficial inthe long–run

• Removing obstacles for firing employees can lead tofurther unemployment in the short-run

• Reforms require a broad political agreement, can bedifficult to achieve

Global Financial Systems © 2017 Jon Danielsson, page 53 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Criticisms of austerity

• Austerity measures too stringent, hindering growth

• Cutting government expenditure during a recessionaggravates downturn, is counterproductive

• Falling GDP would counteracts efforts to reduce thedebt/GDP ratio through debt reduction

• Lower living standards, with no improvement of debtsustainability

• Government spending has positive multiplier effect

• Backed up by evidence from the Great Depression

• Ideally, the exchange rate should be adjusted

Global Financial Systems © 2017 Jon Danielsson, page 54 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Proponents of austerity

• Stimulus multiplier is <1 — crowding out

• Stimulus might just lead to increased savings if seen astemporary

• Increase in government debt might simply encouragelenders to demand higher interest rates, which in turnwould drag down growth

• Praise for Latvia

Global Financial Systems © 2017 Jon Danielsson, page 55 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Political instability

• Austerity causes protests and encourages extreme politicalparties

• Makes it difficult to accept austerity

• Feelings of lack of democracy

• Many governments changed consequently

Global Financial Systems © 2017 Jon Danielsson, page 56 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

The Greek crisis

Global Financial Systems © 2017 Jon Danielsson, page 57 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

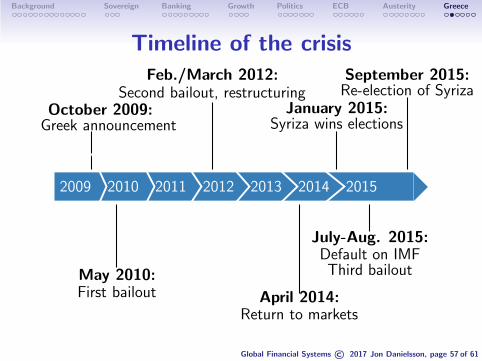

Timeline of the crisis

October 2009:Greek announcement

May 2010:First bailout

Feb./March 2012:Second bailout, restructuring

April 2014:Return to markets

January 2015:Syriza wins elections

July-Aug. 2015:Default on IMFThird bailout

September 2015:Re-election of Syriza

2009 2010 2011 2012 2013 2014 2015

Global Financial Systems © 2017 Jon Danielsson, page 58 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Origins of the crisis

• Greece could borrow credibility by entering the monetaryunion

• So its interest rates on sovereign bonds decreased

• Between 2001 and 2009, government spending increasedfrom 45% to 50% of GDP, financed by borrowing oncapital markets

• Low competitiveness (red carpet, weak bankruptcy law,high unit labour costs)

• Combined with rapid growth, the current account deficitgrew fast

Global Financial Systems © 2017 Jon Danielsson, page 59 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

The crisis: events and aftermaths

• In October 2009, the newly elected Prime Ministerrevealed revised official financial data

• In April 2009, the government predicted a deficit of 3.7%of GDP

• After the elections predictions were raised to 12.5% andfurther to 15.4%

Global Financial Systems © 2017 Jon Danielsson, page 60 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

How the ECB contributed to fragilities in

the Greek banking sector

• Under EU law, the ECB was forbidden from directlyfinancing member countries until 2015

• But it encouraged European and Greek banks to buyGreek government bonds

• It was a QE program “by the backdoor”

• So it transferred the risk of default from the sovereigns tothe banks

Global Financial Systems © 2017 Jon Danielsson, page 61 of 61

Background Sovereign Banking Growth Politics ECB Austerity Greece

Who owns Greek debt?

• The debt has shifted hands: from private to officialcreditors

• A major part of the first and second bailouts was used tohelp private creditors reduce their exposure to Greek debtby around $56 billion

• This has been a major point of contest by Syriza

• Among official creditors, Eurozone members owned 60%of the Greek debt through the EFSF and the GLF

• Among Eurozone members, Germany is by far the largestcreditor