global brands - im - 2010.10.27

TRANSCRIPT

J&E Davy, trading as Davy, is regulated by the Central Bank of Ireland. Davy is a member of the Irish Stock Exchange, the London Stock Exchange and Euronext.

Important: This is neither a full prospectus nor a supplement, both of which are available on request from Davy, Davy House, 49 Dawson Street, Dublin 2. Investors are advised to read these documents prior to making an investment decision.

Davy Private Clients

Global Brands Equity Fund i n f o r m at i o n m e m o r a n d u m oCtober 2010

c a p i ta l ma r k e t s | co r p o r at e f i n a n c e | p r i vat e c l i e n t s | r e s e a r c h

Global brands Equity Fund

Powerful Global Brands

Emerging Markets

New Consumers

Growing Companies

Strong Balance Sheets

contents

Section Title page

1 Summary of Investment 4

2 Investment Opportunity 5

2.1 Why Global Brands? 5

2.2 Investment Management Process 7

2.3 Biographies 12

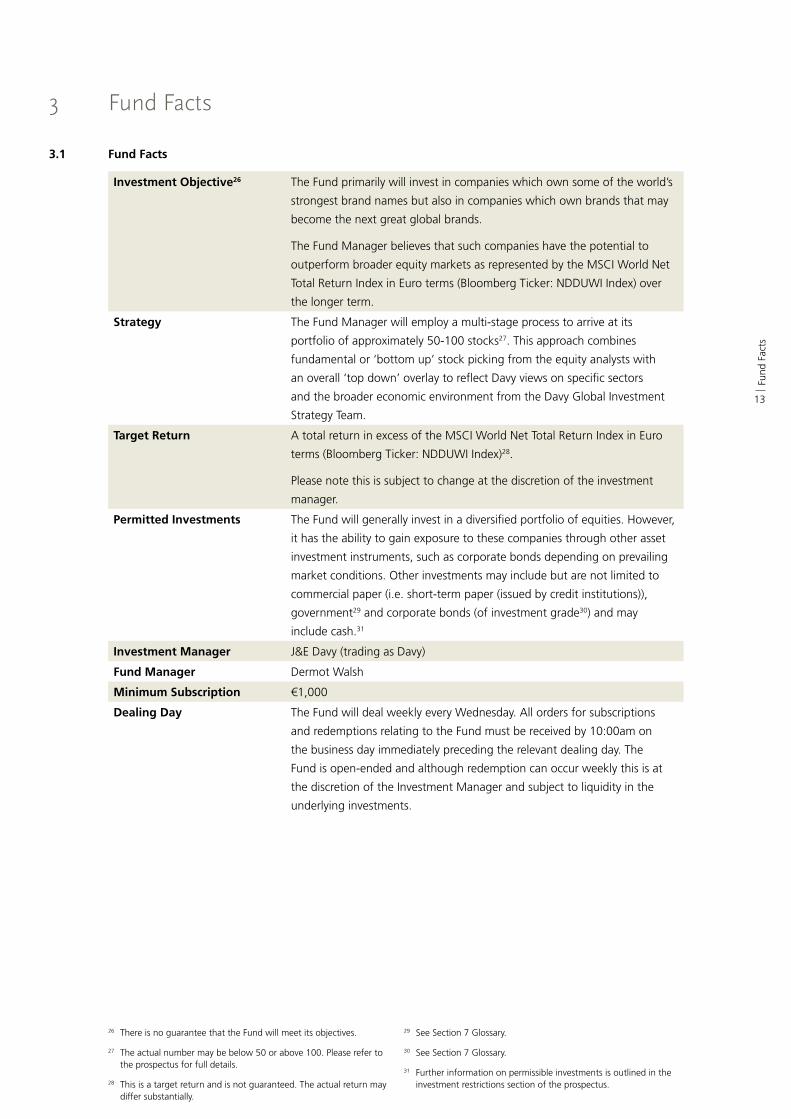

3 Fund Facts 13

3.1 Fund Facts 13

3.2 Investment Restrictions 16

4 Taxation 17

5 Risk Factors 18

6 Important Information 21

7 Glossary 23

8 Disclaimer 24

The Global Brands Equity Fund, (the “Fund”)1, will invest primarily in companies which own some of the

world’s strongest brand names but also in companies which own brands that may become the next great

global brands2.

Davy believes that such companies have the potential to outperform broader equity markets as

represented by the MSCI World Net Total Return Index in Euro terms (Bloomberg Ticker: NDDUWI Index)

over the long-term.3 Please note this is subject to change at the discretion of the investment manager.

The Davy investment team will actively manage a portfolio of 50-1004 companies which share a number of

key characteristics including:

– owning powerful global brands

– Where an increasing portion of earnings are derived from emerging markets

– that are profitable with strong balance sheets

– that have a reasonable valuation

The Fund will generally invest in a diversified portfolio of equities. However, it has the ability to gain exposure

to these companies through other investment instruments such as corporate bonds and commercial paper5

depending on prevailing market conditions.6

The Fund will offer different share classes, including accumulation units (where any dividends and/or income

are reinvested) and distributing units (where any dividends and/or income are distributed to investors).

Davy will charge 2% commission on all subscriptions to the Fund and an exit charge of 0.5% on all

redemptions out of the Fund. An annual management fee of between 0.675% and 1.35% of the net asset

value of the Fund will be deducted from the Fund’s assets dependent on the share class. For further details

on all fees, please refer to Section 3 Fund Facts.

WarnIng: the value of an investment can fall as well as rise and income may fluctuate in

accordance with market conditions. there is no guarantee that investors will receive any income

on their invested capital or their invested capital back and an investor could suffer a loss in whole

or part. as some of the underlying investments are denominated in non-Euro currencies, the Fund’s

performance may be affected by changes in exchange rates. While the Fund manager may choose

to hedge the currency exposures of the Fund, there is no guarantee that they will be successful

in doing so.

1 Summary of Investment

1 The Global Brands Equity Fund is a sub-fund of the Davy Equity Trust, an open-ended umbrella unit trust authorised in Ireland by the Central Bank of Ireland pursuant to the provisions of the Unit Trusts Act 1990. For the purposes of this document the sub-fund, Global Brands Equity Fund, will be referred to as the Fund throughout.

2 There is no guarantee that the Fund will meet its objectives.

3 See Section 7 Glossary.

4 The actual number may be below 50 or above 100. Please refer to the prospectus and supplement for full details.

5 See Section 7 Glossary.

6 The corporate bonds must be of investment grade, i.e. have an S&P rating of BBB or higher or the equivalent rating from another rating agency, such as Moody’s or Fitch.

4

Sum

mar

y of

Inve

stm

ent

2.1 Why global Brands?

The Fund will primarily invest in companies which own some of the world’s strongest brand names but also in

those companies which own brands that, in Davy’s opinion, may become the next great global brands. The Fund

will aim to give investors exposure to some of the world’s strongest and most profitable companies.

The companies chosen will have a number of common characteristics, including:

owning powerful global brands

Having an increasing portion of their earnings derived from emerging markets

that are profitable with strong balance sheets

Have a reasonable valuation

A successful brand can be a powerful driver of a company’s profitability. Customers may become attached to the

values that they feel differentiate the particular brand from its competitors. In some instances these customers

can be relatively price insensitive and the successful brand can attract a premium price.

For example, Kellogg’s can charge more than twice the price for its cornflakes than Tesco’s own brand and over

four times the price of Tesco’s Value brand.

2 Investment Opportunity

FIGURE 1: The Pricing Power of a Strong Brand

Sour

ce: m

ysup

erm

arke

t.co

.uk

as a

t 5t

h O

ctob

er 2

010

Tesco Value Cornflakes

6.2pper 100g

Tesco Cornflakes

18.8pper 100g

Kellogg’s Cornflakes

39.6pper 100g

EQUITY ANALYISTS

FIGURE 2: Investment Management Team and Process

DAVY GLOBAL INVESTMENT STRATEGY TEAM

THE FUND

Robbie Kelleher HEAD OF GLOBAL INVESTMENT STRATEGY

Ronan O’HoulihanINVESTMENT DIRECTOR

Aidan Donnelly

Declan Magee

Dermot WalshFUND MANAGER

‘BOTTOM UP’ STOCK SPECIFIC VIEWS

‘TOP DOWN’ VIEWS ON GLOBAL ECONOMY

Sour

ce: D

avy

Priv

ate

Clie

nts

FIGURE 3: Investment Process

b o t t o m u p

t o p d o w n

STOCKSELECTION

Does the company have an

Attractive Valuation?*

Does the company have a

Consistent Dividend Track Record?

Does the company have a Strong Sustained

Cash Flow?

Do the company’s sales have a Sector and

Regional mix?

Does the company have an

Attractive Business Model?

GLOBAL

TECHNIC

AL

INDIC

ATORS

SECTOR

THEMES

ECONOMICOUTLOOK

Source: Davy Price Clients

Future growth

Companies such as Coca-Cola and Kellogg’s have demonstrated a strong track record of profit growth.

Coca-Cola has grown earnings per share in 24 of the past 29 years, Kellogg’s in 17 of the past 22 years7.

The traditional U.S. and European markets for companies such as Coca-Cola are mature and have limited

opportunities for significant growth. However, the growth opportunity now appears to be stemming from

emerging markets. For example, Coca-Cola earned 35% of its 2009 revenues outside its traditional U.S. and

European markets.8

7 Source: Davy with reference to Bloomberg. 8 Source: Bloomberg.

5

Inve

stm

ent

Opp

ortu

nity

Volkswagen China promotional material for the Passat Saloon. Source: Volkswagen China

the new Consumer

In countries such as China, India and Brazil a new, wealthier consumer is emerging. These consumers have many

of the same goals and aspirations as those in the U.S. and Europe and this is reflected in their appetite for the

world’s most recognisable brands. Volkswagen, which is the market leader in its sector in China, sold 457,000

vehicles in the first three months of 2010. This is more than a quarter of Volkswagen’s total sales for the period

and by far the largest sales volume of all its global markets. It is unsurprising therefore that Volkswagen calls

China its ‘second home market’.9

Luxury goods companies are also targeting

new consumers in the emerging markets.

More than 60% of the Gucci Group’s

capital investment in 2010 is to be aimed at

expansion in Asia and in particular in China10.

Asia-Pacific, excluding Japan, accounted for

28% of Gucci Group sales in 2009, up from

16% in 200510. It’s not only Asia that the firm

is looking to for expansion opportunities.

The company is also looking at Latin

America, including Mexico, Brazil and Chile.10

Such investments are a clear signal of the

dependence of luxury goods companies such

as Gucci on emerging markets for growth.

By 2025, 8 of the 10 world’s largest cities will be in developing nations that will house an estimated 177 million

people.13 These new city dwellers, typically from rural areas, aspire to higher living standards. These aspirations

and the ability to fund them from the higher wages available in the cities should foster the demand for

branded goods.

The owners of the world’s leading brands have long recognised these developments. Yum!, which owns brands

including KFC, Taco Bell and Pizza Hut, was one of the companies to recognise this potential opportunity early.

KFC was the first fast-food restaurant chain

to enter China in 1987, the first to bring

franchising to China in 1992 and the first to

open a drive-through in China in 2002. KFC

continues to be the number one fast food -

restaurant brand and the largest and fastest

growing restaurant chain in mainland China

today, with nearly 3,000 restaurants in more

than 650 cities.15 Yum! opens nearly one new

KFC every day in mainland China.

Pizza Hut was the first restaurant chain to

introduce pizza to China in 1990 and the first

to introduce pizza delivery in 2001. Today,

there are nearly 470 Pizza Hut Casual Dining

restaurants in more than 100 cities with

an additional 104 Pizza Hut Home Service

delivery units.16

Rural customers from Gaochun County, Nanjing, the capital city of Jiangsu province China purchasing white goods under the government’s household appliance to rural customers subsidy program. Gaochun County, a predominately agricultural region outside Nanjing, has a population of 500,000. Nanjing City itself has a population of 7.4 million people and the region of Jiangsu a staggering 74.3 million people (France by comparison has a population of 62 million people).14

9 Source: www.ft.com/beyondbrics ‘China sales soar for BMW, Daimler and Audi,’ 5th May 2010.

10-12 Source: www.livetradingnews.com/gucci-heads-to-asia-10062. htm

13 Source: United Nations, Department of Economic and Social Affairs, Population Division.

14 Sources: World Bank Development Indicators, Jiansu.net, cbw.com, made-in-china.com.

15-16 Source: www.yum.com/company/china.asp as at 5th October 2010.

6

Inve

stm

ent

Opp

ortu

nity

The continued importance of China to Yum! is clear by the firm’s ambitious expansion plans.

Over time, we want to open over 20,000 restaurants and plan to expand our average unit volumes, which are high already, to even higher levels. With unit growth, same store sales growth and high returns, we’re winning BIG in China and the best is yet to come

samuel su, Chairman and CEO of Yum! Brands China Division (October 2010)17

“”

With rising living standards, products that are as in demand in Boston are increasingly in demand in

Beijing. As a result, by investing in companies which possess strong global brands, investors can gain

exposure to emerging economies which are expected to be key drivers of global economic growth.

2.2 the Investment management process

The Fund will be managed by an experienced investment team consisting of an experienced Fund

Manager supported by two equity analysts. The Fund Manager will employ a multi-stage process to

arrive at the portfolio of approximately 50-100 large-cap stocks,18 diversified by both geography and

sector. This process will combine fundamental or ‘bottom up’ stock picking views from the equity

analysts with an overall ‘top down’ overlay to reflect Davy views on specific sectors and the broader

economic environment from the Davy Global Investment Strategy Team. The Davy Global Investment

Strategy Team comprises of Robbie Kelleher and Ronan O’Houlihan.

17 Source: www.yum.com/company/china.asp as at 5th October 2010.

18 The actual number may be below 50 or above 100. Please refer to the prospectus for full details.

FIGURE 2: Investment Management Team and Process

DAVY GLOBAL INVESTMENT STRATEGY TEAM

EQUITY ANALYISTS

Robbie Kelleher HEAD OF GLOBAL INVESTMENT STRATEGY

Ronan O’HoulihanINVESTMENT DIRECTOR

Aidan DonnellyDeclan Magee

Dermot WalshFUND MANAGER

Sour

ce: D

avy

Priv

ate

Clie

nts

FIGURE 2: Investment Management Team and Process

Source: Davy Private Clients

‘bottom up’ stock specific views

‘top down’ views on global economy

b o t t o m u p

t o p d o w n

Ronan O’HoulihanINVESTMENT DIRECTOR

Robbie Kelleher HEAD OF GLOBAL

INVESTMENT STRATEGY

DAVY GLOBAL INVESTMENT STRATEGY TEAM

Declan Magee Aidan Donnelly

EQUITY ANALYISTS

Dermot WalshFUND MANAGER

‘to

p dow

n’ v

iew

s o

n g

loba

l ec

onomy

‘bottom u

p’ stock specific views

EquIty analysts

7

Inve

stm

ent

Opp

ortu

nity

stock selection process – a Fundamental ‘Bottom up’ approach

The Fund Manager looks at companies on an individual basis to determine if a company is an attractive

investment opportunity. The Fund Manager will seek to identify individual companies with good revaluation

potential that may not be recognised by the market at large and therefore are expected to appreciate in value.

The stocks in the portfolio will be biased towards large capitalisation19 names in each sector of the MSCI World

Net Total Return Index in Euros. The Fund can also invest in smaller cap20 stocks that may not be held in the

Index where the Fund Manager believes it is appropriate.

In selecting individual companies for investment, the following factors will be considered:

Does the company own powerful globally recognised brands?

Is it focused on long-term shareholder value creation?

Does it have an experienced and effective management team?

Does it have an effective research, product development and marketing department?

Is it undervalued allowing for its historic values, geographical area, industry sector or its intrinsic value?

Does the company have competitive advantages?

Does the company have a strong financial position, has it stable or improving credit quality and has it historically provided returns on capital?

Is the company attractively priced relative to its future earnings power and expected dividend-paying capability?

Are there other technical and sentiment factors affecting the company’s share price? The interpretation of market activity using technical analysis provides clues as to the future behaviour of the stock price. Sentiment

towards a stock can also drive future price moves.

WarnIng: please note the factors listed are neither comprehensive nor exhaustive. there may be

other factors that may influence the selection of an individual stock.

Forming regional/sector Views – a ‘top Down’ approach

By spreading the Fund’s investments across a range of international markets, the Fund aims to reduce volatility

compared to an investment in a single region. In allocating assets among regions and sectors the Fund Manager

will take a ‘top down’ approach, focusing on economic, political and fundamental factors that may include:

Expected relative economic growth outlook between regions

Low or decelerating inflation which creates a favourable environment for securities markets

Stable governments with policies that encourage economic growth, equity investment and development of

securities markets

The impact of the local currency relative to the Euro

Likely sector rotation over the mid-term21

The historical valuation of the sector coupled with its earnings growth potential

WarnIng: please note the factors listed are neither comprehensive nor exhaustive. there may be

other factors that may influence the selection of an individual stock.

19 Large-cap companies typically have a market capitalisation in excess of €5 billion. See Section 7 Glossary.

20 Small-cap equities typically have a market capitalisation of between €250 million and €1.5 billion. See Section 7 Glossary.

21 See Section 7 Glossary.

8

Inve

stm

ent

Opp

ortu

nity

FIGURE 3: Investment Process

b o t t o m u p

t o p d o w n

STOCKSELECTION

Source: Davy Private Clients

b o t t o m u p

t o p d o w n

STOCKSELECTION

GLOBAL

TECHNIC

AL

INDIC

ATORSSECTOR

THEMES

ECONOMICOUTLOOK

Does the company have an

Attractive Valuation?*

Does the company have a

Consistent Dividend Track Record?

Does the company have a Strong Sustained

Cash Flow?

Do the company’s sales have a Sector and

Regional mix?

Does the company have an

Attractive Business Model?

Does the company have an Attractive Valuation?*

Does the company have a

Consistent Dividend Track Record? Does the

company have a Strong Sustained

Cash Flow?

Do the company’s sales have a Sector and

Regional mix?

Does the company have an Attractive

Business Model?

GLOBAL

ECONOMICOUTLOOK

TECH

NIC

ALIN

DIC

ATO

RS

SECTOR

THEM

ES

WarnIng: please note the factors listed are neither comprehensive nor exhaustive. there may be

other factors that may influence the investment process.

* See Section 7 Glossary.

9

Inve

stm

ent

Opp

ortu

nity

additional Filters

Once the Fund Manager has arrived at a universe of stocks from which a portfolio will be chosen, a number of

filters to choose the final portfolio will be applied as follows:

a Each of the companies in the portfolio must own at least one or more leading global consumers

focused brands or a brand that has a global presence or the potential to have a global presence.

RatIoNale: Companies with strong brands have a sustainable competitive advantage as it’s often difficult

to re-create or duplicate a well-known brand. Strong brand recognition tends to be driven by innovation

(apple), advertising, customer loyalty, copyrights and distribution networks. Physical assets such as factories

are more easily replicated which leads to price competition and therefore reduced profits. While it’s easy to

build a bottling plant how does one create a brand like Coca-Cola, the world’s number one brand for the

past nine years22?

taBlE 1: Examples of Brand ownership by sector

22 Source: Interbrand Best Global Brands 2009.

Household goods Colgate PalmoliveProctor & Gamble reckitt benckiser Kimberly-Clark

Foods®

unilever

®®

danone

Beverages PepsiCoCoca-Cola Pernod ricard diageo

personal Care beiersdorf l’oréal

Financials MasterCard

Internet ebay

restaurants yum! brands Mcdonalds

luxury lVMH richemont

sports Clothing nike adidas

Sour

ce: D

avy

Priv

ate

Clie

nts

with

ref

eren

ce t

o Bl

oom

berg

and

Inte

rbra

nd.

10

Inve

stm

ent

Opp

ortu

nity

B the companies must derive a high (and growing) proportion of their revenues from

emerging markets.

RatIoNale: the traditional markets of companies such as Coca-Cola have matured with limited

opportunities for further growth. Many companies with strong brands have been successful in tapping the

faster growth from the rise of the consumer in emerging markets.

taBlE 2: Emerging market contribution to revenue and earnings for a sample of companies

rEVEnuEs EarnIngs

Company 2009 groWtH ratEs 2009 groWtH ratEs

% 1yr 3yr 5yr % 1yr 3yr 5yr

1 reckitt Benckiser 19% 25% 19% 18% 11% 33% 31% 39%

2 procter & gamble 32% 1% 13% 19% - - - -

3 Kimberly-Clark 32% 3% 11% 12% 30% 14% 15% 15%

4 Colgate palmolive 46% 3% 12% 12% 48% 22% 20% 18%

5 unilever 37% 3% 11% 9% 30% 13% 13% 13%

6 Danone 40% 9% 2% 12% 37% 67% 11% 5%

7 Coca-Cola 35% 1% 9% 8% 58% -1% 9% 6%

8 pernod ricard 30% 7% 27% - 28% 14% 39% -

9 Diageo 44% 15% 13% - 31% 6% 8% -

10 pepsiCo 39% 3% 16% 16% - - - -

11 Beiersdorf 20% 8% 19% 17% 5% -3% -7% -7%

12 l’oréal 31% 13% 14% - 34% 14% 29% -

13 masterCard 54% 5% 21% 21% - - - -

14 eBay 29% 12% 50% - - - - -

15 yum! Brands 34% 18% 31% 27% 34% 28% 27% 24%

16 mcDonalds 19% 3% 12% 10% 14% 21% 40% 38%

17 lVmH 32% 9% 13% 14% - - - -

18 richemont 29% 19% 19% 17% - - - -

19 nike 24% 14% 16% - 35% 20% 24% -

20 adidas 35% 2% 13% 21% - - - -

* the geographic classification of revenues and earnings varies by company. For the most part emerging market revenues are those other than U.S. and europe and where shown separately other developed markets e.g. Japan, australia and Canada.

WarnIng: past performance is not a reliable guide to future performance. the value of an

investment can fall as well as rise and income may fluctuate in accordance with market conditions.

there is no guarantee that investors will receive any income on their invested capital or their invested

capital back and an investor could suffer a loss in whole or part

C the majority of companies must have been profitable every year for the last 5 years and have low

levels of debt.

RatIoNale: the Fund will look to invest in profitable companies which have demonstrated ability to

create value for shareholders. the Fund Manager will look for companies that have a number of desirable

characteristics such as a high return on invested capital (RoIC)23 which have recurring revenues at high profit

margins and those that do not have excessive levels of debt.

Sour

ce: D

avy

with

ref

eren

ce t

o Bl

oom

berg

23 See Section 7 Glossary.

11

Inve

stm

ent

Opp

ortu

nity

Companies with a demonstrated record of sustainable profitability tend to have stable demand for their

goods and services and are therefore typically less sensitive to economic conditions. Companies with lower

levels of debt are typically better able to weather turbulent economic times with the valuations of such

companies being more resilient than those of other more highly indebted companies.

D reasonable valuations

all companies have a forecast 2010 p/E ratio24 of <20.

RatIoNale: While the Fund aims to invest in good companies it will seek to do so at reasonable

valuations. the Fund will therefore typically invest in companies which have a P/e ratio of less than 20.

2.3 Biographies

THE FUND MANAGER

Dermot Walsh

Dermot joined Davy Private Clients from Focus Investments25, where he was Investment Manager, Executive Director and a founding shareholder of the company. He was previously Head of the Investment Services Division in Davy. Prior to joining Davy he worked with Guinness & Mahon Bank, initially as an investment manager and subsequently as a Director of Investment Services. Dermot holds a BA Degree in Economics from Trinity College, Dublin and a MBS in Banking and Finance from University College Dublin. He is also a Registered Stockbroker and a member of the Securities Institute.

THE GLOBAL INVESTMENT STRATEGY TEAM

robbie Kelleher Head of Global Investment Strategy: Robbie has worked in the investment business in Dublin for more than

thirty years. He joined Davy in 1981, having previously worked as an investment manager with Irish Life and an economist with the Central Bank. In Davy he established the consultancy business DKM, worked as a bond economist in the mid 1980s and was in charge of the institutional research division for twenty years. He has been ranked as a top equity strategist and economist in institutional surveys. He joined the Private Clients division in 2008.

ronan o’Houlihan Investment Director: Ronan has worked in the investment industry for more than 20 years. He was an

investment manager with Hibernian Investment Managers, AIB Investment Managers and was an original shareholder in Montgomery Govett. Ronan has managed Irish, Japanese and other Asian equities and set up Ireland’s first ever Latin-American fund in 1994. Ronan specialises in asset allocation and investment strategy.

THE EQUITY ANALYSTS

Declan magee Declan has 22 years of investment experience. He joined Davy in 2009 having previously worked as a European

Fund Manager with Focus Investments. Prior to that Declan worked as an equity analyst with international fund management firms Pioneer Investments and ABN Amro in Dublin, London and Hong Kong.

aidan Donnelly

Aidan has 15 years investment experience. He joined Davy in 2005 from AIB Investment Managers where he

worked as a Fund Manager, specialising in UK and U.S. equities.

24 The P/E ratio of an equity is a measure of the price paid for the equity relative to the annual net income or profit earned by the firm per share. See Section 7 Glossary.

25 Focus Investments is subsidiary of J&E Davy Holdings (the parent company).

12

Inve

stm

ent

Opp

ortu

nity

3.1 Fund Facts

Investment objective26 The Fund primarily will invest in companies which own some of the world’s

strongest brand names but also in companies which own brands that may

become the next great global brands.

The Fund Manager believes that such companies have the potential to

outperform broader equity markets as represented by the MSCI World Net

Total Return Index in Euro terms (Bloomberg Ticker: NDDUWI Index) over

the longer term.

strategy The Fund Manager will employ a multi-stage process to arrive at its

portfolio of approximately 50-100 stocks27. This approach combines

fundamental or ‘bottom up’ stock picking from the equity analysts with

an overall ‘top down’ overlay to reflect Davy views on specific sectors

and the broader economic environment from the Davy Global Investment

Strategy Team.

target return A total return in excess of the MSCI World Net Total Return Index in Euro

terms (Bloomberg Ticker: NDDUWI Index)28.

Please note this is subject to change at the discretion of the investment

manager.

permitted Investments The Fund will generally invest in a diversified portfolio of equities. However,

it has the ability to gain exposure to these companies through other asset

investment instruments, such as corporate bonds depending on prevailing

market conditions. Other investments may include but are not limited to

commercial paper (i.e. short-term paper (issued by credit institutions)),

government29 and corporate bonds (of investment grade30) and may

include cash.31

Investment manager J&E Davy (trading as Davy)

Fund manager Dermot Walsh

minimum subscription €1,000

Dealing Day The Fund will deal weekly every Wednesday. All orders for subscriptions

and redemptions relating to the Fund must be received by 10:00am on

the business day immediately preceding the relevant dealing day. The

Fund is open-ended and although redemption can occur weekly this is at

the discretion of the Investment Manager and subject to liquidity in the

underlying investments.

3 Fund Facts

26 There is no guarantee that the Fund will meet its objectives.

27 The actual number may be below 50 or above 100. Please refer to the prospectus for full details.

28 This is a target return and is not guaranteed. The actual return may differ substantially.

29 See Section 7 Glossary.

30 See Section 7 Glossary.

31 Further information on permissible investments is outlined in the investment restrictions section of the prospectus.

13

Fund

Fac

ts

Davy will offer both accumulating and distributing units for both Class A and Class B Units:

Accumulating units will be non-distributing with all net dividend income and any gains being accumulated

within the Fund.

Distributing units will aim to make semi-annual distributions of dividends.32

WarnIng: Investors should note that the Fund can invest in equities which are not Euro

denominated. the performance of the Fund may therefore be impacted by changes in exchange

rates. While the Fund manager may choose to hedge the currency exposures of the Fund there is no

guarantee that they will be successful in doing so.

summary of Classes

Class a accumulating units

Class A - Accumulating units will be non-distributing with all net dividend income reinvested as

received. Any gains are also accumulated within the Fund.

Class a Distributing units

Class A - Distributing units will aim to make semi-annual distributions of dividends.

Class B accumulating units

Class B - Accumulating units will be non-distributing with all net dividend income reinvested as

received. Any gains are also accumulated within the Fund.

Class B Distributing units

Class B - Distributing units will aim to make semi-annual distributions of dividends.33

32 The payment and size of a semi-annual distribution is at the discretion of the investment manager. It is not guaranteed and may be zero.

33 The payment and size of a semi-annual distribution is at the discretion of the investment manager. It is not guaranteed and may be zero

Davy will offer Euro denominated Class A and Class B Units.

Class A Units are offered to clients with Discretionary or Advisory service level agreements with Davy and

who pay portfolio management fees. Class A Units have a lower annual management fee to account for

the Davy Portfolio Management fees which are charged separately and on an ongoing basis.

Class B Units are offered to all investors. The Class B Units have a higher annual management fee than

the Class A Units.

WarnIng: the classes of units offered are at the sole discretion of the Investment manager.

Classes of units

14

Fund

Fac

ts

Distribution Dates The distributing classes will distribute net income and gains, if any, semi-

annually. Distributions will be declared on the Distribution Date (usually the

30th June and the 31st December) and will be normally paid on or before the

14th Business Day following the Distribution Date. The payment and size of

a semi-annual distribution is at the discretion of the investment manager. It is

not guaranteed and may be zero.

net asset Value The Fund will be valued at the close of business each Wednesday34. From

this valuation the units are priced and will be updated on Davy’s website

each Thursday.

Commission Davy will charge a 2% commission on any subscription for units and a 0.5%

exit charge on any redemptions of units.35

Fund annual management

Fee

Class A Units will attract an annual management fee of 0.675% of the net

asset value of the Fund, which will be accrued weekly and paid monthly in

arrears out of the assets of the Fund.

Classs B Units will attract an annual management fee of 1.35% of the net

asset value of the Fund, which will be accrued weekly and paid monthly in

arrears out of the assets of the Fund.

operational administration

Fees & trustees Fees

The Fund will be liable for certain fees, expenses and disbursements related

to the provision of these services. Please see Page 33 of the prospectus and

Pages 3-4 of the supplement for additional information.

Fund structure The Fund is a sub-fund of the Davy Equity Trust, an open-ended umbrella unit

trust authorised and regulated by the Irish Central Bank of Ireland, pursuant

to the provisions of the Unit Trusts Act 1990. Authorisation by the Central

Bank of Ireland is not an endorsement of the Fund and does not constitute a

guarantee or a warranty as to the performance of the Fund. This Information

Memorandum has not been reviewed or approved by the Central Bank of

Ireland.

taxation See Section 4 Taxation.

34 If the valuation day falls on a non-business day the valuation day will be the immediately preceding business day.

35 Advisory and Discretionary clients should note that a Davy Portfolio Management Fee is payable on the funds under management held in your Davy account which is charged separately and on an ongoing basis. Execution Only clients will be subject to a nominee charge of €40 semi-annually. Please refer to your terms and conditions for more details.

15

Fund

Fac

ts

3.2 Investment restrictions

The Fund has a number of investment restrictions placed upon it as outlined below. Please refer to the

prospectus for full details.

The Fund may not invest more than 10% of its net assets in securities which are not traded in or dealt on a

Recognised Exchange.

The Fund may not invest more than 10% of its net assets in securities issued by a single issuer.

The Fund may acquire the units of other Investment Funds subject to the following:

- the Fund may not invest more than 20% of its net assets in Regulated Funds;

- where the Fund invests in units of Investment Funds managed by the same management company or by

an associated or related company, the manager of the scheme in which the investment is being made

must waive the preliminary/initial charge which it is entitled to charge for its own account in relation to

the acquisition of units;

- where a commission is received by the Manager of the Fund by virtue of an investment in the units of

Investment Funds this commission must be paid into the property of the Fund;

- the Fund may not invest more than 10% of its net assets in Unregulated Funds.

No more than 10% of the Fund’s net assets may be kept on deposit with any one institution. This limit

is increased to 30% in certain circumstances as outlined in the Investment Restrictions Section of the

prospectus which is available on request.

The Fund may not hold more than 10% of any class of security issued by any single issuer.

The Investment Manager acting in connection with all of the schemes which it manages may not acquire any

shares carrying voting rights which would enable it to exercise significant influence over the management of

an issuing body.

The Fund may hold ancillary liquid assets; and

The Fund may, subject to authorisation by the Central Bank of Ireland invest up to 100% of its net assets in

transferable securities issued or guaranteed by any State, its constituent states, its local authorities, or public

international bodies of which one or more States are members.

Borrowings

The Investment Manager shall have the power from time to time to borrow for the account of a fund from

bankers and other lenders sums not exceeding 25% of the net asset value of the Fund provided such borrowing

is on a temporary basis and the Trustee36 has given its prior consent to such borrowings. (For more information

please see page 16 of the prospectus ‘Borrowings’).

36 See Section 7 Glossary.

16

Fund

Fac

ts

For Irish resident Investors

WarnIng: this information is provided for Irish resident investors only and is based on our

understanding of Irish tax legislation and the known current revenue interpretation thereof. this

can vary according to individual circumstances and is subject to change without notice, including

retrospectively. It is intended as a guide only and not a substitute for professional advice. this

information is not applicable to uK resident clients. you should consult the ‘taxation’ section of the

prospectus for additional information as well as your tax advisor for the rules that apply in your

individual circumstances.

It is our current understanding that an investment in the Fund operates on what is known as a ‘gross roll-up’

taxation basis. This means that there are no income or capital gains taxes incurred on investment earnings

generated within the Fund. This enables the Fund to add to its value by reinvesting any income and gains

without any deductions for tax.

tax rates37

Table 3 below outlines the current Irish taxation rates applicable to the Fund in the case of redemptions from the

Fund or deemed disposals.

taBlE 3: taxation rates for Irish resident Investors

type of Irish Investor taxation rates on gains

Irish Tax Resident Individual 28%

Irish Tax Resident Corporate 28%

Source: the Revenue Commissioners

Capital losses on disposal cannot be used to shelter capital gains from other investments and investors should

note that health levies will apply to any annual and non-annual income distributions received by Irish resident

individuals from the Fund.

Irish Exempt Investors

Some investors may be exempt from tax. They include Irish resident pension schemes and charities which are

approved by the Revenue and have completed the relevant revenue declaration. (Please note that there is no

provision for a refund of tax in cases where tax has been withheld from the proceeds of a sale and the investor

has not made the relevant declaration as an exempted investor).

8-year Deemed Disposal rule

A liability to tax currently applies to Irish individual investors and Irish corporate investors on the ending of the

eighth anniversary of their acquisition of an interest in the Fund and each subsequent 8-year period beginning

when the previous one ended. The tax is payable on any unrealised uplift in the value of the investment at that

date. Where the investment is subsequently sold, the amount of tax paid under this 8-year rule is treated as a

payment on account in respect of any further tax due.

Deemed Disposals

Where an investor dies while holding a material interest in the Fund, this event gives rise to a deemed disposal

of the investment at market value at that point in time. Any taxable gain arising on this deemed disposal event is

liable to Irish tax currently at a rate of 28%.

non-residents

Different rules may apply in the case of certain non-residents. For more details, please consult your tax advisor.

4 Taxation

37 Rates correct as of 30th September 2010; these rates may be subject to change. Investors should consult their own tax advisor for the rules that apply in their own individual circumstances.

17

Taxa

tion

WarnIng: the following is a list of some of the important risks factors that prospective investors

should consider prior to making a decision to invest in the Fund. the list is not intended to be

comprehensive or exhaustive. Various other risks may also apply. you should read the complete list of

risks contained in the full prospectus and supplement. terms not defined herein shall have the same

meaning as they do in the prospectus.

no assurance of Investment return

The Fund is an equity market based investment and therefore carries with it a high degree of risk. There is no

guarantee that the shares in which the Fund invests will achieve results comparable to those achieved in the

past, that targeted performance will be met or that capital will be returned to investors. Investors may not

recoup the original amount they invest in the Fund. Investors should note that there is no guarantee the Fund

will meets its objectives.

Economic, social and political risks

As a result of the broad geographic investment mandate of the Fund it is possible that the Fund will invest in

regions or countries that are considered to be developing markets. Investments in such countries may be subject

to potentially higher economic, social and political risks than investments in developed countries.

Currency risk

The Fund may invest in shares which are not Euro denominated. This means they carry a risk related to currency.

In some cases, investments may be Euro denominated, but the underlying equities may themselves be subject to

exchange rate and currency fluctuations and risks. Any currency fluctuations may affect the Fund’s return in Euro

terms. The Fund Manager may enter into hedging transactions at its sole discretion and solely for the purposes

of efficient fund management.

Non-Euro based investors should note that this is a Euro denominated fund and that changes in the Euro

exchange rates relative to non-Euro currencies, including sterling will affect returns in their base currency.

use of Derivative Instruments

The Fund may invest in derivative instruments. The types and degrees of risk vary depending upon the

characteristics of the particular instrument and the assets of the relevant fund as a whole. Use of these

instruments may entail investment exposures that are greater than their cost would suggest, meaning that a

small investment in derivatives could have a large impact on a fund’s performance.

Each fund may have credit exposure (i.e. credit risk) to counterparties by virtue of an investment position in

swaps, options, forward exchange rate and other derivative contracts held by the Fund. To the extent that a

counterparty defaults on its obligation and the Fund is delayed or prevented from exercising its rights with

respect to the investments in its portfolio, it may experience a decline in the value of its position, lose income

and incur costs associated with asserting its rights.

The use of futures and futures options also involves risks; including the potential for losses in excess of the

amount invested in the futures contract. There can be no guarantee that there will be a correlation between

price movements in the instruments used and the securities of the Fund that are being hedged through the

use of the instrument. Moreover, there are significant differences between the securities and futures markets

that could result in imperfect correlation between the markets, causing the use of a particular technique not

to achieve its intended objective. The degree of imperfection of correlation depends upon circumstances such

as variations in speculative market demand and differences between financial instruments being hedged and

instruments underlying the standard contracts available for trading in such respects as interest rate levels,

maturities and creditworthiness of issuers. A decision as to whether, when and how to hedge involves exercise

of skill and judgement and even a well conceived hedge may be unsuccessful to some degree because of market

behaviour or unexpected interest trends.

5 Risk Factors

18

Risk

Fac

tors

Futures exchanges may limit the amount of fluctuation permitted in certain futures contract prices during a

single trading day. The daily limit establishes the maximum amount that the price of a futures contract may vary,

either up or down, from the previous day’s settlement price at the end of the current trading session. Once the

daily limit has been reached in a futures contract subject to such a limit, no more trades may be made on that

day at a price beyond that limit. The daily limit governs only price movements during a particular trading day

and therefore does not limit potential losses because the limit may work to prevent a liquidation of unfavourable

positions.

In addition, the ability to establish and close out a position in options and futures contacts will be subject to the

development and maintenance of a liquid market in the options. There can be no assurance that a liquid market

on an exchange would exist for any particular option or for any particular time.

Use of forward currency contracts as a method of protecting the value of the Fund assets against a decline in

a value of a currency, establishes a rate of exchange which can be achieved at some future point in time, but

does not eliminate fluctuations in the underlying prices of securities. Use of forward currency contracts may also

reduce any potential gain which may have otherwise occurred had the currency value increased more above

the settlement price of the contract. Successful use of forward contracts depends on the Fund Manager’s skill

in analysing or predicting relevant currency values. Forward contracts alter the Fund’s exposure to currency

exchange varied activity and could result in losses to the Fund in the event that the currencies do not perform in

the manner that the Fund Manager anticipated. The Fund may also incur significant cost from converting assets

from one currency to another.

Investments in Emerging markets

Emerging markets with emerging economies or stock markets may lack the social, political, economic and

regulatory stability characteristic of more developed countries. .As a result, the risks from investing in those

countries, including the risks of nationalisation, expropriation and repatriation of assets, may be heightened.

In addition, unanticipated political or social developments may affect the values of a Fund’s investments in

those countries and the availability to the Fund of additional investments in those countries. The small size and

inexperience of the securities markets in some of these countries and the limited volume of trading in securities

in these countries may make a fund’s investments in such countries illiquid and more volatile than investments

in more established markets. There may be little financial or accounting information available with respect to

issuers located in some of these countries and it may be difficult as a result to assess the value or prospects of an

investment in such issuers.

settlement and Clearing risk

The trading and settlement practices on some of the Recognised Exchanges on which a fund may invest may not

be the same as those in more developed markets of western Europe and the United States. In particular, some

or all of the following additional risks may be associated with settlement and clearing of securities transactions

in emerging markets. These additional risks include but are not limited to delays experienced in repatriation of

sales proceeds due to local exchange controls, an uncertain legal and regulatory environment and the possibility

that transactions may be settled by a free delivery of stock with payment of cash in an uncollateralised manner.

That may increase settlement and clearing risk and/or result in delays in realising investments made by the

relevant fund.

Custody risk

Local custody services in some of the market countries in which the Fund may invest may not be the same as

those in more developed market countries and there is a transaction and custody risk involved in dealing in such

markets, for which the Trustee will have no liability.

Diversification risk

While diversification is an objective of the Fund, there is no assurance as to the degree of diversification that will

actually be achieved. The Fund may invest in a limited number of investments and as such, the performance of a

single investment may have a substantial impact on the overall performance of the Fund.

19

Risk

Fac

tors

tax risk

The information contained herein is based on our understanding of tax legislation and the current interpretation

thereof, and is subject to change without notice. It is intended as a guide only and not as a substitute

for professional advice. You should consult your tax adviser about the rules that apply in your individual

circumstances.

market risk

Some of the Recognised Exchanges on which a fund may invest may prove to be illiquid, insufficiently liquid

or highly volatile from time to time. This may affect the price at which a fund may liquidate positions to meet

redemption requests or other funding requirements.

liquidity risk

The Fund may invest in shares of companies listed on markets which are less liquid and more volatile than the

world’s leading stock markets and this may result in greater fluctuations in the price of units of the Fund. There

can be no assurance that there will be any market for an investment acquired in an emerging market and such

lack of liquidity may adversely affect the value or ease of disposal of such investments.

Credit / Issuer risk

The Fund could lose money if the issuer or guarantor of a fixed income security, or the counterparty to a

derivatives contract, is unable or unwilling to make timely principal and/or interest payments, or to otherwise

honor its obligations. Securities are subject to varying degrees of credit risk, which in the case of fixed income

instruments are reflected in credit ratings.

Valuation risk

Where the Fund Manager of a Portfolio, at the request of the Investment Manager, values investments which are

not listed, quoted or dealt in on a Recognised Exchange, there may be an inherent conflict of interest between

the involvement of the Investment Manager in determining the valuation price of the Fund’s investments and the

Investment Manager’s other responsibilities.

Industry risk

While the Fund intends to be well diversified, it may invest in equities of different corporations in the same

industry. Industry risk refers to factors specific to a particular industry that may affect the performance of all or

the majority of companies in the industry.

Foreign Investment risk

A fund can invest globally. A fund that invests in foreign securities may experience more rapid and extreme

changes in value. The value of the Fund’s assets may be affected by uncertainties such as international political

developments, changes in government policies, changes in taxation, restrictions on foreign investment and

currency repatriation, currency fluctuations and other developments in the laws and regulations of countries in

which investment may be made.

20

Risk

Fac

tors

Eligibility

Units may be held by individuals, charities, corporate entities, pension schemes and partnerships (with the

exception as set out in excluded investors below). All investments will be registered in the name of a nominee

company of the Davy Group.

Excluded Investors

Units cannot be offered in the United States or to any U.S. citizen. Applicants will be required to certify that they

are not U.S. citizens.

redemption limits

Davy may refuse to encash units if total requested encashment on any one dealing day exceeds 10 per cent of

the total number of units in issue. In such cases, requests for repurchases will be held over until the next dealing

day. Please refer to the prospectus for further details.

suspension of the Fund

The manager may temporarily suspend the calculation of the net asset value and the issue and redemption

of units of the Fund. The conditions under which the temporary calculation of the net asset value may be

suspended are outlined in the prospectus, which is available on request.

legal structure

The Fund is a sub-fund of the Davy Equity Trust, an open-ended umbrella unit trust authorised and regulated

by the Irish Central Bank of Ireland. Subscriptions may only be based on the current prospectus, supplement

and together (where applicable) with the most recent annual report and (if issued after such a report) the most

recent semi-annual report. A copy of the prospectus, supplement and reports where issued may be obtained free

of charge from Davy or the administrator of the Fund.

switching

Republic of Ireland investors will be permitted to switch at no charge between the Global Brands Equity Fund

and other funds which are under the Davy Equity Unit Trust, a list of which is available in the Fund prospectus.

It is our current understanding that switching between funds of the Davy Equity Trust does not under current

legislation constitute a taxable event. Advisory and discretionary clients can get further information on switching

from your Portfolio Manager, execution only clients should contact the Davy Telephone Share Dealing Desk.

Davy will not charge a fee for switches between different classes of unit of the same fund.

Investors should note that Davy reserves the right to switch clients between unit classes of the

same fund in the event that they no longer meet the criteria for holding a specific class of unit.

Conflicts of Interest

Investors should be aware that the Directors of the Manager (Davy International Financial Services) are also the

Directors of the Investment Manager and the Distributor (J&E Davy); both companies are part of the J&E Davy

Holdings Group. Further information in relation to the management of this conflict is available upon request.

The Fund Manager, Investment Manager, Trustee, Administrator, Distributor and their respective affiliates,

officers and shareholders (collectively the ‘Parties’) are or may be involved in other financial, investment and

professional activities which may on occasion cause conflict of interest with the management of a fund. These

include management of other funds, purchases and sales of securities, investment and management counselling,

brokerage services, trustee and custodial services and serving as directors, officers, advisers or agents of other

funds or other companies, including companies in which the Fund may invest. In particular, it is envisaged that

the Fund Manager and Investment Manager may be involved in managing or advising on the investments of

other investment funds which may have similar or overlapping investment objectives to or with the Fund. Each

of the Parties will respectively ensure that the performance of their respective duties will not be impaired by any

such involvement that they might have. In the event that a conflict of interest does arise, the directors of the

6 Important Information

21

Impo

rtan

t In

form

atio

n

manager shall endeavour to ensure that it is resolved fairly and in the interests of unitholders.

The Parties may engage in transactions with a fund where any one or more of the Parties is acting in the

capacity as principal or as agent, provided that such transactions are carried out on terms similar to those

which would apply in a like transaction between parties not connected with the Parties or any one of them and

that such transactions are carried out on normal commercial terms negotiated at arms length and in the best

interests of the unitholders.

Connected Party Transactions permitted are subject to:

a certified valuation of a transaction by a person approved by the Trustee as independent and competent; or

the transaction is executed on best terms reasonably obtainable on an organised investment exchange in

accordance with the rules of such exchange; or

where (a) and (b) are not practical, execution on terms which the Trustee is satisfied conforms with the

principle outlined in the preceding paragraphs.

22

Impo

rtan

t In

form

atio

n

Commercial paper: an unsecured obligation issued

by a corporation or bank to finance its short-term

credit needs. Maturities typically range from 2 to 270

days. Commercial paper is usually issued by companies

with high credit ratings, meaning that the investment

is almost always relatively low risk compared to

other investments.

Corporate Bond: When you invest in a corporate

bond, the corporation pays you interest on the bonds

you own. at a stated date in the future (maturity

date), the company returns your principal to you. the

maturity dates on corporate bonds can range from

one to 40 years.

government Bond: a bond issued by a government.

Such bonds usually have the highest credit ratings.

Investment grade: a bond or other fixed income

instrument which has a credit ratings of BBB/Baa (S&P/

Moody’s) or above.

large-Cap: Companies are typically categorised into

large-cap, mid-cap and small-cap. the capitalisation

refers to market value and is a measure of the size

of a company. It is calculated as the share price times

the number of shares outstanding. large-cap equities

typically have a market capitalisation in excess of

€5 billion.

p/E ratio: the P/e ratio (price-to-earnings ratio) of

a stock (also called its ‘P/e’, or simply ‘multiple’) is a

measure of the price paid for a share relative to the

annual net income or profit earned by the company

per share. It is a financial ratio used for valuation: a

higher P/e ratio means that investors are paying more

for each unit of net income, so the stock is more

expensive compared to one with lower P/e ratio.

return on Invested Capital (roIC): a measure of

how efficiently the company uses the money invested

in the firm’s operations.

sector rotation: Sector rotation involves shifting

investments from one sector of the economy to

another, e.g. from healthcare to industrials. Not all

sectors of the economy perform well at the same

time. Sector rotation is a portfolio manager’s attempt

to profit through timing a particular economic cycle.

small-Cap: Small-cap stocks are those with a relatively

small market capitalisation. the definition of small-

cap can vary, but generally it is a company with a

market capitalisation of between €250 million and

€1.5 billion.

total return: the total return on an investment

takes into account not only the capital appreciation

on the portfolio, but also any income such as

dividends received.

trustee: a trustee assumes legal responsibility for the

proper administration of the Fund. It is legally obliged

to investigate claims against the Fund and opposes

invalid claims in court and to seek legal counsel

when needed.

Value Investing: this is the strategy of selecting

stocks that trade for less than their intrinsic value.

Value investors actively seek stocks of companies

that they believe the market has undervalued.

they believe the market overreacts to good and

bad news, resulting in stock price movements that

do not correspond with the company’s long-term

fundamentals. the result is an opportunity for

value investors to profit by buying when the price

is deflated.

7 Glossary

23

Glo

ssar

y

This Information Memorandum has been issued by

Davy and is provided on a confidential basis, to and

for use solely by those parties who have expressed

an interest in the Global Brands Equity Fund (the

‘Investment’ or the ‘fund’), for the purpose of

providing certain information about the Investment.

The information contained herein does not purport

to be comprehensive, all inclusive or to contain all

of the information that a prospective investor might

reasonably require in considering the Investment. It is

strictly for information purposes only. Investors should

request a copy of the Fund prospectus (including

the relevant supplement and simplified prospectus,

together the ‘prospectus’) prior to making a decision

to invest.

The information contained in this Information

Memorandum is not Investment research or a research

recommendation for the purposes of regulations.

The Information Memorandum does not constitute

an offer for the purchase or sale of any financial

instruments, trading strategy, product or service. No

one receiving this Information Memorandum should

treat any of its contents as constituting advice. It does

not take into account the investment objectives or

financial situation of any particular person. Prospective

investors are advised to make their own independent

commercial assessment of the information contained

herein and obtain independent professional advice

(including inter alia legal, financial and tax advice)

suitable to their own individual circumstances, before

making an investment decision and only make

such decisions on the basis of their own objectives,

experience and resources. Interested parties are

not entitled to rely on any information or opinions

contained in this Information Memorandum or the

fact of its distribution for the purpose of making any

investment decision or entering into any contract or

agreement with Davy in relation to the investment.

Before making investments in collective investment

schemes, investors should obtain and carefully read

the relevant prospectus, which contain additional

information needed to evaluate the investment

and which provide important disclosures regarding

risks, fees and expenses. In the event of any conflict

or inconsistency between the information, views

and opinions in this Information Memorandum, in

so far as they relate to the Investment and/or its

proposed activities and the prospectus (including any

relevant supplement), the prospectus shall apply. The

prospectus (including any relevant supplement), may

be obtained free of charge from Davy. An investor’s

choice of investment funds may be restricted by the

law that applies in either their location or their country

of citizenship, residence or domicile. If the investor

has any doubt about whether or not a particular

investment fund may be promoted to him/her/it or

whether or not the investor may invest in a particular

investment fund, the investor should seek advice

from his/her/its professional advisor. On the realisation

of any investment in the investment, there is no

guarantee that investors will receive back the original

amount invested or anything at all.

Tax information contained herein is based on

Davy’s current understanding of the tax legislation

in Ireland and the UK and the relevant Revenue

interpretation thereof. It is provided by way of general

guidance only and is neither exhaustive nor definitive

and is subject to change without notice, including

retrospectively. It is not a substitute for professional

advice. You should consult your tax advisor about the

rules that apply in your individual circumstances.

This Information Memorandum contains summary

information regarding the Investment. Statements,

expected performance and other assumptions

contained in this Information Memorandum, are

based on current expectations, estimates, projections,

opinions and/or beliefs of Davy at the time of

publishing. These assumptions and statements may or

may not prove to be correct. Actual events and results

may differ from those statements, expectations and

assumptions. Estimates, projections, opinions or beliefs

are not a reliable guide to the future performance

of any investment. In addition, such statements

involve known and unknown risks, uncertainties

and other factors and undue reliance should not be

placed thereon. Certain information contained in

this Information Memorandum constitutes ‘forward

looking statements’, which can be identified by the

use of forward-looking terminology, including but

not limited to the use of words such as ‘may’, ‘can’,

‘will’, ‘would’, ‘should’, ‘seek’, ‘expect’, ‘anticipate’,

‘project’, ‘target’, ‘estimate’, ‘intend’, ‘continue’ or

‘believe’ or the negatives thereof or other variations

thereon or comparable terminology. Due to various

risks and uncertainties, actual events or results, the

actual performance of the Investment may differ

materially from those reflected or contemplated in

such forward-looking statements. There can be no

8 Disclaimer

24

Dis

clai

mer

assurances that projections are attainable or will be

realised or that unforeseen developments or events

will not occur. Accordingly, actual realised returns

may differ materially from any estimates, projections,

opinions or beliefs expressed herein.

Economic data, market data and other statements

regarding the financial and operating information of

the investment that are contained in this update, have

been obtained from published sources or prepared

by third parties. While such sources are believed to

be reliable, Davy shall have no liability, contingent

or otherwise, to the user or to third parties, for the

quality, accuracy, timeliness, continued availability or

completeness of same, or for any special, indirect,

incidental or consequential damages which may

be experienced because of the use of the data or

statements made available herein. As a general matter,

information set forth herein has not been updated

through the date hereof and is subject to change

without notice.

While reasonable care has been taken by Davy in

the preparation of this Information Memorandum, no

warranty or representation, express or implied, is or

will be provided by Davy or any of its shareholders,

subsidiaries or affiliated entities or any person, firm or

body corporate under its control or under common

control or by any of their respective directors, officers,

employees, agents, advisers and representatives, all

of whom expressly disclaim any and all liability for

the contents of, or omissions from this Information

Memorandum, the information or opinions on which

it is based and/or whether it is a reasonable summary

of and/or otherwise in conformity with the underlying

fund documentation and for any other written or oral

communication transmitted or made available to the

recipient or any of its officers, employees, agents or

representatives. Davy gives no undertaking to provide

investors or prospective investors with access to any

additional information or to update this Information

Memorandum, or to correct any inaccuracies in it

which may become apparent and Davy reserves the

right, without giving reasons, at any time and in

any respect, to amend or terminate the procedure

for investing in the Investment or to terminate

negotiations with any prospective investor. The issue

of this Information Memorandum shall not be deemed

to be any form of commitment on the part of Davy

to proceed with any transaction with any prospective

investor or any other party.

Neither Davy nor any of its shareholders,

subsidiaries, affiliated entities or any person, form or

body corporate under its control or under common

control or their respective directors, officers,

agents, employees, advisors, representatives or any

associated entities (each an ‘Indemnified Party’)

will be responsible or liable for any costs, losses or

expenses incurred by investors in connection with

the Investment. The investor indemnifies and holds

harmless Davy and each Indemnified Party for any

losses, liabilities or claims, joint or several, howsoever

arising, except upon such Indemnified Party’s bad

faith or gross negligence. With the exception of

liabilities arising from fraud or willful neglect, any

liability, where it exists, for any losses, damages,

costs and expenses, including legal fees, howsoever

incurred, shall not exceed four times the value of any

commissions fees and charges paid on the Investment.

Davy and each Indemnified Party shall have no liability

or obligation for any direct or indirect consequential

loss after the first anniversary following investment.

This Information Memorandum has been

made available on the express understanding that

any written or oral information contained herein

or otherwise made available will be kept strictly

confidential and is only directed to the parties to

whom it is addressed. This brochure must not be

copied, reproduced, distributed or passed to others at

any time without the prior written consent of Davy.

Davy may have acted, in the past 12 months, as lead

manager / co-lead manager of a publicly disclosed

offer of the securities in certain companies included

in this report. Investors should be aware that Davy

may have provided investment banking services to

and received compensation from certain companies

included in this report in the past twelve months or

may provide such services in the next three months.

The term investment banking services includes acting

as broker as well as the provision of corporate finance

services, such as underwriting and managing or

advising on a public offer. Our conflicts of interest

management policy is available at www.davy.ie.

J&E Davy, trading as Davy, is regulated by the

Central Bank of Ireland. Davy is a member of the

Irish Stock Exchange, the London Stock Exchange

and Euronext. Davy is authorised by the Central Bank

of Ireland and regulated by the Financial Services

Authority for the conduct of business in the UK.

25

Dis

clai

mer

www.davy.ie

Dublin office Davy House 49 Dawson StreetDublin 2, Ireland T +353 1 679 7788 F +353 1 671 2704 [email protected]

Belfast office Donegall House 7 Donegall Square North Belfast BT1 5GB, Northern Ireland T +44 28 90 310 655 F +44 28 90 310 656 [email protected]

Cork office 89/90 South Mall Cork, Ireland T +353 21 425 1420 F +353 21 425 1410 [email protected] galway office 1 Dockgate, Dock Road Galway, Ireland T +353 91 530 520 F +353 91 530 710 [email protected]

london office13th Floor, Dashwood House69 Old Broad StreetLondon EC2M 1QS, EnglandT +44 207 448 [email protected]

www.davy.ie

J&e Davy, trading as Davy, is regulated by the Central Bank of Ireland. Davy is a member of the Irish Stock exchange, the london Stock exchange and euronext. No part of this document is to be reproduced without our written permission. this publication is solely for information purposes and does not constitute an offer or solicitation to buy or sell securities or investments. this document has been prepared and issued by Davy on the basis of sources believed to be reliable. While Davy has sought to take reasonable care in the preparation of this document, we do not guarantee the accuracy or completeness of the information contained herein and we do not give any warranty or representation express or implied regarding the contents. Neither this document nor any of its contents will form the basis of or part of any contract or any legal or binding obligation or commitment of any kind. any opinion expressed (including estimates and prospective performance) may be subject to change without notice. We or any of our connected or affiliated companies or their employees may have a position in any of the securities or may have provided, within the last twelve months, significant advice or investment services in relation to any of the securities or related investments referred to in this document. Information in this document relating to tax was provided for Irish residents based on current tax legislation in Ireland and the known current Revenue interpretation thereof, at the time of original deal launch. this can vary according to individual circumstances and investors should be aware that this may have changed since original deal launch. this is not applicable to UK residents. this is provided for information only, is subject to change without notice and is not a substitute for professional advice. Please contact your tax advisor for the rules that apply in your individual circumstances. Details of past performance noted in this document are not a reliable guide to future performance. Figures for current or estimated performance are for illustration purposes only. they are not a reliable guide to future performance and they do not constitute forecasts.

Ref:

GBE

F/10

/10