gitmanjoeh_238702_im09

DESCRIPTION

godoofoaefn snd obkhcbhTRANSCRIPT

Chapter 9Market Price Behavior

Outline

Learning Goals

I. Technical Analysis

A) Principles of Market Analysis

B) Using Technical Analysis

C) Measuring the Market

1. The Big Picturea. Dow theoryb. Trading actionsc. Confidence index

2. Technical Conditions Within the Marketa. Market volumeb. Breadth of the marketc. Short interestd. Odd-lot trading

3. Trading Rules and Measuresa. Advance-Decline lineb. New highs-New lowsc. The Arms indexd. Mutual fund cash ratioe. On balance volumef. Investment newsletter sentiment index

163 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

4. Charting a. Bar chartsb. Point-and-figure chartsc. Chart formationsd. Moving averages

Concepts in Review

II. Random Walks and Efficient Markets

A) A Brief Historical Overview

1. Random Walks2. Efficient Markets

B) Why Should Markets Be Efficient?

Chapter 9 Market Price Behavior 164

C) Levels of Market Efficiency

1. Weak Form2. Semi-Strong Form3. Strong Form4. Market Anomalies

a. Calendar effectsb. Small firm effectc. Earnings announcementsb. P/E effect

D) Possible Implications

1. Implications for Technical Analysis2. Implications for Fundamental Analysis

E) So Who Is Right?

Concepts in Review

III. Behavioral Finance: A Challenge to The Efficient Markets Hypothesis

A) Investor Behavior and Security Prices

1. Overconfidence2. Biased-Self Attribution3. Loss Aversion4. Representativeness5. Narrow Framing6. Belief Perseverance

B) Behavioral Finance at Work in the Markets

1. Stock Return Predictability2. Investor Behavior3. Analyst Behavior

C) Implications for Security Analysis

D) Your Behavior as an Investor: It Does Matter

Concepts in Review

Summary

Putting Your Investment Know-How to the Test

Discussion Questions

Problems

Case Problems9.1 Rhett Runs Some Technical Measures on a Stock9.2 Deb Takes Measure of the Market

Excel with Spreadsheets

Trading Online with OTIS

165 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

Key Concepts

1. Technical analysis, its role in its role in the security analysis and stock selection process, and the various measures of market performance that make up technical analysis.

2. The idea of random walks and efficient markets, particularly with regard to how the efficient market concept explains why prices move randomly, and to caution the investor not to expect to consistently outperform the market.

3. Weak, semi-strong, and strong versions of the efficient market hypothesis and market anomalies.

4. Behavioral finance as a challenge to market efficiency and how psychological factors can effect investors’ decisions.

Overview

The accuracy of stock market prices is considered in this chapter. Analyzing the various forces at work in the stock market is known as technical analysis. Information is divided into three categories—price and volume, fundamental data, and information known only to insiders. Market efficiency is examined at each level, along with some pieces of information that seem to provide returns in excess of what would be expected based solely on the basis of risk. Emotions and other subjective factors play a role in investment decisions. Hence, this chapter includes information on the new area of behavioral finance, so that readers can appreciate the ongoing debate between behaviorists and supports of the EMH

1. One set of technical indicators provides insight to general stock market conditions. Dow theory, trading action, and Confidence Index measures are presented.

2. Another technical analysis approach is that of measuring variables that drive market behavior. Technical indicators such as market volume, breadth of the market, short interest, odd–lot trading, and relative price levels should are covered.

3. Technical analysts develop trading rules based on mathematical equations and measures as a way to assess market conditions. Among the most widely used technical indicators are the advance-decline line, new highs-new lows, Arms Index, mutual fund cash ratio, on balance volume, and investment newsletter sentiment index. It is usually best to bring current levels of these measure to class.

4. Charting is discussed next. Details about different types of charts (bar charts, point and figure charts, and chart formations) are best explained with visual examples.

5. The random walk and efficient market theories are then described. The different levels of market efficiency based on the type of information that is incorporated into market prices are also described. Usually students are curious to know which of the various theories best explains the “real world.” The instructor may expect some lively classroom interchange on this, especially if the implications for technical and fundamental analysis are presented.

6. Coverage of the behavioral finance segment of the chapter is best done through a discussion of the factors that students see impacting investor decisions. Those frequently mentioned include overconfidence, biased self-attribution, and loss aversion. You will want to follow this up with a discussion of the “herding” behavior of security analysts. This tends to be one of the chapters that students greatly enjoy.

Chapter 9 Market Price Behavior 166

Answers to Concepts in Review

1. Technical analysis involves the study of the various forces at work in the marketplace. Technical analysts argue that internal market factors, such as trading volume and price movements, often reveal the market’s future direction before the cause is evident in financial statistics. Thus, by revealing the market’s future direction, technical analysis provides insight that is supposed to be helpful to investors in timing their investment decisions. If technical analysis indicates the market is about to move up, it signals a good time to buy; if it indicates the market is about to turn down, it signals a good time to sell.

2. The market can definitely have an impact on the prices of individual securities, and a significant one at that. In fact, studies have indicated that between 20 and 50 percent of stock price behavior can be traced to market forces. When the market is bullish, stock prices rise in general. When market participants become bearish, most prices fall. This is because stock prices are simply the result of supply and demand forces in the market. Since the demand for and supply of securities depends on the general condition of the market, stock prices are affected by the general behavior of the marketplace. (Note: To really drive the point home, just discuss how stocks behaved on Black Monday, October 19, 1987.)

3. Dow theory is a technical approach based on the idea that the stock market’s behavior can be best described by the long-term price trend of the Dow Jones Industrial Index and the Dow Jones Transportation Index. If the values of both indexes are rising, we say that we are in a bull market. If the Dow Jones Industrial Average declines and the Transportation index follows suit, we say that the markets have entered into a bearish period. The confidence index is the ratio of the average yield on high-grade corporate bonds to the average yield on low-grade corporate bonds. Low-rated bonds always provide a higher yield than high-grade bonds. If investors are pessimistic about the future, they will require a much higher yield on low-rated bonds, resulting in a decline in the confidence index. The unique feature of this index is that it uses bond yields to judge stock market performance.

4. The breadth-of-the-market measure contrasts the number of firms with share price advancing to the number of firms with share price declining. When investors are optimistic, the number of advances will generally outnumber the frequency of declining share prices.

Short interest is a measure of the number of shares in the stock market that have been sold short. Because shares sold short will have to be purchased by the short sellers in order to cover their positions, the short sale measure is an indicator of future demand for the shares. Hence, the short interest measure provides insight to the current expectations regarding share prices and future potential demand.

Odd-lot trading is based on the cynical assumption that small investors will be the last to invest in a bull market and last to sell in a bear market. Hence, as the number of odd-lot purchases increases, there is supposedly an increasing chance of a market decline. If the number of odd-lot sales exceeds the number of odd-lot purchases by an increasing amount it is an indication that the least knowledgeable group is giving up. The supply of additional shares will reduce price to sellers, but increase the likelihood that subsequent prices will be higher.

167 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

5. An advance-decline line is the difference between the number of shares going up in price and the number going down in price. The NYSE, AMEX, and Nasdaq publish statistics on how many of their stocks closed higher and lower than the previous day. Each day’s net number is added to (or subtracted from) the running total, and the result is plotted on a graph. If the graph is rising, then advancing issues are more numerous than declining issues, and the market is considered strong.

Chapter 9 Market Price Behavior 168

The Arms index builds on the advance-decline line by considering the volume in advancing and declining stocks. The ratio of advancing issues to declining issues is divided by the volume of declining issues to rising issues to create a trading index, or TRIN. The higher the TRIN the worse the market condition. A bullish market would have more advances than declines and greater volume in the rising stocks than falling ones.

On balance volume (OBV) is a momentum indicator that relates volume to price change. When the security closes higher than the previous day, all the day’s volume is considered up volume and added to the running total. If it closes lower, all of the day’s volume is considered down volume and subtracted from the running total. If prices are rising and OBV measures are rising, it is very bullish. A bearish measure would consist of both prices and OBV values declining. If they are going in opposite directions, even if share prices are rising, technical analysts would be concerned.

The relative strength index (RSI) is a measure of the average price change on up days to the average price change on down days. If the average price change is the same on up and down days, the RSI value will be 50. If the average price change is twice as high on up days as down days, the RSI value will be 67. High values actually suggest that there is more buying than the fundamentals will justify.

Moving averages compare current share price to the average share price over a specified period. The period might, for instance be 200 days. Every new day is added to the average and the oldest day is dropped from the average. When current share prices advance above their 200-day moving average, share prices are expected to continue to rise. Whereas, when stock prices drop below their moving average, they are expected to continue to decline.

6. A stock chart is simply a historical record (or “picture”) of the behavior of a stock, the market, or some technical measure (like short interest). Chartists believe that price patterns evolve into chart formulations, which provide signals about the future course of the market or a particular stock.

(a) In a bar chart, prices (or some other market or share statistic) are plotted against the vertical axis and time is plotted on the horizontal axis. Prices are recorded as vertical bars which depict the high, low, and closing prices. A point-and-figure chart, in contrast, has no time dimension, and only significant price changes are recorded on these charts.

(b) Chart formations are said to result because of certain supply and demand forces in the marketplace. Some investors argue that history repeats itself, and so chart formations indicate the course of events to come. Of course, the formations are often not very clear, so identification and interpretation can be a most difficult job.

7. The random walk hypothesis claims that stock prices follow a random or erratic pattern. That is, people who believe in this theory claim that price movements are unpredictable and as a result, there’s little that you can do to predict future behavior. An efficient market is one in which the market price of the security always fully reflects all available information, so it is difficult, if not impossible to consistently outperform the market by picking undervalued stocks. It is argued that in an efficient market, random price movements simply reflect a highly competitive market where investors quickly use and digest any new information. This competition holds security prices close to their correct (justified) level; as new information becomes available (in a random manner), adjustments in price are random and quick to follow.

8. To outperform the market, one must consistently earn more than the required rate of return on securities. In other words, one must be able to consistently find stocks selling below their justified prices, and then realize the expected return on the security. In an efficient market, current prices reflect all information, therefore, current prices equal justified prices, and investors can expect to earn only the required (risk-adjusted) rate of return.

169 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

(a) Efficient markets do not make high rates of return unavailable, but they make it (nearly) impossible to consistently earn returns higher than the rates of return required for the risk levels of the securities purchased. Hence a stock with high rates of return will also be more risky.

(b) Investors can earn high rates of return through luck, or through accepting stocks with higher risks. They can also minimize transaction and tax expenses, along with unnecessary risk, to make their returns more satisfactory.

9. Market anomalies are deviations from what one would expect in an efficient market and hence refute the efficient market hypothesis. Most of these anomalies are empirical anomalies, suggesting that over a specified period certain information could have been used to earn abnormal, risk-adjusted returns. There is no guarantee that they will provide anomalous returns in the future. Some popular ones are:

(a) The January effect is the term applied to the tendency for small stocks’ prices to go up during the month of January.

(b) The P/E effect us the term applied to the tendency for low P/E stocks to outperform high P/E stocks.

(c) The size effect is the term applied to the tendency for investments in the common stock of small firms to outperform investment in large firms.

10. Random walks offer a serious challenge to technical analysis. If price fluctuations are purely random, charts of past behavior cannot produce significant trading profits. If the market is efficient, shifts in supply and demand occur so rapidly that technical measures simply measure the past and have no implications for the future. What’s more, in an efficient market, extreme competition among investors will keep security prices at or very close to their justified levels, so fundamental analysis will not lead to returns above those required by the amount of risk exposure.

If markets are efficient, benefits from technical analysis are minimal. Fundamental analysis should still be utilized, however, to identify fundamentally strong (and weak) firms. So, even if firms are not undervalued, analysis can be directed to and used in the selection of fundamentally strong stocks.

11. Beyond firm fundamentals, behavioral finance advocates believe that investors’ decisions are affected by a number of personal beliefs and preferences. Consequently investors will over react to some types of financial information and under react to others, resulting in pricing that cannot be justified on the basis of the firm itself. An understanding of these behavioral factors can improve stock price prediction resulting in an inefficient market and lack of support for the EMH.

12. (a) Since investors tend to extrapolate past bad news into the future to an extent that would not be justified based on the information alone, one should sell firms that have done poor recently (say over the past 6 to 12 months) and buy firms that have done poorly over a longer period of time (say over the past 3 or 5 years). Also, investors tend to be overly optimistic about growth stocks, resulting in lower subsequent returns than earned on value stocks.

(b) Investors who feel they have superior information tend to trade more, and consequently earn lower net returns due to higher transactions costs. Investors tend to exhibit loss aversion, by hanging on to shares that have declined and selling those that have increased.

(c) Analysts tend to exhibit “herding” behavior, by issuing similar recommendations or earnings forecasts for stocks. They also tend to be optimistic. Research has shown that hyped stocks tend to underperform the market.

13. Listed below are several ways to use behavioral finance to improve stock returns.

(a) Don’t hesitate to sell a losing stock.(b) Don’t chase performance.

Chapter 9 Market Price Behavior 170

(c) Be humble and open-minded. (d) Review performance of your investments on a periodic basis.(e) Don’t trade too often.

Suggested Answers to Investing in Action Questions

Finding Strong Stocks can be a Relative Proposition (p. 380)

How does relative strength help identify price trends?

Answer:

The relative strength index measures a security’s price momentum. It measures the average price change on up days relative to the average price change on down days. If the average price change is the same, the RSI value is 50 (100 – (100/(1 + 1). If the market advances twice as much on up days as down days, suggesting that there is stronger buying than fundamentals justify, the RSI value is 66.7 (100 – (100 (1 + 2)). A RSI value above 80 is an indication that the market is overbought and the price will decrease in the future. Whereas, an RSI value below 20 suggests that the security is oversold, and prices will move upward. Note that average price increases would have to be 4 times average price decreases, before the RSI would reach 80 and suggest that shares were overbought.

Values obtained from www.stockcharts.com will vary daily. Students can indicate the number of days over which they want the RSI to be calculated at the site. The default is 14 days.

Showdown at the EMH Corral (p. 396)

Would you consider yourself a rational or an emotional investor? How would you apply EMH and behavioral finance?

Answer:

Answers to these questions will vary across stdents. The article points out that there is some truth in both sides of the EMH issue. Rational investors fully analyze each situation, while emotional investors employ instincts about the future. Ironically, representatives from both camps conclude that individuals should build well-diversified portfolios. The EMH camp asserts that the use of index funds minimizes expenses, while the behavioral finance camp asserts the typical investor does not have the skills to benefit from behavioral finance’s insights.

Suggested Answers to Discussion Questions

1. Technical analysis involves the study of the various forces at work in the marketplace. Technical analysts argue that internal market factors, such as trading volume and price movements, often reveal the market’s future direction before the cause is evident in financial statistics. Thus, by revealing the market’s future direction, technical analysis provides insight that is supposed to be helpful to investors in timing their investment decisions. If technical analysis indicates the market is about to move up, it signals a good time to buy; if it indicates the market is about to turn down, it signals a good time to sell.

2. (a) The confidence index is the ratio of the average yield on high-grade corporate bonds to the average yield on low-grade corporate bonds. Low-rated bonds always provide a higher yield than high-grade bonds. If investors are pessimistic about the future, they will require a much higher yield on low-rated bonds, resulting in a decline in the confidence index. The unique feature of this index is that it uses bond yields to judge stock market performance.

171 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

(b) The Arms index builds on the advance-decline line by considering the volume in advancing and declining stocks. The ratio of advancing issues to declining issues is divided by the volume of declining issues to rising issues to create a trading index, or TRIN. The higher the TRIN the worse the market condition. A bullish market would have more advances than declines and greater volume.

(c) Trading actions are price patterns that seem to occur over long periods of time. Examples include the likelihood that a January with above average returns is going to be followed by eleven months with above average returns, and presidential election cycle impacts on the stock market.

(d) Odd-lot trading is based on the cynical assumption that small investors will be the last to invest in a bull market and last to sell in a bear market. Hence, as the number of odd-lot purchases increases, there is supposedly an increasing chance of a market decline. If the number of odd-lot sales exceeds the number of odd-lot purchases by an increasing amount it is an indication that the least knowledgeable investors are giving up. The supply of additional shares arising from short selling will reduce price to sellers, but increase the likelihood that subsequent prices will be higher.

(e) Charting results in a visual summary of share price over time. Technical analysts believe the charts provide valuable information about developing trends and the future behavior of the market and/or individual stocks. There are a wide variety of popular chart formations.

(f) Moving averages compare current share price to the average share price over a specified period. The period might, for instance be 200 days. Every new day is added to the average and the oldest day is dropped from the average. When current share prices advance above their 200-day moving average, share prices are expected to continue to rise. Whereas, when stock prices drop below their moving average, they are expected to continue to decline.

(g) On balance volume (OBV) is a momentum indicator that relates volume to price change. When the security closes higher than the previous day, all the day’s volume is considered up volume and added to the running total. If it closes lower, all of the day’s volume is considered down volume and subtracted from the running total. If prices are rising and OBV measures are rising, it is very bullish. If they are going in opposite directions, even if share prices are rising, technical analysts would be concerned.The confidence index, arms index, moving averages, and on balance volume statistics require some type of mathematical equation or ratio.

3. (a) Breadth of the market deals with advances and declines. So long as the number of stocks that advance in price on a given day exceeds the numbers that decline, the market is considered strong.

(b) Short interest deals with the amount of investors who borrow stocks to sell in anticipation of a weak market. A low level of short interest would indicate a strong market.

(c) The relative strength index (RSI) is the ratio of the average price change on up days versus down days during the same period. Different sectors and industries have varying RSI threshold levels.

(d) The theory of contrary opinion is a technical indicator that uses the amount and type of odd-lot trading as an indicator of the current state of the market.

(e) Head and shoulders is a chart formation. When prices break out above a support level, a buy signal has occurred indicating the beginning of a strong market.

Chapter 9 Market Price Behavior 172

4. Answers will vary by student. The main points to include would be:

(a) An efficient market is one in which securities fully reflect all possible information quickly and accurately. Both sides can argue security markets are or are not efficient especially when it comes to the levels of efficiency.

(b) Market prices may not always be correctly set especially in the securities markets of emerging economies where volatility is common and persistent. It is an opportunity to find profitable sales or purchases.

(c) Answers will vary by student. The key reason for using fundamental analysis arises from the fact that firm success will be a function of its financial success, its competitive advantage, and the macroeconomic environment in which it carries on business.

5. Several of the key assumptions about investor behavior that serve as a basis for behavioral finance are given below.

(a) Loss aversion is the tendency for individuals to dislike losses more than they like gains. As a consequence, investors hold on to losing stocks in hopes that they will bounce back.

(b) Representativeness reflects an individual’s tendency to make strong conclusions from limited samples. A successful stock analyst over the past three years is not necessarily going to be correct again. Across the thousands of stock analyst there are some that make good decisions by random chance.

(c) Investors guilty of narrow framing analyze an investment on its own merits without considering how that security correlates with the other investments in their portfolio. They might end up with an undiversified portfolio.

(d) Investors might become overconfident in their judgments. Three consequences are that they might underestimate the amount of risk, make unduly positive forecasts, and participate in excessive trading.

(e) Investors guilty of biased self-attribution will take undue credit for good selections and blame others for bad decisions. If these investors pick an above average mutual fund it is to their supposed credit, but if the mutual fund does poorly these individuals will blame the portfolio manager for bad selection and/or timing. These individuals place more value on information that agrees with their selections.

6. Stock valuation often is based on forecasts of dividends and discount rates. Overly optimistic investors will overstate the expected dividend stream and underestimate the risk (and hence discount rate). Methods to minimize optimism include the use or more conservative estimates or future cash flows and comparison of expectations for a single firm to the expectations for comparable firms. Another option is one of hypothesizing a variety of market conditions and estimate how the company would perform in each of these scenarios.

Solutions to Problems

1. TRIN (# of up stocks/# of down stocks)/(Up volume / Down volume)

TRINDay 1 (350/150)/(850 million/420 million) 2.33/2.02 1.15TRINDay 1 (275/225)/(450 million/725 million) 1.22/0.62 1.97TRINDay 1 (260/240)/(850 million/420 million) 1.08/2.02 0.53More stocks rose than fell on all three days. Hence the numerator is always greater than 1.0. On Day 2, however, the volume of declining issues exceeded the volume of increasing issues, resulting in a denominator that was less than 1.0. Higher TRIN values are interpreted as being bad for the market, because even though more stocks rose than fell, the trading volume in the falling stocks was greater.

173 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

2. Using the Investment Newsletter Sentiment Index, investors should buy when less than 40% of the newsletter writers are bullish and sell when over 60% are bullish. Consequently, the investors should by been buying shares in January and February and selling shares in May. One is essentially doing the opposite of what the so-called market experts urge readers to do.

3. OBVt+1 OBVt + Total Volume if price rose (or less Total Volume price fell)

Day 1: Up Day: OBV 50,000 + 70,000 120,000Day 2: Down Day: OBV 120,000 – 45,000 75,000Day 3 Up Day: OBV 75,000 + 120,000

195,000

In general there is an upward trend. There was lower volume on the day the stock price fell.

4. One approach would subtract the number of new lows from the number of new highs. Resulting values are added together, as shown below.

July 117 – 22 95 95 August 95 34 61 95 + 61

156September 84 41 43 156 + 43

199October 64 79 –15 199 – 15

184November 53 98 –45 184 – 45

139December 19 101 –82 139 – 82

57

Chapter 9 Market Price Behavior 174

The number of new highs exceeded the number of new lows from July through September. Starting in October, new the number of stocks with new lows exceeded the number with new highs. Although the cumulative total reaches a high of 199, a bearish trend follows with the cumulative number falling to a level below where it was at the end of July. Over this period there were on average 9.5 more stocks each month reaching new highs.

5. For every stock that declined, 1.2 issues advanced. Or, put another way, for every five stocks that declined, six advanced.

6. Advance-decline number of issues advancing minus number of issues declining.2,200 – 1,000 1,200.

7. (a)

Day New Highs New Lows NH-NL Indicator

1 117 22 952 95 34 613 84 41 434 64 79 –155 53 98 –456 19 101 –827 19 105 –868 18 110 –929 19 90 –7110 22 88 –66

Average –25.8

175 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

(b)

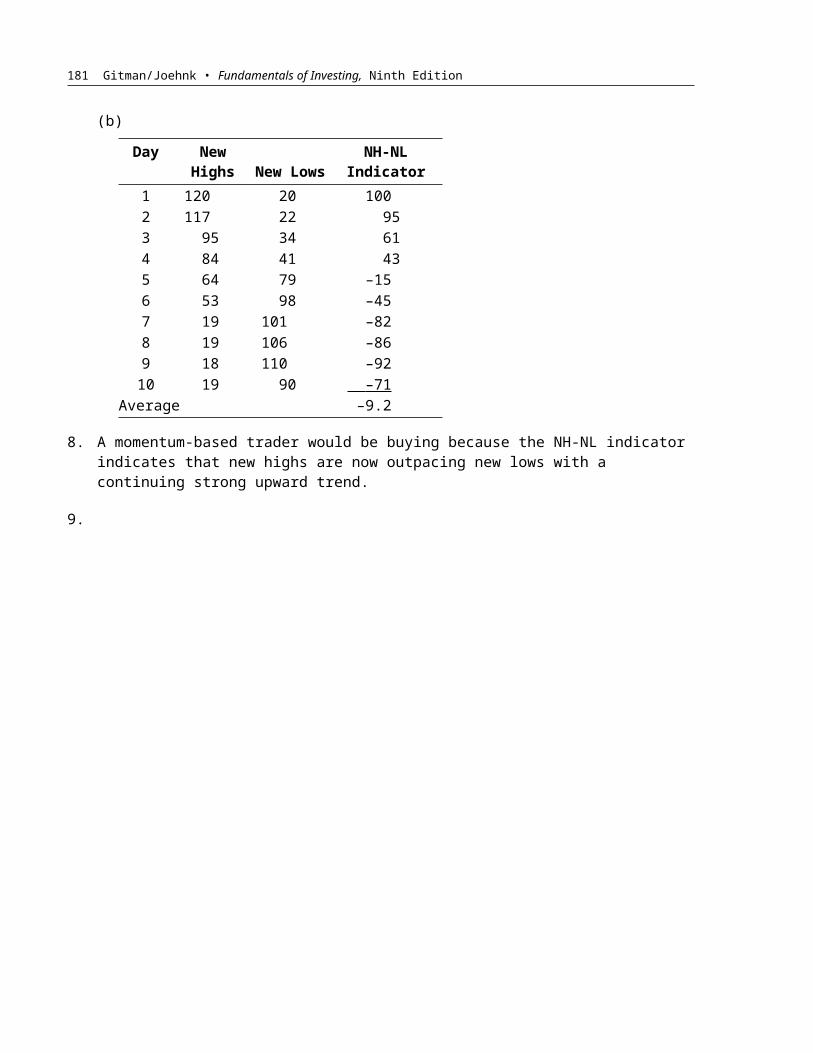

Day New Highs New Lows NH-NL Indicator

1 120 20 1002 117 22 953 95 34 614 84 41 435 64 79 –156 53 98 –457 19 101 –828 19 106 –869 18 110 –9210 19 90 –71

Average –9.2

8. A momentum-based trader would be buying because the NH-NL indicator indicates that new highs are now outpacing new lows with a continuing strong upward trend.

9.

Conventional wisdom says that when the cash ratio exceeds 10 to 12%, the ratio is sending a bullish signal. However, students may also argue that, given the trend and recent the buildup in cash is, that the signal is bearish in the current time frame.

10.

Day Closing Price Day Closing Price10-Day

Moving Avg.

1 $25.25 11 $30.00 $27.75 2 $26.00 12 $30.00 $28.15 3 $27.00 13 $31.00 $28.55 4 $28.00 14 $31.50 $28.90 5 $27.00 15 $31.00 $29.30 6 $28.00 16 $32.00 $29.70 7 $27.50 17 $29.00 $29.85 8 $29.00 18 $29.00 $29.85 9 $27.00 19 $28.00 $29.9510 $28.00 20 $27.00 $29.85

Based on the data, the price fell below the 10-day moving average on day 17, providing a sell signal. Based on the 10-day average, the stock should be sold. Longer averages are generally used, such as 50-day and 200-day, for this purpose.

A B A/BWeek Mutual Fund Cash Position Mutual Fund Total Assets MFCRMost recent $281,478,000.00 $2,345,650,000.00 12% 2 $258,500,000.00 $2,350,000,000.00 11% 3 $234,800,000.00 $2,348,000,000.00 10% 4 $211,950,000.00 $2,355,000,000.00 9% 5 $188,480,000.00 $2,356,000,000.00 8%

Chapter 9 Market Price Behavior 176

Solutions to Case Problems

Case 9.1 Rhett Runs Some Technical Measures on a Stock

(a) RSI 100 – [100/(1 + APC up days / APC down days)]APC average price change

Day of 9/30/04–10/31/04 11/30/04–12/31/04

Perod Advance Decline Advance Decline 1 0.55 –0.75 2 0.10 –0.75 3 0.15 0.25 4 0.20 0.50 5 0.10 1.05 6 –0.18 1.25 7 –0.37 –0.30 8 –1.05 –0.25 9 -- 0.75 10 –0.25 0.90 11 –0.25 0.10 12 –0.25 0.75 13 –0.25 0.75 14 0.05 0.75 15 –0.40 0.75 16 0.65 0.25 17 0.35 –0.10 18 0.07 0.60 19 0.09 0.25 20 0.50 21 0.05 Average 0.231 –0.375 0.591 –0.430

RSI (October): 100 – [100/(1 + (0.231/0.375))] 100 – 61.9 38.1RSI (December ): 100 – [100/(1 + (0.591/0.430))] 100 – 42.1 57.9

1. The RSI is getting bigger, suggesting that Nautilus Navigation is reaching a point where it is overpriced. This would be bad for shareholders of Nautilus, because it suggests that there will be a reduction in share price.

2. The higher RSI value suggest that prices will decline. As such, it is giving a sell signal. However, the RSI has not yet reached 70 (or 80). Hence, the sell signal is weak at this point.

177 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

(b) 1. Ten-day moving averages and respective share price are given below.

PriceMovingAverage Price

MovingAverage Price

MovingAverage

17.20 15.85 17.31 (10/31) 16.87 17.50 19.6018.00 16.25 17.77 16.92 16.75 19.2218.00 (9/30) 16.62 18.23 17.04 17 18.8418.55 17 19.22 17.29 17.50 18.5918.65 17.32 20.51 17.69 18.55 18.4418.80 17.60 20.15 18.05 19.80 18.419.00 17.90 20 18.44 19.50 18.3519.10 18.20 20.21 18.78 19.25 18.3318.92 18.35 20.25 19.09 20.00 18.4118.55 18.48 20.16 19.38 20.90 18.68

17.50 18.51 20.00 19.65 21 19.0217.50 18.46 20.25 19.90 21.75 19.5217.25 18.38 20.50 20.12 22.50 20.0817.00 18.23 20.80 20.28 23.25 20.6516.75 18.04 20 20.23 24 21.2016.50 17.81 20 20.22 24.25 21.6416.55 17.56 20.25 20.24 24.15 22.1016.15 17.27 20 20.22 24.75 22.6616.80 17.06 19.45 20.14 25 23.16

17.15 16.92 19.20 20.04 25.50 23.6217.22 16.89 18.25 (11/30) 19.87 25.55 (12/31) 24.07

2. At the end of August, the price is above the moving average. From that point forward, there are six times when the price crosses the moving average value, as signified by the arrow signs. There would have been a sell signal when the price dropped to $17.50, $20.00, and $20.00 shortly thereafter. Buy signals would have been provided when the price was at $17.15, $20.25, and $18.55. In only the last instance did one actually repurchase shares in Nautilus Navigation at a price below what they had sold their shares.

3. The moving average signal as of 12/31/04 would be to buy shares, since its current share price exceeds the 10-day moving average. However, those faithfully using the 10-day moving average, would have purchased shares 17 days earlier, at a price of $18.55. Both the RSI and moving average indicators suggest that concern about a correction in share price is warranted, though not officially predicted at this point in time.

Chapter 9 Market Price Behavior 178

(c) 1. The point-and-figure chart, given below, shows that Nautilus Navigation’s shares are following an upward trend.

179 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

Point and figure charts (along with other charts) are used by chartists to plot everything from the Dow Jones average to the share price movements of individual stocks. Chartists believe they contain valuable information about developing trends and the future behavior of both the market as a whole and individual stocks. (The instructor should perhaps review the popular chart formations and discuss the implications chartists find in them.)

(d) The technical indicators are in general sending Rhett a positive signal. The RSI index suggests that the share prices may be in for a correction, but the RSI for December is over ten points below 70. The firm’s share prices are comfortably above their 10-day moving average. Meanwhile, the point-and-figure chart indicates that the price of Nautilus Navigation has moved up dramatically, with only short, relatively minor corrections.

Case 9.2 An Analysis of a High-Flying Stock

Answer:

(a) Dow Theory. Students should graph the DOW averages. The graph is presents as follows:

Students should recognize that the upward trend in the Dow Industrials is confirmed by the Dow Transportation Index in period 4, and continues in period 5. This would be a positive sign that the market has turned bullish.

(b) Advance-Decline Line. The Advance Decline chart based on the data from the table:

Chapter 9 Market Price Behavior 180

Advancing Issues (NYSE) 1,120 1,278 1,270 1,916 1,929

Declining Issues (NYSE) 2,130 1,972 1,980 1,334 1,321 Advance/Decline Plot (1,010) (694) (710) 582 608Plot Point (1,010) (1,704) (2,414) (1,832) (1,224)

The Advance Decline Line, adding the net advance/decline from previous period (Plot Point):

Based on the rising Advance/Decline line, it appears the market has turned bullish. Many more stocks are closing up than down since period three. This confirms the reading from the Dow Theory above.

(c) New Highs-New Lows (the NH-NL indicator):

New Highs 68 85 85 120 200

New Lows 75 60 80 75 20 NH-NL (7) 25 5 45 180

The problem states that the current NH-NL 10 day moving average is 0 and that the past 10 periods were 0. Therefore, students should begin with zero and add each period while subtracting zero for the moving average. The graph presents as follows:

The NH-NL Indicator is very positive. This is further confirmation of the bullish trend because many more stocks are closing at new highs than at new lows since period three. The trend has accelerated in period 5.

181 Gitman/Joehnk • Fundamentals of Investing, Ninth Edition

(d) The Arms Index, or TRIN, is calculated as follows:

TRIN [(# of up stocks)/(# of down stocks)]/[(volume in up stocks)/(volume in down stocks)].

Advancing Issues (NYSE) 1,120 1,278 1,270 1,916 1,929Declining Issues (NYSE) 2,130 1,972 1,980 1,334 1,321Advances/Declines 0.53 0.65 0.64 1.44 1.46

Volume up 600,000,000 836,254,123 275,637,497 875,365,980 1,159,534,297Volume down 600,000,000 263,745,877 824,362,503 424,634,020 313,365,599Up/Down 1.00 3.17 0.33 2.06 3.70

TRIN 0.52 0.20 1.92 0.70 0.39

Higher TRIN values are interpreted as bad for the market, while lower TRIN values are interpreted as a bullish sign. Here again, it appears that the market swung into a bullish trend in after the third period, as evidenced by the declining TRIN. This is further confirmation of the bullish trend.

(e) The Mutual Fund Cash Ratio is calculated as follows:

MFCR Mutual Fund Cash Position/Total Assets Under Management.

Mutual Fund Cash (Tril.$) $0.31 $0.32 $0.47 $0.61 $0.74 Total Assets Managed (Tril.$) $6.94 $6.40 $6.78 $6.73 $7.42 MFCR 4.5% 5.0% 7.0% 9.0% 10.0%

The MFCR is also positive, again confirming the bullish trend. Funds are holding a large amount of cash in period 5 at 10% of total assets. There could be pent-up demand for stocks even with the other positive indicators already in play. In addition, if the market turns down and investors liquidate mutual fund positions, the funds will have available cash and will not be forced to sell securities to raise cash.

This problem has been designed to give students a positive experience with market analysis and get them excited about it. As such, the trends are all up, up, and away. Students should certainly conclude, based on the data presented, that all signs point to a bullish market and now would be a good time to invest in the market.

Time Period Comment: Some students may point to changes in the trends over the 5 period time horizon and express concern that they may have missed the trend. This is healthy skepticism and should be encouraged. Since the time periods are not defined, this could be a valid observation. One way to address this issue is to discuss the time period as an issue, and conclude that if the time intervals were long periods, the student would want to use more and shorter intervals to gain a more accurate reading. If, on the other hand, the time intervals were relatively short, students may want further confirmation before jumping in.