gib2015_investors approach to sustainable infrastructure_valahu

TRANSCRIPT

This presentation was held during the 5th GIB

Summit, May 27-28 2015. The presentation and

more information on the Global Infrastructure Basel Foundation are available

on www.gib-foundation.org

The next GIB Summit will take place in Basel, May 24-25, 2016.

The information and views set out in this presenation are those of the author(s) and do not necessarily reflect the opinion of the Global Infrastructure Basel Foundation. Neither the Global Infrastructure Basel Foundation nor any person acting on its behalf may be held responsible for the use of the information contained therein.

The 5th Global Infrastructure Basel Summit

27-28 May 2015 Basel, Switzerland

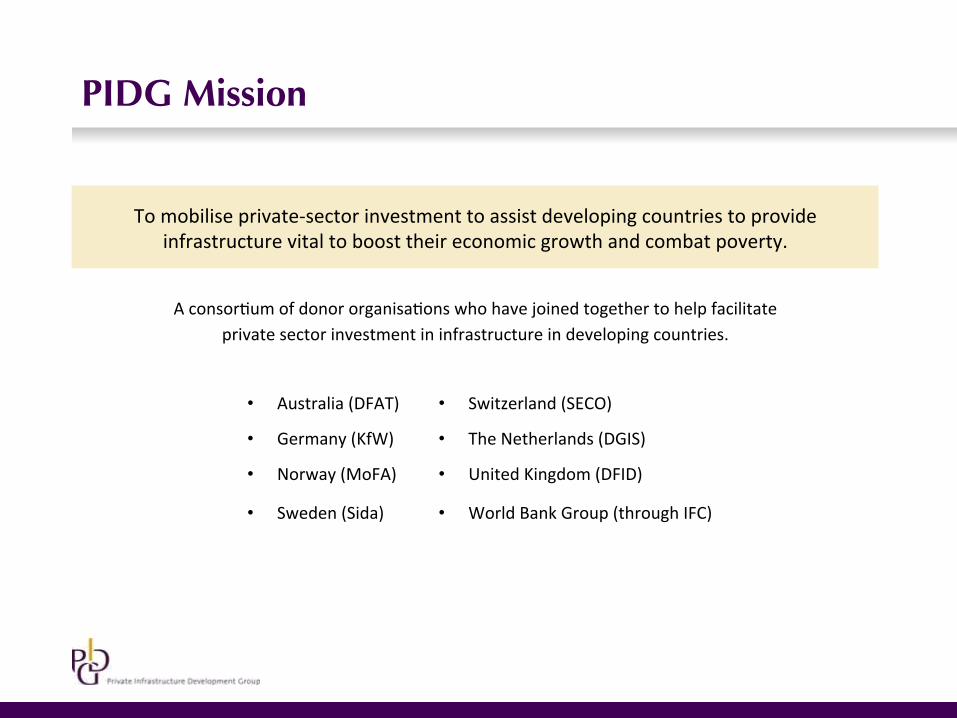

PIDG Mission

To mobilise private-‐sector investment to assist developing countries to provide infrastructure vital to boost their economic growth and combat poverty.

A consor;um of donor organisa;ons who have joined together to help facilitate private sector investment in infrastructure in developing countries.

• Australia (DFAT) • Switzerland (SECO)

• Germany (KfW) • The Netherlands (DGIS)

• Norway (MoFA) • United Kingdom (DFID)

• Sweden (Sida) • World Bank Group (through IFC)

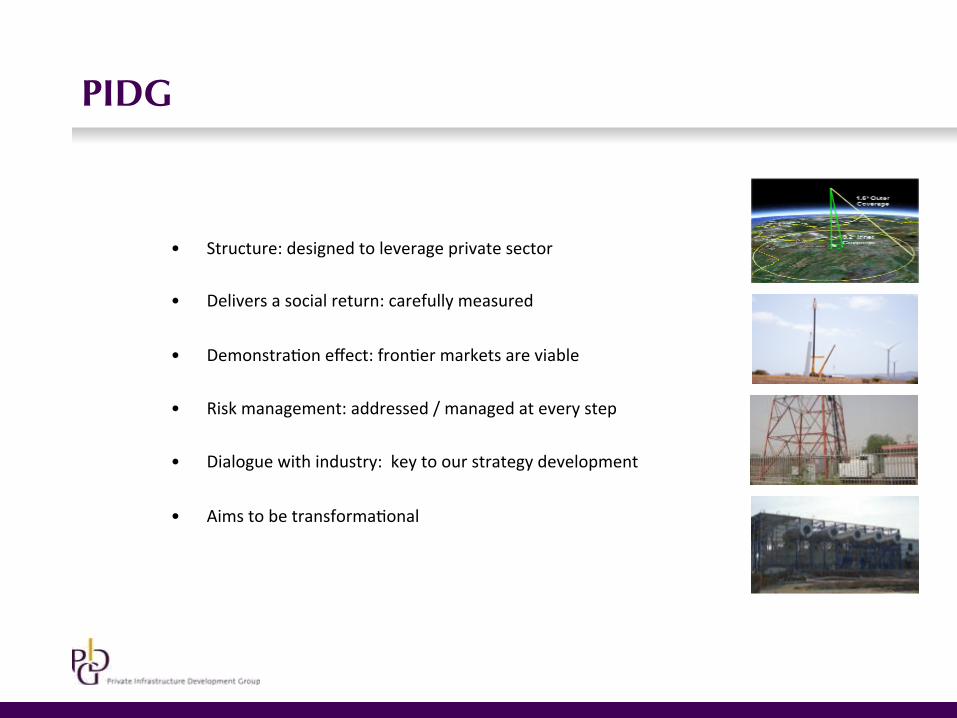

PIDG

• Structure: designed to leverage private sector

• Delivers a social return: carefully measured

• Demonstra;on effect: fron;er markets are viable

• Risk management: addressed / managed at every step

• Dialogue with industry: key to our strategy development

• Aims to be transforma;onal

Constraints to Private Investment / Risks

• Lack of bankable projects or limited developer capacity

• Shortage of long-‐term FX / local debt (liquid, longer term domes;c investment instruments), depth of capital markets

• Public sector capacity constraints

• Lack of credit-‐worthy counter-‐par;es

• Affordability risk

• Regulatory risks

6

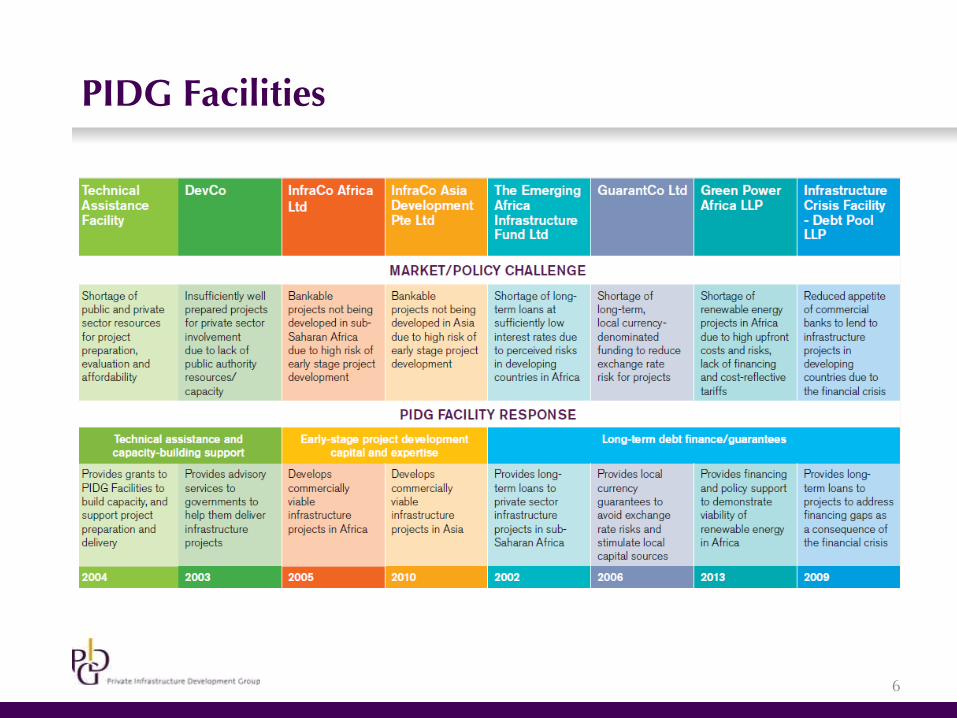

PIDG Facilities

7

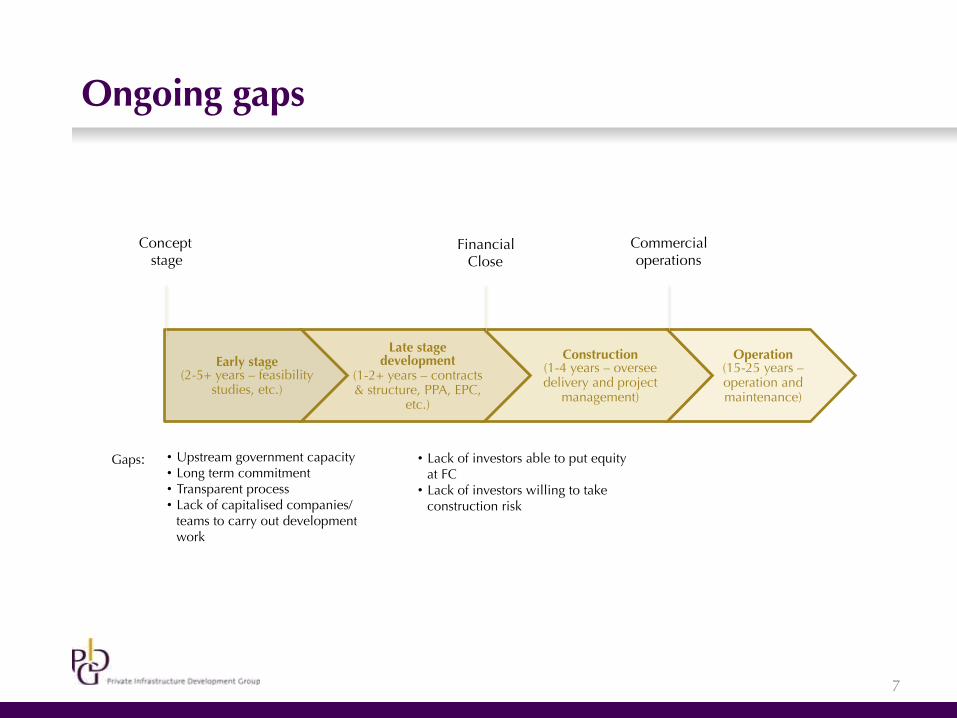

Ongoing gaps

Early stage (2-5+ years – feasibility

studies, etc.)

Late stage development

(1-2+ years – contracts & structure, PPA, EPC,

etc.)

Construction (1-4 years – oversee delivery and project

management)

Operation (15-25 years – operation and maintenance)

Commercial operations

Financial Close

Concept stage

Gaps: • Upstream government capacity • Long term commitment • Transparent process • Lack of capitalised companies/

teams to carry out development work

• Lack of investors able to put equity at FC

• Lack of investors willing to take construction risk

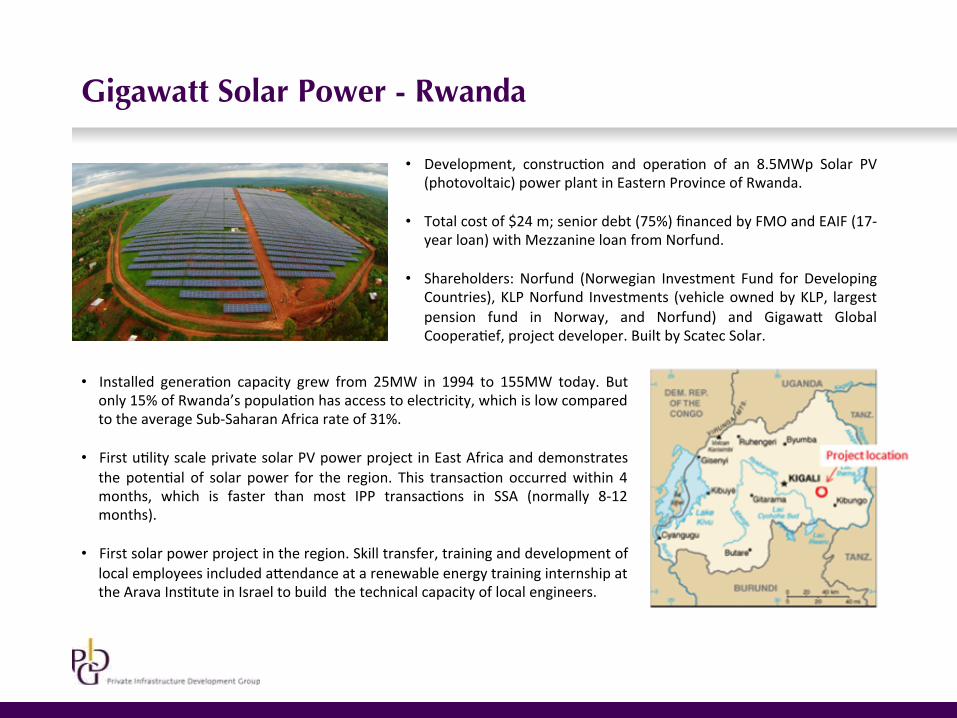

Gigawatt Solar Power - Rwanda

• Development, construc;on and opera;on of an 8.5MWp Solar PV (photovoltaic) power plant in Eastern Province of Rwanda.

• Total cost of $24 m; senior debt (75%) financed by FMO and EAIF (17-‐

year loan) with Mezzanine loan from Norfund.

• Shareholders: Norfund (Norwegian Investment Fund for Developing Countries), KLP Norfund Investments (vehicle owned by KLP, largest pension fund in Norway, and Norfund) and Gigawad Global Coopera;ef, project developer. Built by Scatec Solar.

• Installed genera;on capacity grew from 25MW in 1994 to 155MW today. But only 15% of Rwanda’s popula;on has access to electricity, which is low compared to the average Sub-‐Saharan Africa rate of 31%.

• First u;lity scale private solar PV power project in East Africa and demonstrates the poten;al of solar power for the region. This transac;on occurred within 4 months, which is faster than most IPP transac;ons in SSA (normally 8-‐12 months).

• First solar power project in the region. Skill transfer, training and development of

local employees included adendance at a renewable energy training internship at the Arava Ins;tute in Israel to build the technical capacity of local engineers.

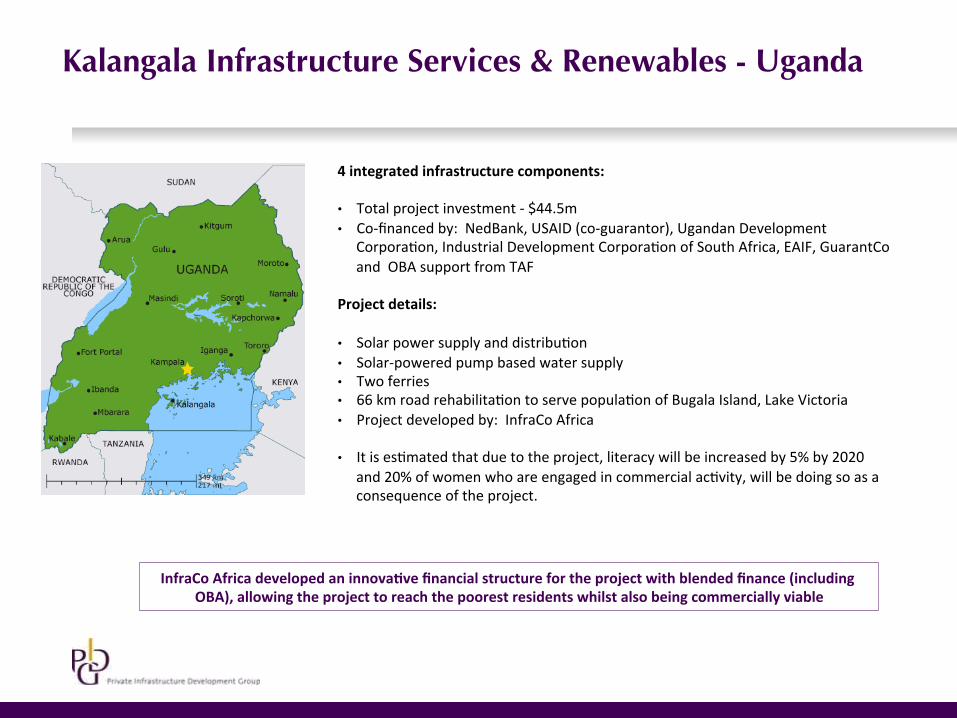

Kalangala Infrastructure Services & Renewables - Uganda

InfraCo Africa developed an innova1ve financial structure for the project with blended finance (including OBA), allowing the project to reach the poorest residents whilst also being commercially viable

4 integrated infrastructure components: • Total project investment -‐ $44.5m • Co-‐financed by: NedBank, USAID (co-‐guarantor), Ugandan Development

Corpora;on, Industrial Development Corpora;on of South Africa, EAIF, GuarantCo and OBA support from TAF

Project details: • Solar power supply and distribu;on • Solar-‐powered pump based water supply • Two ferries • 66 km road rehabilita;on to serve popula;on of Bugala Island, Lake Victoria • Project developed by: InfraCo Africa

• It is es;mated that due to the project, literacy will be increased by 5% by 2020 and 20% of women who are engaged in commercial ac;vity, will be doing so as a consequence of the project.

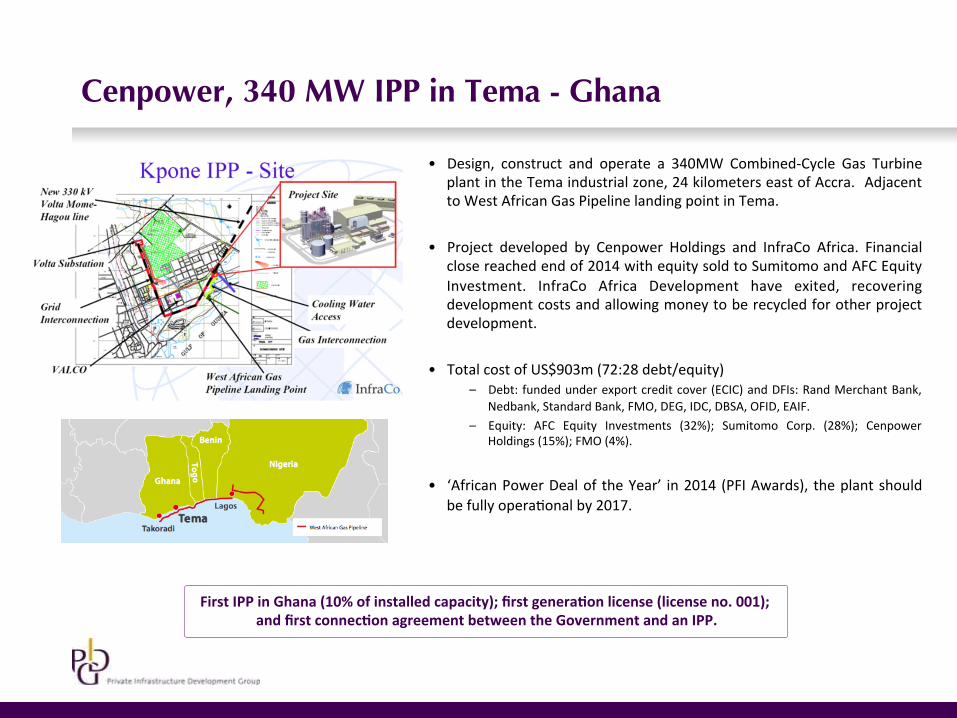

• Design, construct and operate a 340MW Combined-‐Cycle Gas Turbine plant in the Tema industrial zone, 24 kilometers east of Accra. Adjacent to West African Gas Pipeline landing point in Tema.

• Project developed by Cenpower Holdings and InfraCo Africa. Financial close reached end of 2014 with equity sold to Sumitomo and AFC Equity Investment. InfraCo Africa Development have exited, recovering development costs and allowing money to be recycled for other project development.

• Total cost of US$903m (72:28 debt/equity)

– Debt: funded under export credit cover (ECIC) and DFIs: Rand Merchant Bank, Nedbank, Standard Bank, FMO, DEG, IDC, DBSA, OFID, EAIF.

– Equity: AFC Equity Investments (32%); Sumitomo Corp. (28%); Cenpower Holdings (15%); FMO (4%).

• ‘African Power Deal of the Year’ in 2014 (PFI Awards), the plant should

be fully opera;onal by 2017.

Cenpower, 340 MW IPP in Tema - Ghana

First IPP in Ghana (10% of installed capacity); first genera1on license (license no. 001); and first connec1on agreement between the Government and an IPP.

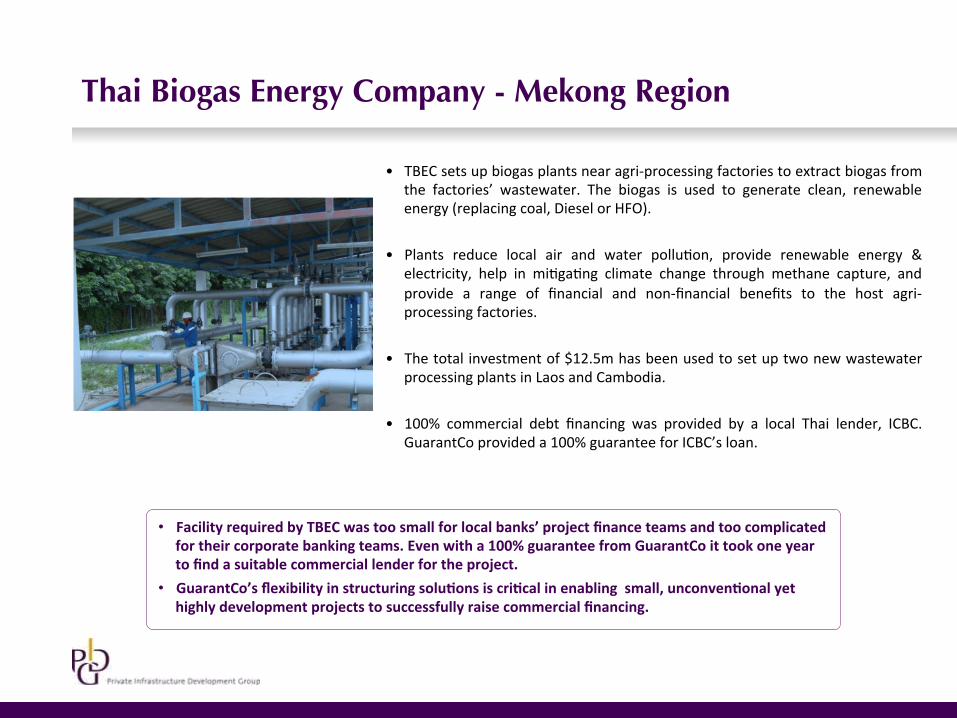

• TBEC sets up biogas plants near agri-‐processing factories to extract biogas from the factories’ wastewater. The biogas is used to generate clean, renewable energy (replacing coal, Diesel or HFO).

• Plants reduce local air and water pollu;on, provide renewable energy & electricity, help in mi;ga;ng climate change through methane capture, and provide a range of financial and non-‐financial benefits to the host agri-‐processing factories.

• The total investment of $12.5m has been used to set up two new wastewater

processing plants in Laos and Cambodia.

• 100% commercial debt financing was provided by a local Thai lender, ICBC. GuarantCo provided a 100% guarantee for ICBC’s loan.

Thai Biogas Energy Company - Mekong Region���

• Facility required by TBEC was too small for local banks’ project finance teams and too complicated for their corporate banking teams. Even with a 100% guarantee from GuarantCo it took one year to find a suitable commercial lender for the project.

• GuarantCo’s flexibility in structuring solu1ons is cri1cal in enabling small, unconven1onal yet highly development projects to successfully raise commercial financing.

Mobilink Pakistan – PKR 8bn ($75m) Sukuk

• The Sukuk was structured as a "Service Ijara", the first ;me this structure has been used in Pakistan.

• Strengthening and deepening local capital markets – mobilising 16 Islamic investors, 60% of financing from new sources.

• GuarantCo now has relevant Islamic capital markets experience that can be applied in other countries.

• CSR ac;vity (part supported by TAF) involves a successful SMS based literacy programme to impart educa;on through mobile phone technology to illiterate women in KPK province of Pakistan.

• Pakistan Mobile Communica;ons Limited was seeking to expand network into underserved rural areas to enable access to telecommunica;on services for wider propor;on of popula;on.

• To fund this capital expenditure PMCL decided to issue a local currency Islamic bond (Sukuk) of up to $75 mm equivalent.

• Given limited size of the corporate bond market in Pakistan PMCL was constrained by exis;ng investors having reached their regulatory limits either in terms of exposure to PMCL or telecommunica;ons sector.

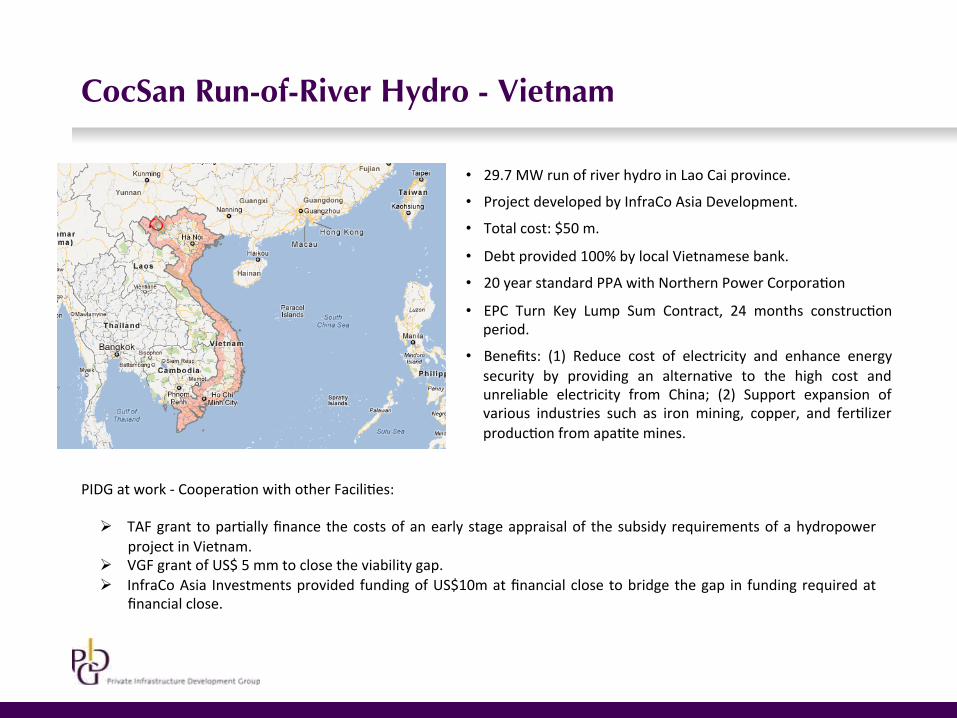

CocSan Run-of-River Hydro - Vietnam

• 29.7 MW run of river hydro in Lao Cai province.

• Project developed by InfraCo Asia Development.

• Total cost: $50 m.

• Debt provided 100% by local Vietnamese bank.

• 20 year standard PPA with Northern Power Corpora;on • EPC Turn Key Lump Sum Contract, 24 months construc;on

period.

• Benefits: (1) Reduce cost of electricity and enhance energy security by providing an alterna;ve to the high cost and unreliable electricity from China; (2) Support expansion of various industries such as iron mining, copper, and fer;lizer produc;on from apa;te mines.

PIDG at work -‐ Coopera;on with other Facili;es:

Ø TAF grant to par;ally finance the costs of an early stage appraisal of the subsidy requirements of a hydropower project in Vietnam.

Ø VGF grant of US$ 5 mm to close the viability gap. Ø InfraCo Asia Investments provided funding of US$10m at financial close to bridge the gap in funding required at

financial close.

Thank you

14

www.pidg.org

15

PIDG Facilities and the Project Cycle

PIDG: Key Facts

• From 2003 to 31 Dec 2014, the PIDG Facili;es have commided US$1.9 bn of funding to 128 PIDG projects that have reached financial close in 58 countries, mobilising:

• US$ 27.3bn of Total Investment Commitments, of which:

– US$ 18.6bn or 68% is from commercial private sector investment (PSI) sources; and – US$ 8.7bn or 32% is through DFI financing.

Every $1 of contribu1on from PIDG donors will leverage $20 of private sector investment in infrastructure

• 49% of project investments mobilised by PIDG facili;es are located in Fragile and Post

Conflict States.

• 55% of project investments mobilised by PIDG facili;es are located in the poorest DAC I/II countries.

16