gfv no 073 rev 1 no 073 rev 1...– ioss vat identification number in accordance with article...

TRANSCRIPT

Ref: Ares(2018)2769352

Commission européenne/Europese Commissie, BE-1049 Bruxelles/Brussel - Belgium. Telephone: +32 229-91111.

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax Administration Value Added Tax

Group on the Future of VAT

22nd

meeting – 13 June 2018

taxud.c.1(2018)3096002 – EN

Brussels, 29 May 2018

GROUP ON THE FUTURE OF VAT

GFV NO

073 REV 1

VAT e-commerce package of 5 December 2017

Implementing provisions to be laid down in Commission Implementing

Regulation (EU) 815/2012 laying down detailed rules for the application

of Council Regulation (EU) 904/2010, as regards special schemes for

non-established taxable persons supplying telecommunications,

broadcasting or electronic services to non-taxable persons

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

2/17

1 PURPOSE OF THE DOCUMENT

On 5 December 2017, the Council adopted:

– Council Directive (EU) 2017/2455 amending Directive 2006/112/EC and Directive

2009/132/EC as regards certain value added tax obligations for supplies of services and

distance sales of goods;

– Council Regulation (EU) 2017/2454 amending Regulation (EU) 904/2010 on

administrative cooperation and combating fraud in the field of value added tax.

Working documents GFV 062 Rev 1, GFV 063 Rev 1 and GFV 065 discussed at the GFV

meetings of 22 January and 9 February 2018 examined whether the provisions of this

Directive relating to, respectively, the non-Union scheme, the Union scheme and the

Import scheme required further implementing provisions to be laid down in Commission

Implementing Regulation (EU) 815/2012 laying down detailed rules for the application of

Council Regulation (EU) 904/2010, as regards special schemes for non-established taxable

persons supplying telecommunications, broadcasting or electronic services to non-taxable

persons. A first draft of the amendments has been presented at the GFV meeting of 12

March 2018 (working document GFV 073).

2 FOLLOW-UP OF THE GFV MEETING OF 12 MARCH 2018

The amendments to Regulation 815/2012 shown in 'track changes' in document GFV 073

have been accepted and are now shown in bold/underline/strikethrough. Only amendments

made following the discussions at the GFV meeting of 12 March 2018 are now shown in

'track changes' and, where necessary, are explained in the column 'Comments' (also added

in Annexes I and III of the draft Regulation). They are submitted to the GFV for

discussion at its meeting of 13 June 2018 (working document GFV 073 Rev1).

As this document is rather technical, it has also been published on CircaBC in the folder of

the meeting of the SCIT (the IT sub-committee of the SCAC) of 5 May 2018. Members of

SCIT have been requested to examine this document as well and to provide you with their

comments prior to the GFV meeting of 13 June 2018. For this meeting, it is important to

try and reach agreement on a number of important issues in order not to delay the IT

development:

(1) The electronic verification of the validity of the individual VAT identification numbers

included in import declarations of small consignments will require that customs authorities

of the Member States dispose of a database of Import One Stop Shop (IOSS) VAT

identification numbers which is up-to-date at all times and with high availability and quick

response times. This question has been discussed at the Fiscalis/Customs 2020 seminar in

Malta from 21 to 23 March 2018 and the conclusion was:

that a central separate database could be better as there are currently problems with

access to VIES and with its availability,

that the database should be supported by the Commission and

that a separate database similar to SEED (database of operators registered for

excise purposes) could be the way forward.

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

3/17

This was also the provisional conclusion of the discussion on this question at the SCIT

meeting of 5 May 2018.

Hence, a draft text creating a legal basis for the operation of a central database of IOSS

VAT identification numbers has been added in the draft modification of Regulation

815/2012 (see Article 3(4)). The text is based on Article 19(4) of Regulation 389/2012 on

administrative cooperation in the field of excise duties.

Do you agree on the principle of putting in place a centrally updated database of

IOSS VAT identification numbers?

(2) The format of the IOSS VAT identification number and of the registration number of

the intermediary.

The formats proposed in footnotes 2 and 10 in Annex I of the draft Regulation attached

are as follows:

– IOSS VAT identification number in accordance with Article 369q(1) and (3):

IMxxxyyyyyyz where: xxx is the 3-digit ISO numeric of the MSI; yyyyy is the 6-digit

number assigned by MSI; and z is a check digit.

– Intermediary registration number in accordance with Article 369q(2): INxxxyyyyyyz

where: xxx is the 3-digit ISO numeric of the MSI; yyyyyy is the 6-digit number

assigned by MSI; and z is a check digit.

Following discussions at the Malta seminar, the number of digits assigned by the MSI has

been increased from 5 to 6.

Do you agree on the formats proposed?

(3) During discussions at the GFV meeting of 12 March 2018, some Member States were

of the opinion that the VAT return in the Union scheme should make a distinction between

supplies of goods, on the one hand, and supplies of services, on the other hand. Some

other Member States expressed a similar view at the meeting of the SCAC-EG on 26 April

2018.

Article 369g(1) does not make a distinction between supplies goods and services

mandatory in the VAT return and would not appear to be required as the records to be kept

by the taxable persons making use of the Union scheme must in any case contain this

information.

Paragraphs 2 and 3 of Article 369g require a separate declaration of, respectively, distance

sales of goods dispatched or transported from Member States other than the Member State

of identification and services supplied form fixed establishments other than in the Member

State of identification. Consequently, a separate part 2(c) has been created in the VAT

return to include the distance sales of goods dispatched or transported from Member States

other than the Member State of identification.

Do you agree with the suggested way forward?

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

4/17

Commission Implementing Regulation (EU) No 815/2012

Adapted version Comments

COMMISSION IMPLEMENTING REGULATION (EU) No 815/2012

of 13 September 2012

laying down detailed rules for the application of Council Regulation (EU) No 904/2010, as regards

special schemes for non-established taxable persons supplying telecommunications, broadcasting or

electronic services to non-taxable persons or making distance sales of goods

The title should be adapted according to the extension of

the OSS

Article 1

Definitions

For the purposes of this Regulation, the following definitions apply:

(1) ‘non-Union scheme’ means the special scheme for telecommunications services, broadcasting services

or electronicservices supplied by taxable persons not established within the Community provided for in

Section 2 of Chapter 6 of Title XII of Directive 2006/112/EC;

(2) ‘Union scheme’ means the special scheme for telecommunications services, broadcasting services or

electronicservices supplied by taxable persons established within the Community but not in the Member

State of consumption and for intra-Community distance sales of goods carried out by any taxable

person provided for in Section 3 of Chapter 6 of Title XII of Directive 2006/112/EC;

(2a) 'Import scheme' means the special scheme for distance sales of goods imported from third

territories or third countries provided for in Section 4 of Chapter 6 of Title XII of Directive

2006/112/EC.

(3) ‘special schemes’ means non-Union scheme, and Union scheme and Import scheme.

(4) 'intermediary' means a person as defined in point (2) of the second paragraph of Article 369l of

Directive 2006/112/EC.

The definitions mirror the extension of the OSS,

including the import scheme and the intermediary.

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

5/17

Article 2

Functionalities of the electronic interface

The electronic interface in the Member State of identification by which a taxable person or an

intermediary acting on his behalf registers the use of one of the special schemes, and via which that

person submits the value added tax (VAT) returns under that scheme to the Member State of identification,

shall have the following functionalities:

(a) it must offer the facility to save the identification details pursuant to Articles 361 and 369p of Directive

2006/112/EC, or the VAT return pursuant to Articles 365, and 369g and 369t of Directive 2006/112/EC,

before they are submitted;

(b) it must allow for the taxable person or the intermediary acting on his behalf to submit the relevant

information relating to the VAT returns via an electronic file transfer in accordance with conditions laid

down by the Member State of identification.

Identification details and the submission of VAT returns

should be given/allowed to be made by the intermediary

as well.

Article 3

Transmission of identification information

1. The Member State of identification shall transmit the following to the other Member States, via the

CCN/CSI network:

(a) information to identify the taxable person using the non-Union scheme;

(b) similar details to identify the taxable person using the Union scheme;

(c) information to identify the taxable person using the Import scheme;

(d) information to identify an intermediary;

(ce) allocated identification number(s).:

The common electronic message set out in Annex I shall be used to transmit the information referred to in

the first subparagraph. Column B of the common electronic message set out in Annex I shall be used for the

non-Union scheme, and column C of that common electronic message shall be used for the Union scheme,

column D of that electronic message shall be used for the Import scheme for the identification of a

taxable person in accordance with Article 369p(1) and (3) of Directive 2006/112/EC and column E of

that common electronic message shall be used for the Import scheme for the identification of an

Deleted:

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

6/17

intermediary in accordance with Article 369p(2) of that Directive.

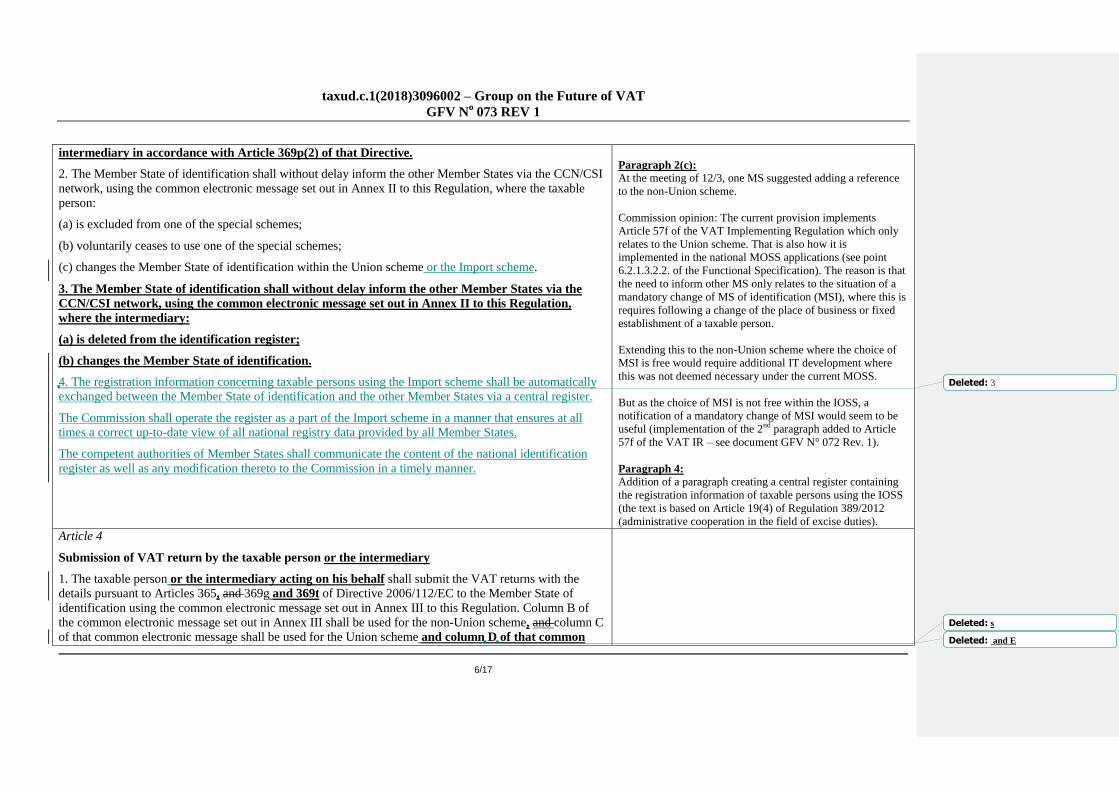

2. The Member State of identification shall without delay inform the other Member States via the CCN/CSI

network, using the common electronic message set out in Annex II to this Regulation, where the taxable

person:

(a) is excluded from one of the special schemes;

(b) voluntarily ceases to use one of the special schemes;

(c) changes the Member State of identification within the Union scheme or the Import scheme.

3. The Member State of identification shall without delay inform the other Member States via the

CCN/CSI network, using the common electronic message set out in Annex II to this Regulation,

where the intermediary:

(a) is deleted from the identification register;

(b) changes the Member State of identification.

4. The registration information concerning taxable persons using the Import scheme shall be automatically

exchanged between the Member State of identification and the other Member States via a central register.

The Commission shall operate the register as a part of the Import scheme in a manner that ensures at all

times a correct up-to-date view of all national registry data provided by all Member States.

The competent authorities of Member States shall communicate the content of the national identification

register as well as any modification thereto to the Commission in a timely manner.

Paragraph 2(c): At the meeting of 12/3, one MS suggested adding a reference

to the non-Union scheme.

Commission opinion: The current provision implements

Article 57f of the VAT Implementing Regulation which only

relates to the Union scheme. That is also how it is

implemented in the national MOSS applications (see point

6.2.1.3.2.2. of the Functional Specification). The reason is that

the need to inform other MS only relates to the situation of a

mandatory change of MS of identification (MSI), where this is

requires following a change of the place of business or fixed

establishment of a taxable person.

Extending this to the non-Union scheme where the choice of

MSI is free would require additional IT development where

this was not deemed necessary under the current MOSS.

But as the choice of MSI is not free within the IOSS, a

notification of a mandatory change of MSI would seem to be

useful (implementation of the 2nd

paragraph added to Article

57f of the VAT IR – see document GFV N° 072 Rev. 1).

Paragraph 4:

Addition of a paragraph creating a central register containing

the registration information of taxable persons using the IOSS

(the text is based on Article 19(4) of Regulation 389/2012

(administrative cooperation in the field of excise duties).

Article 4

Submission of VAT return by the taxable person or the intermediary

1. The taxable person or the intermediary acting on his behalf shall submit the VAT returns with the

details pursuant to Articles 365, and 369g and 369t of Directive 2006/112/EC to the Member State of

identification using the common electronic message set out in Annex III to this Regulation. Column B of

the common electronic message set out in Annex III shall be used for the non-Union scheme, and column C

of that common electronic message shall be used for the Union scheme and column D of that common

Deleted: 3

Deleted: s

Deleted: and E

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

7/17

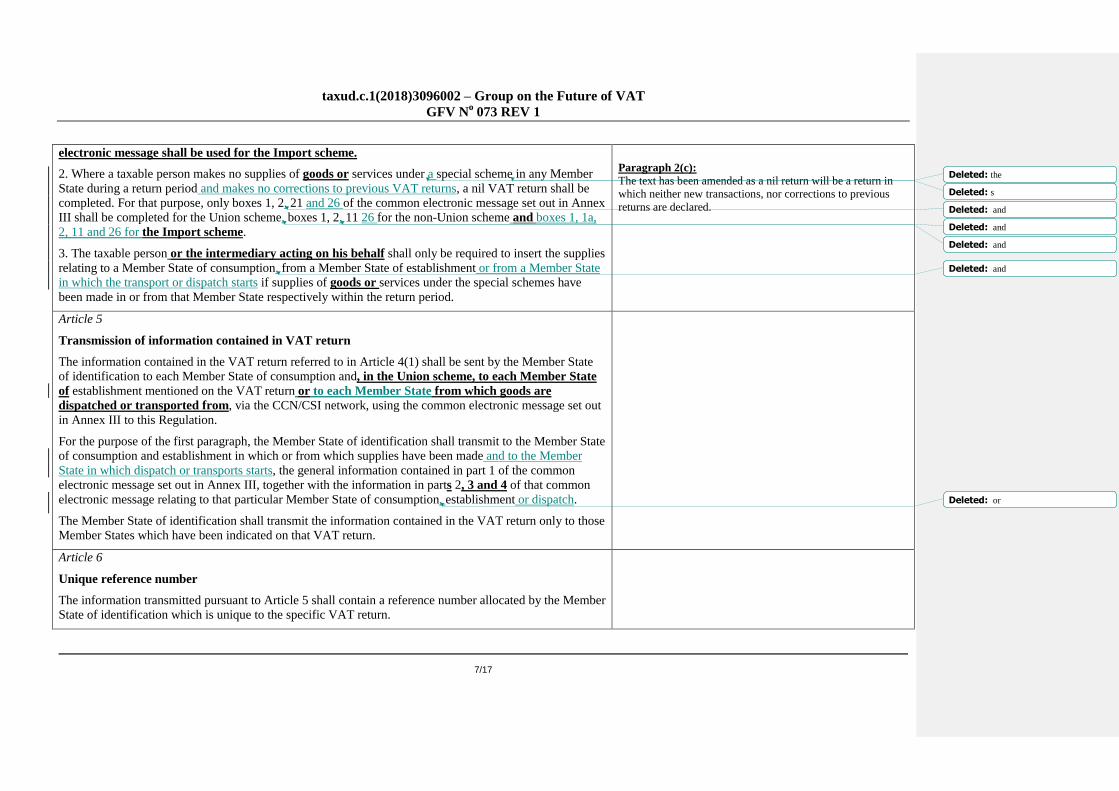

electronic message shall be used for the Import scheme.

2. Where a taxable person makes no supplies of goods or services under a special scheme in any Member

State during a return period and makes no corrections to previous VAT returns, a nil VAT return shall be

completed. For that purpose, only boxes 1, 2, 21 and 26 of the common electronic message set out in Annex

III shall be completed for the Union scheme, boxes 1, 2, 11 26 for the non-Union scheme and boxes 1, 1a,

2, 11 and 26 for the Import scheme.

3. The taxable person or the intermediary acting on his behalf shall only be required to insert the supplies

relating to a Member State of consumption, from a Member State of establishment or from a Member State

in which the transport or dispatch starts if supplies of goods or services under the special schemes have

been made in or from that Member State respectively within the return period.

Paragraph 2(c):

The text has been amended as a nil return will be a return in

which neither new transactions, nor corrections to previous

returns are declared.

Article 5

Transmission of information contained in VAT return

The information contained in the VAT return referred to in Article 4(1) shall be sent by the Member State

of identification to each Member State of consumption and, in the Union scheme, to each Member State

of establishment mentioned on the VAT return or to each Member State from which goods are

dispatched or transported from, via the CCN/CSI network, using the common electronic message set out

in Annex III to this Regulation.

For the purpose of the first paragraph, the Member State of identification shall transmit to the Member State

of consumption and establishment in which or from which supplies have been made and to the Member

State in which dispatch or transports starts, the general information contained in part 1 of the common

electronic message set out in Annex III, together with the information in parts 2, 3 and 4 of that common

electronic message relating to that particular Member State of consumption, establishment or dispatch.

The Member State of identification shall transmit the information contained in the VAT return only to those

Member States which have been indicated on that VAT return.

Article 6

Unique reference number

The information transmitted pursuant to Article 5 shall contain a reference number allocated by the Member

State of identification which is unique to the specific VAT return.

Deleted: the

Deleted: s

Deleted: and

Deleted: and

Deleted: and

Deleted: and

Deleted: or

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

8/17

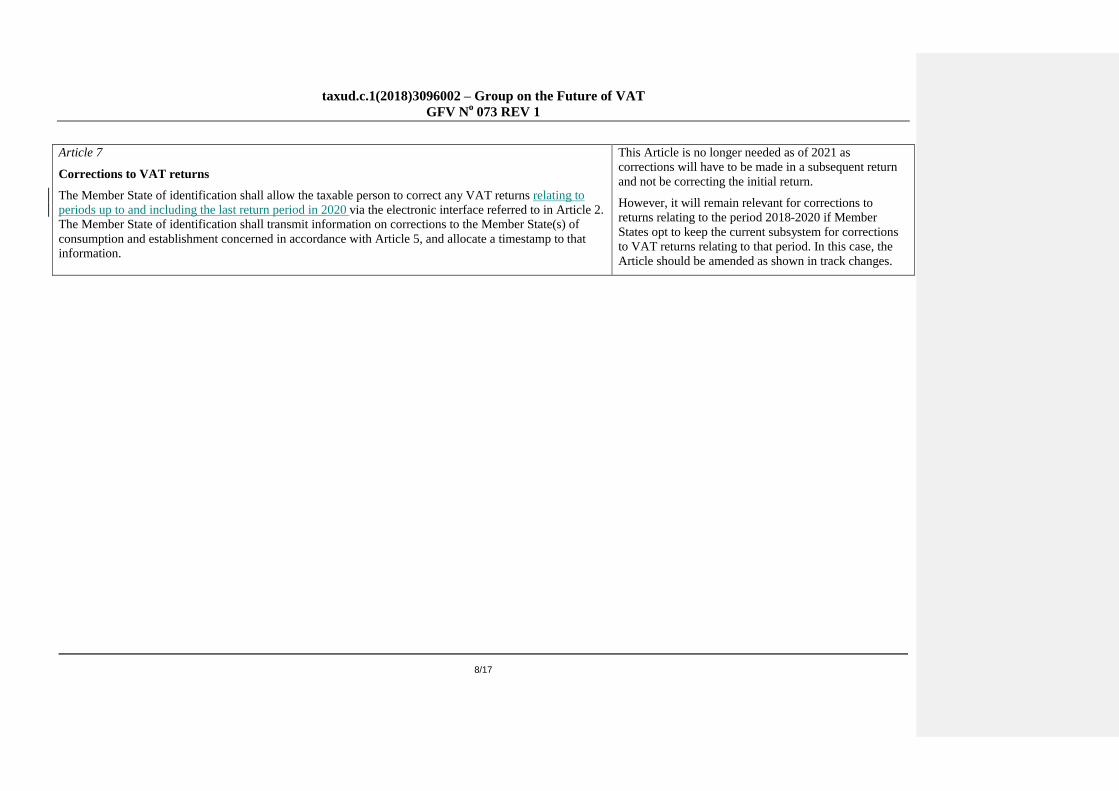

Article 7

Corrections to VAT returns

The Member State of identification shall allow the taxable person to correct any VAT returns relating to

periods up to and including the last return period in 2020 via the electronic interface referred to in Article 2.

The Member State of identification shall transmit information on corrections to the Member State(s) of

consumption and establishment concerned in accordance with Article 5, and allocate a timestamp to that

information.

This Article is no longer needed as of 2021 as

corrections will have to be made in a subsequent return

and not be correcting the initial return.

However, it will remain relevant for corrections to

returns relating to the period 2018-2020 if Member

States opt to keep the current subsystem for corrections

to VAT returns relating to that period. In this case, the

Article should be amended as shown in track changes.

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

9/17

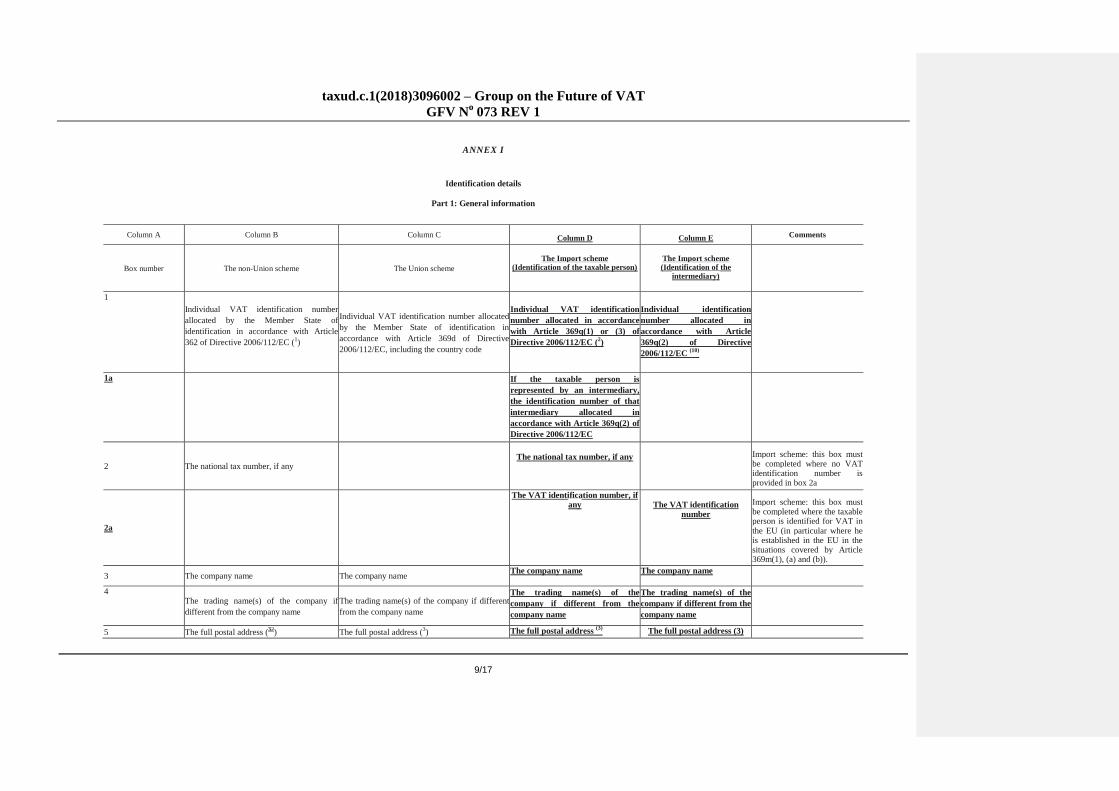

ANNEX I

Identification details

Part 1: General information

Column A Column B Column C

Column D

Column E Comments

Box number The non-Union scheme The Union scheme

The Import scheme

(Identification of the taxable person)

The Import scheme (Identification of the

intermediary)

1

Individual VAT identification number

allocated by the Member State of

identification in accordance with Article

362 of Directive 2006/112/EC (1)

Individual VAT identification number allocated

by the Member State of identification in

accordance with Article 369d of Directive

2006/112/EC, including the country code

Individual VAT identification

number allocated in accordance

with Article 369q(1) or (3) of

Directive 2006/112/EC (2)

Individual identification

number allocated in

accordance with Article

369q(2) of Directive

2006/112/EC (10)

1a

If the taxable person is

represented by an intermediary,

the identification number of that

intermediary allocated in

accordance with Article 369q(2) of

Directive 2006/112/EC

2 The national tax number, if any

The national tax number, if any

Import scheme: this box must be completed where no VAT identification number is provided in box 2a

2a

The VAT identification number, if any

The VAT identification

number

Import scheme: this box must be completed where the taxable person is identified for VAT in the EU (in particular where he is established in the EU in the situations covered by Article 369m(1), (a) and (b)).

3 The company name The company name The company name The company name

4 The trading name(s) of the company if

different from the company name The trading name(s) of the company if different

from the company name

The trading name(s) of the

company if different from the

company name

The trading name(s) of the

company if different from the

company name

5 The full postal address (32

) The full postal address (3) The full postal address

(3) The full postal address (3)

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

10/17

6 The country in which the taxable person has

his place of business The country in which the taxable person has his

place of business if not in the Union

The country in which the taxable

person has his place of business

The Member State in which

the intermediary has his

place of business or, in the

absence of a place of business

in the Union, has a fixed

establishment where he will

make use of the scheme

The information in Columns D and E determines which

MS is the MSI.

7 The e-mail address of the taxable person The e-mail address of the taxable person The e-mail address of the taxable person

The e-mail address of the intermediary

8 The website(s) of the taxable person where

available The website(s) of the taxable person where available

The website(s) of the taxable person

9 Contact name Contact name Contact name Contact name

10 Telephone number Telephone number Telephone number Telephone number

11 IBAN or OBAN number IBAN number

IBAN number (11

) IBAN number (12

) Import scheme:

Column D: The IBAN and BIC number of the taxable person must only be provided if the taxable person registers directly.

Column E: In case of registration of a taxable person by an intermediary acting on his behalf, possible reimbursements should be made to the bank account of the intermediary, the IBAN and BIC numbers of which have been provided upon registration as an intermediary (see Article 63 of the VAT Implementing Regulation (GFV 072 Rev. 1).

12 BIC number BIC number

BIC number (11

) BIC number (12

)

13.1

Individual VAT identification number(s) or if

not available, tax reference number(s) allocated

by the Member State(s) in which the taxable

person has a fixed establishment(s) (4) other than

in the Member State of identification from

which services are supplied,- or by the

Member State(s) from which the taxable

person carries out intra-Community distance

sales of goods (4).

'of' has been replaced by ''by',

to make it clear that the words 'fixed establishment'

only apply to supplies of

services and not to distance sales of goods.

In addition, the text of

footnote (4) has been amended.

Deleted: of

Deleted: places

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

11/17

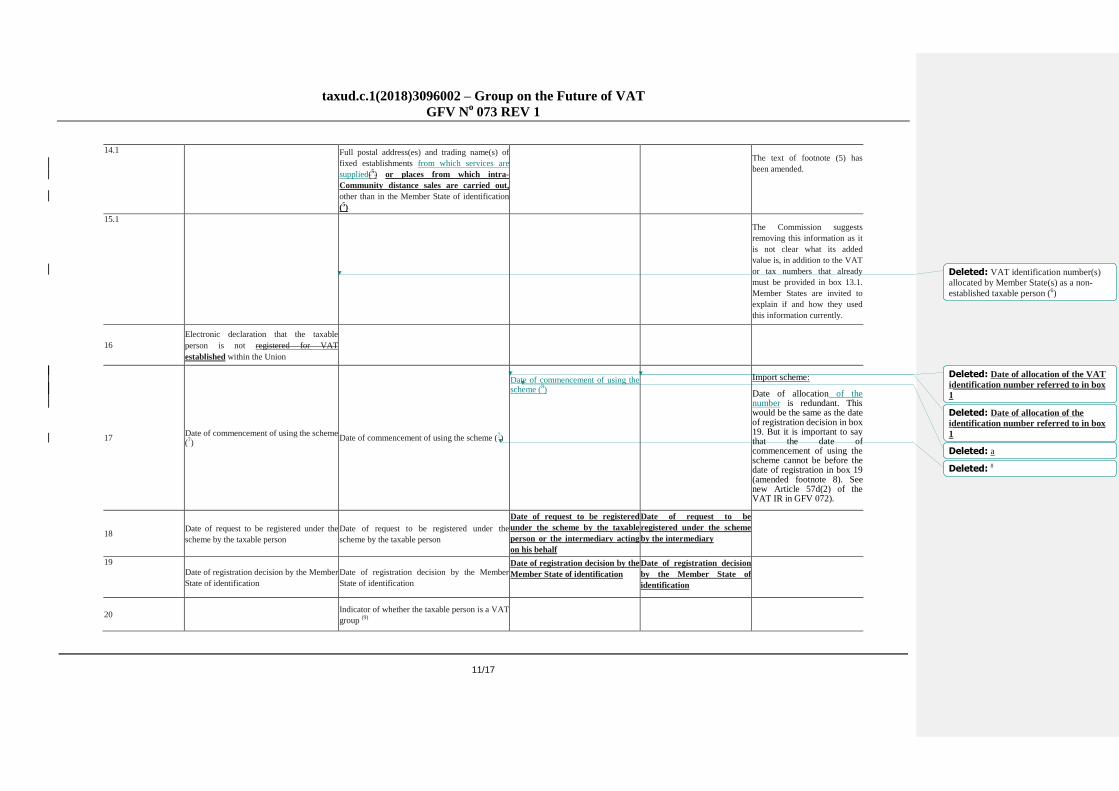

14.1 Full postal address(es) and trading name(s) of

fixed establishments from which services are

supplied(5) or places from which intra-

Community distance sales are carried out,

other than in the Member State of identification

(5)

The text of footnote (5) has

been amended.

15.1

The Commission suggests

removing this information as it

is not clear what its added

value is, in addition to the VAT

or tax numbers that already

must be provided in box 13.1.

Member States are invited to

explain if and how they used

this information currently.

16 Electronic declaration that the taxable

person is not registered for VAT

established within the Union

17 Date of commencement of using the scheme (7)

Date of commencement of using the scheme (7)

Date of commencement of using the scheme (

8)

Import scheme:

Date of allocation of the number is redundant. This would be the same as the date of registration decision in box 19. But it is important to say that the date of commencement of using the scheme cannot be before the date of registration in box 19 (amended footnote 8). See new Article 57d(2) of the VAT IR in GFV 072).

18 Date of request to be registered under the

scheme by the taxable person Date of request to be registered under the

scheme by the taxable person

Date of request to be registered

under the scheme by the taxable

person or the intermediary acting

on his behalf

Date of request to be

registered under the scheme

by the intermediary

19 Date of registration decision by the Member

State of identification Date of registration decision by the Member

State of identification

Date of registration decision by the

Member State of identification

Date of registration decision

by the Member State of

identification

20

Indicator of whether the taxable person is a VAT

group (9)

Deleted: VAT identification number(s) allocated by Member State(s) as a non-

established taxable person (6)

Deleted: 8

Deleted: Date of allocation of the VAT

identification number referred to in box

1

Deleted: a

Deleted: Date of allocation of the

identification number referred to in box

1

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

12/17

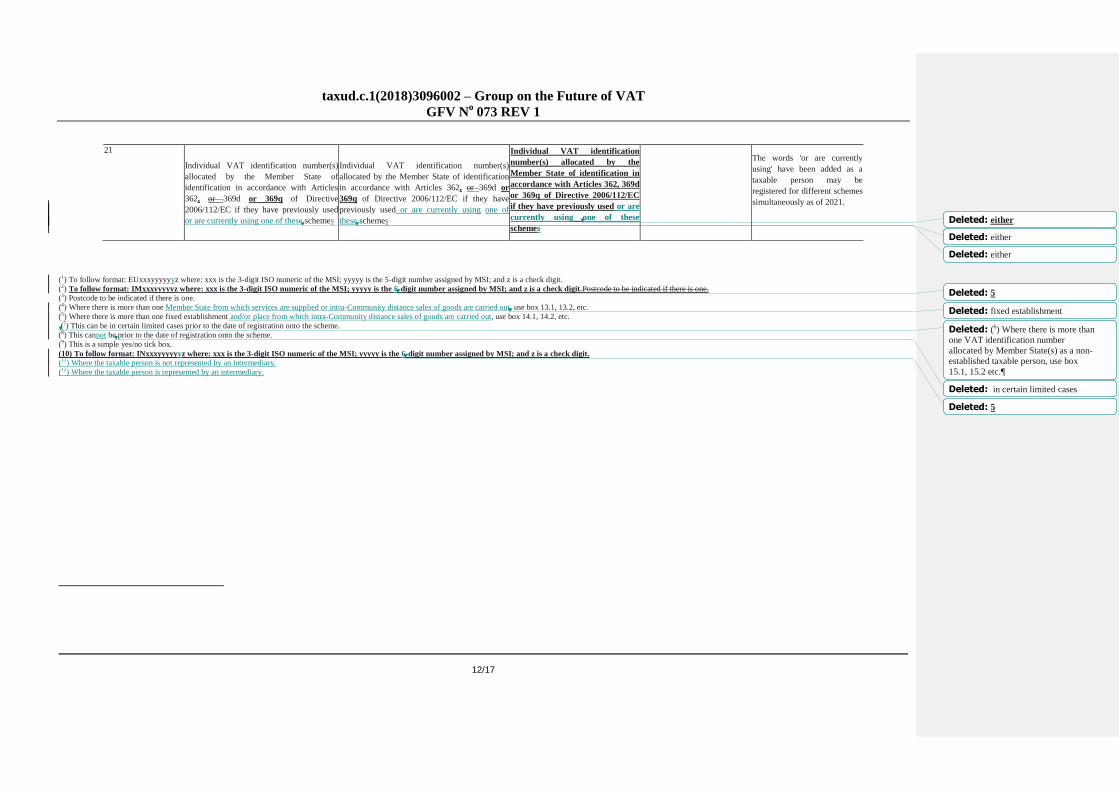

21

Individual VAT identification number(s)

allocated by the Member State of

identification in accordance with Articles

362, or 369d or 369q of Directive

2006/112/EC if they have previously used

or are currently using one of these schemes

Individual VAT identification number(s)

allocated by the Member State of identification

in accordance with Articles 362, or 369d or

369q of Directive 2006/112/EC if they have

previously used or are currently using one of

these schemes

Individual VAT identification

number(s) allocated by the

Member State of identification in

accordance with Articles 362, 369d

or 369q of Directive 2006/112/EC

if they have previously used or are

currently using one of these

schemes

The words 'or are currently

using' have been added as a

taxable person may be

registered for different schemes

simultaneously as of 2021.

(1) To follow format: EUxxxyyyyyyz where: xxx is the 3-digit ISO numeric of the MSI; yyyyy is the 5-digit number assigned by MSI; and z is a check digit. (2) To follow format: IMxxxyyyyyz where: xxx is the 3-digit ISO numeric of the MSI; yyyyy is the 6-digit number assigned by MSI; and z is a check digit.Postcode to be indicated if there is one. (3) Postcode to be indicated if there is one. (4) Where there is more than one Member State from which services are supplied or intra-Community distance sales of goods are carried out, use box 13.1, 13.2, etc. (5) Where there is more than one fixed establishment and/or place from which intra-Community distance sales of goods are carried out, use box 14.1, 14.2, etc. (7) This can be in certain limited cases prior to the date of registration onto the scheme. (8) This cannot be prior to the date of registration onto the scheme. (9) This is a simple yes/no tick box.

(10) To follow format: INxxxyyyyyyz where: xxx is the 3-digit ISO numeric of the MSI; yyyyy is the 6-digit number assigned by MSI; and z is a check digit. (11) Where the taxable person is not represented by an intermediary.

(12) Where the taxable person is represented by an intermediary.

Deleted: either

Deleted: either

Deleted: either

Deleted: 5

Deleted: fixed establishment

Deleted: (6) Where there is more than one VAT identification number

allocated by Member State(s) as a non-established taxable person, use box

15.1, 15.2 etc.¶

Deleted: in certain limited cases

Deleted: 5

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

13/17

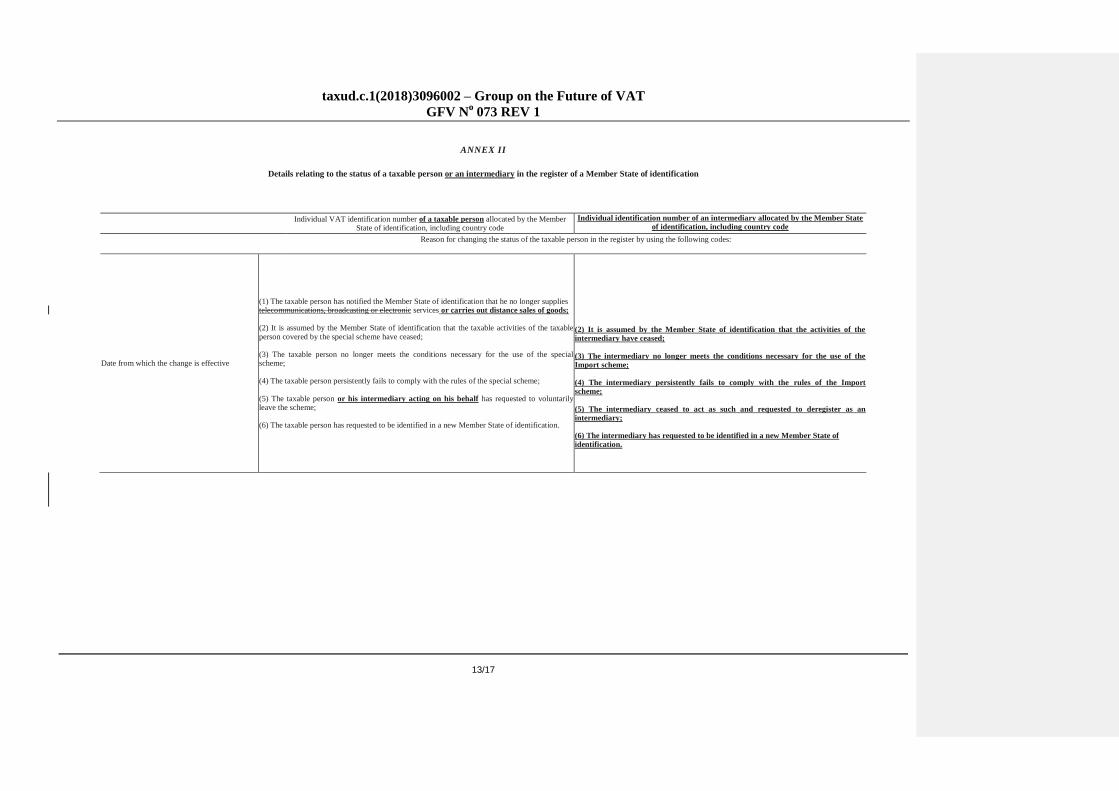

ANNEX II

Details relating to the status of a taxable person or an intermediary in the register of a Member State of identification

Individual VAT identification number of a taxable person allocated by the Member State of identification, including country code

Individual identification number of an intermediary allocated by the Member State of identification, including country code

Reason for changing the status of the taxable person in the register by using the following codes:

Date from which the change is effective

(1) The taxable person has notified the Member State of identification that he no longer supplies telecommunications, broadcasting or electronic services or carries out distance sales of goods; (2) It is assumed by the Member State of identification that the taxable activities of the taxable person covered by the special scheme have ceased; (3) The taxable person no longer meets the conditions necessary for the use of the special scheme; (4) The taxable person persistently fails to comply with the rules of the special scheme; (5) The taxable person or his intermediary acting on his behalf has requested to voluntarily leave the scheme; (6) The taxable person has requested to be identified in a new Member State of identification.

(2) It is assumed by the Member State of identification that the activities of the intermediary have ceased;

(3) The intermediary no longer meets the conditions necessary for the use of the Import scheme; (4) The intermediary persistently fails to comply with the rules of the Import scheme;

(5) The intermediary ceased to act as such and requested to deregister as an intermediary; (6) The intermediary has requested to be identified in a new Member State of identification.

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

14/17

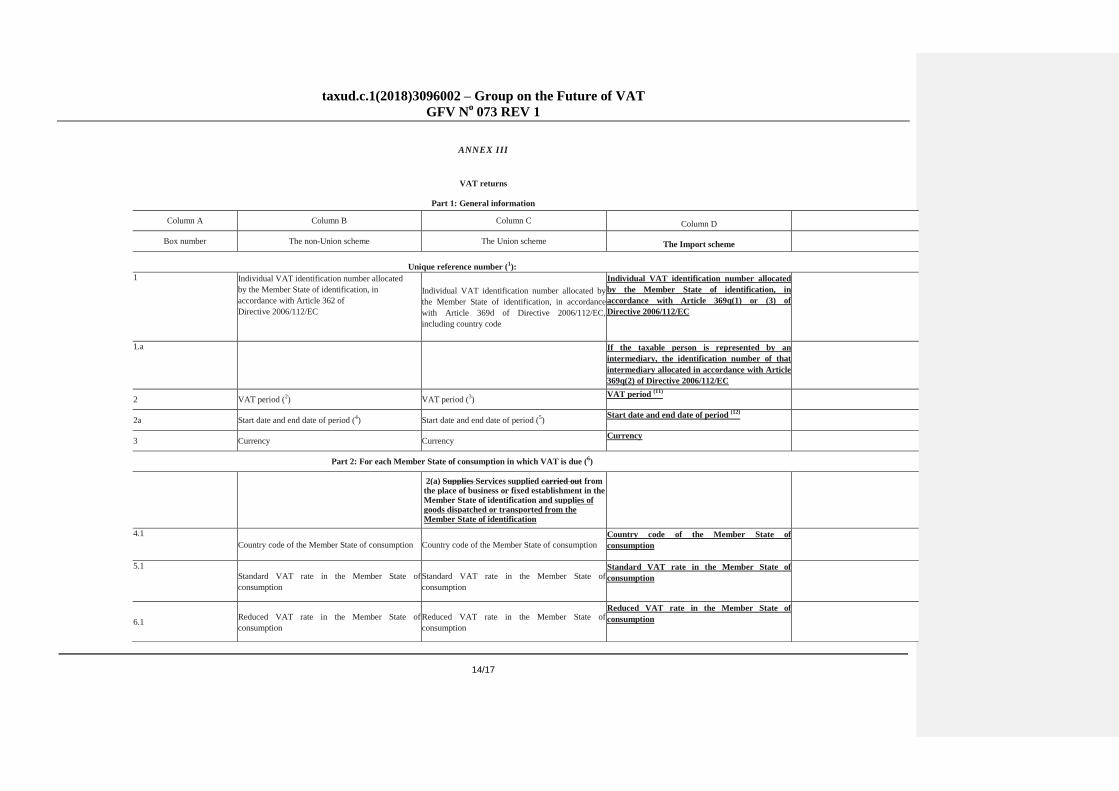

ANNEX III

VAT returns

Part 1: General information

Column A Column B Column C

Column D

Box number The non-Union scheme The Union scheme

The Import scheme

Unique reference number (1):

1 Individual VAT identification number allocated

by the Member State of identification, in

accordance with Article 362 of

Directive 2006/112/EC

Individual VAT identification number allocated by

the Member State of identification, in accordance

with Article 369d of Directive 2006/112/EC,

including country code

Individual VAT identification number allocated

by the Member State of identification, in

accordance with Article 369q(1) or (3) of

Directive 2006/112/EC

1.a

If the taxable person is represented by an

intermediary, the identification number of that

intermediary allocated in accordance with Article

369q(2) of Directive 2006/112/EC

2 VAT period (2) VAT period (

3)

VAT period (11)

2a Start date and end date of period (4) Start date and end date of period (

5)

Start date and end date of period (12)

3 Currency Currency Currency

Part 2: For each Member State of consumption in which VAT is due (6)

2(a) Supplies Services supplied carried out from the place of business or fixed establishment in the Member State of identification and supplies of goods dispatched or transported from the Member State of identification

4.1

Country code of the Member State of consumption Country code of the Member State of consumption

Country code of the Member State of

consumption

5.1

Standard VAT rate in the Member State of

consumption

Standard VAT rate in the Member State of

consumption

Standard VAT rate in the Member State of

consumption

6.1 Reduced VAT rate in the Member State of

consumption

Reduced VAT rate in the Member State of

consumption

Reduced VAT rate in the Member State of

consumption

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

15/17

7.1 Taxable amount at standard rate Taxable amount at standard rate (services; goods; total)

Taxable amount at standard rate

8.1 VAT amount at standard rate VAT amount at standard rate VAT amount at standard rate

9.1 Taxable amount at reduced rate Taxable amount at reduced rate (services; goods; total)

Taxable amount at reduced rate

10.1 VAT amount at reduced rate VAT amount at reduced rate VAT amount at reduced rate

11.1 Total VAT amount payable

Total VAT amount payable for supplies of services

carried out supplied from the place of business or

fixed establishment in the Member State of

identification

Total VAT amount payable

2(b) Supplies Services carried out supplied

from fixed establishments not in the Member

State of identification (7)

Part 2(c) is added as supplies of

services from fixed establishments

and distance sales from Member

States other than the MS of identification must be declared

separately where a taxable person

would supply both services and

goods from the same Member State.

Boxes 12.1 to 20.1 apply separately

to supplies of services and distance

sales of goods.

2(c) Supplies of goods dispatched or

transported from a Member States other than

the Member State of identification (7)

12.1

Country code of the Member State of consumption

13.1 Standard VAT rate in the Member State of

consumption

14.1 Reduced VAT rate in the Member State of

consumption

15.1

Individual VAT identification number, or if not

available tax reference number, allocated by the

Member State of fixed establishment for supplies of

services or by the Member State from which the

taxable person carries out intra-Community

distance sales of goods, including country code

16.1

Taxable amount at the standard rate

Deleted: and supplies of goods

dispatched or transported from a

Member States other than the Member

State of identification

Deleted: of

Deleted: places

Deleted: (services; goods; total)

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

16/17

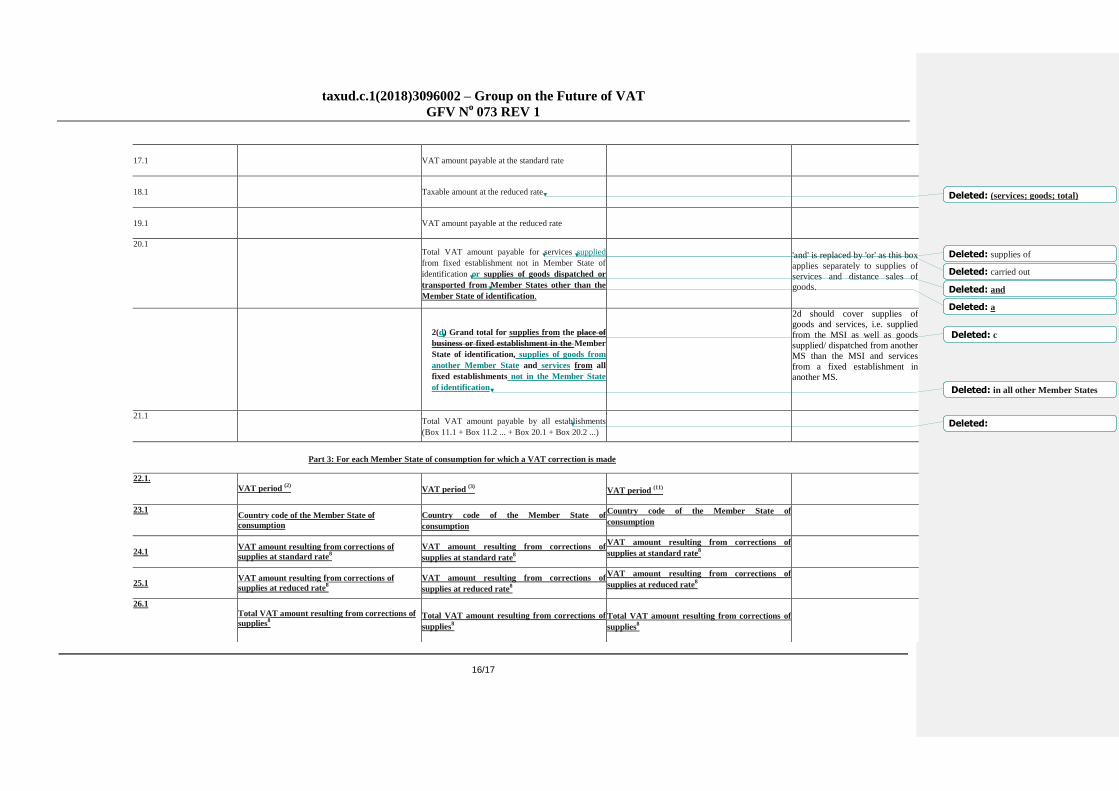

17.1

VAT amount payable at the standard rate

18.1

Taxable amount at the reduced rate

19.1

VAT amount payable at the reduced rate

20.1 Total VAT amount payable for services supplied

from fixed establishment not in Member State of

identification or supplies of goods dispatched or

transported from Member States other than the

Member State of identification.

'and' is replaced by 'or' as this box

applies separately to supplies of

services and distance sales of goods.

2(d) Grand total for supplies from the place of

business or fixed establishment in the Member

State of identification, supplies of goods from

another Member State and services from all

fixed establishments not in the Member State

of identification

2d should cover supplies of goods and services, i.e. supplied

from the MSI as well as goods supplied/ dispatched from another

MS than the MSI and services

from a fixed establishment in another MS.

21.1 Total VAT amount payable by all establishments

(Box 11.1 + Box 11.2 ... + Box 20.1 + Box 20.2 ...)

Part 3: For each Member State of consumption for which a VAT correction is made

22.1.

VAT period (2)

VAT period (3)

VAT period (11)

23.1 Country code of the Member State of

consumption

Country code of the Member State of

consumption

Country code of the Member State of

consumption

24.1 VAT amount resulting from corrections of

supplies at standard rate8

VAT amount resulting from corrections of

supplies at standard rate8

VAT amount resulting from corrections of

supplies at standard rate8

25.1 VAT amount resulting from corrections of

supplies at reduced rate8

VAT amount resulting from corrections of

supplies at reduced rate8

VAT amount resulting from corrections of

supplies at reduced rate8

26.1 Total VAT amount resulting from corrections of

supplies8

Total VAT amount resulting from corrections of

supplies8

Total VAT amount resulting from corrections of

supplies8

Deleted: (services; goods; total)

Deleted: supplies of

Deleted: carried out

Deleted: and

Deleted: a

Deleted: c

Deleted: in all other Member States

Deleted:

taxud.c.1(2018)3096002 – Group on the Future of VAT

GFV No 073 REV 1

17/17

(1) Unique reference number as allocated by the Member State of identification shall consist of country code of MSI/VAT number/period - i.e. GBCZ/xxxxxxxxx/Q1.yy (or M01.yy for the Import scheme) + add timestamp for each version. The number shall be attributed by the Member State of identification before transmission of the return to the other Member States concerned.

(2) Relates to calendar quarters: Q1.yyyy - Q2.yyyy - Q3.yyyy Q4.yyyy. (3) Relates to calendar quarters: Q1.yyyy - Q2.yyyy - Q3.yyyy Q4.yyyy. (4) To be completed only in cases where the taxable person submits more than one VAT return for the same quarter. Relates to calendar days: dd.mm.yyyy - dd.mm.yyyy. (5) To be completed only in cases where the taxable person submits more than one VAT return for the same quarter. Relates to calendar days: dd.mm.yyyy - dd.mm.yyyy. (6) Where there is more than one Member State of consumption (or if in a single Member State of consumption there has been a VAT rate change in the middle of a quarter/month), use box 4.2, 5.2, 6.2 to 11.2,

etc. (7) Where there is more than one fixed establishment or more than one Member State other than the Member State of identification from which goods are dispatched or transported, use box 12.1.2 to 20.2,13.1.2 14.1.2

etc. (8) This amount can be negative. (9) Negative amounts in boxes 26.1, 26.2, etc. can only be taken into account to the extent that they do not exceed the amounts in boxes 11.1, 11.2, etc. (10) Negative amounts in boxes 26.1, 26.2, etc. can only be taken into account to the extent that they do not exceed the amounts in boxes 21.1, 21.2, etc. (11) Relates to calendar months: M01.yyyy – M02.yyyy – M03.yyyy – etc. (12) To be completed only in cases where the taxable person submits more than one VAT return for the same month. Relates to calendar days: dd.mm.yyyy - dd.mm.yyyy.

Part 4: Balance of VAT due for each Member State of consumption

27.1.

Total VAT amount due including corrections of

previous returns per Member State (Box 11.1 +

Box 11.2 … + Box 26.1 + Box 26.2. …)9

Total VAT amount due including corrections of

previous returns per Member State (Box 21.1 +

Box 21.2 … + Box 26.1 + Box 26.2. …)10

Total VAT amount due including corrections of

previous returns per Member State (Box 11.1 +

Box 11.2 … + Box 26.1 + Box 26.2. …)9

Part 5: Total Amount of VAT due for all Member State of consumption

28.

Total VAT amount due for all Member States

(Box 27.1+ 27.2. …)

Total VAT amount due for all Member States

(Box 27.1+ 27.2. …)

Total VAT amount due for all Member States

(Box 27.1+ 27.2. …)

Deleted:

Deleted: 1