gcc demographic shift - markaz...gcc demographic shift intergenerational risk-transfer at play ......

TRANSCRIPT

Kuwait Financial Centre “Markaz”

R E S E A R C H

GCC Demographic Shift Intergenerational risk-transfer at play

“At some point around 1800, after untold millennia of human history,

the global population reached its first billion. The world’s population

now grows by 1 billion about every 12 years” -2010 World

Population Datasheet, Population Reference Bureau.

The demographic structure of a country or region has wide-ranging

implications, from health and education, to labor force make-up and fiscal budgeting. The population is the driving force of an economy; it is

the unit by which economic output is realized and as such, should be invested in and shaped in a manner to better influence economic

growth.

That being said, population – no matter the structure – constitutes a burden on the country’s fiscal budget. An old population will be exiting the workforce, and hence their productivity will drop, while at the same time their retirement compensation, i.e. social security, will be drawn

upon, draining fiscal reserves. Conversely, a very young population also

requires a great deal of government expenditure, particularly in welfare-based states such as the Gulf, in terms of , education,

subsidies, and wages.

The GCC is in a unique position of having an extensive welfare system based on hydrocarbon revenues; this has created a growing drain on

fiscal reserve as the demographic structure is skewed towards the younger population which is entering the labor force in higher numbers

each year.

The GCC has a low population, when compared with other regions,

totaling 45 mn people in 2011, less than 1% of the global population. Moreover, the region is young with 54% under the age of 25, though

this is expected to rise to about 36 by 2050.

The current demographic structure has created several pressure points for the GCC economies. The report pinpoints these pressure points,

explains their implications and offers alternative reforms for them.

Figure 1: GCC Population Pyramid – 2010/2050

Source: US Census

June 2012

Research Highlights:

Analyzing the demographic structure of the GCC in

addition to implications on various economic and fiscal

aspects

Markaz Research is

available on Bloomberg

Type “MRKZ” <Go>

M.R. Raghu CFA, FRM Head of Research +965 2224 8280

Mai Sartawi

Intern

Kuwait Financial Centre

S.A.K. “Markaz”

P.O. Box 23444, Safat 13095, Kuwait

Tel: +965 2224 8000 Fax: +965 2242 5828

www.markaz.com

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

2

Table of Contents

1. Overview .................................................................................................... 3

GCC Demographic Structure ................................................................................. 6

2. Pressure Points ........................................................................................ 13

Welfare ............................................................................................................. 13

Housing ............................................................................................................ 15

Education.......................................................................................................... 16

Employment ...................................................................................................... 20

3. Policy Agenda .......................................................................................... 25

Housing Reform ................................................................................................ 25

Education Reform .............................................................................................. 25

Governance and Regulation of Education Sector .................................................. 26

Labor Reform .................................................................................................... 26

Appendix 1: MENA Statistics ......................................................................... 28

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

3

1. Overview

The global population currently stands at just under 7 billion, nearly 40% of

which are in China and India. The third most populous country, the United States, is far behind at 312mn.

By 2050, the UN projects the world population to hit 9 billion, with India and

China’s share of world total declining to 30%. Nigeria will have usurped the United States as the third most populous nation, at 433mn. Russia and Japan

will have dropped out of the top ten, making way for Ethiopia and the

Philippines with 174mn and 150mn, respectively.

Table 1: World’s Most Populous Countries

2011 2050

Country Population (mn) Country Population (mn)

1 China 1,346 India 1,692

2 India 1,241 China 1,313

3 United States 312 Nigeria 433

4 Indonesia 238 United States 423

5 Brazil 197 Pakistan 314

6 Pakistan 177 Indonesia 309

7 Nigeria 162 Bangladesh 226

8 Bangladesh 151 Brazil 223

9 Russia 143 Ethiopia 174

10 Japan 128 Philippines 150

Source: 2011 World Population Data Sheet, Population Reference Bureau

Billion after Billion

The world is adding people at an alarming rate, adding over 80 mn people a year, despite world population growth rates declining to about 1.2% p.a. Birth

rates around the world are highly variable, with the number falling to two children per family in some countries while the same has barely decreased in other countries.

As seen below, the first billion total population was reached in the 1800s,

encompassing all of human history to that point, while the second billion was reached just 130 years later, in 1930. The rate of addition declined exponentially thereafter, with the fifth, sixth, and seventh billion milestones

reached in 12 year intervals.

This pattern suggests that the world could hit 8 billion in another decade, with 9 billion reached by 2035, i.e. 15 years ahead of the UN projection

Figure 2: Billionth Milestones

The global population currently stands at just under 7 billion,

nearly 40% of which are in China and India

The world is adding people at

an alarming rate, adding over 80 mn people a year

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

4

The Population Clock

Almost all of the world’s population is in less developed countries; consequently

the main driver of the global population is in those regions, where 27 infants are born per minute in developed countries, 239 are born in less developed

regions. Health care divergences and life expectancy have decreased the number of deaths per minute in developed countries at 23 versus 84 in their

less developed counterparts. Predictably, infant mortality is also higher is less developed countries, at 11 per minute or over 16,000 per day.

Table 2: The Population Clock

World

More Developed Countries

Less Developed Countries

Population 6,986,951,000 1,241,580,000 5,745,371,000

Births per Year 139,558,000 14,070,000 125,488,000

Day 382,351 38,548 343,803

Minute 266 27 239

Deaths per Year 56,611,000 12,201,000 44,410,000

Day 155,099 33,427 121,671

Minute 108 23 84

Natural Increase per (Birth-Death) Year 82,947,000 1,869,000 81,078,000

Day 227,252 5,121 222,132

Minute 158 4 154

Infant Deaths per Year 6,078,000 77,000 6,001,000

Day 16,652 211 16,441

Minute 12 0.1 11

Source: 2011 World Population Data Sheet, Population Reference Bureau

How Does the GCC Measure up?

As a region, the GCC has a very small population, with just around 45mn, less

than 1% of the global population. However, in contrast to the small population, the GCC is one of the wealthier regions, in terms of GDP/capita (at just under

$32,000), well above the MENA Ex. GCC, and in line with North America and

Europe.

Figure 3: Population versus GDP/capita

Source: IMF Note: Size of the Bubble indicates population percentage.

Asia

North America

MENA

Europe

GCC

0

10,000

20,000

30,000

40,000

50,000

60,000

0 1000 2000 3000 4000 5000

GD

P/

ca

pit

a (

US

D)

Population (Millions)

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

5

The Four Phases of Demographic Transition

(Excerpt - 2011 World Population Data Sheet, Population Reference Bureau)

In the parish of Mouy, north of Paris, there were 47 burials recorded in 1693; in 1694, the number jumped to

an appalling 262. This is a dramatic example of life during Phase 1 of the demographic transition (albeit a somewhat modern one compared to the 50,000 years of human existence that preceded Phase 1). A rise in

the price of grains meant more people could not afford food, a situation that nearly always led to excessive

mortality, as happened in Mouy.

In Phase 2 of the transition—roughly the beginning of the Industrial Revolution—death rates began to fall more regularly, although the preference for larger families may have remained for a time. Next, increasing

urbanization lessened the need for children even as early public health measures improved life spans. Now the transition was really underway. By the 20th century, the development of modern medicine and the desire to

limit family size combined to cause the low death rates and very low birth rates we see today. That, at least,

is what happened over the centuries in Europe and North America. Most developing countries arrived in the 20th century still in the first phase of the transition. In the aftermath of World War II, however, the benefits

of public health and modern medicine became available to them in a comparatively short period of time. Mortality fell with unusual rapidity but the desire for large families remained. Then, with mounting concern

over record rates of population growth, birth rates did begin to fall in many countries.

Today, we can find examples around the world of all four stages of the transition.

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

6

GCC Demographic Structure

Size and Growth

The GCC has a low population, when compared with other regions, totaling

nearly 45 mn people in 2011. The most populated country is Saudi Arabia with 28 mn (65% of the total), followed by nearly 8 mn in the UAE. The

International Monetary Fund forecasts a compounded growth rate (CAGR) of

2.41% in the next 5 years, increasing the population further to 49 mn in 2016. The growth rate is substantially lower than the CAGR throughout 2004-2008 of

5.9%.1 By 2025, the GCC is expected to have a total population of 57mn, to grow by

about 14mn more by 2050.

As of 2011, the lowest median age in the GCC is 24 yrs in Oman and the highest is 31 yrs in Qatar. The average age in the entire GCC region is 27 yrs

with over 20% below the age of 15.

Table 3: GCC Population Statistics

Population mid-2011 (mn)

Births per 1,000 pop.

Deaths per 1,000 pop.

Rate of Natural Increase

%

Projected Population

(mn)

2050 pop. as

multiple of 2011

Infant Mortality Rate

Total Fertility Rate

% of population

ages

mid-2025

mid-2050

<15 65+

World 6,987 20 8 1.2 8,084 9,587 1.4 44 2.5 27 8

Saudi Arabia 27.90 21 4 1.8 36.0 44.6 1.6 18 2.9 31 3

United Arab Emirates

7.90 13 1 1.2 9.9 12.2 1.5 7 1.8 18 1

Oman 3.00 29 3 2.6 3.9 5.3 1.8 12 3.3 24 2

Kuwait 2.80 19 3 1.6 3.7 5.2 1.8 9 2.3 26 3

Qatar 1.70 11 1 1.0 2.1 2.4 1.4 8 2.1 14 1

Bahrain 1.30 15 2 1.3 1.7 2.0 1.5 7 1.9 20 2

GCC Total* 44.6 18 2 1.6 57.3 71.7 1.6 10 2.4 22 2

* All GCC averages denote the average of six member nation figures Source: 2011 World Population Data Sheet, Population Reference Bureau

The Pyramids

The population pyramid in more developed countries (Figure ) is relatively uniform, with a small tapering at the higher age range. The median age for the

developed world is over 35. By contrast, developing countries have a bottom heavy pyramid, indicating support for the aging population through youth

entering the labor force; here the median age remains below 30, with some

countries having a median age of 24. But developing countries’ pyramids are liable to change with modernization, increased life expectancy, and family

planning.

By 2050, the developed world pyramid becomes more column-like, with the bulk of the population in the higher age brackets; the median age will have

increased to 45 in some cases such as Europe, while remaining in the low 40s

in the US.

1 GCC Population Forecast to Reach 50 Million in 2013, Business Intelligence Middle East, 18 February 2012

The GCC has a low population,

when compared with other regions, totaling nearly 45 mn

people in 2011

By 2050, the developed world

pyramid becomes more

column-like, with the bulk of the population in the higher age brackets

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

7

In the developing world, the pyramid also bulges at the mid-age range by 2050

as the younger population ages and birthrates decline or slow. The median age

will increase to around 37 by then.

Figure 4: Population Pyramids – Developed World vs. Developing World 2010/2050

Source: US Census

GCC Pyramids

The fertility rate in the GCC has been declining as there is greater awareness of

family planning. With the exception of Oman, all other GCC countries’ fertility rates have decreased by more than 50%.2 This could also be correlated to the

increased cost of living as well as increased education opportunities for women. As the age of marriage increases, this decreasing trend in birth rates is

expected to continue.

Moreover, GCC pyramids have a skewed bulge in the male bracket, specifically working age, which is due to the high number of male expatriates in the

countries.

Saudi Arabia’s population pyramid is expansive3 showing that the majority of

the population is below the age of 30, with a median age of 26. This alludes that there is a high birth rate as well as a high death rate and a relatively short

life expectancy. However, a decreasing birth rate suggests that the pyramid will

2 Arab Human Development Report, United Nations Development Program, 2010 3 Smaller Old age population and the number of people in each age group increases as we move down the population pyramid

The fertility rate in the GCC

has been declining as there

is greater awareness of family planning

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

8

transform into a contractive pyramid where the majority of the population is in the middle ages as seen in the 2050 chart.

Figure 5: Saudi Arabia and Kuwait Population Pyramids - 2010/2050

Source: US Census

Kuwait’s pyramid is less expansive than Saudi Arabia’s, with most of its

population below the age of 35 yrs, but over 20. There is also more discrepancy between the higher numbers of males to females, particularly in the 20-40 age

brackets. This is attributed to the high flow of expatriates looking for

employment, usually in this age bracket. The high expatriate rate is expected to decrease as more nationals enter the labor force and demand jobs. Similar to Kuwait, UAE also has a very high expatriate rate. UAE’s population

pyramid would look more expansive if it was exclusive to the national population. However, its total population, including expatriates, is a more

contractive pyramid with the majority of the population between the ages of

20-60. The UAE population’s growth is expected to continue, driven by a steady inflow of expatriates.

Qatar has the highest expatriate rate in the region. Its population pyramid alludes to it with the higher percentage of males in all working age groups,

above the age of 20. Qatar’s demographic boom is accompanied by its economic boom that gave rise to many opportunities for expatriates. However,

population growth is expected to decrease as expatriates exit to be replaced by local talent

Kuwait’s pyramid is less

expansive than Saudi

Arabia’s, with most of its population below the age of

35 yrs, but over 20

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

9

Figure 6: Qatar and UAE Population Pyramids – 2010/2050

Source: US Census

Oman’s population pyramid is the most expansive in the GCC region. Similar to

Saudi Arabia, Oman has the second highest population of nationals compared

to expatriates in the region. The majority of Oman’s population is also under the age of 25. The pyramid is projected to become more contractive as the

fertility rate decreases and health care services are availed of.

Bahrain is the least populated country in the GCC. Its population pyramid shows

that there is no huge discrepancy between the age groups. There is also an equal distribution of males to females, with exception of the 40-60 yrs age

brackets. Bahrain population is expected to grow.

Bahrain is the least populated country in the

GCC. Its population pyramid shows that there is no huge discrepancy between the age group

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

10

Figure 7: Bahrain and Oman Population Pyramids – 2010/2050

Source: US Census

While the younger age group (15-24) comprises the bulk of the Arab population, growth rates among countries differ greatly and are falling over

time, indicating that this bracket will experience declining growth rates going forward. Between 1995-2010 Yemen had the highest rate among Arab

countries, with the youth population nearly doubling, however this is expected

to grow by under 40% over the next 15 years.

Saudi Arabia saw its youth population grow by 66% over the last 15 years, but this rate is expected to fall to just 15% through 2025.

It is interesting to note that the youth population aged 15-24 will decline in

Iran, Algeria, Morocco, Tunisia, Lebanon, and Turkey over the next 15 years,

indicating sharply declining birth rates and/or increased infant mortality rates.

While the young bracket (15-

24) comprises the bulk of the Arab population, growth

rates among countries differ greatly and are falling over time

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

11

Figure 8: Youth Population Growth

Source: 2011 World Population Data Sheet, Population Reference Bureau

The “Expat” Factor

The majority of the GCC population consists of expatriates. Based on 2010

data, Credit Suisse reported Qatar as having 86.5% expatriates, the highest percentage of international migrants in the world, although these tend to have

a transient quality and migrate in and out on a seasonal basis. This is followed

by 70% and 68.8% in Kuwait and the UAE, respectively.

The GCC region as a whole has an average of 53.43% of expatriates compared to an average of 9.5% in the MENA region. Qatar has the largest immigration

rate in the world with 40.62 of 1,000 people entering the country being expatriates. None of the GCC countries have a negative net immigration rate

which indicates that there is always a higher rate of expatriates entering than

leaving the region.

Source: Credit Suisse

The high inflow of expatriates is reflected in the GCC labor force. The positions

filled by expatriates range from low-paying, low-skilled construction jobs to highly professional and specialized jobs. Nearly, , 4.5 million nationals are

potentially entering the job market compared to 5 million nationals who were

employed in 2010. IMF predicts that an additional 2 to 3 million nationals will not be able to find employment.4

4 Meeting the Unemployment Challenge, Masood Ahmed, 19 January 2012

Table 4: Expatriates Population 2010

Qatar 86.5%

UAE 70%

Kuwait 68.8%

Bahrain 39.1%

Oman 28.4%

Saudi Arabia 27.8%

The majority of the GCC population consists of expatriates

The GCC region as a whole has an average of 53.43% of

expatriates compared to an

average of 9.5% in the MENA region

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

12

Fiscal Situation

The GCC is a distinctive region due to its unique hydrocarbon reserves

compared to a relatively small, although increasing, national population. Growth in the six economies, in terms of spending and GDP/Capita as well as welfare,

heavily relies on oil rent to attract private investors and to provide extensive public services and subsidies to nationals. With not enough diversification in the

economy, the GCC countries’ government spending will continue to cause a

drain on fiscal accounts.

Based on unchanged policies and historic trend, the International Monetary Fund (IMF) forecast a 2% annual growth in real GDP for the rest of the decade. In addition, IMF also predicted an annual increase in population of 3.5%. The

imbalance in growth rates requires GCC governments to look closer at their policies to better match macroeconomics priorities and objectives.

Fiscal Balance as a % of GDP has been decreasing in all GCC countries, in

standing budget deficit which is expected to increase to 9.7% this year.5 UAE was also severely affected by the financial crisis due to their broad exposure to

the global Oman, Saudi Arabia and Bahrain government expenditures exceeded

revenues in 2009 as the economies were downturned during the financial crisis, causing government budget deficits. Saudi and Oman recovered the following

year, on higher oil prices, yet Bahrain is still suffering from its long market.

Figure 9: Fiscal Balance as % of GDP

Inefficient policies to allocate governments’ budgets will cause the GCC to experience continued and exacerbated fiscal drain. GCC citizens feel

unaccountable for their welfare, the current education systems do not provide

them with world-class, competitive skills, government employment and unemployment benefits remove the incentive for specialization and dynamic job seeking and the lack of skilled national manpower, and consequent dependence on expatriate labor will remain. Reforms are needed to aid countries to diversify

their economies to head away from an unrestrained fiscal drain.

5 Bahrain’s Budget Deficit up 5-fold in 10 Years, SyndiGate.info, 4 April 2012

The GCC is a distinctive region due to its unique hydrocarbon reserves compared to a relatively

small, although increasing,

national population

Inefficient policies to allocate governments’ budgets will

cause the GCC to experience continued and exacerbated fiscal drain

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

13

2. Pressure Points

Welfare

GCC countries are known for their generous and extensive welfare system. The

government distributed its oil revenues for strategic reasons to ensure available essential services. Most government services are either at no cost or at highly subsidized prices such as electricity, water, gas, healthcare and commodities

such as food. Except for Oman where local companies are taxed, taxes in the other GCC countries mainly consist of foreign corporation income taxes.

This welfare system is strained and exasperated by the Elderly Support Ratio,

which calculates the degree to which the youth population is able to support

the aging and retired. Currently, on a global scale, there are 9 working age persons supporting one non-working age person while in the GCC the ratio is

significantly higher, with the UAE and Qatar having the highest at nearly 80 people in support of one senior citizen.

However, a stark reversal is expected in just 40 years, when this ratio is expected to drop to the low single digits across the GCC. This essentially means

that by 2050, Kuwait, for example, will have just 3 working age persons supporting one senior citizen; this will constitute a major strain on resources for

the country.

Table 5: GCC Elderly Support Ratio

Elderly Support

Ratio* Life Expectancy at Birth

(yrs)

2010 2050 All Male Female %

Urban Pop. Per km2

GDP/capita (US$) – 2009

Mobile

Subscribers per 100

inhabitants

World 9 4 69 67 71 50 51 10,030 60

United Arab

Emirates 79 9 77 77 79 83 14 38,960 143

Qatar 78 5 76 75 77 100 152 61,532 131

Bahrain 32 4 75 73 77 100 1,807 17,609 186

Kuwait 32 3 78 76 80 98 175 41,365 100

Saudi Arabia 22 5 76 74 78 81 64 13,901 209

Oman 21 4 72 70 74 72 10 17,280 116

* Elderly Support Ratio = Working age population (age 15-64)/ Population 65+ Source: 2010 World Population Data Sheet, Population Reference Bureau, GDP/Capita sourced from World Bank Data

Kuwait’s welfare system subsidizes many of its citizens’ essential needs such as government housing for employed married Kuwaitis, free healthcare, and free

education. Kuwait’s welfare housing is emphasized more as a form of

sustenance for low-income citizens and Bedouins. Expenses on subsidies and other transfers were almost all of the Kuwaiti government’s expenses after the

Gulf War. In 2010, welfare expenses took up 30% of all government expenses.

Similar to Kuwait, the Saudi Arabia housing program exists to guarantee housing for lower income nationals. Saudi Arabia successfully implemented

developmental plans from 1970 to 1995 encompassing social services and free

healthcare and a system of free enterprise, which requires and encourages the private sector to play a bigger role in the economy.6 Saudi’s subsidies alone

6 A Welfare System, Kingdom of Saudi Arabia Ministry of Foreign Affair

GCC countries are known for

their generous and extensive

welfare system

In 2010, welfare expenses

took up 30% of all Kuwait government expenses

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

14

make up a large percentage of total expenditure. For example, subsidies expense on electricity accounted for 9% of total expenditure in 2009.7

UAE’s welfare system is as encompassing as the other GCC countries. Welfare expenses fell to a little more than 10% of total expenditure in 2009 after

steadily increasing to reach 25% of expenditure in 2006 (Figure 4). The retail price of fuel increased three times in the UAE. The volatile world oil prices have

made most GCC countries more aware of a need to reform their subsidies and

welfare system. For example, Qatar increased fuel prices by 25% and Saudi reduced domestic wheat production which relies on heavy subsidies. Regional

inflation is better controlled with measured reduction on state subsidies. Qatar’s Ministry of Labor and Social Affairs provides free education and health

services as well as assistance for those in need such as orphans and widows. Free healthcare extends to all residents of Qatar, regardless of nationality.

Qatar’s expenses on welfare equaled a little more than 20% of total expenditures in 2009.

Bahrain’s welfare system includes a social security system which provides

citizens with several benefits. Foreign corporations contribute to the system as

well as employers. Benefits contain health care payments, housing benefits, and unemployment benefits. Health care is free for citizens. A state pension

scheme is also available for citizens of the country but require a percentage payment of income to be accessed.

Bahrain’s expenses on welfare in 2008 reached its highest since 1990 reaching

around 20% of all government expenses.

Oman’s welfare average expenses as a percentage of government expenditure is the lowest in the GCC region. Healthcare subsidies alone are 5% of total

expenditure.8 In addition to education and interest on housing, Oman subsidizes development loans, farmers and fishermen equipment, and some

exemptions from in income tax for some companies. Oman is expecting to

allocate 8.5% of total expenditure on welfare for its 2012 budget.9

GCC governments use welfare to provide a high standard of living for their citizens. Citizens of the GCC rely on their country’s welfare system without

feeling any sense of accountability, unlike when citizens pay taxes for public services. In return, citizens’ expectations for welfare grow as they remain

unconscious of the expensive cost of their governments’ far-reaching subsidies

and transfers.

With the help of an extensive welfare system, GCC citizens’ wealth has been increasing at the cost of a fiscal drain on government accounts. Citizens can

afford unemployment, living off the paradise supply of transfers from their

governments which derive from unsustainable oil rent. Welfare in the GCC is creating adverse incentives to its citizens by indirectly demotivating dynamic job seeking attitudes since there is little fear of unemployment. Kuwait’s government spending and welfare spending was the highest recorded in 2009.

Welfare spending included a one time payment of KD 5.5 billion for the Public Institution for Social Security.10

7 Employment and Salary Trend in the Gulf 2010, GulfTalent, 2011 8 The State General Budget for 2012, Omanet, 2011 9 Oman Budget 2012, Ministry of National Economy, 15 January 2012 10 Assembly Closes Term by Approving ‘Crazy’ Budget, Kuwait Times, 30 June 2011

Qatar’s expenses on welfare equaled a little more than 20% of total expenditures in 2009

Oman’s welfare average

expenses as a percentage of government expenditure is the lowest in the GCC region

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

15

Figure 10: Welfare as % of Government Expenses

Source: IndexMundi Database and UAE National Accounts 2009

Housing

In addition to public services and subsidies, increasing demand for housing with

a rising population requires additional spending on infrastructure. Governments in the GCC are aware of the demographic boom and its resulting pressure on

the government’s fiscal budget.

Some residential markets in the GCC are already facing shortages due to

increasing demand for housing. Sale prices for residential properties increased in 2011 compared to 2010. There is a strong demand for compounds and a

short supply, leading to growth in the rental segment. Riyadh’s office market is facing an oversupply and moderate demand.11

Similar to Saudi Arabia, Kuwait is facing a strong demand for residential housing. Growth in the real estate market is mainly driven by the residential

segment. Only Kuwaiti nationals are permitted to buy residential property.12 National Bank of Kuwait sourced robust credit growth which is stimulating

private residential segment growth.13

Dubai’s real estate suffered the most in the GCC region. There is an oversupply

of rental apartments which caused downward pressure on prices. Oversupply is due to delayed projects from 2011, which are adding to residential units. Office

space rental prices declined and are expected to continue to decline in 2012. In Abu Dhabi also commercial segment faces low demand.

In Oman, the demand for higher-end properties has been decreasing as the demand for affordable housing increases. The residential property market is

expected to improve in 2012. The lower priced areas Bowsher and Mawaleh face increased demand, and villas in the Waves and Muscat are still demanded

by foreigners due to their higher quality and modern design as they are short in supply.14

Qatar was the least affected country by the global financial crisis. Qatar is suffering from an oversupply in the residential and commercial property market.

Rental prices have been declining in Doha. The Qatari government is expected

11 Real Estate Commentary, Kuwait Financial Centre’Markaz’, 26 February 2012-03 March 2012

12 GCC Real Estate- Back on Growth? Al Masah Capital, 13 March 2011 13Real Estate Market Commentary, Kuwait Financial Centre ‘Markaz’, 25 March 2012 14 Real Estate Market Commentary, Kuwait Financial Center ‘Markaz’. 12 February 2012

In addition to public services and subsidies, increasing

demand for housing with a

rising population requires additional spending on

infrastructure

Growth in the real estate

market is mainly driven by

the residential segment

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

16

to increase spending for infrastructure in preparation for the 2022 World FIFA Cup. Qatar’s current main concern is attracting foreigners to buy property and

hosting them in 2022, benefiting Qatar’s real estate market. However,

foreigners’ ownership permits are limited to designated areas. Similar to Saudi Arabia, Qatar has potential for growth as demand rises for affordable housing.

The Bahraini residential market is slowing down in both the free-hold and

leasehold segments. There has been a declining trend in the residential rental

market and are expected to remain flat throughout the year. Office Rentals have declined compared to the third quarter of 2011. This is due to supply-side

competition between demanded small offices against large unfitted units.15 Residential supply is also expected to decrease due to the political unrest in the country. Bahrain and UAE are expected to face declines in the real estate

market due to an over supply and decreased demand for rentals.

Generally, GCC real estate is stabilizing in terms of commercial rentals due to an oversupply.. Most GCC countries are facing an increased demand for

affordable housing, which demands extensive spending on infrastructure. As population increases, GCC countries should allocate infrastructure spending to

provide their citizens with affordable housing needs before accommodating

expatriates and attracting foreign investments.

a) Government Developmental Plans

GCC governments’ fiscal balances could face a severe drain with the rising pressure on infrastructure and housing. GCC countries are already taking

initiatives with infrastructure and development plans. Kuwait’s development plan

is allocating KD995 mn on human and social development agencies. Effectively, for the years 2009-2010 and 2010-2011, respectively, 5,169 and 6,740 housing

units and houses were built. 16

In Saudi Arabia, Alwaleed Bin Talal Foundation initiated a Housing Development Program in 2003. The project identified low-income families in need. In addition,

King Abdulla has allocated $62 billion to build 500,000 homes in Jeddah with an

addition of $15 billion to fund 1.65 million homes in over five years. Such immediate public spending ambitiously provides incentive for short-term

development in construction and other support sectors.17

Education

Except for Oman, all GCC citizens belonging to the matching age group are

enrolled in primary education.18 Oman primary gross enrollment ratio was 75% in 2008 which causes a high illiteracy rate in the country, reflecting its high

unemployment rate of 15%.

15 Real Estate Market Commentary, Kuwait Financial Centre “Markaz”, 08 April 2012-14 April 2012 16 The Supreme Council for Planning and Development- State of Kuwait 17 Saudi Construction Leads the Region, Construction Week Online, March 31 2012 18 Primary education is preceded by nursery or pre-school and is also known as elementary school.

Secondary education is preceded by elementary school, and is also known as high school. Tertiary education is usually preceded by high school and is also known as higher education such as college or university curriculum.

Qatar is suffering from an oversupply in the residential

and commercial property

market

GCC governments’ fiscal

balances could face a severe

drain with the rising pressure on infrastructure and housing

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

17

Figure 11: Gross Enrollment Ratio (2008)

Source: Alpen Capital Report

In 2008, GCC’s secondary education gross enrollment ratio average was a high

93.3% with Bahrain leading at 96.8% and Oman lagging at 88.1%. Having a

primary gross enrollment ratio lower than a secondary gross enrollment ratio forecasts a lower secondary gross enrollment ratio in future, which could be

problematic for Oman. On the other hand, Oman is focusing on tertiary education. ; however, this will create a great imbalance between its citizens’

education. Primary education is necessary to increase the literacy rate of Oman, which was recorded as 86.6% in 2008.19

For the year 2020, Alpen Capital forecast that primary and secondary enrollment to reach 100% in all GCC countries. Bahrain’s tertiary enrollment is

predicted to be the highest in the region at 57.6% by 2020. Qatar’s tertiary enrollment is forecast to improve but growth is expected to be slow, resulting in

the lowest enrolment among the GCC nations at 15.7% in 2020. The GCC

average for tertiary enrollment is forecast to improve by 14.6% to reach 38.6% in 2020.

Figure 12: Tertiary Enrollment Forecast

Source: Indexmundi

With rising GDP/capita, the GCC population has become more aware of the necessity of education. Primary completion rate has risen as well as secondary

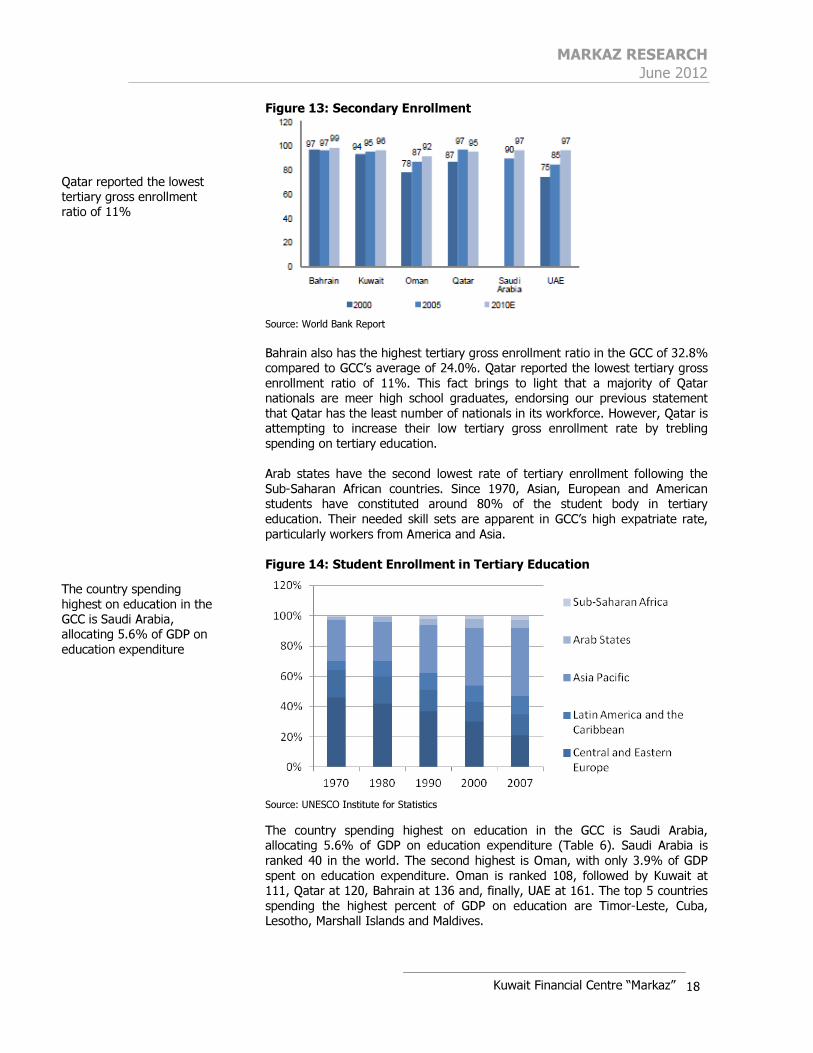

enrollment throughout the region. For 2010, IMF estimated Secondary enrollment to reach an average of 96% in the GCC region. UAE secondary enrollment has been increasing at the fastest pace. This is coupled with the rise in UAE’s exposure to global standards through its international economy (Figure

6).

19 Indexmundi Database

Bahrain’s tertiary enrollment is predicted to be the highest

in the region at 57.6% by 2020

With rising GDP/capita, the GCC population has become

more aware of the necessity of education

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

18

Figure 13: Secondary Enrollment

Source: World Bank Report

Bahrain also has the highest tertiary gross enrollment ratio in the GCC of 32.8% compared to GCC’s average of 24.0%. Qatar reported the lowest tertiary gross

enrollment ratio of 11%. This fact brings to light that a majority of Qatar nationals are meer high school graduates, endorsing our previous statement

that Qatar has the least number of nationals in its workforce. However, Qatar is attempting to increase their low tertiary gross enrollment rate by trebling

spending on tertiary education.

Arab states have the second lowest rate of tertiary enrollment following the

Sub-Saharan African countries. Since 1970, Asian, European and American students have constituted around 80% of the student body in tertiary

education. Their needed skill sets are apparent in GCC’s high expatriate rate,

particularly workers from America and Asia.

Figure 14: Student Enrollment in Tertiary Education

Source: UNESCO Institute for Statistics

The country spending highest on education in the GCC is Saudi Arabia, allocating 5.6% of GDP on education expenditure (Table 6). Saudi Arabia is

ranked 40 in the world. The second highest is Oman, with only 3.9% of GDP

spent on education expenditure. Oman is ranked 108, followed by Kuwait at 111, Qatar at 120, Bahrain at 136 and, finally, UAE at 161. The top 5 countries

spending the highest percent of GDP on education are Timor-Leste, Cuba, Lesotho, Marshall Islands and Maldives.

Qatar reported the lowest tertiary gross enrollment ratio of 11%

The country spending

highest on education in the GCC is Saudi Arabia, allocating 5.6% of GDP on

education expenditure

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

19

Table 6: Education Expenditure

% of GDP Country Rank Year

Bahrain 2.9 135 2008

Kuwait 3.8 111 2006

Oman 3.9 108 2006

Qatar 3.3 120 2005

Saudi 5.6 40 2008

UAE 1.2 161 2009

Source: CIA World Factbook

a) Education Shortcomings

Most nationals enroll in the public sector, attracted by its free cost. As a result, private schools have less than 50% enrollment. Other than private schools being expensive, there are notable differences between private and public

education. Government schools use Arabic as the primary language and focus

on humanities, most importantly Islamic Studies. On the other hand, private schools usually use English as the main language and accord importance to

sciences and mathematics. All GCC countries scored lower than the Organization for Economic Co-operation and Development (OECD) nations in

the International Trends in International Mathematic and Science Study test

(TIMSS) for 8th grade.

Figure 15: Grade 8 TIMSS Score (2007)

Source: World Bank Note: The test is conducted every four years; 2011 results will be published end of 2012.

GCC countries have the resources to enhance their human capital. As projected

by the World Bank, 20.5 million nationals will enter the labor force by 2020. Unemployment is expected to rise only if GCC governments do not tackle the

core of the problem. Governments in the GCC should commit to investment

opportunities in the education sector, the healthiest and most vital long-term investment.

Predominantly, GCC primary and secondary education does not prepare its

citizens for modern industries and is not united with world-class qualifications. The stability of the economy mainly lies in the education system which should

prepare national manpower to better integrate in the workforce. Especially with

the rising need of the GCC countries to diversify their economies, governments should insure that their citizens have the opportunities and resources to excel in

needed specializations.

Most nationals enroll in the public sector, attracted by its

free cost. As a result, private

schools have less than 50% enrollment

Predominantly, GCC primary and secondary education

does not prepare its citizens

for modern industries and is not united with world-class

qualifications

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

20

According to Alpen Capital, students in the region are expected to grow “from

9.5 million in 2010, to 11.3 million in 2020” (2010). Educating the new wave of

students at global standards would require 163,200 additional teachers. The GCC has a student to teacher ratio of 11:1 compared to developed nations’

ratio of 15:1. Even though the GCC’s average is better, the teachers lack the required skill-sets to be as effective. GCC countries have a very low percentage

of vocational training compared to the 10% global average (Figure 8). .

Figure 16: Technical and Vocational Training Enrollment (2007)

Source: UNESCO

Employment

More dangerously, GCC governments dominate the economy by being the

biggest employers of their citizens. Nationals lose motivation to compete on a global level in the private sector as public sector employment offers them

higher wages with more attractive benefits and requires fewer skills.

This overstaffed safe haven of employment for GCC citizens exacerbates the

most problematic factors for doing business in Kuwait which, according to the World Economic Forum, are an inadequately educated workforce and an

inefficient government bureaucracy. The bureaucratic system of GCC countries is saturated with public workers. This increasingly complicates the regulatory

framework which undermines and slows down private ventures and risk-taking.

From 2000 to 2010, an estimated 7,072 thousand jobs were created in both the

private and public sector. Only 1.15% of the jobs were created by the public sector. Out of those 7,072 thousand job openings, only 25% were taken by

nationals. Based on the following estimates, Qatar created 96.4% new jobs for

expatriates, which is justified by its high expatriate ratio. Only 3.6% new jobs were taken by nationals. Nevertheless, Out of the six GCC countries, Qatar has

the lowest population of nationals. Their dependence on expatriate labor is necessary to spur economic growth and to maintain the highest GDP/capita in

the region.

The GCC has a student to teacher ratio of 11:1

compared to developed nations’ ratio of 15:1

More dangerously, GCC

governments dominate the

economy by being the biggest employers of their

citizens

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

21

Table 7: 2000-2010 Job Creation

Source: International Monetary Fund Middle East and Central Asia

Throughout 2000 to 2010, Saudi Arabia witnessed the highest population growth in the region as well as the highest job creation, an estimate of 2,598

thousand jobs. Exactly one half of the new jobs were taken by nationals. Yet,

Saudi Arabia’s unemployment rate is still high at 10.8%. Bahrain and Oman have even higher unemployment rates and only 19% and 30%, respectively, of

new jobs created were taken by nationals.

The average unemployment rate is higher than the world’s average which was

estimated to be 8.7% in 2010.20 However, the GCC average does not account for masked unemployment and underemployment which have similar

implications as unemployment. Unemployment is masked by bloated bureaucracies with ineffective and overstaffed employees. In addition, the

nationalization quota system has also resulted in private employers who deploy nationals without utilizing their labor. For this reason, the unemployment in the

GCC is swayed to look lower and less challenging than its actual connotations,

especially with the rising population.

a) Expatriate Labor

Job creation is not the biggest challenge of the GCC as much as the mismatch between national labors’ demand and supply in the job market. For GCC

countries, expatriate labor is more attractive than national labor. Even though

the latter is more robust, expatriate labor is cheaper, highly skilled and more flexible. In addition, the types of jobs experiencing steady growth are

unappealing to nationals, such as jobs in services, construction, and trade. On the other hand, Expatriates accept lower wages, longer hours and come with

more foreign experience and skill.

20 Indexmundi Database

Throughout 2000 to 2010, Saudi Arabia’s population

witnessed the highest population growth in the

region as well as the highest

number of job creation

Oman has the highest

unemployment rate of 35%

and Kuwait’s 0.5% unemployment rate is the

lowest in the GCC

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

22

Figure 17: Salary Increases for 2010

Source: GulfTalent

Expatriate labor, especially Asian, has become harder to attract with the growing opportunities in their domestic economies and the rising cost of labor

such as in India. A survey by Gulf Talent showed that westerners in the GCC received the lowest salary increases; this is rationed by the high unemployment rate in western countries which make it harder for them to find better job

opportunities. Nevertheless, another Gulf Talent Survey indicated that in both UAE and Saudi Arabia, Western professionals in mid-management received a

higher average salary than Emiratis and Saudis, reflecting their superior skills. Nationals in the private sector did not receive the highest salary increases,

supporting nationals’ lack of appeal to the private sector compared to the better paying public sector.

The restrictions on expatriate labor make them even more attractive to be hired by employers. The No-Objection Certificate (NOC) requirement prohibits

expatriates to switch from one employer to another. This restriction makes employers have better control on expatriate labor in terms of pay and mobility.

Qatar uses NOC strictly as a retention tool, attracting professionals with high

job offers and forcing them to relocate when they want to change jobs. NOC has been liberalized in Bahrain and Oman resulting in higher payments to

expatriates as competitive pay offers arise.

b) Nationalization Policies

GCC countries are aware of their dependence on expatriate labor in the private sector and the threat of higher unemployment as young nationals enter the

labor force. Since governments can no longer absorb the large pool of

graduates, GCC countries have implemented nationalization policies in an attempt to increase the percentage of nationals in the private sector. GCC

countries are trying different approaches such as subsidizing salaries in a firm willing to hire nationals, or in the case of Bahrain, taxing companies for hiring

foreign employees.

The aim of nationalization policies is to decrease the dependence of one foreign

nationality in certain specialized fields and to make the GCC country nationality the highest single nationality in each sector. In Saudi Arabia, “visa slots” are given to each employer based on the nationality of expatriates being hired. UAE

uses a similar approach and charges higher visa fees when a certain nationality visa slot is being exceeded. By contrast, when UAE employers surpass the

Emiratisation minimum employment requirement, they are rewarded with lower visa fees.

Job creation is not the biggest challenge of the GCC

as much as the mismatch

between national labors’ demand and supply in the

job market

Expatriate labor, especially

Asian, has become harder to attract with the growing

opportunities in their domestic economies and the

rising cost of labor such as in

India

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

23

Nationalization targets in the GCC are more pragmatic in some countries than in others. Bahrain removed its unsuccessful quota system all together before

implementing its tax on companies who hire expatriate employees. Some

nationalization policies focus on target benchmarks of nationals in different sectors and others focus specifically on positions in organizations.

The Saudization policy mainly aims at growing Saudi manpower by requiring

companies to increase Saudi employment by 5% annually. The quota-system

sets different targets for different sectors. For instance, the media industry, commercial sector, insurance companies and public schools have a target of

19% nationalization compared to a low 6% in construction and a 49% target in the banking sector.

The actual policies put in place are mainly associated with Article 45 of Labour and Workman Law of Saudi Arabia: “Saudi workers shall not comprise less than

75% of the total number of the company/establishment [and] their wages shall not be less than 5% of total wages of workers; the employer shall vocationally

train his Saudi workers to replace foreign workers” and should keep a record of the replacements’ names.21 The policy has enforced a responsibility on

employers to train nationals and increase Saudi manpower. Companies are

rated as Red, Green or Yellow depending on their commitment to the policy and face resultant consequences.

The Kuwaitization policy is considered to be more of a nationalization approach

“by decree”, aiming to increase employment of nationals simply by enforcing

strict quotas in different sectors and professions (Figure 6). In an attempt to fill the quotas, employers are offering nationals a pay worth double of expatriates

even when the latter is being more productive. With such rigorous policies, employers look for policy exemption rather than seek a long-term collective

alternative.

In 1997, Kuwait experienced a sudden increase in unemployment and in

response organized the Manpower and Government Restructuring Program (MGRP). MGRP is a government organization aiming to increase the percentage

of nationals in the private work force while improving Kuwaiti manpower. MGRP’s creation aims to help the economy meet the Kuwaitization policy

quotas.

MGRP recognize that nationals prefer working the public sector due to better

working conditions and higher wages. To bridge the gap between the private and public sector, MGRP implemented a social allowance limited to nationals working in the private sector in an attempt to decrease their unwillingness to

work in the private sector. Also, MGRP imitated the public sector by paying social allowances for private sector’s national employees’ children. However,

conflictingly, the government faces societal pressures to increase government wages and continuously responds with public salary increases. Other than an

increased cost of living, and influencing inflationary problems, the government is countering MGRP motives by increasing the salary gap between the private

and public sector.22

21 Human Resource Management (HRM) in Saudi Arabia: A Closer, 11 March 2011 22 MGRP- The Kuwaitization Engine, Ahmad Saeid, 16 August 2009

Since governments can no

longer absorb the large pool

of graduates, GCC countries have implemented

nationalization policies in an attempt to increase the

percentage of nationals in the private sector

Nationalization targets in the GCC are more pragmatic in

some countries than in others

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

24

Table 8: Nationalization policy by sector

Saudi UAE Kuwait Oman Qatar Bahrain

Local Workforce 28% 12% 18% 46% 17% 45%

Oil Refinery 30% 50-90%

79%

Contracting 5%

30-80%

Construction 30%

5%

Banking 49% 50% 60% 90%

Investment 40%

Transport 78-95%

Communication 56% 50-80%

Hotels and Restaurants 75-100%

Agriculture 2%

Manufacturing 2%

Source: WikiLeaks, Qatarization, Arabian Business, Zawya Note: Local Workforce percentages represent private sector quotas states by nationalization policies

The Emiratization policy also consists of different quotas in different job sectors. The banking, insurance, and trade sectors are imposed to increase the Emirati

employees by 4%, 5%, and 2% respectively. Human resources and secretarial

positions were also nationalized in 2006. Emiritization policies also increase the costs of the firm when the proportion of expatriate to national employees rises,

constituting an implicit tax on firms. This form of penalizing indirectly lowers the ability of employers in the private sector to employ national employees who

require a higher labor cost.

Even with their unemployment rate still highest in the GCC, Oman’s

nationalization policies are more encompassing with their encouragement of citizens to work in private semi-skilled positions and increased enrollment in

vocational training.23 The government set different quotas for different job

sectors: 60% in transport, storage and communication sectors; 45% in finance, insurance and real estate sectors; 35% in industries; 30% in hotels and

restaurants; and 20% in wholesale and retail trading. Employers who successfully reach the corresponding quotas are rewarded by press recognition

and privileged treatment by the government. The most thriving aspect of the Omanization policies is its alignment with Oman’s educational reform. The

government instituted federal universities to train Omani workers. Omanization

also supports The Committee for Vocational Training with compensation schemes for the private sector and subsidizing salaries for Omani workers

during their training period.

Bahrain’s nationalization policy began in the early 1980s with the introduction of a committee instituted to tackle unemployment problems among nationals. However, time has proven that Bahrainization policies increase the employment

of nationals in the public sector and decrease their employment in the private sector due to the former’s better pay and working conditions. In 2001,

Bahrain’s Ministry of Labor and Social Affairs initiated a project which consists of a training program for employees combined with wage subsidies for

employers who replace expatriated with Bahraini citizens.

Many employers find their governments’ targets unrealistic such as the 15%

Emiratisation target in the engineering sector or the 60% Kuwaitisation target

23 Work Nationalization in the Gulf Cooperation Council States, Kasim Randeree, 2012

The government faces societal pressures to increase government wages and

continuously responds with public salary increases

The Emiratization policy also

consists of different quotas in different job sectors

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

25

in the banking sector. Employers are unable to find such high percentages of qualified nationals. Qatar realizes that the educational gap and low rate of

competition between expatriates and nationals is the main problem that

Qatarization is facing. With the public sector saturated, Qatar realizes that the lack of competition specifically between nationals and expatriates in the labor

market will cause unproductive nationalized allocation of supply and demand for skills in the private sector. For this reason, Qatar is focusing on increasing

the education and skills of its national labor force through increased spending

on tertiary education, vocation education and post-compulsory training.

3. Policy Agenda

Housing Reform

Housing projects are low yield investments, making it harder to attract companies to manage housing projects. Private public partnerships would help

make housing projects more attractive to foreign investors. Instead of government spending face value on housing and infrastructure project (includes

hospitals and amenities), foreign private investors would bid for the

government contract. The government would offer the land where a city needs to be constructed. Specific criteria will be given listing the specific amenities

needed. The private investor with the most efficient project, in terms of time and space, would hire the contractors needed to initiate and construct the

project. The investment would be similar to a bond. Yearly, or depending on the terms of the contract, the government would pay back the investment at a

bargained interest rate.

City development projects could also be used to create more jobs in the private

sector. The government contract would also impose the private investor to abide by nationalization policies. Government would create incentives by

creating more attractive yields for private investors who dynamically seek local

contractors.

Education Reform

GCC governments should allocate more of their budget towards education

expenditure. Saudi Arabia increased their budget allocation on education by 13% to reach 25% of their budget in 2010. Education expenses included the construction of 1,200 new schools, rehabilitation of 2,000 existing schools.

However, the challenges of education are graver than infrastructure-related issues. Like the rest of the GCC, Saudi students are weak in English,

Mathematical and Science subjects. With exception to Bahrain and the UAE, investments in research and development are very low in the region, less than

1% of Saudi Arabia’s budget allocation. Saudi schools curricula are not unified

and lack national standards. Parallel to the UAE, there is a gap between local universities subjects and private sector job requirements, mainly due to the

inflexibility and dearth of varied courses.

The challenge all GCC countries face is the low qualification of teachers in

schools, specifically public schools. There is a stark difference between teaching methods in public school and private schools. GCC governments should unify

the training methods of teachers by providing all teachers with a unified training program. Compulsory collective workshops between private and public

school teachers should be initiated and subsidized by the government. Certifications should be renewed yearly for public schools to be aware of the

areas where teachers lack skills and for teachers to be updated with advanced

teaching methods. Governments could take advantage of workshops to recognize public schools subjects that need to be improved or even introduced.

Qatar is focusing on

increasing the education and skills of its national labor

force through increased spending on tertiary

education, vocation

education and post-compulsory training

Private public partnerships

would help make housing projects more attractive to

foreign investors

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

26

Governance and Regulation of Education Sector

For the education sector to grow efficiently, it needs entities that provide

competent regulatory framework. Such entities exist such as the Council of

Higher Education in Saudi Arabia, Dubai Schools Inspection Bureau and the Supreme Education Council in the UAE and the Quality Assurance Authority for

Education in Bahrain. To better govern the increasing number of schools, the number of administrative education committees should rise. Governments

could encourage such entities to form and improve standards in schools by

creating competition between them.

Public schools would be required to run under a certain educational governing institution. The Ministry of Education would provide criteria for the Institution to comply by. The objective of the institution should be to increase research,

develop teaching methods, increase exposure with varied subjects, and integrate new technology and global standards in their schools curriculum. The

institutions will also be responsible for the teaching methods and qualifications of the teachers. Yearly, the Ministry of Education would compose surveys and

introduce standardized tests (measures are derived from workshops). The results would spotlight the improvements in students’ performance and the

curriculum as a whole. Schools would be scored and the institution with the

highest average score would be rewarded with higher wages for both teacher and members of the board as well as grants for infrastructure, rehabilitation

and needed equipment. Entities with the lowest scores could, eventually, be dissolved, or absorbed into a stronger entity. The schools they overlook will be

governed by the institution with better output. Where applicable, private

schools could be imposed with governing entities. Government could encourage private institution to create vocational training programs and foster progressive

competition between them.

There is no doubt that GCC countries could attract global tertiary education standards in the region. This is apparent in the rise of international recognized

foreign universities opening campuses in the region. Some of them are Paris

Sorbonne and New York University in Abu Dhabi, the LSE and INSEAD offering their most distinguished MBA programs in UAE, Qatar Education City which

includes Texas A&M University, Carnegie Mellon University, Georgetown and Northwestern. Through private-public partnerships (PPP), GCC countries are

able to attract private investors with free land and electricity, tax exemption

and monetary grants.

Following the same manner, GCC countries could attract private investors in secondary education and vocational programs by offering them government contracts. Private investors will operate the schools and then transfer them to

the government depending on the terms of the contract. In the mean time, however, the government should train nationals with the expertise of their

international private investors. Governments should create partnerships to bridge the gap between the private sector’s demand and national workforce

required skills as a commitment to long-term economic growth.

Labor Reform

Governments should cease job creation in the public sector before reforming it in addition to taking the initiative to identify unproductive jobs in the public

sector and simplify the framework of its job structure. Vocational training could be given to low skill-set workers, with their salaries still subsidized by the

government. With such training, governments would help the private sector

implement nationalization quotas by subsidizing the training and required skills needed for replacing expatriates.

GCC governments should

allocate more of their budget towards education

expenditure

To better govern the

increasing number of schools, the number of

administrative education

committees should rise

There is no doubt that GCC

countries could attract global tertiary education standards

in the region

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

27

Government workers transferred to the private sector could have half of their wages subsidized by the government for a specific time period. The implication

behind this time period is for employees to easier accept longer hours with their

salaries still unchanged, as they would otherwise drop in the private sector. Private employers will take the time to train the new employee and face a lower

opportunity cost for replacing expatriates with the higher skill-sets and lower wages. In return, the saturation of the public sector will decrease and its

efficiency will increase, clarifying the regulatory framework given to the private

sector.

To better control the flow of expatriates, governments should be stricter with employers’ foreign employees’ visa applications. Before accepting an expatriate workers’ visa application, stricter guidelines for applying should impose

employers to specify the job position, specialization and the necessary skill in the expatriate that nationals lack. One of the criteria for accepting to process

the visa would also verify that the employers seek expatriate’s employment only after advertising the job opening to nationals and only after an extensive search

in the national labor market for such skill. Governments would have a clearer idea of the training needed to provide nationals with the skills of professional

jobs, and could choose to afford it when necessary.

MARKAZ RESEARCH June 2012

Kuwait Financial Centre “Markaz”

28

Appendix 1: MENA Statistics

Country Population Median Age

Internet users GDP

Inflation (%)

Poverty Rate

Current Account Balance

Public Debt

External Debt

Foreign Reserves

Unemployment (USD Bn)

(mn)

% under 25

yrs % (mn)

(USD

bn)

Per capita

($)

(USD

Mn)

(%)

GDP % GDP % GDP

Algeria 34.5 50% 27 10 4.7 172 4,762 5.50 23% 7,010 0.9 - 3.7 161

Egypt 80.5 36% 24 15 20 239 2,998 12.00 20% -4,318 -1.5 74.7 18 35

Jordan 6.4 58% 22 9.2 1.6 30 4,746 11.70 20% -1,711 -5.9 68.3 61.2 14

Libya 6.4 63% 24 15.3 0.35 85 12,951 5.10 25% 15,908 15.9 1.8 6.1 124

Morocco 31.6 50% 27 14.6 13.2 96 2,987 9.50 18% -4,259 -5.2 49.9 28.8 24

Syria 22.1 59% 22 13 4.4 66 3,110 5.50 14% 299 1 - 10.3 -

Tunisia 10.5 42% 30 1.6 3.5 46 4,274 4.10 N/A -2,071 -6 42.1 47.2 9

Yemen 23.4 53% 18 30 2.2 33 1,319 4.50 30% -2,565 -9.7 - 25.5 -

Iran 76.9 50% 26 9.6 8.21 342 4,467 1.50 15% 13,248 3.1 - 4.1 78

Iraq 26.67 49% 20 15 1.2 93 2,827 4.40 N/A 27,133 31.4 - - -

Kuwait 2.5 33% 29 0.5 1.1 128 34,743 1.00 N/A 44,957 38.1 9.9 26.5 21

Saudi Arabia 23.68 51% 25 10.5 9.77 476 17,840 9.80 N/A 49,259 10 10 22.7 507

United Arab Emirates

4.77 59% 30 10.9 3.45 255 48,990 5.50 12% 15,709 9.2 26.4 60 54

Bahrain 1.11 44% 31 13.2 0.42 24 21,605 5.00 4% 1,795 6.6 37.5 132 4

Qatar 1.45 35% 31 2.4 0.56 158 89,320 4.50 N/A 9,908 6.5 12.1 71.5 26

Oman 2.87 67% 24 35 1.47 59 19,135 2.00 45% 4,642 5.1 4.7 22.1 15

Source: IMF, IIF, World Bank, CIA World fact book and Markaz Research

MARKAZ RESEARCH June 2012

Disclaimer This report has been prepared and issued by Kuwait Financial Centre S.A.K (Markaz), which is regulated by the Capital Markets Authority and the Central Bank of Kuwait. The report is owned by Markaz and is privileged and proprietary and is subject to copyrights. Sale of any copies of this report is strictly prohibited. This report cannot be quoted without the prior written consent of Markaz. . Any user after obtaining Markaz permission to use this report must clearly mention the source as “Markaz “. The report is intended to be circulated for general information only and should not to be construed as an offer to buy or sell or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy in any jurisdiction. The information and statistical data herein have been obtained from sources we believe to be reliable but no representation or warranty, expressed or implied, is made that such information and data is accurate or complete, and therefore should not be relied upon as such. Opinions, estimates and projections in this report constitute the current judgment of the author as of the date of this report. They do not necessarily reflect the opinion of Markaz and are subject to change without notice. Markaz has no obligation to update, modify or amend this report or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate, or if research on the subject company is withdrawn. This report may not consider the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors are urged to seek financial advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and to understand that statements regarding future prospects may not be realized. Investors should note that income from such securities, if any, may fluctuate and that each security’s price or value may rise or fall. Investors should be able and willing to accept a total or partial loss of their investment. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily indicative of future performance. Kuwait Financial Centre S.A.K (Markaz) may seek to do business, including investment banking deals, with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of

this report. This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of Markaz, Markaz has not reviewed the linked site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to Markaz’s own website material) is provided solely for your convenience and information and the content of the linked site does not in any way form part of this document. Accessing such website or following such link through this report or Markaz’s website shall be at your own risk. For further information, please contact ‘Markaz’ at P.O. Box 23444, Safat 13095, Kuwait ; Email: [email protected] ; Tel: 00965

1804800; Fax: 00965 22450647.

R E S E A R C H June 2012