gao-01-525 information technology: architecture …architecture framework, version 2.0 (september...

TRANSCRIPT

Report to the Secretary of DefenseUnited States General Accounting Office

GAO

May 2001 INFORMATIONTECHNOLOGY

Architecture Neededto GuideModernization ofDOD’s FinancialOperations

GAO-01-525

Page i GAO-01-525 DOD Financial Management Enterprise Architecture

Letter 1

Appendix I Objectives, Scope, and Methodology 33

Appendix II Description of DOD Architecture Framework

Essential Products 35

Appendix III Comments From the Department of Defense 39

Tables

Table 1: Seven Essential Products for the DOD C4ISR ArchitectureFramework 14

Table 2: Summary Comparison of DFAS’ Architecture ProductsWith the DOD C4ISR Architecture Framework EssentialProducts 16

Table 3: Comparison of DOD’s Management Practices toRecognized Practices for Developing an EnterpriseArchitecture 21

Table 4: Comparison of DOD’s Management Practices toRecognized Practices for Implementing an EnterpriseArchitecture 23

Figures

Figure 1: Simplified Diagram of Organizations Responsible forDOD Financial Management 5

Figure 2: Overview of DOD’s Financial Management Operations 7Figure 3: Interrelationship of Three Architecture Views 12Figure 4: Simplified Diagram of the Enterprise Architecture

Management Framework 19

Contents

Page 1 GAO-01-525 DOD Financial Management Enterprise Architecture

May 17, 2001

The Honorable Donald H. RumsfeldThe Secretary of Defense

Dear Mr. Secretary:

To correct its long-standing and pervasive financial managementweaknesses, the Department of Defense (DOD) plans to invest billions ofdollars to modernize its financial management operations and supportingsystems. Effectively managing such a large and complex endeavorrequires, among other things, a well-defined and enforced blueprint foroperational and technological change, commonly referred to as anenterprise architecture. Such an architecture provides a clear andcomprehensive picture of an entity, whether it is an organization (e.g.,federal department, agency, or bureau) or a functional or mission area thatcuts across more than one organization (e.g., financial management orcombat identification1). This picture consists of three integratedcomponents: a snapshot of the enterprise’s current operational andtechnological environment, a snapshot of its target environment, and acapital investment road map for transitioning from the current to thetarget environment.

The use of enterprise architectures is a best practice in informationtechnology (IT) management followed by leading public and privateorganizations and is required by the Clinger-Cohen Act of 1996, the Officeof Management and Budget (OMB), and DOD.2 Our experience withfederal agencies has shown that attempting a major modernization effortwithout a complete and enforceable enterprise architecture results insystems that are duplicative, are not well integrated, are unnecessarily

1Combat identification refers to operations and systems that provide the means to identifyfriendly and hostile forces, noncombatants, and neutrals on the battlefield and convey thatinformation across the military services and to our allies.

2The fiscal year 1997 Omnibus Consolidated Appropriations Act, Public Law 104-208,renamed both Division D (the Federal Acquisition Reform Act) and E (the InformationTechnology Management Reform Act) of the 1996 DOD Authorization Act, Public Law 104-106, as the Clinger-Cohen Act of 1996; OMB Circular No. A-130, Management of FederalInformation Resources (November 30, 2000); and DOD’s Command, Control,Communications, Computers, Intelligence, Surveillance, and Reconnaissance (C4ISR)Architecture Framework, Version 2.0 (September 1997).

United States General Accounting Office

Washington, DC 20548

Page 2 GAO-01-525 DOD Financial Management Enterprise Architecture

costly to maintain and interface, and do not effectively optimize missionperformance.3

Because of the importance of an enterprise architecture to effectivesystems modernization,4 we reviewed DOD’s efforts to develop andimplement a departmentwide financial management5 enterprisearchitecture to guide and constrain its modernization activities. Ourobjectives were to determine (1) the status of these efforts and (2) theeffectiveness of DOD’s structures and processes for developing andimplementing an architecture. This work on the use of an architecture-based approach to systematic financial management reform is part of ourlarger efforts to provide DOD with a framework for management reformand change. Details on our objectives, scope, and methodology arediscussed in appendix I.

DOD does not have a financial management enterprise architecture, nordoes it have the management structures and processes in place toeffectively develop and implement one. Without this “blueprint” to guideand constrain DOD’s investments in financial management operations andsystems, the military services and defense agencies find themselvescurrently operating unique and nonstandard financial processes andsystems. Exacerbating this situation are DOD’s plans to spend billions ofdollars on new and modified financial management systems independentlyfrom one another and outside the context of an integrated enterprisearchitecture. The result will be more processes and systems that areduplicative, not interoperable, and unnecessarily costly to maintain andinterface, and that do not effectively address long-standing problems oroptimize financial management performance and accountability.

3Air Traffic Control: Complete and Enforced Architecture Needed for FAA SystemsModernization (GAO/AIMD-97-30, February 3, 1997) and Customs Service Modernization:Architecture Must Be Complete and Enforced to Effectively Build and Maintain Systems(GAO/AIMD-98-70, May 5, 1998).

4Effective system modernization management also requires such institutional managementcontrols as disciplined software and systems acquisition and development products; aportfolio-based approach to investment selection, control, and evaluation; proactive humancapital investment; and continuous information security management.

5DOD defines financial management as any action that involves budgeting, tracking,management, oversight, reporting, or exchanging of actual financial data or property,inventory, or other resource information that ultimately translates to or affects financialinformation.

Results in Brief

Page 3 GAO-01-525 DOD Financial Management Enterprise Architecture

Instead of an enterprise architecture, officials within the Office of theUnder Secretary of Defense (Comptroller), which is the DOD organizationresponsible for DOD financial management, point to (1) DOD’s FinancialManagement Improvement Plan, (2) an enterprise architecture that theDefense Finance and Accounting Service (DFAS) is developing, and(3) DOD’s recently launched Finance and Feeder System ComplianceProcess as the tools for guiding and constraining DOD’s plannedinvestment of billions of dollars to modernize its financial managementoperations and systems. However, these tools do not provide thearchitectural definition and content specified by both federal and DODstandards6 and thus are not, singularly or collectively, sufficient surrogatesfor a DOD financial management enterprise architecture.

DOD’s lack of a financial management enterprise architecture is largelydue to its lack of effective management structures and processes (i.e.,management controls) for developing and implementing one. The federalChief Information Officers (CIO) Council, in collaboration with us andOMB, has recently published a framework that defines effectivearchitecture management controls that successful organizations practice.7

A foundational element of these best practices is the need to fixaccountability and responsibility for architecture development with anentity that has the authority to ensure that the architecture’s scope(1) spans the full breadth of the enterprise and (2) provides sufficientdefinitional depth in all areas of the enterprise where system andsupporting technical infrastructure investments are to be made. Anotherfoundational element is that the decisionmaking body for system andinfrastructure investments needs to have the authority to ensure thatinvestments are approved only if they are compliant with the completedarchitecture, unless an explicit waiver is obtained. In the case of DOD’smany financial management modernization activities, neither of these twofoundational elements nor other important architecture managementcontrols are in place.

6Chief Information Officers Council, Federal Enterprise Architecture Framework, Version1.1 (September 1999); OMB Circular No. A-130, Management of Federal InformationResources (November 30, 2000); and DOD’s Command, Control, Communications,Computers, Intelligence, Surveillance, and Reconnaissance (C4ISR) ArchitectureFramework, Version 2.0 (September 1997).

7Chief Information Officers Council, A Practical Guide to Federal Enterprise Architecture,Version 1.0 (February 2001).

Page 4 GAO-01-525 DOD Financial Management Enterprise Architecture

To assist the department in effectively managing its financial managementmodernization efforts, we are making recommendations to the Secretaryof Defense aimed at providing the means for effectively developing andimplementing a financial management enterprise architecture.

In written comments on a draft of this report, DOD stated that it wouldconsider our recommendations as part of ongoing efforts to develop astrategy for improving financial management.

DOD is one of the largest and most complex organizations in the world.Defense operations involve about $1 trillion in assets, $310 billion inannual budgetary authority, $24 billion in monthly disbursements, and3 million military and civilian employees. Moreover, execution of theseoperations spans a wide range of defense organizations, including themilitary services and their respective major commands and functionalactivities, numerous large defense agencies and field activities, andvarious combatant and joint operational commands that are responsiblefor military operations for specific geographic regions or theaters ofoperations.

Effectively managing DOD’s finances across this complex array oforganizations is both a formidable challenge and a prerequisite foreffective and efficient departmental performance and accountability.Without reliable financial management information, DOD cannot makeinformed decisions among competing spending priorities and cannoteffectively identify opportunities for reducing costs and reallocatingresources to pressing needs.

DOD’s financial management operations and systems span numerousorganizations (see fig. 1). The Under Secretary of Defense (Comptroller) isDOD’s Chief Financial Officer and the principal advisor to the Secretary ofDefense for budgetary and fiscal matters. The DOD Comptroller isresponsible for promulgating financial management policies andprocedures relating to financial management matters and the productionof financial statements. Under the Comptroller is DFAS, which wasestablished in November 1990 to consolidate DOD’s diffused disbursementand accounting functions.

Background

Responsibility for DODFinancial Management IsShared Among DepartmentComponents

Page 5 GAO-01-525 DOD Financial Management Enterprise Architecture

Figure 1: Simplified Diagram of Organizations Responsible for DOD FinancialManagement

Secretary ofDefense

Assistant Secretaryof the Army(Financial

Management and Comptroller)

Assistant Secretaryof the Navy(Financial

Management)

Assistant Secretary of the Air Force

(Financial Management

and Comptroller)

Defense Agency Field ActivityComptrollers

Under Secretary ofDefense (Comptroller)DOD Chief Financial

Officer

Secretary of the Army

Secretaryof the Navy

Secretary of the Air Force

Defense Agenciesand Field Activities

(except DFAS)Defense

Finance and Accounting

Service

Pensacola, FL

Memphis, TN

Rome, NY

Seaside, CA

Cleveland Center(Navy)

Columbus Center(Defense Logistics

Agency)

Denver Center(Air Force)

IndianapolisCenter(Army)

Kansas CityCenter

(Marine Corps)

Honolulu, HI

Oakland, CA

San Diego, CA San Bernardino, CA

San Antonio, TX

Omaha, NE

Limestone, ME

Lexington, KY

Dayton, OH Lawton, OK

Orlando, FL

Rock Island, IL

St. Louis, MO

Norfolk, VA

Charleston, SC

Note: Except for Honolulu, Norfolk, Orlando, and San Antonio, each operating location providesservices to the single military service identified. Honolulu serves all of the military services; Norfolkserves Navy and Army customers; and Orlando and San Antonio both serve Army and Air Forcecustomers. In addition, Charleston, Pensacola, and Omaha provide civilian pay service to all militaryservices and defense agencies.

Source: DOD Financial Management Improvement Plan, January 2001, and DFAS OperationalArchitecture, Version 1.2, March 1999.

Page 6 GAO-01-525 DOD Financial Management Enterprise Architecture

Each of DOD’s components (military services and defense agencies) has afinancial management and comptroller organization that is responsible forfinancial matters within that component, except for those performedcentrally by DFAS. These functions include managing financialmanagement activities and operations, directing the preparation of budgetestimates, approving asset management systems, collecting debts, andaccounting for property and inventories. The DOD Comptroller does nothave direct authority over any of the financial management organizationswithin the military services and defense agencies. However, DOD hasdirected the military services and defense agencies to follow the DODComptroller’s guidance and regulations.8

With the establishment of DFAS, the military services and defenseagencies generally no longer perform the finance (disbursing) andaccounting (reporting) functions. However, they continue to performother financial management functions, such as initiating financial events,obligating and authorizing the expenditure of funds, maintainingstewardship over DOD assets, and accounting for assets, liabilities, andequity. Accordingly, these components are responsible for the systemsthat create financial event data and “feed” these data to DFAS. Accordingto DOD, the “feeder” systems provide about 80 percent of the financialdata used by DFAS.

As shown in figure 2, DFAS uses these data, as well as data from non-DODentities (contractors, vendors, and commercial carriers), to perform thecore financial management functions of transaction processing,accounting, and reporting. Transaction processing includes recording theresults of financial events in detailed accounts and disbursing payments toDOD personnel and others. Accounting and reporting uses varioussubfunctions9 (see fig. 2) to show the financial impact of all thedepartment’s financial events.

8DOD Directive 5118.3, Under Secretary of Defense (Comptroller) (USD(C)/Chief FinancialOfficer (CFO) and DOD Directive 5025.1, DOD Directives System.9General ledger accounting ensures that financial events are defined consistently andrecorded accurately. Funds control records the results of budget execution to maintain andaccount for appropriations. Cash management tracks the cash position and provides thenecessary reports for managing cash. Cost accounting accumulates and records costs formanagement to develop customer billing rates, fees, and pricing structures.

Page 7 GAO-01-525 DOD Financial Management Enterprise Architecture

Figure 2: Overview of DOD’s Financial Management Operations

Source: DOD Financial Management Improvement Plan, 1999, and DFAS Operational Architecture,Version 1.2, March 1999.

The department’s long-standing and pervasive financial managementproblems are well chronicled by the DOD Inspector General (IG), themilitary service audit agencies, and us. These problems include(1) weaknesses in budget execution accounting, (2) inability to properlyaccount for and report on weapon system support equipment, (3) inabilityto account for and control its investment in inventories, and (4) inability tocapture and accurately report the full costs of its programs.

Such problems led us in 1995 to add DOD financial management to our listof high-risk programs vulnerable to waste, fraud, abuse, andmismanagement. Since 1995, we have continued to designate DOD

DOD Recognizes the Needto Improve FinancialManagement Operationsand Has Taken Some Stepsto Begin Doing So

Records results of payments to DOD personnel, retirees, annuitants,

and contractors, and recordsand tracks funds received by

the department.

• general ledger• funds control• cost accounting• cash management

Accounting andreporting

Transaction processing

DFAS Core Functions

Disburse-ments

Military Services and Defense Agencies

Event Program function

• acquire• transport• manage• use• dispose

• acquisition• personnel• cost management• property management• inventory management

Event data

Financial event data

Reporting

Other GovernmentCongressOMBOSD

TreasuryFederal IRSState IRSCourts

Financial eventdata

Reporting

contractorsvendorscommercial carriersbankscivilian employeesmilitary membersretireesannuitants

• receivables • collections• payables• payroll• property accounting• inventory accounting

Page 8 GAO-01-525 DOD Financial Management Enterprise Architecture

financial management a high-risk program.10 DOD has acknowledged thatits present financial management environment has serious inadequaciesand does not, for the most part, comply with the framework for financialreform set out by the Congress in the Chief Financial Officers Act of 1990and the Federal Financial Management Improvement Act of 1996, as wellas OMB direction and guidance, such as OMB Circular A-127, FinancialManagement Systems (June 10, 1999).

To help alleviate these problems, the National Defense Authorization ActFor Fiscal Year 1998 (P.L. 105-85) directed the Secretary of Defense tosubmit to Congress a biennial strategic plan for improving financialmanagement within the department. The Secretary submitted DOD’s firstFinancial Management Improvement Plan to Congress on October 26,1998. The plan identified over 200 initiatives that were intended to improvethe department’s financial operations and systems. In January 1999, wereported11 that the plan provided the first-ever vision of the department’sfuture financial management environment. We also noted that the planwas an important first step in improving DOD’s financial managementoperations, because it discussed for the first time the importance of theprogrammatic functions of personnel, acquisition, property management,and inventory management to the department’s ability to provideconsistent, accurate information. However, we also reported that theplan’s discussion of the future environment was focused on DFAS and didnot address how financial management reform and modernization wouldaddress such areas as asset accountability and control and budgetformulation. Additionally, we reported that the 200 planned initiativeswere not clearly linked to DOD’s future financial managementenvironment and that the plan did not address feeder systems’ dataintegrity. In September 1999, DOD updated the plan, and in July 2000, wetestified12 that although the plan provided more detail on strategies and onthe hundreds of improvement initiatives, the fundamental issues that wereported on in January 1999 still remained.

10High-Risk Series: An Overview (GAO/HR-95-1, February 1995); High-Risk Series: DefenseFinancial Management (GAO/HR-97-3, February 1997); High-Risk Series: An Update(GAO/01-263, January 2001).

11Financial Management: Analysis of DOD’s First Biennial Financial ManagementImprovement Plan (GAO/AIMD-99-44, January 29, 1999).

12Department of Defense: Implications of Financial Management Issues(GAO/T-AIMD/NSIAD-00-264, July 20, 2000).

Page 9 GAO-01-525 DOD Financial Management Enterprise Architecture

In January 2001, DOD issued an updated plan and stated that it hadestablished a process for the military services and defense agencies tofollow in making their respective accounting, finance, and feeder systemscompliant with federal financial management requirements.13 Under theFinancial and Feeder System Compliance Process, DOD components areassigned responsibility for ensuring, in consultation with DFAS, that theirsystems are compliant. Modeled after the department’s Year 2000 process,the process consists of five phases: awareness, evaluation, renovation,validation, and compliance. Each component is to have defined exitcriteria for each phase. The Senior Financial Management OversightCouncil is to provide oversight and guidance.14 The National DefenseAuthorization Act For Fiscal Year 2001 directs that we review the plan andthat we report our results to the defense authorization and appropriationscommittees. Our work to respond to this mandate is ongoing.

An enterprise architecture systematically captures in useful models,diagrams, and narrative the full breadth and depth of the mission-basedmode of operations for a given enterprise, which can be (1) a singleorganization or (2) a functional or mission area that transcends more thanone organizational boundary (e.g., financial, acquisition, or logisticsmanagement). Further, such an architecture describes the enterprise’soperations in both (1) logical terms, such as interrelated businessfunctions, information needs and flows, work locations, and systemapplications, and (2) technical terms, such as hardware, software, data,communications, and security attributes and performance standards. An

13The Federal Financial Management Improvement Act of 1996 mandates that agencies’financial management systems comply substantially with (1) federal financialrequirements, (2) federal accounting standards, and (3) the United States General Ledger atthe transaction level. Within the Department of Defense, these three mandates are referredto as the federal financial management system requirements.

14The Senior Financial Management Oversight Council membership includes the UnderSecretary of Defense (Comptroller) (Chair); Principal Deputy Under Secretary of Defense(Comptroller) (Vice Chair); Under Secretary of Defense (Acquisition, Technology andLogistics); Under Secretary of Defense (Personnel and Readiness); Assistant Secretary ofDefense (Command, Control, Communications and Intelligence); Deputy Chief FinancialOfficer (Executive Secretary); Director, Defense Finance and Accounting Service; Director,Defense Logistics Agency; Assistant Secretaries of the Military Departments (FinancialManagement and Comptroller); Assistant Secretary of the Army (Acquisition, Logistics andTechnology); Assistant Secretary of the Navy (Research, Development and Acquisition);Assistant Secretary of the Air Force (Acquisition); Assistant Secretary of Defense forSpecial Operations and Low-Intensity Conflict; and the Deputy Chief of Staff forInstallations and Logistics (Air Force).

Enterprise Architecture: AKey to Effective SystemModernization

Page 10 GAO-01-525 DOD Financial Management Enterprise Architecture

architecture also provides operational and technological perspectives orviews both for the enterprise’s current (or “as is”) environment and for itstarget (or “to be”) environment, and it provides an IT capital investmentroad map for moving between the two environments.

The development, implementation, and maintenance of enterprisearchitectures are recognized hallmarks of successful public and privatesector organizations. Managed properly, an enterprise architecture canclarify and thus help to optimize the interdependencies andinterrelationships among an organization’s business operations and theunderlying IT infrastructure and applications supporting these operations.Employed in concert with other important IT management controls, suchas portfolio investment management (selection, control, and evaluation)practices15 and continuous information security management practices,16

enterprise architectures can greatly increase the chances of modernizationprograms succeeding.

Congress, OMB, and the CIO Council have recognized the importance ofenterprise architectures. The Clinger-Cohen Act of 1996 mandates that anagency’s CIO develop, maintain, and facilitate the implementation of thesearchitectures as means for managing the integration of business processesand agency goals with IT. Further, OMB has issued guidance17 that, amongother things, requires system investments to be consistent with thesearchitectures. Similarly, the CIO Council has issued guidance providing(1) a federal framework for the content and structure of an enterprisearchitecture,18 (2) a process for assessing investment compliance with anenterprise architecture,19 and (3) a set of management controls fordeveloping, implementing, and maintaining an enterprise architecture.20

15Information Technology Investment Management: A Framework for Assessing andImproving Process Maturity (Exposure Draft) (GAO/AIMD-10.1.23, May 2000).

16Executive Guide: Information Security Management (GAO/AIMD-98-68, May 1998).

17OMB Circular No. A-130, Management of Federal Information Resources (November 30,2000).

18Chief Information Officers Council, Federal Enterprise Architecture Framework, Version1.1 (September 1999).

19Chief Information Officers Council, Architecture Alignment and Assessment Guide(October 2000).

20Chief Information Officers Council, A Practical Guide to Federal Enterprise Architecture,Version 1.0 (February 2001).

Page 11 GAO-01-525 DOD Financial Management Enterprise Architecture

DOD has also issued enterprise architecture policy, including a frameworkdefining an architecture’s structure and content. Specifically, in February1998,21 DOD directed its components and activities to use the Command,Control, Communications, Computers, Intelligence, Surveillance, andReconnaissance (C4ISR) Architecture Framework, Version 2.0. Accordingto DOD, the C4ISR Architecture Framework is a critical tool for achievingits strategic direction, and all DOD components and activities should usethe framework for all functional areas and domains within the department.The C4ISR Architecture Framework is recognized in the CIO Council’s APractical Guide to Federal Enterprise Architecture as a model architectureframework. (Appendix II provides more detailed information on the C4ISRArchitecture Framework.)

DOD does not have an enterprise architecture to guide and constrain thebillions of dollars it plans to spend to modernize its financial managementoperations and systems. Rather, DOD is relying upon three other initiativesfor directing operational and technology change in this area: the DODFinancial Management Improvement Plan, a DFAS enterprise architecturethat is under development, and the DOD Financial and Feeder SystemCompliance Process. While each of these three initiatives has value,neither singularly nor collectively do they provide sufficient architecturaldefinition, as specified by the DOD C4ISR Architecture Framework, formodernizing something as large and complex as DOD financialmanagement. Moreover, none of the DOD entities responsible for theseinitiatives currently have plans for producing a departmentwidearchitecture.

21The February 28, 1998, memorandum was jointly signed by the Under Secretary ofDefense (Acquisition and Technology), the Acting Assistant Secretary of Defense(Command, Control, Communications, and Intelligence), and the Director for C4 Systems,Joint Chiefs of Staff.

DOD Does Not Have aDepartmentalFinancialManagementEnterpriseArchitecture

Page 12 GAO-01-525 DOD Financial Management Enterprise Architecture

The C4ISR Architecture Framework, Version 2.0, defines the type andcontent of architectural artifacts, as well as the relationships amongartifacts, that are needed to produce a useful enterprise architecture.Briefly, the framework decomposes an enterprise architecture into threeprimary views (windows into how the enterprise operates): theoperational, systems, and technical views. According to DOD, the threeinterdependent views are needed to ensure that IT systems are developedand implemented in an interoperable and cost-effective manner. Each ofthese views is summarized below. (Fig. 3 is a simplified diagram depictingthe interrelationships among the views.)

Figure 3: Interrelationship of Three Architecture Views

Source: C4ISR Architecture Framework, Version 2.

The operational architecture view defines the operational elements,activities, tasks, and information flows required to accomplish or supportan organizational mission or business function. According to DOD, it isuseful for facilitating a number of actions and assessments across DOD,

DOD’s EnterpriseArchitecture Framework:A Brief Description

Technicalview

Specific capabilities identifiedto satisfy information exchangelevels and other operationalrequirements

Technical criteria governinginteroperable implementation/procurement of the selected system capabilities

Relates capabilities and characteristicsto operational requirements

Systemsview

Proce

ssin

g an

d in

tern

odal

leve

ls of

info

rmat

ion

exch

ange

requ

irem

ents

Syste

ms

asso

ciatio

ns to

node

s, a

ctivi

ties,

nee

dlin

es

and

requ

irem

ents

Processing and levels of

information exchange

requirementsBasic technology

supportability and

new capabilities

Identifies warfighterrelationships and information needs

Operationalview

Prescribes standards andconventions

Page 13 GAO-01-525 DOD Financial Management Enterprise Architecture

such as examining business processes for reengineering or definingoperational requirements to be supported by physical resources andsystems.

The systems architecture view defines the systems and theirinterconnections supporting the organizational or functional mission incontext with the operational view, including how multiple systems linkand interoperate, and may describe the internal construction andoperations of particular systems. According to DOD, this view has manyuses, such as helping managers to evaluate interoperability improvementand to make investment decisions concerning cost-effective ways tosatisfy operational requirements.

The technical architecture view defines a minimum set of standards andrules governing the arrangement, interaction, and interdependence ofsystem applications and infrastructure. It provides the technical standards,criteria, and reference models upon which engineering specifications arebased, common building blocks are established, and applications aredeveloped.

Within the three architectural views, the C4ISR Architecture Frameworkidentifies 26 graphical, textual, and tabular architectural artifacts orproducts. Of the 26, DOD specifies that 7 are essential and must bedeveloped for each enterprise architecture. Table 1 briefly describes thecontent of each essential product.

Page 14 GAO-01-525 DOD Financial Management Enterprise Architecture

Table 1: Seven Essential Products for the DOD C4ISR Architecture Framework

Essential product DescriptionOverview and summaryinformation

Serves as a planning guide and summarizes the “who,what, when, why, and how” for the architecture to bedeveloped.

Integrated dictionary Provides a central source for definitions of all termsused in all architecture products.

High-level operational conceptgraphic

Shows a high-level graphic description of theoperational concept including organizations, missions,and geographic distribution of assets.

Operational node connectivitydescription

Identifies the organizational elements that produce,process, and consume information, the need toexchange information between elements, and thecharacteristics of the information exchanged, includingcontent, media, volume requirements, securityclassification, timeliness, and interoperabilityrequirements.

Operational informationexchange matrix

Provides information exchange requirements identifyingwho exchanges what information with whom, why theinformation is necessary, and how it is needed.

System interface description Links the operational and systems architecture views bydepicting the information systems and their interfaces tothe organizational elements that produce, process, andconsume information.

Technical architecture profile Establishes a set of rules governing systemimplementation and operation. Normally, referencesexisting technical guidance and discusses how thatguidance has been or needs to be implemented.

DOD Comptroller officials acknowledge that they do not have anenterprise architecture for the department’s financial managementfunctional area. Rather, they stated that DOD is relying upon the FinancialManagement Improvement Plan to describe the department’s vision of itsfuture financial management operations and to define the interimstrategies for achieving this vision.

We compared this plan against DOD’s C4ISR Architecture Frameworkrequirements and determined that the plan is not a sufficient surrogate fora financial management enterprise architecture. To DOD’s credit, the planprovides useful conceptual information on the department’s current andfuture financial management operations and supporting systems, andbriefly describes over 200 initiatives for transitioning to this future state.Also, the plan provides some information on existing interfaces betweencomponents’ feeder systems and DFAS’ finance and accounting systems.In our view, such information would be valuable input in developing an

DOD’s FinancialManagement ImprovementPlan Is Not an EnterpriseArchitecture

Page 15 GAO-01-525 DOD Financial Management Enterprise Architecture

enterprise architecture. However, the plan does not satisfy any of theC4ISR Architecture Framework requirements for essential products.

For example, the plan does not provide a full definition of each of thedepartment’s financial management processes or discuss theinterrelationships among the processes and related systems. Morespecifically, the plan does not address the entire business process forproperty, from acquisition to disposal, nor the interrelationships amongthe functional areas of acquisition, property management, and propertyaccounting. Additionally, the plan does not provide specific information(1) defining the operational elements that produce, consume, or processdata; (2) describing the information exchanged between operationalelements; and (3) specifying the characteristics of information beingexchanged (content, format, media, volume, security classification,timeliness, and interoperability requirements). Further, the plan does notdefine the interfaces between systems in terms of the proceduresgoverning the systems, applications present, infrastructure capabilitiesand services supporting the applications, and the means by which thesystems process, manipulate, store, and exchange data. Such information,which is part of the operational and systems view product requirements, iscritical for linking information system requirements with the functionalprocesses that support the agency’s mission.

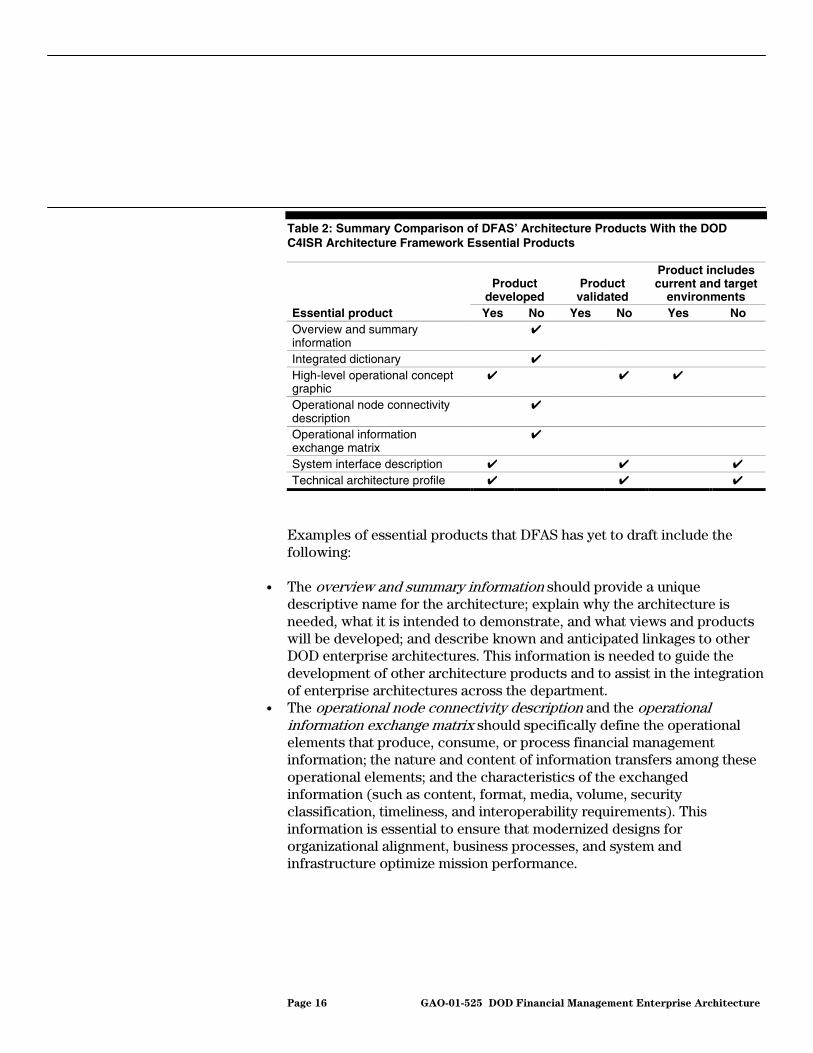

DFAS recognizes that it needs an enterprise architecture to guide andconstrain its investment in modern finance and accounting systems, and ithas begun efforts to develop one. As of February 2001, DFAS had draftedthree of the seven essential products defined in the DOD C4ISRArchitecture Framework. However, DFAS had not validated any of thethree products and had yet to begin developing the other four essentialproducts. Moreover, our analysis of the three draft products showed thatnone of the three fully satisfied DOD’s requirements. Table 2 summarizesthis analysis.

DFAS’ Efforts to Developan Enterprise ArchitectureAre Not Complete andInclude Only Finance andAccounting Functions

Page 16 GAO-01-525 DOD Financial Management Enterprise Architecture

Table 2: Summary Comparison of DFAS’ Architecture Products With the DODC4ISR Architecture Framework Essential Products

Productdeveloped

Productvalidated

Product includescurrent and target

environmentsEssential product Yes No Yes No Yes NoOverview and summaryinformation

✔

Integrated dictionary ✔

High-level operational conceptgraphic

✔ ✔ ✔

Operational node connectivitydescription

✔

Operational informationexchange matrix

✔

System interface description ✔ ✔ ✔

Technical architecture profile ✔ ✔ ✔

Examples of essential products that DFAS has yet to draft include thefollowing:

• The overview and summary information should provide a uniquedescriptive name for the architecture; explain why the architecture isneeded, what it is intended to demonstrate, and what views and productswill be developed; and describe known and anticipated linkages to otherDOD enterprise architectures. This information is needed to guide thedevelopment of other architecture products and to assist in the integrationof enterprise architectures across the department.

• The operational node connectivity description and the operationalinformation exchange matrix should specifically define the operationalelements that produce, consume, or process financial managementinformation; the nature and content of information transfers among theseoperational elements; and the characteristics of the exchangedinformation (such as content, format, media, volume, securityclassification, timeliness, and interoperability requirements). Thisinformation is essential to ensure that modernized designs fororganizational alignment, business processes, and system andinfrastructure optimize mission performance.

Page 17 GAO-01-525 DOD Financial Management Enterprise Architecture

DFAS has drafted various documents22 that partially satisfy therequirements for three essential products. For example, the DFAS Financeand Accounting Activity (Process) Model provides a functionaldecomposition of all finance and accounting processes, including theinputs, outputs, and controls, showing how an activity is to be performedin the target environment. However, this model does not provide requiredinformation on where a process activity is to be performed and who isresponsible for performing the activity.

Besides being incomplete, in that they do not include all essentialarchitectural products specified by the DOD C4ISR ArchitectureFramework, DFAS’ architectural documents do not include DOD financialmanagement operations and supporting systems that are outside DFAS’span of control. DFAS recognizes that systems outside its boundariesprovide data that are critical for its finance and accounting missionperformance and accountability. For example, the systems view states thatDFAS cannot control the characteristics of any external system. As aresult, the systems view does not include the approximately 90 feedersystems belonging to the military services and defense agencies thatsupport other functional areas (e.g., acquisition management, inventorymanagement, and human capital management) and according to DODoriginate and process about 80 percent of the data that DFAS uses. Rather,this product states that interoperability between DFAS and the feedersystems must be achieved through properly and completely definedinterfaces—hardware and software that can integrate disparate systemsand their data sets. However, the systems view does not define theseinterfaces.

DFAS officials agreed that they have not yet completed the essentialarchitectural products, as defined by the DOD C4ISR ArchitectureFramework. According to the CIO, DFAS intends to develop and validatethese products, but it has not developed a plan that specifies when theywill be completed. Additionally, even if the agency completes itsarchitecture, it will be limited to DFAS’ organizational boundaries,

22Financial management operations and systems documents include the DOD CFOFinancial Management 5-Year Plan (1997), DFAS Accounting Systems Strategic Plan (1997),DFAS Business Plan (June 1997), DFAS Finance and Accounting Activity (Process) Model(Version 4, December 1997), DFAS Information Technology Management Strategic Plan(January 2, 1998), A Guide to Federal Requirements for Financial Systems (April 4, 1998),DFAS Strategic Plan (4th update, June 1998), Defense Finance and Accounting Data Model(Version 6, February 28, 1999), and the DFAS Financial Systems Strategic Plan (Version 3.0,December 1999).

Page 18 GAO-01-525 DOD Financial Management Enterprise Architecture

meaning that this architecture will omit important DOD financialmanagement operations and systems.

DOD’s Financial and Feeder System Compliance Process and the charterof the Council that is overseeing the process, while not precludingdevelopment and use of a DOD financial management enterprisearchitecture, do not explicitly provide for developing and using one as partof either this process or DOD’s other financial management modernizationefforts. Like the Year 2000 program that it is modeled after, the complianceprocess is designed to correct weaknesses in the current accounting,finance, and feeder systems so that they substantially comply with federalfinancial systems requirements, federal accounting standards, and the U.S.Government Standard General Ledger at the transaction level as mandatedby the Federal Financial Management Improvement Act of 1996. Thesecorrective actions include making procedural changes to improvemanagement controls surrounding manual interfaces among systems, aswell as making changes to software and hardware to introduce missingmanagement controls.

Under the compliance process, each component establishes its own plansand criteria for system compliance. The Council approves the complianceplans and criteria, coordinates efforts among components, and ensuresthat defined compliance criteria are met. The purpose of the process is toensure that the accounting, finance, and feeder systems provide timely andaccurate financial data to senior DOD decisionmakers and help achievefavorable audit opinions on the department’s financial statements. As aresult, the process is intended to modify rather than modernize andoptimize the department’s current financial management operationsthrough such actions as eliminating duplicative systems, promoting systeminteroperability, and/or reengineering business processes.

Financial and FeederSystem ComplianceProcess Does Not Includean Architecture

Page 19 GAO-01-525 DOD Financial Management Enterprise Architecture

The CIO Council, in collaboration with OMB and us, has incorporatedenterprise architecture management practices used by successful publicand private sector organizations into a management framework foreffectively developing, implementing, and maintaining enterprisearchitectures.23 This framework consists of eight interrelated phases,including steps for obtaining executive support, for establishingmanagement structures and process controls, and for initiating,developing, and maintaining an enterprise architecture program (seefig. 4).

Figure 4: Simplified Diagram of the Enterprise Architecture ManagementFramework

Source: Chief Information Officers Council, A Practical Guide to Federal Enterprise Architecture,Version 1.0, February 2001.

23Chief Information Officers Council, A Practical Guide to Federal Enterprise Architecture,Version 1.0 (February 2001).

Structures andProcesses Are Not inPlace to EffectivelyDevelop andImplement a DODFinancialManagementEnterpriseArchitecture

Obtainexecutive buy-in

and support

Definearchitecture

processand approach

Developbaseline

enterprise architecture

Developtarget

enterprisearchitecture

Developsequencing plan

Useenterprise

architecture

Maintainenterprise

architecture

Establishmanagementstructure and

control

Controland

oversight

Page 20 GAO-01-525 DOD Financial Management Enterprise Architecture

The DOD organizations currently involved in directing financialmanagement modernization activities, namely the DOD ComptrollerOffice, the DFAS CIO Office, and the Senior Financial ManagementOversight Council, neither singularly nor collectively have in place thenecessary structural and process controls needed for effectivelydeveloping and implementing an enterprise architecture. Rather, theseorganizations are continuing DOD’s traditional practice of havingcomponents independently implement business processes and supportingsystems—a practice that has historically produced systems that areduplicative, not interoperable, and unnecessarily costly to interface andmaintain, and that do not optimize DOD-wide financial managementperformance and accountability.

Among other things, the architecture and management guide published bythe CIO Council presents the following recognized practices forsuccessfully initiating and developing an enterprise architecture:

• Because the enterprise architecture is a corporate asset for systematicallymanaging institutional change, the support and sponsorship of the head ofthe enterprise are essential for the architecture effort to be successful.Obtaining a clear mandate for the architecture in the form of an enterprisepolicy statement is a critical success factor and will be instrumental ingaining the buy-in and commitment of all organizational components ofthe enterprise, whose participation is vital to successfully developing andimplementing the enterprise’s architecture.

• The enterprise architecture effort should be directed and overseen by anexecutive body empowered by the head of the enterprise, whose membersrepresent all stakeholder organizations and have the authority to commitresources and to make and enforce decisions for their respectiveorganizations.

• The enterprise architecture effort should be led by a Chief Architect andmanaged as a formal program: that is, a program office should be created,core staff committed, a program management plan implemented thatdetails work breakdown structures and schedules, budgetary resourcesand tools allocated, basic program management functions performed (e.g.,risk management, change control, quality assurance, configurationmanagement), and progress tracked and reported against measurablegoals.

• The enterprise architecture’s intended use should be defined and itsappropriate scope and definitional depth specified. In doing so, it iscritically important that architecture development be approached in a top-down, incremental manner, consistent with the hierarchical architectural

DOD Does Not HaveManagement Structuresand Processes toEffectively Develop aFinancial ManagementEnterprise Architecture

Page 21 GAO-01-525 DOD Financial Management Enterprise Architecture

views that are the building blocks of published architecture frameworks,such as the DOD C4ISR Architecture Framework. It is equally importantthat the higher level architecture views span the entire enterprise. Onlythen can the needed enterprisewide understanding be developed to permitinformed decisions about whether the enterprise, and thus the enterprisearchitecture, can be compartmentalized without sacrificing its intendedpurpose.

• The enterprise architecture should be developed according to a specifiedframework and using an interactive architecture development andmaintenance tool.24

As shown in table 3, the financial management improvement efforts beingsponsored by the DOD Comptroller, DFAS, and the Senior FinancialManagement Oversight Council do not satisfy most of these recognizedpractices for effective enterprise architecture development.

Table 3: Comparison of DOD’s Management Practices to Recognized Practices forDeveloping an Enterprise Architecture

DOD (C)a DFAS SFMOCb

Recognized practices Yes No Yes No Yes NoObtain support and sponsorship of headof enterprise and gain buy-in andcommitment of all organizationalcomponents of enterprise.

✔ ✔ ✔

Establish executive body to direct andoversee architecture development andimplementation that is empowered byhead of enterprise.

✔ ✔ ✔

Appoint a Chief Architect to leadenterprise architecture effort and manageit as a formal program, including creationof a program office.

✔ ✔ ✔

Define intended use of enterprisearchitecture and specify its appropriatescope and definitional depth.

✔ ✔ ✔

Develop enterprise architectureaccording to a specified framework. ✔ ✔ ✔

aOffice of the Under Secretary of Defense (Comptroller).

bSenior Financial Management Oversight Council.

24A set of integrated and automated templates that provide the repository for eacharchitectural artifact and the means for managing the relationships and dependenciesamong these artifacts.

Page 22 GAO-01-525 DOD Financial Management Enterprise Architecture

For example, while DFAS’ ongoing architecture development efforts arefollowing the DOD C4ISR Architecture Framework, the scope of theseefforts is limited to what DFAS can control; therefore, even if itsarchitecture is completed, it will not provide a sufficient basis for effectiveand efficient DOD-wide financial management change. Moreover, DFAS isnot managing its architecture effort as a program, with a Chief Architect,detailed development plans and work breakdown structures andschedules, requisite resources, established progress and performancemeasures, and progress reporting against these measures. During thecourse of our work, the DFAS CIO told us that the agency would takesteps to strengthen its architecture management controls, such asestablishing an architecture council made up of senior agencymanagement that will be responsible for completing the architecture. InFebruary 2001, the DFAS CIO stated that the council had been establishedand its charter drafted. However, DFAS has yet to develop a detailed planwith milestones for the completion of the remaining four essentialproducts.

Similarly, neither the DOD Comptroller, who is responsible for DOD’sFinancial Management Improvement Plan, nor the Senior FinancialManagement Oversight Council, which is responsible for the Financial andFeeder System Compliance Process, plans to develop a DOD financialmanagement architecture, nor to implement the above-cited practices forarchitecture development.

According to CIO Council guidance, the following are recognized practicesto successfully implementing an enterprise architecture:

• The enterprise architecture should be integrated into the enterprise’scapital planning and investment control process and its project life-cycledevelopment/acquisition management process. Compliance of new andongoing investment projects with the architecture should be addressed bythe enterprise’s investment decisionmaking body at the projects’ key life-cycle decision points.

• All enterprise IT capital investments should be compliant with theenterprise architecture as a condition of approval and funding; waivers tothe architecture compliance requirement should be granted only if acompelling case can be made for doing so.

• An architecture technical review committee should be established toassess the architectural alignment of proposed investments and makerecommendations to the enterprise’s capital investment decisionmakingbody.

DOD Does Not HaveManagement Structuresand Processes toEffectively Implement aFinancial ManagementEnterprise Architecture

Page 23 GAO-01-525 DOD Financial Management Enterprise Architecture

As shown in table 4, the financial management improvement efforts beingsponsored by the DOD Comptroller, DFAS, and the Senior FinancialManagement Oversight Council do not satisfy these recognized practicesfor effective implementation of an enterprise architecture.

Table 4: Comparison of DOD’s Management Practices to Recognized Practices forImplementing an Enterprise Architecture

DOD (C) DFAS SFMOCRecognized practices Yes No Yes No Yes NoThe enterprise architecture is integratedinto the enterprise’s capital planning andinvestment control and project life-cycledevelopment/acquisition managementprocesses.

✔ ✔ ✔

All enterprise IT capital investments arecompliant with the architecture as acondition of approval and funding, orhave been granted a waiver.

✔ ✔ ✔

An architecture technical reviewcommittee has been established andmakes recommendations to theenterprise’s capital investmentdecisionmaking body.

✔ ✔ ✔

Since DOD has not developed a complete DOD financial managemententerprise architecture, it cannot determine whether proposed systeminvestments are compliant with one. However, even if such an architectureexisted, neither DFAS nor the DOD Comptroller has the investmentdecisionmaking authority across all DOD financial managementoperations to ensure that modernization investments comply with thearchitecture. Further, neither has established the structural and processcontrols cited above to ensure that DOD financial managementinvestments are architecturally compliant.

According to a representative of the DOD Comptroller, rather thandevelop and implement a financial management architecture, the DODComptroller’s office is working with the DOD CIO’s office to implementportfolio management as a way of guiding and constraining thedepartment’s financial management investments. However, portfoliomanagement cannot be fully effective without an enterprise architecture.According to OMB Circular A-13025 and the CIO Council’s published

25OMB Circular A-130, Management of Federal Information Resources (November 30,2000).

Page 24 GAO-01-525 DOD Financial Management Enterprise Architecture

enterprise architecture management guide, effectively managing aninvestment portfolio, whether it is based on an organization or a functionalarea, requires that the portfolio be grounded in and derived from theenterprise architecture capital investment sequencing plan. Moreover, theDOD CIO’s draft policy and guidance on portfolio management state thatfunctional area portfolios should be based on architectures. Thus, theDOD Comptroller Office’s plans for employing portfolio investmentmanagement in place of an enterprise architecture are not consistent withOMB and DOD positions.

Also, the Senior Financial Management Oversight Council’s charter, whilenot precluding the Council from enforcing the implementation of anenterprise architecture, if one existed, does not explicitly provide for thisrole and responsibility, nor for establishing any type of architecturetechnical review committee to support the Council in doing so. Instead,the Council is to

• be the final approval authority for all action plans developed by themilitary services and defense agencies;

• provide oversight and guidance on all matters concerning the complianceprocess;

• review the status of the applicable systems efforts at least quarterly;• approve the exit criteria for the phases of the compliance process;• establish and oversee a Systems Compliance Working Group to, among

other things, (1) review all corrective action plans developed by themilitary services and defense agencies before they are submitted to theCouncil and the head of the responsible component, (2) coordinate actionspertaining to compliance of critical accounting, finance, and feedersystems with the respective components, (3) review quarterly statusbriefings, and (4) recommend systems for exit from the phases of thecompliance process; and

• verify that all established exit criteria for a particular phase have beenfulfilled.

Page 25 GAO-01-525 DOD Financial Management Enterprise Architecture

DOD has long operated and evolved its existing financial managementprocesses and systems without a financial management enterprisearchitecture. Under this approach, each military service and defenseagency developed its own processes and supporting systemsindependently from one another. Even after the establishment of DFAS toconsolidate certain financial management operations and systems, DODcomponents have continued to play a vital role in the end-to-end financialmanagement process. Specifically, the components still operate andmaintain their own unique program management systems that capturefinancial event data and provide these data to DFAS for its use inpreparing various financial reports on DOD operations. To furthercomplicate this situation, the financial management functions that areperformed by DFAS and the components have been allowed to vary fromcomponent to component.

The result of this architecturally unguided and unconstrained environmentis understandably a collection of existing DOD financial managementprocesses and systems that are nonstandard and “siloed,” causingprocesses to be slow and susceptible to error. In many cases, the use ofhard-copy information, such as from faxed forms, and manual entry arenecessary to ensure that data from the feeder systems are entered intoDFAS’ systems.26 This extensive reliance on these manual interfaces meansthat millions of transactions must be keyed and rekeyed into multiplesystems.27 This lack of standard finance and accounting processes and thedifficulty of sharing data among heterogeneous systems are a root cause ofmultiple problems, including (1) disbursements that are not properlymatched to specific obligations recorded in the department’s records,(2) unauditable financial statements, (3) delays in obtaining data,(4) duplicate system interfaces that must be maintained, and (5) manualreconciliation of the reported differences between different sets ofrecords.28

Another example of this lack of standardization is the complex line ofaccounting code required for recording of financial transactions; thesecodes accumulate appropriation, budget, and management information. To

26DFAS Financial Systems Strategic Plan (December 1999).

27Performance and Accountability Series: Major Management Challenges and ProgramRisks, Department of Defense (GAO-01-244, January 2001).

28DFAS Financial Systems Strategic Plan (December 1999).

Without a Completeand EnforcedFinancialManagementArchitecture, NeitherDOD’s ExistingSystems Nor ItsModernization PlansAre Well Integrated

Page 26 GAO-01-525 DOD Financial Management Enterprise Architecture

illustrate, the following line of code is used for the Army’s Operations andMaintenance appropriation:

2162020573106325796.BD26FBQSUPCA200GRE12340109003AB22WORNAAS34030

An error in any one character in such a line of code can delay paymentprocessing or affect the reliability of the data used to support managementand budget decisions. Compounding this problem is that the lines of codeare not standard between the military services and fund types.

Without a financial management enterprise architecture, DOD willperpetuate its existing problems of disparate and noninteroperableprocesses and systems. According to a recent DOD Inspector Generalreport,29 these problems continue. The DOD Inspector General reportedthat DFAS’ current modernization efforts are not being managed as anintegrated set of projects and thus will not likely succeed in creating a setof integrated financial management systems. The report stated thateffective and comprehensive management controls and oversight wereneeded to achieve the DOD financial management modernization goals ofstandardized business processes and a reduced number of accounting,finance, and feeder systems. These management controls and oversightinclude effective use of a financial management enterprise architecture.

Currently, DOD is investing and planning to invest significant resources toaddress its financial management challenges. DFAS, military service, anddefense agency financial management modernization initiatives number inthe hundreds and are expected to cost billions of dollars. However,because responsibility and accountability for these initiatives are diffusedacross many DOD components and activities, and because these initiativesare not part of an integrated portfolio of investments, departmentwideaggregated information on the estimated costs for these initiatives islimited.

To illustrate, DFAS currently has 32 modernization projects underway, butneither DFAS’ System Integration Directorate nor its CIO could provide uswith either the total acquisition cost or the life-cycle cost30 of these

29Oversight of Defense Finance and Accounting Service Corporate Database Development(Report No. D-2001-030, December 28, 2000).

30Life-cycle cost is the total cost to the government for an information system over itsexpected useful life. It includes costs to design, develop, acquire, operate, and dispose ofthe system.

Page 27 GAO-01-525 DOD Financial Management Enterprise Architecture

projects, because such information is not maintained centrally in DFASand would have to be obtained from the managers for the respectiveprojects. Instead of estimated costs, DFAS officials provided budgetarydata for fiscal years 2000 through 2007, which show that DFAS plans toinvest $2.2 billion during this 8-year period to acquire and operate systemsassociated with its modernization activities.

Similarly, DOD does not have a reliable estimate of the cost to make themilitary service and defense agency feeder systems compliant with federalfinancial management requirements. While the Financial ManagementImprovement Plan identifies approximately $1.4 billion, this covers only aportion of the projects identified in the plan. Moreover, the Director forBusiness Policy, Office of the DOD Comptroller, who is responsible formaintaining the plan, told us that this cost estimate was questionable andthat one of the first steps in the Financial and Feeder System ComplianceProcess is to develop a reliable cost estimate for the effort.

We also found that some DOD components are investing in differentfinancial management solutions. For example, the Army, Naval AirSystems Command, and the Defense Logistics Agency (DLA) haveseparate programs underway that are estimated to cost about $700 million,$750 million, and $900 million, respectively, to implement differentcommercially available products for automating and reengineering variousenterprise operations.31 Among the functions that these commercial“enterprise resource planning” products address is financial management.In the case of DLA, the agency plans to establish teams that would defineinterfaces (hardware and software) that are to perform, for example, rateconversion to allow DLA to exchange information with DFAS and others.

DOD acknowledges the need to manage the relationships among thesedifferent modernization activities. Specifically, it recently issued aprogram budget decision directing all components that are pursuingenterprise resource planning solutions to report to the Deputy ChiefFinancial Officer by March 31, 2001, on how their respective efforts willuse and interface with DOD’s current and planned standard systems.Additionally, in the future, all DOD components must submit a similarreport no later than 90 days after they decide to begin planning or

31These commercial products are referred to as enterprise resource planning (ERP)solutions. ERP products consist of multiple, integrated functional modules that do differenttasks, such as track payroll, keep a standard general ledger, manage supply chains, andorganize customer data.

Page 28 GAO-01-525 DOD Financial Management Enterprise Architecture

designing an enterprise resource planning systems solution. While thisdecision acknowledges the above-cited problem of DOD componentsinvesting separately in financial management processes, it does notaddress the root problem—that a DOD-wide financial managemententerprise architecture is not being used to guide and constrain theseinvestments.

DOD does not have a financial management enterprise architecture, and itdoes not currently have the management structures and processes in placeto effectively develop, implement, and maintain one. DOD has not appliedrecognized best practices: in particular, support and sponsorship by thehead of the enterprise, and assignment of accountability andcommensurate authority for developing, implementing, and maintaining aDOD-wide financial management enterprise architecture. Nevertheless,DOD’s various components are either spending or planning to spendbillions of dollars to acquire new or modify existing financial managementsystems. In the absence of a complete, enforceable enterprise architecturefor DOD-wide financial management operations and systems, making suchinvestments is unwise. If DOD continues down this road, it runs theserious risk that its components will spend billions of dollars modifyingand modernizing financial management systems independently from oneanother, resulting in DOD perpetuating an existing systems environmentthat suffers from duplication of systems, limited interoperablity, andunnecessarily costly operations and maintenance.

As part of its plans for investing in financial management systemsmodernization, DOD has taken some actions that appropriately exploitlessons learned from its Year 2000 program. DOD can build upon actionssuch as these and activities already underway to ensure that it employsrecognized best practices for enterprise architecture management. DODcan thus position itself to cost effectively manage the billions of dollars itplans to spend to address its high-risk financial management operations.This approach will increase DOD’s chances of modernizing its financialmanagement operations and supporting systems in a way that willoptimize financial management performance and accountability.

We recommend that the Secretary of Defense immediately designate DODfinancial management modernization a departmental priority andaccordingly direct the Deputy Secretary of Defense to lead an integratedprogram across the department for modernizing and optimizing financialmanagement operations and systems.

Conclusions

Recommendations forExecutive Action

Page 29 GAO-01-525 DOD Financial Management Enterprise Architecture

We further recommend that the Secretary immediately (1) issue a DODpolicy that directs the development, implementation, and maintenance of afinancial management enterprise architecture and (2) modify the SeniorFinancial Management Oversight Council’s charter to

• designate the Deputy Secretary of Defense as the Council chair and theUnder Secretary of Defense (Comptroller) as the Council vice-chair;

• empower the Council to serve as DOD’s financial management enterprisearchitecture steering committee, giving it the responsibility and authorityto ensure that a DOD financial management enterprise architecture isdeveloped and maintained in accordance with the DOD C4ISRArchitecture Framework;

• empower the Council to serve as DOD’s financial management investmentreview board, giving it the responsibility and authority to (1) select andcontrol all DOD financial management investments and (2) ensure that itsinvestment decisions treat compliance with the financial managemententerprise architecture as an explicit condition for investment approvalthat can be waived only if justified by a compelling written analysis; and

• expand the role of the Council’s System Compliance Working Group toinclude supporting the Council in determining the compliance of eachsystem investment with the enterprise architecture at key decision pointsin the system’s development or acquisition life cycle.

Additionally, we recommend that the Secretary immediately make theAssistant Secretary of Defense (Command, Control, Communications &Intelligence), in collaboration with the Under Secretary of Defense(Comptroller), accountable to the Senior Financial Management OversightCouncil for developing and maintaining a DOD financial managemententerprise architecture. In fulfilling this responsibility, we recommend thatthe Assistant Secretary appoint a Chief Architect for DOD financialmanagement modernization and establish and adequately staff and fund anenterprise architecture program office that is responsible for developingand maintaining a DOD-wide financial management enterprisearchitecture in a manner that is consistent with the framework defined inthe CIO Council’s published guide for managing enterprise architectures.In particular, the Assistant Secretary should take appropriate steps toensure that the Chief Architect

• obtains executive buy-in and support,• establishes architecture management structure and controls,• defines the architecture process and approach,• develops the baseline architecture, the target architecture, and the

sequencing plan,

Page 30 GAO-01-525 DOD Financial Management Enterprise Architecture

• facilitates the use of the architecture to guide financial managementmodernization projects and investments, and

• maintains the architecture.

In addition, we recommend that the Assistant Secretary of Defense(Command, Control, Communications & Intelligence) report at leastquarterly to the Senior Financial Management Oversight Council on theChief Architect’s progress in developing a financial managemententerprise architecture, including the Chief Architect’s adherence toenterprise architecture policy and guidance from OMB, the CIO Council,and DOD.

Further, we recommend that the Senior Financial Management OversightCouncil report to the Secretary of Defense every 6 months on progress indeveloping and implementing a financial management enterprisearchitecture. We also recommend that the Secretary report every 6 monthsto the congressional defense authorizing and appropriating committees onprogress in developing and implementing a financial managemententerprise architecture.

Until a financial management enterprise architecture is developed and theCouncil is positioned to serve as DOD’s financial management investmentreview board as recommended above, we also recommend that theSecretary of Defense limit DOD components’ financial managementinvestments to (1) deployment of systems that have already been fullytested and involve no additional development or acquisition cost, (2) stay-in-business maintenance needed to keep existing systems operational,(3) management controls needed to effectively invest in modernizedsystems, and (4) new systems or existing system changes that arecongressionally directed or are relatively small, cost effective, and low riskand can be delivered in a relatively short time frame.

In written comments on a draft of this report, the DOD DeputyComptroller stated that the Secretary of Defense is committed toimproving the department’s financial management operations andproviding departmental managers and the Congress with more accurateand reliable information for use in the decisionmaking process (seeappendix III). The Deputy Comptroller further stated that the departmentwould consider our recommendations, in conjunction withrecommendations from ongoing studies directed by the Secretary, indeveloping a strategy to improve DOD’s financial management operations.

Agency Comments

Page 31 GAO-01-525 DOD Financial Management Enterprise Architecture

This report contains recommendations to you. The head of a federalagency is required by 31 U.S.C. 720 to submit a written statement onactions taken on these recommendations. You should submit yourstatement to the Senate Committee on Governmental Affairs and theHouse Committee on Government Reform within 60 days of the date ofthis report. A written statement also must be sent to the House and SenateCommittees with the agency’s first request for appropriations made morethan 60 days after the date of this report.

We are sending copies of this report to Senator John Warner, Chairman,and Senator Carl Levin, Ranking Member, Senate Committee on ArmedServices; Senator Ted Stevens, Chairman, and Senator Daniel Inouye,Ranking Member, Senate Appropriations Subcommittee on Defense;Representative Bob Stump, Chairman, and Representative Ike Skelton,Ranking Democratic Member, House Armed Services Committee;Representative Jerry Lewis, Chairman, and Representative John P. Murtha,Ranking Minority Member, House Appropriations Subcommittee onDefense; Representative Stephen Horn, Chairman, and RepresentativeJanice D. Schakowsky, Ranking Minority Member, Subcommittee onGovernment Efficiency, Financial Management, and IntergovernmentalRelations, House Committee on Government Reform; the HonorableMitchell E. Daniels Jr., Director, Office of Management and Budget; theHonorable Dov S. Zakheim, Under Secretary of Defense (Comptroller);and the Honorable Thomas R. Bloom, Director, Defense Finance andAccounting Service. Copies of this report will be made available to othersupon request.

Page 32 GAO-01-525 DOD Financial Management Enterprise Architecture

If you or your staff have any questions on matters discussed in this report,please contact either of us at (202) 512-3439 or (202) 512-9095. We can alsobe reached by e-mail at [email protected] or [email protected]. Key contributorsto this report were Robert L. Crocker, Jr., Jean K. Lee, Madhav S. Panwar,Sanford F. Reigle, Phillip E. Rutar, and Darby W. Smith.

Sincerely yours,

Randolph C. HiteDirector, Information Technology Systems Issues

Gregory D. KutzDirector, Financial Managementand Assurance

Appendix I: Objectives, Scope, and

Methodology

Page 33 GAO-01-525 DOD Financial Management Enterprise Architecture

The objectives of our review were to determine (1) the status of DOD’sefforts to develop and implement a departmentwide financial managemententerprise architecture to guide and constrain its modernization programand (2) the effectiveness of DOD’s structures and processes for managingthis architecture.

To determine the status of DOD’s efforts to develop this architecture, wereviewed relevant federal and DOD enterprise architecture policy andguidance, including OMB memorandums and circulars,1 the CIO Council’sFederal Enterprise Architecture Framework Version 1.1, and DOD’sCommand, Control, Communications, Computers, Intelligence,Surveillance, and Reconnaissance (C4ISR) Architecture Framework,Version 2.0. In addition, we identified the DOD organizations involved inefforts to reform and modernize DOD financial management operationsand systems, as well as organizations responsible for DOD policy andguidance on enterprise architectures, including the Office of the UnderSecretary of Defense (Comptroller); the Office of the Assistant Secretaryof Defense (Command, Control, Communications and Intelligence); theDFAS Office of the Director, Information and Technology; and the DFASOffice of the Director for Systems Integration. From each of theseorganizations, we solicited information on plans and activities that definedthe form and content of these reform and modernization efforts. We thenquestioned officials from each organization about planned and existingarchitectural documents and obtained copies of all such plans andarchitectural documents. Next, we analyzed the information provided,including DOD’s Financial Management Improvement Plans, DOD’sFinancial and Feeder Systems Compliance Process documentation, andavailable DFAS enterprise architecture documentation, against DOD’sC4ISR Architecture Framework to determine the extent to which theseorganizations individually or collectively had produced architecturaldocumentation that satisfied DOD requirements.

To determine the effectiveness of DOD’s structure and processes formanaging the development and implementation of a financial managemententerprise architecture, we obtained and reviewed the CIO Council’s APractical Guide to Federal Enterprise Architecture, Version 1.0, as well aspublished information related to the enterprise architecture best practices

1Clinger-Cohen Act of 1996; OMB Circular No. A-130, Management of Federal InformationResources (November 30, 2000); and the Chief Information Officers Council, A PracticalGuide to Federal Enterprise Architecture, Version 1.0 (February 2001).

Appendix I: Objectives, Scope, andMethodology

Appendix I: Objectives, Scope, and

Methodology

Page 34 GAO-01-525 DOD Financial Management Enterprise Architecture

that the guide is based upon. We then obtained descriptions of themanagement controls in place, including policies, procedures, andcharters, for these organizations and their respective reform andmodernization activities. We also interviewed officials from theseorganizations about controls in place and planned. We then analyzed thesecontrols against the best practices described in the CIO Council guide toidentify any variances.

Additionally, we requested cost data on DFAS’ modernization program andreviewed information in the Year 2000 Financial ManagementImprovement Plan about other DOD component initiatives to improvesystems that provide financial management data. We then discussed withDFAS officials the nature and extent of efforts underway to define therelationship between the DFAS modernization program and the financialelements of these improvement initiatives.

We conducted our work at the above-cited agencies and offices inWashington, D.C., and Crystal City, VA. We performed our review fromApril 2000 through March 2001 in accordance with generally acceptedgovernment auditing standards.

Appendix II: Description of DOD Architecture

Framework Essential Products

Page 35 GAO-01-525 DOD Financial Management Enterprise Architecture

The C4ISR Architecture Framework, Version 2.0, provides the rules,guidance, and products for all DOD components to use in developingenterprise architectures. This framework requires three interrelatedarchitecture views: operational, systems, and technical. Within theseviews, the framework defines a total of 26 architecture products anddesignates 7 of these products essential or mandatory for all architectures.According to the framework, these seven products provide the minimumarchitectural description needed to permit, among other things,integration of architectures across the department and informedinvestment decisionmaking. Each of these seven essential products isdescribed below under the primary view that it supports. Two of theproducts support all three views and are described under “All Views.”