francis w. seymore

TRANSCRIPT

1 decontamination of contaminated systems, e.g., ,using aggressive chemical solvents

2 to dissolve corrosionfilms holding radionuclides, thereby reducing radiation levels.

3 While effective, the on-site decontamination processes are nof expected to

4 reduce residual, radioactivity to the levels necessary to release the material as clean

5 scrap. Therefore, all contaminated components will have to be removed for

6 controlled burial. However, decontamination will reduce personnel exposure and will

7 permit workers to operate in the immediate vicinity of most components, cutting and

8 removing them for controlled disposition at a low-level radioactive waste burial

9 facility.

10

Contaminated piping to and from major components will be cut and removed.

11

Selected major components such as the reactor coolant pumps, steam generators,

12

pressurizers, and other large 6omponents will then tie removed intact and sealed so

13

that they may be transported off-site. Smaller components, such as sampling

14

system pumps, filters, filter housings, strainers, etc., will be loaded into containers

15

and shipped for controlled disposal.

16

The reactor vessel and its internals will be segmented and remotely loaded

17

into,steel liners for transport to the burial facility in heavily shielded shipping casks.

18

The =reactor vessel and internals will have sufficiently high radiation levels to require

19

all cutting to be done underwater or behind heavy shields, using cutting tools

20

operated by remote control to reduce radiation exposure to the workers.

21

Concrete immediately surrounding the reactor vessel is expected to be

22

radioactive and will be removed by controlled blasting. This blasting process is well

23

developed, safe, and is the most cost effective way to remove the heavily-reinforced

24

concrete from the structure.

25 Some surfaces of sections of interior floors within areas of the Containment

26 and other buildings in the power block are expected to be contaminated from

21 DIRECT TESTIMONY OF FRANCIS W. SEYMORE

600

1 exposure to contaminated air/water as a result of plant operations. This

2 contamination will be removed by scarification (surface removal) so that the

3 remaining surfaces will be cleaned to release levels and will not require disposal as

4 Class A radioactive waste.

5 Contaminated process equipment, pipe hangers, supports, dnd el,ectrical

6 components will be removed and routed for controlled disposal.

7 Finally, an extensive radiation survey will be performed to ensure all

8 radioactive materials above the levels specified by the NRC have been removed

9 from the site. With NRC confirmation, the NRC license for Most of the site (excluding

10 the ISFSI) will be terminated.

11

12 C. Period 3 — Site Restoration

13, This period begins once license termination activities have concluded and

14 involves the demolition of all remaining structures, typically to a depth, of three feet

15 below grade. Clean concrete rubble would be used on-site for fill and additional soil

16 would be used to cover each subgrdde structure. Excess rubble is trucked, off-site

17 for disposal.,

18

19 D. Post Period 3 — Spent Fuel Storage

20 The ISFSI wilF pontinue to operate under a Part 50 license following the

21 transfer of the spent fuel inventory from the Fuel Building. Transfer of spent fuel to a

22 DOE or interim facility will be exclusively from the ISFSI once the fuel pools have

23 been emptied and the struciures 'released for decommissioning. Palo Verde will

24 continue shipping spent fuel canisters to DOE through the year 2098.

25 At the conclusion of the spent fuel transfer process, the ISFSI will be

26 decommissioned. TLG's estimate includes the cost to decommission the ISFSI. In

22 DIRECT TESTIMONY OF FRANCIS W. SEYMORE

601 ,

the ISFSI, the spent fuel assemblies are contained within stainless .steel canisters.

2 On the IŠFSI pad, these canisters are housed within reinforced concrete and steel

3 shield cylinders khown as gverpacks. The canisters are assumed to 'be removed,

4 shipped, and disposed of by the DOE. The steel overpack liners are assumed to

5 have some level of neutron-indUced, activation as a result of the long-term storage of

6 the fuel, i.e., to levels exceeding free-release limits. As an allowance, seven

7 overpacks per unit (site total of 21) are assumed to require remediation, equivalent to

8. the number of overpacks required to accommodate the final core- offloads at Palo,

9 Verde (241 assemblie5 per unit for a site total of 723 assernblies).. The cost of the

10 disposition of, this material, as well as the demolition of the ISFSI facility, is included

11 in. the estimate. The NRC will terminate the remaining license if it determines that

12 site remediation has been performed in accordance with a license .termination plan

13 and the terminal radiation survey and' associated documentation demonstrate that

14 the facility meets the release criteria. Once the requirements are satisfied, the NRC

15 can terminate the remaining license for the ISFSI.

16 The remaining reinforced concrete dry storage modules are then demolished,

17 the concrete storage pad,is removed, and the area graded and landscaped to 11.

18 conform to the surrounding environment.

19 '

20 Q. HOW DOES THE PRESENCE OF SPENT FUEL ON SITE AFTER PLANT

21 SHUTDOWN AFFECT THE DECOMMISSIONING PROCESSES?

22 A. Although the study does not address the transport or disposal of spent fuel from the

23 •Palo Verde site, it does consider the:constraint that the presence of spent fuel on the

24 site can impose on other decommissioning activities. •In particular, the

25 decommissioning scheduling developed in support of the last four cycles of cost

26 updates for• the Palo Verde estimates incorporates an APS request for a six-year

23 DIRECT TESTIMONY OF FRANCIS W. SEYMORE

• 602

1 rninimum cooling prerequisite for off-loading the fuel from the storage pools. As

2 such, these spent.fuel management activities will necessarily delay the final release

3 of the power blocks-for alternatiVe/unrestricted use. This delay is reflected in the

4 increased cost of the period-dependent activities. To the extent possible, the

5 decommissioning estimates were structured around the spent fuel areas of the units

6 and their availability for decontamination, such that delays in decommissioning other

7 portions of the facility could be minimized. Decommissioning would proceed on the

8 surrounding facilities and non-essential systems during the approximately six-year

9 pool off-load period. The operating licenses can then be amended with the.

10 remaining fuel placed in dry storage.

11 Some small portion of the existing.Palo Verde site will continue to be licensed

12 by the NRC under the existing Part 50 license for the ISFSI. The endpoint of this

13 storage period is estimated to be in 2098. Following this, the ISFSI will be

14 decommissioned, the license terminated, and the concrete storage casks and pads

15 crushed and removed.

16

17- Q. DOES THE PROCESS OF DECOMMISSIONING EXTEND BEYOND REMOVAL OF

18 CONTAMINATED AND ACTIVATED MATERIAL FROM THE SITE?

19 A. Yes. There are additional activities .beyonct the removal of contaminated' material

20 that will be undertaken in the process ofreleasing the šite for alternative use. This

21 work includes costs for the remaining dismantling and .grading operations and is

22 generally referred to assite restoration.

23

24 Q. PLEASE DESCRIBE THE SITERESTORATION ACTIVITIES.

25 A. These activities begin once license termination activities have concluded and involve

26 the demolition of all remaining structures, typically to a depth of three feet below

24 DIRECT TESTIMONY OF FRANCIS W. SEYMORE

603

1

2

3-

4

5

6

7

8

9

10

11

12

13 Q.

14

15 A.

16

17

18

19

20

21

22

23

24

25*

26

grade. Clean concrete rubble generated from the demolition of the Containment,

Auxiliary, Fuel, Radwaste, and Turbine Buildings, etc., would be used on-site for fill

and additional soil would be used to cover each subgrade structure. Excess rubble

is trucked off-site for disposal. Either any below grade structures will be removed, or

voids below grade, such as the 31-mile buried water line from Phoenix to the Water

Reclamation Facility, will belilled with sand or concrete. The object is to prevent any

future surface subsidence.

Once the below grade features of the site have been addresed, the surface

of the site will be graded to conform to the surrounding environs. The evaporation

and makeup water reservoir walls will be breached to prevent retaining water. At thie

point, the site is available for reuse, except for the footprint otthe ISFSI.

WHY WERE THE REMAINING STRUCTURES ON SITE ASSUMED TO BE .

DISMANTLED?

Efficient removal of the contaminated materials and verification that the radionuclide

concentrations are below the stringent NRC limits will require substantial damage to

many of the structures. Blasting, coring, drilling, scarification (surface removal), and

the other décontamination work will damage power block structures including the

Containrnent, Radwaste, Auxiliary, •and Fuel Buildings. Verifying that subsurface

radionuclide concentrations meet NRC site release requirements may require

removal, of grade slabs and lower floors, potentially weakening footings and

structural supports.

It is also important 4o remember that the Palo Verde-structures were custom

designed and built to supp'Ort a specific nutlear unit design that went into service in

the 1980s. They would most likely be an impediment rather than a benefit to any

potential future plant, if one were ever to be constructed at the site. Moreover, the

25 DIRECT TESTIMONY OF FRANCIS W. SEYMORE

604

1 facilitys infrastructure degrades without continual maintenance. Unless the site is

2 redeveloped shortly after release of its NRC license, the value in reusing plant

3 facilities quickly diminishes.

4 As demonstrated by U.S. experience, dismantling is clearly the most

5 appropriate and cost-effective option and should serve as the foundation for the

6 decommissioning cost estimates. It is unreasonable to anticipate that these

7 structures would be repaired and preserved after the radiological contamination is

8 removed.

9

10 Q. WHAT ASSURANCE IS THERE THAT THE ESTIMATED COST' FOR

11 DECOMMISSIONING WILL REFLECT FUTURE DEVELOPMENTS AND

12 INCREASES OR DECREASES IN COSTS?

13 A. The cost estimate prepared for Palo Verde is based on present technology, the

14 current information available on decornmissioning costs, and on existing federal

15 regulations. No provision is made to include future costs or savings due to the

16 uncertainties in improvements in technology, major regulatory changes, inflation

17 factors, etc. It should be noted that the contingency, as used in the estimates, only

18 covers uncertainties within the decommissioning schedule timeframe.

19 ,

20 VII. RECOMMENDATIONS

21 Q. IS IT NECESSARY TO SELECT A SPECIFIC DECOMMISSIONING METHOD• AT

22 THIS TIME?'

23 A. No. The .actual method or •combination of methods selected to decommission

24 Palo Verde should be based on a detailed. economic, engineering, and

25 environmental evaluation of the alternatives considering the site and surroundings at

26 the time of decommissioning and reflecting the latest experience in the

26• DIRECT TESTIMONY OF FRANCIS W. SEYMORE

605

1 decommissioning of similar nuclear power facilities. The owners of Palo Verde will

2 make such evaluations near the time of final.shutdown of the units.

3

4 Q. WHAT ARE YOUR RECOMMENDATIONS?

5 A. I recommend that, for planning purpose§, the decommissioning cost funding be

6 based upon reinoval of Palo Verde using- the DECON alternative. This alternative

7 provides the most reasonable mbans for amending/terminating the license for the

8 site in the shortest possible time. Furthermore, this alternative avoids the long-term

9 costs and commitments associated with the maintenance, surveillance and security

10 requirements of the conventional delayed dismantling alternatives. The Commission

11 has adopted the DECON alternative as a basis for ,funding nuclear plant

12 decommissioning in every case in which a TLG witness has testified.

13 The DECON alternative also allows use of the plants knowledgeable

14 operating staff, a valuable asset to a well-managed, efficient decommissioning

15 program. Equipment needed to support decommissioning operations such as

16 cranes, ventilation. systems, and radwaste processing equipment would be fully

17 operational. In addition, the site would be available for other use in the near term,

18 with the exception of the area immediately surrounding the plants fuel storage,

19 facility.

20

21 VIII. CONCLUSION

22 Q. PLEASE SUMMARIZE YOUR ;TESTIMONY.

23 A. In 2016, TLG performed site-specific cost estimates for the decommissioning of

24 Palo Verde. The total estimated cost for the decommissioning in 2016 dollars was

25 $2,739.1 million. The study shows an increase of approximately $330 million dollars,

26 or 13.7 percent, from the 2013 estimate. These amounts includes costs to remove

27 DIRECT TESTIMONY OF FRANCIS W. SEYMORE

1 all radioactive materials from the site which exceed the release criteria, terminate the

2 NRC operating licenses, remove all structures above the three foot below grade

3 elevation and backfill all below grade voids to the surface elevation, transfer all spent

4 fuel from all three Fuel Buildings to the on-site ISFSI, operate thisiSFSI until 2098

5 (excluding ISFSI security and operating staff and ISFSI operating expenses, which

6 •are assumed to be recovered from the DOE and therefore not included), and

7 decommissiOn the ISFSI following removal of all spent fuel and GTCC material by

8 the DOE, currently estimated to occur in the year 2099..

10 Q. DOES THIS CONCLUDE YOUR TESTIMONY?

11 A. Yes, it does.

28 DIRECT TESTIMONY OF FRANCIS W. SEYMORE

607

FRANCIS W. SEYMORE, PE EXHIBIT FWS-1

Manager, Engineering Design Page 1 of 6

EDUCATION:

Rensselaer Polytechnic Institute, Troy, New York B.S. Nuclear Engineering, Rensselaer Polytechnic Institute, 1977 M.E Nuclear Engineering, Rensselaer Polytechnic Institute, 1979

CERTIFICATIONS:

Licensed Professional Engineer: State of Connecticut Registered'Professional Engineer, Commonwealth of Pennsylvania

WORK EXPERIENCE:

TLG Services, Inc. (An Entergy Company)

Project Managementand •Regulatory Support 1982 - Present

As the Manager, Engineering Design, directS the technical aspect's and acceptance .criteria of technical and financial studies supporting the planning of nuclear power plant decommissioning. These studies provide both the engineering scope and financial resources associated with the projected disposition of a nuclear generating unit at its end of operating life.

Project Manager for the following U.S. commercial decommissioning cost estimates:

• Beaver Valley • Perry • Browns.Ferry • Prairie Island' • Brunswick • H.B. Robinson Unit' No. 2 • Calvert Cliffs . San Onofre • Davis-Besse . Sequoyah • R.E. Ginna • Shearon Harris • Millstone . Shoreham • Monticello • Three Mile Island Unit 2 • Nine Mile Point ' . Watts Bar

Technical Manager or provided calculations for the decommissioning costs for the folliming U.S. commercial decommissioning cost estimates:

• Arkansas Nuclear One • North Anna . Big Rock Point • 'Oconee ., Braidwood • •Oyster Creek . Byron • Palisades .. Callaway • Peach Bottom . Catawba . Pilgrim • Clinton • Point Beach . Comanche Peak • Quad Cities . Cooper • Rancho Seco • Crystal River 3 •' River Bend . Diablo Canyon . SI. Lucie . Dresden • ISaleM . Duane Arnold . Seabrook • Farley • South Texas Project • FitzPatrick • Surry'

As of 08/20.12 608

Francis W. Seymore EXHIBIT FWS-1 Page 2 of 6

• Fort Calhoun • Susquehanna • Grand Gulf • Three Mile Island Unit 1 • Hatch • Trojan (aka Columbia) • Hope Creek • Turkey Point • Humboldt Bay Unit 3 • V.C. Summer • Indian Point' • Vermont Yankee • Kewaunee • Vogtle • LaSalle County • Waterford 3 • Limerick • Wolf Creek • McGuire • Zion

Project Manager or provided calculations for the financial escal6tion and present value model of future decommissioning costs for the following U.S. commercial nuclear power plantš:

• Beaver Valley • Palo Verde • Braidwood • Peach Bottom • ; Byron • Perry • Clinton • Pilgrim • Comanche Peak • Quad Cities • Davis-Bessel • Salem • Dresden • Three Mile Island Unit 1 • Indian Point Energy Center • Three Mile Island Unit 2. • LaSalle County • Vermont Yankee • Limerick • Zion

Oyster Creek

Project Manager for the following U.S. cornmercial fossil dismantling cost estimates: • • Pacific Gas & Electric Renewable (2 stations)

• Westar Energy (32 units / 3 wind farms), • Xcel Energy / Northern States Power (46 units / 2 wind farms) • Xcel Energy / Public Service of Colorado (27 units) • Xcel Energy / Southwestem Public Service (32.units)

609

Francis W. Seymore EXHIBIT FWS-1 Page 3 of 6

Project Manager for the following neutron activation analyses for commercial nuclear power reactors:

• Humboldt Bay Power Plant Unit 3' • Fort Calhoun Station • Oyster Creek Nuclear Generating Station • Pathfinder • Rancho Seco Nuclear Generating Station • Saxton Experimental Nuclear Facility • Shoreham Nuclear Power Station • Trojan Nuclear Plant (aka Columbia) • Yankee-Rowe

Developed a finite element analysis model for the Trojan Reactor Pressure Vessel and Internals package to determine the thermal profile during shipping conditions, using the FEA computer code ALGOR.

Project manager for• estimates to determine the cost to stabilize, decontaminate and decommission a PWR and a BWR commercial power reactor following a severe nuclear accident involving a reactor core meltdown and breach of the reactor vessel

Contributing author on a study for the Atomic, Industrial Forum on the standardization of cost' estimating in decommissioning as used in the support of regulatory and/or rate case hearings.

While stationed on site at Three, Mile Island Unit 2 (1982-83) as part of the recovery effort, wrote, tested, and implemented procedures for removal of the Unit 2 reactor vessel closure head as well as sampling and remote examination of the damaged core:

DECCER Cost Model Development 1984 -.Present

Converted and expanded the DECCER (DECcommissioning Costs, Exposures and Radwaste) BASIC computer logic to become the leading decommissioning cost estimating model for the U.S. comrnercial nuclear power industry. Handles all revisions and. verifications for over 40,000 lines of computer code, supporting data files, and specialized Microsoft Excel spreadsheets. Provides training to TLG users and.to customers regarding process and capabilities of the cost model.

TLG Computer Support 1984 — Present

Lead technical specialist at TLG for supporting TLG employees in the day-to-day operations of Windows-based compLiter equipment. Local Area Network Administrator. Procures and implements computer hardware and software installation and upgrades for servers and workstations.

Nuclear Energy Services, inc. Waste Management Engineer 1979 - 1982

Provided technical expertise in the planning and engineering of nuclear facility decontamination and decommissioning. Developed methodologies and cost-benefit approaches to dismantle a nuclear facility while minimizing occupational expOSure and 'waste generation. Participated in

610

Francis W. Seymore EXHIBIT-FWS-1 Page 4 of 6

developing engineering criteria and recommendations for the design of a radioactive waste immobilization system slated for use at the Western New York Nuclear Service Center.

Participated in the engineering planning for decommissioning the Shippingport Atomic Power Station, where he was involved in- the development of activity specifications associated with the decontamination of the nuclear steam supply system end the dismantling of radioactive structures.

Project Engineer responsible for a technical assessment of the costs associated with decommissioning the Humboldt Bay Unit • 3 generating station: The assessment, involved in establishing of a methodology for dismantling the facility, necessitated supporting analyses such as detailed activation study to determine the radioactive inventory of the reactor vessel and surrounding structures.

Provided general staff support for various nuclear engineering projects, including the Nine Mile Point Unit 1 shielding design review, Cooper Nuclear Station high-density spent fuel rack. boron depletion, Humboldt Bay Unit 3 spent fuel rack criticality analysis, and the LaCrosse BWR off-site dose calculation manual

EXPERT TESTIMONY:

Regulatory supporrfor nuclear utilities on decommissioning funding in state and federal dockets. Preparation of expert testimony, briefs, rebuttal, and responses to discovery and witness cross.

Testified: September 2016, before the Califomia Public Utilities Comrnission, for Pacific Gas and Electric Company on the 2015 Nuclear Decommissioning Cost Triennial Proceeding, Application 16-03-006.

Testified: April 2016, before the State of Illinois Property Tax Appeal Board, regarding the 2012 AssessMent of Byron Nuclear Power Station, Docket Nos. 12-01248 & 12-02297

Testimony Filed: October 2015, before the New Mexico Public Regulation Commission on dismantling cost estimates for 27 fossil units in Texas and New Mexico. Case settled before hearing. Case No. 15-00296-UT

Testimony Filed: August 2015, before the Public Utilities Commission of Texas for El Paso Electric Company for the Palo Verde Nuclear Generating Station. Not called at hearing. PUC docket No. 44941

Testified: June 2015, before the Texas Public Utility Commission for Southwestern Public Service Company on dismantling cost estimates for 27 fossil units in Texas and New Mexico. PUCT docket No. 43695

Testimony Filed: February 2013, before the New Mexico Public Regulation Commission for Southwestern Public Service Company on dismantling cost estimates for 28 fossil units in Texas and New Mexico. Case settled before hearing. Case No. 12-00350-UT

Testimony Filed: November 2012, before the Texas Public Utility Commission for Southwestem Public Service Company on dismantling cost estimates for 28 fossil units in Texas- and New Mexico. ease settled before hearing. PUCT docket ,No. 40824

Deposition: February 2012, before the United States Court of Federal Claims for Amergen Energy Co. LLC on decommissioning cost eitimates for the Oyster Creek, Three Mile Island Unit 1, and Clinton Power Station units. Docket No. 09-108 T.

611

Francie W. Seynnore EXHIBIT FWS-1 Page 5 of 6

Testimony Filed: February 2012,, before. the Public Utilities Commission of Texas for El Paso Electric Company for the Palo Verde Nuclear Generating Station. Case settled before hearing. PUC docket No. 40094.

Testimony Filed: November 2011, before the Public Service Commission for the State of Colorado for Public Service.Company for 32 fossil units in Colorado. Case settled before hearing. PSC docket No. 11AL-947E.

Testimony Filed: August 2011, before the Kansas Corporation Commission for Westar Energy on dismantling cost estimates for seven fossil units in Kansas. Not called at hearing. KCC docket No. 12-WSEE-112-RTS.

Testimony Filed: April 2010 before the U.S. Tax Couft for Entergy Nuclear on the decommissioning costs for the Pilgrim Nuclear Power Station. Not called at the trial due to an agreement between the parties. Docket No. 10557-08.

Deposition: October 2008, before the Texas Public Utilities Commission for Southwestern Public Service Company on dirnantling cost estimates for 28 fossil units in Texas and New tvlexico. PUCT docket no. 35763.

Testified: May 2006, before the Califomia Public Utilities Commission, for Pacific Gas and Electric Company on the Nuclear Decommissioning Costs 2005 Triennial Proceedings, Application 05-11-009.

Deposition: March 2004, by the U.S. Department of Justice for Exelon Generation Company on decommissioning cost estimates and their relation to spent fuel disposition, Commonwealth Edison Company v. United States, Case No. 98-621C

Testified: January 1990, before the New York State Public Service Commission, for Rochester Gas & Electric Company, on the Robert E. Ginna Power Plant rate case, docket 89-E-166, 167 and 168.

Testified: December 1990, before the Alabama Public Service Commission, for Alabama Power Company on the Joseph M. Farley Nuclear Plant, docket U3295.

Testified: August 1989, before the North Carolina Utilities Commission, for Duke Power Company, Carolina Power & Light, and Virginia Power Company on -decommissioning costs and waste volumes for decommissioning the Catawba Nuclear Station and Brunswick Steam Electric Plant, docket E-100, Sub 56.

PUBLICATIONS:

"Impediments to Nuclear Decommissioning Due to the Presence of Spent Fuel On Site," with William A. Cloutier Jr., presented at the ASTM Las Vegas meeting, January 1990.

"Influence of Decommissioning on Radioactive Waste Stream", with J. Adler and W. Cloutier, presented at the 1988 ANS Topical Conference: Radiological Effects on the Environment Due to Electrical Generation, July 1988.

"Decommissioning of Commercial Power Reactors: Rationale, Impetus, Execution and Consequence," with William A. Cloutier Jr., presented ai the Low Level Waste Forum, January 1986.

AIF/NESP-036, "Guidelines for Producing Commercial Nuclear Power Plant Decommissioning Cost Estimates," with Thomas S. LaGuardia et al, May 1986.

612

Francis W. Sernore EXHIBIT-FWS-1 Page 6 of 6

PROFESSIONAL ORGANIZATIONS:

National Society of Professional Engineers Connecticut Society of Professional Engineers American Nuclear Society Association for the Advancement of Cost Engineering International

613

DOCKET NO. 46831

APPLICATION OF EL ?ASO ELECTRIC COMPANY TO CHANGE RATES

PUBLIC UTILITY COMMISSION OF TEXAS

DIRECT TESTIMONY

OF

CYNTHIA S. PRIETO

FOR

EL PASO ELECTRIC COMPANY

FEBRUARY 2017

614

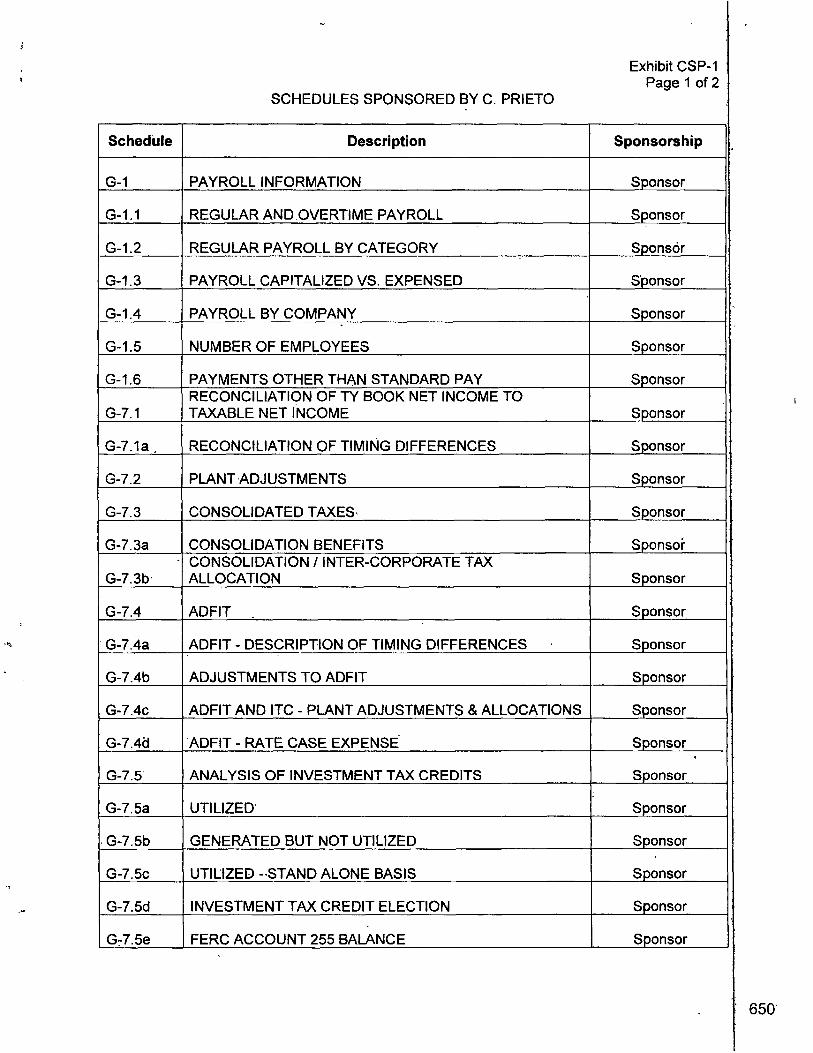

EXECUTIVE SUMMARY

Cynthia S. Prieto, Director of Tax for El Paso Electric Company (the. "Company" or

"EPE"), presents the payroll -and tax schedules and amounts included in the cost of service

and deferred tax amounts considered 'in the determination of rate base for the Company for

the historical Test Year. In her testimony,..she specifically discusses:

• Federal and State Income taxes included in'.Cost of Service

• Tax and Payroll Schedules provided in the Rate Filing Package (RFP"),

• Taxes Other Than Income

Federal and state income tax expense included in EPE's cost of service. has been

calculated using • the "return" method for the historical Test Year, as required by the

Instructions and Schedules, to the RFP. This refurn, method calculation reflects a

"stand-alõne" approach that includes in cost of service only federal and state income taxes

that result from the provision of utility service to customers. Ms., Prieto demonstrates that it

is neither appropriate nor equitable to increase or reduce cost of service by tax costs or

benefits that are not related to the rendition of utility service to custorners.

'Use of the return method also .satisfies the provisions ,of PURA § 36.060. In -the

Companys filing, requested tax expense is based solely on the income and expenses used

in determining the Companys revenue requirement and rate base. The Companys

stand-alone method ensures that customers benefit from the tax deductions that are

generated by the expenses included in cost olservice. This approach is reasonable and fair

for all parties.

Ms. Prieto demonstrates that the federal and state income tax schedules that are

part of the CompanY's filing are in compliance -with the prescribed RFP and are in

accordance with the Substantive Rules of the Public Utility Commission of Texas (pucr).

Adjustments made to tax expense, cost of sei-vice, and to rate base are both reasonable

and appropriate:

DIRECT TESTIMONY OF • CYNTHIA S. PRIETO.

61'5

Ms. Prieto also explains that the treatment of state deferred income taxes is iñ

compliance with the Final Order in PUCT Docket No. 44941.

In her discussion of "taxes other than income," Ms. Prieto discusses th.e Test Year

property tax amount and demonstrates that the remaining "revenue-related taxes,"

(e.g., local franchise fees, sales, ,use and gross receipts taxes and other miscellaneous

taxes plus state regulatory assessments) are reasonable and necessary.

in her discussion of payroll schedules Ms. Prieto describes the calculation of- the

salaries and wages and payroll taxes included in the revenue requirement including all

applicable proforma adjustments.

DIRECT TESTIMONY OF CYNTHIA S. PRIETO

616

TABLE OF CONTENTS

SUBJECT PAGE

I. INTRODUCTION AND QUALIFICATIONS 1

II. PURPOSE OF TESTIMONY 2

III. BACKGROUND-OF INCOME TAX ACCOUNTING AND RATEMAKING 3

IV. NORMALIZATION REQUIREMENit 8

V. FEDERAL INCOME TAXES 10

VI. STATE INCOME TAXES 14

VII. INCOME TAX SCHEDULES 16

VIII. TAXES OTHER' THAN INCOME 26

A. Property Taxes 26

B. Revenue-Related Taxes 28

IX. FAYROLL INFORMATION (G-1 SCHEDULES) 30

X. CONCLUSION 31

EXHIBITS

CSP-1 — Listing of Rate Filing Package Schedules Sponsored or Co-sponsored by Cynthia S. Prieto

DIRECT TESTIMONY OF CYNTHIA S. PRIETO

617

1 l. INTRODUCTION AND QUALIFICATIONS

2 Q. PLEASE STATE YOUR NAME AND BUSINESS ADDRESS.

3 A. IVly name is Cynthia S. Prieto. My business address is 100 North Stanton Street,

4 El_Paso, Texas 79901.

5

6 Q. BY WHOM ARE YOU EMPLOYED AND IN WHAT CAPACITY?

7 A. I am, employed by El Paso Electric Company ("EPE" or the "Company") as Director

8 of Tax.

9

10 Q. DESCRIBE BRIEFLY YOUR EDUCATIONAL BACKGROUND ANp

11 PROFESSIONAL EXPERIENCE.

12 A. I earned a Bachelor of Eusiness Administration Degree with a concentration in-

13 Accounting from the University of New Mexico in 1985. I was employed by Ernst &'

14 YoUng in the Audit section from 1985 to 1992 where I was assigned to various

15 clients, including various oil and gas companies. I was employed as an Audit Senior

16 Manager by KPMG LLP from, 1993 to 1996 where I was assigned to various clients:

17 I accepted a position with the Company in 2006 as a financial accountant where I

18 worked until I was transferred to the Tax department in 2007. Since that time, Lhave

19 held various positions until I was promoted to my current position in September.

20 2009.

21

22 Q. WHAT ARE YOUR PRINCIPAL AREAS OF RESPONSIBILITY?

23 A. I am responsible for preparing the federal and state income tax returns and

24 maintaining tax accounting data for the Company. This includes the preparation of

25 tax accounting and related tax data used 'in regulatory filings. I am also responsible

1 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

618

1 for the payroll department, which includes thepreparation of payroll and related tax

2 data used in regulatory filings.

3

4 Q. HAVE YOU PREVIOUSLY FILED TESTIMONY OR TESTIFIED BEFORE ANY

5 REGULATORY AUTHORITIES?

6 A. Yes. l-have filed testimony before the Public Utility Commission of Texas (pucr or

7 "Commission") and have filed testimony and testified before the New Mexico Public

8 Regulation Commission.

9

10 II. PURPOSE OF TESTIMONY

11 Q. WHAT IS THE PURPOSE OF YOUR TESTIMONY?

12 A. My direct testimony addresses a nurnber of topics. First, l support the Companys

13 federal and state income tax amounts found in the G-7 schedules of the Rate Filing

14 Package (RFP") and included in EPE's requested cost of service and rate base. My

15 testimony will also address the calculation of income tax expense on a stand-alone

16 basis and explains that the Cornpany began normalizing state income tax expense in

17 accordance with. the settlement agreement approved by the Commission in the

18 Company's last rate case, PUCT Docket No. 44941. V.also sponsor EPE's taxes

19 other Than income, referenced on the 0-9 schedules. Finally, my testimony supports

20 the Company's requested payroll expense reflected in the RFP's G-1 schedules.

21

22 Q. WHY ARE YOU THE APPROPRIATE-PERSON TO SPONSOR THESE TOPICS?

23 A. In thy role as Director of Tax, I have detailed knowledge, regarding the income tax

24 accounts used to determine income tax expense as well as the amounts included in,

25 current income taxes payable, unamortized investment tax credit, a"ccumulated

26 deferred income taxes, and ta.xes other than income paid by the Company. As

2 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

619

1 indicated earlier, I assumed responsibility for the Company's payroll department in

2 2016.

3

4 Q. WHAT TEST YEAR IS THE COMPANY USING IN THIS FILING?

5 A. This filing uses the 12 months énded September 30, 2016, as the Test Year.

6

7 Q. WHAT RFP SCHEDULES DO YOU SPONSOR OR CO-SPONSOR IN THIS

8 PROCEEDING?

9 A. Exhibit CSP-1 indicates the *schedules that I am sponsoring or co-sponsoring wi6

10 other witnesses.

11

12 Q. WERE THE SCHEDULES AND EXHIBITS YOU ARE SPONSORING OR CO-

13 SPONSORING PREPARED BY YOU OR UNDER YOUR DIRECT SUPERVISION?

14 A. Yes, they were.

15

16 Q. ON WHAT BASIS.WERE THE REFERENCED SCHEDULES PREPARED?'

17 A. The schedules were prepared using the books and records of the Company, and

18 they are accurate summaries of the business records upon which they are based.

19

20 III. BACKGROUND OF INCOME TAX ACCOUNTING AND RATEMAKING

21 Q. CAN YOU PLEASE DESCRIBE THE ACCOUNTING" FOR INCOME TAXES

22 REQUIRED UNDER GENERALLY ACCEPTED ACCOUNTING PRINCOLES

23 ("GAAP")?

24 A. Yes. Accounting for income taxes under GAAP is contained in the Accounting

25 .Standards Codification ("ASC") in section ASC 740 (formerly SFAS No. 109,

26' Accounting for Income Taxes ("SFAS 109)). There are several components to the

3 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

620

1 calculation: currently payable income taxes, deferred income taxes, and investment

2 tax credits.

3

4 Q. WHAT IS THE FIRST COMPONENT, CURRENTLY PAYABLE INCOME TAXES?

5 A. Currently, payable income tax expense represents the estimated amount of current

6 year income taxes payable based on current year taxable income. Taxable income

7 for -ihe year is determined in accordance with the Internal Revenue Code ("IRC").

8 For purposes of preparing an income tax return each year, the- IRC contains

9 procedures for determining if and when an item is "taxable-or "deductible."

10

11 Q. WHAT IS THE SECOND COMPONENT, DEFERRED INCOME TAXES?

12 A. The IRC rules for determining what is taxable or deductible rnay differ from what is

13 reportable as -"revenue" or "expense" under GAAP. For instance,. certain expenses

14 recorded on the financial statements under GAAP in.one year may be dedUctible on

15 the tax return in. a different period. There are also instances where the amounts

16 shown as deductions on the tax. return in one year are not reflected on the financial

17 statements until a later year. As a result; at the end of each reporting period, there

18 will likely be accumulated differences.of reported assets and liabilities resulting frorn,

19 different book and tax return treatment of revenues and expenses. These

20 differences are referred to as temporary differences.

21

22 Q. CAN YOU FURTHEI3 EXPLAIN WHAT IS MEANT BY THE TERM "TEMPORARY

23 DIFFERENCES" AND PROVIDE AN EXAMPLE?

24 A. Yes. One common temporary difference iš depreciation. For book purposes, GAAP

25 requires that the asset be depreciated over-its estimated useful life in a sSisternatic

26 and rational manner. As a result, straight-line depreciation. over the useful life- of

4 DIRECT TESTIMONY OF CYNTHIA'S. PRIETO

621

1 assets is used for book purposes. For income, tax purposes, the asset may be

2 depreciated using an accelerated depreciation method which is generally shorter

than the estimated useful life. Initially, tax depreciation will exceed book

4 depreciation. In the later years, the reverse will be true because given the same

5 capitalized asset cost, over the life of the asset total depreciation will be the same.

6

7 Q. WHAT IS THE ACCOUNTING FOR TEMPORARY DIFFERENCES UNDER

8 ASC 740?

9 A. Under GARP, because the financial statements reflect accrual and not cash basis

10 accounting, deferred income taxes are recorded on temporary. differences. As a

11 result, income tax expense under GAAP includes both a currentlji payable,

12 component (as previously described, based on the.tax return) as well as a "deferred"

13 income tax component (based on temporary differences). Such- deferred, income

14 taxes reflect the liability or asset forincome taxes payable or receivable in the future

15 stemming from transactions recorded in the financial statements currently. The

16 balance sheet liability or asset- for future taxes is referred to as Accumulated

17 i Deferred Income Tax ("ADIT'). In other words; to the extent that accelerated tax

18 depreciation iš claimed on the income tax return in an amount that exceeds book

19 depreciation reported on the financial statements, a liability for future taxes results.

20 This future tax liability is due to the fact that greater depreciation claimed in early

21 years will "use ur the tax basis of'assets and result in higher taxes in the future.

22 Under ASC 740, a calculation of required ADIT is performed at the end of

23 each reporting period. The required ADIT is measured by multiplying the temporary

24 differences by the currently applicable income tax rates. Comparing the ADIT at the

25 current balance sheet date to the ADIT at the previous balance sheet date results in

26 "deferred income tax expense." For regulated, entities, such as EPE, the process of

5 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

622

1

recording deferred income taxes on temporary differences is referred to as

2

"normalization," "deferred tax accounting," or "comprehensive interperiod income tax

3

allocation."

4

5 Q. DOES CLAIMING DEDUCTIONS FOR INCOME TAX PURPOSES IN EXCESS OF

6 EXPENSES RECORDED FOR BOOK .PURPOSES PROVIDE INCENTIVES TO

7 THE COMPANY THAT BENEFIT CUSTOMERS?

8 A. Yes. By claiming tax deductions for such things as accelerated depreciation, the

Company reduces its current income tax payments. But, with respect to temporary

10 differences, tax payments will be higher in the future when the temporary differences

11 reverse. As a result, ADIT balances are "interest free loans" from the U.S. Treasury.

12 This was the objective Congress intended when it included accelerated depreciation

13 provisions in the IRC. Congress believed that allowing companies to increase their tax

14 depreciation deductions (and thereby reduce curreni income tax payments), would

15 lower the financing costs of their investment ih capital assets and thus they would be

16 incented to make such expenditures. For accounting purposes, using up the tax basis

17 of capital assets is both a cost to be recognized in the- financial statements when

18 claimed (i.e., deferred tax expense) and a liability for future taxes due when the

19 turnaround occurs and book depreciation exceeds tax depreciation (i.e., ADIT).

20

21 Q. ARE ALL BOOK/TAX DIFFERENCES "TEMPORARY DIFFERENCES" AND

22 SIMPLY A MATTER OF WHEN THE ITEM IS INCLUDED ON THE TAX RETURN

23 VERSUS WHEN THE ITEM IS SHOWN ON THE FINANCIAL STATEMENTS?

24 A. No. Most differences between their treatment on the books and ihcome tax return

25 are simply. "temporary" and over time, the same amount will be included on the

26 financial statements and tax returns. However, certain items of revenue and

6 DIRECT TESTIMONY OF CYNTHIA-S. PRIETO

623

1 expense are, over time, treated differently for financial reporting purposes than for

2 incorne tax purposes. These are referred to as permanent differences.

3

Deferred income taxes are not required on permanent differences. In the

4

period reported, current income taxes will be adjusted to reflect the jncreased

5 deduction or non-deductibility of these costs and there will be no deferred income

6 taxes since these amounts will "never" be included in the financial statements or

7 deducted on the tax retum thereby permanently decreasing or increasing current tax

8 expense.

9

10 Q. IS THE DISTINCTION BETWEEN PERMANENT AND TEMPORARY

11 DIFFERENCES IMPORTANT IN THE INCOME TAX CALCULATION?

12 A. Yes. Permanent differences need to bd separately identified and included in the

13 income tax. calculation because they 'do not require deferred income tax accounting,

14 and permanently increase or decrease total income tax expense that needs to be

15 recovered in revenue requirements in a rate case.

16

17. Q. IS THERE ANOTHER COMPONENT OF THE INCOME TAX CALCULATION?

18 A. Yes. In addition to current and deferred income taxes, a third element of the tax

19 computation is the Investment Tax Credit ("ITC").

20

21 Q. CAN YOU PLEASE SUMMARIZE WHAT THE ITC IS AND HOW IT IS TREATED

22 FOR ACCOUNTING/RATEMAKING PURPOSES?

23 A. The ITC, which has gone in and out of existence over.the years, lowers income tax

24 expense permanently, if ceqain qualifying investments are made. It, is intended as

25 an incentive for companies to invest in qualifying assets. To make. sure that its

7 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

624

1 objectives are !net for regulated •utilities, the IRC prescribes methods of sharing the

2 benefit between customers and-shareholders.

3 The ITC is a direct reduction of incipme taxes payable in a given year. pnlike

4 accelerated depre9iation and other book/tax differences that will eventually reverse

5 or turn around, the ITC is comparable to a rebate. The ITC provides an incentive to

6 capital investment by granting a tax credit (a direct dollar-for-dollar• offset to current

7 taxes, payable) based on a percentage applied to investMent in tangible personal

property (most generation, transmission and distribution assets).

9 The accounting for the ITC is contained in ASC 740, codifying the accounting

10 for ITC -previously contained in Accounting Principles Board Opinions 2 and 4,

11 Accounting for the Investment Credit. Most utilities, like EPE, account for the ITC by

12 reducing current income taxes payable in the year the credit is earned for the full

13 amount of the credit but recognize an equal and offsetting amount of deferred tax

14 expense. The amount of the credit is then. amortized to reduce income tax expense

15 over the book life of the property giving rise to the ITC.

16 " In 1972, for ratemaking purposes, the IRS required utilities to elect how they

• 17 intended to share the ITC between customers and shareholders. Most utilities,

18 including EPE, elected to share the ITC as described in the preceding paragraph, by

19 including the annual amortization to income tax expense as a reduction to income tax

20 expense. In accordance with- this election, the unamortized ITC basis is not deducted

21 from rate base. Reduced income tax expense benefits customers when it is included in

22 . rates.

23

24 IV. NORMALIZATION REQUIREMENtS

25 .Q. WHAT IS THE FEDERAL ENERGY REGULATOIRY COMMISSION'S (FERC")

26 POSITION ON DEFERRED INCOME TAXES?

8 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

625

-1 A. The FERC Uniform System of Accounts embraces "normalization" of deferred

income taxes by requiring comprehensive interperiod income tax allocation for all

3 book/tax timing/temporary differences. FERC Order Nos. 144 and 144A provide

4 guidance in this area. This has been the FERC methodology since the early 1980s.

5

6 Q. IS NORMALIZATION ACCOUNTING REQUIRED. FOR A UTILITY TO REFLECT

7 CERTAIN DEDUCTIONS AND CREDITS ON ITS FEDERAL TAX RETURN?

8 A. Yes. The IRC requires that regulated utilities rnust use the normalization method,

9 and not the flow-through method, to calculite the tax expense related to

10 depreciation-related temporary differences (IRC Section 168), Contributions In Aid of

11 Construction (IRS Notice 87-82), investment tax credits, excess deferred taxes, and

12 net operating losses (NOLus) created by accelerated depreciation in orderto avoid

13 certain penalties.

14

15 Q. IN THE PREVIOUS QUESTION, YOU MENTIONED THAT NOLS CREATED BY

16 ACCELERATED DEPRECIATION WERE REQUIRED TO BE NORMALIZED. IS

17 EPE IN A NOL CARRYFORWARD POSITION?

18 A. Yes. EPE is currently in a. NOL carlyforward position. EPE's NOL was created in

19 tax year 2015 and the Test Year from tax deductions which exceeded taxable

20 income. These deductions "arose from temporary differences related to accelerated

21 tax depreciation allowed by the extension of bonus depreciation in the Protecting

22 Americans from ,Tax Hikes Act of 2015 (PATH Acr), whiCh was signed into law

23 December 2015 and applicable retroactively to January 1, 2015.

24

25 Q. HAS EPE INCLUDED A NOL CARRYFORWARD ADIT ASSET IN RATE BASE IN

26 THE TEST YEAR?

9 DIRECT TESTIMONY OF CYNTHIA S. PRIÈTO

'626

1 A. Yes, it has,, consistent with IRS normalization requirements. When a company has

negative current taxable income, it cannot realize the cash benefit of all of its

3 deductions, because it cannot reduce its tax payments below zero. The NdLs must

4 be.deferred and carried forward to be used against taxable income in future periods,

5 subject to certain limitations. Only then will the taxpayer receive the cash tax benefit

6 of these NOLs. When carried forward, the NOL is'a temporary difference for which

7 an ADIT asset must be recorded. The net of the ADIT liability created by the bonus

8 •depreciation and the AD1T asset created by the NOL carryforward represents the

9 cash tax benefits that were actually received by the Company.

10

11- Q. WHAT IS THE PENALTY FOR VIOLATING THE IRS• NORMALIZATION

12 REQUIREMENT REGARDING NOLS?

13 A. The NOL normalization rules are a subset of the depreciation normalization rules,

14 therefore, a violation of the NOL normalization requirement would result in the loss of

15 the ability to ,u,se accelerated tax depreciation on all public utility property. held by the

16 utility.

17

18 V. FEDERAL INCOME TAXES

19 Q. 'HOW HAVE FEDERAL INCOME TAXES INCLUDED IN COST OF SERVICE BEEN

20 CALCULATED?

21, A. Federal income taxes have been calculated using the "return" method for the

22 historical year, as required by the Instructions and Schedules to the RFP.

23

24 Q. WHAT IS THE "RETURN" METHOD?

25 A. The calculation of federal income takes provided on Schedule G-7.8 is comrnonly

26 referred to as the "return" method because it calculates federal income taxes using

' 10 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

627

after-tax return as the starting point. Under this method, equity retum, or total retum

2

less interest, is adjusted for items for which there is no tax deduction to offset

3

amounts recovered through revenues — such as book amortization of Allowance kr

4

Funds Used During Construction ("AFUDC") equity, "flow-through differences,"

5

permanent differences, ITC amortization, and the amortization of excess ADIT. The

6

"return" method calculates federal income tax expense in total, with no segregation

7

between current and deferred federal income taxes. The return method tax

8

calculation provided on Schedule G-7.8 reflects a stand-alone approach to

9

cglculating federal income taxes.

10

11 Q. WHAT IS THE BASIS FOR' THE PERMANENT DIFFERENCES INCLUDED IN THE

12. RETURN METHOD?

13 A. Permanent differences can arise when costs are reported as expenses in the

14 financial statements but will never be deductible on the income tax return. In

15 addition, permanent differences can also arise when deductions are allowed on the

16 income tax return that will never be reported as expenses in the financial statements.

17 Examples of permanent differences in EPE's tax Calculation are the cost of meals

18 and entertainnient and the domesti6 próduction'activities- deduction (DPAD"). The-

19 cost of meals and entertainment are reported as expenses in the financial

20 s-tatements but, under the IRC, are not completely deductible on the income tax

21 return and is therefore a permanent difference which increases current tax expense.

22 The ,DPAD is a deduction allowed by the IRC for domestic manufacturing activities

23 but is limited by several factors including taxable income. This deduction will never

24 be an expense in the GAAP financial statements and is therefore a perManent

25 difference which decreases current tax expense.

26

11 DIRECT TESTIMONY OF CYNTHIA S. PRIETO-

628

1 Q. WHAT IS MEANT BY A "STAND-ALONE" APPROACH?

2 A. The ."stand-alone" methodology calculates federal income taxes on utility revenues

3 and expenses that are included in the utility's revenue requirement. This approach

4 appropriately allocates federal income taxes between customers and shareholders

5 using the benefits/burdens criteria outlined by FERC Opinion No. 173. Under this

6 methodology, federal income tax expense relates to, and results from, the provision

7 of utility service to customers. Additionally, the "stand-alone federal income tax

8 calculation includes an adjustment -to synchronize interest. Synchronized interest

9 represents the portion of return that is deductible for -tax purposes and ie calculated

10 by multiplying'the weighted cost of debt by rate 'base. Use of synchronized interest

11 in the tax calculation effectively "synchronizes" the calculation of federal income tax

12 expense with rate base and' rate of return. Synchronized interest may be more or

13 less than the actual interest deducted on the tax return.

14

15 Q. WHY IS THE "STAND-ALONE" APPROACH THE PROPER METHODOLOGY TO USE

16 IN CALCULATING FEDERAL INCOMETAXES,FOR RATEMAKING PURPOSES?

17 A. The "stand-alone approach; required by Section 36.060 of the Public Utility

18 Regulatory Act ("PURA") as amended, in 2013, includes in cost of service only

19 federal income- taxes that result from the provision of utility service to customers.

20 Federal income taxes requested by the Company are based on revenues and

21 expenses included in the cost of service calculation. There are no additions to or

22 reductions from tax expense resulting from revenues or expenses notincluded in the

23 Company's request.' It is rieither appropriate nor equitable to increase or reduce cost

24 of service by tax costs or benefits that are not related to the rendition of utility service

25 to customers.

12 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

629

1 Said another way, income taxes have no independentexistence of their own.

2 They are based on revenues and expenses. Once the Commission decides on the

3 appropriate reVenues and expenses that are necessary for the provision of electric

4 service, the related income taxes can be determined.

5

6 Q. WHAT IS THE AMOUNT OF FEDERAL INCOME TAX EXPENSE THE COMPANY

7 'IS REQUESTING TO BE INCLUDED IN RATES?

8 A. The Company is requesting the amount of federal income tax expense that is

9 included in cost of service reflected on Schedule G-7.8.

10

11 Q HAS THE COMPANY COMPUTED FEDERAL INCOME TAXES IN ACCORDANCE

12 WITH SECTIONS 36.059 AND 36.060 OF PURA?

13 A. Yes. PURA Sections 36.059 'and 36.060 address the treatment of certain tax

14 benefits; including ITC and consolidated tax savings. PURA Sections 36.059(b) and

15 36.060(c) specifically require a utility .that retains ITC to deduct it from the rate base

16 to which tlie credit applied, to the extent allowed by the IRC. The post-1970 portion

17 of unamortized ITC is not included as a r.eduction of rate base because. the Company.

18 is an "Option 2" company for ITC purposes. Under IRC Section 46(f), an "Option 2"

19 election requires that the post-1970 ITC be returned to customers as a reduction of

20 cost-of-service, rather than as a reduction of rate base.

21 Additionally, PURA Section 36.060(b) requires that income taxes related to

22 intercompany profits on affiliated purchases be applied tb reduce 'the cost of the

23 property or service purchased., The Comioany had no affiliates or subsidiaries for the

24 Test Year ended September 30, 2016, or during the Test Year. As a result, tax

25 expense included in this filing has been, calculated in accordance with PURA

26 Section 36.060(b).

13 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

630

1

Further, PURA SeOtion 36.060(a) requires that income tax expense included

2

in cost of service reflect only expenses and investments- included in cost of service

3

and rate base. The Companys income tax amounts included in cost of service are

consistent with this provision.

5

6 VI. STATE INCOME TAXES

7 Q. WHAT IS THE AMOUNT OF STATE INCOME TAX EXPENSE THE COMPANY IS

8 REQUESTING TO BE INCLUDED IN RATES?

9 A. The Company is requesting the amount of state income tax expense that is included

10 in cost of service reflected on Schedule G-7.8.

11

12 Q. WHICH ACCOUNTING METHOD HAS EPE USED TO DETERMINE STATE

13 INCOME TAX EXPENSE IN THIS CASE?

14 A. Pursuant to the settlement agreement that was approved by the Commission Final

15 Order in the Company's last rate case, PUCT Docket No. 44941, the Company has

16 used the normalization method to determine the state income tax expense included

17 in cost of service.

18

19 Q. WHAt DID THE SETTLEMENT IN PUCT DOCKET NO. 44941 PROVIDE WITH

20 RESPECT TO STATE INCOME TAX EXPENSE?

21 A. Prior to, PUCT Docket No. 44941, the Company used the flow through method to

22 calculate state income tax' expense: However, in- PUCT Docket No. 44941, the

23 Company requested to switch to the normalization method. The settlement

24 approved in the case authorized the change in methodologies. Article I. Section F. of

25 the Settlement Agreement stated:

14 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

631.

1

Beginning January 1, 2016, EPE should begin normalizing state income tax

2

expense. In other words, it should begin including both current and deferred

3

state income tax expenše in its revenue requirement (just as it- does for

4

federal incõme tax expense) instead of just the current portion of state

5

income tax expense. On that date, it should also begin amortizing the test

6

year-end balance of accumulated deferred state income tax expense that has

7

not yet been included in cost of service over a 15-year period.

8

This provision was. adopted in Findings of Fabt Nos. 40 and 60 in the Final Order

9 issued in PUCT Docket No. 44941.

10

11 Q. HAS THE COMPANY COMPLIED WITH THIS PROVISION?

12 A. Yes, it has. In August ,2016, after the Final Order was issued in PUCT Docket

13 No. 44941, the Company began normalizing state income tax expense and recorded

14 adjustments to make the change retroactive to January 1, 20161. In this filing it has

15 included both ci.Frent and deferred state income tax,expense in its state income tax

16 expense request. Further, the Company also began amortizing its balance of

1T accumulated deferred state income tax expense• that has not yet been included in

18 cost of service over a 15-year period.

19

20 Q. WHAT IS THE AMOUNT OF STATE INCOME TAX EXPENSE THE COMPANY IS

21 REQUESTING BE INCLUDED IN ITS COST OF SERVICE?

22 A. State income tax expense is shown on pages 3 to 5 of Schedule G-7.8. The annual

23 amortization of the January 1, 2016 balance of accumulated deferred state income

24 tax not yet included in cost of service is calculated on Schedule G-7.9(a), line 59,

Although the Final Order in PUCT DoCket No. 44941 was issued August 25, 2016, the Company's accounting treatment was"retroactive to January 1, 2016.

15 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

632

1 column (c) and included in incorrie tax expense on Schedule G-7.8, page 1, line 17,

2 column (c).

3

4 \ill. INCOME TAX SCHEDULES

5 Q. PLEASE DESCRIBE SCHEDULE G-7.1, RECONCILIATION OF TEST YEAR BOOK

6 NET INCOME TO TAXABLE NET INCOME.

7 A. Schedule G-7.1 is the reconciliation .of book net income to taxable net income on a

8 total company basis for the Test Year and for the most recently filed federal' income

9 tax return. Schedule G-7.1 contains explanations of all iterns in the reconciliation for

10 both the Test Year and the ta-x return.

11

12 Q: PLEASE ,DESCRIBE SCHEDULE G-7.1(a), RECONCILIATION OF TIMING

13 DIFFERENCES.

14 A. This schedule includes a listing of timing differences and other items that produce

15 federal income tax for the Test Year at a tax rate different than the statutory 35% tax

16 rate, with explanations describing each item.

17

18 Q. PLEASE DESCRIBE SCHEDULE G-7.2, PLANT ADJUSTMENTS.

19 A. This schedule provides the tax.basis, tax in-service date, tax depreciation rnethods,

20 and tax depreciation in the Test Year and projected for the two subsequent years,

21 and the amount of ADFIT as of the Test Year-end for any new generating unit

22 requested (purchased or constructed since the Companys last rate case) and any

23 requested plant adjustments to the Test Year.

24

16 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

633

1 Q. PLEASE.DESCRIBE SCHEDULE G-7.3, CONSOLIDATED TAXES.

2 A. This schedule is not applicable. The Company, did not have any subsidiaries in the

3 Test Year ended September 30, 2016 or during the Test. Year.

4

5 Q. PLEASE DESCRIBE SCHEDULE G-7.3(a), CONSOLIDATION BENEFITS.

6 A. This schedule is not applicable. The Company did not have any subsidiaries in the

7 Test Year ended September 30, 2016.

8

9 Q. IS THE COMPANY A MEMBER OF A CONSOLIDATED GROUP OR DOES THE.

10 COMPANY HAVE ANY SUBSIDIARIES?

11 A. No. The Company did not have any subsidiaries in the Test Year, and it is not part

12 of a consolidated group.

13

14 Q. PLEASE DESCRIBE SCHEDULE G-7.3(b), CONSOLIDATION/INTER-CORPORATE

15 TAX ALLOCATION.

16 A. This schedule is not applicable to the Company. The Company-did not have an9

17 subsidiaries in the Test Year ended September 30, 2016.

18

19, Q. PLEASE DESCRIBE SCHEDULE G-7.4, ADFIT.

20 A. This schedule shows the balance sheet amourit of ADIT for each of the twelve

21 months of the• Test Year; at the end of the Test Year; and the additions and

22 reductions during the Test Year as well as the requested adjustments to the

23 balances. Each item that gives rise to ADIT is shown separately on this schedule.

24

25 Q. PLEASE DESCRIBE StHEDULE G-7.4(a), ADFIT-DESCRIPTION OF TIMING

26 DIFFERENCES.

17 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

634

A. This schedule includes a description of the nature and remaining life, where

2 applicable, of each timing difference listed in Schedule G-7.4.

3.

4 Q. PLEASE DESCRIBE'SCHEDULEG-7.4(b), ADJUSTMENTS TO ADFIT.

5 A. This schedule shows the details of the adjustments to the balance sheet ADIT

6 accounts. The reasons for these adjustments are included as well as the supporting

7 calculations, if any.

8

9 Q. DOES THIS SCHEDULE REFLECT THE IMPACTS OF BONUS DEPRECIATION?

10 A. Yes. The Company can and has claimed bonus depreciation as permitted by the

11 IRC. Depending on the year certain capital assets were placed in service, the

12 additions are eligible 'for 50 percent or 100 percent bonus depreciation. This

13 effectively means that for income tax purposes; in addition to tax depreciation

14 computed using the Modified Accelerated Cost Recovery System ("MACRS"), the

15 Company can claim an additional 50 percent or 100 percent of the eligible tax basis

16 as a tax depreciation deduction in the first year. As a result, EPEs Test Year end

17 ADIT related to these book/tax depreciation temporary differences has increased to

18 reflect the future tax liability associated with these accelerated deductions.

19

20 Q. DID THE COMPANY REMOVE TEST YEAR END ADIT FOR AMOUNTS RELATED

21 TO UNCERTAIN TAX POSITIONS REQUIRED TO BE IDENTIFIED AND

22 ACCOUNTED FOR BY FINANCIAL ACCOUNTING STANDARDS BOARD

23 INTERPRETATION 48 ("FIN 48")?

24 A. NO reductions were made'to Test Year end ADIT in rate base for FIN 48 reserves.

25

18 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

635

1 Q. PLEASE DESCRIBE SCHEDULE G-7.4(c), ADFIT AND ITC — PLANT

2 ADJUSTMENTS AND ALLOCATIONS.

3 A. This schedule provides the accumulated deferred income tax balances at Test Year

4 end related to additions to new generating plant in service since the Company's last

filing and any plant adjustments to the Test Year end requested by the Company and

6 the supporting calculations.

7

8 Q. PLEASE DESCRIBE SCHEDULE G7.4(d), ADFIT-RATE CASE EXPENSE.

9 A. This schedule is not applicable. The Company does not have any ADIT assóciated

10 with rate case expense reflected on the books at September 30, 2016.

11-

12 Q. PLEASE DESCRIBE SCHEDULE G-7.5; ANALYSIS OF ITCS.

13 A. This sthedule presents the analysis of the ITC adjustment for Deferred Investment

14 Tax Credit (DITC") to be included in cost of service. The Company's election under

15 Section 46(f)(2) of the IRC does not permit amortization of ITC to reduce income tax

16 expense in cost of service at a rate more rapidly than ratably — no faster than over

17 the book life-of the assets that generated the ITC. The "stripped" book depreciation

18 rate requested is derived from the book depreciation calculation reflecting , the life

19 extension of the Palo Verde Nuclear Generating Station ("PVNGS") unit where

20 applicable. This rate represents the life or investrnent portion of the book

21 depreciation rate without regard to amounts for cost of removal or salvage. The

22 stripped depreciation rate is multiplied by the ITC amortization base to calculate the

23 annual amount of DITC amortization included in cost of service. The stripped

24 depreciation rate is used in this computation to avoid a potential normalization

25 violation that could result if the ITCs were amortized in cost of service at a rate more

26' rapid than ratably. Workpaper G-7.5 shows the calculation of the Test Year ITC. For

19 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

636

1

3

4

each class of assets generating the ITC, the Company applied the stripped

depreciation rate to the ITC amortization base to arrive at the ITC amortization used

to reduce income tax expense.

5 Q. PLEASE pESCRIBE SCHEDULE G-7.5(a), UTILIZED.

A. This schedule shows the ITC utilized (claimed on the income tax return) each year.

7

8 Q. PLEASE DESCRIBE SCHEDULE G-7.5(b), GENERATED BUT NOT UTILIZED.

9 A. This schedule presents the ITC generated but not utilized at the Test Year end

10 September 30, 2016. This schedule is not applicable to the Company. All

11 investment credits that were generated prior to September 30, 2016 have been

12 utilized by EPE.

13

14 Q. PLEASE DESCRIBE SCHEDULE G-7.5(c), UTILIZED — STAND-ALONE BASIS.

15. A. This schedule is not applicable to the Company. All investment credits have been

16 utilized by EPE.

17

18 Q. PLEASE DESCRIBE SCHEDULE G-7.5(d), ITC ELECTION.

19 A. This schedule describes the tax elections made by EPE with regard to ITC.

20

21 Q. PLEASE DESCRIBE SCHEDULE G-7.5(e), FERC ACCOUNT 255 BALANCE.

22 A. This schedule shows the account balance for FERC Account No. 255 — Accumulated

23 Deferred Investment Tax Credits as of September 30, 2016.

24

25 Q. PLEASE DESCRIBE SCHEDULE G-7.6, ANALYSIS OF TEST YEAR FIT AND

26 REQUESTED EIT — TAX METHOD 2.

20 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

637

1 A. This schedule calculates federal and state income tax expense for the Test Year

2 using Tax Method 2. This method of calculating federal and state jncome tax

3 expense determines the current and deferred components of tax expense

4 separately. The components of tax expense shown on this schedule include taxes

5 currently payable, deferred taxes, and D1TC amoriizkion. The Tax Method 2

6 calculation is equal to the amount of tax expense computed under the return method

7 (see Schedule G-7.8).

9 Q. PLEASE DESCRIBE SCHEDULE G-7.6(a), ANALYSIS OF DEFERRED FIT.

10 A. This schedule is an analysis of each deferred tax item that makes up the federal

11 deferred tax expense,in Schedule G-7.6.

12

13 Q. PLEASE DESCRIBE SCHEDULE G-7.7, ANALYSIS OF ADDITIONAL

14. DEPRECIATION REQUESTED.

15 A. This schedule provides the detail stipport for the requested adjustment to return for

16 additional depre,ciation. This schedule summarizes the major components related to

17 flow-through book depreciation for which there is no tax benefit. Workpaper G-7.7

18 provides the detail calculations for this schedule.

19

20 Q. PLEASE DESCRIBE SCHEDULE G-7.8, ANALYSIS OF TEST YEAR FIT &

21 REQUESTED FIT — TAX METHOD 1.

22 A. This schedule calculates federal and state income tax expense for the Test Year

23 using Tax Method 1, corniputed under the return method. The Tax Method 1

24 calculation is equal to the amourit of tax expense computed under Tax Method -2

25 (see Schedule G-7:6).

26

21 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

638

1 Q. DID THE COMPANY REFLECT AN ADJUSTMENT TO ITS TEST YEAR DPAD

2 AMOUNT ON SCHEDULE G-7.8?

3 A. Yes. Although the DPAD is generally a deduction for income tax purposes, the

4 federal income tax calculation for the Test Year has an adpition of $4 million related

5 to the DPAD on Schedule G-7.8, line 8, column (b). This situation arose due to the

6 enactment of the PATH Act in December 2015. In the third quarter of 2015, the

7 Company was projecting taxable income for 2015 and therefore was eligible- to

8 deduct the DPAD. Based on the projection of taxable income, the Company

9 recorded a deduction of $4 million for the DPAD in its tax accrual in the third quarter

10 of 2015. However, when the PATH Act was enacted in December 2015,. additional

11 tax depreciation. deductions for bonus depreciation resulted in a net operating loss

12 'for the Company for the tax year 2015. Because the Company did not have taxable

13 income, it was no longer eligible for the DPAD and reversed this 'deduction in the

14 December 2015 tax accrual. The tax accrual for the Test Year includes the fourth

15 quarter of 2015 and therefore includes the reversal of the DPAD in the amolint of

16 $4 million. The Companys requested income .tax calculation does not include a

17 reversal or deduction for the'DPAD because the requested dncome tax calculation

18 results in a net operating loss for the rate year and threfore the Company is not

19 eligible for the DPAD. As explained earlier, the net operating loss was due to tax

20 depreciation deductions from bonus depreciation.

21

22 Q. PLEASE DESCRIBE SCHEDUCE G-7.9, AMORTIZATION OF 11.'ROTECTED AND'

23 UNPROTECTED EXCESS DEFERRED TAXES..

24 A. This schedule summarizes the amortization of protected and unprotected excess

25 deferred federal income tax and the amortization methodology utilized.. Taxes that

26 relate to timing differences that are in excess of the statutory tax rate of 35 percent

22 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

639

1

are referred to as "excess deferred tax6s." These "excess deferred taxes" are

2

further categorized as "protected" or "unprotected." Protected excess deferred taxes

3

refer to specific rate treatments in the IRC that dictate how these amounts of excess

4

deferred taxes should 'reverse. Violation of the rate treatment specified by the IRC is

5

a nórmalization violation which, as described previously, results in the loss of

6

favorable income tax treatment of certain tax deductions (such as accelerated

7

depreciation), requiring the payment of higher current federal income taxes than

8

would have been paid if the proper rate treatment were followed. Unprotected

9

excess deferred taxes have no such rate treatment required in the IRC.

10

11 Q. PLEASE DESCRIBE SCHEDULE G-7.9(a), ANALYSIS OF EXCESS DEFERRED

12 TAXES BY TIMING DIFFERENCE.

13 A. This schedule shows the details of the information contained in Schedule G-7.9 by

14 timing difference. Workpaper G-7.9(a) includes the remaining excess deferred tax

15 balance at the end of the Test Year and the requested amortization for each item.

16 This schedule includes the calculation of the amortization of the excess deferred

.17 taxes that arose from the change to the normalization method for state income taxes

18 at January 1, 2016 that was described previously.

19

20 Q. PLEASE DESCRIBE SCHEDULE G-7.9(b), RECONCILIATION OF EXCESS.

21 A. This schedule provides the unamortized excess deferred tax balances at the Test

22 Year end September 30,. 2016, and a reconciliation, by timing difference, to the

23 unamortized excess tax balances ,at March 31, 2015, that were filed with the

24 Commission in Docket No. 44941.

25

23 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

640

1 Q. PLEASE DESCRIBE SCHEDULE G-7.9(c), ANALYSIS OF RESERVE

2 ACCOUNTING FOR EXCESS DEFERRED TAXES.

3 A. This schedule is, not applicable to the Company. The Company was not required by

4 prior Commission order to establish reserve accounting for excess deferred taxes.

5

6 Q. PLEASE DESCRIBE SCHEDULE G-7.10, EFFECTS OF ACCOUNTING ORDER

7 DEFERRALS.

8 A. This schedule is not applicable. The Company does not have any ADIT or fedèral

9 income tax as 9f September 30, 2016, relate'd to accounting order deferrals.

10

11 Q. PLEASE DESCRIBE SCHEDULE G-7.11,, EFFECTS OF POST-TEST YEAR

12 ADJUSTMENT.

13 A. This schedule is not applicable. The Companys request does not include post-test

14 year adjustments to plant.

15

16 Q. PLEASE DESCRIBE SCHEDULE G-7.12, EFFECT.S OF RATE MODERATION

17 PLAN.

18 A. The Company does not have an existing rate moderation plan and is not requesting

19 a rate moderation plan. Rate moderation plans adopted in the past have no effect on

20 federal income tax and ADIT.

21

22 Q. PLEASE DESCRIBE SCHEDULE G-7.12(a), TREATMENT pF FIT AND ADFIT IN

23 RATE MODERATION PLAN.

24 The.Company does not have an existing rate moderation plan and all federal income

25' tax and ADIT from previous rate moderation plans have been fully amortized.

26

24 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

641

1 Q. PLEASE DESCRIBE SCHEDULE G-7.13, LIST OF FIT TESTIMONY.

2 A. This schedule lists all witnesses that are filing testimony in this case that support the

3 Company's federal income tax and ADIT requests. The most 'recent tax return filed

(for the year 2015) is included as part of the. cqnfidential workpapers for this

5 schedule.

6

Q. PLEASE DESCRIBE SCHEDULE G-7.13(a), HISTORY OF TAX NORMALIZATION.

8 A. This schedule details the history • of tax normalization for the Company and also

9 provides details of the first year for each timing difference and the first year normalized.

10

11 Q. PLEASE DESCRIBE SCHEDULE G-7.13(b), TAX ELECTIONS.

12 A. Tax elections made by the Company since the Test Year end reflected in the last

13 rate filing, Docket No. 44941, are detailed' in this schedule.

•14

15 Q. PLEASE DESCRIBE THE CHANGES IN ACCOUNTING FOR DEFERRED TAXES•

16 SHOWN ON SCHEDULE G-7.13(c)?

17 A. There have been no changes, in accounting for federal deferred income taxes. •As

18 previously discussed, the Company has included deferred state income taxes in cost

19 of service and has proposed recovery of the prior accumulated state ADIT usinT a

20 South deorgia methodology.

21

22 Q. PLEASE DESCRIBE SCHEDULE G-7.13(d), IRS'AUDIT.STATUS.

23 A. This schedule explains the Companyš current federal income tax audit status. For

24 tax years 2016 and 2017, the Company is participating in the IRS Compliance

25 Assurance Process ('CAP) Program. As described in this Schedule, the CAP is a

26 method of resolving tax issues between the taxpayer and the IRS through open and

25 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

, 642

1 transparent interactions and communications to resolve issues prior to the filing of

2 tax returns.

3

4 Q. SCHEDULE G=7.13(e) RELATES TO PRIVATE LETTER RULINGS SINCE THE

5. LAST RATE FILING. HAVE, THERE BEEN ANY PRIVATE LETTER RULINGS

6 RECEIVED SINCE THE LAST RATE FILING THAT AFFECT THE FEDERAL

7 INCOME TAX OF THE COMPANY?

8 A. There have been no private letter rulings received by the Company since the last

9 rate filing..

10

11 Q. PLEASE DESCRIBE SCHEDULE G-7.13(f),, METHOD OF ACCOUNTING- FOR

12 ADFIT RELATED TO NOL CARRYFORWARD.

13 A. This schedule describes the method of accounting for the Company's NOL

14 Carryforwards and the balances included in ADIT at the Test Year end

15 September 30, 2016.

16

17 VIII. TAXES OTHER THAN INCOME

18 Q-. WHAT IS THE PURPOSE OF THIS SECTION OF YOUR TESTIMONY?

19 A. In this section of my testimony, I first discuss the Companys property taxes. I then

20 discuss the remaining taxes other than income that the Company incurs.

21

22 A. Property Taxes

23 Q. WHAT-WAS THE TOTAL AMOUNT OF PROPERTY TAXES DURING THE TEST

24 YEAR?

25 A. The total• amount of property, taxes for the Company in the Test Year is shown on

26 ScheclUle G-9, column' (e), lines 1 to 3.

26 DIRECT TESTIMONY OF CYNTHIA S. PRIETO

643

1 Q WHAT IS THE NET REQUESTED RECOVERY AMOUNT FOR THE COMPANY'S,

2 • PROPERTY TAXES?

3 A. The total amount of requested property taxes can be found on Schedule G-9,

4 column (g), lines 1 to 3.

5

6 Q. • HOW ARE THE PROPERTY TAXES FOk THE COMPANY DETERMINED?

7 A. The property taxes charged to the Company' are the amounts imposed by taxing

8 authorities. to which the Company is. subject. Property taxes are capitalized to

9 construction work in proce 'Ss for assets currently under construction based on an

'10 assessed value, or are expensed for assets placed in service.

11

12 Q. PLEASE DESCRIBE THE VARIOUS TAXING AUTHORITIES , THAT LEVY

13 PROPERTY TAXES AGAINST THE COMPANY'S PROPERTY.

14 A. The Company is subject to property taxation by many different taxing jurisdictions.

15 These taxing jurisdictions include, but are not limited to, counties, cities, independent*