fourth quarter 2016 investor presentation - enable...

TRANSCRIPT

Enable Midstream Partners, LP

Fourth Quarter 2016 Investor Presentation

Non-GAAP Financial MeasuresThe Partnership has included the non-GAAP financial measures gross margin, Adjusted EBITDA, Adjusted interest expense,

distributable cash flow and distribution coverage ratio in this presentation based on information in its condensed consolidated

financial statements.

Gross margin, Adjusted EBITDA, Adjusted interest expense, distributable cash flow and distribution coverage ratio are

supplemental financial measures that management and external users of the Partnership’s financial statements, such as industry

analysts, investors, lenders and rating agencies may use, to assess:

• The Partnership’s operating performance as compared to those of other publicly traded partnerships in the midstream energy

industry, without regard to capital structure or historical cost basis;

• The ability of the Partnership’s assets to generate sufficient cash flow to make distributions to its partners;

• The Partnership’s ability to incur and service debt and fund capital expenditures; and

• The viability of acquisitions and other capital expenditure projects and the returns on investment of various investment

opportunities.

This presentation includes a reconciliation of gross margin to total revenues, Adjusted EBITDA and distributable cash flow to net

income attributable to limited partners, Adjusted EBITDA to net cash provided by operating activities and Adjusted interest expense

to interest expense, the most directly comparable GAAP financial measures, as applicable, for each of the periods indicated.

Distribution coverage ratio is a financial performance measure used by management to reflect the relationship between the

Partnership's financial operating performance and cash distributions. The Partnership believes that the presentation of gross

margin, Adjusted EBITDA, Adjusted interest expense, distributable cash flow and distribution coverage ratio provides information

useful to investors in assessing its financial condition and results of operations. Gross margin, Adjusted EBITDA, Adjusted interest

expense, distributable cash flow and distribution coverage ratio should not be considered as alternatives to net income, operating

income, revenue, cash flow from operating activities, interest expense or any other measure of financial performance or liquidity

presented in accordance with GAAP. Gross margin, Adjusted EBITDA, Adjusted interest expense, distributable cash flow and

distribution coverage ratio have important limitations as analytical tools because they exclude some but not all items that affect the

most directly comparable GAAP measures. Additionally, because gross margin, Adjusted EBITDA, Adjusted interest expense,

distributable cash flow and distribution coverage ratio may be defined differently by other companies in the Partnership’s industry,

its definitions of gross margin, Adjusted EBITDA, Adjusted interest expense, distributable cash flow and distribution coverage ratio

may not be comparable to similarly titled measures of other companies, thereby diminishing their utility.

2

Forward-looking Statements

This presentation and the oral statements made in connection herewith may contain “forward-looking statements” within

the meaning of the securities laws. All statements, other than statements of historical fact, regarding Enable Midstream

Partners’ (“Enable”) strategy, future operations, financial position, estimated revenues, projected costs, prospects, plans

and objectives of management are forward-looking statements. These statements often include the words “could,”

“believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” “forecast” and similar expressions and are intended to

identify forward-looking statements, although not all forward-looking statements contain such identifying words. These

forward-looking statements are based on Enable’s current expectations and assumptions about future events and are

based on currently available information as to the outcome and timing of future events. Enable assumes no obligation to

and does not intend to update any forward-looking statements included herein. When considering forward-looking

statements, which include statements regarding future commodity prices, future capital expenditures and our financial

and operational outlook for 2017, among others, you should keep in mind the risk factors and other cautionary

statements described under the heading “Risk Factors” and elsewhere in our SEC filings. Enable cautions you that these

forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many

of which are beyond its control, incident to the ownership, operation and development of natural gas and crude oil

infrastructure assets. These risks include, but are not limited to, contract renewal risk, commodity price risk,

environmental risks, operating risks, regulatory changes and the other risks described under “Risk Factors” and

elsewhere in our SEC filings. Should one or more of these risks or uncertainties occur, or should underlying assumptions

prove incorrect, Enable’s actual results and plans could differ materially from those expressed in any forward-looking

statements.

3

1. Enable Midstream Overview

2. Gathering and Processing Segment Overview

3. Transportation and Storage Segment Overview

4. 2017 Outlook

5. Appendix

4

Contents

1. Enable Midstream Overview

5

Key Highlights

6

• Assets are located in prominent natural gas and crude oil producer basins with a

market-leading midstream position in the SCOOP and STACK plays

• Significant drilling activity across gathering and processing footprint

• Well-positioned to support the long-term supply and demand dynamics in the Mid-

Continent, Gulf Coast and Southeast regions

• Fully integrated suite of assets: ~12,500 miles of gathering systems, 14 major

processing plants, ~7,900 miles of interstate pipelines1, ~2,200 miles of intrastate

pipelines and eight storage facilities comprising 85.0 Bcf of storage capacity

• High degree of interconnectivity between assets and end markets and consumers

• Favorable contract structure with significant fee-based and demand-fee margin

• Long-term contracts with large-cap producers and utilities, many of whom are

investment grade

• Continue to prioritize efficient capital deployment and cost discipline

• Investment grade credit metrics and $1 billion of available liquidity2

• Strong distribution coverage

Strategically

Located

Assets

Significant

Size and

Scale

Long-term,

Fee-based

Contracts

Financially

Disciplined

1. Includes SESH, in which the partnership owns a 50% interest2. As of September 30, 2016; available liquidity calculated as Revolving Credit Facility of $1.75 billion less principal advances of $755 million less $3 million

in letters of credit plus $23 million of cash on hand

60%26%

14% Firm/MVC Fee-based

Other Fee-based

Commodity-based, includingHedges

57%

43% G&P

T&S

Interconnected, Diverse and Strategically Located

7

• Enable provides operating reach and scale with complementary capabilities

• Assets are well-positioned to support the long-term supply and demand dynamics in the Mid-

Continent, Gulf Coast and Southeast regions

Enable’s Transportation and Storage (T&S) and Gathering and Processing (G&P) Assets1

1. Map as of November 3, 20162. For nine months ending September 30, 2016; percentages represent gross margin contribution excluding eliminations3. For nine months ending September 30, 2016

YTD Gross Margin Profile3

YTD Segment Contribution2

Recent Commercial Successes

8

In October 2016, signed a new 10-year,

fee-based natural gas gathering and

processing agreement with one of the

most active producers in the STACK

• Replaces an existing percent-of-proceeds

(POP) processing arrangement

• Adds an additional 61,400 gross acres of

dedication to Enable in the STACK

• Increases fee-based margin

• Reduces commodity exposure

• Increases the volume-weighted average

term on gathering contracts

• Supports continued capital deployment at

returns consistent with Enable’s

objectives

In the third quarter of 2016, Enable’s

Mississippi River Transmission, LLC (MRT)

subsidiary extended natural gas

transportation service agreements with its

largest customer, St. Louis-based Laclede

Gas Company

• Extends existing demand levels of ~300,000

dekatherms per day (Dth/d) from 2017 to

2020

• Continues 87-year relationship with Laclede

• Increases average contract life on MRT

• Contributes to Enable’s significant firm, fee-

based business

Gathering and Processing Interstate Pipelines

Large and Diverse Customer Base

9

Top Customers1

Enable’s revenues are strengthened by a diverse, high-quality customer base, many of whom are

investment-grade or affiliates of investment-grade companies

(Investment Grade)

(Investment Grade) (Investment Grade) (Investment Grade)(Investment Grade)

► Many of our customers rely on us for multiple midstream services across both G&P and T&S

► Loyal customer base through exemplary customer service and reliable project execution

(Investment Grade)

(Investment Grade) (Investment Grade) (Investment Grade)

(Investment Grade)

1. Standard and Poor’s, Moody’s and Fitch credit ratings from Bloomberg as of November 4, 2016 – customers with split credit ratings are included as

investment-grade entities

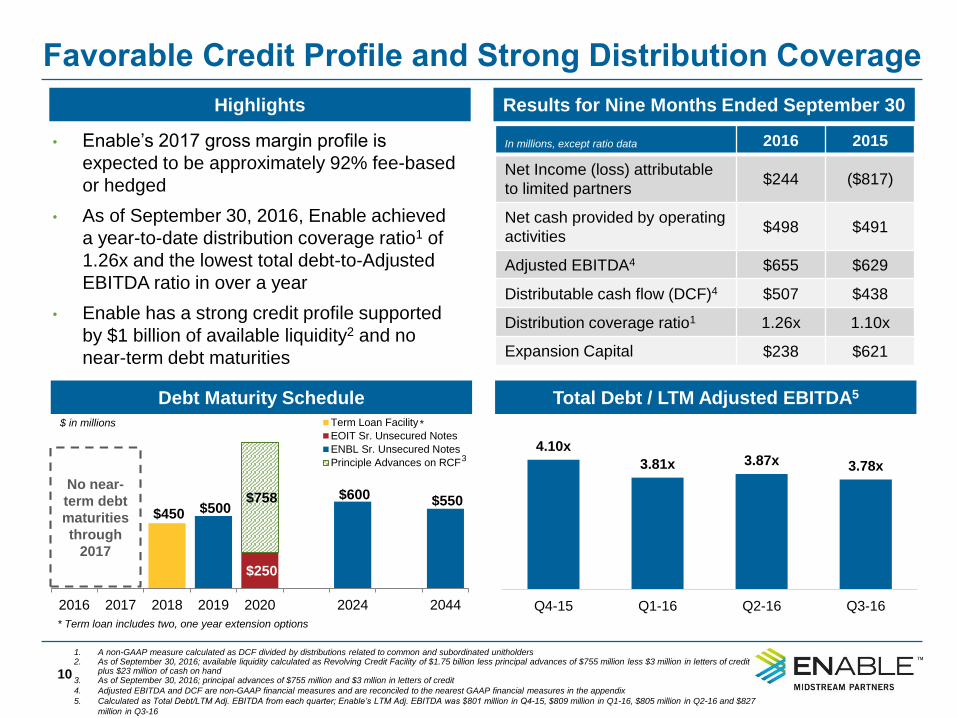

$450

$250

$500 $600 $550 $758

2016 2017 2018 2019 2020 2024 2044

Term Loan Facility

EOIT Sr. Unsecured Notes

ENBL Sr. Unsecured Notes

Principle Advances on RCF

10

Results for Nine Months Ended September 30

Debt Maturity Schedule Total Debt / LTM Adjusted EBITDA5

• Enable’s 2017 gross margin profile is

expected to be approximately 92% fee-based

or hedged

• As of September 30, 2016, Enable achieved

a year-to-date distribution coverage ratio1 of

1.26x and the lowest total debt-to-Adjusted

EBITDA ratio in over a year

• Enable has a strong credit profile supported

by $1 billion of available liquidity2 and no

near-term debt maturities

1. A non-GAAP measure calculated as DCF divided by distributions related to common and subordinated unitholders2. As of September 30, 2016; available liquidity calculated as Revolving Credit Facility of $1.75 billion less principal advances of $755 million less $3 million in letters of credit

plus $23 million of cash on hand3. As of September 30, 2016; principal advances of $755 million and $3 mllion in letters of credit

4. Adjusted EBITDA and DCF are non-GAAP financial measures and are reconciled to the nearest GAAP financial measures in the appendix

5. Calculated as Total Debt/LTM Adj. EBITDA from each quarter; Enable’s LTM Adj. EBITDA was $801 million in Q4-15, $809 million in Q1-16, $805 million in Q2-16 and $827

million in Q3-16

$ in millions

Highlights

Favorable Credit Profile and Strong Distribution Coverage

In millions, except ratio data 2016 2015

Net Income (loss) attributable

to limited partners$244 ($817)

Net cash provided by operating

activities$498 $491

Adjusted EBITDA4 $655 $629

Distributable cash flow (DCF)4 $507 $438

Distribution coverage ratio1 1.26x 1.10x

Expansion Capital $238 $621

4.10x

3.81x 3.87x 3.78x

Q4-15 Q1-16 Q2-16 Q3-16

*

* Term loan includes two, one year extension options

3

No near-

term debt

maturities

through

2017

Appendix

11

2. Gathering and Processing

Segment Overview

• Significant size and scale in prominent basins

underpinned with favorable contract structures

• 14 major processing plants with ~2.5 Bcf/d of

processing capacity located in the Anadarko, Arkoma

and Ark-La-Tex basins1

• Acreage dedications of 6.7 million gross acres with a

volume-weighted average remaining term of ~7 years2

• G&P segment gross margin is 79% fee-based1

• Contracts with minimum volume commitment features

in lean natural gas developments of 2.1 Bcf/d with

committed volume-weighted average remaining terms

of ~6 years2

• New 10-year, fee-based gathering and processing

contract in the STACK play that replaces a contract

with a POP processing arrangement

• 33 rigs are currently contractually dedicated to Enable3

15

8 8

1 1

STACK SCOOP Ark-La-Tex Arkoma Williston

Peers67%

Enable33%

Gathering and Processing Segment

12

Gathering and Processing Highlights Market-Leading SCOOP and STACK Position

1. As of September 30, 2016

2. As of December 31,2016

3. Per Drillinginfo, represents rigs that are drilling wells that are contractually dedicated to Enable – as of October 26, 2016

4. Bentek processing capacity in associated SCOOP and STACK counties as of September 30, 2016

5. Rigs contractually dedicated to Enable as a percentage of total active rigs in the respective plays

6. Per Drillinginfo, there were 19 total rigs in the counties designated under SCOOP and 46 total rigs in counties designated under STACK as of October 26, 2016

7. Per Baker Hughes, there were 17 gas rigs operating in Haynesville as of October 21, 2016

SCOOP6 STACK6 Haynesville7

Market Share of Active Rigs5

Market-Leading

Active Rig Count3

#1 in Processing

Capacity4

Peers 71%

Enable 29%

Peers58%

Enable 42%

Note: SCOOP designated as Caddo, Carter, Garvin, Grady, McClain and Stephens counties of Oklahoma;

STACK designated as Blaine, Canadian, Custer, Dewey, Kingfisher, Major and Woodward counties of

Oklahoma

Anadarko Basin

13

• Enable serves over 200 producers in the

Anadarko basin and has secured 4.6 million

gross acres of dedication under long-term, fee-

based contracts1

• The super-header system interconnects 9 of

Enable’s 11 natural gas processing plants and

has over 1.685 Bcf/d of processing capacity2

• The super-header system is uniquely positioned

to serve the prominent SCOOP and STACK

plays and allows Enable to:

• Optimize the economics of its natural gas processing

• Respond quickly to customer needs

• Efficiently phase in new production

• 7,900 miles

• 690,600 Horsepower

• 1.64 TBtu/d gathering volumes

• 11 processing plants

• 1.845 Bcf/d processing capacity

• 64.53 MBbl/d NGLs produced

• 4.6 mm gross acres of dedication

1. As of December 31, 20152. As of September 30, 20163. Map as of November 3, 2016; volumes as of nine months ended September 30, 2016; processing capacity and miles of pipe as of as of September 30, 2016;

horsepower and gross acres of dedication as of December 31, 2015

System Map3System Highlights

Bradley Processing Complex

14

• Enable’s Ark-La-Tex and Arkoma gathering and processing contracts are primarily fee-based

contracts with significant support from minimum volume commitment and guaranteed return features

• The Haynesville Shale is well-positioned to serve demand growth from LNG exports and power

generation markets

• Eight rigs are currently drilling wells that are contractually dedicated to Enable in the Ark-La-Tex

basin and one rig is currently drilling wells contractually dedicated to Enable in the Arkoma basin2

Ark-La-Tex System Map1

System Highlights

Arkoma System Map1

1. Maps as of November 3, 2016; volumes as of nine months ended September 30, 2016; processing capacity and miles of pipe as of as of September 30, 2016; horsepower and gross acres of dedication as of December 31, 2015

2. Per Drillinginfo as of October 26, 2016

Ark-La-Tex and Arkoma Basins

• 2,900 miles

• 135,800 Horsepower

• 0.63 TBtu/d gathering volumes

• 1 processing plant

• 0.060 Bcf/d processing capacity

• 4.90 MBbl/d NGLs produced

• 1.4 mm gross acres of dedication

• 1,700 miles

• 150,000 Horsepower

• 0.84 TBtu/d gathering volumes

• 2 processing plants

• 0.545 Bcf/d processing capacity

• 14.5 MBbl/d fractionation capacity

• 8.65 MBbl/d NGLs produced

• 0.7 mm gross acres of dedication

Crude Gathering Systems in the Williston Basin

15

• Enable’s first crude gathering system, the

Bear Den system, was fully operational in

the first quarter of 2015 and Enable

continues to connect new wells onto the

system

• The Nesson system commenced operations

in the second quarter of 2015 and additional

infrastructure is expected to be placed into

service as activity warrants

• Fee-based contract structures, including

some support from contracts with minimum

volume commitment features

• XTO Energy, Enable’s top customer in the

Bakken, is one of the most active producers

in North Dakota1

System Map2System Highlights

1. Per North Dakota’s Department of Mineral Resources website as of November 3, 20162. Map as of November 3, 2016; gross acres data as of December 31, 2015

• Total of 0.2 million

gross acres dedicated

Appendix3. Transportation and Storage

Segment Overview

16

G&P57%

T&S43%

Fee-based 96%

IG Customers

65%

• Significant firm, fee-based margin with high-

quality customers across 9 states

• Enable Oklahoma Intrastate Transmission

(EOIT), Mississippi River Transmission (MRT)

and Southeast Supply Header (SESH) all

have significant interconnectivity with Enable

Gas Transmission (EGT)

• Well-situated to facilitate natural gas demand

growth in the Mid-Continent, Gulf Coast and

Southeast regions

• Enable’s interstate and intrastate pipeline systems

continue to meet the residue gas transportation

needs of the growing SCOOP and STACK plays

• Shippers have the ability to access almost

every major consuming market east of the

Mississippi River through Perryville Hub and

associated trading points

Transportation and Storage Segment

17

1. Map as of November 3, 2016

2. As of September 30, 2016

3. Customers as of September 30, 2016; Standard and Poor’s, Moody’s and Fitch credit ratings from Bloomberg as of October 24, 2016 – customers with split

credit ratings are included as investment-grade entities

Transportation and Storage Highlights Transportation and Storage System1

Revenues from

Investment-grade

(IG) Customers3

T&S YTD

Gross Margin2

EGT

EOIT

Perryville Hub

YTD Total Margin

Contribution2

Enable Gas Transmission (EGT)

18

• 5,900-mile interstate pipeline serving the

Anadarko, Ark-La-Tex and Arkoma basins1

• EGT’s primary customers include LDCs, gas

producers and gas-fired power generators

• ~28% of EGT’s gross margin is attributable to

services provided to subsidiaries of CenterPoint

Energy2

• ~85% of EGT’s capacity is under contract with an

average remaining contract life of 3.4 years2

• ~54% of total T&S segment gross margins derived

from demand charges under EGT’s firm contracts2

• EGT is well-positioned to serve increasing

Oklahoma production

• Announced Line AD expansion, with related new

shipper commitments in excess of 175,000 Dth/d,

expected to be in-service in Q2-17

• Completed the Bradley Lateral in the fourth quarter

of 2015 which added over 200,000 Dth/d of long-

term, firm transportation contracts

• Total system utilization continues to increase

including deliveries to power generators and off-

system interconnects

Pipeline Map3Pipeline Highlights

1. As of September 30, 20162. As of December 31, 20153. Map as of November 3, 2016; pipeline miles as of September 30, 2016, and capacity data as of December 31, 2015

• 5,900 miles

• 6.5 Bcf/d capacity

• 29.5 Bcf storage capacity

Mississippi River Transmission (MRT)

19

• 1,700-mile interstate pipeline that

offers shippers competitive rates

and is interconnected to diverse

supply points1

• MRT’s primary customers are local

distribution companies and industrial

markets in the St. Louis market area

• ~89% of capacity is under contract1

• ~14% of total T&S segment gross

margins derived from demand charges

under MRT’s firm contracts1

• Extended contracts expiring in 2017

with Laclede Gas Company through

2020 in the third quarter of 2016

Pipeline Map2Pipeline Highlights

• 1,700 miles

• 1.9 Bcf/d capacity

• 31.5 Bcf storage capacity

1. As of December 31, 20152. Map as of November 3, 2016; pipeline miles and capacity data as of December 31, 2015

Select Interconnects Supply Basin/Region

EGT Anadarko, Fayetteville and Haynesville

Perryville Hub Barnett, Haynesville and Gulf Coast

NGPL & Trunkline Marcellus/Utica, Mid-Con and Gulf Coast

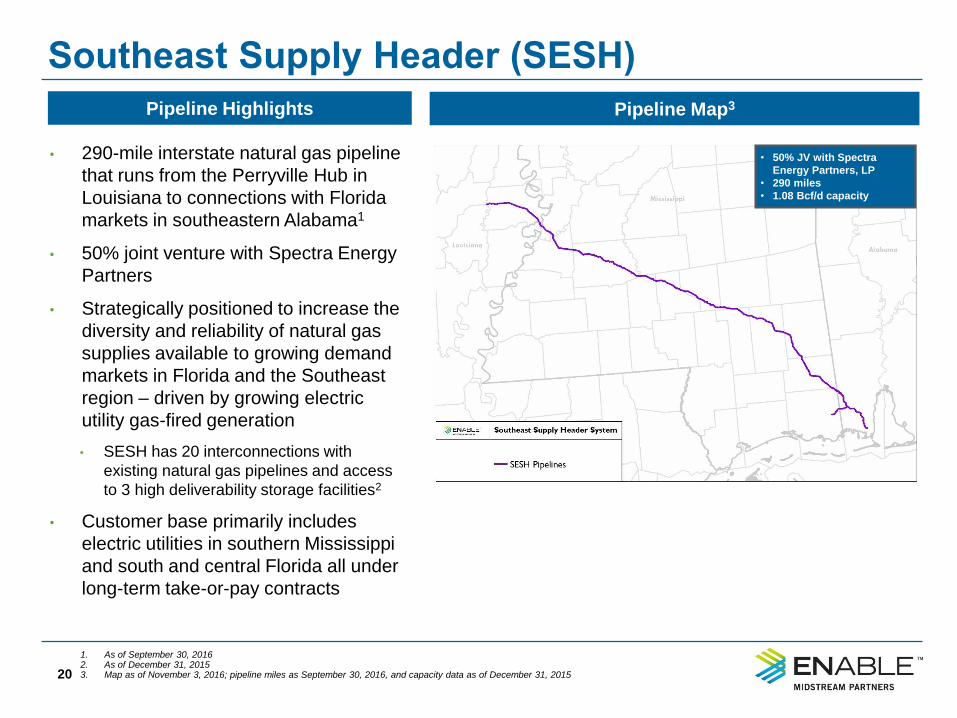

Southeast Supply Header (SESH)

20

• 290-mile interstate natural gas pipeline

that runs from the Perryville Hub in

Louisiana to connections with Florida

markets in southeastern Alabama1

• 50% joint venture with Spectra Energy

Partners

• Strategically positioned to increase the

diversity and reliability of natural gas

supplies available to growing demand

markets in Florida and the Southeast

region – driven by growing electric

utility gas-fired generation

• SESH has 20 interconnections with

existing natural gas pipelines and access

to 3 high deliverability storage facilities2

• Customer base primarily includes

electric utilities in southern Mississippi

and south and central Florida all under

long-term take-or-pay contracts

Pipeline Map3Pipeline Highlights

1. As of September 30, 20162. As of December 31, 20153. Map as of November 3, 2016; pipeline miles as September 30, 2016, and capacity data as of December 31, 2015

• 50% JV with Spectra

Energy Partners, LP

• 290 miles

• 1.08 Bcf/d capacity

21

• Interconnects natural gas supply from

the Anadarko and Arkoma basins to

Enable’s EGT system and 12 third-party

natural gas pipelines with 67

interconnect points1

• Connected to 36 end-user customers,

including 14 natural gas-fired electric

generation facilities in Oklahoma1

• Major customers include Oklahoma Gas &

Electric, an affiliate of OGE Energy Corp.,

and Public Service Company of Oklahoma

(PSO), an affiliate of American Electric

Power Co.

• Functions as a delivery system for

Enable’s super-header processing

system and is well-positioned to serve

transportation needs for producers in the

SCOOP, STACK, Mississippi Lime and

Greater Granite Wash plays

EOIT Pipeline Map2Pipeline Highlights

1. As of December 31, 20152. Map as of November 3, 2016; pipeline miles as of September 30, 2016; throughput and capacity data as of December 31, 2015

Enable Oklahoma Intrastate Transmission (EOIT)

• 2,200 miles

• 2.1 Bcf/d peak throughput

• 24.0 Bcf storage capacity

Appendix4. 2017 Outlook

22

Significant Producer Acreage and Activity

23

STACK and SCOOP Acreage and Activity1 Haynesville Activity1

• Drilling activity in the STACK, SCOOP and Haynesville is expected to

drive significant volume growth for 2017

1. Assets as of November 3, 2016 and rig data per Drillinginfo as of October 26, 2016

Others

24

2017 Operational

Outlook

Natural Gas Gathered Volumes (TBtu/d) 3.3 – 3.8

Anadarko 1.7 – 2.0

Arkoma 0.5 – 0.7

Ark-La-Tex 0.9 – 1.3

Natural Gas Processed Volumes (TBtu/d) 1.9 – 2.3

Anadarko 1.6 – 1.9

Arkoma 0.1 – 0.2

Ark-La-Tex 0.1 – 0.3

Crude Oil – Gathered Volumes (MBbl/d) 23.0 – 28.0

Interstate Firm Contracted Capacity (Bcf/d) 6.1 – 6.5

2017 Operational Outlook 2017 Financial Outlook

2017 Operational, Financial and Capital Outlook

$ in millions

2017 Financial

Outlook

Net Income Attributable to Common and

Subordinated Unit Holders$315 – $385

Interest Expense $114 – $122

Adjusted EBITDA3 $825 – $885

Preferred Equity Distributions4 $36

Adjusted Interest Expense3 $120 – $130

Maintenance Capital $95 – $125

Distributable Cash Flow3 $555 – $605

Distribution Coverage Ratio5 1.0x or greater

54%31%

7%

8% Firm/MVCFee-based

Other Fee-based

Commodity-based Hedged

Commodity-basedUnhedged

2017 Margin Profile62017 Capital Outlook

$ in millions

2017 Capital

Outlook

Gathering Related Expansion Capital $320 – $420

Processing Plants1 $90 – $100

Transportation and Storage Organic

Growth2 $45 – $55

Total Capital $455 – $575

~92% fee-

based or

hedged

1. Represents capital associated with the Wildhorse Plant, if elected to resume construction; the Wildhorse Plant is a 200 MMcf/d cryogenic processing facility located in Garvin County,

Oklahoma

2. Primarily represents a new end-user transportation project

3. Adjusted EBITDA, adjusted interest expense and distributable cash flow are non-GAAP financial measures and are reconciled to the nearest GAAP financial measures in the appendix

4. Includes the fourth quarter 2017 distribution that will be paid in the first quarter 2018

5. A non-GAAP measure calculated as DCF divided by distributions related to common and subordinated unitholders

6. Gross margin profile represents forecasted Q1-17 through Q4-17; percentages in pie charts based on Gross Margin contribution

As of November 2, 2016

2017 Price Assumptions and Sensitivities

25

2017 Prices Assumptions

Natural Gas – Henry Hub ($/MMBtu) $3.05 – $3.45

NGLs – Mont Belvieu, Texas ($/gal)1 $0.46 – $0.56

NGLs – Conway, Kansas ($/gal)1 $0.44 – $0.54

Crude Oil – WTI ($Bbl) $48.00 – $58.00

1. NGL composite based on assumed composition of 45%, 30%, 10%, 5% and 10% for ethane, propane, normal butane, isobutane and natural gasoline,

respectively

2. The price sensitivities assume 2017 price changes occur on January 1, 20173. The impact of price sensitivities is the same for net income attributable to limited partners and net income attributable to common and subordinated units

Impact to 2017 Net Income (including impact of hedges)3

% Change in Prices

$ in millions +10% -10%

Natural Gas and Ethane $5 ($5)

NGLs (excluding ethane) and Condensate $6 ($6)

Impact to 2017 Adjusted EBITDA (including impact of hedges)

% Change in Prices

$ in millions +10% -10%

Natural Gas and Ethane $5 ($5)

NGLs (excluding ethane) and Condensate $6 ($6)

2017 Price Sensitivities2

As of November 2, 2016

Appendix

26

5. Appendix

Public Unitholders

Enable Ownership Structure

27

GP Interest50% management interest40% economic interest

LP Interest55.4% of common and subordinated units100% of Series A Preferred Units

Incentive DistributionRights

Note: As of September 30, 20161. Percentage of common and subordinated units

GP Interest50% management interest60% economic interest

LP Interest26.3% of common and subordinated units

LP Interest18.3% of common units1

NYSE: ENBL

Operating Statistics by Basin

28

Anadarko Arkoma Ark-La-Tex

Q3-16 Q3-15 Q3-16 Q3-15 Q3-16 Q3-15

Natural Gas Gathered Volumes (TBtu/d) 1.66 1.70 0.61 0.65 0.89 0.82

Natural Gas Processed Volumes (TBtu/d) 1.50 1.49 0.10 0.09 0.18 0.29

Gross NGL Production (MBbl/d)1 65.24 70.02 4.69 4.73 7.60 9.05

Anadarko Arkoma Ark-La-Tex

Q2-16 Q2-15 Q2-16 Q2-15 Q2-16 Q2-15

Natural Gas Gathered Volumes (TBtu/d) 1.62 1.63 0.65 0.67 0.83 0.89

Natural Gas Processed Volumes (TBtu/d) 1.44 1.41 0.10 0.11 0.22 0.32

Gross NGL Production (MBbl/d)1 69.64 58.63 5.03 4.96 8.42 10.60

Third Quarter 2016 & 2015

Second Quarter 2016 & 2015

1. Excludes condensate

Hedging Summary

29

1. Table includes hedges and commodity exposures associated with equity volumes resulting from Enable's Gathering, Processing and Transportation businesses; percentage hedged includes hedges executed through November 3, 2016

2. Enable hedges net condensate/natural gasoline exposure with crude3. Percentage hedged for 2016 reflects November-December hedges only

Commodity1 2016 3 2017

Natural Gas

Exposure Hedged (%) 98% 66%

Average Hedge Price ($/MMBtu) $2.73 $2.64

Crude2

Exposure Hedged (%) 82% 45%

Average Hedge Price ($/Bbl) $54.93 $48.44

Propane

Exposure Hedged (%) 90% 51%

Average Hedge Price ($/gal) $0.49 $0.46

Non-GAAP Reconciliations

30

Three Months Ended

September 30, Nine Months Ended

September 30,

2016 2015 2016 2015

(In millions)

Reconciliation of Gross Margin to Total Revenues:

Consolidated

Product sales $ 326 $ 357 $ 837 $ 1,043

Service revenue 294 289 821 809

Total Revenues 620 646 1,658 1,852

Cost of natural gas and natural gas liquids (excluding

depreciation and amortization) 268

287

717

856

Gross margin $ 352 $ 359 $ 941 $ 996

Reportable Segments

Gathering and Processing

Product sales $ 295 $ 299 $ 759 $ 875

Service revenue 160 157 416 404

Total Revenues 455 456 1,175 1,279

Cost of natural gas and natural gas liquids (excluding

depreciation and amortization) 246

235

642

698

Gross margin $ 209 $ 221 $ 533 $ 581

Transportation and Storage

Product sales $ 150 $ 166 $ 348 $ 467

Service revenue 135 133 408 408

Total Revenues 285 299 756 875

Cost of natural gas and natural gas liquids (excluding

depreciation and amortization) 141

161

346

459

Gross margin $ 144 $ 138 $ 410 $ 416

Non-GAAP Reconciliations Continued

31

1. Distributions from equity method affiliate includes

an $8 million and $7 million return on investment

and a $5 million and $3 million return of investment

for the three months ended September 30, 2016

and 2015, respectively. Distributions from equity

method affiliate includes a $22 million and $26

million return on investment and an $18 million and

$11 million return of investment for the nine

months ended September 30, 2016 and 2015,

respectively. Equity in earnings of equity method

affiliate, net of distributions only includes those

distributions representing a return on investment.

2. Other non-cash losses includes decreases in the

fair value of derivatives, lower of cost or net

realizable value adjustments, loss on sale of

assets and write-downs of materials and supplies.

3. Other non-cash gains includes lower of the cost or

net realizable value adjustment recoveries upon

the sale of the related inventory and increases in

the fair value of derivatives.

4. This amount represents the quarterly cash

distributions on the Series A Preferred Units

declared for the three and nine months ended

September 30, 2016. In accordance with the

Partnership Agreement, the Series A Preferred

Unit distributions are deemed to have been paid

out of available cash with respect to the quarter

immediately preceding the quarter in which the

distribution is made.

5. See slide 25 for a reconciliation of Adjusted

interest expense to Interest expense.

6. Represents cash distributions declared for

common and subordinated units outstanding as of

each respective period. Amounts for 2016 reflect

estimated cash distributions for common and

subordinated units outstanding for the quarter

ended September 30, 2016.

Three Months Ended

September 30, Nine Months Ended

September 30,

2016 2015 2016 2015

(In millions, except Distribution coverage ratio)

Reconciliation of Adjusted EBITDA and DCF to net income

(loss) attributable to limited partners and calculation of

Distribution coverage ratio:

Net income (loss) attributable to limited partners $ 119 $ (985 ) $ 244 $ (817 )

Add:

Depreciation and amortization expense 84 84 248 233

Interest expense, net of interest income 26 23 74 66

Income tax expense 2 — 3 2

EBITDA $ 231 $ (878 ) $ 569 $ (516 )

Add:

Distributions from equity method affiliate (1) 13 10 40 37

Non-cash equity based compensation 4 1 9 7

Other non-cash losses(2) 3 4 61 30

Impairments 8 1,105 8 1,105

Less:

Other non-cash gains(3) (7 ) (7 ) (10 ) (7 )

Noncontrolling Interest Share of Adjusted EBITDA — (6 ) — (6 )

Equity in earnings of equity method affiliate (8 ) (7 ) (22 ) (21 )

Adjusted EBITDA $ 244 $ 222 $ 655 $ 629

Less:

Series A Preferred Unit distributions(4) (9 ) — (22 ) —

Adjusted interest expense(5) (27 ) (27 ) (76 ) (77 )

Maintenance capital expenditures (21 ) (41 ) (51 ) (113 )

Current income taxes 2 — 1 (1 )

DCF $ 189 $ 154 $ 507 $ 438

Distributions related to common and subordinated unitholders (6) $ 134 $ 134 $ 402 $ 400

Distribution coverage ratio 1.41 1.15 1.26 1.10

Non-GAAP Reconciliations Continued

32

1. Distributions from equity method affiliate

includes an $8 million and $7 million return

on investment and a $5 million and $3

million return of investment for the three

months ended September 30, 2016 and

2015, respectively. Distributions from equity

method affiliate includes a $22 million and

$26 million return on investment and an

$18 million and $11 million return of

investment for the nine months ended

September 30, 2016 and 2015,

respectively. Equity in earnings of equity

method affiliate, net of distributions only

includes those distributions representing a

return on investment.

2. Other non-cash losses includes decreases

in the fair value of derivatives, lower of cost

or net realizable value adjustments, loss on

sale of assets and write-downs of materials

and supplies.

3. Other non-cash gains includes lower of the

cost or net realizable value adjustment

recoveries upon the sale of the related

inventory and increases in the fair value of

derivatives.

Three Months Ended

September 30, Nine Months Ended

September 30,

2016 2015 2016 2015

(In millions)

Reconciliation of Adjusted EBITDA to net cash provided by

operating activities:

Net cash provided by operating activities $ 209 $ 207 $ 498 $ 491

Interest expense, net of interest income 26 23 74 66

Net income attributable to noncontrolling interest — 6 — 6

Income tax expense 2 — 3 2

Deferred income tax expense (benefit) (4 ) — (4 ) (1 )

Equity in earnings of equity method affiliate, net of

distributions(1) —

(3 ) —

(16 )

Impairments (8 ) (1,105 ) (8 ) (1,105 )

Non-cash equity based compensation (4 ) (1 ) (9 ) (7 )

Other non-cash items (1 ) 4 (7 ) 11

Changes in operating working capital which (provided) used

cash:

Accounts receivable 47 37 25 35

Accounts payable 4 12 88 82

Other, including changes in noncurrent assets and

liabilities (40 ) (58 ) (91 ) (80 )

EBITDA $ 231 $ (878 ) $ 569 $ (516 )

Add:

Non-cash equity based compensation 4 1 9 7

Distributions from equity method affiliate (1) 13 10 40 37

Impairments 8 1,105 8 1,105

Other non-cash losses(2) 3 4 61 30

Less:

Other non-cash gains(3) (7 ) (7 ) (10 ) (7 )

Noncontrolling Interest Share of Adjusted EBITDA — (6 ) — (6 )

Equity in earnings of equity method affiliate (8 ) (7 ) (22 ) (21 )

Adjusted EBITDA $ 244 $ 222 $ 655 $ 629

Non-GAAP Reconciliations Continued

33

Three Months Ended

September 30, Nine Months Ended

September 30,

2016 2015 2016 2015

(In millions)

Reconciliation of Adjusted interest expense to Interest expense:

Interest Expense $ 26 $ 23 $ 74 $ 66

Add:

Amortization of premium on long-term debt 1 2 4 4

Capitalized interest on expansion capital — 3 1 9

Less:

Amortization of debt costs — (1 ) (3 ) (2 )

Adjusted interest expense $ 27 $ 27 $ 76 $ 77

Forward Looking Non-GAAP Reconciliation

34

1. Other non-cash losses includes changes in the fair value of derivatives, lower of cost or net realizable value adjustments, loss on sale of assets and write-

downs of materials and supplies.

2. Other non-cash gains include lower of the cost or net realizable value adjustment recoveries upon the sale of the related inventory.

3. Outlook includes the fourth quarter 2017 distribution that will be paid in first quarter 2018

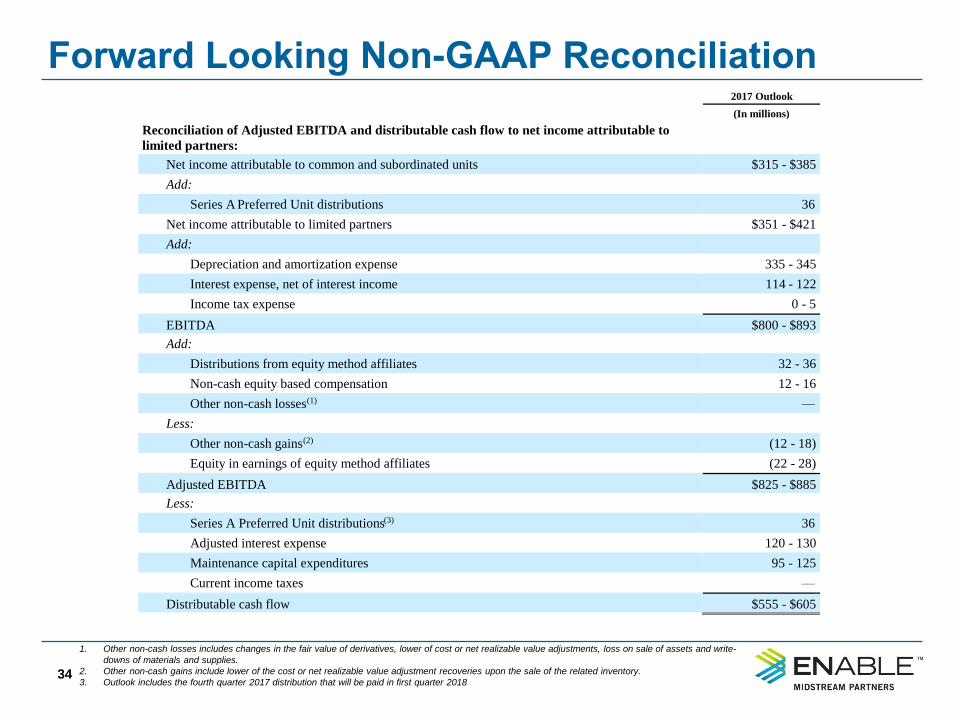

2017 Outlook

(In millions)

Reconciliation of Adjusted EBITDA and distributable cash flow to net income attributable to

limited partners:

Net income attributable to common and subordinated units $315 - $385

Add:

Series A Preferred Unit distributions 36

Net income attributable to limited partners $351 - $421

Add:

Depreciation and amortization expense 335 - 345

Interest expense, net of interest income 114 - 122

Income tax expense 0 - 5

EBITDA $800 - $893

Add:

Distributions from equity method affiliates 32 - 36

Non-cash equity based compensation 12 - 16

Other non-cash losses(1) —

Less:

Other non-cash gains(2) (12 - 18)

Equity in earnings of equity method affiliates (22 - 28)

Adjusted EBITDA $825 - $885

Less:

Series A Preferred Unit distributions(3) 36

Adjusted interest expense 120 - 130

Maintenance capital expenditures 95 - 125

Current income taxes —

Distributable cash flow $555 - $605

Forward Looking Non-GAAP Reconciliation Continued

35

Enable is unable to present a quantitative reconciliation of forward looking Adjusted EBITDA to Net Cash Provided by

Operating Activities because certain information needed to make a reasonable forward-looking estimate of changes in

working capital which may (provide) use cash during the calendar year 2017 cannot be reliably predicted and the

estimate is often dependent on future events which may be uncertain or outside of Enable's control. This includes

changes to Accounts Receivable, Accounts Payable and Other changes in non-current assets and liabilities.

2017 Outlook

(In millions)

Reconciliation of Adjusted interest expense to Interest expense:

Interest Expense $114 - $122

Add:

Amortization of premium on long-term debt 5

Capitalized interest on expansion capital 0 - 6

Less:

Amortization of debt costs (0 - 4)

Adjusted interest expense $120 - $130