fourth quarter 20162016 can be characterized as a tale of two halves after weak commodity prices,...

TRANSCRIPT

Quarterly Commentary

Fourth Quarter 2016

333 S. Grand Ave., 18th Floor || Los Angeles, CA 90071 || (213) 633-8200

2

Quarterly Commentary 12/31/16

Quarterly Commentary

2016 can be characterized as a tale of

two halves after weak commodity

prices, low inflation, falling rates and

uncertain global growth expectations

were later met with some political

certainty and a reversal of these

trends as investors became optimistic

about the future. During the fourth

quarter, global markets were heavily

focused on the outcome of the U.S.

presidential election and what impact

the newly elected president would

have on the global economy. After

correctly calling for higher rates and a

Trump victory earlier in the year,

Jeffrey Gundlach is encouraging

investors to move forward with

caution as an enthusiastic December

could be met with some

disappointment in the coming months

as proposed policy changes may take

several months/years to take effect.

During the quarter, investors took to

risk assets despite the expected

Federal Open Market Committee

(FOMC) December rate hike which

brought the Fed Funds Rate target

range up to 0.50-0.75%. Although the

rate hike was underwhelming relative

to the three hikes expected at the

beginning of 2016, the expectation is

set again for three more hikes during

2017. Instead of the global sell-off

equity markets experienced at this

time last year, the investment thesis

for investors is predicated on any

positive change the policies enacted

by the Trump administration would

bring.

It appears, for now at least, that a

Trump presidency has given investors

a sense of confidence evident by the

renewed interest for equities,

particularly Financials and Industrials,

which performed well post-election.

Additionally, the U.S. Dollar (USD), as

measured by the trade-weighted

Dollar Spot Index (DXY), rose to the

highest level in years as uncertainty

over trade policy loomed. The U.S.

economy also experienced higher

inflation expectations, stable energy

prices and higher rates over the

quarter.

What is largely unknown, however, is

how President-elect Trump will

actually act and uphold promises

made to various groups during his

campaign. As such, his success may be

highly dependent on measures such as

higher average hourly earnings and

greater opportunities for

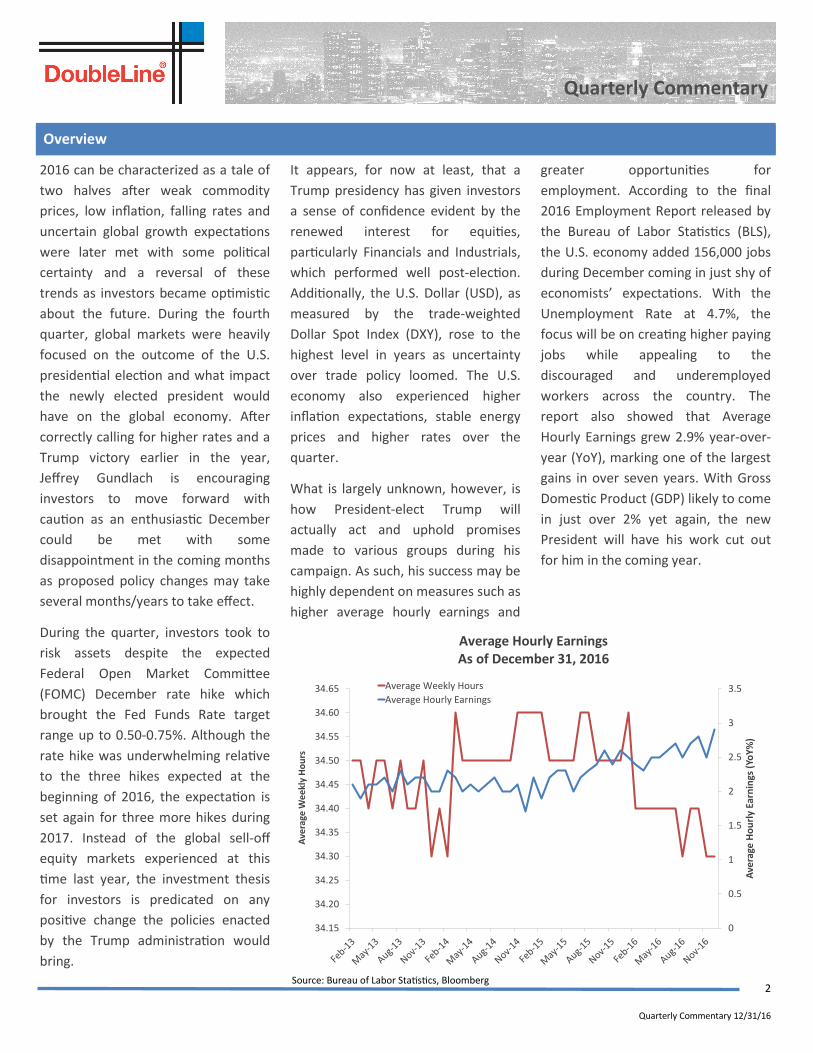

employment. According to the final

2016 Employment Report released by

the Bureau of Labor Statistics (BLS),

the U.S. economy added 156,000 jobs

during December coming in just shy of

economists’ expectations. With the

Unemployment Rate at 4.7%, the

focus will be on creating higher paying

jobs while appealing to the

discouraged and underemployed

workers across the country. The

report also showed that Average

Hourly Earnings grew 2.9% year-over-

year (YoY), marking one of the largest

gains in over seven years. With Gross

Domestic Product (GDP) likely to come

in just over 2% yet again, the new

President will have his work cut out

for him in the coming year.

Overview

Average Hourly Earnings As of December 31, 2016

Source: Bureau of Labor Statistics, Bloomberg

0

0.5

1

1.5

2

2.5

3

3.5

34.15

34.20

34.25

34.30

34.35

34.40

34.45

34.50

34.55

34.60

34.65

Ave

rage

Ho

url

y Ea

rnin

gs (

YoY

%)

Ave

rage

We

ekl

y H

ou

rs

Average Weekly Hours

Average Hourly Earnings

3

Quarterly Commentary 12/31/16

Quarterly Commentary

Prepayment speeds declined by

about 10% on an aggregate basis,

month-over-month (MoM) for

December. Not surprisingly, lower

coupon securities declined in

prepayment speeds the most due

to the rise in mortgage rates.

Thirty-year conventional paper

slowed down in prepayment

speeds by approximately 11% and

15-year paper declined by

approximately 6%. Refinancing

activity also declined materially

by about 23%, while purchase

activity declined slightly by about

2%.

Total gross issuance for

December was roughly $165

billion, the second highest

issuance month of 2016, bringing

year-to-date (YTD) volumes to

over $1.5 trillion. This is

approximately 17% higher than

2015’s total issuance numbers

and in line with most research

desks’ expectations given the

higher prepayment activity for

most of this year.

The Federal Housing

Administration (FHA) announced

another decrease in mortgage

insurance premiums by 25 bps,

bringing the MIP (mortgage

insurance premium) to about 5

basis points (bps) higher to pre-

crisis levels. While this will have

an impact on prepayment speeds

for Ginnie Mae collateral, it will

likely not have the same impact

as the MIP reduction in early

2015; the 2015 reduction was due

to the combination of a higher

reduction in MIPs against a

rallying market with mortgage

rates declining materially.

The biggest headline affecting the

non-Agency Residential Mortgage

-Backed Securities (RMBS) market

was the presidential election. As

risk assets rallied post-election, so

did the non-Agency RMBS

market. Spreads ended the

quarter approximately 25-50 bps

tighter, and 150-200 bps tighter

from the wides of the year in

February. For the month, spreads

were largely flat to slightly

tighter.

During the quarter, the

Citigroup’s reps and warrants

settlement was paid. Combined

with the Countrywide settlement

payout during the summer, two

of the three big originator

settlements have now been paid.

Chase will likely pay their

settlement in 2017.

Total secondary BWIC (bids

wanted in competition) volume

Agency Mortgage-Backed Securities

Mortgage Bankers Association (MBA) Purchase Index

As of December 30, 2016

Non-Agency MBS

Source: eMBS, Barclays Capital

Source: Bloomberg

MBA Refinance Index As of December 30, 2016

Source: Bloomberg

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

12/30/20161,132

120

140

160

180

200

220

240

260

280

12/30/2016228

Conditional Prepayment Rates (CPR)

2016 Jan Feb Mar Apr May Jun July Aug Sept Oct Nov Dec

Fannie Mae (FNMA) 9.3% 10.1% 14.7% 14.2% 15.0% 16.3% 15.0% 20.0% 18.9% 17.9% 17.0% 15.1%

Freddie Mac (FHLMC) 9.3% 10.0% 14.6% 14.1% 15.0% 16.1% 14.8% 19.8% 18.6% 17.7% 16.6% 14.7%

Ginnie Mae (GNMA) 13.4% 14.2% 19.3% 18.5% 19.6% 21.5% 19.9% 23.8% 22.5% 21.7% 21.2% 18.5%

Bloomberg Barclays Capital U.S.

MBS Index 9/30/2016 10/31/2016 11/30/2016

MoM

Change

Average Dollar Price $105.39 $103.82 $103.52 -$0.30

Duration 3.09 4.46 4.61 0.15

Bloomberg Barclays Capital U.S.

Index Returns 10/31/2016 11/30/2016 12/31/2016

Aggregate -1.10% -2.37% 0.41%

MBS -0.56% -1.71% 0.00%

Corporate -1.44% -2.73% 0.61%

Treasury -1.28% -2.67% -0.11%

4

Quarterly Commentary 12/31/16

Quarterly Commentary

was $6.3 billion in the fourth

quarter. The previous three

quarters averaged close to $20

billion in BWIC volume. The fourth

quarter volume was lower than

usual due to the election;

however BWIC volume is expected

to be lower in 2017 due to lower

supply. December BWIC volume

was $4.7 billion, in line with prior

months.

Prepayment speeds in the

December remittance report

(which represents November

performance) were flat to slightly

down MoM, due to the election

and holidays in November. As we

move forward in a higher rate

environment, prepayment speeds

should slow in 2017. Liquidation

rates were unchanged from the

prior month. Loss severities were

slightly higher in the December

remittance report due to an

increase in loans from judicial

states like New York, where

foreclosure timelines can be very

long due to the need for the

foreclosure to be seen by a judge

for approval, being liquidated.

Eight private-label transactions

totaling $5.3 billion priced in

December bringing total 2016

Commercial Mortgage-Backed

Securities (CMBS) issuance to

$66.3 billion, 28% lower than 2015

issuance. Fourth quarter issuance

was 29% higher quarter-over-

quarter (QoQ), with conduit

issuance 18% higher and single-

asset single-borrower (SASB) 59%

higher.

Conduit spreads ended the year

20-70 bps tighter compared to

year-end 2015. However, all-in

yields were only moderately lower

due to rising U.S. Treasury (UST)

rates. Fourth quarter 10- year last

cash flow (LCF) bonds priced in a

range of swaps +100 bps to swaps

+120 bps, with the last deal of the

quarter pricing 5 bps tighter than

the first deal of the quarter. BBB-

bonds priced in a range of swaps

+480 bps to swaps +700 bps, with

the final deal pricing 35 bps

tighter than the quarter’s initial

deal.

The Trepp CMBS Delinquency Rate

rose 20 bps in December to

5.23%, its highest level since

October 2015. The delinquency

rate has increased nine of the last

ten months. The current rate is 6

bps higher YoY. The all-time high

Delinquency Rate was 10.34% in

July 2012. This continued uptick in

delinquencies is anticipated as a

wave of deals issued pre-crisis

(2006/2007), primarily

collateralized by 10-year loans,

continues to mature. As of

November, the Moody’s/RCA

Commercial Property Price Indices

(CPPI) National All-Property

Composite Index gained 103.5%

since its financial crisis trough in

January 2010. Prices are now

22.3% above their pre-crisis peak

in November 2007.

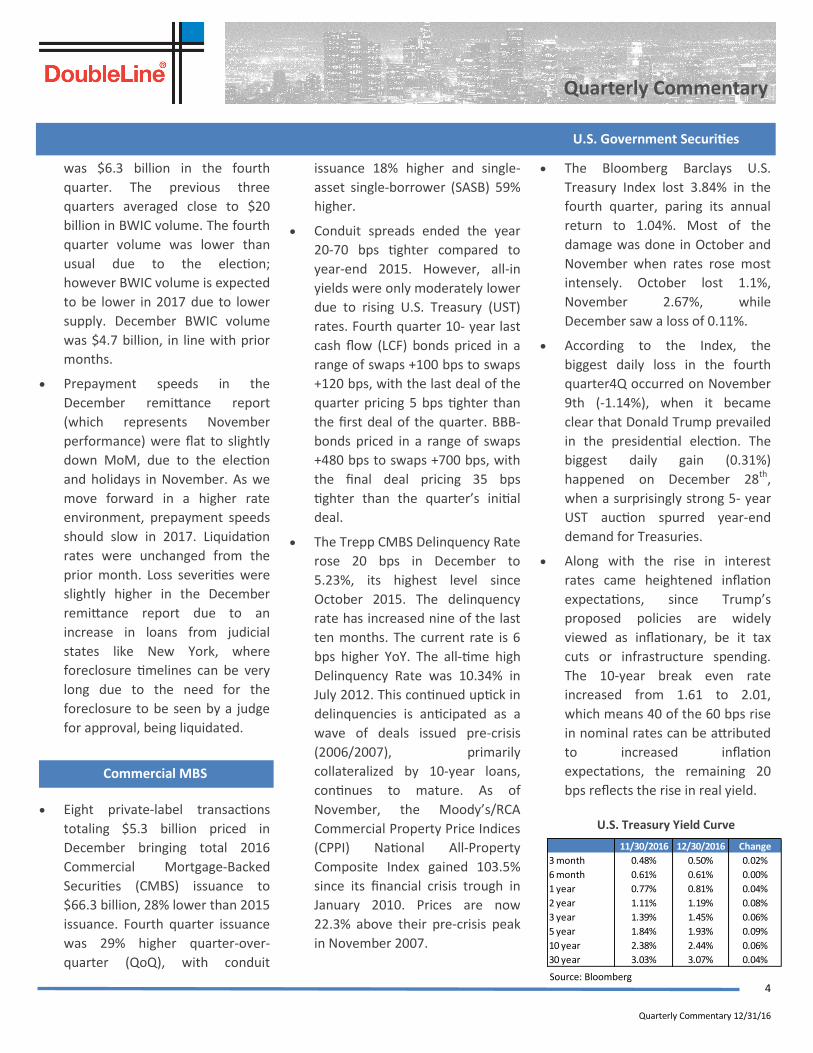

The Bloomberg Barclays U.S.

Treasury Index lost 3.84% in the

fourth quarter, paring its annual

return to 1.04%. Most of the

damage was done in October and

November when rates rose most

intensely. October lost 1.1%,

November 2.67%, while

December saw a loss of 0.11%.

According to the Index, the

biggest daily loss in the fourth

quarter4Q occurred on November

9th (-1.14%), when it became

clear that Donald Trump prevailed

in the presidential election. The

biggest daily gain (0.31%)

happened on December 28th,

when a surprisingly strong 5- year

UST auction spurred year-end

demand for Treasuries.

Along with the rise in interest

rates came heightened inflation

expectations, since Trump’s

proposed policies are widely

viewed as inflationary, be it tax

cuts or infrastructure spending.

The 10-year break even rate

increased from 1.61 to 2.01,

which means 40 of the 60 bps rise

in nominal rates can be attributed

to increased inflation

expectations, the remaining 20

bps reflects the rise in real yield.

U.S. Treasury Yield Curve

Source: Bloomberg

Commercial MBS

U.S. Government Securities

11/30/2016 12/30/2016 Change

3 month 0.48% 0.50% 0.02%

6 month 0.61% 0.61% 0.00%

1 year 0.77% 0.81% 0.04%

2 year 1.11% 1.19% 0.08%

3 year 1.39% 1.45% 0.06%

5 year 1.84% 1.93% 0.09%

10 year 2.38% 2.44% 0.06%

30 year 3.03% 3.07% 0.04%

5

Quarterly Commentary 12/31/16

Quarterly Commentary

Due to the increase in rates by the

Federal Reserve (Fed), the

Barclays U.S. Credit Index was

down 2.97% but delivered 1.56%

of excess return as spreads

tightened by 12 bps.

In December, while rates in the

UST market ended the month

virtually unchanged, the volatility

in rates continued to impact net

new issuance. New issuance in

December slowed to $38.9 billion

from $72.8 billion in November

and $55.4 billion in December

2015. Despite the slowdown, new

issuance for the year ended at an

all-time high of $1.44 billion.

Higher beta and longer dated

bonds continued to deliver higher

excess returns. The Long U.S.

Credit Index outperformed

duration matched treasuries by

384 bps in the quarter and 205

bps in December. The best

performing sector was in Energy

with Independents up 50 bps in

the quarter, and up 2.92%

December.

The outperformance relative to

UST in 2016, especially at the long

end of the market, was driven by

a strong technical backdrop.

Credit metrics, as measured by

gross and net leverage, are near

all-time highs, however, higher

U.S. yields have continued to

attract flows into the asset class

albeit at a slowing pace over the

past two months. Year-to-date

(YTD), Investment Grade (IG) has

seen mutual fund flows of $145

billion (8.5% as a percentage of

the asset class). It would appear

difficult to replicate the strong

technicals of 2016 but we would

expect to see continued interest

in the asset class if rates in the

U.S. remain higher than other

developed markets.

The Collateralized Loan Obligation

(CLO) new issue market ended the

year with monthly issuance of

$7.16 billion. This brings the yearly

issuance total of CLO paper to

$72.30 billion across 156 deals by

81 unique managers, meeting the

market’s original expectations of

$70 billion. The fourth quarter

saw the highest issuance of the

year with $26.21 billion in

issuance. Not only was the quarter

the highest quarterly issuance for

the year, but October, November

and December were the top three

months of issuance for 2016.

December also marked the final

month before Risk Retention

implementation. Managers rushed

to refinance and reset their deals

before December 24th. 23 deals

either refinanced or reset their

deals in December. In 2016, there

was a total of $41 billion in resets

and refinances, more than four

times the amount of refinancing

and reset activity seen in 2015.

The December Opal Conference

participants were constructive on

the loan and CLO market for their

2017 outlook. A majority of the

managers attending the

conference attended with plans

for Risk Retention and expected to

issue compliant deals in the first

quarter of 2017. Despite the

positive outlook, most managers

expect defaults in the Energy

sector and in some Retail areas

that have been displaced by

online shopping.

The S&P/LSTA Leveraged Loan

Index returned 1.16% in

December and 2.26% in the fourth

quarter. In 2016 the Index

achieved its second best

performance on record returning

10.16%, the highest since 2009.

Total returns for loans rated CCC

and below were more than 4

times the returns for loans rated B

for December and the quarter.

CCCs and below returned 4.31% in

December and 8.73% in the

quarter vs. single-Bs which

returned 1.09% in December and

2.18% in the quarter. However,

loans rated CCC and below only

represent approximately 7% of

the Index by market value and

Source: S&P Capital IQ

U.S. CLO Monthly Issuance January 2016— December 2016

Collateralized Loan Obligations

Investment Grade Credit

0

5

10

15

20

25

-

2.00

4.00

6.00

8.00

10.00

12.00

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec

-16

# o

f D

eal

s

Issu

ance

($

Bill

ion

s)

Number of Deals

Issuance

Bank Loans

6

Quarterly Commentary 12/31/16

Quarterly Commentary

thus only contributed

approximately 30 bps in

December and 60 bps in the

quarter to the overall total return

of the Index.

Performance by sector was

relatively uniform with most

sectors matching or marginally

underperforming the Index with a

few notable exceptions. Oil & Gas

and Metals & Mining led the pack

by wide margins, returning

14.20% and 12.53%, respectively,

during the quarter. Consumer-

related sectors generally

underperformed with Retailers,

Beverage & Tobacco & Food/Drug

Retailers returning -0.87%, -0.20%

and 0.61%, respectively, during

the quarter.

The weighted average bid price of

the Index rose $0.99 to $98.08

during the month, up $2.96 in the

quarter. At the end of the year

67% of the Index was bid at or

above par, the highest level since

the first quarter 2014. Yields

across the Index fell in December

and the fourth quarter. The

weighted average yield-to-

maturity (YTM), excluding

defaulted loans, fell 34 bps to

5.18% over the quarter.

Technicals have been supportive

for loans for most of the year and

especially over the past two

quarters. New demand for

leverage loans increased for the

sixth consecutive month in

December to $14.62 billion, up

from $13.49 billion in November.

During the quarter, demand for

leverage loans increased to $38.86

billion, comprised of $25.3 billion

of CLO issuance and $13.5 billion

of prime fund flows. The new

issue market was active with

$19.35 billion of institutional loan

volume in December, bringing

fourth quarter institutional loan

volume to $101 billion. Given that

refinancing activity made up

nearly 40% of new issue volume in

the quarter, the net increase in

par outstanding for the Index was

$8.95 billion in December and

$25.32 billion in the fourth

quarter.

The lagging 12-month issuer

weighted default rate fell slightly

to 2.06% in December, down from

2.11% in November and 2.23% at

the end of last quarter, but is up

from 1.08% a year ago.

In December, high-yield (HY)

bonds responded well to higher

oil prices, supported by the

Organization of Petroleum

Exporting Countries’ (OPEC) late

November agreement, as well as

the possibility of pro-business U.S.

legislative action in 2017. The Citi

High-Yield Cash-Pay Capped

Index’s monthly gain of 1.9% was

driven by lower-rated assets,

along with the Energy, Healthcare

and Aerospace sectors.

In December, high-yield (HY)

bonds responded well to higher

oil prices, supported by the

Organization of Petroleum

Exporting Countries’ (OPEC) late

November agreement, as well as

the possibility of pro-business U.S.

legislative action in 2017. The Citi

High Yield

U.S. Corporate High Yield Option-Adjusted Spread March 31, 2006 to December 31, 2016

Source: Barclays Live

1.2

501.2

1,001.2

1,501.2

2,001.2

2,501.2

12/30/2016409.0

7

Quarterly Commentary 12/31/16

Quarterly Commentary

High-Yield Cash-Pay Capped

Index’s monthly gain of 1.9% was

driven by lower-rated assets,

along with the Energy, Healthcare

and Aerospace sectors.

These themes generally held true

for the fourth quarter and full-

year 2016 as the Index returned

1.8% and 17.3%, respectively, with

CCC-rated assets significantly

outperforming the B- and BB-

rated categories. Commodity-

driven sectors also outperformed

as this 2016’s returns represented

a snapback from the previous two

years’ weakness in Metals, Mining

and Energy prices. The notable

underperformer in 2016 was

Pharmaceuticals, an industry

dominated by a few large HY

names that have been in the

political crosshairs.

According to Barclays, HY new

issuance volume totaled $216

billion in 2016, representing the

fourth consecutive YoY decrease

since a record-setting $344 billion

priced in 2012. When backing out

bond redemptions, net new bond

supply in 2016 was -$64 billion.

This net number has also been

shrinking since 2012, which is a

positive supply-demand technical

within HY.

J.P. Morgan notes that 62

companies defaulted in 2016 with

debt totaling $59.3 billion, 57%

higher than in 2015. This year’s

default volume ranks as the fifth

highest annual total on record.

Notably, more than half of 2016’s

default volume occurred in the

first quarter, and commodity-

driven industries accounted for

over 80% of activity.

As treasury bonds have sold-off

since the U.S. election, HY spreads

have tightened to offset rising

rates due to positive sentiment

regarding economic prospects and

fiscal stimulus. The most recent

economic data points have also

been stronger, but we are

watching for more fundamental

economic follow-through as the

year unfolds. In light of below-

average credit spreads combined

with above-average financial

leverage across HY issuers, any

softening of economic data,

corporate profits, oil prices or

political sentiment could cause

spreads to widen.

In December 2016 the broad

commodity market rallied by

1.76% and 4.67%, as measured by

the BCOM and S&P GSCI,

respectively. During the quarter

the broad commodity market

rallied by 2.55% and 5.65%, as

measured by the Bloomberg

Commodity Index (BCOM) and

S&P Goldman Sachs Commodity

Index (GSCI), respectively.

The commodity sectors with

positive returns in the fourth

quarter were Energy, as measured

by the S&P GSCI Energy, Livestock,

as measured by the S&P GSCI

Livestock, and Industrial Metals,

as measured by the S&P GSCI

Industrial Metals, with returns of

8.54%, 18.29% and 5.56%,

respectively. The commodity

sectors with negative returns in

the fourth quarter were Precious

Metals, as measured by the S&P

GSCI Precious Metals and

Agriculture, as measured by the

S&P GSCI Agriculture with returns

of -13.33% and -3.25%,

respectively.

In December the Energy and

Livestock sectors rallied with

returns of 8.32% and 7.47%. The

worst performing sector in

December was Industrial Metals

followed by Precious Metals and

Agriculture, with returns of

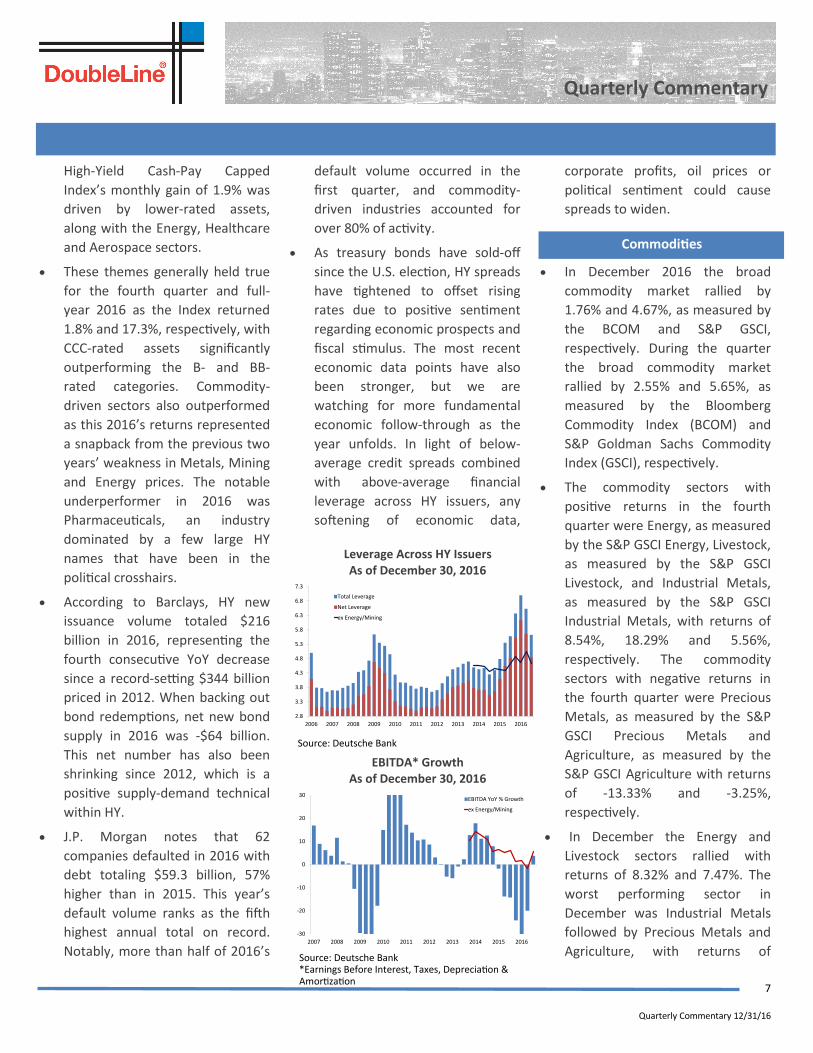

Leverage Across HY Issuers As of December 30, 2016

Source: Deutsche Bank *Earnings Before Interest, Taxes, Depreciation & Amortization

EBITDA* Growth As of December 30, 2016

Source: Deutsche Bank

-30

-20

-10

0

10

20

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

EBITDA YoY % Growth

ex Energy/Mining

2.8

3.3

3.8

4.3

4.8

5.3

5.8

6.3

6.8

7.3

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total Leverage

Net Leverage

ex Energy/Mining

Commodities

8

Quarterly Commentary 12/31/16

Quarterly Commentary

-5.43%, -2.02% and -1.34%,

respectively.

Emerging Market (EM) corporate

and sovereign external

performance was positive during

the month on improving

sentiment after a steep decline in

November following the U.S.

Presidential election.

The JP Morgan EMBI Global

Diversified Index returned 10.15%

in 2016, its best annual

performance since 2012, driven

primarily by spread performance,

with Latin America contributing to

almost half of the total return.

We expect to see fairly robust EM

sovereign and corporate gross

issuance in 2017, continuing the

trend from 2016, which could

provide the opportunity to

selectively add to issuers coming

with a new issue premium.

In 2017, headwinds could arise

from rising UST yields, a stronger

USD, increased protectionism and

trade barriers, potentially pivotal

elections in Europe, and policy risk

stemming from the U.S., Europe

and China.

December saw a more measured

continuation of the broad

reflationary themes that had

intensified in November in the

aftermath of the U.S. election with

a stronger USD and higher global

government yields.

The Italian referendum boosted

European periphery yields higher

as the Prime Minister, Matteo

Renzi, stepped down after his

planned reforms were soundly

rejected by a popular vote.

European government bond

markets also focused on the limits

to central bank monetary policy

accommodation. The European

Central Bank (ECB) extended its

quantitative easing (QE) program

to December 2017, but reduced

the monthly pace of bond

purchases to €60 billion¹ from €80

billion², which was interpreted by

some market participants as a

“tapering” or “trimming” of QE.

Developed market currencies sold

off this month. The Euro fell to its

lowest level against the USD in

almost 14 years with news of a

government rescue package for

the Italian banking sector, and an

attack on a Christmas market in

Berlin. Market participants also

looked ahead to pivotal elections

in Europe next year in France, the

Netherlands, Germany, and

potentially Italy.

The Japanese Yen also sold off

over the month, driven by the

yield differential between

Treasuries and benchmark ten-

year Japanese government bonds

(JGB).

Trading and new issue volume

were strong going into year-

end. As rates steadily rose during

December, issuers sought to price

transactions prior to the New

Year. From a sector perspective,

corporate issues in the Power and

Energy (refining) sectors

dominated while structured

JP Morgan Emerging Markets Bond Index Performance December 31, 2015 to December 31, 2016

Source: JP Morgan

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

JPM Emerging Markets Bond Global Diversified Index (EMBI)

JPM Corporate Emerging Markets Bond Broad Diversified Index (CEMBI)

JPM Government Bond Emerging Markets Broad Diversified Index (GBI EM)

International Sovereign

Emerging Markets

Infrastructure

1. Approximately $63.1 billion USD as of December 31, 2016 2. Approximately $84.2 billion USD as of December 31, 2016

9

Quarterly Commentary 12/31/16

Quarterly Commentary

products issues mostly focused on

clean energy and aircraft

securitizations. Spreads were

volatile with spreads tightening

early in the month and widening

modestly as year-end

approached. Asset-Backed

Securities (ABS) securitizations

saw strong demand throughout

the year, but with rising rates and

the desire for many market

participants to retain larger cash

positions, spreads also widened.

Mr. Trump identified

infrastructure spending as one of

his highest priorities and has

further supported this agenda by

nominating members to his

cabinet with significant expertise

in energy and infrastructure

financing.

Against this backdrop, financing

for infrastructure assets remained

robust. Rising interest rates

dampened issuance volume in

October, while November and

December witnessed robust

primary issuance as issuers looked

to lock in financing before year

end. Debt issues related to

utilities, midstream energy assets,

transportation and renewables

were met with fervent investor

demand.

While not as pronounced as what

investors experienced during the

first quarter, spread volatility

reappeared in the fourth quarter.

October saw marginal spread

widening in the U.S. Utility and

Transport sectors, only to tighten

back in November and December.

EM infrastructure issues saw the

opposite occur. ABS issues were

the least volatile, showing only

marginal spread movement during

the fourth quarter.

While the S&P 500’s advance

stalled in the third quarter, the

market quickly discounted the

prospect of more inflationary and

expansionary fiscal policies, as

well as a more business-friendly

regulatory environment, with the

election of Trump. Between

Election Day and the end of 2016,

the S&P 500 Index gained

approximately 5% to end the year

up almost 12%. We believe it

would be a mistake to attribute all

of the market’s actions in the last

two months of the year to the

outcome of the Presidential

election. Looking within the

market, many of the November

and December trends were an

acceleration of trends that were

already well established since the

summer. Specifically, the

bottoming of inflation

expectations and 10-year UST

yields in July saw a rotation in the

market. Formerly strong-

performing and defensive “yield-

proxy” sectors such as Consumer

Staples and Utilities began to

underperform. At the same time,

more cyclical sectors such as

Energy and Technology began

outperforming the broader index,

as did Financial Services –

perceived as a beneficiary of

higher rates and a steeper yield

curve.

These sector-level trends gained

momentum following the

election. Financial Services was

the leadership sector, regarded as

the greatest beneficiary from a

steeper yield-curve and less

regulation. The reaction of

Healthcare stocks was somewhat

counter-intuitive: the sector

initially rallied following the

election, only to sell off on the

realization that the shape of the

next round of healthcare policy

reform is very uncertain.

With YoY earnings expected to

grow in the fourth quarter, the

“earnings recession” is at an end.

Despite this, consensus estimates

for fourth quarter and 2017

earnings continued to fall through

the quarter and, in our opinion,

continue to be fairly optimistic.

As we enter 2017, we remain

cautious on the market. The

market seems to have quickly

concluded that the new

administration’s policies will

simultaneously be meritorious,

quickly passed into law, and

successful. Even if these

assumptions are true – a big “if” -

progress is rarely linear. After all,

it took Reagan two years to pass

tax reform. History teaches that

sometimes the underlying

momentum of the business cycle

and global economy can

temporarily overtake the best

conceived and executed of

policies.

U.S. Equities

10

Quarterly Commentary 12/31/16

Quarterly Commentary

Global equities, as measured by

the Morgan Stanley Capital

International All-Country World

Index (MSCI ACWI), returned

2.18% in December and 1.30% for

the quarter. European equities

outperformed the broader market

in December with the Eurostoxx

50 returning 7.94%. For the

quarter, European equities posted

positive returns with the

Eurostoxx 50 up 10.05%, DAX up

9.23%, CAC up 9.72%, FTSEMIB up

17.64% and IBEX up 7.83%. The

European banking sector

continued to recover in the fourth

quarter with the Eurostoxx Banks

Index returning 27.77%. UK

equities continued to rally during

the quarter with the FTSE 100 up

4.34%.

Asian equities were mixed in

December with the Nikkei

returning 4.70%, Shanghai

Composite returning -4.73%, and

Kospi returning 2.19%. For the

quarter, Asian equities were

mixed, with the Nikkei up 16.53%,

Shanghai Composite up 3.06%,

and Kospi returning -

0.82%. Weaker Japanese Yen

supported Japanese equities.

EM equities were little changed in

December with the MSCI EM

Index returning 0.05%, but posted

a -4.74% return in the fourth

quarter. Russian equities rallied in

December with the MSCI Russia

Index up 12.26% and ending the

quarter up 18.39%. Brazilian

equities, as measured by the

Bovespa, declined -2.71% in

December ending the quarter

3.19%.

Global Equities

11

Quarterly Commentary 12/31/16

Definitions

Bloomberg Barclays U.S. Corporate Index -An index designed to be a broad-based measure of the global investment-grade, fixed rate, fixed income corporate markets

outside the United States.

Bloomberg Barclays U.S. Credit Index—The US Credit component of the U.S. Government/Credit Index. This index consists of publically-issued U.S. corporate and

specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered. The US

Credit Index is the same as the former US Corporate Investment Grade Index.

Bloomberg Barclays U.S. Government Index - An index that measures the performance of all public U.S. government obligations with remaining maturities of one year

or more.

Bloomberg Commodity Index (BCOM) - An index calculated on an excess return basis that reflects commodity futures price movements. The index rebalances annually

weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector and group level for diversification. Roll period

typically occurs from 6th-10th business day based on the roll schedule.

Citi High-Yield Cash-Pay Capped Index -This index represents the cash-pay securities of the Citigroup High-Yield Market Capped Index, which represents a modified

version of the High Yield Market Index by delaying the entry of fallen angel issues and capping the par value of individual issuers at $5 billion par amount outstanding.

Cotation Assistee en Continu 40 (CAC 40) - The CAC 40 Index which is a French stock market index. It tracks 40 of the largest French stocks on the Paris Bourse, or

stock exchange.

Consumer Price Index (CPI) - A measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, fo od and

medical care. The CPI is calculated by taking price changes for each item in the predetermined basket of goods and averaging them; the goods are weighted according to

their importance. Changes in CPI are used to assess price changes associated with the cost of living.

Credit Suisse High Yield Index - The index reflects a trader-priced portfolio constructed to mirror the global high-yield debt market.

Deutsche Borse AG German Stock Index (DAX) - The German stock index, which represents 30 of the largest and most liquid German companies that trade on the

Frankfurt Exchange.

Dow Jones Industrial Average (DJIA) - A price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq.

ECB Corporate Sector Purchase Program - A program established by the European Central Bank with the goal of strengthening financing conditions. Six national

central banks will coordinate to purchase IG Euro-denominated bonds issued by non-bank corporations established in the euro area.

Eurostoxx 50 Index - A stock index of Eurozone stocks designed by STOXX, an index provider owned by Deutsche Borse Group and SIX group, with the goal of

providing a blue-chip representation of Supersector leaders in the Eurozone.

Financial Times Stock Exchange 100 (FTSE 100) - A capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange.

Financial Times Stock Exchange Milano Italia Borsa (FTSE MIB) - The benchmark stock market index for the Borsa Italiana, the Italian national stock exchange, which

superseded the MIB-30 in September 2004. The index consists of the 40 most-traded stock classes on the exchange.

Foreign Direct Investment - An investment made in business interests in a country other than the company or individual’s residing country through set up of business

operations or acquiring business assets in a foreign company.

S&P Goldman Sachs Commodity Index (GSCI) - Standard & Poor’s Goldman Sachs Commodity Index, or GSCI, is a composite index of commodity sector returns which

represents a broadly diversified, unleveraged, long-only position in commodity futures. The index’s components qualify for inclusion in the index based on liquidity

measures and are weighted in relation to their global production levels, making the Index a valuable economic indicator and commodities market benchmark.

Hang Seng Index - A free-float capitalization-weighted index of a selection of companies from the Stock Exchange of Hong Kong. The components of the index are divided

into four subindices: Commerce and Industry, Finance, Utilities, and Properties.

Ibovespa - This accumulation index represents the present value of a portfolio begun on 2 January 1968, with a starting value of 100 and taking into account share price

increases plus the reinvestment of all dividends, subscription rights and bonus stocks received.

Indice Bursatil Espanol (IBEX) - The official index of the Spanish Continuous Market. The index is comprised of the 35 most liquid stocks traded on the Continuous

market. It is calculated, supervised and published by the Sociedad de Bolsas.

JP Morgan Corporate Emerging Markets Bond Broad Diversified Index (CEMBI) -This index is a market capitalization weighted index consisting of US-denominated

Emerging Market corporate bonds. It is a liquid global corporate benchmark representing Asia, Latin America, Europe and the Middle East/Africa.

An investment cannot be made in an index.

12

Quarterly Commentary 12/31/16

Definitions

JP Morgan Emerging Markets Bond Global Diversified Index (EMBI) -This index is uniquely-weighted version of the EMBI Global. It limits the weights of those index

countries with larger debt stocks by only including specified portions of these countries’ eligible current face amounts of debt outstanding. The countries covered in the

EMBI Global Diversified are identical to those covered by EMBI Global.

JP Morgan Government Bond Emerging Markets Broad Diversified Index (GBI EM) -This index is the first comprehensive, global local Emerging Markets index, and

consists of regularly traded, liquid fixed-rate, domestic currency government bonds to which international investors can gain exposure.

Korea Composite Stock Price Index (Kospi) - A market capitalization weighted index of all common stocks traded on the Stock Market Division—previously, Korea

Stock Exchange—of the Korea Exchange. It is the representative stock market index of South Korea, similar to the Dow Jones Industrial Average or S&P 500 in the United

States.

London Interbank Offered Rate (LIBOR) - An indicative average interest rate at which a selection of banks known as the panel banks are prepared to lend one another unsecured funds on the London money market.

Moody’s/RCA Commercial Property Price Indices (CPPI) National All-Property Composite Index - The Moody's/RCA Commercial Property Price Index (CPPI) describes various non-residential property types for the U.S. (10 monthly series from 2000). The Moody's/RCA Commercial Property Price Index is a periodic same-property round-trip investment price change index of the U.S. commercial investment property market. The dataset contains 20 monthly indicators.

Morgan Stanley Capital International All Country World Index (MSCI ACWI) -A market-capitalization-weighted index designed to provide a broad measure of stock

performance throughout the world, including both developed and emerging markets.

MSCI Emerging Markets (MSCI EM)- An index that covers 23 Emerging Market countries and is designed to capture the large and mid-cap representation across those

countries.

MSCI Emerging Markets Latin America - A subindex of that MSCI Emerging Markets Index that covers 5 EM countries in Latin America and is designed to capture large

and mid cap representation from 119 constituents.

MSCI Russia Index - An index that includes 85% of the free float-adjusted market capitalization of Russia. It is designed to measure the performance of the large and

midcap segments of the Russian market.

NASDAQ - A stock market index of the common stocks and similar securities (e.g. ADRs, tracking stocks, limited partnership interests) listed on the NASDAQ stock

market with over 3,000 components. This index is highly followed in the U.S. as an indicator of the performance of stocks of technology companies and growth

companies. Since both U.S. and non-U.S. companies are listed on the NASDAQ stock market, the index is not exclusively a U.S. index.

Nikkei 225 Index - A price-weighted index comprised of Japan's top 225 blue-chip companies on the Tokyo Stock Exchange. The Nikkei is equivalent to the Dow Jones

Industrial Average Index in the U.S.

Russell 2000 Index - A subset of the Russell 3000 Index representing approximately10% of the total market capitalization and measuring the perform ance of the small-

cap segment of the U.S. equity universe.

Shanghai Composite Index - A capitalization-weighted index that tracks the daily performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The

index was developed on December 19, 1990 with a base value of 100.

S&P Goldman Sachs Commodity Index (GSCI) - An index that measures investment in the commodity markets and commodity market performance over time.

S&P 500 Index - Standard & Poor’s US 500 Index, a capitalized-weighted index of 500 stocks.

S&P/LSTA Leveraged Loan Index - An index designed to track the market-weighted performance of the largest institutional leveraged loans based on the market

weightings, spreads and interest payments.

World Interest Rate Probability (WIRP) - A Bloomberg function used as a measure of the likelihood of a Fed rate move using the Fed Funds futures and options

contracts.

An investment cannot be made in an index.

13

Quarterly Commentary 12/31/16

Disclaimers

Important Information Regarding This Report

Issue selection processes and tools illustrated throughout this presentation are samples and may be modified periodically. Such charts are not the only tools used by the

investment teams, are extremely sophisticated, may not always produce the intended results and are not intended for use by non-professionals.

DoubleLine has no obligation to provide revised assessments in the event of changed circumstances. While we have gathered this information from sources believed to

be reliable, DoubleLine cannot guarantee the accuracy of the information provided. Securities discussed are not recommendations and are presented as examples of

issue selection or portfolio management processes. They have been picked for comparison or illustration purposes only. No security presented within is either offered for

sale or purchase. DoubleLine reserves the right to change its investment perspective and outlook, as well as portfolio construction, without notice as market conditions

dictate or as additional information becomes available. This material may include statements that constitute “forward-looking statements” under the U.S. securities laws.

Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to a client’s account, or market

or regulatory developments.

Ratings shown for various indices reflect the average for the indices. Such ratings and indices are created independently of DoubleLine and are subject to change without notice.

Important Information Regarding Risk Factors

Investment strategies may not achieve the desired results due to implementation lag, other timing factors, portfolio management decision-making, economic or market

conditions or other unanticipated factors. The views and forecasts expressed in this material are as of the date indicated, are subject to change without notice, may not

come to pass and do not represent a recommendation or offer of any particular security, strategy, or investment. Past performance (whether of DoubleLine or any index

illustrated in this presentation) is no guarantee of future results. You cannot invest in an index.

Important Information Regarding DoubleLine

In preparing the client reports (and in managing the portfolios), DoubleLine and its vendors price separate account portfolio securities using various sources, including

independent pricing services and fair value processes such as benchmarking.

To receive a complimentary copy of DoubleLine’s current Form ADV (which contains important additional disclosure information), a copy of the DoubleLine’s proxy voting

policies and procedures, or to obtain additional information on DoubleLine’s proxy voting decisions, please contact DoubleLine’s Client Services.

Important Information Regarding DoubleLine’s Investment Style

DoubleLine seeks to maximize investment results consistent with our interpretation of client guidelines and investment mandate. While DoubleLine seeks to maximize

returns for our clients consistent with guidelines, DoubleLine cannot guarantee that DoubleLine will outperform a client's specified benchmark. Additionally, the nature

of portfolio diversification implies that certain holdings and sectors in a client's portfolio may be rising in price while others are falling; or, that some issues and sectors

are outperforming while others are underperforming. Such out or underperformance can be the result of many factors, such as but not limited to duration/interest rate

exposure, yield curve exposure, bond sector exposure, or news or rumors specific to a single name.

DoubleLine is an active manager and will adjust the composition of client’s portfolios consistent with our investment team’s judgment concerning market conditions and

any particular security. The construction of DoubleLine portfolios may differ substantially from the construction of any of a variety of bond market indices. As such, a

DoubleLine portfolio has the potential to underperform or outperform a bond market index. Since markets can remain inefficiently priced for long periods, DoubleLine’s

performance is properly assessed over a full multi-year market cycle.

Important Information Regarding Client Responsibilities

Clients are requested to carefully review all portfolio holdings and strategies, including by comparing the custodial statement to any statements received from

DoubleLine. Clients should promptly inform DoubleLine of any potential or perceived policy or guideline inconsistencies. In particular, DoubleLine understands that

guideline enabling language is subject to interpretation and DoubleLine strongly encourages clients to express any contrasting interpretation as soon as practical. Clients

are also requested to notify DoubleLine of any updates to Client’s organization, such as (but not limited to) adding affiliates (including broker dealer affiliates), issuing

additional securities, name changes, mergers or other alterations to Client’s legal structure.

DoubleLine® is a registered trademark of DoubleLine Capital LP.

© 2017 DoubleLine Capital LP