fouad basrawi-m00466885

TRANSCRIPT

Declaration of Originality

I hereby declare that this project is entirely my own work and that any additional sources of

information have been duly cited.

I hereby declare that any internet sources, published or unpublished works from which I have

quoted or drawn reference have been referenced fully in the text and in the contents list. I

understand that failure to do this will result in a failure of this project due to Plagiarism.

I understand I may be called for a viva and if so must attend. I acknowledge that is my

responsibility to check whether I am required to attend and that I will be available during the

viva period.

Signed …………………………………………………………….

Date …………………………………………………...................

Name of Supervisor ………………………………………………..

1

The Valuable Impact of the Balanced Scorecard on Saudi Arabian

Companies

Fouad Basrawi

M00466885

Middlesex University Business School

Msc Financial Management

2014/2015

Supervisor: Dr. Jatin Pancholi

6th May, 2015

2

Abstract:

This research aims to represent an insightful understanding about the beneficial impacts of

implementing the BSC through Saudi Arabian companies. From an economic perspective,

due to its fast and consistent growth, Saudi Arabia is considered by many to be one of the top

emerging economies. This paper is part of broader research seeking to know whether Saudi

Arabian companies are aware of the BSC concept or they apply other techniques to measure

its performance. Questionnaire and telephone interview were carried on seven companies, in

order to provide understanding into the degree of implementation in addition to the beneficial

issues that the BSC has bring for the companies. The results showed that slightly few

companies are aware of the BSC approach; however, the majority of the companies are not

considering or currently using the BSC.

Acknowledgment:

I would like to thank my family for the opportunity and support they offered me for

undergoing my Master’s Degree and in successfully completing this dissertation.

I also would like to thank my supervisor Dr. Jatin Pancholi for his feedback and assistance

that had smoothed the work for me.

I give Special thanks for my colleagues in Saudi Arabia that supported me allocating the right

contacts for the company being surveyed.

Finally I would like to thank the Saudi Cultural bureau for the financial support and

assistance they offered me in completing my studying years.

3

Contents:

Title Page Number

Title Page......................................................................................................2

Abstract ...........................…………………………………………………...3

Acknowledgment ...................................................................................…...3

CHAPTER ONE: INTRODUCTION………………………………….….8

1.1 Introduction………………………………………………………….......8

1.2 Context and Significance of the Study.....................................................9

1.3 Research Question ...…………........……………………………….…...10

1.4 Research Objectives……………………………………………………. 11

1.5 Limitation of the Study………………………………………………..….11

1.6 Layout of the Study...................................................................................12

CHAPTER TWO: Literature Review and Analytical Framework ...............13

2.1 Introduction……………………………………………………………......13

2.2 Balanced Scorecard Concept…………………………………………...….14

2.3 Balanced scorecard promise........................................................................16

2.4 The cause and effect of the BSC’s four perspectives...................................17

4

Title Page Number

2.5 Research method and limitation of the BSC …...................................................18

2.6 Companies performance within BSC ..........…………………………..…….......19

2.7 Implementation process of the BSC.....................................................................21

2.8 Summary............................................................................................................. .31

CHAPTER THREE: Research Methodology, Research Methods, and Data Collection

……………….............................................................................................................31

3.1 Introduction…………………………………………………………….................31

3. 2 Research Methodology ……………………………...............................…..........32

3.3 Research Methods….………………………………………………...….…..........33

3.4 Research Design……………………………………………….......…...……........35

3.5 Data Sources and data Collection …………………………………...………........35

CHAPTER FOUR: Discussion and Analysis.......................................…………..…36

4.1 Jude Water Case Study ……………………………………………………....…...37

4.1.2 Jude Water analysis .....................................................…..................................37

4.2.1 Introduction HAYAT BUILDING MATERIAL COMPANY AND UNITECH

…………………………………………………..........................................................38

4.2.2 Analysis of the group .....................…………………………….........................39

5

4.2.3 Implementation of the BSC at IKK group................................................ 39

4.3.1 Omix Introduction ….......................................................…………......................40

4.3.2 Omix Analysis …………….......................................…………........................…41

4.3,3 Implementation of the BSC at Omix …………........………….......................41

4.4.1. Introduction Al Yaseen Agri ..................…………………......….....................42

4.4.2. Analysis of Al Yaseen Agri ……………………………………….......................43

4.4.3. Implementation of the BSC at Al Yaseen Agri ………………...….....................43

4.5.1. Introduction Jarir Book Store …………………………………….......................44

4.5.2. Jarir Analysis …………………………………………………….......................45

4.5.3. Implementation of BSC at Jarir Book Store.........................................................45

4.6.1. Introduction United Cooperative Assurance.......................................................46

4.6.2. United Cooperative Assurance Analysis ..............................................................47

4.6.3. Implementation of BSC at United Cooperative Assurance...................................47

4.7.1 Introduction Bahri Company .................................................................................48

4.7.2 Bahri Company Analysis........................................................................................48

4.7.3 Implementation of BSC at Bahri Company ............................................................49

6

CHAPTER FIVE: Analysis of Evidence from the case Studies ….........................52

5.1 Introduction ........................................................................................................52

5.2. Analysis of Data.................................................................................................53

Chapter 6: Conclusions and Recommendations ....................................................54

6.1 Summary............................................................................................................54

References.............................................................................................................56

Appendix.................................................................................................................59

Title Page Number

List of Figures

Figure 2-1 Balanced Scorecard Strategy Map…......................…...............………40

Figure 2-2 Balanced Scorecard Quadrants……………………………..................42

Figure 2-3 Examples of Quadrants Objectives and Measures…………….……….42

Figure 2-4 Numbers of Voyages performed by Vlcc in 2013 VS 2012...................44

Figure 2-5 Break Down of VLCCs Voyages by route 2012 VS 2013..............……44

Figure 2-6 Oil Transportation Voyages During 2013...............................................44

7

Chapter 1: Introduction

This section highlights the research content which is about the valuable impact of

implementing the balanced scorecard (BSC) in Saudi Arabian companies. Hence, it has a

brief overview of the research as well as the main subject selected for the study. This section

starts by stating a summarized background for the economical environment of Saudi Arabia.

Moving on, it will discuss the context and significance of the study, followed by the research

question. After that, it will identify the research objective. Bearing this in mind, the paper

will also discuss the limitations of the research and the final section will draw on the main

elements within each chapter of this research paper.

1.1. Introduction

The 2008 financial crisis had left long term influence on the world economy up till present,

affecting the stock markets, MNC’s and other various sized enterprises that had suffered a

great loss and economic deficit. As a consequence of this dreaded event, a high rise in

unemployment rate, inflation rate, poverty as well as less balance trade activities has been

witnessed. The Arabian Gulf and Egypt are the most Arabian countries which were affected

by the crisis since they have a direct contact with the world economy. One of the main

reasons behind the failure of the organizations is that they were structured in a very weak

frame work that involved in lack of management and monitoring that had resulted in its

collapsing from facing any economic deficiency. Maintaining the good performance and

structure of organization is not an easy job as individual believe. It must be linked by

developed strategies and measures which will have a direct influence on the organization in

both period short and long run. Most organization possesses a well-developed and innovative

8

strategies but had failed in implementing them accurately which resulted in effecting its

performance negatively.

The kingdom of Saudi Arabia is considered as the largest oil producer and exporter in the

world, where a large proportion of its income is derived from the oil industry. The country

has witnessed a high economic growth by diversifying its investments and subsidizations into

different field in the Kingdom. Such investments had led to develop a very solid and active

market structure which had a very good impacts for both group who are interested in

investing in the country whether the local citizen or foreign investors. It’s concordant with

facts that Saudi Arabia economy is flourishing and implementing high efforts to decrease

some of the factors that have a direct influence on its economy and reputation.

1.2 Context and Significance of the Study

The developed and followed strategies implemented by the company play a very

significance role in leading the company to its success or fiasco. As it has been noticed

recently, the high competitiveness among organizations will state the necessity of choosing

the most suitable strategies along with implementing them which has been considered as the

ultimate challenge. The balance scorecard was created by Robert Kaplan and David Norton in

1992, which has earned a great deal of popularity from different corporations, is also

considered one of important and popular tools employed by the organizations which

contribute in allocating the link between the alternative options of strategy along with its

implementation process. Applied by several different organizations such as government’s

business industries and non-profit organization the balance scorecard was able to prove the

9

improvement that were engaged in different areas, such areas include: the organizational

communications, fitting the business activities with the vision and the strategy of the

organization and, monitoring the total performance of the organization in parallel with their

objectives. The balance scorecard apply four various approaches to examine the total

performance of the organization along with helping it meet its objectives. These approaches

include: the financial perspective, the growth and learning perspective, the internal process

perspective, and the customer perspective. By implementing and aligning with those

approaches it will defiantly contribute for a better performance measurement for the

organizations.

1.3 Research Question

The present debate of this research will address some questions concerning the issue of

whether implementing the balance scorecard (BSC) will generate positive influences on the

company performance. The main research question for this study focuses on:

1. To what extent the BSC benefits Saudi Arabian companies in their management in

order to achieve more goals efficiently?

2. Is there a link between BSC and other performance indicators?

This study systematically reviews the data and tools for one of the significant key elements in

measuring organization performance which is known as the balance scorecard

10

1.4 Research Objectives

The main purpose of this research is to find out a result that can be linked with the research

objectives of the company. Following are the research objective for this thesis that needs to

be evaluated and the outcome may be found out.

1. What is the performance measurement methods implemented across organisation?

2. Are there any non financial methods to measure performance of the company?

3. What does the company and employees know about the balance score card?

4. To what extent the company has implemented the balance score card in its organisation?

5. If there is any balance score card, is it linked to the key strategy of the company?

1.5 Limitations of the study

The researcher used primary and also some secondary data in such way that each information

source should complement each other to produce an effective result. Every possible step has

been taken to achieve the desired result from this study. However, there are certain

limitations with this study which are as follows:

- The researcher could possibly have unwittingly acted in a biased manner during the

collection of data

- It was very time consuming to collect a large data sample by selecting organisations

in Saudi Arabia

- The number of organisations selected for this research may not be truly representative

of Saudi industry

11

- The researcher didn’t use any sampling techniques for this study when selecting the

data

- The organisations studied in this research were mostly small and private where

Balanced Scorecards have not been implemented

- The case study for this research is not truly representative of the different industrial

sectors found across the entirety of Saudi Arabia

- The researcher possibly placed too much emphasis on private limited companies

- Due to confidentiality reasons, some of the managers didn’t answer all of the

questions

- Questionnaire was not answered accordingly towards its target, because candidate do

not have any background about the BSC approach.

1.6 Layout of the study

The overall structure of the study takes the form of six chapters, including this

introductory chapter. Chapter Two begins by revealing a variety of literature review and

analytical framework. The third chapter is concerned with the methodology, data sources and

collection used in this study. The fourth section explains the discussions and findings of the

research. Chapter five will clarify the analysis of evidence from the case Studies

implementation of this tool on the Saudi Arabian companies. Chapter six will give a brief

conclusion and recommendation of this research.

12

Chapter 2: Literature Review and Analytical Framework

2.1. Introduction

The modern business environment is characterized by a high degree of

competitiveness between organizations and, therefore, choosing the right strategies and

implementing them properly has been a crucial challenge. Strategy is a fundamental key for

any organization to achieve a favourable outcome. It provides the organization with

convenient guiding principles and measures for the purpose of obtaining specific goals and

targets. MacCrimmon (1993, 115) explained that an organization ought to have planned a

symmetrical sequence flow of actions involving resource deployment in order to single out its

strategy. Pinnell (1986, 28) elucidated the purpose of setting objectives by the management in

order to identify the future position of the organization by specifying the required steps and

operations to achieve such objectives. Failure to understand the objective clearly will obstruct

the organization’s activities. Furthermore, planning may be effective in some parts of the

organization but failing in other parts (ibid). MacCrimmon (1993, 117) stated that strategy

aims to achieve objectives; therefore, regulating the executed actions is important. Ohmae

(1982, 92) clarified that strategies can be defined as the technique used by an organization to

distinguish itself positively from its competitors. All of this debate concerning the strategy

operations within organizations demonstrates how crucial is the role of corporate

management through planning, organizing and executing actions and decisions to proceed

towards the stated goals.

2.2. Balanced scorecard concept

13

The Balanced Scorecard (BSC) framework, developed by Robert Kaplan and David

Norton in 1992, is a tool that measures the drive performance of an organization as well as

translating strategic objectives into a set of performance measures (Kaplan and Norton, 1993,

P.2). Used by businesses, industries, governments and non-profit organizations, the BSC has

proved useful for delivering improvements in internal and external communications. The

BSC contributes to improving the organization’s vision, objectives, core values and

performance measures and is able to measure financial and nonfinancial metrics (Kulkarni,

Messina et al., 2008, 1166). According to Abu Sharma (2009, 2), the purpose of the BSC is to

direct, control and support an organization’s long-term strategy. Gumbus (2005, 619) stated

that the BSC also helps in aligning business activities with the vision and strategy of the

organization and in monitoring the overall performance of the organization with respect to

the strategic goals set. The BSC uses four different perspectives to consider the overall

performance of the organization and in helping it meet its strategic goals.

According to Kaplan and Norton (1996, P.56), the four perspectives of the BSC play

an important role in aligning different measures such as short- and long-term intentions, hard

and soft objectives, and between required outcomes and the performance drivers of those

outcomes. These perspectives include: the financial perspective, the growth and learning

perspective, the internal process perspective and the customer perspective. The need for

financial data is not disregarded by the BSC. Funding data must be accurate and timely in

order for any organization to function well because it is a key perspective for its success

(Sharma, 2009, pp.7-16). Financial measures will indicate whether the implementation and

execution of the organization’s strategies are working effectively to meet the required

outcome (Kaplan and Norton 2006, P.6). Financial perspective is divided into different

14

financial themes: growth strategies which aim to expand revenue scope and customer value,

whereas productivity strategies involve improving cost and asset utilization (Wu and Hung

2007, p.775). These themes can be employed with any of the business strategy events such as

growth, sustain and harvest depending on the intended objectives and situation (Kaplan and

Norton 1996, p.56). The second perspective involves training the employees and developing

cultural attitudes: the learning and growth perspective. Workers in the current climate must

be in continuous training and learning processes in order to deliver organizational self-

improvement. Kaplan and Norton (1996, p.64) postulated that learning and growth will

determine the framework that the organization must develop to create long-term growth and

improvement by employing the mean of human, information and organization capital (Wu

and Hung, 2007 p.775). Kaplan and Norton (1996, p.64) point out that organizations tend to

train their employees, develop better information technology and systems and align their

objectives in order to close the gap that is revealed from other perspectives between the

existing capabilities of the organization and the required performance to achieve certain

targets. The third perspective, which is the internal process, addresses which actions are most

effective for satisfying both customers and shareholders. According to Kaplan and Norton

(1996, p.62), the internal process perspective will outline some key aspects for executives to

focus on and which the organization must excel at which, in return, will increase customer

satisfaction and shareholder expectations. Norreklit (2000, p.67) believes that the internal

process perspective describes the organization’s operation for achieving the required targets

in order to continue growing and add value to customers. The internal process perspective

will deliver an integrated set of objectives and measures for both periods: the long-term

innovation cycle and short-term operation cycle (Kaplan and Norton, 1996, p.63). The fourth

element is the customer perspective. As Kaplan and Norton stated (1992, p.73), in this

perspective the BSC will require managers to render their mission statement for customer

15

service into specific measures that are concerned with the matter of customers. In other

words, the customer perspective will focus on the target market which must be determined

along with the organization’s policies in serving them. The way in which customers are

viewed is the key to success in this category. According to Kaplan and Norton (1996, p.59),

this perspective will direct managers in identifying the market and customer sector that the

business unit must excel in and measure business performance in such sectors. Moreover,

they emphasized the importance of measures included in this perspective that will result in

producing good outcomes. Such measures include customer retention, customer acquisition,

customer profitability and customer satisfaction. Kaplan and Norton (2006, p.6) stated that

when organizations tend to achieve the desired value and quality of their customer demand,

they will build customer loyalty and profit will then increase. Jones and Sasser (1995, P.90)

agreed with Kaplan and Norton, stating their beliefs based on validated research that there is

a relationship between an increase in customer loyalty and long-term financial performance.

Kaplan and Norton (1992, p.71) stated that managers should monitor the organization from

different areas using different instruments at the same time rather than depending on one

instrument which may work against their objectives.

2.3 Balanced scorecard promise

Accordong to Cokins (2010, P25) the BSC will assist managers to establish unity

between organizations’ objectives and strategies which is known as translating the vision

phase. In order to follow the designed framework, the statements must have a clear set of

objectives and measures that are being discussed by all senior managers around the long-term

drivers of success. The second approach of the balance scorecard is to control the strategy

above and under organisation and individual objectives. Normally, divisions are assessed

16

through their financial performances which are connected to short-term financial targets. The

BSC will help managers to ensure that all levels of the divisions are acknowledged including

the long-term master plan, managerial and individual purposes that are in line with it. The

third approach which is known as business planning enables organisations to merge their

work and financial plans. Most organisations today implement different strategic approaches

which tie up executive time, energy and resources and, as a result, managers will encounter

difficulties in assimilating to those strategic goals which lead to continual failure in

outcomes. However, when managers implement and follow the specific goals structured in

the BSC for assigning resources and setting priorities, they can engage and match only those

actions that best fit their long-term strategic goals. The fourth approach is known as strategic

learning. This approach involves analyzing feedback and assessing processes that concentrate

on whether the company, divisions and individuals have achieved their financial goals. The

BSC will operate as the centre management of the company where it can control short-term

results using three additional perspecctives. Furthermore, the scorecard empowers companies

to adjust strategies to reflect reality (ibid).

2.4. The cause and effect of the BSC’s four perspectives

Kaplan and Norton (1992,1996,2000,2002) ,explained that there is a cause and effect

relationship between the four perspectives. The subsequent chain assumes that the operations

of the organizational learning and growth are the operator of the internal and business process

activity. Therefore, the operations of the process are, in turn, the operators of the customer

perspective that are the operators of the financial measure activities. They also emphasize the

significance of mixed outcome measures (lag indicators) and performance drivers (lead

indicators) as a prerequisite for the success of the BSC. In contrast, Norreklit (2000, P.75)

argued that the cause and effect relationship demands a time lag between the cause and effect

17

because it uses them at the same time without taking into account any time lag which

indicates it has no time dimension. In spite of this, the effect of the operational activity will

occur at different times because the effects of different activities involve different timescales.

The absence of a time lag hinders both the difference and the relationship between operations

and development.

Furthermore, Norreklit (ibid) also proved that there is an absence of any casual

relationship between the perspectives. Donaldson (1984, P, 1831) agreed with Norreklit by

showing that the link between the growth and debt equity ratio can be described as a more

interdependent relationship. Laitinen (2003, P.314) stated that the four perspectives along

with their interrelationship complexity is causing the measures in the functional framework to

appear to be more unsteady to each other. Therefore, it will not be possible to deliver

evidence for how the organisational internal factors must be developed. Furthermore,

Norreklit (2000, P.81) observed that the BSC was not the proper strategic management tool

that Kaplan and Norton alleged, seeing that there were obstacles in confirming organizational

and social environmental implanting.

2.5 Research method and limitation of the BSC

According to Chang (2012), the BSC is researched in comparison with previous measuring

methods such as the Intellectual Capital method and the Enterprise Value method. It was

argued that the BSC model clarifies inadequate measures for past financial performance as

well as serving as a tool integrated with the company’s mission and vision. This gave the

BSC the lead in strategy measurement tools because it offers these two factors unlike the

other methods which offer inferior results with lower accuracies. Other alternative research

methods include the effects of the BSC on capital structure, on overall company performance

and its relation with intellectual capital.

18

Thomas Housel (1994, p.5) argued that “the BSC needs an objective measure” because the

BSC model is not objective. He also believed that it doesn’t allow for the necessary

comparison to rate or measure performance. This makes financial and accounting analysis

impossible unless the model results in an objective measure of value, considering the

financial perspective part useless. This shows a limitation because the model lacks a specific

objective measure. Kulkarni et al (2008: 1166-1171) stated that the subjectivity of measures

in the BSC model will lead to ambiguity in the vision statement given by the organization.

Objective measures must be taken in the third step of the BSC model in order to address this

lack of clarity. Kulkarni (ibid) effectively makes the same point as Housel, confirming the

fact that the real limitation and the research gaps in the issue of the BSC model are due to the

absence of objectivity in measurements. Other limitations include confidential data from

companies. This forbids researchers from comparing the different effects of the BSC on the

different types of companies which use it. The tool is also far more complex than other tools,

making it a difficult tool to analyze.

2.6 Companies performance within BSC

The empirical literature and reports have shown the performance of companies that started to

implement the BSC in their strategic plans. Howie and Macht (2009, p123) stated that highly

recognized private and public industries from different countries around the globe have

implemented the BSC since the year 2000 and had announced that the BSC management

system was a significant key for achieving certain valuable targets

Based on an executive management tools and trends survey (2009), the reports have shown

that the BSC ranks among the top ten most used tools. Moreover, a recent study by Crabtree

and Debusk (2008, P.10) indicated empirical and quantifiable indicators showing the

significant role of the BSC in creating organisational value by analyzing the share price

19

performance of more than 150 companies, both BSC users and nonusers, resembled by their

activity, size and other standards over the performance of the BSC users for three years post

espouse period. The results demonstrated that firms employing the BSC outperformed non-

user firms in three measures of performance: net assets, book to market ratio and market

value of equity. Moreover, Word (2009) focused on the effectiveness of the BSC when

technologies such as business intelligence and decision analytics contribute to the

performance of the BSC. This confirms that if business analytics can be aligned with those

applying the BSC, 57% will achieve breakthrough performance and this figure rises to 77%

when the BSC has been applied for three years or more. As such, an organisation will benefit

from a technological framework if it wishes to measure and maintain strategic performance.

The hall of fame report reflected the performance of numerous companies operating in

various activities that had implemented the BSC framework through their strategies. For

instance, Volkswagen (Palladium Group, 2010) showed a superior improvement in its

performance among different perspectives. They witnessed better employee engagement, an

increase in production and revenue volume and the number of repairs declined by 40%.

Megasalud, the Chilean healthcare network, (Palladium Group, 2010) experienced an

improvement in its performance after introducing the BSC where it succeeded in doubling

revenues, profit and return on equity, while decreasing the waiting time for clients in clinics

by half with fewer errors being made when calculating the fee paid to doctors. Another

example from the hall of fame is the first New Zealand-owned consumer bank, Kiwi Bank,

which experienced some difficulties such as rising costs and other issues which made it hard

to maintain growth. The BSC was able to deliver several successes for the institution from

different angles such as an increase in both the deposits and loan transactions of the bank,

more employee engagement in work activities, as well as improvement in Internet banking

usage (ibid).

20

Ramos and Caudeli (2013, P.20) studied introducing the BSC in the Spanish Port System.

Within five years the port managed to employ the BSC in all of its departments. The BSC

contributed to an increase in regional competitiveness by means of better strategy and

operations actions within the port agency. The economic and customer indicators were higher

than the previous year because the effects of BSC implementation increase over time.

Kaplan, Norton and Rugelsjoen (2010, P.13) explained the experience of two

companies (Solvay Pharmaceuticals and Quintiles) where in 2006 they upgraded their

partnership from a preferred partnership to true alliance. The BSC helped to identify the role

of each partner in relation to specific objectives. Implementing the BSC involved a joint

steering committee to oversee the creation of the map, scorecard and identify the alliance

objectives such as: living the alliance, collaboration, speed and process innovation, growth

and value for both parties. The alliance reduced total cycle time for clinical studies by

approximately 40% by bringing new products to the market more quickly, reducing costs,

registering programmes in a timelier manner, keeping everyone focused on delivering the

alliance strategy. Finally, it is possible to infer that both companies implemented unified BSC

techniques to create alliance value that will contribute to their future success.

2.7 Implementation process of the BSC

Kaplan & Norton in 1996 developed the balanced scorecard (BSC) after studying various

other introductory management theories including the following:

Management by objectives (Drucker, 1954)

Principles of management (Fayol, 1916)

Value disciplines (Treacy & Wiersema, 1995)

21

Theory Y (McGregor, 1960)

Hierarchy of needs (Maslow, 1962)

Open-book management (Case, 1995)

Leading change (Kotter, 1996)

As mentioned previously, the BSC is a widely accepted tool measuring the performance of

management. It is used across many different organizations has yielded positive benefits in its

initial time. A BSC technique is very productive for an organization’s current management

environment and flexible towards any dynamic environment where there is any change in

social or technological factors within the organization.

It’s necessary to make an analysis for the BSC in order to establish how successful the

techniques will be if implemented. Treacy (1995) concept of value disciplines can be

identified on how to implement the BSC across an organization successfully. An organization

can adopt such scorecards or bring itself closer to that category. After successful

acknowledgment these tools can be used to develop best practice scorecards in line with

different types of organization strategies.

Many researchers and experts have advocated the BSC as a powerful management concept

for developed countries. Many surveys have been performed on the successful

implementation of the BSC in many European countries including the UK (Francis and

Minchington, 2000), Denmark, Finland, Sweden and Norway (Kald and Nilsson, 2000) as

well as the USA (Silk 1998). The implementation process of the BSC is not a rule of thumb

that has a fixed formula but is far more flexible and can be adopted in many ways, especially

in a dynamic environment. It was clearly endorsed by Kaplan and Norton; the BSC concept is

very flexible and can have a wide range of applications in various situations.

22

Braam and Nijssen (2004, p.336) described the development stages of the BSC in 2004 and

stated that Kaplan and Norton in 1996 emphasized driving scorecard information and

business strategy towards congruency. In order to be successful and interpret these strategic

goals into the real objectives of the business in a more economical way they implied four

management processes: clarification and translation of vision and strategy; communication

and linking strategic objectives with measures; target setting and business plan; and

enhancing strategic feedback and learning.

To keep strategy as the focal point of the management process, Kaplan and Norton (2001)

extended the above work by presenting five principles. These are translation of strategy into

operational terms; organisation and strategy alignment; strategy as everyone’s everyday job;

strategy a continued process; and organizing change through leadership. Hoque and James

(2000) found that the use of the BSC brings related critical strategic measures onto a single

platform in such an arrangement that keeps the manager away from focusing and improving

one thing at the expense of another and makes cause-and-effect interactions clear. For an

organisation to achieve long-term goals and objectives this is considered a very good process

in management accounting to measure financial and non-financial performance for several

linked goals (Ittner et al., 2003).

Kaplan and Norton (1993, p.3) established that an organization’s mission, culture and use of

technology have a greater impact on the overall business. For that reason, Kaplan and Norton

agreed that organizations need to clarify their strategy on the basis of the competition they’re

facing and the nature of the environment in which they are operating because this will help

managers regarding what to implement when making a performance evaluation.

During his research on the implementation of the BSC, Mendes (2002, as quoted in Jordão

and Novas 2013, p.102) found that the BSC not only measures past performance but also

23

plans for future measures. The BSC is widely used as a tool for performance measurement;

some researchers including Nakmura et al. (2005) have suggested that in an organization’s

strategic activities are clearly linked with functional activities like production, research and

development and human resources etc. They found that an effective system for measuring the

performance of an organization should be made of the different processes of an organization

Many companies implemented the BSC in their organization key strategy which helped

Kaplan and Norton (2001, p.92) to find that in an organization it’s not only important to

develop a strategy but also to implement it. For that reason Norton and Kaplan suggested five

key strategic principles that need to be included when implementing a strategy:

Translate the strategy to operational terms

Align the organization to the strategy

Make strategy everyone’s everyday job

Make strategy a continual process

Mobilize change through executive leadership

From the above five principles it is possible to derive several other elements such as strategy

maps which mean that the overall strategy of the organization should be aligned with a value

proposition such as the maximization of overall shareholder value. It also includes elements

of personal objectives to be aligned with the strategy of the company along with other things

like incentives aligned with team goals. It means that during implementation the strategic

process should be aligned to the gross root of the organization; all employees of the

organization should have access to information and meetings in order to discuss performance

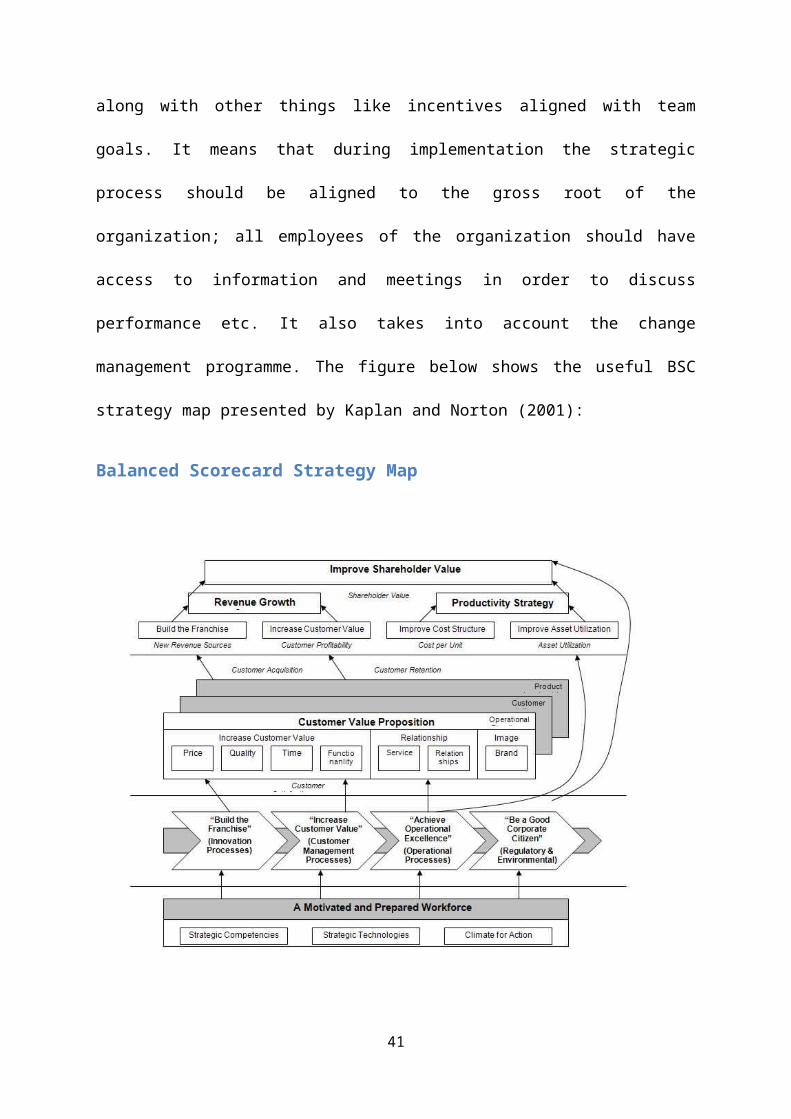

etc. It also takes into account the change management programme. The figure below shows

the useful BSC strategy map presented by Kaplan and Norton (2001):

24

Balanced Scorecard Strategy Map

Balanced Scorecard Strategy Map (Kaplan & Norton, 2001)

The four interrelated perspectives of the Kaplan & Norton BSC (financial, customer,

internal process and learning and growth) are designed to cover the function of the

organization, whether internal or external, in terms of the present and in the future.

Below is a figure taken from A Practitioner’s Guide to the Balanced Scorecard conducted by

CIMA:

25

An organization’s strategy can be rendered into detailed objectives lying within each

of the above four areas identified. The breakdown of the above four main areas into

detailed objectives is necessary to align strategy with functional activities (Nakmura et

al., 2005) and to find appropriate quantitative measures to ascertain the success of

these objectives. The following table lists some examples that can be found in each of

the four perspectives. Below is a figure taken A Practitioner’s Guide to the Balanced

Scorecard conducted by CIMA:

26

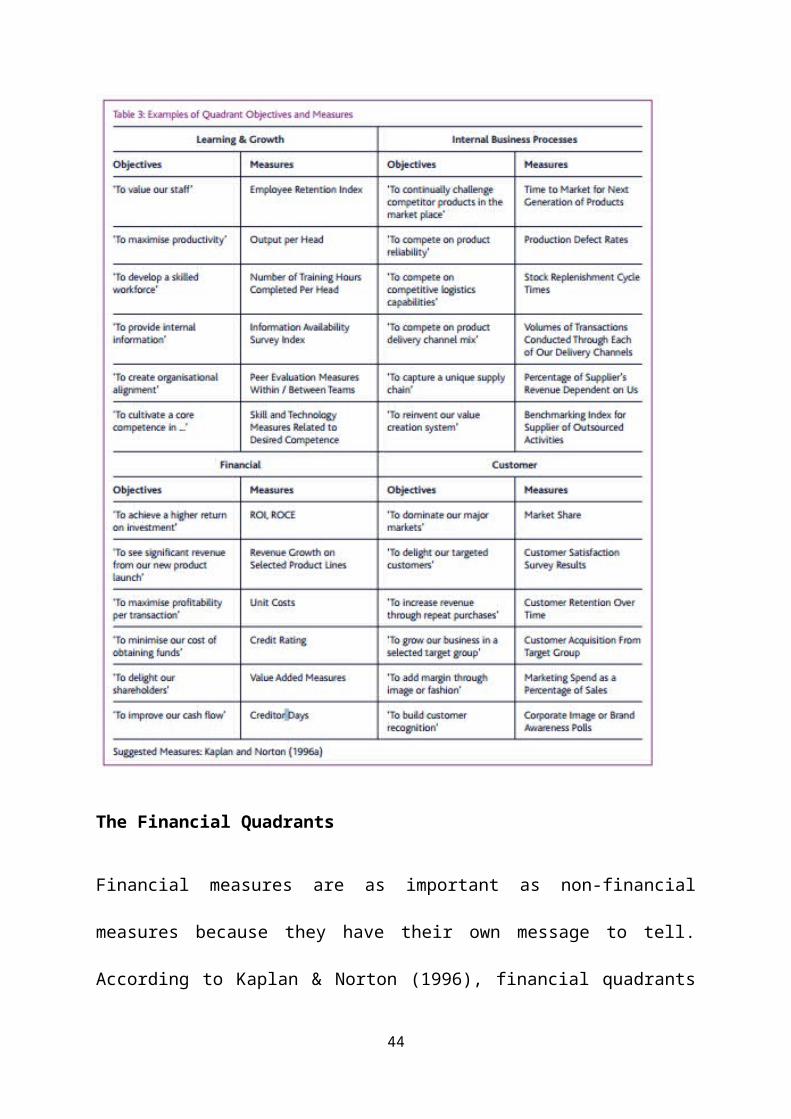

The Financial Quadrants

Financial measures are as important as non-financial measures because they have their

own message to tell. According to Kaplan & Norton (1996), financial quadrants are

the focal point of the remaining three quadrants.

27

The overall objective of the company is to maximize shareholder value. However,

according to Jensen (2002), the BSC is not concerned with shareholder value. Be that

as it may, Kaplan and Norton proposed that the BSC is a guide, not a straight coat and

that mangers are free to make choices. It means that an organization can use the BSC

in any way that is consistent with their strategy and makes allowance for both

measures: operational and shareholder value. It can also be derived from the above

discussion that the BSC can be very helpful for many organizations to provide a base

for appraising and linking financial measurements with strategy and to motivate

managers to accomplish this by making incentives related.

The Customer Quadrants

Customers are very important for most of the executives in order to improve the

performance of the organization. For that reason, organizations mostly focus on

customers’ needs, their satisfaction and adapting their business from customer

crossing point. Many organizations’ mission statements stress the need to attract

customers and if an organization wants to be profitable it needs to keep an eye on and

deal with their customers.

In this quadrant of the BSC, an organization can measure success in terms of how

happy their existing customers are with the company’s products and services by

measuring customer satisfaction through surveys and reviews.

To select the most appropriate objectives and measures for this quadrant of the BSC, it

is necessary to identify what is valued by the customers so as to meet their needs.

Michael Porter states in his book ‘Competitive Advantage: Creating and Sustaining

28

Superior Performance’:

‘An organisation’s competitive advantage grows fundamentally out of the value a

firm is able to create for its buyers that exceed the firm’s cost of creating it. Value is

what buyers are willing to pay’ (Porter, 1985).

Porter (1980; 1985) postulated that buyer value is created and passed on into goods

and services through an organisation’s value chain. The customer quadrant of the BSC

may be used as a tool to find the perception of customers, such as what they value

when receiving products and services.

The Internal Business Processes Quadrant

This quadrant essentially focuses on the non-financial measures of the organization

that could be quality of products and services, timeliness and output. This is usually

done by checking operational processes. Cost accounting is very helpful in this regard

for control and bringing improvements to processes. For many commercial businesses,

enhanced operational processes are very important but in terms of competitive

advantage it’s not sufficient because Porter (1996) stated:

‘The quest for productivity, quality and speed has spawned a remarkable number of

management tools and techniques: total quality management, benchmarking, time-

based competition, outsourcing, partnering, reengineering, and change management.

Although the operational improvements have often been dramatic, many companies

have been frustrated by their inability to translate those gains into sustainable

profitability… A company can outperform rivals only if it can establish a difference

29

that can be preserved’.

So in a BSC an organization needs to focus both on enhancing processes along with

those that will help them in achieving a competitive advantage.

The Learning and Growth Quadrant

This quadrant’s objective is to find an infrastructure for the organization that will help

it with future development and learning. This principally deals with people, processes,

culture, and information systems within organizations. Most business organizations

will measure this quadrant with investment in skill and training, individual

development and providing a system that delivers information efficiently. However, it

is very difficult to identify the main strategic measure in this area. Identification of

other soft issues such as team motivation, culture, creativity, and knowledge

management is ambiguous. Some examples of objectives and measures within the

learning and growth quadrant are given in the above table.

According to Kaplan and Norton, measuring this quadrant should include such things

as organization alignment, motivation, employee skills and the ability of information

systems.

In 1996, Kaplan and Norton stated that:

‘When it comes to specific measures concerning employee skills, strategic information

availability and organizational alignment, companies have devoted virtually no effort

to measuring either the outcomes or the drivers of these capabilities’ (1996a: 144).

30

2.8 Summary

This section has provided significant insight into some of the companies that have already

implemented the BSC into their organisations. The empirical literature and sources used in

this section have demonstrated that the BSC was an essential key for the organisations to

develop their performance and unlock new potential that aligns with their strategic interests

such as improving profitability, increasing revenue, enhancing customer satisfaction,

improving efficiency and enabling technological advances.

Chapter 3: Research Methodology, Research Methods, and Data Collection

3.1. Introduction

The research methodology shows the approach that is to be applied and the basis used for this

study. This chapter shows how the data were gathered and also examines any ethical issues in

relation to the study along with any limitations associated with this study.

The aim of this report is to examine the implementation of the Balanced Scorecard in Saudi

Arabian companies in order to establish whether organisations across Saudi Arabia are using

the Balanced Scorecard as a tool for measuring performance. This study was designed to

clarify any reasons or limitations why they may not have been able to implement it.

31

3.2. Research Methodology

This dissertation is of an interpretive nature, discovering the issues, and the best suitable

method to tackle this is to approach it using a qualitative research method. This research is

not going to evaluate numbers because it is not concerned with quantifying in relation to

Balanced Scorecard implementation. Also it is not seeking any numbers reflecting how many

organisations have implemented the Balanced Scorecard. Alternatively, it looks at the

implementation of the Balanced Scorecard as a tool of measure in organisations across Saudi

Arabia. It sets out to establish whether or not organisations in Saudi Arabia have

implemented the Balanced Scorecard.

According to Strauss and Corbin, qualitative research is defined as:

"Any kind of research that produces findings not arrived at by means of statistical procedures

or other means of quantification" (Strauss and Corbin, 1990, p. 17).

Further to the definition of qualitative research, Bryman describes the difference between

qualitative and quantitative research as follows:

Quantitative research can be illustrated as a study planning that pay attention to

quantification in the gathering and data analysis process, qualitative research can be

illustrated as a research strategy that usually emphasises words (Bryman, 2004, p.19).

32

Individuals express themselves and their insights of their world through words. Such a

method helps in examining and finding out the key information that is most appropriate for

this study. Furthermore, it is necessary to decide upon a research design and method.

Bryman (2004) offers insight about the research design and emphasised the following key

elements:

A research design is all about the framework for the research, which guides you about the

how to collect and analyse the data. An option regarding how to design the research shows

the different priorities being assigned to a wide range of available research process

dimensions.

On the other hand, a research method is simply the approach that is to be used for the

collection of data such as through questionnaires, interviews or observations. Observations

involve the researcher listening to and watching others (Bryman, 2004, p.27).

3.3. Research Methods

The research method chosen to collect data for this study is a questionnaire and semi-

structured telephone interviews. Some of the differences between semi-structured and

unstructured interviews are outlined below:

- “In unstructured interview the researcher uses an assistance records that gives a

concise detail that tend to deal with a certain range of topics. There may be just a

single question that the interviewer asks and the interviewee is then allowed to

respond freely, with the interviewer simply responding to points that seem worthy of

33

being followed up. Unstructured interviewing tends to be very similar in character to

a conversation.

- A semi-structured interview. The researcher has a list of questions or fairly specific

topics to be covered, often referred to as an interview guide, but the interviewee has a

great deal of leeway in how to reply. Questions may not follow on exactly in the way

outlined on the schedule. Questions that are not included in the guide may be asked as

they pick up on things said by interviewers. But, by and large, all of the questions will

be asked and a similar wording will be used from interviewee to interviewee.

- In both cases, the interview process is flexible. Also, the emphasis is on how the

interviewee frames and understands issues and events - that is, what the interviewee

views as important in explaining and understanding events, patterns and forms of

behaviour” (Fds.oup.com p.314).

The aim of this research is to understand the implementation process of the Balanced

Scorecard in organisations across Saudi Arabia. It was deemed by the researcher that the

most appropriate method for the collection of data will be through questionnaires but the

problem is that only conducting questionnaires would not help the participant to express their

own personal experiences. For that reason the research uses some of the base questions that

were put to all participants as the basis for additional semi-structured interviews as a lever to

allow participants to expand upon their stance by expressing their views.

34

3.4. Research Design

A number of different models were studied before deciding upon the research design for this

dissertation, such as comparative design, cross-sectional design and case study design.

Comparative and cross-sectional design were both rejected for this study because they do not

offer a standardised approach to be used for assessing the key research questions for this

dissertation. Therefore, it was decided that the best approach was to carry out a multiple case

study.

Blaxter et al. (2003) described a case study as:

“In many ways, ideally suited to the needs and resources of the small scale researcher”

(Blaxter et al., 2003, p.71).

It was further described by Yin (1994) that there are three types of case study and that the

most appropriate out of these three would be the critical case. This is important because it

will decide on the basis of a hypothesis whether Saudi Arabian organisations have embraced

the Balanced Scorecard across their operations.

3.5. Data Sources and data Collection

Data were chiefly collected by sending questionnaires to selected companies across Saudi

Arabia. An explanatory email was sent to them, inviting them to take part in the study and

also let them know about the researcher and the aims of the study.

35

In addition, telephone interviews were arranged with the owners and top-level managers of

the companies. At the start of each interview, the researcher introduced himself and then

asked a few question about the research in order to understand their perspective.

However, Questionnaire was not answered effectively as demanded. The reason behind the

semi failure of the questionnaire is that the companies being surveyed are not aware of the

balanced scorecard. The majority of the companies were telephone interviewed to discuss

some of the questions of the questionnaire to get more validated data to implement in the

study.

Chapter 4: Discussion and Analysis

This chapter presents the case studies for the companies participating in this paper and the

vital observations that have been made to present the empirical evidence gathered for this

research along with other expressive sections of the data. To analyse and explain the

empirical facts, these data are presented and rationalized with as much accuracy as possible.

First of all, a number of companies are described along with the market in which they operate

in order to better appreciate the framework and connotation of the findings. Secondly, in

order to better understand how strategy is managed across these organisations,

implementation processes and strategy communication are studied for a boarder picture about

these companies. The next step is to examine the Balanced Scorecard along with its measure

and framework across these companies. Finally, a conclusion is derived on the participation

of these companies in implementing the Balanced Scorecard and how it is affecting these

organisations.

36

4.1. Jude Water Case Study:

Jude Water distillates and distributes bottled water and was established in 1990. Today it is

recognised as producing the best quality bottled water across Saudi Arabia. The company is

constantly improving to meet the demands of customers by looking at their different

requirements. Bottled water is considered to be a healthier package for the growing market

that faces health challenges, especially in Saudi Arabia where water quality is a problem.

4.1.2. Jude Water analysis:

The Jude Water factory is very cautious about its customers and provides them with quality

products with low calories and perfect taste. Therefore, it continuously researches in order to

fully comprehend the vital role of water and hydration for consumers’ health. The stated

objectives of Jude Water are as follows:

Maximise profit

Delivering high quality bottled water

Conduct research to provide quality services, keeping in mind the consumers’ health

and hydration requirements

Jude Water is a private company and its operations are relatively modest in size. Most of the

decisions taken at Jude are made at the apex level and are decided by either top

management or the owner himself. There is no formal implementation of the Balanced

Scorecard at this company. In fact, one of the answers to the questionnaire by the managing

director of the company was:

“We don’t have any set of rules to measure non-financial indicators for the company’s

growth.”

The reason for this is because of the culture in Saudi Arabia where the head of the

department is responsible for everything, as is the case in most private companies like a

sole trader and they don’t have the required resources to implement this. Therefore, a

37

telephone conversation was followed up to find out much more about the company’s

performance measuring tools, the managing director said:

“As Jude’s overriding manager, my objective is to maximize my company’s profit. As such,

we don’t have performance measuring tools but we are looking at maximization of sales and

cutting our expenses and providing quality services to customers.”

This express that the company strategy is to generate revenue as their priority mission

leaving behind other perspectives such as customer and other perspective that will have a

positive influence for their performance in the long run.

4.2.1. Introduction HAYAT BUILDING MATERIAL COMPANY AND UNITECH

The Al-Hayat Building Material Company is part of IKK group which was established in Saudi

Arabia in the 1960s to provide services to the construction industry and meet clients’

demands. Al-Hayat was later founded in 1983. Today, Al-Hayat is one of Saudi Arabia’s

largest merchants of basic sanitary items such as chrome bathroom fixtures, electric water

heaters cast iron manhole covers, brass valves, flexible hoses etc. It is well known as a

major market leader with more than 21 branches and outlets providing services to thousands

of contractors and traders. Al Hayat is the representative and distributor of major

international manufacturers such as Grohe, Ariston, Kludi, Ottone Meloda, Savil, Fiore,

Mamoli, Duravit, Sangra, Hebei, and Hitachi among others.

The goals of the group are to serve its clients according to their needs, to seek out new

business opportunities and diversify into various industries to fulfil clients’ needs under one

roof.

Unitech is part of IKK; it secured second position in terms of revenue within the group and

continues to dominate a larger geographical presence in comparison to other companies in

the group.

38

Following the construction boom, Unitech has enjoyed several years of successful strategic

growth through its diversified range of products and its geographical expansion that covers

the major parts of the GCC and MENA region stretching into the heart of Europe. This

expansion had allowed Unitech to record revenues of US$190 million in 2010 with 1259

employees in total.

Unitech today has an extensive presence across 70 locations in 40 cities distributed across

14 countries. Their operations incorporate 36 sales offices and showrooms, 5 factories, 22

warehouses and 7 outlets.

4.2.2 Analysis of the group:

The group aims to strengthen its global market position, continuing to enhance its product

portfolio across its business segments and capitalize on regional expansion opportunities.

Particular focus is being placed on:

- Product quality

- Service network

- Brand awareness

- Focused production structure and efficient logistics flow

According to Mr. Talal Hajjar, Deputy General Manager at Al Hayat Building Material, the

overall focus of the group is on quality and there is no compromise on quality and we believe

in consultation, production and delivering on time, caring for customers and after market

service.

The group is continuously researching implementing automated tasks and upgrading

procedures. They believe in client satisfaction and are committed to offering competitive

products and services. Mr. Hajjar added up: “Our organisation is quite diversified in terms of

functions and it is geographically spread out. What I like about our business is our collective

ability to correct mistakes and upgrade performance.”

39

Mr. Hajjar emphasised in his interview said that employees are their key assets and was

quoted as saying:

“….Twice a year we make a list of employment history and those who have served the

company over a period of time are recognized. We have staff members who have been

working at Unitech since 1983 and quite others who have been with the company more than

20 years. This shows the importance that Unitech gives to its colleagues; members of its big

family….”

4.2.3. Implementation of the BSC at IKK group

With a strong commitment and passion for customer care, satisfaction and delivering quality

products on time, the group has applied BSC since 2007. Initially there were no experienced

staffs available within the group to implement the Balanced Scorecard so in the very early

stages an American company was outsourced for this purpose due to its widespread

experience in the relevant field. The outsourced company initially started working on

collecting information about previous performance measurement with IKK by conducting

meetings with seniors managers, followed by mid-level managers and at last with lower level

managers. After this long process, the results were submitted to senior-level management

and responsibility for the BSC was given to the quality control department which is

responsible for customer care; the quality of products; employees; finance; and the

education and research perspective.

4.3.1 Omix Introduction:

Omix is an engineering construction company also known as Abdul Aziz Bin Omran Al

Omran & Partners Company based in Riyadh Saudi Arabia. Its vision is to become one of the

largest integrated construction companies and to contribute effectively to the state economy.

Its primary objective is to offer a high level of customer service and be distinguished in

40

developing and training national manpower and stability at a high level of quality in concern

of social values and high work ethics.

4.3.2. Omix Analysis:

Omix construction has similar objectives to other companies, providing quality services and

goods, and customer care but in addition they are particularly focussed on national policies

offering the following:

- Supporting Saudi gross domestic product

- Training and development of national competencies

- Supporting national industry

It is important to understand Omix’s strategies in order to know much more about how they

would cope with implementing the Balanced Scorecard. Some of the strategies are as follows:

- Support national industry

- Improve work ethics

- Ensure environmental protection

- Quality policy

- Safety of workers

4.3.3. Implementation of the BSC at Omix:

Omix were not able to answer the questionnaire. It was found that the corporation is

knowledgeable about the Balanced Scorecard as a performance measurement but it was found

that the system is not implemented across the organisation, which measures non-financial

indicators.

41

To find out more in a telephone conversation, one of the senior managers was asked: “What

is it that increases your sales?” He answered: “Great service. It’s what the customer

demands!” This can be taken as a customer perspective or objective. It was also asked how

Omix delivers great service? Omix must research different customer needs and should deliver

within an agreed timeframe, which reflects the characteristics of then internal process

perspective in the BSC.

A further question asked was “how do employees learn the processes for different clients’

needs to meet deadlines?” He answered: “By providing proper training and continuous

professional development.” This is known as the Learning & Growth Perspective in the

Balanced Scorecard.

All of the mechanisms described above support the ultimate goals and mission of Omix. In

light of the above discussion, the senior manager can find out how Omix business is running

and where it needs improvement. It can also be found out what employees need to

understand and what they need to do to help them achieve the overall goal.

Omix has the full balanced picture of what matters, whether its what matters most to OMIX,

what matters most to customers or what matters most internally to achieve the overall

mission. However, as a private company with limited resources there is no proper

mechanism for implementation of the Balanced Scorecard to measure non-financial

indicators.

4.4.1. Introduction Al Yaseen Agri:

Al Yaseen Agri operates in the agricultural sector providing a wide range of products and

services across Saudi Arabia. It was founded in 1980 in Ahsa as a single branch mainly

focusing on vegetable growers and opened its second branch in 2000 in Dammam and started

providing services in gardening and public health services. In 2009 it experienced rapid

42

growth, opening 11 branches across Saudi Arabia and expanding its operations from the

machinery division to the integrated pest management division.

4.4.2. Analysis of Al Yaseen Agri:

Al Yaseen Agri’s vision is to achieve leadership and excellence in the Saudi agricultural

market and to provide efficient and cost effective services to its customers.

The goals of Al Yaseen Agri are given as follows:

- Continuous quest for excellence in performance

- Transfer ideal technologies to the Saudi agricultural market

- Attain adequate financial returns to ourselves and to our customers

4.4.3. Implementation of the BSC at Al Yaseen Agri

Al Yaseen Agri is a private company and has grown in recent years, and is still in the process

of expanding its business across Saudi Arabia, and is looking for opportunities in other

countries. They are currently providing services to Saudi vegetable growers and the farming

community. This includes supplying a range of vegetable seeds, specialty fertilizers,

agrochemicals and an assortment of other agricultural inputs.

The company claims to have secured a prominent position across the market. It also claims to

have a wide spectrum of customers ranging from individual vegetable growers to large Saudi

agricultural companies. However, they have no processes for non-financial performance

measurement. As the Financial and Administrative Manager of the company, Mr. Sameh

Fouad replied to one of the questions:

43

“Although we care about customer services and the quality of products, we don’t have clear

Balanced Scorecard processes implemented to measure them but to some extent we take steps

to research and know about the markets and take measure in those areas.”

Al Yaseen Agri claims to be a marketing company and they state that their marketing strategy

is as follows:

“We are basically a marketing company. We make meticulous efforts to study and segment

our market needs in order to be able to provide efficient and cost-effective solutions to satisfy

our customers' requirements and supply outstanding, competitively priced and innovative

agricultural technologies. We screen the world market seeking agricultural technologies

suitable for Saudi farming. We do a thorough field assessment in our "Trial Station" to

ascertain their technical and economical viabilities before we put our marketing force behind

them. In so doing, we obtain a fair market share for our suppliers and seek to financially

reward both our customers and our suppliers.”

It can be derived that Al Yaseen Agri has not implemented the Balanced Scorecard but from

their marketing strategy it seems that they are using this up to a moderate level to provide

quality services and thus being rewarded.

4.5.1. Introduction Jarir Book Store:

Jarir was founded in 1979 in Riyadh and was later changed into a joint stock company that

become listed on the Saudi capital market in 2003. The paid up capital of Jarir is SR900

Million. The main operation of the company across KSA and other GCC countries are as a

retailer and wholesaler. One of the divisions is Jarir Bookstore which has 31 outlets in 14

cities across Saudi Arabia and another 5 outlets in GCC countries. In addition, Jarir has a

wholesale division with 4 stores and 6 direct sales offices.

44

4.5.2. Jarir Analysis:

Jarir’s activities includes office and school supplies, selling toys and educational aids,

different types of books and publications, arts and craft materials, computer peripherals and

software, mobile phones and accessories, audio visual instruments, photography tools, and

maintenance of computers and electronic items. Jarir operates through two divisions under

the trademark of Jarir Bookstore.

- To maintain leadership in the quality of service to our customers

- To provide products of superior quality at the best price to our customers

- To be the market leader in office supplies, I.T. products and books

- To respect individual initiative and provide opportunities for personal growth to our

employees

- To build a strong management team with effective leadership skills

- To serve and give back to the community because we believe it is our social

responsibility

- To achieve profit and growth in order to make all of the other values and objectives

possible

- Ensure the health and safety of its employees

4.5.3. Implementation of BSC at Jarir Book Store

Jarir uses the Balanced Scorecard as a performance measurement tool. The company values

its customers and provides quality services and products. It respects its employees and backs

45

them to build effective leadership skills. Esam El Hassan, Marketing director of the company,

said about its employees:

“Our employees are our key assets and they are the engineers who build our dreams into

realities.”

Esam also mentioned in his conversation that:

“The company is maintaining a very high standard of health safety. Management of the

company includes a team of professional safety advisers who monitor key safety performance

indicators. Performance and recommendations are presented to the board. A key

performance indicator for health and safety is calculated by comparing the number of

injuries with previous years. Actions are always taken to reduce it.”

“The company sets targets in terms of customer satisfaction, quality assurance, learning and

development and other key areas and then employees are pushed to achieve those and this is

regularly monitored and then performance is measured at the end of the financial year.”

4.6.1. Introduction United Cooperative Assurance

United cooperative

United Cooperative Assurance is mutual insurance cooperation and is registered on Tadawul in 2008

with a total capital of SAR 300,000,000. The company has distinguished itself from its competitors by

providing the Saudi markets with the best opportunities in serving its required insurance demand for

all types of companies and project. The services that the company provide range from casualty and

incident events, corporate medical, marine cargo and hull, flight incident as well as energy insurance.

The company headquarters is located in Riyad and their operations extend throughout the kingdom

with more than 115 points of sale. Its strategic focus on selected categories has contributed to

46

rapid growth, market acceptance and the overall success of the company. The prosperity of

United Cooperative Assurance is linked with good business decisions and business practices.

The achievement of this company have enabled them the opportunity to extend their

operations in the near future in other countries such as Qatar, Kuwait and Dubai.

4.6.2 United Cooperative Assurance Analysis

- To be a centre of excellence in providing the best offers to the customer by top

quality, safe and successful products to meet customer needs

- To give the highest priority to their customers and the environment

- To manage growth based on the principles of sustainable development

- The company will encourage a motivating mission climate recognized by an

organizational culture that focus attention on performance, team work, learning and

development

- Employees and stakeholders will share the rewards of sustained profitable growth

4.6.3. Implementation of BSC at United Cooperative Assurance

The group is has extensive experience in implementing the Balanced Scorecard to measure

non-financial performance across its activities. Some of the index that is weighted across the

company was stated by one of the sales managers, Mr. Yasser Al Rifae, throughout his

answers to the questionnaire

The company is focusing on the quality perspective for how to increase servicing capacity,

where they believe in achieving goals by expanding projects and providing essential facilities

for planning and customer outturn.

The second issue the company takes into consideration is the employee perspective by

improving and developing its staff members, they are looking for competent employees to

47

retain. Therefore, the main objectives is to provide a friendly environment to their employees

and to continuously develop them professionally with their skills.

“Apart from that, we have an education and research perspective where we are looking to

improve our systems to assure quality. We research for the use of advance information

technology for our services. We also have financial measures like general revenues,

budgets andEPS.

4.7.1 Introduction Bahri Company:

The National Shipping Company of Saudi Arabia, widely known as Bahri, was founded in

1978 through a Royal Decree. It was formed as a public company from the very beginning

with 58% of the shares being held by Saudi nationals, 22% by the Saudi Government Public

Investment Fund, and the remaining 20% by Saudi Aramco Development Company.

Bahri initially was a very small multipurpose shipping company but has grown rapidly and is

now one of the biggest shipping conglomerates in the world. Bahri also owns a subsidiary

known as the National Chemical Carrier, which has a fleet of 24 chemical carriers. This

subsidiary was founded in partnership with SABIC and is now one of the largest

companies of its type in the world. Bahri has diversified rapidly since its formation and now

the company's services include transportation of crude oil, general cargo, chemicals, LPG and

other dry bulk.

4.7.2 Bahri Company Analysis:

Bahri’s vision is “linking economies, sharing prosperity and driving excellence in global

logistics services.”

48

Bahri’s mission is to focus on values and responsible business fundamentals, and it wants to

be a leading service provider for running a world class fleet through best practice. Their

mission also includes building mutually beneficial relationships with all stakeholders.

4.7.3. Implementation of BSC at Bahri Company:

We were unable to have any connection with the Bahri Company, instead we had analysed

their annual report to get valuable information about whether they are implementing the BSC

or not.

Bahri is a public limited company and it has provided some values and guidelines for

operations in order to provide best service. The values of Bahri are:

- Driven

- Relentless

- Transparent

- Considered

Meanwhile, the guidelines for the operations of the company are as follows:

- Effective customer care set-up

- Reliable service and excellent safety record

- Maintain customer confidence

- E-service to keep track of cargo

Along with all these, Bahri’s management are considered:

- Dynamic, qualified, experienced, focused and determined

- Having operational expertise across all business segments

49

- Pursuing expansion of new business opportunities with a synergy

- Adhering to organizational strategic initiatives