for personal use only · from wts project. for the year ended 31 march 2012, the group has recorded...

TRANSCRIPT

ARBN 065 191 782

Canada Land Limited 加拿大置地有限公司

ANNUAL REPORT 2011/12F

or p

erso

nal u

se o

nly

Contents

Annual Report 2011/12 Canada Land Limited

1

Page

Corporate Information 2

Chairman’s Statement 4

Report of the Directors 5

Additional Information 8

Financial Statements– Independent Auditors’ Report 13– Consolidated Statement of Comprehensive Income 15– Consolidated Statement of Financial Position 17– Statement of Financial Position 19– Consolidated Statement of Changes in Equity 21– Consolidated Statement of Cash Flows 22– Notes to the Consolidated Financial Statements 24

Statement by Directors 70

Notice of Annual General Meeting 71

For

per

sona

l use

onl

y

Corporate Information

Annual Report 2011/12Canada Land Limited

2

BOARD OF DIRECTORS

Dr. William S.L. Yip (Chairman)Mr. M.B. Lee (Deputy Chairman)Mr. Chow Yuk WahMrs. Eva L.M. Yip

COMPANY SECRETARY

Derrick Siu Ming YIP

AUSTRALIAN REGISTERED OFFICE

Sino Investment Services Pty. Ltd.Suite 1-3, 107-117 High Street,Prahran, VIC, 3181Australia

HONG KONG REGISTERED OFFICE

15th Floor, Yat Chau Building262 Des Voeux Road CentralHong Kong

REPRESENTATIVE OFFICE IN CHINA

No. 1 Gu Ci LuLi Wan DistrictGuangzhou Postal Code 510370China

SOLICITORS – HONG KONG

Fred Kan and Company3104-7, 31st Floor, Central Plaza18 Harbour RoadHong Kong

SOLICITORS – CHINA

Guangdong Kings Law FirmRoom A802 China Shine BuildingNo. 9 Lin He Xi LuTian He DistrictGuangzhouChina

Guangzhou Foreign Economic Law Office18th Floor, Guangdong Holdings TowerNo. 555 Dongfeng Road GuangzhouChina

FINANCIAL ADVISER

Sino Investment Services Pty. Ltd.Suite 1-3, 107-117 High Street,Prahran, VIC, 3181Australia

BANKERS

HSBC Bank Australia Limited, MelbourneDBS Bank (Hong Kong) LimitedBank of East Asia, Hong KongBank of East Asia, GuangzhouBank of China, Hong KongBank of China, GuangzhouChina Construction Bank, GuangzhouIndustrial and Commercial Bank of China, GuangzhouGuangzhou Rural Credit Union, Guangzhou

SHARE REGISTRY – AUSTRALIA

Computershare Investor Services Pty. LimitedYarra Falls452 Johnston StreetAbbotsford Victoria, 3067Australia

For

per

sona

l use

onl

y

Corporate Information

Annual Report 2011/12 Canada Land Limited

3

SHARE REGISTRY – HONG KONG

Incorporated Company Secretaries Limited21st Floor, Euro Trade Centre,13-14 Connaught RoadCentral,Hong Kong

CHARTERED SURVEYORS

Knight Frank4/F Shui On Centre6-8 Harbour RoadWanchaiHong Kong

QUALIFIED VALUER

Guangdong Nan Yue Real Estate and Land Valaution Co., Ltd9th FloorYue Hai Kai Xuan Building190 Xian Lie Dong RoadTianhe District, GuangzhouChina

Guangdong Nan Yue Appraisal Co., Ltd9th FloorYue Hai Kai Xuan Building190 Xian Lie Dong RoadTianhe District, GuangzhouChina

AUDITORS

HLB Hodgson Impey ChengChartered AccountantsCertified Public Accountants31st Floor, Gloucester TowerThe Landmark11 Pedder StreetCentralHong Kong

HOME STOCK EXCHANGE

Australian Stock Exchange (ASX)Exchange Centre20 Bridge StreetSydneyNSW 2000

ASX CODE

CDL

For

per

sona

l use

onl

y

Chairman’s Statement

Annual Report 2011/12Canada Land Limited

4

Dear Shareholders,

The CDL Group (“the Group”) experienced a challenging year in 2011 with a decrease in revenue from reduction in sale of niches from WTS Project. For the year ended 31 March 2012, the Group has recorded an audited consolidated turnover of HK$13.6 million (A$1.7 million) and net loss of HK$6.6 million (A$0.8 million). For the past twelve months, none of the niches were transacted due to regulation of the authorities, and we are still under negotiation with the local authorities and will inform shareholders if there is any update. We shall continue to impose measures in cost control to improve its medium to long-term performance.

The global market looks flimsy in 2012, with the already fragile US market and also the weakening European market, the financial turmoil is gradually moving to Asian market and we start to see the impacts in China. The exports and housing prices continue to decline in China, and the Central Government has lowered the current year GDP growth rate to 7.5%. As we expect China market will have a soft landing in upcoming years, therefore the Group will continue to exercise due care to ensure we have a healthy liquidity. The Group currently maintains a strong cash position with a low gearing ratio at 7.97%, and we will continue to act cautiously to manage all the risks in the coming year.

On behalf of all Board members, I would like to express my sincere appreciation to the Group’s management who play an important role in imparting the culture and value of the Group which they are facing this challenge every day. My profound thanks extend to the Group’s shareholders for their continuous support and I look forward to deliver sound results in the years to come.

Dr William S. L. Yip B.A., F.I.A.P., LL.DChairman and Managing Director

30 May 2012

For

per

sona

l use

onl

y

Report of the Directors

Annual Report 2011/12 Canada Land Limited

5

The Directors herein present their report and the audited financial statements of Canada Land Limited (the “Company”) and its subsidiaries (hereinafter referred to as the “Group”) for the year ended 31 March 2012.

PRINCIPAL ACTIVITIES

The principal activities of the Company during the financial year were investment holding and acting as a real estate agent. The principal activities of the Company’s subsidiaries are set out in note 18 to the consolidated financial statements. There were no significant changes in the activities of the Company and its subsidiaries during the year.

An analysis of the Group’s performance for the year by business and geographical segments is set out in note 6 to the financial statements.

RESULTS AND APPROPRIATIONS

The results of the Group for the year are set out in the consolidated statement of comprehensive income on Page 15 and 16.

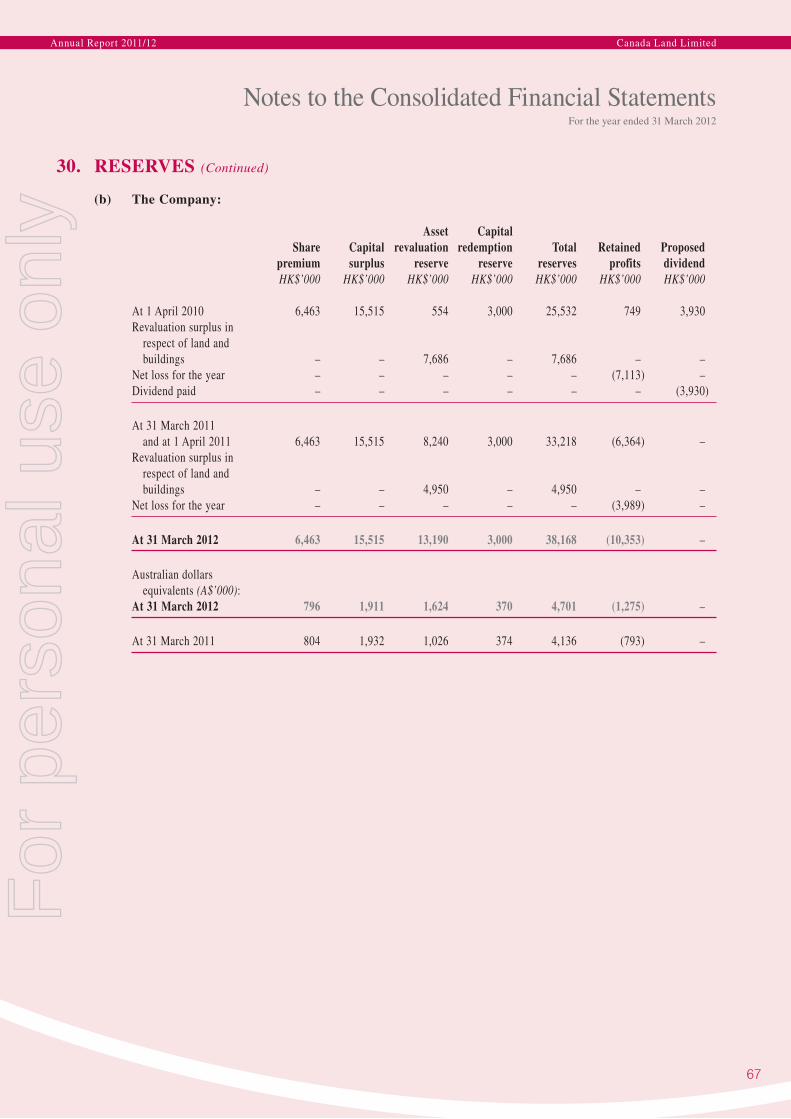

RESERVES

The movements in reserves of the Group and the Company during the year are set out in note 30 to the consolidated financial statements.

PROPERTY, PLANT AND EQUIPMENT AND INVESTMENT PROPERTIES

Details of the movements in property, plant and equipment and investment properties during the year are set out in notes 15 and 16 to the consolidated financial statements respectively.

DIRECTORS

The names, qualifications and details of the Directors of the Company during the year end up to the date of this report were:

Dr. William S. L. Yip, B.A., F.I.A.P., LL.D.Chairman and Managing Director

Dr. Yip founded Canada Land Limited in 1972, pioneering the development of investment properties in Canada and the United States for their sale to Asian interests. In 1991 he turned his investment strategy to the development of real estate and tourist attractions in Guangzhou, the capital city of Guangdong Province, China.

Dr. Yip is also a writer in the field of real estate development in Canada, the United States, and Southern China. He has written extensively on China’s strategic economic development since 1990, lectured in universities and given seminars on these subjects, and has also contributed frequently to various publications. He was a co-author of the book “Doing Business in China” published by McGraw-Hill Ryerson in 1995.

In 1997 Dr. Yip was appointed a Member of the People’s Consultative Committee of Guangzhou and Muizhou, in recognition of his contributions in the cities. He was also awarded the “Voyageur” Award of the Canadian Chamber of Commerce in Hong Kong, which recognises outstanding entrepreneurs in the community.

In 1998 Dr. Yip received an Honorary Doctor of Laws Degree from his Alma Mater, Concordia University in Montreal, Canada, in recognition of his service in particular to the field of education in Canada, Hong Kong and China. He was also elected the President of the Canadian Chamber of Commerce in Hong Kong in 1998 and Chairman of the Board of Governors in 1999. In 2003 Dr. Yip was awarded as Guangzhou Municipal Honorable Citizen for his achievement and contributions in Guangzhou, China.

For

per

sona

l use

onl

y

Report of the Directors

Annual Report 2011/12Canada Land Limited

6

In December 2004, Dr. Yip was appointed as an independent Non-Executive Director of Galaxy Entertainment Group Limited, a listed company in the Stock Exchange of Hong Kong Limited (Stock code: 0027). In June 2008, Dr. Yip was appointed as an independent Non-Executive Director of K. Wah International Holdings Limited, a listed company in the Stock Exchange of Hong Kong Limited (Stock code: 0173).

Mr. M. B. Lee, S.B.S., M.B.E., F.C.P.A., F.C.I.S., F.H.K.S.A., C.P.A., J.P.Deputy Chairman

Mr. Lee holds directorships in both public and private companies engaged in real estate, merchant banking, electronic and the electrical industries in Australia, Canada, Hong Kong and China. He is the Chairman of the Hong Kong Society for Rehabilitation which is a voluntary organisation serving persons with disability for the last 50 years in Hong Kong. He advises the Chairman on the development of long term strategies for the Group.

Mr. Chow Yuk Wah, B. Comm.

Mr. Chow has been a successful entrepreneur in a number of fields including real estate development, the securities and foreign exchange businesses, the distribution of marine products, and the ownership and management of a chain of restaurants in Hong Kong. He continues to be actively involved in formulating the Group’s strategy.

Mrs. Eva Loke Moy Yip, S.R.N., S.C.M.

Mrs. Yip brings to the Group her significant knowledge of the China consumer market gained from experiences with other multinational companies. She uses this knowledge in supporting the Chairman in strategic planning for the Group.

In accordance with Article 58 of the Company’s Articles of Association, Mrs. Eva Loke May Yip retire at the forthcoming annual general meeting and, being eligible, offers themselves for re-elections.

DIRECTORS’ INTERESTS IN CONTRACTS

The Directors’ interests in contracts are set out in note 31 to the consolidated financial statements. Apart from the foregoing, no other contracts of significance in relation to the Group’s business to which either the Company or any of its subsidiaries was a party and in which a director of the Company had a material interest subsisted at the end of the year or at any time during the year.

DIRECTORS’ INTERESTS IN EQUITY OR DEBT SECURITIES

As at 31 March 2012 the interests of the Directors and their associates in the share capital of the Company were as follows:

Number of ordinary shares

Dr. William S. L. Yip 25,397,900Mr. M. B. Lee 25,176,206Mr. Chow Yuk Wah 10,970,000Mrs. Eva L. M. Yip 2,200,000

Other than as disclosed above, at no time during the financial year was the Company or any of its subsidiaries a party to any arrangements to enable the Directors of the Company to acquire benefits by means of acquisition of shares in, or debentures of, the Company or any other body corporate.

For

per

sona

l use

onl

y

Report of the Directors

Annual Report 2011/12 Canada Land Limited

7

CONTROLLED ENTITIES AND RELATED BODIES CORPORATE

Details of the Company’s subsidiaries are set out in note 18 to the consolidated financial statements.

BANK LOANS

Details of the bank loans of the Group are set out in note 26 to the consolidated financial statements.

DIRECTORS’ MEETINGS

During the financial year, 3 Directors’ meetings were held. The number of meetings in which Directors were in attendance is as follows:

Number of meetings Number of held while meetings in office attended

Dr. William S. L. Yip 3 3Mr. M. B. Lee 3 3Mr. Chow Yuk Wah 3 3Mrs. Eva L. M. Yip 3 3

AUSTRALIAN TAKEOVER PROVISION

The Company is not subject to any takeover provisions under the Australian Corporations Law.

AUDITORS

The financial statements for the year were audited by HLB Hodgson Impey Cheng whose term of office will expire upon the forthcoming annual general meeting. In March 2012, the practice of HLB Hodgson Impey Cheng was reorganised as HLB Hodgson Impey Cheng Limited. A resolution for the appointment of HLB Hodgson Impey Cheng Limited as the auditors of the Company for the subsequent year is to be proposed at the forthcoming annual general meeting.

On Behalf of the Board

Dr. William S. L. Yip Mr. M. B. LeeChairman Director

Hong Kong, 30 May 2012

For

per

sona

l use

onl

y

Additional Information

Annual Report 2011/12Canada Land Limited

8

1. SHAREHOLDINGS AS AT 31 MARCH 2012

(a) Distribution of Ordinary Shareholders Category (Size of Holding) No. of Shareholders

1 — 1,000 29

1,001 — 5,000 112

5,001 — 10,000 145

10,001 — 100,000 185

100,001 and over 57

(b) There is no any shareholding held in less than marketable parcels.

(c) The names of shareholders listed in the Company’s Register of Substantial Shareholders as at 31 March 2012 are:

No. of OrdinaryShareholder Shares held

William S. L. Yip 25,397,900M. B. Lee 25,176,206Chow Yuk Wah 10,970,000

(d) Top Twenty Shareholders — Ordinary Shares (as at 31 March 2012)

% held of No. of total issued ordinary ordinaryName shares held Shares

MR WILLIAM SHUE LAM YIP 16,101,900 16.39%MAN BAN LEE 12,550,000 12.77%YUK WAH CHOW 10,970,000 11.17%KENTVIEW INVESTMENTS LTD 9,296,000 9.46%B & M CORPORATION 5,024,000 5.11%LEE YIU SUM 3,670,000 3.74%M & J LIMITED 3,380,000 3.44%MS EVA LOKE MOY YIP 2,200,000 2.24%LUI SAU FUN 2,120,609 2.15%CHIU CHOR LUNG 2,000,000 2.04%LIPPO SECURITIES LTD 1,807,960 1.84%MR KWOK WAI JONATHAN LEE 1,711,933 1.74%UOB KAY HIAN (HONG KONG) LIMITED 1,456,000 1.48%LUI WAI CHAI 1,170,000 1.19%MANNAB HOLDINGS INC 1,040,000 1.06%MR WOOD LUN FRANKIE KWAN 750,000 0.76%DABVALE PTY LIMITED 700,000 0.71%PELTON LIMITED 540,000 0.55%CALM NOMINEES PTY LTD 500,000 0.51%CHENG CHAN YAT YIU TRUST FUND 500,000 0.51%

For

per

sona

l use

onl

y

Additional Information

Annual Report 2011/12 Canada Land Limited

9

(e) Vendor Securities

As at the date of this report no securities were considered as Vendor Securities by Australian Stock Exchange Limited.

(f) Voting Rights

As at 31 March 2012 there were 528 holders of fully paid ordinary shares with a par value of HK$0.13 each. Subject to the Articles of Association of the Company and to any rights or restrictions attaching to shares, every member is entitled to be present at a meeting in person, by proxy, representative or attorney. On a show of hands, every member has one vote and on a poll, every member has (i) one vote for each fully paid share held by that person or (ii) voting rights pro-rata to the amount paid up on each partly paid share held by that person.

2. THE NAME OF THE COMPANY SECRETARY IS:

Mr. Derrick S. M. YIP

3. THE ADDRESS OF THE PRINCIPAL REGISTERED OFFICE IN HONG KONG IS:

15th Floor, Yat Chau Building262 Des Voeux Road CentralHong KongTelephone: (852) 2854 4333

THE ADDRESS OF THE COMPANY’S LOCAL AGENT IN AUSTRALIA IS:

Sino Investment Services Pty. Ltd.Suite 1-3, 107-117 High Street,Prahran, VIC 3181AustraliaTelephone: (03) 9629 6615

4. REGISTERS OF SECURITIES ARE KEPT AT THE FOLLOWING ADDRESSES:

Hong Kong Australia

Incorporated Company Secretaries Limited Computershare Investor Services Pty. Limited21st Floor, Euro Trade Centre, Yarra Falls, 452 Johnston Street,13-14 Connaught Road, Abbotsford Victoria 3067Central AustraliaHong Kong Telephone: (161) 39415 5000Telephone: (852) 3181 9338

5. DIRECTORS’ INTERESTS IN EQUITY OR DEBT SECURITIES

Please refer to the section under the heading “Directors’ Interests in Equity or Debt Securities” on page 7 of Report of the Directors.

For

per

sona

l use

onl

y

Additional Information

Annual Report 2011/12Canada Land Limited

10

6. STOCK EXCHANGE LISTING

Official quotation has been granted for all issued ordinary shares of the Company on Australian Stock Exchange Limited.

7. AUDIT COMMITTEE

As at 31 March 2012, the Company did not have an audit committee of the Board of Directors. The Directors do not consider that such a committee would add value to the Group’s operations or its ability to report to shareholders at the present time.

8. CORPORATE GOVERNANCE

The Board of Directors of Canada Land Limited (“the Company”) is committed to ensure that the Company is properly managed to achieve the highest standards of corporate governance and meet the interests of shareholders. This statement outlines the Company’s main corporate governance practices that were in place throughout the financial year ended 31 March 2012. The Company believes it has generally complied with the Australian Securities Exchange Corporate Governance Council’s Corporate Governance Principles and Recommendations (“ASX Corporate Governance Principles”) which took effect from 1 January 2008, unless indicated otherwise. The ASX Corporate Governance Principles are as follows:

Principle 1 – Lay solid foundations for management and oversight

The responsibilities of the Board include:

– Setting goals and policies for the operation of the Company;– Overseeing the Company’s management; and– Reviewing performance regularly and monitoring the Company’s affairs in the best interests of

shareholders;

The responsibilities of the Chairman include:

– Being a leading role of the Board;– Ensuring Directors are properly briefed in all matters relevant to their roles and responsibilities; and– Facilitating Board discussion and managing the Board’s relationship with the Company’s senior

executives.

The Chairman has delegated some of the duties to the General Manager and the Financial Controller as follows:

General Manager:

– Overseeing the overall operation of the Company and approving all top level decisions related to the Company;

– Ensuring proper controls are in place in different level of management in the Company and regularly meeting with senior staff to understand the current operation status;

Financial Controller:

– Overseeing all financial reporting issues of the Company;– Reviewing the financial performance of the Company on monthly basis and ensuring proper control

measures are in place for all revenue and expenses of the Company;

The Company has its own performance appraisal system to evaluate the performance of its senior executives on a yearly basis. The appraisal system base on the company profitability, operating efficiency and cost control variables in order to determine the requisite for remuneration revision of the senior executives.

For

per

sona

l use

onl

y

Additional Information

Annual Report 2011/12 Canada Land Limited

11

Principle 2: Structure the Board to Add Value

The Board of Directors is composed of Executive and non-Executive Directors as follows:

Dr. William S. L. Yip, Chairman and Managing Director Executive DirectorMr. M. B. Lee, Deputy Chairman Non-executive DirectorMr. Chow Yuk Wah Non-executive DirectorMrs. Eva L. M. Yip Non-executive Director

The Company’s governing body is the Board of Directors. Individuals were, and continue to be, recommended for election to the Board on the basis of their experience in the type of business in which the Company operates, the knowledge of the requirements and obligations of being a public company, and their abilities to help the Company grow in a rapidly developing and unique market.

As Dr. William Yip is an Executive Chairman, the Board does not currently comply with the recommendation that the chairman of the Board be an independent director. The Board supports having Dr. William Yip as Executive Chairman because he founded the Company and has a thorough knowledge of the Company’s operations.

Currently the Company does not have a nomination committee but the Board regularly reviews succession plans taking into consideration the range of skills, experience and expertise of the current members. Each director is required to notify the Board of any change in circumstances that could impair their position as a director.

According to the Articles of Association of the Company, on a rotational basis all current Directors are required to retire and, if they so wish, offer themselves for re-election. Every year one-third of the Board or, if their number is not multiple of three, then the number nearest to but not exceeding one-third of the Board is required to retire. At the date of this report the Company has followed this process every year and the Directors retiring and offering themselves for re-election have been re-elected.

Principle 3: Promote Ethical and Responsible Decision Making

Currently the Company does not have any Code of Conduct Statement or Trading Policy in place and publicly published to the Company website.

However, the Company, including its Directors and key executives, constantly stresses the need to maintain the highest ethical standards to ensure all its activities are undertaken with honesty and fairness. The relatively small size of the Company’s work force and the presence of full time Executive Director enable the Company to do this. Regular staff meetings are held in which this issue is constantly stressed.

Furthermore, the Directors and employees of the Company are advised only to deal in the Company’s shares after a reasonable time gap lapsed following the issue of an announcement to the ASX, especially half-year and year end results.

Principle 4: Safeguard Integrity in Financial Reporting

As at 31 March 2012, the Company did not have an audit committee of the Board of Directors. The General Manager and the Financial Controller stated to the Board that the Group’s consolidated financial report presents a true and fair view, in all material respects, of the Group’s financial condition and operational results and are in accordance with relevant accounting standards. The Board reviews external audit reports, the consolidated financial statements and other information distributed externally and accounting policies and practices. The Financial Controller and the Company Secretary liaise with the external auditors and ensure that the annual statutory audit and half-year limited review are conducted in an effective manner.

For

per

sona

l use

onl

y

Additional Information

Annual Report 2011/12Canada Land Limited

12

Principle 5: Make timely and balanced disclosure

The Company Secretary has been nominated as the person responsible for communications with the ASX. This role includes responsibility for ensuring compliance with the continuous disclosure requirement in the ASX Listing Rules and overseeing and co-coordinating information disclosure to the ASX, analysts, brokers, Shareholders, the media and the public.

All material information concerning the Company, including its financial situation, performance and ownership are posted on the Company website after the approval of the Chairman to ensure all investors have equal and timely access.

Principle 6: Respect the Rights of Shareholders

The Board aims to ensure that shareholders are informed of all major developments through the annual report, the half-yearly report and the encouragement of full participation in the Annual General Meeting. This is achieved by way of detailed reports on the half year and annual results and through the Chairman’s address at general meetings. Copies of announcements made to the ASX are available from the websites of the ASX, www.asx.com.au, and the Company, www.canadaland.com.hk.

Principle 7: Recognise and Manage Risk

The Board acknowledges that it is responsible for the overall internal control framework, and recognises that no cost effective internal control system will preclude all errors and irregularities. The system is based upon procedures, policies, guidelines and organisational structures that provide an appropriate division of responsibility and the careful selection and training of qualified personnel.

Authorisation of projects implementation, entering into debt facilities and major capital expenditure or commitments requires Board approval. All routine operating expenditures are the responsibility of management in accordance with programs and budgets approved by the Board.

The Company does not establish any policies on risk oversight and management of material business risks. A significant portion of the Group’s operations is conducted in the People’s Republic of China (the “PRC”) where growth is rapid and the legal framework is occasionally uncertain when compared to the more developed economic nations in the world. In the opinion of the Board, through constant contact with appropriate officials inside and outside government and discussions with external advisers the Group reduces unnecessary risk to the minimum. The Board have regular discussion with management on the monitoring of such risk and proper action will be taken place once the management aware there would be significant impact of such risk on the Group’s business operation.

Principle 8: Remunerate Fairly and Responsibly

The Company does not have a remuneration committee. The remuneration policy has been determined by the Board. The Board reviews the performance and salary of the General Manager and other senior management staff whereas the General Manager in turn reviews the executive officers’ performance and salaries in Hong Kong/China respectively.

Directors are compensated according to their Executive or non-Executive status. Executive Directors are paid a monthly salary and are also paid fees for acting as Directors if so approved by the Board as a whole. Non-Executive Directors are paid fees for acting as such if approved by the shareholders in general meeting.

The Company has to prepare financial statements in Hong Kong according to the local legislative requirement.

For

per

sona

l use

onl

y

Independent Auditors’ Report

Annual Report 2011/12 Canada Land Limited

13

31/F, Gloucester TowerThe Landmark

11 Pedder StreetCentral

Hong Kong

TO THE SHAREHOLDERS OF CANADA LAND LIMITED(incorporated in Hong Kong with limited liability)

We have audited the consolidated financial statements of Canada Land Limited (the “Company”) and its subsidiaries (collectively referred to as the “Group”) set out on pages 15 to 69, which comprise the consolidated and company statements of financial position as at 31 March 2012, and the consolidated statement of comprehensive income, the consolidated statement of changes in equity and the consolidated statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information.

DIRECTORS’ RESPONSIBILITY FOR THE CONSOLIDATED FINANCIAL STATEMENTS

The directors of the Company are responsible for the preparation of consolidated financial statements that give a true and fair view in accordance with Hong Kong Financial Reporting Standards issued by the Hong Kong Institute of Certified Public Accountants and the Hong Kong Companies Ordinance, and for such internal control as the directors determine is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

AUDITORS’ RESPONSIBILITY

Our responsibility is to express an opinion on these consolidated financial statements based on our audit and to report our opinion solely to you, as a body, in accordance with section 141 of the Hong Kong Companies Ordinance, and for no other purpose. We do not assume responsibility towards or accept liability to any other person for the contents of this report. We conducted our audit in accordance with Hong Kong Standards on Auditing issued by the Hong Kong Institute of Certified Public Accountants. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditors’ judgement, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the entity’s preparation of consolidated financial statements that give a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the directors, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

For

per

sona

l use

onl

y

Independent Auditors’ Report

Annual Report 2011/12Canada Land Limited

14

OPINION

In our opinion, the consolidated financial statements give a true and fair view of the state of affairs of the Group and of the Company as at 31 March 2012, and of the Group’s loss and cash flows for the year then ended in accordance with Hong Kong Financial Reporting Standards and have been properly prepared in accordance with the Hong Kong Companies Ordinance.

HLB Hodgson Impey ChengChartered AccountantsCertified Public Accountants

Hong Kong, 30 May 2012

For

per

sona

l use

onl

y

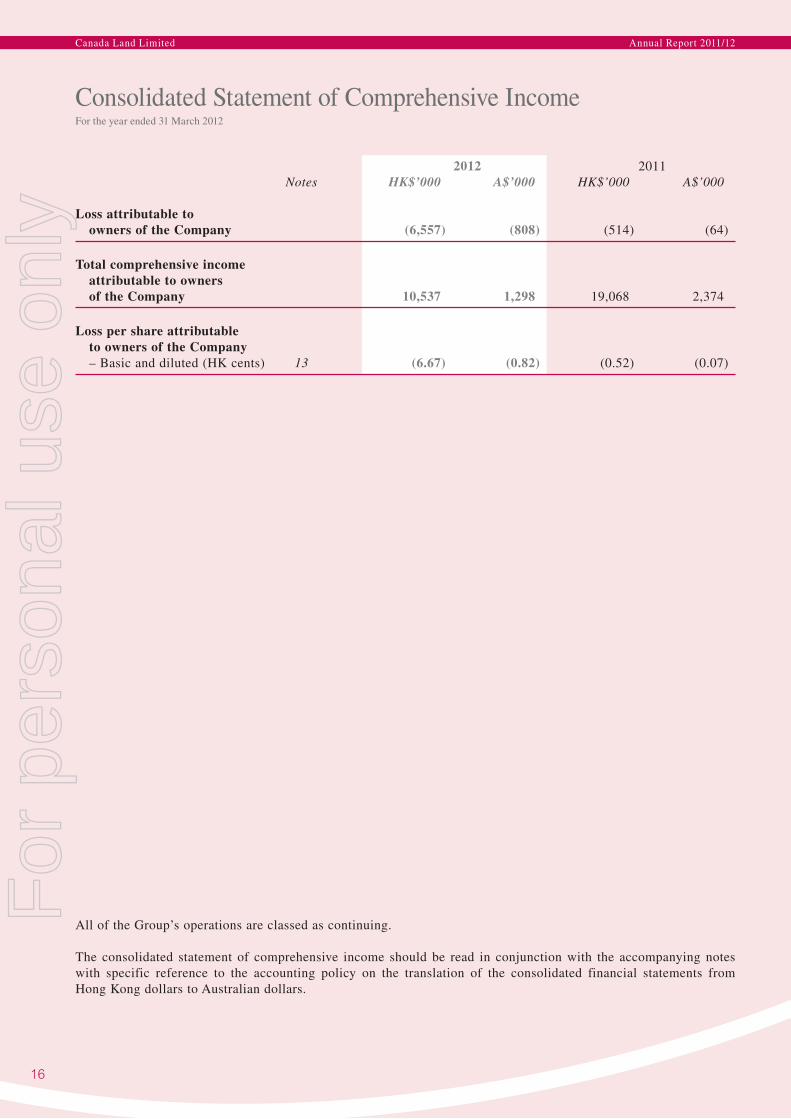

Consolidated Statement of Comprehensive IncomeFor the year ended 31 March 2012

Annual Report 2011/12 Canada Land Limited

15

2012 2011 Notes HK$’000 A$’000 HK$’000 A$’000

Turnover 7 13,577 1,672 24,471 3,047

Cost of sales (1,899) (234) (2,798) (348)

Gross profit 11,678 1,438 21,673 2,699

Other revenue 7 3,041 375 835 104

Staff costs (8,975) (1,105) (9,831) (1,224)

Amortisation and depreciation 8 (4,697) (579) (4,108) (512)

Administrative expenses (9,760) (1,202) (9,745) (1,214)

Loss from operations 8 (8,713) (1,073) (1,176) (147)

Fair value gains in respect of investment properties 16 4,883 601 1,208 150

Impairment loss on goodwill 20 (303) (37) – –

Finance costs 10 (183) (23) (184) (22)

Loss on ordinary activities before taxation (4,316) (532) (152) (19)

Taxation 11 (2,241) (276) (362) (45)

Loss for the year (6,557) (808) (514) (64)

Other comprehensive incomeRevaluation surplus 11,144 1,373 14,322 1,783Exchange differences on translating foreign operations 5,950 733 5,260 655

Other comprehensive income for the year, net of tax 17,094 2,106 19,582 2,438

Total comprehensive income for the year 10,537 1,298 19,068 2,374

For

per

sona

l use

onl

y

Consolidated Statement of Comprehensive IncomeFor the year ended 31 March 2012

Annual Report 2011/12Canada Land Limited

16

2012 2011 Notes HK$’000 A$’000 HK$’000 A$’000

Loss attributable to owners of the Company (6,557) (808) (514) (64)

Total comprehensive income attributable to owners of the Company 10,537 1,298 19,068 2,374

Loss per share attributable to owners of the Company – Basic and diluted (HK cents) 13 (6.67) (0.82) (0.52) (0.07)

All of the Group’s operations are classed as continuing.

The consolidated statement of comprehensive income should be read in conjunction with the accompanying notes with specific reference to the accounting policy on the translation of the consolidated financial statements from Hong Kong dollars to Australian dollars.

For

per

sona

l use

onl

y

Consolidated Statement of Financial PositionAs at 31 March 2012

Annual Report 2011/12 Canada Land Limited

17

2012 2011 Notes HK$’000 A$’000 HK$’000 A$’000

Non-current assets Property, plant and equipment 15 160,751 19,800 147,661 18,387 Investment properties 16 32,102 3,954 24,675 3,073 Prepaid lease payments for land 17 7,445 917 7,448 927 Intangible assets 19 – – 469 58 Goodwill 20 – – 303 38

200,298 24,671 180,556 22,483

Current assets Inventories 21 204 25 171 21 Trade receivables 22 365 45 1,407 175 Prepayments, deposits and other receivables 23 6,322 779 2,177 271 Amount due from a related company 24 – – 428 53 Cash and bank balances 30,593 3,768 36,174 4,505

37,484 4,617 40,357 5,025

Less: Current liabilities Trade and other payables 25 1,611 198 782 97 Interest-bearing bank borrowings, secured – due within one year 26 13,874 1,709 13,874 1,728 Tax payable 7,358 906 7,061 879

22,843 2,813 21,717 2,704

Net current assets 14,641 1,804 18,640 2,321

Total assets less current liabilities 214,939 26,475 199,196 24,804

For

per

sona

l use

onl

y

Consolidated Statement of Financial PositionAs at 31 March 2012

Annual Report 2011/12Canada Land Limited

18

2012 2011 Notes HK$’000 A$’000 HK$’000 A$’000

Less: Non-current liabilities Provision for long service payments 27 680 84 680 85 Deferred taxation 28 40,191 4,951 34,985 4,356

40,871 5,035 35,665 4,441

Net assets 174,068 21,440 163,531 20,363

Capital and reserves Share capital 29 12,773 1,573 12,773 1,590 Retained profits 30(a) 32,077 3,951 38,634 4,811 Reserves 30(a) 129,218 15,916 112,124 13,962

Total equity attributable to owners of the Company 174,068 21,440 163,531 20,363

The consolidated financial statements on pages 15 to 69 were approved by the board of directors on 30 May 2012 and signed on its behalf by:

Dr. William S. L. Yip Mr. M. B. LeeChairman Director

The consolidated statement of financial position should be read in conjunction with the accompanying notes with specific reference to the accounting policy on the translation of the consolidated financial statements from Hong Kong dollars to Australian dollars.

For

per

sona

l use

onl

y

Statement of Financial PositionAs at 31 March 2012

Annual Report 2011/12 Canada Land Limited

19

2012 2011 Notes HK$’000 A$’000 HK$’000 A$’000

Non-current assets Property, plant and equipment 15 30,137 3,712 25,537 3,180 Investment properties 16 1,428 175 – – Interests in subsidiaries 18 11,773 1,450 11,773 1,466 Intangible assets 19 – – 469 58

43,338 5,337 37,779 4,704

Current assets Amounts due from subsidiaries 18 22,439 2,764 22,350 2,783 Prepayments, deposits and other receivables 23 3,766 464 83 10 Cash and bank balances 9,587 1,181 884 110

35,792 4,409 23,317 2,903

Less: Current liabilities Amounts due to subsidiaries 18 21,687 2,671 4,884 608 Other payables and accruals 25 243 30 418 52 Interest-bearing bank borrowings, secured – due within one year 26 13,874 1,709 13,874 1,728

35,804 4,410 19,176 2,388

Net current (liabilities)/assets (12) (1) 4,141 515

Total assets less current liabilities 43,326 5,336 41,920 5,219

Less: Non-current liabilities Provision for long service payments 27 680 84 680 85 Deferred taxation 28 2,058 253 1,613 201

2,738 337 2,293 286

Net assets 40,588 4,999 39,627 4,933

For

per

sona

l use

onl

y

Statement of Financial PositionAs at 31 March 2012

Annual Report 2011/12Canada Land Limited

20

2012 2011 Notes HK$’000 A$’000 HK$’000 A$’000

Capital and reserves Share capital 29 12,773 1,573 12,773 1,590 Retained profits 30(b) (10,353) (1,275) (6,364) (793) Reserves 30(b) 38,168 4,701 33,218 4,136

Total equity 40,588 4,999 39,627 4,933

The financial statements on pages 15 to 69. were approved by the board of directors on 30 May 2012 and signed on its behalf by:

Dr. William S. L. Yip Mr. M. B. LeeChairman Director

The statement of financial position should be read in conjunction with the accompanying notes with specific reference to the accounting policy on the translation of the consolidated financial statements from Hong Kong dollars to Australian dollars.

For

per

sona

l use

onl

y

Consolidated Statement of Changes in EquityFor the year ended 31 March 2012

Annual Report 2011/12 Canada Land Limited

21

Asset Capital Exchange Capital Share Share Capital revaluation reserve on fluctuation redemption Total Retained Proposed capital premium surplus reserve consolidation reserve reserve reserves profits dividend Total HK$’000 HK$’000 HK$’000 HK$’000 HK$’000 HK$’000 HK$’000 HK$’000 HK$’000 HK$’000 HK$’000

At 1 April 2010 12,773 6,463 12,964 63,218 2,239 4,658 3,000 92,542 39,148 3,930 148,393

Net loss for the year – – – – – – – – (514) – (514)Other comprehensive income for the year – – – 17,052 – 2,530 – 19,582 – – 19,582

Total comprehensive income for the year – – – 17,052 – 2,530 – 19,582 (514) – 19,068

Dividend paid – – – – – – – – – (3,930) (3,930)

At 31 March 2011 and at 1 April 2011 12,773 6,463 12,964 80,270 2,239 7,188 3,000 112,124 38,634 – 163,531

Net loss for the year – – – – – – – – (6,557) – (6,557)Other comprehensive income for the year – – – 14,020 – 3,074 – 17,094 – – 17,094

Total comprehensive income for the year – – – 14,020 – 3,074 – 17,094 (6,557) – 10,537

At 31 March 2012 12,773 6,463 12,964 94,290 2,239 10,262 3,000 129,218 32,077 – 174,068

Australian dollars equivalents (A$’000)

At 31 March 2012 1,573 796 1,597 11,614 276 1,264 369 15,916 3,951 – 21,440

At 31 March 2011 1,590 804 1,614 9,996 279 895 374 13,962 4,811 – 20,363

The consolidated statement of changes in equity should be read in conjunction with the accompanying notes with specific reference to the accounting policy on the translation of the consolidated financial statements from Hong Kong dollars to Australian dollars.

For

per

sona

l use

onl

y

Consolidated Statement of Cash FlowsFor the year ended 31 March 2012

Annual Report 2011/12Canada Land Limited

22

2012 2011 Notes HK$’000 A$’000 HK$’000 A$’000

Cash flows from operating activitiesLoss before taxation (4,316) (532) (152) (19)

Adjustments for: Amortisation and depreciation 8 4,697 579 4,108 512 Fair value gains in respect of investment properties 16 (4,883) (601) (1,208) (150) Interest income 7 (697) (86) (169) (21) Finance costs 10 183 23 184 22 Exchange loss – – 71 8 Impairment loss on goodwill 8 303 37 – – Tax refund 7 (1,504) (185) – – Loss on disposal of intangible assets 8 7 1 – –

Operating (loss)/profit before working capital changes (6,210) (764) 2,834 352

(Increase)/decrease in inventories (27) (3) 13 2Decrease in trade receivables 1,057 130 654 81(Increase)/decrease in prepayments, deposits and other receivables (4,125) (508) 1,358 169Decrease in amount due from a related company 428 53 – –Increase/(decrease) in trade and other payables 815 100 (507) (63)

Cash (used in)/generated from operations (8,062) (992) 4,352 541

Interest paid (183) (23) (184) (22)

Net cash (used in)/generated from operating activities (8,245) (1,015) 4,168 519

For

per

sona

l use

onl

y

Consolidated Statement of Cash FlowsFor the year ended 31 March 2012

Annual Report 2011/12 Canada Land Limited

23

2012 2011 Notes HK$’000 A$’000 HK$’000 A$’000

Cash flows from investing activitiesPurchase of property, plant and equipment – – (33) (4)Proceed from disposal of intangible assets 441 54 – –Interest received 697 86 169 21

Net cash generated from investing activities 1,138 140 136 17

Cash flows from financing activitiesBank loan repayments – – (7,455) (929)Proceeds from bank loan – – 13,874 1,728Dividend paid – – (3,930) (489)

Net cash generated from financing activities – – 2,489 310

Net (decrease)/increase in cash and cash equivalents (7,107) (875) 6,793 846

Cash and cash equivalents at the beginning of the year 36,174 4,456 28,747 3,579

Effects of exchange rate changes on the balance of cash held in foreign currencies 1,526 187 634 80

Cash and cash equivalents at the end of the year 30,593 3,768 36,174 4,505

Analysis of balances of cash and cash equivalents

Cash and bank balances 30,593 3,768 36,174 4,505

The consolidated statement of cash flows should be read in conjunction with the accompanying notes with specific reference to the accounting policy on the translation of the consolidated financial statements from Hong Kong dollars to Australian dollars.

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12Canada Land Limited

24

1. CORPORATE INFORMATION

The Company was incorporated on 25 February 1972 in Hong Kong with limited liability and its shares are listed on Australian Stock Exchange.

The Hong Kong registered office and principal place of business of the Company is located at 15/F, Yat Chau Building, 262 Des Voeux Road Central, Hong Kong.

The Company is an investment holding company. The principal activities of its subsidiaries are set out in Note 18 to the consolidated financial statements.

2. APPLICATION OF NEW AND REVISED HONG KONG FINANCIAL REPORTING STANDARDS (“HKFRSs”)

The Hong Kong Institute of Certified Public Accountants (the “HKICPA”) has issued certain new and revised standards, amendments and interpretations (the “new HKFRSs”) to existing standards have been published that are mandatory for accounting periods beginning on or after 1 April 2011. A summary of the effect on initial adoption of these new HKFRSs is set out below.

HKFRSs (Amendments) Improvements to HKFRSs issued in 2010HKAS 24 (Revised) Related Party DisclosuresHKFRS 1 (Amendment) Limited Exemption from Comparative HKFRS 7 – Disclosures for First-time AdoptersHK(IFRIC) – Int 14 (Amendment) Prepayments of a Minimum Funding RequirementHK(IFRIC) – Int 19 Extinguishing Financial Liabilities with Equity Instruments

The directors consider that the application of these new HKFRSs has no material impact on the results and the financial position of the Group.

The Group has not early applied the following new and revised standards, amendments and interpretations that have been issued but are not yet effective.

HKFRS 1 (Amendment) Severe Hyperinflation and Removal of Fixed Dates for First-time Adopters1

HKFRS 1 (Amendments) Government Loans4

HKFRS 7 (Amendments) Disclosures – Transfers of Financial Assets1

HKFRS 7 (Amendments) Disclosures – Offsetting Financial Assets and Financial Liabilities4

HKFRS 7 and HKFRS 9 (Amendments) Mandatory Effective Date of HKFRS 9 and Transition Disclosures6

HKFRS 9 Financial Instruments6

HKFRS 10 Consolidated Financial Statements4

HKFRS 11 Joint Arrangements4

HKFRS 12 Disclosures of Interests in Other Entities4

HKFRS 13 Fair Value Measurements4

HKAS 1 (Amendments) Presentation of Items of Other Comprehensive Income3

HKAS 12 (Amendments) Deferred Tax – Recovery of Underlying Assets2

HKAS 19 (as revised in 2011) Employee Benefits4

HKAS 27 (as revised in 2011) Separate Financial Statements4

HKAS 28 (as revised in 2011) Investments in Associates and Joint Ventures4

HKAS 32 (Amendments) Presentation – Offsetting Financial Assets and Financial Liabilities5

HK(IFRIC) – Int 20 Stripping Costs in the Production Phase of a Surface Mine4

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12 Canada Land Limited

25

2. APPLICATION OF NEW AND REVISED HONG KONG FINANCIAL REPORTING STANDARDS (“HKFRSs”) (Continued)

1 Effective for annual periods beginning on or after 1 July 20112 Effective for annual periods beginning on or after 1 January 20123 Effective for annual periods beginning on or after 1 July 20124 Effective for annual periods beginning on or after 1 January 20135 Effective for annual periods beginning on or after 1 January 20146 Effective for annual periods beginning on or after 1 January 2015

The amendments to HKFRS 7 increase the disclosure requirements for transactions involving transfers of financial assets. These amendments are intended to provide greater transparency around risk exposures when a financial asset is transferred but the transferor retains some level of continuing exposure in the asset. The amendments also require disclosures where transfers of financial assets are not evenly distributed throughout the period.

The revised disclosure requirements contained in the amendments HKFRS 7 are intended to help investors and other financial statements users to better assess the effect or potential effect of offsetting arrangements on a company’s financial position. The amendments also improve transparency in the reporting of how companies mitigate credit risk, including disclosure of related collateral pledged or received. Companies and other entities are required to apply the amendments for annual periods beginning on or after 1 January 2013, and also interim periods within those annual periods. The required disclosures should be provided retrospectively.

HKFRS 9 issued in 2009 introduces new requirements for the classification and measurement of financial assets. HKFRS 9 amended in 2010 includes the requirements for the classification and measurement of financial liabilities and for derecognition.

Key requirements of HKFRS 9 are described as follows:

• HKFRS 9 requires all recognised financial assets that are within the scope of HKAS 39“Financial Instruments: Recognition and Measurement” to be subsequently measured at amortised cost or fair value. Specifically, debt investments that are held within a business model whose objective is to collect the contractual cash flows, and that have contractual cash flows that are solely payments of principal and interest on the principal outstanding are generally measured at amortised cost at the end of subsequent reporting periods. All other debt investments and equity investments are measured at their fair values at the end of subsequent accounting periods. In addition, under HKFRS 9, entities may make an irrevocable election to present subsequent changes in the fair value of an equity investment (that is not held for trading) in other comprehensive income, with only dividend income generally recognised in profit or loss.

• The most significant effect of HKFRS 9 regarding the classification and measurement of financialliabilities relates to the presentation of changes in the fair value of a financial liability (designated as at fair value through profit or loss) attributable to changes in the credit risk of that liability. Specifically, under HKFRS 9, for financial liabilities that are designated as at fair value through profit or loss, the amount of change in the fair value of the financial liability that is attributable to changes in the credit risk of that liability is presented in other comprehensive income, unless the recognition of the effects of changes in the liability’s credit risk in other comprehensive income would create or enlarge an accounting mismatch in profit or loss. Changes in fair value attributable to a financial liability’s credit risk are not subsequently reclassified to profit or loss. Previously, under HKAS 39, the entire amount of the change in the fair value of the financial liability designated as at fair value through profit or loss was presented in profit or loss.

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12Canada Land Limited

26

2. APPLICATION OF NEW AND REVISED HONG KONG FINANCIAL REPORTING STANDARDS (“HKFRSs”) (Continued)

HKFRS 9 is effective for annual periods beginning on or after 1 January 2015, with earlier application permitted.

HKFRS 10 replaces the parts of HKAS 27 “Consolidated and Separate Financial Statements” that deal with consolidated financial statements and HK (SIC) – Int 12 “Consolidation – Special Purpose Entities”. HKFRS 10 includes a new definition of control that contains three elements: (a) power over an investee, (b) exposure, or rights, to variable returns from its involvement with the investee, and (c) the ability to use its power over the investee to affect the amount of the investor’s returns. Extensive guidance has been added in HKFRS 10 to deal with complex scenarios.

HKFRS 11 replaces HKAS 31 “Interests in Joint Ventures” and HK (SIC) – Int 13 “Jointly Controlled Entities – Non-Monetary Contributions by Venturers”. HKFRS 11 deals with how a joint arrangement of which two or more parties have joint control should be classified. Under HKFRS 11, joint arrangements are classified as joint operations or joint ventures, depending on the rights and obligations of the parties to the arrangements. In contrast, under HKAS 31, there are three types of joint arrangements: jointly controlled entities, jointly controlled assets and jointly controlled operations.

In addition, joint ventures under HKFRS 11 are required to be accounted for using the equity method of accounting, whereas jointly controlled entities under HKAS 31 can be accounted for using the equity method of accounting or proportionate accounting.

HKFRS 12 is a standard for disclosure and is applicable to entities that have interests in subsidiaries, joint arrangements, associates and/or unconsolidated structured entities. In general, the disclosure requirements in HKFRS 12 are more extensive than those in the current standards.

These standards are effective for annual periods beginning on or after 1 January 2013. Earlier application is permitted provided that all of these five standards are applied early at the same time.

HKFRS 13 establishes a single source of guidance for fair value measurements and disclosures about fair value measurements. The standard defines fair value, establishes a framework for measuring fair value, and requires disclosures about fair value measurements. The scope of HKFRS13 is broad; it applies to both financial instrument items and non-financial instrument items for which other HKFRSs require or permit fair value measurements and disclosures about fair value measurements, except in specified circumstances. In general, the disclosure requirements in HKFRS13 are more extensive than those in the current standards. For example, quantitative and qualitative disclosures based on the three-level fair value hierarchy currently required for financial instruments only under HKFRS 7 “Financial Instruments: Disclosures” will be extended by HKFRS 13 to cover all assets and liabilities within its scope.

HKFRS 13 is effective for annual periods beginning on or after 1 January 2013, with earlier application permitted.

The amendments to HKAS 1 retain the option to present profit or loss and other comprehensive income in either a single statement or in two separate but consecutive statements. However, the amendments to HKAS 1 require additional disclosures to be made in the other comprehensive income section such that items of other comprehensive income are grouped into two categories: (a) items that will not be reclassified subsequently to profit or loss; and (b) items that may be reclassified subsequently to profit or loss when specific conditions are met. Income tax on items of other comprehensive income is required to be allocated on the same basis.

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12 Canada Land Limited

27

2. APPLICATION OF NEW AND REVISED HONG KONG FINANCIAL REPORTING STANDARDS (“HKFRSs”) (Continued)

The amendments to HKAS 1 are effective for annual periods beginning on or after 1 July 2012. The presentation of items of other comprehensive income will be modified accordingly when the amendments are applied in the future accounting periods.

The amendments to HKAS 12 provide an exception to the general principles in HKAS 12 that the measurement of deferred tax assets and deferred tax liabilities should reflect the tax consequences that would follow from the manner in which the entity expects to recover the carrying amount of an asset. Specifically, under the amendments, investment properties that are measured using the fair value model in accordance with HKAS 40 “Investment Property” are presumed to be recovered through sale for the purposes of measuring deferred taxes, unless the presumption is rebutted in certain circumstances.

The amendments to HKAS 12 are effective for annual periods beginning on or after 1 January 2012.

The amendments to HKAS 19 change the accounting for defined benefit plans and termination benefits. The most significant change relates to the accounting for changes in defined benefit obligations and plan assets. The amendments require the recognition of changes in defined benefit obligations and in the fair value of plan assets when they occur, and hence eliminate the ‘corridor approach’ permitted under the previous version of HKAS 19. The amendments require all actuarial gains and losses to be recognised immediately through other comprehensive income in order for the net pension asset or liability recognised in the consolidated statement of financial position to reflect the full value of the plan deficit or surplus.

The amendments to HKAS 19 are effective for annual periods beginning on or after 1 January 2013 and require retrospective application with certain exceptions.

The amendments to HKAS 32 address inconsistencies in current practice when applying the offsetting criteria and clarify:

• themeaningof“currentlyhasalegallyenforceablerightofset-off”;and

• thatsomegrosssettlementsystemsmaybeconsideredequivalenttonetsettlement.

The amendments are effective for annual periods beginning on or after 1 January 2014 and are required to be applied retrospectively.

The Group is in the process of assessing the potential impact of the above new HKFRSs upon initial application but is not yet in a position to state whether the above new HKFRSs will have a significant impact on the Group’s and the Company’s results of operations and financial position.

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12Canada Land Limited

28

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

These consolidated financial statements have been prepared in accordance with Hong Kong Financial Reporting Standards (which also include Hong Kong Accounting Standards (“HKASs”) and Interpretations) issued by the HKICPA, accounting principles generally accepted in Hong Kong, the Hong Kong Companies Ordinance and the applicable disclosure requirements of Australian Stock Exchange Listing Rules.

The preparation of the consolidated financial statements in conformity with HKFRSs requires management to make judgments, estimates and assumptions that affect the application of policies and reported amounts of assets, liabilities, income and expenses. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making judgments about carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates. The estimates and assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period, or in the period of revision and future periods if the revision affects both current and future periods.

Judgments made by management in the application of HKFRSs that have significant effect on the consolidated financial statements and estimates with a significant risk of material adjustments in the next year are discussed in Note 4 to the consolidated financial statements.

The consolidated financial statements have been prepared on the historical cost basis except for certain properties that are measured at fair values, as explained in the accounting policies below. Historical cost is generally based on the fair value of the consideration given in exchange for assets.

A summary of the significant accounting policies adopted by the Group in the preparation of the consolidated financial statements is set out below:

Basis of preparation

The measurement basis used in the preparation of the consolidated financial statements is historical cost as modified for the revaluation of land and buildings and investment properties which are carried at fair value as explained in the accounting policies set out below.

Basis of consolidation

The consolidated financial statements incorporate the financial statements of the Company and entities (including special purpose entities) controlled by the Company (its subsidiaries). Control is achieved where the Company has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

Income and expenses of subsidiaries acquired or disposed of during the year are included in the consolidated statement of comprehensive income from the effective date of acquisition and up to the effective date of disposal, as appropriate. Total comprehensive income of subsidiaries is attributed to the owners of the Company and to the non-controlling interests even if this results in the non-controlling interests having a deficit balance.

Where necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies into line with those used by other members of the Group.

All intra-group transactions, balances, income and expenses are eliminated in full on consolidation.

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12 Canada Land Limited

29

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Basis of consolidation (Continued)

Changes in the Group’s ownership interests in subsidiaries that do not result in the Group losing control over the subsidiaries are accounted for as equity transactions. The carrying amounts of the Group’s interests and the non-controlling interests are adjusted to reflect the changes in their relative interests in the subsidiaries. Any difference between the amount by which the non-controlling interests are adjusted and the fair value of the consideration paid or received is recognised directly in equity and attributed to owners of the Company.

Subsidiaries

A subsidiary is an entity in which the Company, directly or indirectly, controls more than half of its voting power or issued share capital or controls the composition of its board of directors; or over which the Company has a contractual right to exercise a dominant influence with respect to that entity’s financial and operating policies.

The results of subsidiaries are included in the Company’s statement of comprehensive income to the extent of dividends received and receivable. The Company’s interests in subsidiaries are stated at cost less any impairment losses.

Goodwill

Goodwill arising on an acquisition of a business is carried at cost as established at the date of acquisition of the business (see the accounting policy above) less accumulated impairment losses, if any.

For the purposes of impairment testing, goodwill is allocated to each of the Group’s cash-generating units (or groups of cash-generating units) that is expected to benefit from the synergies of the combination.

A cash-generating unit to which goodwill has been allocated is tested for impairment annually, or more frequently when there is indication that the unit may be impaired. If the recoverable amount of the cash-generating unit is less than its carrying amount, the impairment loss is allocated first to reduce the carrying amount of any goodwill allocated to the unit and then to the other assets of the unit on a pro-rata basis based on the carrying amount of each asset in the unit. Any impairment loss for goodwill is recognised directly in profit or loss in the consolidated statement of comprehensive income. An impairment loss recognised for goodwill is not reversed in subsequent periods.

On disposal of the relevant cash-generating unit, the attributable amount of goodwill is included in the determination of the profit or loss on disposal.

Property, plant and equipment

Properties held for own use where the fair values of the leasehold interest in the land and buildings cannot be measured separately at the inception of the lease and the building is not clearly held under an operating lease, are stated in the consolidated statement of financial position at their revalued amount, being their fair value at the date of revaluation less any subsequent accumulated depreciation.

Buildings held for own use which are situated on leasehold land, where the fair value of the building could be measured separately from the fair value of the leasehold land at the inception of the lease, are stated in the consolidated statement of financial position at their revalued amount, being their fair value at the date of revaluation less any subsequent accumulated depreciation.

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12Canada Land Limited

30

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Property, plant and equipment (Continued)

Revaluations are performed periodically by external independent valuers. Any accumulated depreciation at the date of revaluation is eliminated against the gross carrying amount of the assets and the net amount is restated to the revalued amount of the assets.

Any revaluation increase arising on revaluation of leasehold land and buildings is credited to the properties revaluation reserve, except to the extent that it reverses a revaluation decrease of the same asset previously recognised as an expense, in which case the increase is credited to the consolidated statement of comprehensive income to the extent of the decrease previously charged. A decrease in net carrying amount arising on revaluation of an asset is dealt with as an expense to the extent that it exceeds the balance, if any, on the properties revaluation reserve relating to a previous revaluation of that asset. On the subsequent sale or retirement of a revalued asset, the attributable revaluation surplus is transferred to retained profits.

Other property, plant and equipment (excluding construction in progress) are stated at cost less accumulated depreciation and impairment losses.

The cost of an item of property, plant and equipment comprises its purchase price and any directly attributable costs of bringing the assets to its location and working condition for its intended use. Expenses incurred after item of property, plant and equipment have been put into operation, such as repairs and maintenance, is normally charged to the consolidated statement of comprehensive income in the period in which it is incurred. In situation where it can be clearly demonstrated that the expenditure has resulted in an increase in the future economic benefits expected to be obtained from the use of an item of property, plant and equipment and the cost of the item can be measured reliably, the expenditure is capitalised as an additional cost of that asset or as a replacement.

Depreciation is provided to write off the cost or valuation of items of property, plant and equipment over their estimated useful lives and after taking into account their estimated residual value, at the following rates per annum:

Land and buildings Over the unexpired terms of the leasesLeasehold improvements 20% on the reducing balance methodPlant and equipment 20% on the reducing balance methodMotor vehicles 20% on the reducing balance method

Where parts of an item of property, plant and equipment have different useful lives, the cost of that item is allocated on a reasonable basis among the parts and each part is depreciated separately.

Residual values, useful lives and depreciation method are reviewed, and adjusted if appropriate, at the end of each reporting period.

An item of property, plant and equipment is derecognised upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss on disposal or retirement recognised in the consolidated statement of comprehensive income in the year the asset is derecognised is the difference between the net sales proceeds and the carrying amount of the relevant asset.F

or p

erso

nal u

se o

nly

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12 Canada Land Limited

31

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Investment properties

Investment properties are interests in land and buildings (including the leasehold interest held under an operating lease which would otherwise meet the definition of an investment property) held to earn rental income and/or for capital appreciation, rather than for use in the production or supply of goods or services or for administrative purposes; or for sale in the ordinary course of business. Such properties are measured initially at cost, including transaction costs. Subsequent to initial recognition, investment properties are stated at fair value, which reflects market conditions at the end of each reporting period.

Gain or loss arising from changes in fair values of investment properties are included in the consolidated statement of comprehensive income in the year in which they arise.

Any gains or losses on the retirement or disposal of an investment property are recognised in the consolidated statement of comprehensive income in the year of retirement or disposal.

For a transfer from investment property to owner occupied property, the deemed cost of property for subsequent accounting is its fair value at the date of change in use.

Intangible assets (other than goodwill)

Intangible assets represent golf club membership. Intangible assets are carried at cost less accumulated amortisation and impairment losses. Intangible assets are amortised over their estimated useful lives of 20 years on a straight line basis. Intangible assets are tested for impairment either individually or at the cash-generating unit level when there is an indication that an asset may be impaired. If the recoverable amount of an asset is estimated to be less than its carrying amount, the carrying amount of the asset is reduced to its recoverable amount. An impairment loss is recognised as an expense immediately.

When an impairment loss subsequently reverses, the carrying amount of the asset is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset in prior years. A reversal of impairment loss is recognised as income immediately.

Leasing

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership to the lessee. All other leases are classified as operating leases.

Leasehold land for own use

When a lease includes both land and building elements, the Group assesses the classification of each element as a finance or an operating lease separately based on the assessment as to whether substantially all the risks and rewards incidental to ownership of each element have been transferred to the Group, unless it is clear that both elements are operating leases in which case the entire lease is classified as an operating lease. Specifically, the minimum lease payments (including any lumpsum upfront payments) are allocated between the land and the building elements in proportion to the relative fair values of the leasehold interests in the land element and building element of the lease at the inception of the lease.

To the extent the allocation of the lease payments can be made reliably, interest in leasehold land that is accounted for as an operating lease is presented as “prepaid lease payments” in the consolidated statement of financial position and is amortised over the lease term on a straight-line basis. When the lease payments cannot be allocated reliably between the land and building elements, the entire lease is generally classified as a finance lease and accounted for as property, plant and equipment.

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12Canada Land Limited

32

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Impairment of non-financial assets

Where an indication of impairment exists, or when annual impairment testing for an asset is required (other than inventories, goodwill, investment properties and financial assets), the asset’s recoverable amount is estimated. An asset’s recoverable amount is calculated as the higher of the asset’s or cash-generating unit’s value in use and its fair value less costs to sell, and is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets, in which case, the recoverable amount is determined for the cash-generating unit to which the asset belongs.

An impairment loss is recognised only if the carrying amount of an asset exceeds its recoverable amount. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. An impairment loss is charged to the consolidated statement of comprehensive income in the period in which it arises.

An assessment is made at the end of each reporting period as to whether there is any indication that previously recognised impairment losses may no longer exist or may have decreased. If such indication exists, the recoverable amount is estimated. A previously recognised impairment loss of an asset other than goodwill and certain financial assets is reversed only if there has been a change in the estimates used to determine the recoverable amount of that asset, however not to an amount higher than the carrying amount that would have been determined (net of any depreciation/amortisation) had no impairment loss been recognised for the asset in prior years. A reversal of such impairment loss is credited to the consolidated statement of comprehensive income in the period in which it arises.

Financial instruments

Financial assets and financial liabilities are recognised when a group entity becomes a party to the contractual provisions of the instrument.

Financial assets and financial liabilities are initially measured at fair value. Transaction costs that are directly attributable to the acquisition or issue of financial assets and financial liabilities (other than financial assets and financial liabilities at fair value through profit or loss) are added to or deducted from the fair value of the financial assets or financial liabilities, as appropriate, on initial recognition. Transaction costs directly attributable to the acquisition of financial assets or financial liabilities at fair value through profit or loss are recognised immediately in profit or loss.

Financial assets

Financial assets are classified into loans and receivables. The classification depends on the nature and purpose of the financial assets and is determined at the time of initial recognition. All regular way purchases or sales of financial assets are recognised and derecognised on a trade date basis. Regular way purchases or sales are purchases or sales of financial assets that require delivery of assets within the time frame established by regulation or convention in the marketplace.

Effective interest method

The effective interest method is a method of calculating the amortised cost of a debt instrument and of allocating interest income over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash receipts (including all fees and points paid or received that form an integral part of the effective interest rate, transaction costs and other premiums or discounts) through the expected life of the debt instrument, or, where appropriate, a shorter period, to the net carrying amount on initial recognition.

Income is recognised on an effective interest basis for debt instruments other than those financial assets classified as at fair value through profit or loss.

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12 Canada Land Limited

33

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Financial instruments (Continued)

Financial assets (Continued)

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Loans and receivables (including trade and other receivables, amount due from a related company and cash and bank balances) are measured at amortised cost using the effective interest method, less any impairment.

Interest income is recognised by applying the effective interest rate, except for short-term receivables when the recognition of interest would be immaterial.

Impairment of financial assets

Financial assets, other than those at fair value through profit or loss, are assessed for indicators of impairment at the end of each reporting period. Financial assets are considered to be impaired when there is objective evidence that, as a result of one or more events that occurred after the initial recognition of the financial asset, the estimated future cash flows of the investment have been affected.

For all other financial assets, objective evidence of impairment could include:

• significantfinancialdifficultyoftheissuerorcounterparty;or

• breachofcontract,suchasadefaultordelinquencyininterestorprincipalpayments;or

• itbecomingprobablethattheborrowerwillenterbankruptcyorfinancialre-organisation;or

• thedisappearanceofanactivemarketforthatfinancialassetbecauseoffinancialdifficulties.

For certain categories of financial assets, such as trade receivables, assets that are assessed not to be impaired individually are, in addition, assessed for impairment on a collective basis. Objective evidence of impairment for a portfolio of receivables could include the Group’s past experience of collecting payments, an increase in the number of delayed payments in the portfolio past the average credit period of 10 days, as well as observable changes in national or local economic conditions that correlate with default on receivables.

For financial assets carried at amortised cost, the amount of the impairment loss recognised is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the financial asset’s original effective interest rate.

For financial assets carried at cost, the amount of the impairment loss is measured as the difference between the asset’s carrying amount and the present value of the estimated future cash flows discounted at the current market rate of return for a similar financial asset. Such impairment loss will not be reversed in subsequent periods (see the accounting policy below).

The carrying amount of the financial asset is reduced by the impairment loss directly for all financial assets with the exception of trade receivables, where the carrying amount is reduced through the use of an allowance account. When a trade receivable is considered uncollectible, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are credited against the allowance account. Changes in the carrying amount of the allowance account are recognised in profit or loss.

For

per

sona

l use

onl

y

Notes to the Consolidated Financial StatementsFor the year ended 31 March 2012

Annual Report 2011/12Canada Land Limited

34

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Financial instruments (Continued)

Financial assets (Continued)

Impairment of financial assets (Continued)

For financial assets measured at amortised cost, if, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised, the previously recognised impairment loss is reversed through profit or loss to the extent that the carrying amount of the investment at the date the impairment is reversed does not exceed what the amortised cost would have been had the impairment not been recognised.