fomc 20071211 material

TRANSCRIPT

Appendix 1: Materials used by Mr. Dudley

December 11, 2007 127 of 138Authorized for Public Release

Class II FOMC – Restricted FR Page 1 of 8

0

4

8

12

16

20

24

5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28Loan Age in Month

Percent of Total

0

4

8

12

16

20

24Percent of Total

ABX 07.01

ABX 07.02

Average 2000-2005 ARMs

ABX 06.02

ABX 06.01

(2) Subprime 60 Day+ Delinquency Rate by Vintage

Source: Merrill Lynch, Intex

0.01.02.03.04.05.06.07.08.09.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Percent of Total Loans

0.01.02.03.04.05.06.07.08.09.0

Percent of Total Loans

60+ Days Delinquent

Entered Foreclosure

(1) Subprime Mortgage Performance Continues to WorsenJanuary 1998 – September 2007

Source: Mortgage Bankers Association and Economy.com

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Percent of Total Loans

0.0

0.2

0.4

0.6

0.8

1.0

1.2Percent of Total Loans

60+ Days Delinquent

Entered Foreclosure

(3) Prime Mortgage Performance Also WorsensJanuary 1998 – September 2007

Source: Mortgage Bankers Association and Economy.com

December 11, 2007 128 of 138Authorized for Public Release

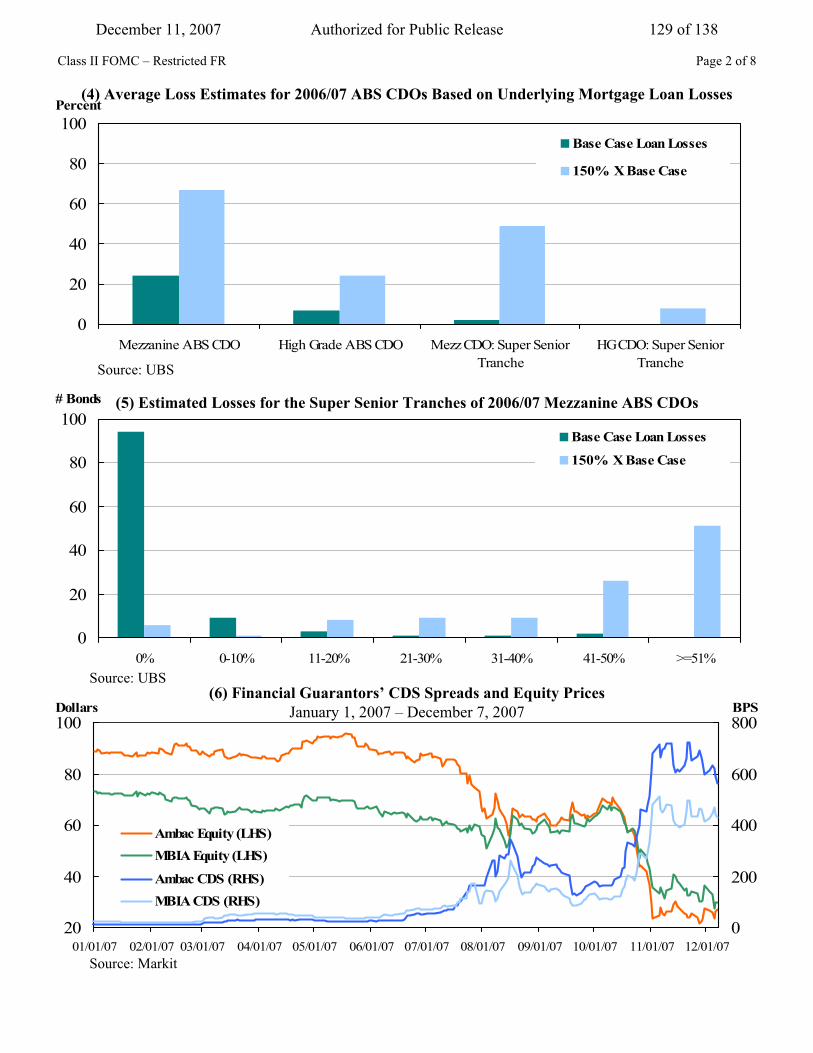

0

20

40

60

80

100

0% 0-10% 11-20% 21-30% 31-40% 41-50% >=51%

# Bonds

Base Case Loan Losses

150% X Base Case

(5) Estimated Losses for the Super Senior Tranches of 2006/07 Mezzanine ABS CDOs

Source: UBS

Class II FOMC – Restricted FR Page 2 of 8

20

40

60

80

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07 11/01/07 12/01/070

200

400

600

100Dollars

800BPS

Ambac Equity (LHS)MBIA Equity (LHS)

Ambac CDS (RHS)MBIA CDS (RHS)

Source: Markit

(6) Financial Guarantors’ CDS Spreads and Equity PricesJanuary 1, 2007 – December 7, 2007

0

20

40

60

80

100

Mezzanine ABS CDO High Grade ABS CDO Mezz CDO: Super Senior HG CDO: Super Senior

Percent

Tranche Tranche

Base Case Loan Losses

150% X Base Case

(4) Average Loss Estimates for 2006/07 ABS CDOs Based on Underlying Mortgage Loan Losses

Source: UBS

December 11, 2007 129 of 138Authorized for Public Release

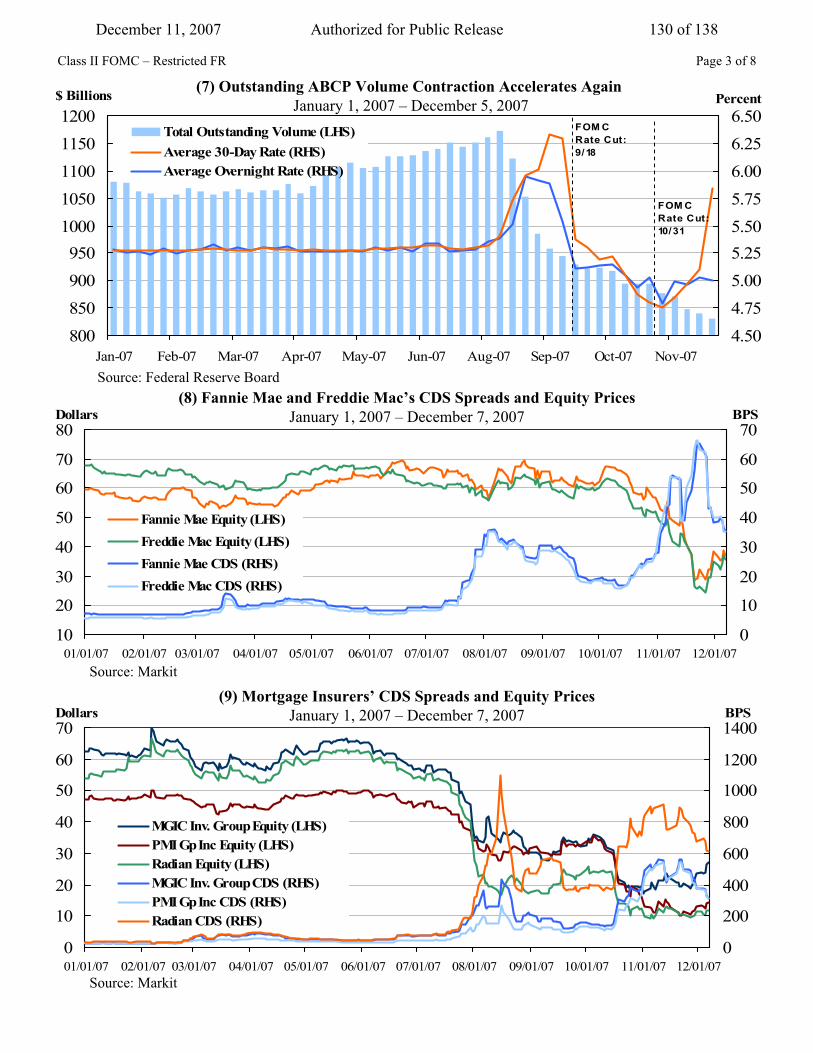

800850900950

10001050110011501200

Jan-07 Feb-07 Mar-07 Apr-07 May-07 Jun-07 Aug-07 Sep-07 Oct-07 Nov-07

$ Billions

4.504.755.005.255.505.756.006.256.50

Percent

Total Outstanding Volume (LHS)Average 30-Day Rate (RHS)Average Overnight Rate (RHS)

FOM C Rate Cut: 9/18

FOM C Rate Cut: 10/31

Source: Federal Reserve Board

(7) Outstanding ABCP Volume Contraction Accelerates Again January 1, 2007 – December 5, 2007

Class II FOMC – Restricted FR Page 3 of 8

0

10

20

30

40

50

60

70

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07 11/01/07 12/01/07

Dollars

0

200

400

600

800

1000

1200

1400BPS

MGIC Inv. Group Equity (LHS)PMI Gp Inc Equity (LHS)Radian Equity (LHS)MGIC Inv. Group CDS (RHS)PMI Gp Inc CDS (RHS)Radian CDS (RHS)

(9) Mortgage Insurers’ CDS Spreads and Equity PricesJanuary 1, 2007 – December 7, 2007

Source: Markit

10

20

30

40

50

60

70

80

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07 11/01/07 12/01/07

Dollars

0

10

20

30

40

50

60

70BPS

Fannie Mae Equity (LHS)Freddie Mac Equity (LHS)Fannie Mae CDS (RHS)Freddie Mac CDS (RHS)

(8) Fannie Mae and Freddie Mac’s CDS Spreads and Equity PricesJanuary 1, 2007 – December 7, 2007

Source: Markit

December 11, 2007 130 of 138Authorized for Public Release

Class II FOMC – Restricted FR Page 4 of 8

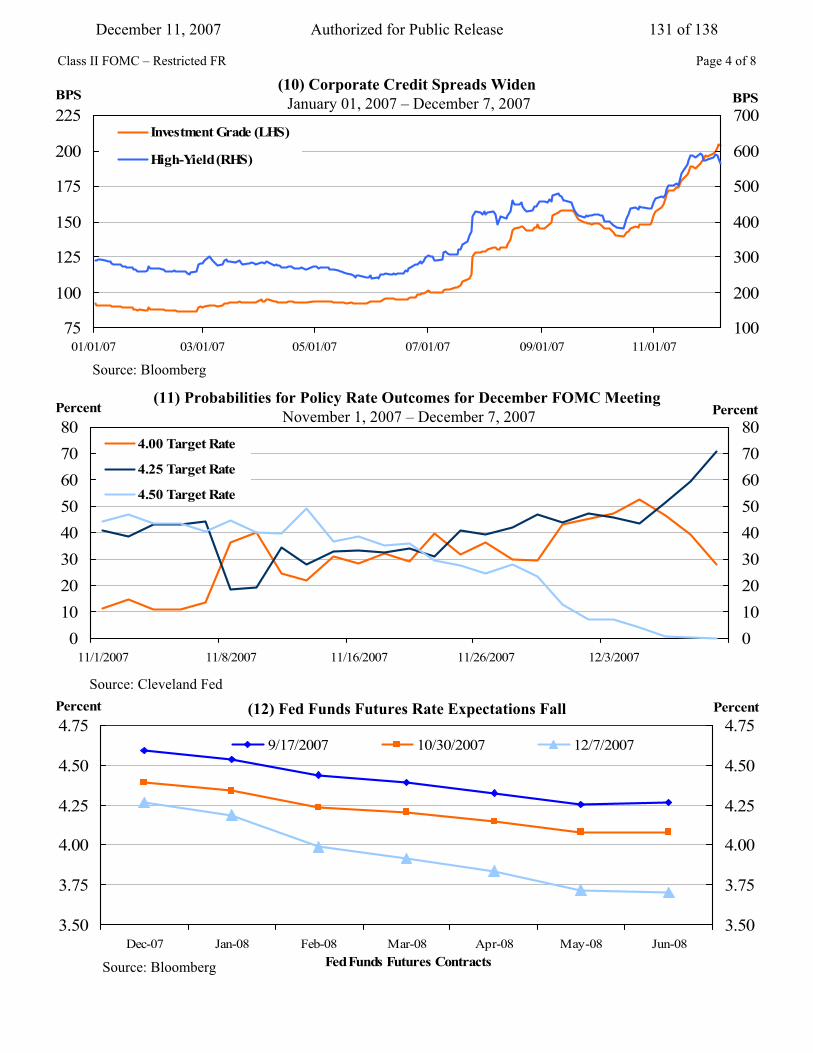

3.50

3.75

4.00

4.25

4.50

4.75

Dec-07 Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08Fed Funds Futures Contracts

Percent

3.50

3.75

4.00

4.25

4.50

4.75 Percent

9/17/2007 10/30/2007 12/7/2007

Source: Bloomberg

(12) Fed Funds Futures Rate Expectations Fall

75

100

125

150

175

200

225

01/01/07 03/01/07 05/01/07 07/01/07 09/01/07 11/01/07

BPS

100

200

300

400

500

600

700BPS

Investment Grade (LHS)

High-Yield (RHS)

(10) Corporate Credit Spreads Widen January 01, 2007 – December 7, 2007

Source: Bloomberg

01020304050607080

11/1/2007 11/8/2007 11/16/2007 11/26/2007 12/3/2007

Percent

01020304050607080

Percent

4.00 Target Rate

4.25 Target Rate

4.50 Target Rate

(11) Probabilities for Policy Rate Outcomes for December FOMC MeetingNovember 1, 2007 – December 7, 2007

Source: Cleveland Fed

December 11, 2007 131 of 138Authorized for Public Release

Class II FOMC – Restricted FR Page 5 of 8

3.25

3.50

3.75

4.00

4.25

4.50

4.75

5.00

Dec-07 Mar-08 Jun-08 Sep-08 Dec-08Eurodollar Futures Contracts

Percent

3.25

3.50

3.75

4.00

4.25

4.50

4.75

5.00 Percent

9/17/2007 10/30/2007 12/7/2007

Source: Bloomberg

(13) Eurodollar Futures Curve Shifts Lower

2.02.5

3.03.54.0

4.55.0

5.56.0Percent

Survey Response -size indicates freq

October Average Forecast

Market Rates as of 10/23

(15) Distribution of Expected Policy Target Among Primary Dealers Prior to October 31 FOMC Meeting

Source: Dealer Policy Survey

Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008

2.02.5

3.03.54.0

4.55.0

5.56.0Percent

Survey Response -size indicates freq

December Average Forecast

Market Rates as of 12/3

(14) Distribution of Expected Policy Target Among Primary Dealers Prior to December 11 FOMC Meeting

Source: Dealer Policy Survey Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008

December 11, 2007 132 of 138Authorized for Public Release

Class II FOMC – Restricted FR Page 6 of 8

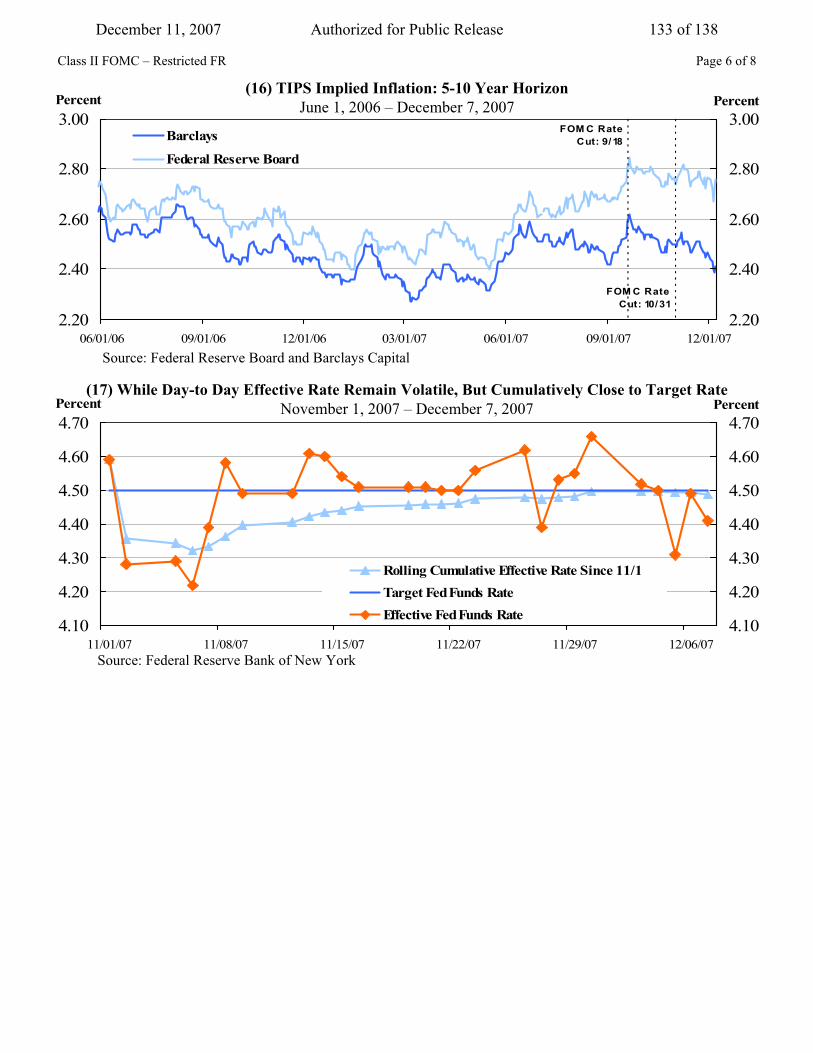

2.20

2.40

2.60

2.80

3.00

06/01/06 09/01/06 12/01/06 03/01/07 06/01/07 09/01/07 12/01/07

Percent

2.20

2.40

2.60

2.80

3.00 Percent

Barclays

Federal Reserve Board

FOM C Rate Cut: 9/18

FOM C Rate Cut: 10/31

(16) TIPS Implied Inflation: 5-10 Year HorizonJune 1, 2006 – December 7, 2007

Source: Federal Reserve Board and Barclays Capital

4.10

4.20

4.30

4.40

4.50

4.60

4.70

11/01/07 11/08/07 11/15/07 11/22/07 11/29/07 12/06/07

Percent

4.10

4.20

4.30

4.40

4.50

4.60

4.70 Percent

Rolling Cumulative Effective Rate Since 11/1Target Fed Funds RateEffective Fed Funds Rate

(17) While Day-to Day Effective Rate Remain Volatile, But Cumulatively Close to Target RateNovember 1, 2007 – December 7, 2007

Source: Federal Reserve Bank of New York

December 11, 2007 133 of 138Authorized for Public Release

90

95

100

105

110

115

120

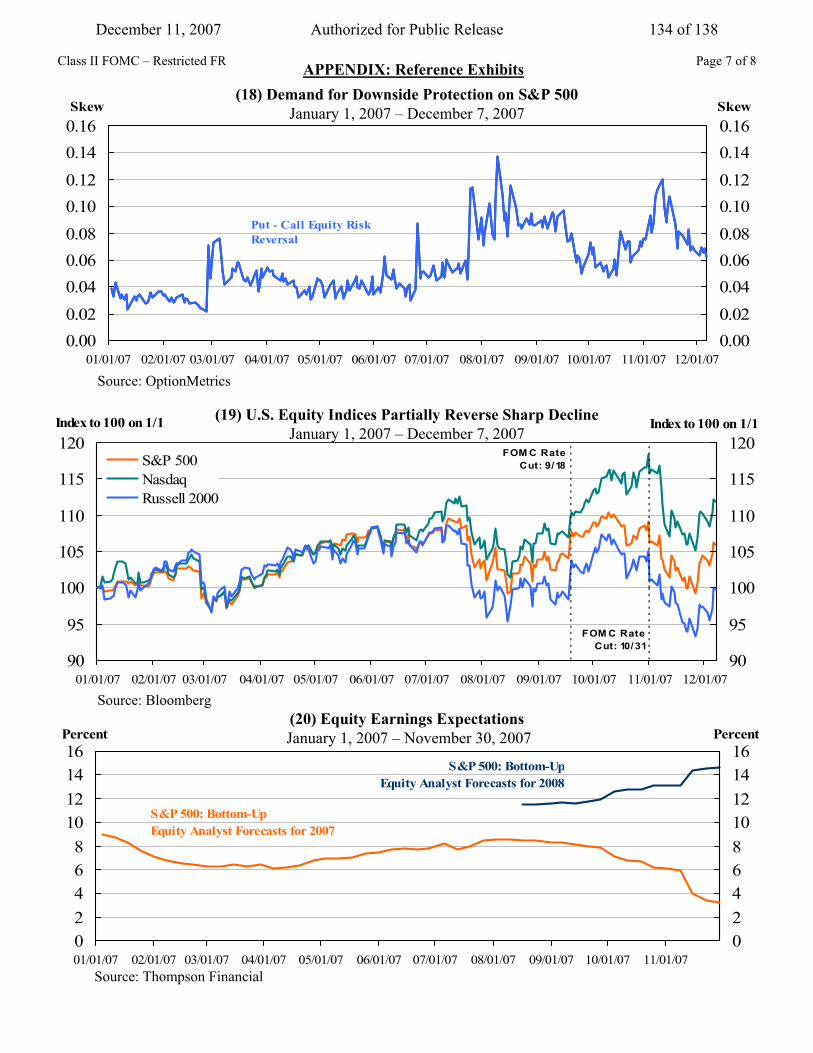

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07 11/01/07 12/01/07

Index to 100 on 1/1

90

95

100

105

110

115

120 Index to 100 on 1/1

S&P 500NasdaqRussell 2000

FOM C Rate Cut: 9/18

FOM C Rate Cut: 10/31

(19) U.S. Equity Indices Partially Reverse Sharp Decline January 1, 2007 – December 7, 2007

Source: Bloomberg

Class II FOMC – Restricted FR

02468

101214

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07 11/01/0702468101214

S&P 500: Bottom-Up Equity Analyst Forecasts for 2007

S&P 500: Bottom-U16

Percent16

Percent

pEquity Analyst Forecasts for 2008

(20) Equity Earnings ExpectationsJanuary 1, 2007 – November 30, 2007

Source: Thompson Financial

Page 7 of 8

0.000.020.040.060.080.100.120.140.16

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07 11/01/07 12/01/07

Skew

0.000.020.040.060.080.100.120.140.16Skew

Put - Call Equity Risk Reversal

(18) Demand for Downside Protection on S&P 500 January 1, 2007 – December 7, 2007

Source: OptionMetrics

APPENDIX: Reference Exhibits

December 11, 2007 134 of 138Authorized for Public Release

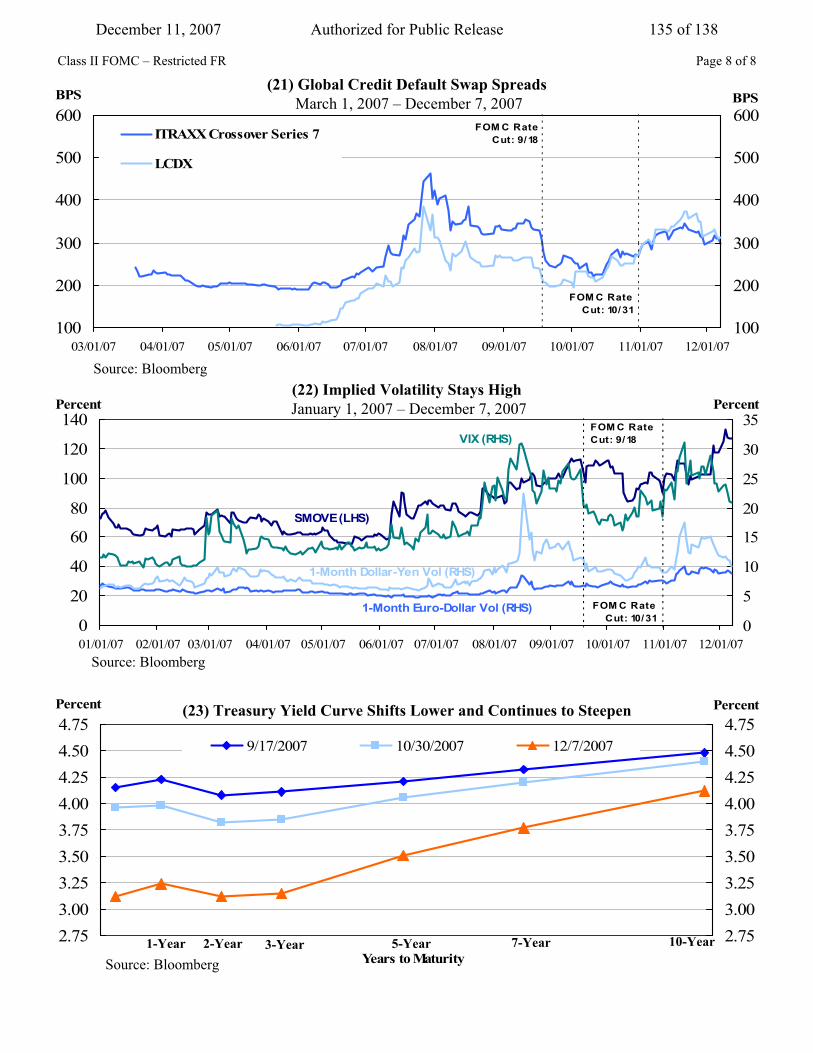

0

20

40

60

80

100

120

140

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07 11/01/07 12/01/07

Percent

0

5

10

15

20

25

30

35 Percent

VIX (RHS)

1-Month Dollar-Yen Vol (RHS)

1-Month Euro-Dollar Vol (RHS)

SMOVE (LHS)

FOM C Rate Cut: 9/18

FOM C Rate Cut: 10/31

Source: Bloomberg

(22) Implied Volatility Stays High January 1, 2007 – December 7, 2007

Page 8 of 8Class II FOMC – Restricted FR

2.753.003.253.503.754.004.254.504.75

Years to Maturity

Percent

2.753.003.253.503.754.004.254.504.75

Percent

9/17/2007 10/30/2007 12/7/2007

(23) Treasury Yield Curve Shifts Lower and Continues to Steepen

Source: Bloomberg1-Year 2-Year 3-Year 5-Year 7-Year 10-Year

100

200

300

400

500

600

03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07 11/01/07 12/01/07

BPS

100

200

300

400

500

600BPS

ITRAXX Crossover Series 7

LCDX

FOM C Rate Cut: 9/18

FOM C Rate Cut: 10/31

(21) Global Credit Default Swap SpreadsMarch 1, 2007 – December 7, 2007

Source: Bloomberg

December 11, 2007 135 of 138Authorized for Public Release

Appendix 2: Materials used by Mr. Madigan

December 11, 2007 136 of 138Authorized for Public Release

Class I FOMC – Restricted Controlled (FR)

Material for FOMC Briefing on Monetary Policy Alternatives Brian Madigan December 11, 2007

December 11, 2007 137 of 138Authorized for Public Release

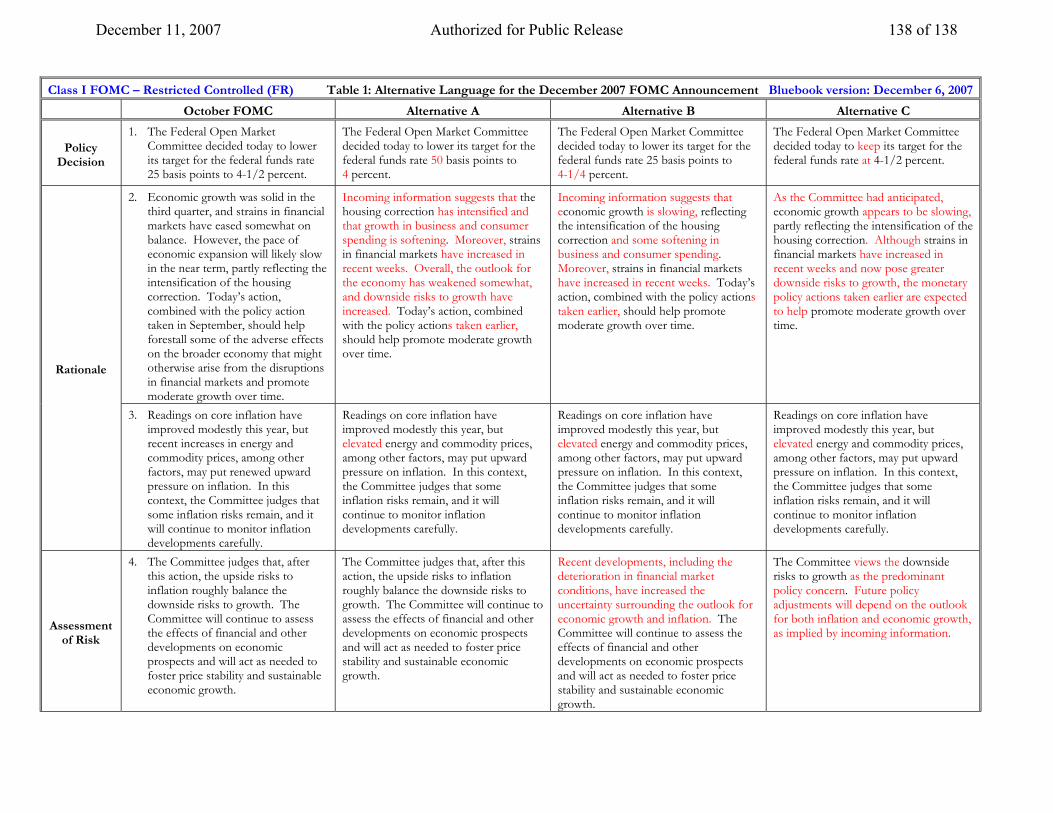

Class I FOMC – Restricted Controlled (FR) Table 1: Alternative Language for the December 2007 FOMC Announcement Bluebook version: December 6, 2007

October FOMC Alternative A Alternative B Alternative C

Policy Decision

1. The Federal Open Market Committee decided today to lower its target for the federal funds rate 25 basis points to 4-1/2 percent.

The Federal Open Market Committee decided today to lower its target for the federal funds rate 50 basis points to 4 percent.

The Federal Open Market Committee decided today to lower its target for the federal funds rate 25 basis points to 4-1/4 percent.

The Federal Open Market Committee decided today to keep its target for the federal funds rate at 4-1/2 percent.

2. Economic growth was solid in the third quarter, and strains in financial markets have eased somewhat on balance. However, the pace of economic expansion will likely slow in the near term, partly reflecting the intensification of the housing correction. Today’s action, combined with the policy action taken in September, should help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in financial markets and promote moderate growth over time.

Incoming information suggests that the housing correction has intensified and that growth in business and consumer spending is softening. Moreover, strains in financial markets have increased in recent weeks. Overall, the outlook for the economy has weakened somewhat, and downside risks to growth have increased. Today’s action, combined with the policy actions taken earlier, should help promote moderate growth over time.

Incoming information suggests that economic growth is slowing, reflecting the intensification of the housing correction and some softening in business and consumer spending. Moreover, strains in financial markets have increased in recent weeks. Today’s action, combined with the policy actions taken earlier, should help promote moderate growth over time.

As the Committee had anticipated, economic growth appears to be slowing, partly reflecting the intensification of the housing correction. Although strains in financial markets have increased in recent weeks and now pose greater downside risks to growth, the monetary policy actions taken earlier are expected to help promote moderate growth over time.

Rationale

3. Readings on core inflation have improved modestly this year, but recent increases in energy and commodity prices, among other factors, may put renewed upward pressure on inflation. In this context, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Readings on core inflation have improved modestly this year, but elevated energy and commodity prices, among other factors, may put upward pressure on inflation. In this context, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Readings on core inflation have improved modestly this year, but elevated energy and commodity prices, among other factors, may put upward pressure on inflation. In this context, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Readings on core inflation have improved modestly this year, but elevated energy and commodity prices, among other factors, may put upward pressure on inflation. In this context, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Assessment of Risk

4. The Committee judges that, after this action, the upside risks to inflation roughly balance the downside risks to growth. The Committee will continue to assess the effects of financial and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

The Committee judges that, after this action, the upside risks to inflation roughly balance the downside risks to growth. The Committee will continue to assess the effects of financial and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

Recent developments, including the deterioration in financial market conditions, have increased the uncertainty surrounding the outlook for economic growth and inflation. The Committee will continue to assess the effects of financial and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

The Committee views the downside risks to growth as the predominant policy concern. Future policy adjustments will depend on the outlook for both inflation and economic growth, as implied by incoming information.

December 11, 2007 138 of 138Authorized for Public Release