focus : macondo: assessing the implications

Post on 21-Jul-2016

215 views

TRANSCRIPT

The explosion, fire and subsequent oil spill from the

well being drilled for BP by Transocean in the Gulf of

Mexico is proving to be a very expensive problem for

the international oil major (see ‘The Month in Brief’).

The ramifications of the disaster go well beyond BP,

however. They have already led to a moratorium on

drilling in the Gulf of Mexico and could slow down or

even prevent exploration in other offshore areas across

the world.

† Actual, January-April * As at 1.1.10 ** Based on current production Source: (Reserves) Oil & Gas Journal

(Other) US Department of Energy

Anatomy of a disaster

On 20th April, 2010, the Deepwater Horizon, a semi-

submersible drilling rig owned and operated by Trans-

ocean, caught fire and sank. The rig was drilling a

prospect known as Macondo, some 50 miles off the

coast of Louisiana, in 5,000 feet of water. BP–along

with its partners Anadarko and Mitsui–acquired the

prospect in 2008 in a sale of leases run by the US gov-

ernment’s Minerals Management Service (MMS).

The well had been drilled to 18,000 feet when a

blowout occurred. The explosion and fire that fol-

lowed killed 11 of the 126-man crew. A day-and-a-

half later, the rig collapsed into the sea and sank, and

oil began to spread across the surface of the water,

eventually making landfall to the north-east.

Various attempts were made to seal the well, which

managed to reduce the volume of oil leaking from the

wellhead but not before an enormous oil-slick had

formed, threatening marine life and beaches. The US

government and the State of Louisiana banned fishing

in waters they controlled; tourist resorts reported that

visitors were staying away; and BP was branded the

villain of the piece.

BP declared itself ready to clean up the oil spill

and put right any damage but was put under consider-

able political pressure to set up an escrow account of

$20 bn to meet an unspecified number of claims for

consequential losses arising from the oil spill. The

company was denounced by US politicians, including

President Barack Obama in what several observers

described as an attempt to improve the President’s

ratings ahead of mid-term Congressional elections

later this year.

The effect on BP was to drive its share price so low

that there were fears for the company’s survival. Ru-

mours soon began to circulate that it was about to be-

come the target of a hostile takeover: possibly by an-

other US oil company, or even a Chinese state oil

company (see ‘Looking Ahead’). A Chinese takeover

is not likely to be welcomed in Washington. Given

BP’s importance as a major producer of oil and gas in

the US, it would not please the US government to see

BP’s North American assets owned–even in part–by

what is likely to be the major competitor-country of

the US in the coming decades.

A campaign began to boycott BP’s petrol-retailing

outlets in several states. Some BP-branded sites re-

ported a drop in sales of up to 40% along the Gulf

Coast, but 5-10% appeared more common. BP an-

nounced that independently-owned sites selling BP

brands would be eligible for financial assistance,

which might be used to enable them to discount their

retail prices.

BP’s Group Chief Executive, Tony Hayward,

warned shareholders that the financial consequences

of Macondo would be ‘severe’, though the company is

cushioned to a considerable extent by its strong cash

flow and the low level of company borrowings, which

should enable it to increase debt levels. It could also

sell some of its non-core assets.

PADD = Petroleum Administration District for Defence PADD 3 = Gulf of Mexico PADD 5 = US West Coast Source: US Department of Energy

Table A US: Oil Reserves and Production, 2010 †

Proven Reserves: 19.1 billion bbl * Reserves remaining: 7.1 years ** (th bpd) Crude Oil

Lower-48 States 4,836 Alaska 636 Total 5,472

NGL Total 1,953

Crude + NGL Total 7,425

Table B US: Offshore Production, 2009

Region Production (th bpd) Federal Offshore

PADD 3 1,540 PADD 5 61 Total 1,601

State Offshore Alaska 203 California Louisiana 65 Texas Total 268

Federal + State Offshore Total 1,869

FOCUS

Macondo: Assessing the implications

© Blackwell Publishing Ltd, 2010

Drilling suspended

There are potentially serious consequences for the US

as well. Before the Macondo disaster, President

Obama had talked of allowing new sections of the US

coastline to be explored for oil, for which he received

much criticism. Following the blowout, the govern-

ment dropped this idea and imposed a six-month

moratorium on the drilling of new deepwater wells in

the US Gulf. In the short term, this could lead to a

drop in US output and in the longer term it may re-

quire a fundamental rethink of US energy policy.

US oil production has been declining since 1970,

and reserves are sufficient for only seven years’ pro-

duction at current levels (see Table A). The decline

appeared to have been halted, however, in 2009,

when output rose by nearly 9%. Much of the new

production responsible for stemming the fall came

from the Gulf of Mexico–together with a rise in out-

put of natural gas liquids.

Source: US Department of Energy

Offshore output

Offshore output in 2009 was higher than in any of the

traditional oil states, like Texas, Alaska and Califor-

nia (see Tables B and C). Production offshore is con-

trolled by the federal or state authorities. Most of it

comes under the federal government, but four states–

Alaska, California, Louisiana and Texas–control

268,000 bpd of offshore production.

Most of the federal production is in the Gulf of

Mexico, with the remainder sited off the West Coast

(see Table B). The total federally- and state-

controlled production in the Gulf is about 1.6 mn bpd.

Before Macondo, it seemed likely that the explora-

tion of the US Continental Shelf would spread–both

to other areas of coastline and also deeper into the

Gulf of Mexico. The Macondo well was in some

ways a test-case for the feasibility of drilling at much

greater depths.

Proposals to increase offshore exploration were

driven by the desire of successive US governments to

Source: US Department of Energy

reduce the country’s reliance on imports, which now

exceed domestic production by a considerable mar-

gin. In 2009, net imports accounted for 52% of US

demand and exceeded US production by 35% (see

Table C US: Crude Oil Production by Region, 2009

Region Production (th bpd) Texas 1,080 Alaska 645 California 568 Colorado 350 North Dakota 218 Louisiana 198 Oklahoma 164 Wyoming 137 Kansas 106 Others 1,844 Total 5,310

Table D US: Oil Balance, 2009

(th bpd) Crude Oil 5,310 NGL 1,886 Total Production 7,196 Imports 11,726 Exports 2,026 Net Imports 9,700 Petroleum Products Supplied 18,686 Processing Gains 981 Oxygenates 735 Stock Change 112 Adjustments 186

© Blackwell Publishing Ltd, 2010

4 OIL AND ENERGY TRENDS, 16 JULY 2010 FOCUS

WHAT NOW FOR THE OIL INDUSTRY? A number of countries have responded to Macondo by an-

nouncing reviews of their offshore regulations covering explo-

ration and production. New regulations will inevitably slow

down offshore developments and increase costs. Industry

sources estimate that costs will rise by at least 10% in the ar-

eas affected.

In the US, the Gulf of Mexico is the most obvious

target for new regulation, particularly following the reorgani-

zation of the Minerals Management Service (see text), which

some saw as providing inadequate levels of supervision over

offshore drilling. Another important area to be affected may

be the Arctic continental shelf off Alaska, which several in-

dustry observers believe contains large volumes of natural gas.

Another impact in the US may be to reduce the role of

the smaller independent exploration and production compa-

nies, which are already affected by the current federal morato-

rium on drilling and now appear to face a rise in operating

costs and insurance payments as well.

The UK has responded by announcing a doubling of

the number of annual inspections of offshore rigs.

The governors of Nigeria’s oil-producing states have

called on the federal government to tighten regulations in an

area that has seen several oil-spills. ExxonMobil is in trouble

with the state authorities of Akwa Ibom for an offshore oil-

spill from a pipeline supplying the Qua Iboe export terminal.

Other countries that have announced reviews of off-

shore safety include Brazil, Canada, China, Ireland, Nor-

way, and Russia.

Some parts of the oil industry may yet benefit from the

Macondo disaster: those proposing to drill onshore. Several

small fields have been identified in Dorset, in Southern Eng-

land which may represent a safer form of oil exploration than

the deep offshore. Other countries where onshore exploration

may increase are Germany and Poland.

Table D).

There have been numerous attempts over the years

to reduce US reliance on oil in the total energy bal-

ance, but oil remains easily the largest component, at

nearly 40% (see Table E). Natural gas has increased

its share in recent years, but this has been on the back

of rising domestic production. While the Macondo

incident affects mainly oil, there are as yet unmeasur-

able consequences for gas, which also has its safety

problems (see ‘The Month in Brief’).

US outlook

Offshore production was largely responsible for the

largest annual increase in US production since 1970

last year. The moratorium on drilling could affect US

output as early as the fourth quarter of 2010. The US

Department of Energy expects the drilling ban to re-

duce output by 26,000 bpd during the fourth quarter

and by 70,000 bpd in 2011, compared with previous

projections for those periods. Other sources project

higher losses. Some analysts predict reductions of

150,000 bpd next year.

The company most affected will be BP. It is the

largest producer and holder of acreage in the Gulf of

Mexico: it is also a major player in other parts of the

US. All companies involved in the offshore sector

are likely to see their costs rise as new restrictions in

drilling are brought in, as well as seeing projects that

were due to be commissioned in the next few years

delayed.

Source: BP Statistical Review of World Energy, 2010

International implications

The fall-out from Macondo has spread well beyond

the US. Other countries are re-examining their up-

stream regulations with an eye to preventing any re-

peat of the disaster. Among the areas that could be

affected are the North Sea and offshore West Africa

and Brazil. The immediate reaction, however, in

many areas has been non-committal.

The British government says it has no plans to ban

deepwater exploration off the Shetland Islands,

though it will increase inspections of existing off-

shore fields (see box). The Macondo disaster may

stimulate more onshore exploration, though.

Iraq is also promoting itself as a ‘safer’ oil prov-

ince. Whilst there have been calls in Nigeria and Bra-

zil for more stringent controls on offshore drilling,

there is no sign so far of any delay to future projects.

Canada may be the first country outside the US to

introduce new regulations. The areas affected could

Table E US: Energy Balance, 2009

Fuel Consumption (mntoe) (%) Oil 842.9 38.6 Natural Gas 588.7 27.0 Coal 498.0 22.8 Nuclear Power 190.2 8.7 Hydro-electricity 62.2 2.9 Total 2,182.0 100.0

© Blackwell Publishing Ltd, 2010

OIL AND ENERGY TRENDS, 16 JULY 2010 5 FOCUS

Source: IEA; WEO; APICORP

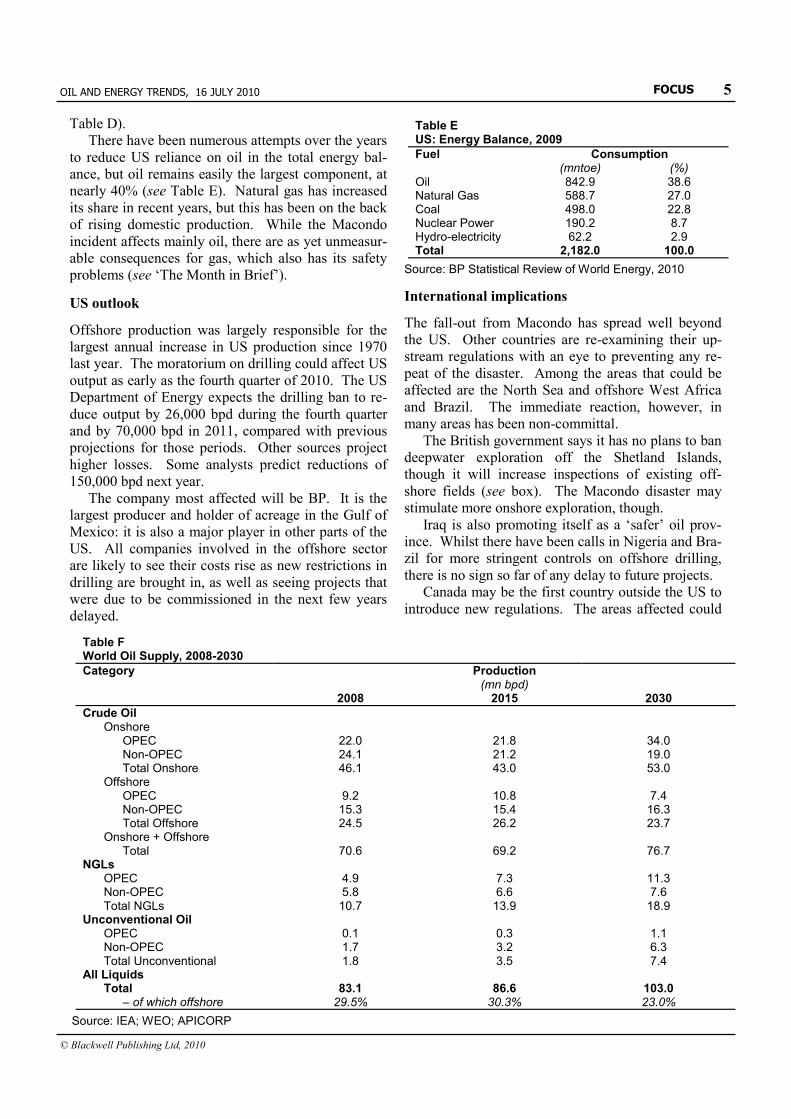

Table F World Oil Supply, 2008-2030

Category Production (mn bpd) 2008 2015 2030

Crude Oil Onshore

OPEC 22.0 21.8 34.0 Non-OPEC 24.1 21.2 19.0 Total Onshore 46.1 43.0 53.0

Offshore OPEC 9.2 10.8 7.4 Non-OPEC 15.3 15.4 16.3 Total Offshore 24.5 26.2 23.7

Onshore + Offshore Total 70.6 69.2 76.7

NGLs OPEC 4.9 7.3 11.3 Non-OPEC 5.8 6.6 7.6 Total NGLs 10.7 13.9 18.9

Unconventional Oil OPEC 0.1 0.3 1.1 Non-OPEC 1.7 3.2 6.3 Total Unconventional 1.8 3.5 7.4

All Liquids Total 83.1 86.6 103.0

– of which offshore 29.5% 30.3% 23.0%

Iraq’s oil production and exports rose during May

following a decline earlier in the year. May’s exports

were 1.9 mn bpd, according to the Oil Ministry; but

exports were hit during June when the export pipeline

to Ceyhan was bombed. The line was closed for four

days early in the month whilst the bomb damage was

repaired; but there was a further interruption to ex-

ports later in the month because of what was de-

scribed as ‘a small leak’.

The pipeline is still operating well below its

1.5 mn bpd capacity. May’s throughput is estimated

at 440,000 bpd. Problems with exports have also

been reported in the south. Iraq has been adding

nearly 50,000 bpd of surplus heavy fuel oil to its Bas-

rah oil blend, which has led to a reduction in the

crude’s gravity of 2°API. The Iraqis have also been

disposing of heavy residue by slugging it into the

Kirkuk crude export stream, with similar results.

There is growing concern inside Iraq about the

current level of oil production. The government has

ambitious plans to increase production following the

award of service contracts to 16 oil companies for

work in 11 oilfields. In early June, the country’s Oil

Minister, Hussain al-Shahristani, announced a target

of ‘more than 11.6 mn bpd’ for 2016, compared with

the present production of about 2.3 mn bpd. Even at

its highest since the US-led invasion of 2003, Iraq’s

production has not exceeded 2.5 mn bpd. Current

concern is with the Rumailah oilfield in southern Iraq

where some wells are reported to have been invaded

by water. The government nevertheless hopes for an

early increase in the output of the Nassiriyah field

from 10,000 bpd to 50,000 bpd as a result of a drilling

programme there.

Total has become the latest company to announce

it is suspending its sales of gasoline to Iran. Gasoline

imports by Iran have fallen by about 15,000 bpd since

the end of March, to 115,000 bpd. In June, the US

Congress voted for increased sanctions against Iran in

protest against Tehran’s nuclear programme. Nige-

ria’s 100,000 bpd EA field has started production fol-

lowing repairs to loading facilities. Exports, how-

ever, have not been resumed. Thailand has revived a

proposal for a scheme to allow oil tankers to bypass

the congested Strait of Malacca by constructing a

1.5 mn bpd pipeline across the south of the country.

There is a further plan to build new oil refineries at

either end of the pipeline. Russia says it wants to

build oil storage facilities at home and overseas to

handle its exports of crude oil. Saudi Arabia has

signed an agreement with Japan to enable it to store

up to 3.8 mn bbl of its crude on the island of Oki-

nawa. The facility will be operated on a commercial

basis but Japan will have first call on the oil in any

international emergency.

BP’s American outlets have been threatened with

boycotts following the explosion and oil spill at

Macondo in the Gulf of Mexico (see ‘Focus’). BP

has been strongly criticized by US President Barack

Obama in what some US observers see as a campaign

to improve his image in advance of mid-term Con-

gressional elections. The incident has damaged BP’s

image and its share price, which has fallen to 14-year

lows. In an unconnected incident, there was a fatal

explosion at a natural gas pipeline owned by Enter-

prise Products Partners in Texas, which led to calls

for more stringent controls on some US gas develop-

ments.

Dubai is considering switching its power stations

to coal as its oil production declines. Pakistan has

told foreign airlines to bring their own fuel, since

there is not enough kerosene available at its airports.

Mexico’s national oil company, Pemex, has accused

US and other foreign companies of buying conden-

sate stolen from its road tankers and storage facilities.

India’s largest private retailer, Essar Oil, is to expand

its network there as a result of the government’s deci-

sion to deregulate the pricing of petrol.

Vietnam is offering stakes in its new Dung Quat

refinery and its proposed Long Son unit to foreign

6 OIL AND ENERGY TRENDS, 16 JULY 2010 FOCUS

© Blackwell Publishing Ltd, 2010

THE MONTH IN BRIEF

Iraq’s exports rise, Iran’s imports fall and BP is in trouble

This section summarizes downstream developments of the previous month. Exploration & Production are

covered in ‘Upstream Review’.

be the Atlantic and Pacific coasts and the Arctic conti-

nental shelf. It looks unlikely, for example, that an

existing moratorium on drilling off British Columbia

will be lifted in the foreseeable future. Furthermore,

events at Macondo may make it much harder for Can-

ada’s Enbridge to build an export terminal to handle

crude produced from oilsands in the north of the Prov-

ince.

Offshore outlook

The importance of the wider impact of Macondo may

be gauged from the results of a recent forecast by the

International Energy Agency. The Agency predicts

that offshore oil production will rise by 1.7 mn bpd, or

7%, between 2008 and 2015 and that its share in world

production will rise as a result (see Table F).