fiscal policy in the monetary union: the stability and growth pact week 7 ch.10

TRANSCRIPT

FISCAL POLICY IN FISCAL POLICY IN THE MONETARY THE MONETARY

UNION: THE UNION: THE STABILITY AND STABILITY AND GROWTH PACTGROWTH PACT

Week 7Week 7

Ch.10Ch.10

ReferencesReferences

• De Grauwe, P. chapter 10

• Reading material:1) De Grauwe, P. (2003), “The Stability and Growth Pact in

Need of Reform”(written before the 2005-reform, which we’ll investigate next

time).2) “Ties that bind” (2004), article from The Region3) “Reform of the Stability and Growth Pact” - article from

“Monetary Policy and the Economy”4) “The Reform of the SGP: an Assessment” – Speech by Josè –

Manuel Gonzalez-Paramo, member of the Executive Board of ECB – Frankfurt – October 2005.

LECTURE PLANLECTURE PLAN

• In a monetary union (=one currency, one monetary policy) should we maintain national fiscal policy?

• Yes. “ What else do you wanna take out of our hands?!?!” – the OCA criticism

• No. “Monetary union cannot work without contraints on national fiscal policies”- the SGP

1) THE ROLE OF FISCAL POLICY IN A 1) THE ROLE OF FISCAL POLICY IN A MONETARY UNIONMONETARY UNION

• What is (macro) economic policy?• a) Monetary policy: movement of short-term

interest rate (i) in order to affect GDP (via consumption and investment)

• b) Exchange-rate policy: movement of nominal exchange rate (E) in order to affect balance of payments- current account (export minus imports) and GDP

• c) Fiscal policy : movement of government spending (G) to affect directly GDP, and taxation / transfers to affect consumption and then GDP (maybe! If….)

• In a monetary union:• a) is managed by ECB

• b) disappears together with national currencies

• c) is the only macroeconomic policy tool left in national hands.

• How it should be used?

Recall Optimal Currency Area (OCA) Recall Optimal Currency Area (OCA) theorytheory

• OCA= a monetary union can take place only among countries which form an optimal currency area.

• How do we define it?• If these countries are hit by an asymmetric shock, there

must be enough:• - wage flexibility• - labour mobility• so to allow the equilibrium to be restored. • Why? Because there’s no much of national macroeconomic

policy left to be fired at asymmetric shocks. So there’d better be some real mechanism able to correct the situation.

France Germany

YFYG

PF PG

DF

D’F

D’G

DG

SF

SG

TWO CASESTWO CASES

• 1) Monetary union with budget centralization (=common fiscal policy)

• 2) Monetary union without budget centralization (=national fiscal policy)

• In case 1):• - there is risk sharing: the centralized budget

(automatically) redistributes income from Germany to France

• In case 2):• - Germany accumulates fiscal surplus (reduces

deficit) and reduces debt• - France increases deficit and debt• - we have inter-generational transfer: hardship

today is paid for by future generations.• If financial markets work efficiently, the risk-

sharing can be accomplished also in case 2), so with no need of common fiscal policy.

• A window on the future: COMMON FISCAL POLICY and INTEGRATION OF FINANCIAL MARKETS are going to be the two next (and final) topics.

• Important: this insurance system (=transfer of resources) can only be temporary, otherwise we’ll have a permanent transfer of resources towards the negatively-hit country, which can be hardly sustainable from a political point of view in the EU.

• If the shock is permanent, factors stressed by OCA have to move (price and wage flexibility, labour and capital mobility) in order to permanently correct the situation.

• Example: Southern Italy

So……So……

• It would be best to have a centralized budget (=common fiscal policy) to be able to deal with asymmetric shock

• If this is not possible, then fiscal policy (the only macroeconomic policy tool left) must be managed at national level, and used in a flexible way (=no limits), in order to fight adequately asymmetric shocks.

• SO THIS VIEW ARGUES FOR NATIONAL AND INDEPENDENT FISCAL POLICY IN A MONETARY UNION.

• Is that really the case?!?!?!

FISCAL RULES TO MAKE EMU WORKFISCAL RULES TO MAKE EMU WORK

• What does it mean to have a single currency?• Having a single (short-term) interest rate,

manouvred by a common central bank.• As we have repeatedly seen, this interest rate

determines (directly or indirectly) the whole structure (=term structure) of the many interest rates in the economy. For the whole Union.

• For the whole Union.• For the whole Union.• For the whole Union.

• So national states, around the Union, cannot implement policies that put upward / downward pressure on the interest rate.

• Because now the interest rate is common.• Guess what are the policies that usually put the

most (upward) pressure on the interest rate structure?

• FISCAL POLICY• Debt issuing increases interest rate:• 1) Financial-market effect• 2) Risk-premium effect

SOMEONE QUESTIONS THE SOMEONE QUESTIONS THE RELEVANCE OF BOTH CHANNELSRELEVANCE OF BOTH CHANNELS

• 1) Financial Market-effect: in a 15 (and more) member monetary union, the impact of a single country’s fiscal indiscipline on EMU interest rate is negligible (1% deficit increase, 0.1% national interest rate increase)

• HOWEVER……• a) Slovenia or Germany?!?! (differences in sizes)• b) Dangerous talking…….what if everybody start

thinking this way?!

• 2) Risk-premium effect: “there is the no-bail-out clause”!!!!

• HOWEVER….• You can write all the no-bail-out clause you

want….when a country is in financial trouble, central banks do step in to save it.

• Even when a simple commercial bank is in trouble, central banks do the same…….any example recently?!?!?!

• Northern Rock (nationalized by BoE), Bear Sterns (saved by Fed the other day).

A row-boat with 15 people and some smart A row-boat with 15 people and some smart assass

• A fiscal expansion has a benefit (increased aggregate demand and output) and a cost (increased interest rate).

• In a monetary union, countries can benefit from fiscal expansion while spreading the costs on everybody else.

• The upward pressure on the interest rate, in fact, is beared by the whole Union.

• It’s like someone suddenly stops rowing and lays back enjoying the sun. The boat still goes…..other people have just to row more intensively.

The “old” SGP (1997)The “old” SGP (1997)• 1) In the short-run, member States

should not exceed 3% limit for their deficit / GDP ratios.

• 2) In the medium run, member States should achieve balanced budget positions

What if they don’t?What if they don’t?

- Ecofin (on the basis of Commission’s proposal) issues an early warning.

- If the country does not get back below 3%, Ecofin imposes a fine equal to 0.2% of its GDP plus 0.1% for every percentage point of violations, up until a maximum fine of 0.5% of GDP.

- After two years, if the country has met the 3% limit it gets its money back; otherwise, it looses permanently the deposit (which is equally spread to other member states).

- A budget deficit in excess of 3% can be tolerated if considered as resulting from “exceptional circumstances” : natural disaster, or a severe (more than minus 2% drop in annual GDP growth) economic downturn.

- If the downturn is between minus 0.75% and minus 2% the country can present arguments in order to justify the excess deficit.

Stability and Growth Pact: Stability and Growth Pact: short-run short-run prescriptionsprescriptions

• EMU is: having a common interest rate• To make it sustainable, there can’t be pressure

on the interest rates coming from national and independent fiscal policies.

• Opposite view to the earlier one (national flexibility).

• So we need common rules for national fiscal policies in the short-run.

• But what rules exactly?• Rescue the fourth Maastricht criterion:• Deficit / GDP ratio = 3%

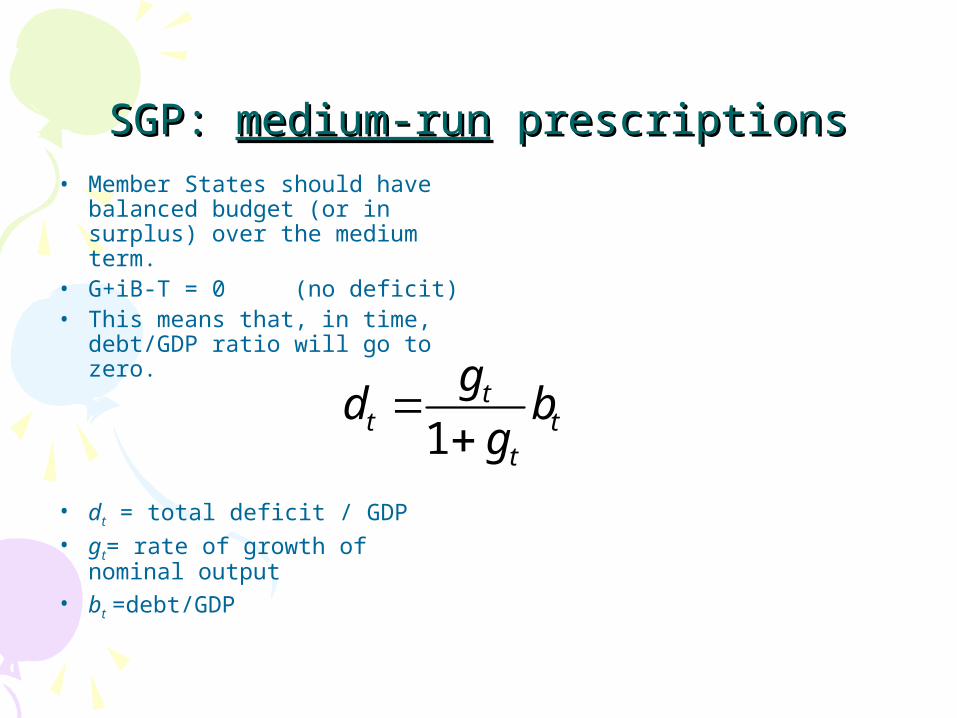

SGP: SGP: medium-runmedium-run prescriptions prescriptions• Member States should have

balanced budget (or in surplus) over the medium term.

• G+iB-T = 0 (no deficit)• This means that, in time,

debt/GDP ratio will go to zero.

• dt = total deficit / GDP• gt= rate of growth of

nominal output• bt =debt/GDP

1t

t tt

gd b

g

• Or, if you prefer:• ABSOLUTE LEVEL:

• Since Bt = Bt-1 +Dt

• If Dt = 0

• B remains fixed at Bt-1 and stays there.

• Now go back to the RELATIVE LEVEL:• B / Y• If the numerator stays fixed and the denominator

keeps growing, sooner or later the fraction will go to zero.

• So the medium-run prescription of the SGP seems to suggest that the long-term debt/GDP ratio should be 0.

Is that desirable?Is that desirable?• No.• Debt is a rational way to finance all those expenditure that

benefit current AND future generations.• Debt issuing, in fact, is a way to make future generations

pay (through future interest payments, or debt service).• There are a lot of public expenditure that fall into this

category (infrastracture, etc). Rigorously, they should be financed mainly by debt emission, so to spread their financing over next generations.

• So a zero level of debt is not optimal. It means:• Either that we are not doing any investment• Or that part of those that will benefit from it (future

generations) will have it for free.

So why the medium-run prescription?!So why the medium-run prescription?!

• Remember potential GDP? The structural level (or the structural rate of growth) of output (determined ultimately by total factor productivity and population growth).

• Every year actual GDP fluctuates around potential output.

• It can be above: the economy is operating above its potential (=inflationary pressures).

• It can be below: the economy is not exploiting all its potential.

• Don’t get confused with recession: two quarters of negative growth.

One step back: how can fiscal policy affect One step back: how can fiscal policy affect GDP?GDP?

• Fiscal policy affect aggregate demand (and hence GDP) via:

1) Government spending (goods, services, investment): it directly creates demand

2) Taxation: it affects private consumption by increasing / decreasing consumers’ disposable income

3) Transfers (social security, unemployment benefits, and so on): same as taxation

DEFICIT = 1+3 -2 = G+Tr – T

How does fiscal policy reacts to GDP How does fiscal policy reacts to GDP movements?movements?

1) When GDP is below potential (or even in recession):a) Increase Gb) Decrease Tc) Increase Tr = INCREASING THE DEFICIT

So that aggregate demand increases and GDP growth can go back to potential.

2) When GDP is above potentiala) Decrease Gb) Increase Tc) Decrease Tr = REDUCING THE DEFICIT

So that the economy cools down and avoid inflationary pressures.

• Fiscal policy aimed at stabilizing the economy moves the deficit in a counter-cyclical fashion:

• Stimulate aggregate demand (=increase the deficit) when the economy is below potential

• Cool down aggregate demand (=reduce the deficit) when the economy is above potential

• In this way, fluctuations of GDP (=volatility) is minimized (=reduction of uncertainty, etc).

• ………but……

• To be able to implement counter-cyclical fiscal policy the deficit must be zero when GDP is in line with potential.

• So that it has a lot of “room to manouvre” (for example, 3% of GDP!!!!) when the economy needs a shot in the arm.

• But government has to save (=reduce the deficit) when GDP is above potential.• SAVE DURING GOOD TIMES, TO BE ABLE TO SPEND (AND SPEND A LOT) WHEN YOU REALLY

NEED IT.• That’s why SGP prescription: in the medium run keep the deficit in balance (we assume that

in the medium run GDP is in line with potential, simply because that’s the way it’s computed).

Can governnment resist temptation?Can governnment resist temptation?• What temptation?• To spend in bad times but also in good times.• To be able to implement counter-cyclical fiscal

policy you need to save during good times (=reducing the deficit when GDP is above potential).

• If you fail to do that (possibly due to political cycles) you simply watch your deficit grow, with the risk of being forced to reduce it (=restrictive fiscal policy) when the economy is below potential or even in recession.

• This is exactly what happened with the Stability and Growth Pact.

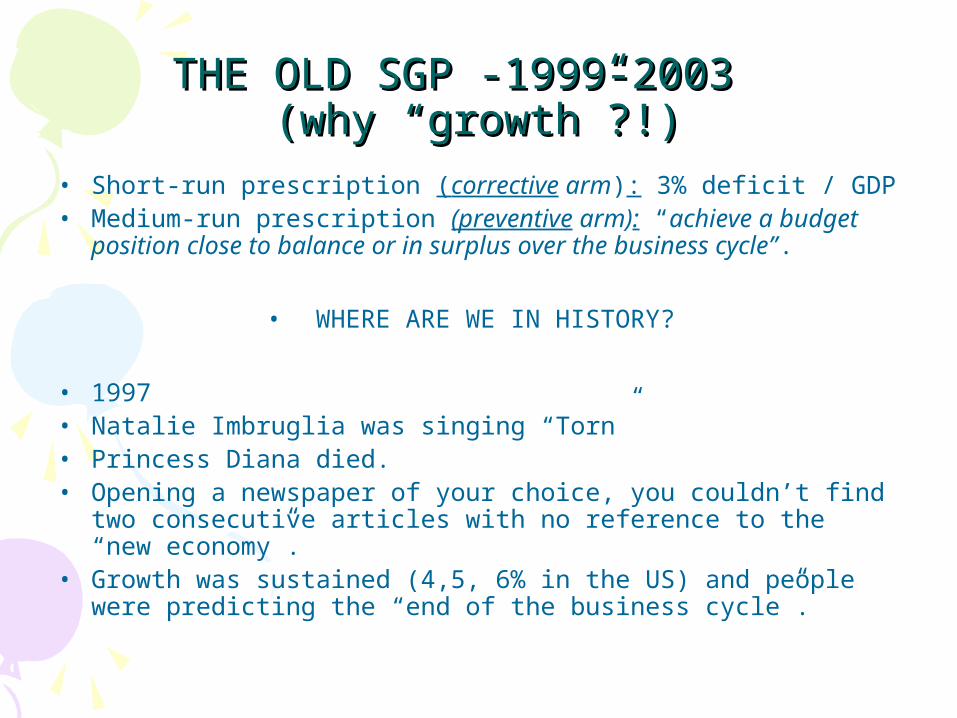

THE OLD SGP -1999-2003 THE OLD SGP -1999-2003 (why “growth”?!)(why “growth”?!)

• Short-run prescription (corrective arm): 3% deficit / GDP• Medium-run prescription (preventive arm): “achieve a budget

position close to balance or in surplus over the business cycle”.

• WHERE ARE WE IN HISTORY?

• 1997• Natalie Imbruglia was singing “Torn”• Princess Diana died.• Opening a newspaper of your choice, you couldn’t find two

consecutive articles with no reference to the “new economy”. • Growth was sustained (4,5, 6% in the US) and people were

predicting the “end of the business cycle”.

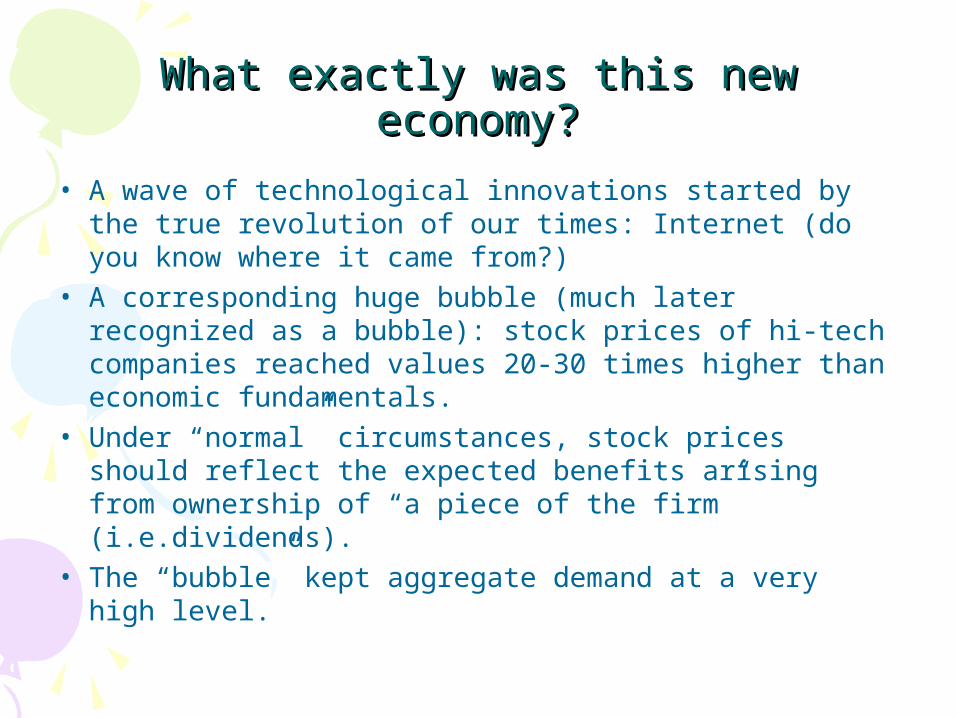

What exactly was this new economy?What exactly was this new economy?

• A wave of technological innovations started by the true revolution of our times: Internet (do you know where it came from?)

• A corresponding huge bubble (much later recognized as a bubble): stock prices of hi-tech companies reached values 20-30 times higher than economic fundamentals.

• Under “normal” circumstances, stock prices should reflect the expected benefits arising from ownership of “a piece of the firm” (i.e.dividends).

• The “bubble” kept aggregate demand at a very high level.

Here’s the question….Here’s the question….

• Was the exceptional growth in the second half of the 90s result of higher potential growth (= effects of the “new economy” revolution on total factor productivity) or a result of sustained aggregate demand growth (=coming from the new economy bubble?).

• In the first case: growth is structural• In the second: growth is temporary and will go

back to the potential level sooner or later.• We don’t know yet. But the second explanations

played a greater role than we though, and the first one wasn’t as important as we hoped it’d be.

Some more elementsSome more elements

• Those stock market values (so much disentangled from real fundamentals) couldn’t last forever.

• In March 2000 the Nasdaq collapsed.• Aggregate demand stopped.• 9/11 did the rest.• Fed cut aggressively the interest rate (it reached

1% in 2003), in the desperate attempt to support aggregate demand.

• It succeeded, but it laid the foundations for future problems.

• a) House bubble.• b) Derivatives and subprime.

Anyway, let’s not get carried away….Anyway, let’s not get carried away….

• The exceptional growth in the second half of the 90s wasn’t as structural as we thought.

• It’s a common error. Between 70s and 80s the opposite mistake was made by economists and policy-makers.

• In Europe, relying on a nominal growth of 5% (=real growth of 3%) was the most evident consequence of those years’optimism (end of Cold War, democracy, emerging countries, and so on).

• During those “good times”, EMU countries didn’t bring their budget “close to balance or in surplus”

• When the business cycle turned bad, at the beginning of the millennium, not surprisingly EMU countries started to break the 3% ceiling of the SGP.

Paramo speech (material n.2), pag.3Paramo speech (material n.2), pag.3

• “Since then, (after entering the euro in 1997),some euro-area countries have succedeed in maintaining progress with fiscal consolidation. But in a number of others, fiscal consolidation has either stalled or even gone into reverse. At first this lack of improvement or even deterioration of fiscal positions was masked by a friendly economic climate. Nominal fiscal balances improved considerably between 1997 and 2000. But this improvement was largely cyclical. And when growth subsequently slowerd, fiscal balances in some countries quickly deteriorated to reach levels close to, or above 3% of the GDP”.

CALENDAR OF VIOLATIONSCALENDAR OF VIOLATIONS

• 2001: Portugal (EDP started in 2002)• 2002: Germany and France• 2003: Greece and Netherland (2004 Italy).• In November 2003, Ecofin was supposed to start

the Excess Deficit Procedure against Germany and France.

• Their hands trembled in that moment.

• The application of SGP was suspended.

• EU commission brought legal action to the European Court of Justice, which in July 2004 basically said something like… “What can I say my dear, you are right, but let’s face it…. national government still run Europe integration process!”

• NEVER-ENDING CONFLICT OF THE EU NATURE: FEDERAL STATE OR INTERNATIONAL

ORGANIZATION ?

No further step of European integration can ever be taken if this question does not receive an

adequate answer.

So….So….• Since we still need fiscal rules to have a well-

functioning monetary union…..how do we change the SGP?!?!

1) Change the numbers, making sure that this time we get the growth right?!?!?!

• No, loss in credibility would be too high.2) “Golden rule”: distinguish between government

expenditure in investment (which are good for growth) and public consumption.

No. You would spend the next ten years establishing what’s investment and what’s public consumption.

And who said that all investments are good for growth and all kinds of public consumption are not?!

2020thth MARCH 2005: THE REFORM OF MARCH 2005: THE REFORM OF THE SGPTHE SGP

• SHORT TERM PRESCRIPTIONS (or corrective arm):• 3% limit is maintained.• - Tolerance is extended to include: a) periods of negative growth b) prolonged periods of growth below

potential c) structural reforms that the government is implementing. Structural reforms have clear upfront fiscal costs but

potential long-term benefits that could justify temporarily higher deficits.

• MEDIUM TERM PRESCRIPTIONS (or preventive arm):• The ultimate goal (pushing member States to run counter-

cyclical fiscal policies) is maintained.• Countries should cut their cyclically-adjusted budget deficit

(net of one-off and temporary measures).• Target and adjustment path of this cut have changed:• a) the Medium- Term- Objective is specified within a

corridor ranging from 1% of deficit to a small surplus.• b) the speed of adjustment must be on average 0.5% per

year, depending on the state of the national business cycle.

• a) and b) are no longer uniform but are country-specific, and are defined according to:

• - state of the business cycle• - level of the debt/GDP ratio• - potential growth• - population aging

• At the end of the day, there are only two words we can use to summarize the reform

of the SGP:

• MORE FLEXIBILITY • (within the same rationale and same

ultimate goals)

The unplesant downside of The unplesant downside of flexibility….flexibility….

• How long is the prolonged period of negative growth or growth below potential ?

• Who decides in real time the correct estimation of potential growth (one of the hardest thing to measure in economics)?

• All accountants in Europe couldn’t agree on the exact specification of the terms “one-off” and “temporary measures”….

• ….but that’s nothing compared to the fights we could have deciding what are structural reforms or how to measure the impact of aging population on public finances….

• Is the “federal state” strong enough to handle potentially 27 different country-specific medium-term objectives?

On the other hand….positive sides of On the other hand….positive sides of the 2005 reformthe 2005 reform

• - debt / GDP ratio (the source of all problems….) plays a bigger role in determining the sustainability of member States’ fiscal positions

• - the use of cyclically-adjusted deficit net of one-off and temporary measures is able to identify much more adequately the fiscal stance of a country

• - it partially settles another “injustice”…..public expenditure is not all the same.

• - it manages to inject more flexibility in the system without loss in credibility

• But maybe it’s too early to establish that.

CONCLUSIONSCONCLUSIONS

• MACROECONOMIC POLICY: monetary, exchange rate and fiscal policy.

• In a monetary union, fiscal policy is the only one left in national hands.

• While we wait that the political integration makes possible a common fiscal policy (week 12), should they be used in a flexible way (to contrast asymmetric shocks) or rather subject to rules?

• Although some still argue for total flexibility (“is US fiscal policy subject to any rules”?!), we proved that a monetary union needs fiscal rules in order to function.

Why?Why?• The need to finance a large stock of public debt pushes up

interest rate (via at least two channels)• Fiscal expansions boost national aggregate demand, which

gives rise to national inflationary pressures

Both these aspects are not-compatible with a monetary union, where monetary policy (=determination of short term interest rate, who affects the whole term structure) is managed by ECB and has the explicit task of fighting inflation.

Allowing full flexibility of national fiscal policies, allow member States to enjoy the benefits of them (=aggregate demand expansion) without paying the costs (=higher interest rate).

The Old SGP (1999-2003)The Old SGP (1999-2003)

• 3% limit for deficit/GDP ratio with tolerance only in case of severe economic downturn (-2% of GDP)

• Balance budget (for everyone) over the medium term.

• Why didn’t it work?• 3% limit was designed under too generous growth

assumptions.• Countries didn’t manage / didn’t want to implement

fiscal consolidation when the business cycle was good (1997-2000), so they rapidly went into troubles when the economic climate changed.

The New SGP (2005 onwards)The New SGP (2005 onwards)

• More flexibility on both short term and medium term prescriptions.

• For the latter, objectives are no longer defined uniformly but depending on country-specific conditions.

• More tolerance.• In 2008, all indisciplined countries came out of

the EDP (Italy in May 2008).• But the enforceability (and the success) of the

new SGP remains a question.

AndAnd now..?now..?COUNTRY DEFICIT 2009

Ireland 11%

France 6.2%

Spain 5.4%

Portugal 4.6%

Italy 3.8%

Germany 2.9%

Greece 3.7%

Belgium 3%

EURO AREA 4%