first edition global economic issues and policies

Post on 19-Dec-2015

216 views

TRANSCRIPT

First edition

Global Economic Issues and Policies

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–2

1. Your Name (First and Last); Include your ID #

2. List of Economics course you have taken so far

3. Briefly describe how you want the lectures/ discussions/tests on this course to be organized

On the Front side

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–3

• What is the most Important GLOBAL ISSUE today? Why?

On the back side

First edition

Global Economic Issues and Policies

Chapter 1

Understanding the Global Economy

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–5

1. Why study global economic issues and policies?

2. How important is the global market for goods and services?

3. How important are the international monetary and financial markets?

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–6

4. What are market supply and demand?

5. What are consumer surplus and producer surplus?

6. How are market prices determined?

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–7

Global Economic Policy and Issues

• GlobalizationThe increasing interconnectedness of peoples and

societies and the interdependence of economies, governments, and environments.

• Economic IntegrationThe extent and strength of REAL-SECTOR and

FINANCIAL-SECTOR linkages among national economies.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–8

The Global Market for Goods and Services

• Real SectorA designation for the portion of the economy

engaged in the production and sale of goods and services.

• Financial SectorA designation for the portion of the economy in

which people trade financial assets.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–9

Global Economic Policy and Issues

• Economic IntegrationThe extent and strength of REAL-SECTOR and

FINANCIAL-SECTOR linkages among national economies.

Depends on… The volume of international trade in the real sector The global market for goods and services The volume of trade in the international monetary, and

financial markets

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–10

Table 1-1

The Top Twenty Globalized Nations

Source: Foreign Policy http://www.foreignpolicy.com.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–11

Figure 1-1

Growth of Global Trade in Goods and Services:

Source: International Monetary Fund, World Economic Outlook, various issues.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–12

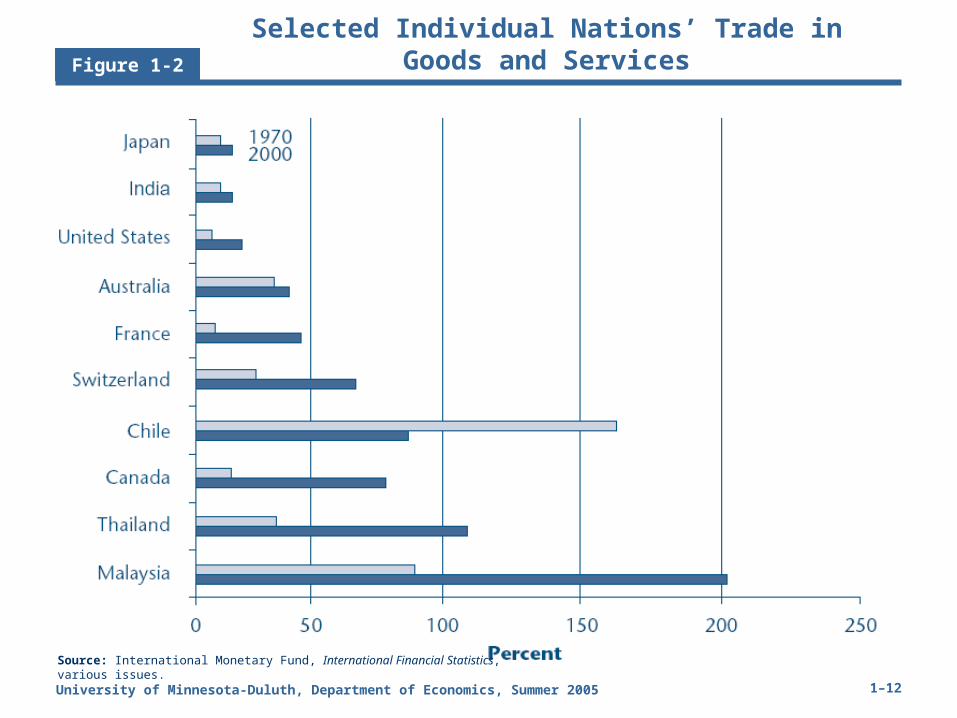

Figure 1-2

Selected Individual Nations’ Trade in Goods and Services

Source: International Monetary Fund, International Financial Statistics, various issues.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–13

The International Monetary and Financial Markets

• Foreign Exchange MarketA Market (involving private banks, foreign

exchange brokers, and central banks) through which households, firms, and governments buy and sell national currencies.

• Foreign Direct InvestmentThe acquisition of assets that involves a long-term

relationship and controlling interest of 10 percent or greater in an enterprise located in another economy.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–14

Table 1-2

Annual Turnover (Value) in Foreign Exchange Markets

Source: Held, David, Anthony McGrew, David Goldblatt, and Jonathan Perraton, Global Transformations, p. 209; Bank for International Settlements, Central Bank Survey of Foreign Exchange and Derivatives Market Activity, 1998, International Monetary Fund, World Economic Outlook, 1998, 2001.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–15

Table 1-3 Global Foreign Direct Investment Flows

Source: UNCTAD, Handbook of Statistics, various issues and author’s estimates.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–16

Figure 1-3

Private Capital Flows to Emerging Economies

Source: International Monetary Fund, Annual Report, and International Capital Markets, various issues.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–17

Understanding Global Markets:Some Basic Economic

Concepts

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–18

Some Basic Economic Concepts

• DemandThe relationship between the prices that

consumers are willing and able to pay for various quantities of a good or service for a given time period, all other things constant.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–19

Table 1-4

An individual Consumer’sDemand Schedule

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–20

Some Basic Economic Concepts

• Law of DemandAn economic law that states that there is an inverse,

or negative, relationship between the price that consumers are willing and able to pay and the quantities that they desire to purchase, Ceteris paribus.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–21

Some Basic Economic Concepts

• SupplyThe relationship between the prices of a good or

service and the quantities supplied to the market by producers within a given time period, all other things constant.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–22

Some Basic Economic Concepts

Table 1-5 An individual Firm’sSupply Schedule

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–23

Some Basic Economic Concepts

• Law of SupplyAn economic law that states that there is a positive

or direct relationship between the prices producers receive and the quantities that they are willing to supply to the market.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–24

Some Basic Economic Concepts

• Presenting Demand and SupplyVarious forms:

Table: Schedule Graph: Curve Mathematical Equation: Function

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–25

Some Basic Economic Concepts

• The Demand Schedule tabulates the price the

consumer is willing and able to pay for various quantities of a good or service during a specified time period, all other things held constant.

Table 1-4

An individual Consumer’sDemand Schedule

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–26

Some Basic Economic Concepts

• The Supply Schedule tabulates the

minimum price a supplier is willing to accept for various quantities supplied of a good or service.

Table 1-5 An individual Firm’sSupply Schedule

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–27

Figure 1-4

The Demand for and Supply of Gasoline

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–28

Some Basic Economic Concepts

• Determinants of demand and supplyWhat factors influence demand and/or supply?

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–29

• Demand FactorsChanges in consumer preferencesChanges in incomeChanges in the prices of related goodsChanges in the number of consumers

Factors Influencing Demand and Supply

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–30

Factors Influencing Demand and Supply

• Supply FactorsChanges in the cost and availability of inputsAdvances in technologyChanges in the prices of related goods of

servicesTaxes and producer subsidiesChange in the number of producers

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–31

Table 1-6 Factors Influencing Demand

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–32

Table 1-7 Factors Influencing Supply

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–33

Market Demand And Supply

• Market Demand A curve that

illustrates the prices that consumers are willing and able to pay for various quantities of a good or service for a given time period, all other things constant.

Always downward slopping

Price

Quantity

Demand

Curve

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–34

Market Demand And Supply (cont’d)• Market Supply

A curve that illustrates the prices that producers are willing to accept for various quantities of a good or service they supply to the market for a given time period, all other things constant. Always upward

slopping

Price

Quantity

Supply Curve

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–35

Copyright©2003 Southwestern/Thomson Learning

Price

0

Supply

Demand

Quantity

P0

Qd Qs

Market Price

=

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–36

Some Basic Economic Concepts

• Why do consumers and producers participate in the market?Consumer and producer surplus

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–37

Consumer and Producer Surplus

• Consumer Surplus

The benefit that consumers receive from the existence of a market price.

The difference between what consumers are willing and able to pay for a good or service and the market price

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–38

Consumer and Producer Surplus

• Producer Surplus

The benefit that producers receive from the existence of a market price.

The difference between the price that producers are willing to accept to supply a particular quantity and the market price.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–39

Figure 1-5 Consumer and Producer Surplus

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–40

Some Basic Economic Concepts

• How Market Prices Are Determined Market prices have the tendency to move to the

equilibrium (center)

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–41

Copyright©2003 Southwestern/Thomson Learning

Price

0

Supply

Demand

Surplus

Quantity

P0

P1

Qd Qs

Surplus( Excess Quantity Supplied)

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–42

Shortage (Excess Quantity Demanded)

Copyright©2003 Southwestern/Thomson Learning

Price

0 Quantity

Supply

Demand

Quantitysupplied

Quantitydemanded

P0

Shortage

P1

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–43

How Market Prices Are Determined

• Market Clearing or Equilibrium PriceThe price at which quantity supplied equals

quantity demanded because neither an excess quantity demanded nor an excess quantity supplied exists at this price.

Prices have a tendency to move to the center (Excess demand keeps upward pressure on prices, and excess supply keeps a downward pressure on supply)

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–45

The Global Market

• The Global Market PlaceGlobal prices are determined based the interaction

between the supply (export) and demand (import) of quantities in excess of domestic demand or supply

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–46

EXPORT

Copyright©2003 Southwestern/Thomson Learning

Price

0

Supply

Demand

Excess domestic supply

Quantity

P0

P1

Qd Qs

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–47

IMPORT

Copyright©2003 Southwestern/Thomson Learning

Price

0 Quantity

Supply

Demand

Quantitysupplied

Quantitydemanded

P0

Excess Domestic Demand

P1

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–48

How Market Prices Are Determined (cont’d)

• Global Markets:Exchange of goods and services beyond national

borders

• For Nations Engaged in International TradeThe global equilibrium market price arises when

excess quantities demanded, or imports, equal excess quantities supplied, or exports.

University of Minnesota-Duluth, Department of Economics, Summer 2005 1–49

Figure 1-7 The Global Coffee Market