finlight research - market perspectives - aug 2015

TRANSCRIPT

Market Perspectives

August 2015

Aug. 10th, 2015

www.finlightresearch.com

Keep Your Powder Dry…

“if the generals are advancing by themselves

they’re not going to get very far !”– Old saying

2FinLight Research | www.finlightresearch.com

Executive Summary: Global Asset Allocation

� Caution is still the watchword for the months ahead

� Economic fundamentals remain mixed to weak

� There is very limited upside for risk assets, and probably a significant

downside over the near future.

� We still believe that equity markets are living on borrowed time. Some

warning signals are already given by small caps underperformance and

market breadth weaknesses.

� The song remains the same in commos. Commodities resumed their slide

without any sign of bottoming…

� We pay a close attention to the VIX reading.

� We continue to expect higher default rates and higher volatility as banks

are likely to be more restrictive in their lending standards

� The prospect of rising interest rates, a stronger US dollar and economic

uncertainty , could also be a trigger for higher cross-asset volatility.

� Thus, a confluence of forces are converging to disrupt global equity and debt

markets.

� We reiterate our view: A perfect storm is building… It combines historically

overvalued stocks with stretched government bonds and corporate credits.

Unlike previous storms (2000, 2008), investors would be left with almost

no place to hide.

� We summarize our views as follows�

3FinLight Research | www.finlightresearch.com

MACRO VIEW

� The Good

� S&P500 earnings growth remains solid at its core� Durable goods orders beat expectations� ISM manufacturing and Non-Manufacturing remained solid

� The Bad

� Consumer confidence took a hit in July and missed expectations (90.9 versus 99.3 on the Conference Board Consumer Confidence Index)

� In June, retail sales fell by 0.6% (MoM) in the Eurozone, and by as much as 2.3 % in Germany� Chinese Caixin manufacturing purchasing managers index (PMI) for July dropped to a two-year

low of 47.8.

� The Ugly

� Main systemic risk resides in China: After a decade of economic boom, China has accumulated significant imbalances. China’s economy is supported by approximately six trillion dollars of 'shadow debt', coupled with an unprecedented credit-fueled construction madness.

� Greece is still a wild card, as the reached deal doesn’t provide a permanent resolution to the crisis.

4FinLight Research | www.finlightresearch.com

5FinLight Research | www.finlightresearch.com

The Big Four Economic Indicators

� The overall picture had been one of a slow recovery, but there is no indication of a recession using the indicators monitored by the NBER.

� The current picture is characterized by relatively strong Employment and Income, a weak Industrial

Production and an erratic to weak Real Sales.

6FinLight Research | www.finlightresearch.com

GDP Growth

� The Atlanta Fed's GDPNow model first

forecast for real GDP growth (annualized

SA) in Q3-2015 was 1.0% on Aug. 6th, well below consensus

� The model projects that lower inventories will subtract 1.7% from Q3 real GDP growth

� The advance estimate from the U.S. Bureau of Economic Analysis of Q2 GDP was reported at +2.3%, exactly in line with the Atlanta Fed's GDPNow estimate.

7FinLight Research | www.finlightresearch.com

ISM

� Conditions in the service sectors of

both the Eurozone and U.S.

economies are improving.

� ISM Manufacturing came in below expectations (at 52.7, down from June’s 53.5).

� US ISM Non-Manufacturing Composite Index came in higher than expected, at 60.3 (versus 56.2), far above the June 56.3 reading

� This is a 10-year high!

8FinLight Research | www.finlightresearch.com

Consumer Confidence

� Consumer confidence disappointed.

� The Conference Board index fell from 99.8 to 90.9, while the Michigan Sentiment Index fell from 96.1 to 93.1

9FinLight Research | www.finlightresearch.com

Economic Surprise

� As shown by the JP Morgan Economic Data Surprise Index (EDSI), recent economic data have been relatively worse than expected, pushing long-term UST yields lower

10FinLight Research | www.finlightresearch.com

GS – Global Leading Indicator (GLI)

� The July Final GLI came in at1.5%yoy. It momentum stands at0.20%.

� According to last estimation, GLIgrowth has been positive andincreasing since February. But this‘Expansion’ phase is anemic andcrossing the border to the“Slowdown” phase could occuranytime.

� Five of the ten underlyingcomponents of the GLI improved inJuly

� We continue to think that the

acceleration we’ve been

witnessing since Jan. ‘15 is quite

modest for a typical expansion

phase

11FinLight Research | www.finlightresearch.com

Guessing the Next Crisis?

� Since 2000, the state and local governments debtrose at double the rate of nominal GDP (150% vs77%)

� Over the same period, state and local taxes haveincreased at a rate twice that of wages (75% vs 38%),and their expenditures have risen faster than GDP.

� Is that a sustainable trend?

� One day, borrowing will become prohibitive andraising taxes will no longer generates morerevenues…

� Cutting spending would become unavoidable.

� Higher taxes, when earnings stagnate and householdincome declines in real terms, will no doubt weigh onconsumption spending.

� Lower private/public consumption = recession.

� Defaulting on debt will trigger the crisis to come.

12FinLight Research | www.finlightresearch.com

EQUITY

� After the Greek & Chinese fears, the market is back to its previous sideways trading range, awaiting again a catalyst to breakout one way or another.

� The million-dollar question: Is that the sideways plateauing process that usually signal a major peak? Or just a neutral range-bound consolidation preparing the way for a material break on either side of the range?

� At the top of the range, 2130 is the level that will make or break the market over the short-term.

� For the moment, the bullish trend has been preserved. But a point of no return could be reached on the S&P500 if it breaks its trendline across the lows since Oct. ‘11 at around 2000

� Some warning signals are given by small caps underperformance and market breadth weaknesses. Many of the individual stocks that make up the S&P 500 Index are suffering major corrections. The advance is led by fewer and fewer stocks

� Recent data shows more evidence of lower productivity, lower potential GDP growth and (later)

higher inflation risk. � This is a bad scenario for stocks

� We keep the same song. We still believe that equity markets are living on borrowed time because…

� Earnings season hasn't provided the catalyst needed for the breakout to the upside� Valuations are well above historical norms, especially when we take into account the slower

revenue growth, the lower margins and the starting wage pressures � The coming rate hikes will depress all asset prices for at least a part of next year

13FinLight Research | www.finlightresearch.com

EQUITY

� Bottom line :

� Nothing new compared to our previous report. We remain Neutral equities as long as the indices stay trapped in their sideways trading range. Our strategy is still to buy the lows and sell the highs, until a material break on either side of the range is attained.

� We may revise our view to OW after a clean break of the 2070-2130 range to the upside on the S&P500, and to UW below the trend since Oct. ‘11 lows (currently at 2000)

� We still think it is wise to incrementally "de-risk" your portfolios by focusing on higher quality / more defensive / more favorably priced companies

� We remain OW on Japan (always on an FX hedged basis) as a positive dynamic is still driving the Japanese economy. But the 21 000 level on the NIKKEI will be key…

� We remain Neutral on Europe vs. US despite the policy divergence between the Fed and the ECB. According to the 12 month forward P/E, Europe is trading at 15 year highs, relative to the

US

� We remain UW in US small caps vs large caps.

14FinLight Research | www.finlightresearch.com

US Earnings

� For Q3 2015, 56 companies have issued negative EPS guidance and 22 companies have issued positive EPS guidance.

� The 12-month forward P/E ratio for the S&P 500 now stands at 16.5, well above historical averages: 5-year (14.0), 10-year (14.1)

� Most of the deterioration in earnings momentum

for the S&P 500 is due to the Energy sector

� Q2 earnings decline -1.0%. The last time we saw a YoY similar decline in earnings was Q3-2012 (the Fed came with its QE4 later that year)

� If the Energy sector is excluded, the earnings growth rate would be at 5.7%

� Of the 436 companies that have reported earnings to date for Q2 2015, 73% have reported earnings above the mean estimate and 51% have reported sales above the mean estimate

15FinLight Research | www.finlightresearch.com

S&P500 – A Long-Term Perspective

� Equity markets appear at lofty valuations, whatever the valuation metric we use.

� We see only a few quarters (during the dot.com bubble) with higher valuations� Valuation alone is very rarely a timing tool for a major market top� Nevertheless, all these indicators suggest a cautious long-term outlook and weak long-term return

expectations

16FinLight Research | www.finlightresearch.com

S&P500 – A Short-Term Perspective

� The S&P500 has been rangy for a while, now. Is that the sideways plateauing process that usually signal a peak? Or just a neutral range-bound consolidation preparing the way for a material break on either side of the range?

� The index hasn't seen a 20% correction over roughly 4 years. But the 200-day MA tests are becoming more and more frequent.

� The range we watch remains the same: 2040 – 2130. A clean break in either direction should

translate in a more impulsive movement: 2215 to the upside, and 1960 to the downside

17FinLight Research | www.finlightresearch.com

S&P500 – A Medium-Term Perspective

� At major market peaks, the advance is usually led by fewer and fewer stocks

� The market breadth seems to be

deteriorating…

� 106 out of the 500 stocks in the S&P500 index have suffered a 20% decline from its 52-week high.

� Additional 136 stocks are -10% from its 52-week high.

� Another warning signal is provided by

the under-performance of small-cap

stocks

18FinLight Research | www.finlightresearch.com

S&P500 – A Medium-Term Perspective

� A third warning signal: The decoupling we see between the S&P500 and market internals is similar to the one we’ve witnessed during the last financial crisis…

19FinLight Research | www.finlightresearch.com

S&P500 – A Medium-Term Perspective

� On the MT, next levels to watch closely are:

� The 55 wMA at 2048. The index has been above for 165 consecutive weekly closes.

� And the trendline across the lows since Oct. ‘11 at around 2000

� Only a material break below these

levels would signal that the

underlying trend is definitely

damaged.

20FinLight Research | www.finlightresearch.com

Japanese Equities

� A positive dynamic is developing in Japanese stocks, mainly due to Yen weakening, but not only.

� Stocks are taking advantage from the exit from deflation, the improvement in macro data and corporate earnings momentum

� We remain OW on Japan (always

on an FX hedged basis)

� But given the toppish view we have on USD-JPY and the closeness of the next important level of 21 000, we are not far from moving back to Neutral again.

21FinLight Research | www.finlightresearch.com

Chinese Equities

� According to a GS estimate, the Chinese government has spent around Rmb 900bn to support the domestic equity market through the so-called 'national team' institution.

� In spite of this massive

government intervention, we still

expect the Chinese equity

market to resume its decline

� Technically speaking, we interpret the triangle pattern we see on the Shanghai Composite Index as a trend continuation formation.

22FinLight Research | www.finlightresearch.com

Chinese Equities

� The picture is even more frightening when equity market is compared to the underlying economic activity…

� Over the last 12 months, the Shanghai Composite has completely decoupled from the PMI

� Filling the gap will necessitate tears and blood.

23FinLight Research | www.finlightresearch.com

Trading Model – S&P500

� As of Aug. 10th, our prop. Short-Term trading model is modestly short on the S&P500 (2104.18).� Out of the 4 active systems, 4 are short with 2082, 2061 and 2041 as targets

� The model has boosted its return generation since Oct. ‘14, exhibiting a pattern similar to the one we’ve seen after Jun. ‘07

24

FIXED INCOME & CREDIT

� We believe the Fed is on track for a September rate hike, when the market continues to price such a scenario very partially. UST yields remain underpriced relative to this scenario.

� Our excitement about inflation expectations was calmed down by the new slide in commodity prices.� Nevertheless, inflationary signs should be watched closely as they will foreshadow a steepening

decline in govies.

� We expect negative total returns on USTs. We still look for the bear market on USTs to resume.� Last month, we moved UW 10y USTs but switched back to Neutral as the 10-year yield moved below

2.30. We wait for a material break either above 2.45-2.50 or below 2.00 to change our positioning� Our ultimate target on 10y yields stands at 2.75 by end of 2015.

� On German Bund, our target zone of 0.75-0.90 were reached and, as expected, we switched from

UW to Neutral. We remain Neutral on German Bund (within the sovereign FI asset class) as long asthe 10-year yield stays above the 0.45 – 0.50 area.

� We will switch to UW again as the 10-year yield breaks above 0.90-1.00.

� Inflation breakevens have risen since the start of the year. We remain OW HICP Inflation through 5y

inflation swaps (long HICP inflation breakevens = receiving HICP vs payind fixed rate) as we expect a steady pick-up in HICP inflation over 2H15

� We expect TIPS to underperform as energy prices continue to decline and Fed tightening tends to push real rates up in the absence of accelerating inflation.

FinLight Research | www.finlightresearch.com

25

FIXED INCOME & CREDIT

� Credit quality further deteriorates in H1, both in IG and HY, as the releveraging continues to rise at a sustained pace (especially in HY space)

� Lower rated new-issue volume has been increasing since the financial crisis. That should drive the default rate higher and HY spreads wider.

� But, the risk that the faster debt accumulation on US balance sheets will drive corporate defaults and downgrades higher remains low in the near to medium term, in our view

� With the Chinese hard landing fears resurfacing, pressure resumed on commodity prices, pushing down credits in the Energy, Metals & Mining sectors, especially in US HY

� We feel more cautious about EUR HY as it continues to show an extremely low level of volatility that hardly capture the underlying single name event risk

� We remain UW on corporate credit, due to valuation, to rising corporate leverage (specially in the US), to rising volatility, to position within the credit cycle and given the weak total return forecast

� Within the credit pocket, and over the very short-term, we move out of our preference for Eurozone

HY corps vs US HY corps, initially inspired by the ECB massive QE (influencing Institutional allocation), and more resilient macro in the Eurozone. We are now Neutral on USD vs. EUR HY

spreads, but we prefer USD on a total return basis, despite its higher beta to energy sector

FinLight Research | www.finlightresearch.com

26

FIXED INCOME & CREDIT

� We still prefer US IG over Eurozone.IG, as we think that more attractive spread valuations and higher carry should fuel a stronger bid for US credit.

� We still prefer IG over HY on a risk-adjusted basis as we expect higher volatility on spreads and we believe IG corporates better positioned to absorb the impact of rising rates

� Bottom line : UW Govies, UW US vs Eurozone Govies, remain long flatteners on the US yield curve, UW credit, Neutral Eurozone vs US HY credit, UW Eurozone vs US IG credit, Neutral TIPS and OW HICP Inflation, UW High Yield vs High Grade, Neutral on EM corporates

FinLight Research | www.finlightresearch.com

27

US Govies – 10y UST

� Last month, we decided to switchfrom Neutral to UW 10y USTs andmoved to 2.30 the threshold belowwhich we become Neutral again.

� We keep this same positioning rule

� Tactically, we are now Neutral

again, waiting for a break eitherabove 2.50 or below 2.00 tochange our positioning.

� We think that the risk is still

biased to the upside on the 10y

yield.

� A better labor market wouldtranslate into higher inflationexpectation later this year (or in2016) and higher LT yields.

� In order to confirm our bearishview, a clean move above 2.40-2.50 is needed..

FinLight Research | www.finlightresearch.com

28FinLight Research | www.finlightresearch.com

US TIPS

� Inflation expectations have resumed their decline, probably because of lower oil / gasoline prices…

� Five-year breakevens are now at their lowest level since Jan. ‘15. Breakevens will stay under pressure until energy prices stabilize.

� We expect TIPS to underperform

as energy prices continue to decline and Fed tightening tends to push real rates up in the absence of accelerating inflation

� As a consequence of this slide in inflation expectation, nominal yields have stayed relatively low despite the imminent Fed rate hike

29

US Credit

� The renewed decline in oil prices induced another leg up in the spread on high-yield energy bonds,reaching new post-recession levels

� As the default risk in the high-yield energy sector heads up, the risk of a credit default contagion isgetting on the radars. But so far, there is no sign of such a contagion.

FinLight Research | www.finlightresearch.com

30

US Credit

� IG spreads have reached a 3-year peak, drivenby heavy supply and concerns about commodityprices.

� With the Chinese hard landing fears resurfacing,pressure resumed on commodity prices,pushing down credits in the Energy, Metals &Mining sectors, and putting pressure on HYbond prices

� We still prefer IG over HY (both in US and

Eurozone) on a risk-adjusted basis as weexpect higher volatility on spreads and webelieve IG corporates better positioned toabsorb the impact of rising rates

FinLight Research | www.finlightresearch.com

31

Credit – Any Warning?

� 2-yr swap spreads acted as an advance warningof widening risk in HY spreads and fundamentaldeterioration in the broad economy

� At this stage, swap spreads are trading

around 20-30 bps. No risk is seen on the

horizon yet!

FinLight Research | www.finlightresearch.com

32

EXCHANGE RATES

� We reiterate our bullish view on USD over the medium-term and expect a rival of the appreciation cycle of the '90s

� Historically, USD cycles have been persistent, lasting 5-6 years in the appreciation phase. We thus see further medium term USD gains against the major crosses (especially EUR and JPY) and expect a cyclical low in EUR/USD somewhere in 2016 (with the ECB tapering)

� The DXY uptrend is still intact even if the pace slows. But current dollar valuation implies 25 to 50 bps higher rates in the US. Without a September hike the uptrend on the US dollar may be damaged

seriously.

� The line in the sand for the DXY index is provided by the lows of May and June. A break below would derail the strength phase.

� Our positioning on USD is driven by (almost) the same trading rules:� During the month, we moved UW as the spot broke below 1.1040 and reached our first target around

1.08.� We remain UW on EUR-USD as long as it stays below 1.1080. We will move back to Neutral if the

spot breaks above 1.1080, and to OW above 1.12

� On USD-JPY, we remain Neutral for the moment, as the spot failed to hold a break above 124-125 resistance

FinLight Research | www.finlightresearch.com

33

US Dollar

� The dollar index remains near a 12-year high

� We still think that the upward

movement in US Dollar should

continue and expect a further 10%-20% appreciation

� At this stage, the dollar (on a real trade-weighted basis) is back to its average level against other currencies. The upside move has further room to go…

� Fundamental US data are also supportive for the USD: the federal deficit is under control, the economy seems in a good shape and the Fed is preparing to tighten.

FinLight Research | www.finlightresearch.com

34

EUR-USD

� EUR-USD is still consolidating

below its July ‘14 downtrend

(currently around 1.10).

� During the month, we moved UW as the spot broke below 1.1040 and reached our first target around 1.08.

� We will move back to Neutral if the spot breaks above 1.1080 and to OW above 1.12

� Only a clean break in either direction (below 1.074 or above 1.108) is able to shed light on the next short-term move.

� We keep our bearish bias, for

the moment.

FinLight Research | www.finlightresearch.com

35

USD-JPY

� In our June Monthly Report, we said “We decide to switch from OW to Neutral and wait to see how the pivot behaves near the 124.73 level. ”

� From a multi-month/year perspective, the 124-125 range appears to be very important and should be watched closely for signs of a turning point formation

� JPY is already at historical low levels in terms of real effective exchange rate

� We stay Neutral for the moment,

as the spot failed to hold a break above 124-125 resistance

FinLight Research | www.finlightresearch.com

36

COMMODITY

� The song remains the same in commos. Commodities resumed their slide in July, led by crudeoil and base metals.

� All commodity families are struggling, but reasons are quite specific to each.� The price trend is probably reflecting the mixed news given by the world economy. The headwinds

responsible for this weakness (supply glut in oil, slowing growth in China, precious metals loosingtheir luster as a safe heaven…) are likely to continue.

� The expected Fed rate hike would put more pressure on the asset class as higher interest rates put ahigher cost on holding commodities

� We remain neutral-to-bearish across all complexes in the near term. To mid-2016, return forecastsare negative for commodities as a whole.

� Despite the rally seen in April (mainly driven by a weaker US dollar and expectation of morestimulus in China), the trend remains bearish. There is no indication of a bottom formation yet.

� We still think that it is still too early to get in the “reflation trade” of a weaker dollar and highercommodity prices

� We remain UW commodities. We continue, however, to like owning the GSCI index, and think

that commodities hold value as cross-asset portfolio diversifiers and as an inflation hedge.

FinLight Research | www.finlightresearch.com

37

COMMODITY

Bottom Line :

� Base Metals: Base metals don’t appear to be stabilizing yet. We remain Neutral on base metals, but

do not like holding Copper as it appears highly overvalued relative to the dollar, the global growth andthe Chinese demand.

� Agriculture: In our May Report, we decided to tactically switch from UW to Neutral because of thebearish bets on agricultural commodities accumulated by managed money. A crowded deal we didn’tlike. We stayed Neutral despite the sharp gains posted over June, gains that were reversed in July (-9.34% on the GSCI Agri Index)

� Energy: We remain of the view that the oil market is oversupplied, still think it is too early to expect

major upside for the price and that the risks remain substantially skewed to the downside� On July 2nd, we moved from Neutral to UW, as the spot dropped below 56, and targeted the

recent lows on WTI at $45/bbl. Since then, our target level has been already reached.

� We will move to Neutral again if the WTI goes above 56.5 and to OW if the it breaks above 63� Given the daily oscillators level, we will also move to Neutral again around 42 and wait to see how

the spot behaves near the previous low of March

FinLight Research | www.finlightresearch.com

38

COMMODITY

� Precious Metals: As trumpeted for months now, the Gold has finally broken its trading range to the downside (1150). But we still believe that betting on a reversal is premature…

� Applying our trading rule, we decided to switch from UW to Neutral.

� We change nothing to our view on precious metals. The stimulus provided by the ECB & BoJ is already factored in gold prices. Precious metals are vulnerable to higher US real yields,

stronger dollar and weaker gold flows to Asia (unlike in 2013) �We maintain the view that Q3 15 is likely to be the weakest quarter for gold

� We think that as long as gold is trading below 1225, it could be heading back down to test theMarch low

� As said in our previous reports, we will move progressively to OW (accumulate) as the spot

slides down towards 1000-980, which is likely the final leg down. Only a clean break above1225 may push us to reconsider our view.

� Our first target on silver at 14.70 has been reached. We still think that Silver (like gold) is probably ready for its final leg down towards 12.50. We remain UW as no material break has occurred

below 14.70. We will switch progressively to OW (accumulate) if the spot breaks the 14.70 resistance and slides down towards 12.50

� We may reconsider our UW position if the Silver breaks above 16.7-17.

FinLight Research | www.finlightresearch.com

39

Commodities

� As expected, commodity prices have resumed their downward slide as Chinese hard landing fears have resurfaced

� The downtrend in commos seems unable to find a bottom.

� Keep away from the asset class.

The move has further room to

go…

FinLight Research | www.finlightresearch.com

40

Precious Metals

� Gold is loosing its glitter…

� Gold downtrend remains in line with the increase in real rates (implied by 5y TIPS).

� Since end of 2011, investors have liquidated about 50% gold ETF holdings

� Betting on a reversal is still premature…

FinLight Research | www.finlightresearch.com

41

Crude Oil – The Supply-Side

� Strong supply is one of the

main factors weighing on oil

prices.

� OPEC output is near an all-timehigh

� The same is true for USproduction despite a near halvingof drilling activity and near 30%drop in capex.

� Future production cuts shouldfinally materialize next year andhelp oil prices to find a bottom inthe $35-40 range (for WTI)

FinLight Research | www.finlightresearch.com

42

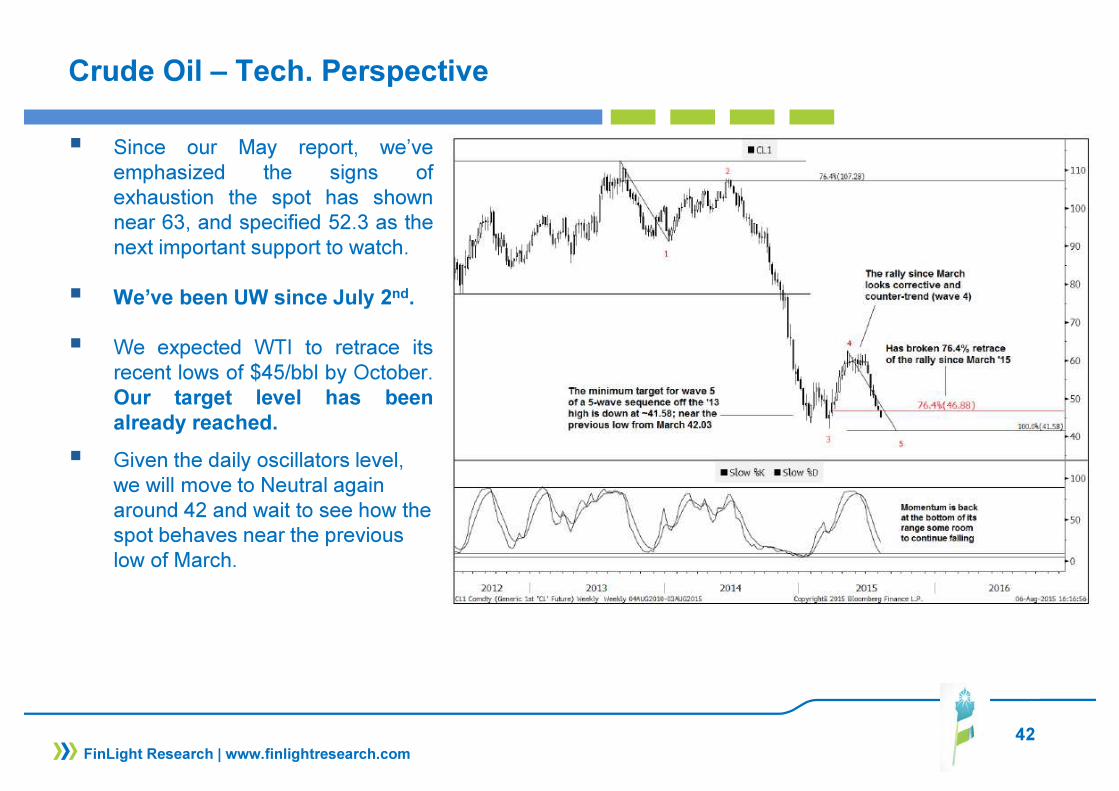

Crude Oil – Tech. Perspective

� Since our May report, we’veemphasized the signs ofexhaustion the spot has shownnear 63, and specified 52.3 as thenext important support to watch.

� We’ve been UW since July 2nd.

� We expected WTI to retrace itsrecent lows of $45/bbl by October.Our target level has been

already reached.

� Given the daily oscillators level, we will move to Neutral again around 42 and wait to see how the spot behaves near the previous low of March.

FinLight Research | www.finlightresearch.com

43

ALTERNATIVE STRATEGIES

� The HFRI Fund Weighted Composite Index was flat in July (+2.5% Ytd), mirroring a large dispersion among its underlying strategies: global macro managers performed well (+2.12% on HFRI Systematic, and 1.24% on HFRI Macro) while their event driven peers did poorly (-0.96% on HFRI Special Sit. sub-index and -0.30% on HFRI Event-Driven). Within the RV strategy, HFRI RV-Vol Index did the best with +2.09%

� The solid performance of CTAs and Macro traders reversed the sharp losses from Jun, thanks to the resumption of global themes in July. Part of this performance is indeed related to short positions on commodities and longs in US Dollar and FI.

� Conversely, event driven strategies suffered oil price weakness and some disappointing earnings calls.

� We stick to our preference for risk diversifiers (pure alpha generation strategies) over return enhancers.

� We believe that diversifying portfolios with an increased allocation to alternatives is particularly attractive at this stage of the cycle.

� We are not changing our recommendations on alternatives which we consider to be suited to current market conditions. We maintain our OW positioning on:� Equity Market Neutrals both for their “intelligent” beta and their alpha contribution. � CTA’s and Global Macro as a diversifier and tail hedge. These strategies should outperform as

FX and commodity current trends are likely to persist.� Vol. Arb strategy and prefer funds that trade volatility globally (all assets / all regions). This is our

way to position for a higher volatility regime.

FinLight Research | www.finlightresearch.com

44

CTA Funds

� CTAs remains our favorite HF strategy.

� After years of outflows, CTAs haveattracted huge inflows in 2015 thanks totheir solid performance.

� The momentum has decreased since thetop reached In April on the strategy

�

FinLight Research | www.finlightresearch.com

Bottom Line: Global Asset Allocation

� Caution is still the watchword for the months ahead

� Economic fundamentals remain mixed to weak

� There is very limited upside for risk assets, and probably a significant

downside over the near future.

� We still believe that equity markets are living on borrowed time. Some

warning signals are already given by small caps underperformance and

market breadth weaknesses.

� The song remains the same in commos. Commodities resumed their slide

without any sign of bottoming…

� We pay a close attention to the VIX reading.

� We continue to expect higher default rates and higher volatility as banks

are likely to be more restrictive in their lending standards

� The prospect of rising interest rates, a stronger US dollar and economic

uncertainty , could also be a trigger for higher cross-asset volatility.

� Thus, a confluence of forces are converging to disrupt global equity and debt

markets.

� We reiterate our view: A perfect storm is building… It combines historically

overvalued stocks with stretched government bonds and corporate credits.

Unlike previous storms (2000, 2008), investors would be left with almost

no place to hide.

� We summarize our views as follows�

45FinLight Research | www.finlightresearch.com

46

Disclaimer

FinLight Research | www.finlightresearch.com

This writing is for informational purposes only and does not constitute an

offer to sell, a solicitation to buy, or a recommendation regarding any

securities transaction, or as an offer to provide advisory or other services

by FinLight Research in any jurisdiction in which such offer, solicitation,

purchase or sale would be unlawful under the securities laws of such

jurisdiction. The information contained in this writing should not be

construed as financial or investment advice on any subject matter.

FinLight Research expressly disclaims all liability in respect to actions

taken based on any or all of the information on this writing.

About Us…

� FinLight Research is a research-centric company focused on Asset Allocation from a top-down

perspective, on Portfolio Construction, and all related quantitative aspects and risk management issues.

� Our expertise expands along 3 axes:

� Asset Allocation with risk control and/or risk budgeting techniques

� Allocation to alternative investments : Hedge funds, rule-based strategies (momentum, value, carry, volatility), real assets (real estate, infrastructure, farmland, timberland and natural resources). Private equity and venture capital should be the next step…

� Allocation with a factorial approach built on the understanding (profiling) of the risk/return drivers of the different asset classes

� FinLight Research is an innovation-oriented company. We target to fill the gap between the academic research and the investment community, especially on real assets and alternatives. We survey on a continuous basis the academic literature for interesting published and working papers related to quantitative investing, non-linear profiling, asset allocation, real assets...

47FinLight Research | www.finlightresearch.com

Our Standard Offer

Provide tailor-made quantitative analysis of your

portfolios in terms of asset allocation, risk profiling and risk contribution

Provide tailor-made quantitative analysis of your

portfolios in terms of asset allocation, risk profiling and risk contribution

•Risk Profiling

Offer a turnkey 3-step factor-based process in GAA

with factor selection, risk budgeting and

dynamic portfolio protection

Offer a turnkey 3-step factor-based process in GAA

with factor selection, risk budgeting and

dynamic portfolio protection

•Factor-based GAA Process

Provide assistance with alternative

investments (including real

assets) in terms of profiling, and

integration in a GAA

Provide assistance with alternative

investments (including real

assets) in terms of profiling, and

integration in a GAA

•Alternative Investments

Provide assistance with asset

allocation and related risk control

and/or risk budgeting techniques

Provide assistance with asset

allocation and related risk control

and/or risk budgeting techniques

•Global Asset Allocation (GAA)

48FinLight Research | www.finlightresearch.com