finite reinsurance reserving

DESCRIPTION

Finite Reinsurance Reserving. Nick Giuntini, FCAS, MAAA CLRS, September 2003. General Approach. Generally Reserved on an Individual Contract Basis Lack of Homogeneity LPTs, Agg XOLs, Q/Ss Varied Terms Varied Underlying Often Large Contracts Underlying Exposure and Deal Modeling - PowerPoint PPT PresentationTRANSCRIPT

Finite Reinsurance ReservingNick Giuntini, FCAS, MAAA

CLRS, September 2003

Finite Reinsurance Reserving2

General Approach

Generally Reserved on an Individual Contract Basis Lack of Homogeneity

LPTs, Agg XOLs, Q/Ss Varied Terms Varied Underlying

Often Large Contracts Underlying Exposure and Deal Modeling Accounting May Vary

Risk Transfer – Reinsurance Accounting Can Reinsurer Discount Reserves?

“No Risk Transfer” – Deposit Accounting

Finite Reinsurance Reserving3

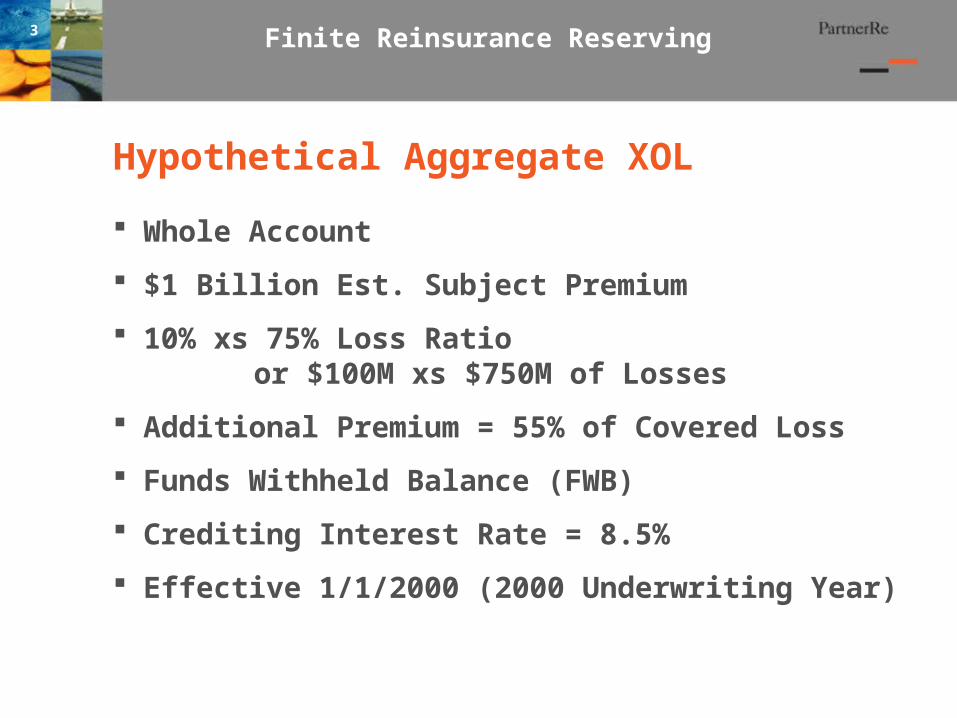

Hypothetical Aggregate XOL

Whole Account

$1 Billion Est. Subject Premium

10% xs 75% Loss Ratio or $100M xs $750M of Losses

Additional Premium = 55% of Covered Loss

Funds Withheld Balance (FWB)

Crediting Interest Rate = 8.5%

Effective 1/1/2000 (2000 Underwriting Year)

Finite Reinsurance Reserving4

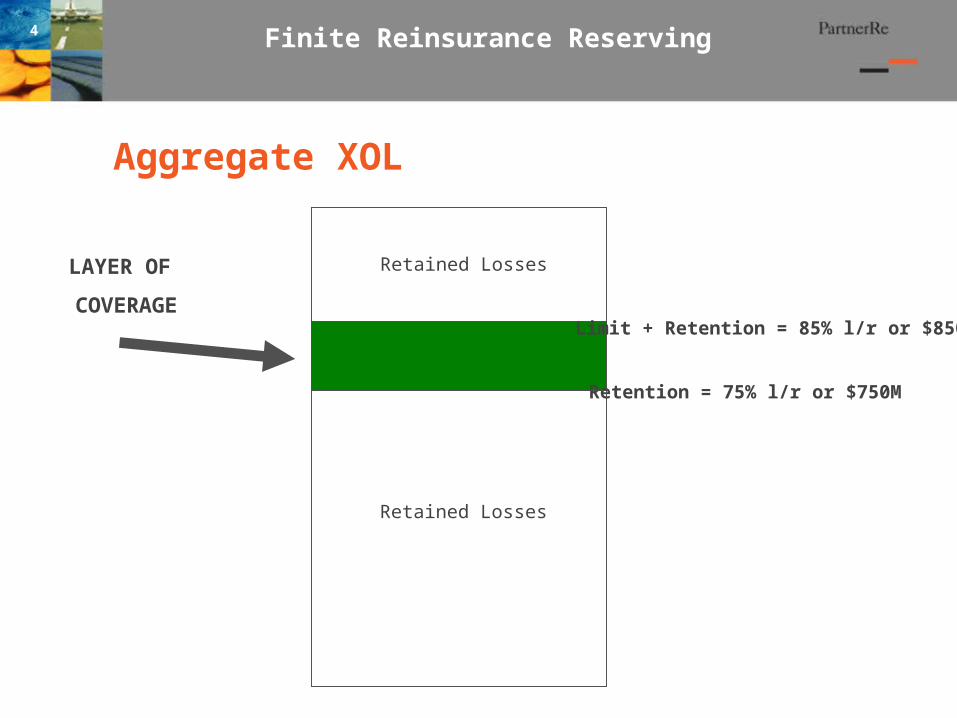

Aggregate XOL

Retention = 75% l/r or $750M

LAYER OF

COVERAGELimit + Retention = 85% l/r or $850M

Retained Losses

Retained Losses

Finite Reinsurance Reserving5

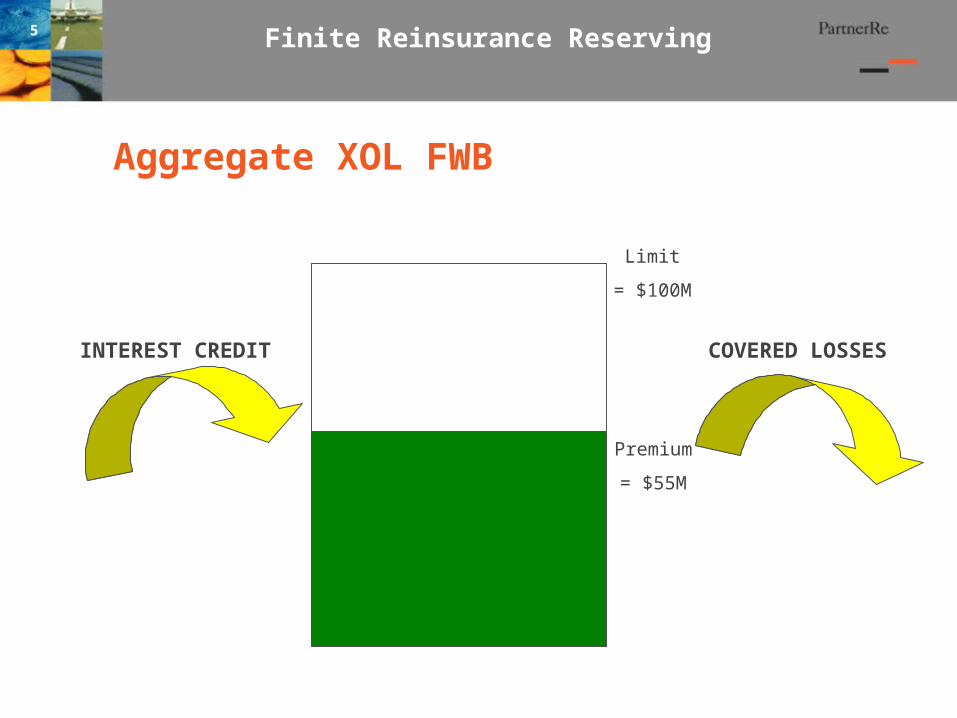

Aggregate XOL FWB

Premium

= $55M

Limit

= $100M

INTEREST CREDIT COVERED LOSSES

Finite Reinsurance Reserving6

Mean or Mode

Assume:

Reinsurer can Discount Losses

Cedent Reports a 80% loss ratio

FWB Expected to Cover Ceded Loss Payout ($27.5M of Premium + Interest for $50M Losses)

Should Reinsurer Set up a Reserve for Obligations in Excess of FWB?

Finite Reinsurance Reserving7

Credit Risk

If Cedent becomes Insolvent, Reinsurer’s Funds are at Risk:

Premiums and Interest “Paid” into FWB Funds Transferred Triggers on Certain Events If not transferred offset generally believed to hold

Premiums not yet Paid into FWB Offset Probably Holds

Future Interest Credits Offset Questionable

Finite Reinsurance Reserving8

Credit Risk – Interest Income

Assume:

Reserving at 12/31/2003

Expected Loss Ratio = 85%

$736M Paid to Date (Paid Losses still in Retention)

FWB = $76M (for $100M of Ceded Losses)

What is the Magnitude of the Reinsurer’s Credit Risk?

Finite Reinsurance Reserving9

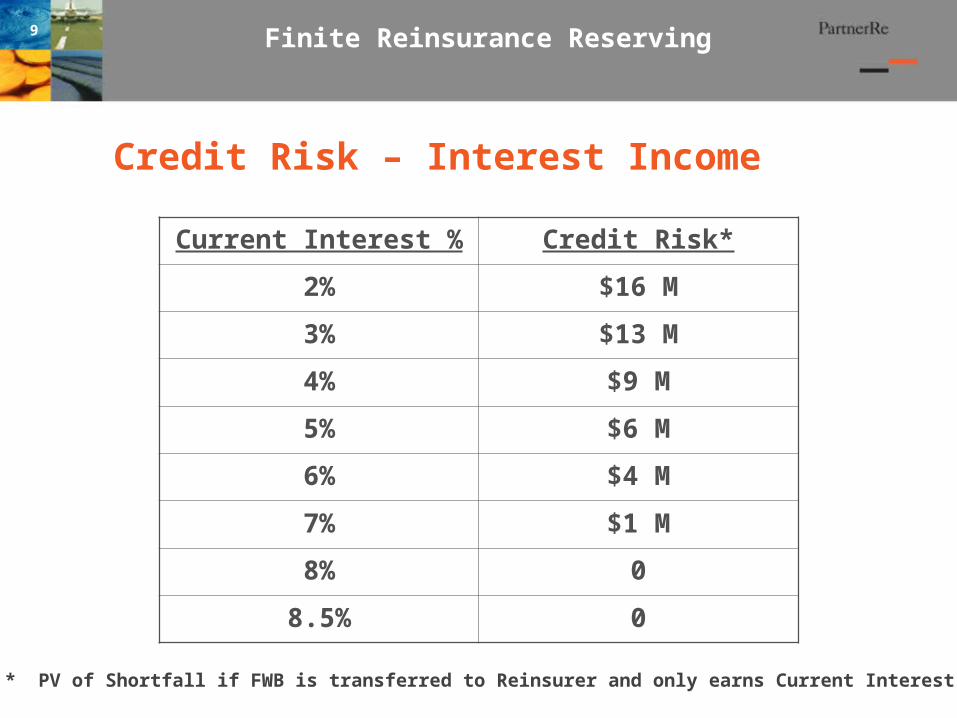

Credit Risk – Interest Income

Current Interest % Credit Risk*

2% $16 M

3% $13 M

4% $9 M

5% $6 M

6% $4 M

7% $1 M

8% 0

8.5% 0

* PV of Shortfall if FWB is transferred to Reinsurer and only earns Current Interest %.

Finite Reinsurance Reserving10

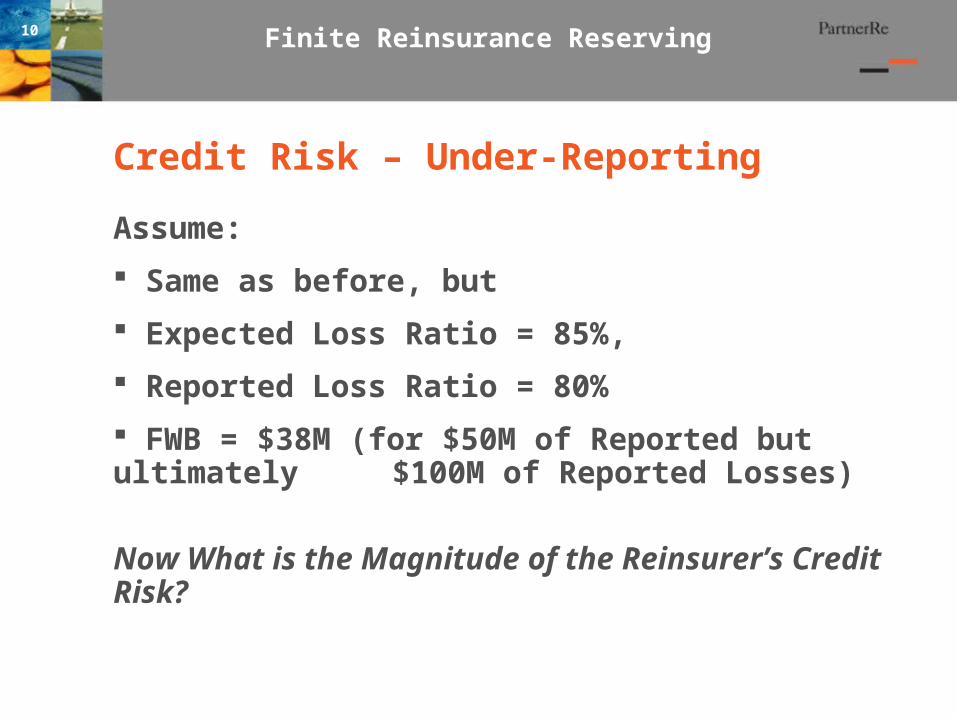

Credit Risk – Under-Reporting

Assume:

Same as before, but

Expected Loss Ratio = 85%,

Reported Loss Ratio = 80%

FWB = $38M (for $50M of Reported but ultimately $100M of Reported Losses)

Now What is the Magnitude of the Reinsurer’s Credit Risk?

Finite Reinsurance Reserving11

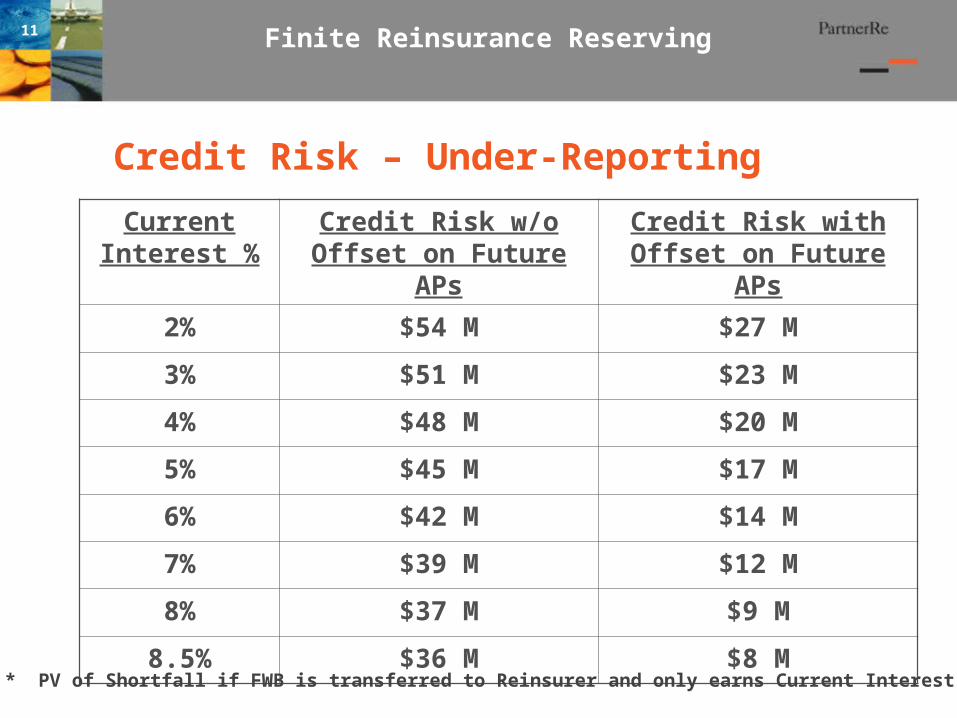

Credit Risk – Under-Reporting

Current Interest %

Credit Risk w/o Offset on Future APs

Credit Risk with Offset on Future APs

2% $54 M $27 M

3% $51 M $23 M

4% $48 M $20 M

5% $45 M $17 M

6% $42 M $14 M

7% $39 M $12 M

8% $37 M $9 M

8.5% $36 M $8 M

* PV of Shortfall if FWB is transferred to Reinsurer and only earns Current Interest %.

Finite Reinsurance Reserving12

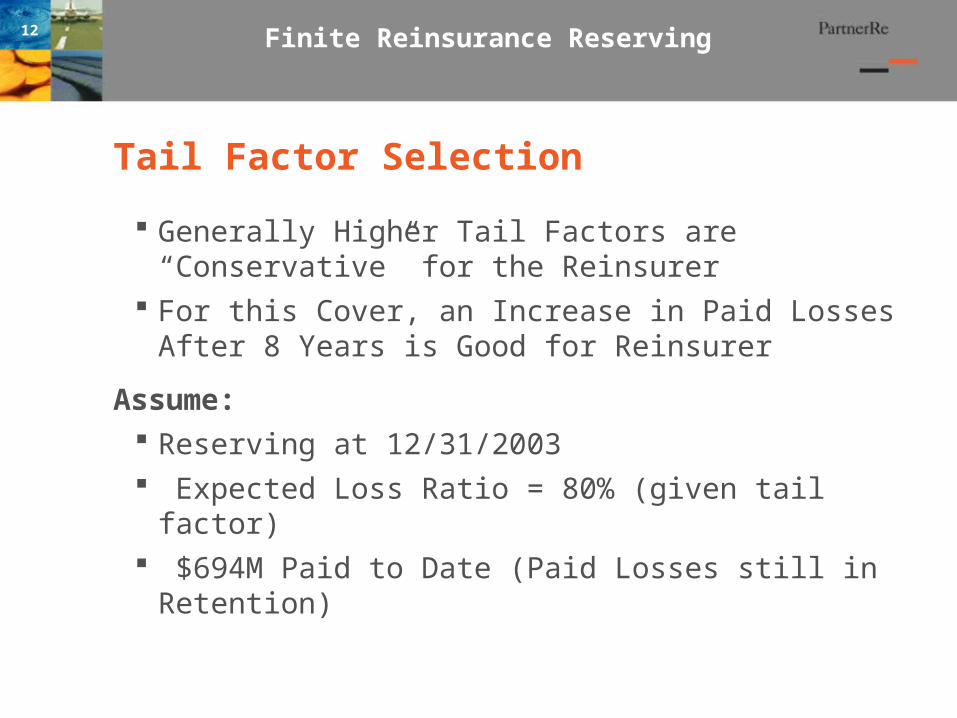

Tail Factor Selection

Generally Higher Tail Factors are “Conservative” for the Reinsurer

For this Cover, an Increase in Paid Losses After 8 Years is Good for Reinsurer

Assume: Reserving at 12/31/2003 Expected Loss Ratio = 80% (given tail factor) $694M Paid to Date (Paid Losses still in Retention)

Finite Reinsurance Reserving13

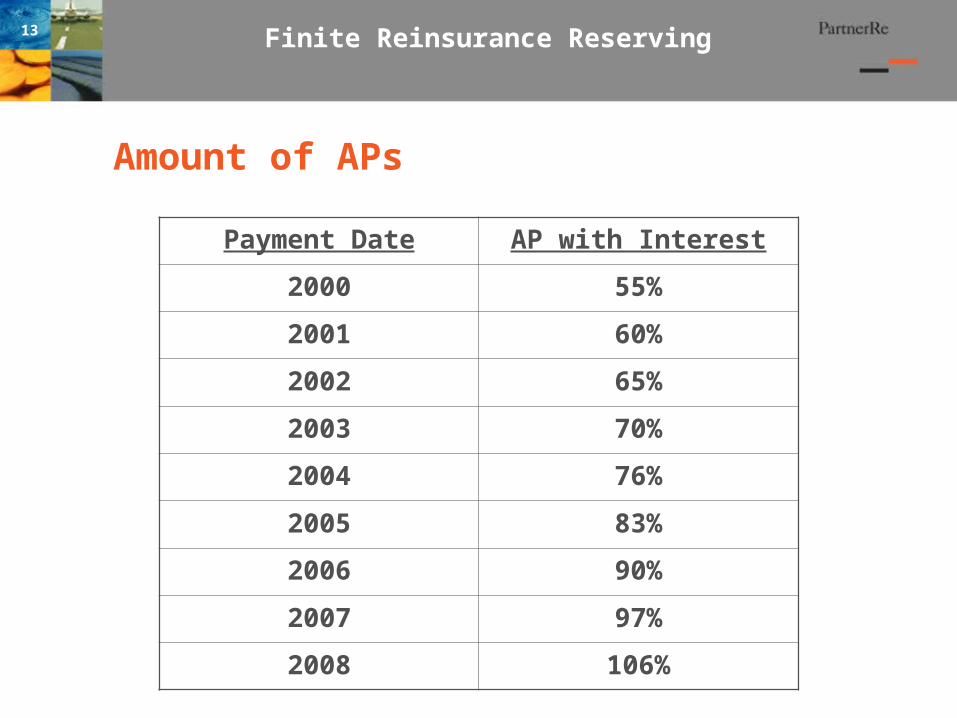

Amount of APs

Payment Date AP with Interest

2000 55%

2001 60%

2002 65%

2003 70%

2004 76%

2005 83%

2006 90%

2007 97%

2008 106%

Finite Reinsurance Reserving14

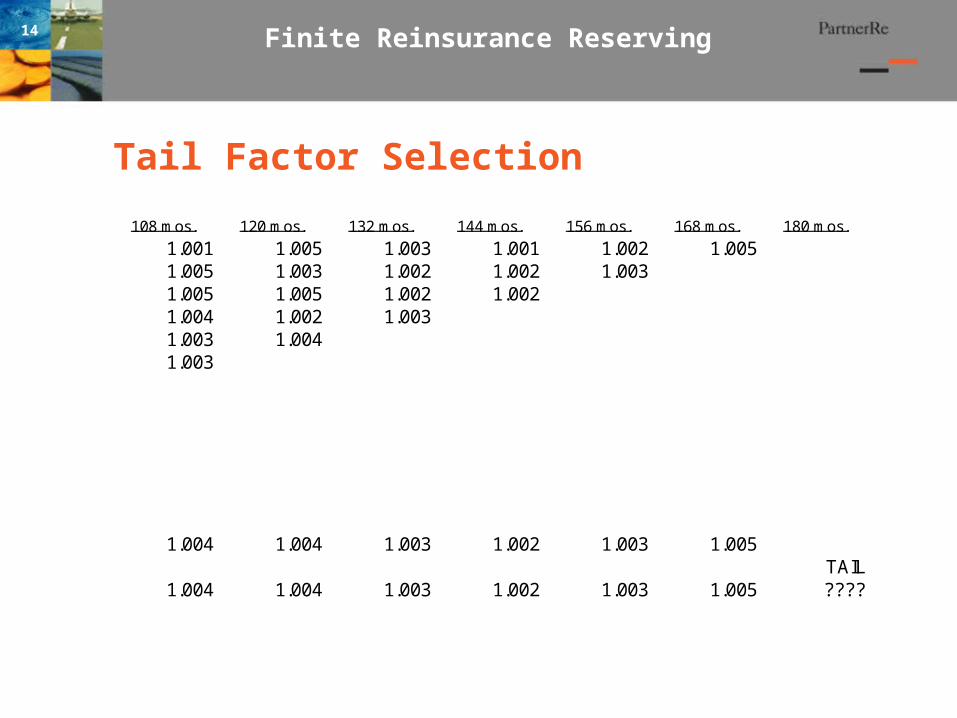

Tail Factor Selection

108 mos. 120 mos. 132 mos. 144 mos. 156 mos. 168 mos. 180 mos.

1.001 1.005 1.003 1.001 1.002 1.0051.005 1.003 1.002 1.002 1.0031.005 1.005 1.002 1.0021.004 1.002 1.0031.003 1.0041.003

1.004 1.004 1.003 1.002 1.003 1.005TAIL

1.004 1.004 1.003 1.002 1.003 1.005 ????

Finite Reinsurance Reserving15

Tail Factor Selection

Tail Factor FWB Cushion*

1.000 - $2.4 M

1.005 - $0.7 M

1.010 $0.6 M

1.015 $1.4 M

1.020 $2.2 M

* Negative Numbers are PV Reinsurers Loss at 4%.

Finite Reinsurance Reserving16

Conclusion

There can be Additional Reserving Issues and Concerns for Finite Contracts Due to:

Contract Structure Legal Jurisdiction Accounting Regime