finding fortune: how do institutional investors pick...

TRANSCRIPT

Finding Fortune: How Do Institutional Investors Pick AssetManagers?

Gregory Brown1, Oleg Gredil2, and Preetesh Kantak1

1UNC Kenan-Flagler Business School2Tulane A.B. Freeman Business School

November 19, 2016

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Research Question

How do asset allocators combine “limited” public and “expensive” privateinformation on delegated managers when choosing with whom to invest?

Asset allocators: endowment, SwF,foundation, insurance and pensions.Managers: explosive AUM growth of“specialist” vs. traditional funds.Limited info.: “bespoke” - not welldefined - managers.Costly info.: manager choice aided byin-house, external consultants.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Research Question

How do asset allocators combine “limited” public and “expensive” privateinformation on delegated managers when choosing with whom to invest?

26.640.3

10.7

23.6

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2004 2013

Delegated AUM

Trillions of U

SD

Asset allocators: endowment, SwF,foundation, insurance and pensions.

Managers: explosive AUM growth of“specialist” vs. traditional funds.Limited info.: “bespoke” - not welldefined - managers.Costly info.: manager choice aided byin-house, external consultants.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Research Question

How do asset allocators combine “limited” public and “expensive” privateinformation on delegated managers when choosing with whom to invest?

26.640.3

10.7

23.6

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2004 2013

Delegated AUM

Trillions of U

SD

Asset allocators: endowment, SwF,foundation, insurance and pensions.Managers: explosive AUM growth of“specialist” vs. traditional funds.

Limited info.: “bespoke” - not welldefined - managers.Costly info.: manager choice aided byin-house, external consultants.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Research Question

How do asset allocators combine “limited” public and “expensive” privateinformation on delegated managers when choosing with whom to invest?

26.640.3

10.7

23.6

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2004 2013

Delegated AUM

Trillions of U

SD

Asset allocators: endowment, SwF,foundation, insurance and pensions.Managers: explosive AUM growth of“specialist” vs. traditional funds.Limited info.: “bespoke” - not welldefined - managers.

Costly info.: manager choice aided byin-house, external consultants.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Research Question

How do asset allocators combine “limited” public and “expensive” privateinformation on delegated managers when choosing with whom to invest?

26.640.3

10.7

23.6

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2004 2013

Delegated AUM

Trillions of U

SD

Asset allocators: endowment, SwF,foundation, insurance and pensions.Managers: explosive AUM growth of“specialist” vs. traditional funds.Limited info.: “bespoke” - not welldefined - managers.Costly info.: manager choice aided byin-house, external consultants.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Data Source

Large institutional investor in long-short hedge funds who maintains...

1 timeline of meetings with funds,

2 depository of pitch-books and notes from meetings,3 dataset of AUM and returns from funds met, and4 flag of funds “admitted” for investment.

Research Findings:

1σ ↑ private information proxy doubles probability of fund admissionand reduces due-diligence time by 20%.“Subjective” judgements not wasteful - 12m peer-adjusted averagereturns is 1.5% higher for admitted funds.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Data Source

Large institutional investor in long-short hedge funds who maintains...

1 timeline of meetings with funds,2 depository of pitch-books and notes from meetings,

3 dataset of AUM and returns from funds met, and4 flag of funds “admitted” for investment.

Research Findings:

1σ ↑ private information proxy doubles probability of fund admissionand reduces due-diligence time by 20%.“Subjective” judgements not wasteful - 12m peer-adjusted averagereturns is 1.5% higher for admitted funds.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Data Source

Large institutional investor in long-short hedge funds who maintains...

1 timeline of meetings with funds,2 depository of pitch-books and notes from meetings,3 dataset of AUM and returns from funds met, and

4 flag of funds “admitted” for investment.

Research Findings:

1σ ↑ private information proxy doubles probability of fund admissionand reduces due-diligence time by 20%.“Subjective” judgements not wasteful - 12m peer-adjusted averagereturns is 1.5% higher for admitted funds.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Data Source

Large institutional investor in long-short hedge funds who maintains...

1 timeline of meetings with funds,2 depository of pitch-books and notes from meetings,3 dataset of AUM and returns from funds met, and4 flag of funds “admitted” for investment.

Research Findings:

1σ ↑ private information proxy doubles probability of fund admissionand reduces due-diligence time by 20%.“Subjective” judgements not wasteful - 12m peer-adjusted averagereturns is 1.5% higher for admitted funds.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Data Source

Large institutional investor in long-short hedge funds who maintains...

1 timeline of meetings with funds,2 depository of pitch-books and notes from meetings,3 dataset of AUM and returns from funds met, and4 flag of funds “admitted” for investment.

Research Findings:1σ ↑ private information proxy doubles probability of fund admissionand reduces due-diligence time by 20%.

“Subjective” judgements not wasteful - 12m peer-adjusted averagereturns is 1.5% higher for admitted funds.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Data Source

Large institutional investor in long-short hedge funds who maintains...

1 timeline of meetings with funds,2 depository of pitch-books and notes from meetings,3 dataset of AUM and returns from funds met, and4 flag of funds “admitted” for investment.

Research Findings:1σ ↑ private information proxy doubles probability of fund admissionand reduces due-diligence time by 20%.“Subjective” judgements not wasteful - 12m peer-adjusted averagereturns is 1.5% higher for admitted funds.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Et(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

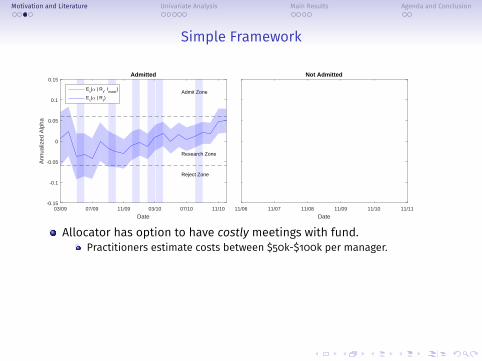

Allocator has a prior of funds’ abilities, α0 ∼ N(µ, 1

τ0

).

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Et(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Allocator has a prior of funds’ abilities, α0 ∼ N(µ, 1

τ0

).

E.g. µ is universe’s average excess returns, rext+1 = rt+1 − rpeert+1 .

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Et(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Allocator has a prior of funds’ abilities, α0 ∼ N(µ, 1

τ0

).

E.g. µ is universe’s average excess returns, rext+1 = rt+1 − rpeert+1 .

Assume Bayesian-normal updating - Ht and ht are realized returnsand precision, inception (t=0) to t.

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Et(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Allocator has a prior of funds’ abilities, α0 ∼ N(µ, 1

τ0

).

E.g. µ is universe’s average excess returns, rext+1 = rt+1 − rpeert+1 .

Assume Bayesian-normal updating - Ht and ht are realized returnsand precision, inception (t=0) to t.

Etαt+1 =tHtht+µτ0th+τ0

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Et(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Allocator has a prior of funds’ abilities, α0 ∼ N(µ, 1

τ0

).

E.g. µ is universe’s average excess returns, rext+1 = rt+1 − rpeert+1 .

Assume Bayesian-normal updating - Ht and ht are realized returnsand precision, inception (t=0) to t.

Etαt+1 =tHtht+µτ0th+τ0

Etτt+1 = th+ τ0,

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Et(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Monthly decision thresholds.

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Research Zone

Reject Zone

Admit ZoneE

t(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Monthly decision thresholds.Average annual rex of admitted funds is 6.6%.

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Research Zone

Reject Zone

Admit ZoneE

t(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Monthly decision thresholds.Average annual rex of admitted funds is 6.6%.Later we show why thresholds are actually defined endogenously.

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Research Zone

Reject Zone

Admit ZoneE

t(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Allocator has option to have costly meetings with fund.Practitioners estimate costs between $50k-$100k per manager.

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Research Zone

Reject Zone

Admit ZoneE

t(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Allocator has option to have costly meetings with fund.Practitioners estimate costs between $50k-$100k per manager.At each meeting allocator receives a signal on ability ∼ N

(S, 1

s).

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Research Zone

Reject Zone

Admit ZoneE

t(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Allocator has option to have costly meetings with fund.Practitioners estimate costs between $50k-$100k per manager.At each meeting allocator receives a signal on ability ∼ N

(S, 1

s).

Signal ∼ as entire sample of returns - i.e. inception to June 2012.

Bayesian-normal updated - now with info from meetings, mt, to t.

Etαt+1 =mtSs+tHtht+µτ0

mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Research Zone

Reject Zone

Admit ZoneE

t(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Bayesian-normal updated - now with info from meetings, mt, to t.Etαt+1 =

mtSs+tHtht+µτ0mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Research Zone

Reject Zone

Admit ZoneE

t(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Research Zone

Reject Zone

Admit Zone

Bayesian-normal updated - now with info from meetings, mt, to t.Etαt+1 =

mtSs+tHtht+µτ0mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Simple Framework

03/09 07/09 11/09 03/10 07/10 11/10

Date

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

Ann

ualiz

ed A

lpha

Admitted

Research Zone

Reject Zone

Admit ZoneE

t(, | R

t, I

meet)

Et(, | R

t)

11/06 11/07 11/08 11/09 11/10 11/11

Date

Not Admitted

Research Zone

Reject Zone

Admit Zone

Bayesian-normal updated - now with info from meetings, mt, to t.Etαt+1 =

mtSs+tHtht+µτ0mts+th+τ0

Etτt+1 = mts+ th+ τ0,

Threshold: tradeoff benefits of greater precision given current α andτ estimate vs. cost of additional due-diligence.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Literature

Mainly regarding mutual funds, little outside...Choosing managers: Evans & Fahlenbrach (2012); Jenkinson, Jones &Martinez (2015); etc.

Skill vs. luck: Korteweg & Sorensen (2014); Berk & Van Binsbergen(2015); etc.Pooling of funds: Berk & Green (2004); Gervais & Strobl (2015); etc.

Contribution to literature:

1 Quantify effects of “private” information on timing and performanceof investment decisions.

2 Develop rigorous, tractable framework for the institutional portfoliomanagement problem.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Literature

Mainly regarding mutual funds, little outside...Choosing managers: Evans & Fahlenbrach (2012); Jenkinson, Jones &Martinez (2015); etc.Skill vs. luck: Korteweg & Sorensen (2014); Berk & Van Binsbergen(2015); etc.

Pooling of funds: Berk & Green (2004); Gervais & Strobl (2015); etc.

Contribution to literature:

1 Quantify effects of “private” information on timing and performanceof investment decisions.

2 Develop rigorous, tractable framework for the institutional portfoliomanagement problem.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Literature

Mainly regarding mutual funds, little outside...Choosing managers: Evans & Fahlenbrach (2012); Jenkinson, Jones &Martinez (2015); etc.Skill vs. luck: Korteweg & Sorensen (2014); Berk & Van Binsbergen(2015); etc.Pooling of funds: Berk & Green (2004); Gervais & Strobl (2015); etc.

Contribution to literature:

1 Quantify effects of “private” information on timing and performanceof investment decisions.

2 Develop rigorous, tractable framework for the institutional portfoliomanagement problem.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Literature

Mainly regarding mutual funds, little outside...Choosing managers: Evans & Fahlenbrach (2012); Jenkinson, Jones &Martinez (2015); etc.Skill vs. luck: Korteweg & Sorensen (2014); Berk & Van Binsbergen(2015); etc.Pooling of funds: Berk & Green (2004); Gervais & Strobl (2015); etc.

Contribution to literature:1 Quantify effects of “private” information on timing and performance

of investment decisions.

2 Develop rigorous, tractable framework for the institutional portfoliomanagement problem.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Literature

Mainly regarding mutual funds, little outside...Choosing managers: Evans & Fahlenbrach (2012); Jenkinson, Jones &Martinez (2015); etc.Skill vs. luck: Korteweg & Sorensen (2014); Berk & Van Binsbergen(2015); etc.Pooling of funds: Berk & Green (2004); Gervais & Strobl (2015); etc.

Contribution to literature:1 Quantify effects of “private” information on timing and performance

of investment decisions.2 Develop rigorous, tractable framework for the institutional portfolio

management problem.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Historical Returns Are Not Enough0

2040

60D

ensi

ty

-.04 -.02 0 .02 .04

1-4 Months

-.04 -.02 0 .02 .04

5-12 Months

Admitted Not Admitted

Closest matched by observables - AUM, age, past info ratio.

Matches limited to same month and strategy - e.g. EM, sector.Ranksum and KS tests rejected at 5%.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Historical Returns Are Not Enough0

2040

60D

ensi

ty

-.04 -.02 0 .02 .04

1-4 Months

-.04 -.02 0 .02 .04

5-12 Months

Admitted Not Admitted

Closest matched by observables - AUM, age, past info ratio.Matches limited to same month and strategy - e.g. EM, sector.

Ranksum and KS tests rejected at 5%.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Historical Returns Are Not Enough0

2040

60D

ensi

ty

-.04 -.02 0 .02 .04

1-4 Months

-.04 -.02 0 .02 .04

5-12 Months

Admitted Not Admitted

Closest matched by observables - AUM, age, past info ratio.Matches limited to same month and strategy - e.g. EM, sector.Ranksum and KS tests rejected at 5%.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Quantity of Soft Information0

.1.2

.3.4

.5M

eetin

gs p

er m

onth

3 6 91=First Due-Diligence Month

-9 -6 -3-1=Last Due-diligence Month

Not Admitted Admitted

First 9 months of due-diligence period.Last 9 months of due-diligence period.Occurrence of meeting - good proxy for quantity of information.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Quantity of Soft Information0

.1.2

.3.4

.5M

eetin

gs p

er m

onth

3 6 91=First Due-Diligence Month

-9 -6 -3-1=Last Due-diligence Month

Not Admitted Admitted

First 9 months of due-diligence period.

Last 9 months of due-diligence period.Occurrence of meeting - good proxy for quantity of information.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Quantity of Soft Information0

.1.2

.3.4

.5M

eetin

gs p

er m

onth

3 6 91=First Due-Diligence Month

-9 -6 -3-1=Last Due-diligence Month

Not Admitted Admitted

First 9 months of due-diligence period.Last 9 months of due-diligence period.

Occurrence of meeting - good proxy for quantity of information.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Quantity of Soft Information0

.1.2

.3.4

Mee

tings

per

mon

th

3 6 91=First Due-Diligence Month

-9 -6 -3-1=Last Due-diligence Month

Not Admitted Admitted

First 9 months of due-diligence period.Last 9 months of due-diligence period.Occurrence of meeting - good proxy for quantity of information.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

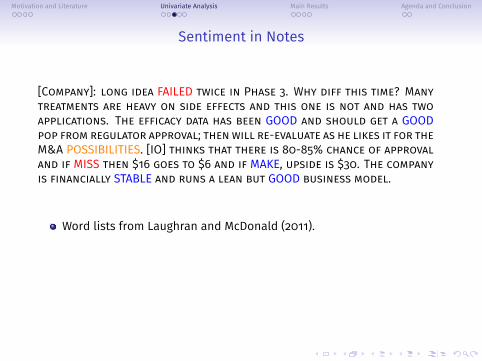

Sentiment in Notes

[Company]: long idea FAILED twice in Phase 3. Why diff this time? Manytreatments are heavy on side effects and this one is not and has twoapplications. The efficacy data has been GOOD and should get a GOODpop from regulator approval; then will re-evaluate as he likes it for theM&A POSSIBILITIES. [IO] thinks that there is 80-85% chance of approvaland if MISS then $16 goes to $6 and if MAKE, upside is $30. The companyis financially STABLE and runs a lean but GOOD business model.

Word lists from Laughran and McDonald (2011).

Positive and negative words tend to involve discussions about valueof positions, under-

or overvalued.

Uncertain words tend to focus on concerns about fund strategy,inconsistency and viability.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Sentiment in Notes

[Company]: long idea FAILED twice in Phase 3. Why diff this time? Manytreatments are heavy on side effects and this one is not and has twoapplications. The efficacy data has been GOOD and should get a GOODpop from regulator approval; then will re-evaluate as he likes it for theM&A POSSIBILITIES. [IO] thinks that there is 80-85% chance of approvaland if MISS then $16 goes to $6 and if MAKE, upside is $30. The companyis financially STABLE and runs a lean but GOOD business model.

Word lists from Laughran and McDonald (2011).Positive and negative words tend to involve discussions about valueof positions, under-

or overvalued.Uncertain words tend to focus on concerns about fund strategy,inconsistency and viability.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Sentiment in Notes

[Company]: short idea where [IO] looked through the case studies andfound that the vaccine didn’t produce the proper anitbodies; onceproven INEFFECTIVE, the stock tanked.

Word lists from Laughran and McDonald (2011).Positive and negative words tend to involve discussions about valueof positions, under- or overvalued.

Uncertain words tend to focus on concerns about fund strategy,inconsistency and viability.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Sentiment in Notes

RISK management is done through sizing of positions and he has a will-ingness to go to CASH if need be. Why? many times these events have 80%type moves so you don’t need full EXPOSURE to move the needle for theoverall portfolio. [Manager] SEEMS to be a solid “sandbox” player in HCand has enough insights to play events.

Word lists from Laughran and McDonald (2011).Positive and negative words tend to involve discussions about valueof positions, under- or overvalued.Uncertain words tend to focus on concerns about fund strategy,inconsistency and viability.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

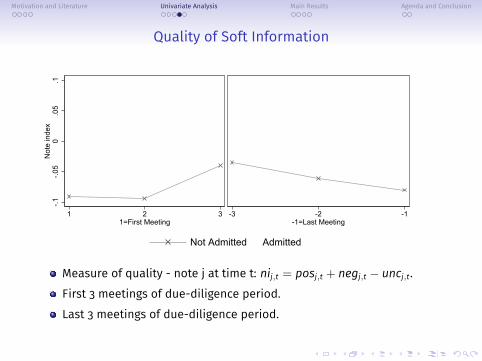

Quality of Soft Information-.1

-.05

0.0

5.1

Not

e in

dex

1 2 31=First Meeting

-3 -2 -1-1=Last Meeting

Not Admitted Admitted

Measure of quality - note j at time t: nij,t = posj,t + negj,t − uncj,t.

First 3 meetings of due-diligence period.Last 3 meetings of due-diligence period.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Quality of Soft Information-.1

-.05

0.0

5.1

Not

e in

dex

1 2 31=First Meeting

-3 -2 -1-1=Last Meeting

Not Admitted Admitted

Measure of quality - note j at time t: nij,t = posj,t + negj,t − uncj,t.First 3 meetings of due-diligence period.

Last 3 meetings of due-diligence period.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Quality of Soft Information-.1

-.05

0.0

5.1

Not

e in

dex

1 2 31=First Meeting

-3 -2 -1-1=Last Meeting

Not Admitted Admitted

Measure of quality - note j at time t: nij,t = posj,t + negj,t − uncj,t.First 3 meetings of due-diligence period.Last 3 meetings of due-diligence period.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Quality of Soft Information-.1

-.05

0.0

5.1

Not

e in

dex

1 2 31=First Meeting

-3 -2 -1-1=Last Meeting

Not Admitted Admitted

Measure of quality - note j at time t: nij,t = posj,t + negj,t − uncj,t.First 3 meetings of due-diligence period.Last 3 meetings of due-diligence period.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Stock of Information1

23

4S

oft i

ndex

3 6 91=First Due-Diligence Month

-9 -6 -3-1=Last Due-diligence Month

Not Admitted Admitted

Define variable that captures stock of soft information, SIi,t:

SIi,t =

Imeeti,t + B (nii,t) at t = 1SIi,t−1 if no meeting at t,SIi,t−1 + Imeeti,t + B (nii,t) if meeting occurs at t.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Stock of Information1

23

4S

oft i

ndex

3 6 91=First Due-Diligence Month

-9 -6 -3-1=Last Due-diligence Month

Not Admitted Admitted

Define variable that captures stock of soft information, SIi,t:

SIi,t =

Imeeti,t + B (nii,t) at t = 1

SIi,t−1 if no meeting at t,SIi,t−1 + Imeeti,t + B (nii,t) if meeting occurs at t.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Stock of Information1

23

4S

oft i

ndex

3 6 91=First Due-Diligence Month

-9 -6 -3-1=Last Due-diligence Month

Not Admitted Admitted

Define variable that captures stock of soft information, SIi,t:

SIi,t =

Imeeti,t + B (nii,t) at t = 1SIi,t−1 if no meeting at t,

SIi,t−1 + Imeeti,t + B (nii,t) if meeting occurs at t.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Stock of Information1

23

4S

oft i

ndex

3 6 91=First Due-Diligence Month

-9 -6 -3-1=Last Due-diligence Month

Not Admitted Admitted

Define variable that captures stock of soft information, SIi,t:

SIi,t =

Imeeti,t + B (nii,t) at t = 1SIi,t−1 if no meeting at t,SIi,t−1 + Imeeti,t + B (nii,t) if meeting occurs at t.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Stock of Information1

23

4S

oft i

ndex

3 6 91=First Due-Diligence Month

-9 -6 -3-1=Last Due-diligence Month

Not Admitted Admitted

Define variable that captures stock of soft information, SIi,t:

SIi,t =

Imeeti,t + B (nii,t) at t = 1SIi,t−1 if no meeting at t,SIi,t−1 + Imeeti,t + B (nii,t) if meeting occurs at t.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Multi-variate Hazard

Logistic discrete time hazard of sequential Admission process -

λ (t|Xi,t) = P (Ai = t|Ai ≥ t)

= log(

pi1− pi

)= µi,0 + µ0,t + βXi,t + f (θ; t)

Xi,t includes hard (observables) and soft (private) information.Simple parametrization of baseline hazard, f (θ; t).Can add time, strategy FE and firm time-invariant attributes.

Variables of interest -

Hard information - returns and AUM.Soft information - SIi,t, affiliated school and fund dummies.Baseline parametrization: f (θ; t) = θdurti + θcon ln ti

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Multi-variate Hazard

Logistic discrete time hazard of sequential Admission process -

λ (t|Xi,t) = P (Ai = t|Ai ≥ t) = log(

pi1− pi

)= µi,0 + µ0,t + βXi,t + f (θ; t)

Xi,t includes hard (observables) and soft (private) information.Simple parametrization of baseline hazard, f (θ; t).Can add time, strategy FE and firm time-invariant attributes.

Variables of interest -

Hard information - returns and AUM.Soft information - SIi,t, affiliated school and fund dummies.Baseline parametrization: f (θ; t) = θdurti + θcon ln ti

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Multi-variate Hazard

Logistic discrete time hazard of sequential Admission process -

λ (t|Xi,t) = P (Ai = t|Ai ≥ t) = log(

pi1− pi

)= µi,0 + µ0,t + βXi,t + f (θ; t)

Xi,t includes hard (observables) and soft (private) information.

Simple parametrization of baseline hazard, f (θ; t).Can add time, strategy FE and firm time-invariant attributes.

Variables of interest -

Hard information - returns and AUM.Soft information - SIi,t, affiliated school and fund dummies.Baseline parametrization: f (θ; t) = θdurti + θcon ln ti

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Multi-variate Hazard

Logistic discrete time hazard of sequential Admission process -

λ (t|Xi,t) = P (Ai = t|Ai ≥ t) = log(

pi1− pi

)= µi,0 + µ0,t + βXi,t + f (θ; t)

Xi,t includes hard (observables) and soft (private) information.Simple parametrization of baseline hazard, f (θ; t).

Can add time, strategy FE and firm time-invariant attributes.

Variables of interest -

Hard information - returns and AUM.Soft information - SIi,t, affiliated school and fund dummies.Baseline parametrization: f (θ; t) = θdurti + θcon ln ti

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Multi-variate Hazard

Logistic discrete time hazard of sequential Admission process -

λ (t|Xi,t) = P (Ai = t|Ai ≥ t) = log(

pi1− pi

)= µi,0 + µ0,t + βXi,t + f (θ; t)

Xi,t includes hard (observables) and soft (private) information.Simple parametrization of baseline hazard, f (θ; t).Can add time, strategy FE and firm time-invariant attributes.

Variables of interest -

Hard information - returns and AUM.Soft information - SIi,t, affiliated school and fund dummies.Baseline parametrization: f (θ; t) = θdurti + θcon ln ti

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Multi-variate Hazard

Logistic discrete time hazard of sequential Admission process -

λ (t|Xi,t) = P (Ai = t|Ai ≥ t) = log(

pi1− pi

)= µi,0 + µ0,t + βXi,t + f (θ; t)

Xi,t includes hard (observables) and soft (private) information.Simple parametrization of baseline hazard, f (θ; t).Can add time, strategy FE and firm time-invariant attributes.

Variables of interest -

Hard information - returns and AUM.Soft information - SIi,t, affiliated school and fund dummies.Baseline parametrization: f (θ; t) = θdurti + θcon ln ti

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Multi-variate Hazard

Logistic discrete time hazard of sequential Admission process -

λ (t|Xi,t) = P (Ai = t|Ai ≥ t) = log(

pi1− pi

)= µi,0 + µ0,t + βXi,t + f (θ; t)

Xi,t includes hard (observables) and soft (private) information.Simple parametrization of baseline hazard, f (θ; t).Can add time, strategy FE and firm time-invariant attributes.

Variables of interest -Hard information - returns and AUM.

Soft information - SIi,t, affiliated school and fund dummies.Baseline parametrization: f (θ; t) = θdurti + θcon ln ti

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Multi-variate Hazard

Logistic discrete time hazard of sequential Admission process -

λ (t|Xi,t) = P (Ai = t|Ai ≥ t) = log(

pi1− pi

)= µi,0 + µ0,t + βXi,t + f (θ; t)

Xi,t includes hard (observables) and soft (private) information.Simple parametrization of baseline hazard, f (θ; t).Can add time, strategy FE and firm time-invariant attributes.

Variables of interest -Hard information - returns and AUM.Soft information - SIi,t, affiliated school and fund dummies.

Baseline parametrization: f (θ; t) = θdurti + θcon ln ti

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Multi-variate Hazard

Logistic discrete time hazard of sequential Admission process -

λ (t|Xi,t) = P (Ai = t|Ai ≥ t) = log(

pi1− pi

)= µi,0 + µ0,t + βXi,t + f (θ; t)

Xi,t includes hard (observables) and soft (private) information.Simple parametrization of baseline hazard, f (θ; t).Can add time, strategy FE and firm time-invariant attributes.

Variables of interest -Hard information - returns and AUM.Soft information - SIi,t, affiliated school and fund dummies.Baseline parametrization: f (θ; t) = θdurti + θcon ln ti

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103 0.00094 0.00089 0.00063 0.00061(6.68) (6.60) (6.86) (6.02) (6.35)

Log(AUM) 0.00095 0.00082 0.00091 0.00060 0.00067(4.63) (4.39) (5.13) (3.82) (4.57)

Soft information:

Affiliated fund (D) 0.00071 0.00053(2.83) (2.26)

Affiliated college (D) 0.00079 0.00082(3.46) (3.81)

Soft index (lagged) 0.00096 0.00088(9.88) (10.67)

Due-diligence spell:

Log(Duration) 0.00073 0.00116 0.00106 0.00055 0.00050(2.93) (3.77) (3.73) (2.38) (2.32)

Duration − 0.00007 − 0.00008 − 0.00008 − 0.00007 − 0.00006(−3.90) (−4.36) (−4.26) (−4.96) (−4.92)

Market variables + + + + +Year FE + + + +Strategy FE + +

Observations 45,714 45,714 45,714 45,714 45,714Pseudo R2 0.1029 0.1223 0.1342 0.1714 0.1819LR-test p-value 0.0000 0.0000 0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103

0.00094 0.00089 0.00063 0.00061

(6.68)

(6.60) (6.86) (6.02) (6.35)

Log(AUM) 0.00095

0.00082 0.00091 0.00060 0.00067

(4.63)

(4.39) (5.13) (3.82) (4.57)

Soft information:

Affiliated fund (D) 0.00071 0.00053(2.83) (2.26)

Affiliated college (D) 0.00079 0.00082(3.46) (3.81)

Soft index (lagged) 0.00096 0.00088(9.88) (10.67)

Due-diligence spell:

Log(Duration) 0.00073 0.00116 0.00106 0.00055 0.00050(2.93) (3.77) (3.73) (2.38) (2.32)

Duration − 0.00007 − 0.00008 − 0.00008 − 0.00007 − 0.00006(−3.90) (−4.36) (−4.26) (−4.96) (−4.92)

Market variables + + + + +Year FE + + + +Strategy FE + +

Observations 45,714 45,714 45,714 45,714 45,714Pseudo R2 0.1029 0.1223 0.1342 0.1714 0.1819LR-test p-value 0.0000 0.0000 0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103

0.00094 0.00089 0.00063 0.00061

(6.68)

(6.60) (6.86) (6.02) (6.35)

Log(AUM) 0.00095

0.00082 0.00091 0.00060 0.00067

(4.63)

(4.39) (5.13) (3.82) (4.57)

Soft information:

Affiliated fund (D) 0.00071 0.00053(2.83) (2.26)

Affiliated college (D) 0.00079 0.00082(3.46) (3.81)

Soft index (lagged) 0.00096 0.00088(9.88) (10.67)

Due-diligence spell:Log(Duration) 0.00073

0.00116 0.00106 0.00055 0.00050

(2.93)

(3.77) (3.73) (2.38) (2.32)

Duration − 0.00007

− 0.00008 − 0.00008 − 0.00007 − 0.00006

(−3.90)

(−4.36) (−4.26) (−4.96) (−4.92)

Market variables + + + + +Year FE + + + +Strategy FE + +

Observations 45,714 45,714 45,714 45,714 45,714Pseudo R2 0.1029 0.1223 0.1342 0.1714 0.1819LR-test p-value 0.0000 0.0000 0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103

0.00094 0.00089 0.00063 0.00061

(6.68)

(6.60) (6.86) (6.02) (6.35)

Log(AUM) 0.00095

0.00082 0.00091 0.00060 0.00067

(4.63)

(4.39) (5.13) (3.82) (4.57)

Soft information:

Affiliated fund (D) 0.00071 0.00053(2.83) (2.26)

Affiliated college (D) 0.00079 0.00082(3.46) (3.81)

Soft index (lagged) 0.00096 0.00088(9.88) (10.67)

Due-diligence spell:Log(Duration) 0.00073

0.00116 0.00106 0.00055 0.00050

(2.93)

(3.77) (3.73) (2.38) (2.32)

Duration − 0.00007

− 0.00008 − 0.00008 − 0.00007 − 0.00006

(−3.90)

(−4.36) (−4.26) (−4.96) (−4.92)

Market variables +

+ + + +Year FE + + + +Strategy FE + +

Observations 45,714 45,714 45,714 45,714 45,714Pseudo R2 0.1029 0.1223 0.1342 0.1714 0.1819LR-test p-value 0.0000 0.0000 0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103

0.00094 0.00089 0.00063 0.00061

(6.68)

(6.60) (6.86) (6.02) (6.35)

Log(AUM) 0.00095

0.00082 0.00091 0.00060 0.00067

(4.63)

(4.39) (5.13) (3.82) (4.57)

Soft information:

Affiliated fund (D) 0.00071 0.00053(2.83) (2.26)

Affiliated college (D) 0.00079 0.00082(3.46) (3.81)

Soft index (lagged) 0.00096 0.00088(9.88) (10.67)

Due-diligence spell:Log(Duration) 0.00073

0.00116 0.00106 0.00055 0.00050

(2.93)

(3.77) (3.73) (2.38) (2.32)

Duration − 0.00007

− 0.00008 − 0.00008 − 0.00007 − 0.00006

(−3.90)

(−4.36) (−4.26) (−4.96) (−4.92)

Market variables +

+ + + +

Year FE

+ + + +Strategy FE + +

Observations 45,714 45,714 45,714 45,714 45,714Pseudo R2 0.1029 0.1223 0.1342 0.1714 0.1819LR-test p-value 0.0000 0.0000 0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103

0.00094 0.00089 0.00063 0.00061

(6.68)

(6.60) (6.86) (6.02) (6.35)

Log(AUM) 0.00095

0.00082 0.00091 0.00060 0.00067

(4.63)

(4.39) (5.13) (3.82) (4.57)

Soft information:

Affiliated fund (D) 0.00071 0.00053(2.83) (2.26)

Affiliated college (D) 0.00079 0.00082(3.46) (3.81)

Soft index (lagged) 0.00096 0.00088(9.88) (10.67)

Due-diligence spell:Log(Duration) 0.00073

0.00116 0.00106 0.00055 0.00050

(2.93)

(3.77) (3.73) (2.38) (2.32)

Duration − 0.00007

− 0.00008 − 0.00008 − 0.00007 − 0.00006

(−3.90)

(−4.36) (−4.26) (−4.96) (−4.92)

Market variables +

+ + + +

Year FE

+ + + +

Strategy FE

+ +

Observations 45,714 45,714 45,714 45,714 45,714Pseudo R2 0.1029 0.1223 0.1342 0.1714 0.1819LR-test p-value 0.0000 0.0000 0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103

0.00094 0.00089 0.00063 0.00061

(6.68)

(6.60) (6.86) (6.02) (6.35)

Log(AUM) 0.00095

0.00082 0.00091 0.00060 0.00067

(4.63)

(4.39) (5.13) (3.82) (4.57)

Soft information:

Affiliated fund (D) 0.00071 0.00053(2.83) (2.26)

Affiliated college (D) 0.00079 0.00082(3.46) (3.81)

Soft index (lagged) 0.00096 0.00088(9.88) (10.67)

Due-diligence spell:Log(Duration) 0.00073

0.00116 0.00106 0.00055 0.00050

(2.93)

(3.77) (3.73) (2.38) (2.32)

Duration − 0.00007

− 0.00008 − 0.00008 − 0.00007 − 0.00006

(−3.90)

(−4.36) (−4.26) (−4.96) (−4.92)

Market variables +

+ + + +

Year FE

+ + + +

Strategy FE

+ +

Observations 45,714

45,714 45,714 45,714 45,714

Pseudo R2 0.1029

0.1223 0.1342 0.1714 0.1819

LR-test p-value

0.0000 0.0000 0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103 0.00094

0.00089 0.00063 0.00061

(6.68) (6.60)

(6.86) (6.02) (6.35)

Log(AUM) 0.00095 0.00082

0.00091 0.00060 0.00067

(4.63) (4.39)

(5.13) (3.82) (4.57)

Soft information:

Affiliated fund (D) 0.00071 0.00053(2.83) (2.26)

Affiliated college (D) 0.00079 0.00082(3.46) (3.81)

Soft index (lagged) 0.00096 0.00088(9.88) (10.67)

Due-diligence spell:Log(Duration) 0.00073 0.00116

0.00106 0.00055 0.00050

(2.93) (3.77)

(3.73) (2.38) (2.32)

Duration − 0.00007 − 0.00008

− 0.00008 − 0.00007 − 0.00006

(−3.90) (−4.36)

(−4.26) (−4.96) (−4.92)

Market variables + +

+ + +

Year FE +

+ + +

Strategy FE

+ +

Observations 45,714 45,714

45,714 45,714 45,714

Pseudo R2 0.1029 0.1223

0.1342 0.1714 0.1819

LR-test p-value 0.0000

0.0000 0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103 0.00094 0.00089

0.00063 0.00061

(6.68) (6.60) (6.86)

(6.02) (6.35)

Log(AUM) 0.00095 0.00082 0.00091

0.00060 0.00067

(4.63) (4.39) (5.13)

(3.82) (4.57)

Soft information:

Affiliated fund (D) 0.00071 0.00053(2.83) (2.26)

Affiliated college (D) 0.00079 0.00082(3.46) (3.81)

Soft index (lagged) 0.00096 0.00088(9.88) (10.67)

Due-diligence spell:Log(Duration) 0.00073 0.00116 0.00106

0.00055 0.00050

(2.93) (3.77) (3.73)

(2.38) (2.32)

Duration − 0.00007 − 0.00008 − 0.00008

− 0.00007 − 0.00006

(−3.90) (−4.36) (−4.26)

(−4.96) (−4.92)

Market variables + + +

+ +

Year FE + +

+ +

Strategy FE +

+

Observations 45,714 45,714 45,714

45,714 45,714

Pseudo R2 0.1029 0.1223 0.1342

0.1714 0.1819

LR-test p-value 0.0000 0.0000

0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103 0.00094 0.00089 0.00063

0.00061

(6.68) (6.60) (6.86) (6.02)

(6.35)

Log(AUM) 0.00095 0.00082 0.00091 0.00060

0.00067

(4.63) (4.39) (5.13) (3.82)

(4.57)

Soft information:Affiliated fund (D) 0.00071

0.00053

(2.83)

(2.26)

Affiliated college (D) 0.00079

0.00082

(3.46)

(3.81)

Soft index (lagged) 0.00096

0.00088

(9.88)

(10.67)

Due-diligence spell:Log(Duration) 0.00073 0.00116 0.00106 0.00055

0.00050

(2.93) (3.77) (3.73) (2.38)

(2.32)

Duration − 0.00007 − 0.00008 − 0.00008 − 0.00007

− 0.00006

(−3.90) (−4.36) (−4.26) (−4.96)

(−4.92)

Market variables + + + +

+

Year FE + + +

+

Strategy FE +

+

Observations 45,714 45,714 45,714 45,714

45,714

Pseudo R2 0.1029 0.1223 0.1342 0.1714

0.1819

LR-test p-value 0.0000 0.0000 0.0000

0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Main ResultsHard information:

Information ratio 0.00103 0.00094 0.00089 0.00063 0.00061(6.68) (6.60) (6.86) (6.02) (6.35)

Log(AUM) 0.00095 0.00082 0.00091 0.00060 0.00067(4.63) (4.39) (5.13) (3.82) (4.57)

Soft information:Affiliated fund (D) 0.00071 0.00053

(2.83) (2.26)Affiliated college (D) 0.00079 0.00082

(3.46) (3.81)Soft index (lagged) 0.00096 0.00088

(9.88) (10.67)Due-diligence spell:

Log(Duration) 0.00073 0.00116 0.00106 0.00055 0.00050(2.93) (3.77) (3.73) (2.38) (2.32)

Duration − 0.00007 − 0.00008 − 0.00008 − 0.00007 − 0.00006(−3.90) (−4.36) (−4.26) (−4.96) (−4.92)

Market variables + + + + +Year FE + + + +Strategy FE + +

Observations 45,714 45,714 45,714 45,714 45,714Pseudo R2 0.1029 0.1223 0.1342 0.1714 0.1819LR-test p-value 0.0000 0.0000 0.0000 0.0000

Univariate Hazard

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

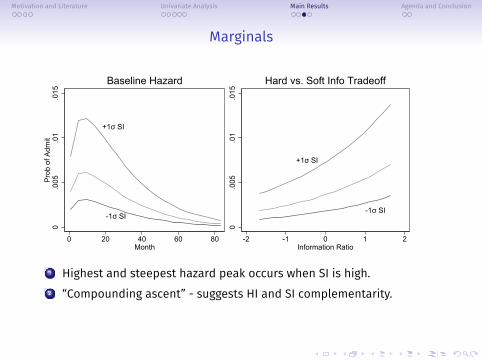

Marginals

+1σ SI

-1σ SI

0.0

05.0

1.0

15P

rob

of A

dmit

0 20 40 60 80Month

Baseline Hazard

0.0

05.0

1.0

15-2 -1 0 1 2

Information Ratio

Hard vs. Soft Info Tradeoff

1 Highest and steepest hazard peak occurs when SI is high.

2 “Compounding ascent” - suggests HI and SI complementarity.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Marginals

+1σ SI

-1σ SI

0.0

05.0

1.0

15P

rob

of A

dmit

0 20 40 60 80Month

Baseline Hazard

+1σ SI

-1σ SI

0.0

05.0

1.0

15-2 -1 0 1 2

Information Ratio

Hard vs. Soft Info Tradeoff

1 Highest and steepest hazard peak occurs when SI is high.2 “Compounding ascent” - suggests HI and SI complementarity.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

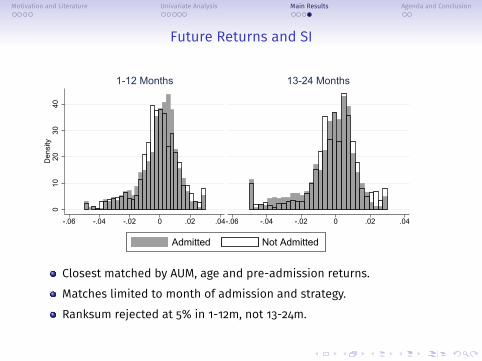

Future Returns and SI0

1020

3040

Den

sity

-.06 -.04 -.02 0 .02 .04

1-12 Months

-.06 -.04 -.02 0 .02 .04

13-24 Months

Admitted Not Admitted

Closest matched by AUM, age and pre-admission returns.

Matches limited to month of admission and strategy.Ranksum rejected at 5% in 1-12m, not 13-24m.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Future Returns and SI0

1020

3040

Den

sity

-.06 -.04 -.02 0 .02 .04

1-12 Months

-.06 -.04 -.02 0 .02 .04

13-24 Months

Admitted Not Admitted

Closest matched by AUM, age and pre-admission returns.Matches limited to month of admission and strategy.

Ranksum rejected at 5% in 1-12m, not 13-24m.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Future Returns and SI0

1020

3040

Den

sity

-.06 -.04 -.02 0 .02 .04

1-12 Months

-.06 -.04 -.02 0 .02 .04

13-24 Months

Admitted Not Admitted

Closest matched by AUM, age and pre-admission returns.Matches limited to month of admission and strategy.Ranksum rejected at 5% in 1-12m, not 13-24m.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Model

V (α) = max{0, π (α), βEVt+1 (α)− c}

Time

Estim

ated

Alpha

Estimated Alpha

Estim

ated

Profits

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Model

V (α) = max{0, π (α), βEVt+1 (α)− c}

Time

Estim

ated

Alpha

Estimated Alpha

Estim

ated

Profits

0

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Model

V (α) = max{0, π (α), βEVt+1 (α)− c}

Time

Estim

ated

Alpha

Estimated Alpha

Estim

ated

Profits

0

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Model

V (α) = max{0, π (α), βEVt+1 (α)− c}

Time

Estim

ated

Alpha

Estimated Alpha

Estim

ated

Profits

‐c

0

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Model

V (α) = max{0, π (α), βEVt+1 (α)− c}

Time

Estim

ated

Alpha

Estimated Alpha

Estim

ated

Profits

‐c

0

1 The value of collecting information is non-increasing in time.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Model

V (α) = max{0, π (α), βEVt+1 (α)− c}

Time

Estim

ated

Alpha

Estimated Alpha

Estim

ated

Profits

‐c

0

N

1 The value of collecting information is non-increasing in time.2 There is an optimal N ≤ ∞ where research stops.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Model

V (α) = max{0, π (α), βEVt+1 (α)− c}

Research Zone

Acceptance Zone

Rejection Zone

Time

Estim

ated

Alpha

Estimated Alpha

Estim

ated

Profits

‐c

0

N

1 The value of collecting information is non-increasing in time.2 There is an optimal N ≤ ∞ where research stops.3 For t ≤ N, there is a lower (rejection) and upper (accept) boundary.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Conclusion

Empirical results and intuition line up on key dimensions:Both HI and SI are consistent with model.Baseline - i.e. passage of due-diligence time - effect is concave.

Contribution to literature:

Importance of the “time-to-decision” in spirit of Berk & Green (2004).Pecuniary benefits of SI in contrast to Jenkinson et al (2015).

Going forward, better link model to richness of data:

1 Different sources - HI cheap/low quality, SI expensive/high quality.2 Varying intensity - precision of meetings is choice variable.3 Competing Hazards - to meet or admit? HI vs. SI complementarity.4 Importance of SI may vary over time as more HI collected.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Conclusion

Empirical results and intuition line up on key dimensions:Both HI and SI are consistent with model.Baseline - i.e. passage of due-diligence time - effect is concave.

Contribution to literature:Importance of the “time-to-decision” in spirit of Berk & Green (2004).Pecuniary benefits of SI in contrast to Jenkinson et al (2015).

Going forward, better link model to richness of data:

1 Different sources - HI cheap/low quality, SI expensive/high quality.2 Varying intensity - precision of meetings is choice variable.3 Competing Hazards - to meet or admit? HI vs. SI complementarity.4 Importance of SI may vary over time as more HI collected.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Conclusion

Empirical results and intuition line up on key dimensions:Both HI and SI are consistent with model.Baseline - i.e. passage of due-diligence time - effect is concave.

Contribution to literature:Importance of the “time-to-decision” in spirit of Berk & Green (2004).Pecuniary benefits of SI in contrast to Jenkinson et al (2015).

Going forward, better link model to richness of data:

1 Different sources - HI cheap/low quality, SI expensive/high quality.2 Varying intensity - precision of meetings is choice variable.3 Competing Hazards - to meet or admit? HI vs. SI complementarity.4 Importance of SI may vary over time as more HI collected.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Conclusion

Empirical results and intuition line up on key dimensions:Both HI and SI are consistent with model.Baseline - i.e. passage of due-diligence time - effect is concave.

Contribution to literature:Importance of the “time-to-decision” in spirit of Berk & Green (2004).Pecuniary benefits of SI in contrast to Jenkinson et al (2015).

Going forward, better link model to richness of data:1 Different sources - HI cheap/low quality, SI expensive/high quality.

2 Varying intensity - precision of meetings is choice variable.3 Competing Hazards - to meet or admit? HI vs. SI complementarity.4 Importance of SI may vary over time as more HI collected.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Conclusion

Empirical results and intuition line up on key dimensions:Both HI and SI are consistent with model.Baseline - i.e. passage of due-diligence time - effect is concave.

Contribution to literature:Importance of the “time-to-decision” in spirit of Berk & Green (2004).Pecuniary benefits of SI in contrast to Jenkinson et al (2015).

Going forward, better link model to richness of data:1 Different sources - HI cheap/low quality, SI expensive/high quality.2 Varying intensity - precision of meetings is choice variable.

3 Competing Hazards - to meet or admit? HI vs. SI complementarity.4 Importance of SI may vary over time as more HI collected.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Conclusion

Empirical results and intuition line up on key dimensions:Both HI and SI are consistent with model.Baseline - i.e. passage of due-diligence time - effect is concave.

Contribution to literature:Importance of the “time-to-decision” in spirit of Berk & Green (2004).Pecuniary benefits of SI in contrast to Jenkinson et al (2015).

Going forward, better link model to richness of data:1 Different sources - HI cheap/low quality, SI expensive/high quality.2 Varying intensity - precision of meetings is choice variable.3 Competing Hazards - to meet or admit? HI vs. SI complementarity.

4 Importance of SI may vary over time as more HI collected.

Motivation and Literature Univariate Analysis Main Results Agenda and Conclusion

Conclusion

Empirical results and intuition line up on key dimensions:Both HI and SI are consistent with model.Baseline - i.e. passage of due-diligence time - effect is concave.

Contribution to literature:Importance of the “time-to-decision” in spirit of Berk & Green (2004).Pecuniary benefits of SI in contrast to Jenkinson et al (2015).

Going forward, better link model to richness of data:1 Different sources - HI cheap/low quality, SI expensive/high quality.2 Varying intensity - precision of meetings is choice variable.3 Competing Hazards - to meet or admit? HI vs. SI complementarity.4 Importance of SI may vary over time as more HI collected.

Additional Material

Hazard Models

Hazard test time and covariates effects on prob of event given event notyet occurred.

Soft vs. hard information on decision to admit.

Right censoring - append public (HFI, CISDM, HFR, TASS) sources ofreturn data.

A simple time-invariant hazard model...

Define due-diligence for fund, Ai, as beginning on first meeting andending on admission or censor date.OLS specification -

ln Ai = µ+ βhiHard Infoi + βsiSoft Infoi + εi.

Assumes a proportional time to hazard, Ai = exp (x′iβ) A0.

Additional Material

Hazard Models

Hazard test time and covariates effects on prob of event given event notyet occurred.

Soft vs. hard information on decision to admit.Right censoring - append public (HFI, CISDM, HFR, TASS) sources ofreturn data.

A simple time-invariant hazard model...

Define due-diligence for fund, Ai, as beginning on first meeting andending on admission or censor date.OLS specification -

ln Ai = µ+ βhiHard Infoi + βsiSoft Infoi + εi.

Assumes a proportional time to hazard, Ai = exp (x′iβ) A0.

Additional Material

Hazard Models

Hazard test time and covariates effects on prob of event given event notyet occurred.

Soft vs. hard information on decision to admit.Right censoring - append public (HFI, CISDM, HFR, TASS) sources ofreturn data.

A simple time-invariant hazard model...Define due-diligence for fund, Ai, as beginning on first meeting andending on admission or censor date.

OLS specification -

ln Ai = µ+ βhiHard Infoi + βsiSoft Infoi + εi.

Assumes a proportional time to hazard, Ai = exp (x′iβ) A0.

Additional Material

Hazard Models

Hazard test time and covariates effects on prob of event given event notyet occurred.

Soft vs. hard information on decision to admit.Right censoring - append public (HFI, CISDM, HFR, TASS) sources ofreturn data.

A simple time-invariant hazard model...Define due-diligence for fund, Ai, as beginning on first meeting andending on admission or censor date.OLS specification -

ln Ai = µ+ βhiHard Infoi + βsiSoft Infoi + εi.

Assumes a proportional time to hazard, Ai = exp (x′iβ) A0.

Additional Material

Hazard Models

Hazard test time and covariates effects on prob of event given event notyet occurred.

Soft vs. hard information on decision to admit.Right censoring - append public (HFI, CISDM, HFR, TASS) sources ofreturn data.

A simple time-invariant hazard model...Define due-diligence for fund, Ai, as beginning on first meeting andending on admission or censor date.OLS specification -

ln Ai = µ+ βhiHard Infoi + βsiSoft Infoi + εi.

Assumes a proportional time to hazard, Ai = exp (x′iβ) A0.

Additional Material

Time-invariant Hazard

Full-sample Matched-sample

β(t-stat)

β(t-stat)

β(t-stat)

β(t-stat)

β(t-stat)

β(t-stat)

Hard information:Et(R− peers) −0.081∗∗∗ −0.079∗∗∗ −0.041 −0.034

(−3.01) (−2.86) (−1.41) (−1.13)σt(R− peers) 0.244∗∗∗ 0.219∗∗∗ 0.284∗∗∗ 0.242∗∗∗

(7.99) (7.74) (9.92) (8.63)Soft information:Meeting number (All) 0.130∗∗∗ 0.126∗∗∗ 0.182∗∗∗ 0.146∗∗∗

(8.20) (7.54) (7.72) (6.54)Words per Document −0.254∗∗∗ −0.179∗∗∗ −0.177∗∗∗ −0.131∗∗∗

(−11.80) (−7.47) (−5.69) (−4.28)

Observations 747 979 744 556 556 548R2 0.1527 0.1439 0.2372 0.1620 0.1050 0.2254

Multivariate Hazard