financial derivatives: an introduction · pdf file5/24/2010 · what is a financial...

TRANSCRIPT

Financial Derivatives:

An Introduction

Options, Futures, and Other Derivatives, 8th Edition, Copyright © John C. Hull 2012

What is a Financial Derivative?

• A derivative is an instrument whose value depends on,

or is derived from, the value of other assets.

• The underlying assets may be stocks, currencies,

interest rates, commodities, debt instruments,

insurance payouts, etc.

• Derivatives’ types: forwards, futures, options, swaps,

exotics, etc.

• Example: a stock option is a derivative whose value is

dependent on the price of a stock.

2

Why Derivatives Are Important?

• Derivatives are actively traded on many exchanges

throughout the world.

• Many different types of forward contracts, swaps,

options, and others have been entered into the Over-

The-Counter (OTC) markets by financial institutions,

fund managers, and corporate treasurers.

• Derivatives are added to bond issues, used in executive

compensation plans, embedded in capital investment

opportunities, used to transfer risks in mortgages from

the original lenders to investors, and so on.

• Numerous financial transactions have embedded

derivatives.

Why Derivatives Are Important?

• Derivatives play a key role in transferring risks in the

economy from one entity to another.

• The derivatives market is huge; it is much bigger than

the stock market when measured in terms of

underlying assets.

• The value of the assets underlying outstanding

derivatives transactions is several times the world’s

GDP.

4

How Derivatives are Used?

• Hedging: traders face a risk exposure to the price of

an asset and take a position in a derivative to offset

this exposure.

• Speculation: traders use derivatives to bet on the

future direction of the price of an asset (they have

no risk to offset).

• Arbitrage: involves taking offsetting positions in two

or more different markets to lock in a profit.

Hedge funds have become big users of derivatives for

all three purposes.

5

Hedge Funds

• Hedge funds are not subject to the same rules as mutual funds and cannot offer their securities publicly.

• Mutual funds must

• disclose investment policies,

• makes shares redeemable at any time,

• limit use of leverage,

• take no short positions.

• Hedge funds are not subject to these constraints.

6

Where Derivatives Are Traded?

In derivatives exchange markets

Traditionally, derivatives exchanges have used what is

known as the ‘open outcry system.’ This involves traders

physically meeting on the floor of the exchange,

shouting, and using a complicated set of hand signals to

indicate the trades they would like to carryout.

Exchanges are increasingly replacing this system by

electronic trading. This involves traders entering their

desired trades at a keyboard and a computer being used

to match buyers and sellers.

7

Where Derivatives Are Traded?

In the OTC markets

It is a telephone and computer-linked network of dealers.

Trades are usually between two financial institutions or

between a financial institution and one of its clients

(typically a corporate treasurer or a fund manager).

Financial institutions often act as market makers: they

are always prepared to quote both a bid price (a price at

which they are prepared to buy) and an offer price (a

price at which they are prepared to sell).

9

Where Derivatives Are Traded?

OTC markets

• Advantage: the terms of a contract do not have to be

those specified by an exchange. Market participants

are free to negotiate any mutually attractive deals.

• Disadvantage: due to differentiation in OTC

derivatives’ contracts, the risk that a contract will not

be honoured is higher.

10

Size of OTC and Exchange-Traded Markets

11

Source: BIS. Chart shows total principal amounts for OTC market and value of

underlying assets for exchange market

Derivatives and the 2007-8 Financial Crisis

• Derivatives markets have come under a great deal of

criticism because of their role in the late 2000s crisis.

• Derivative products were created from portfolios of

risky mortgages in the U.S. using a procedure known

as securitisation. Many of the products that were

created became worthless when house prices

declined.

• Financial institutions, and investors throughout the

world lost a huge amount of money and the world was

plunged into the worst recession it had experienced for

many generations.

The Lehman Brothers Bankruptcy

• Lehman’s filed for bankruptcy in 2008. This was the

biggest bankruptcy in the US history.

• Lehman was an active participant in the OTC

derivatives markets and got into financial difficulties

because it took high risks and found it was unable

to roll over its short-term funding.

• It had hundreds of thousands of transactions

outstanding with about 8,000 counterparties.

• Unwinding these transactions has been challenging

for both the Lehman liquidators and their

counterparties.

13

Forward contracts

A forward contract is an agreement to buy or sell an

asset at a certain future time for a certain price. It

can be contrasted with a spot contract, which is an

agreement to buy or sell an asset today.

Forward traders are trading for delivery at some

future time; spot traders are trading for immediate

delivery.

The party that agrees to buy the underlying contract

assumes a long position to a forward contract. The

other party agrees a short position.

14

Forward contracts

• The forward price for a contract is the delivery price

that would be applicable to the contract if were

negotiated today.

• The forward price may be different for contracts of

different maturities.

15

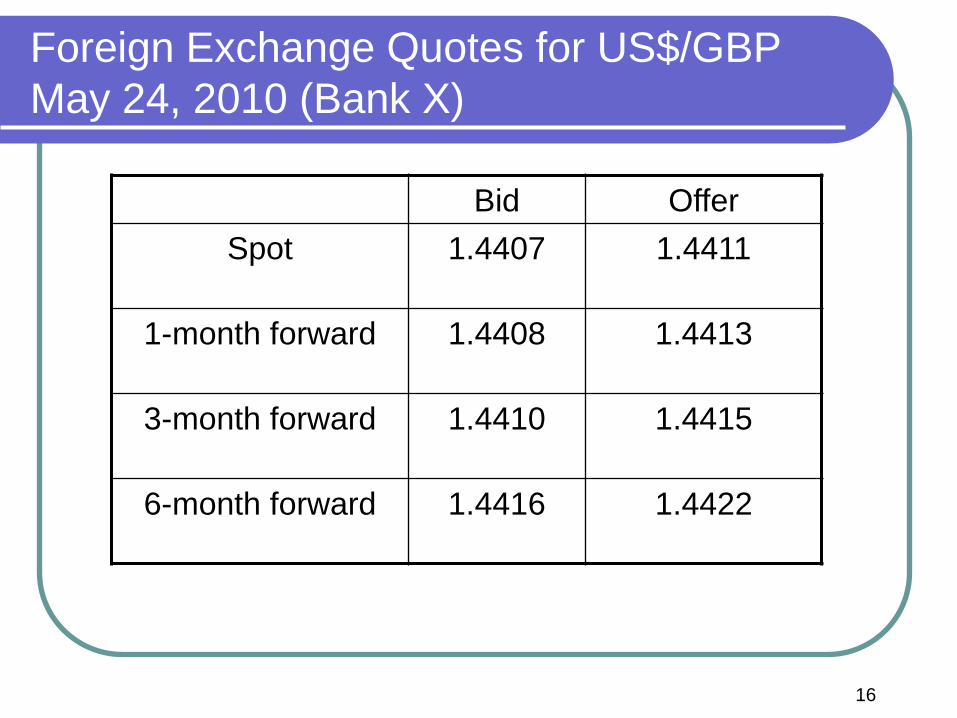

Foreign Exchange Quotes for US$/GBP

May 24, 2010 (Bank X)

16

Bid Offer

Spot 1.4407 1.4411

1-month forward 1.4408 1.4413

3-month forward 1.4410 1.4415

6-month forward 1.4416 1.4422

Foreign exchange forward contracts: Example

• On May 24, 2010 the treasurer of a corporation enters

into a long forward contract to buy £1m in six months

at an exchange rate of 1.4422

• This obligates the corporation to pay $1,442,200 for £1

million on November 24, 2010

• Both sides have made a binding commitment.

17

Profit from a Long Forward Position

18

Profit

Price of Underlying at

Maturity, ST K

Profit from a Short Forward Position

19

Profit

Price of Underlying

at Maturity, ST K

Foreign exchange forward contracts: Exercise

Investor B enters into a short forward contract to sell

£100,000 for US $ at an exchange rate of 1.4000 US $

per £.

How much does B gain or lose if the exchange rate at

the end of the contract is:

(a) 1.3900

(b) 1.4200

20

Futures Contracts

• Like a forward contract, a futures contract is an

agreement between two parties to buy or sell an

asset at a certain time in the future for a certain

price.

• A wide range of commodities and financial assets

form the underlying assets in futures contracts. The

commodities include pork bellies, live cattle, sugar,

wool, lumber, copper, aluminum, gold, and tin. The

financial assets include stock indices, currencies,

and Treasury bonds. Futures prices are regularly

reported in the financial press.

21

Futures Contracts

• Unlike forward contracts, futures contracts are

normally traded on an exchange. Hence, their price

is determined by the laws of demand and supply.

• As the two parties usually do not know each other,

the exchange provides a mechanism that gives the

two parties a guarantee that the contract will be

honoured.

22

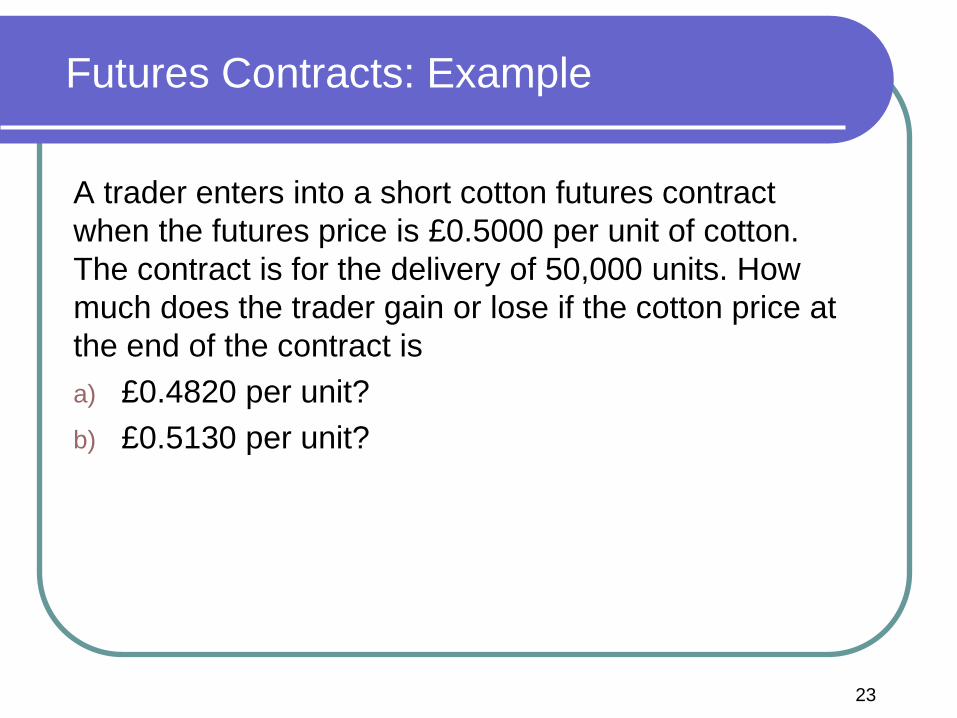

Futures Contracts: Example

A trader enters into a short cotton futures contract

when the futures price is £0.5000 per unit of cotton.

The contract is for the delivery of 50,000 units. How

much does the trader gain or lose if the cotton price at

the end of the contract is

a) £0.4820 per unit?

b) £0.5130 per unit?

23

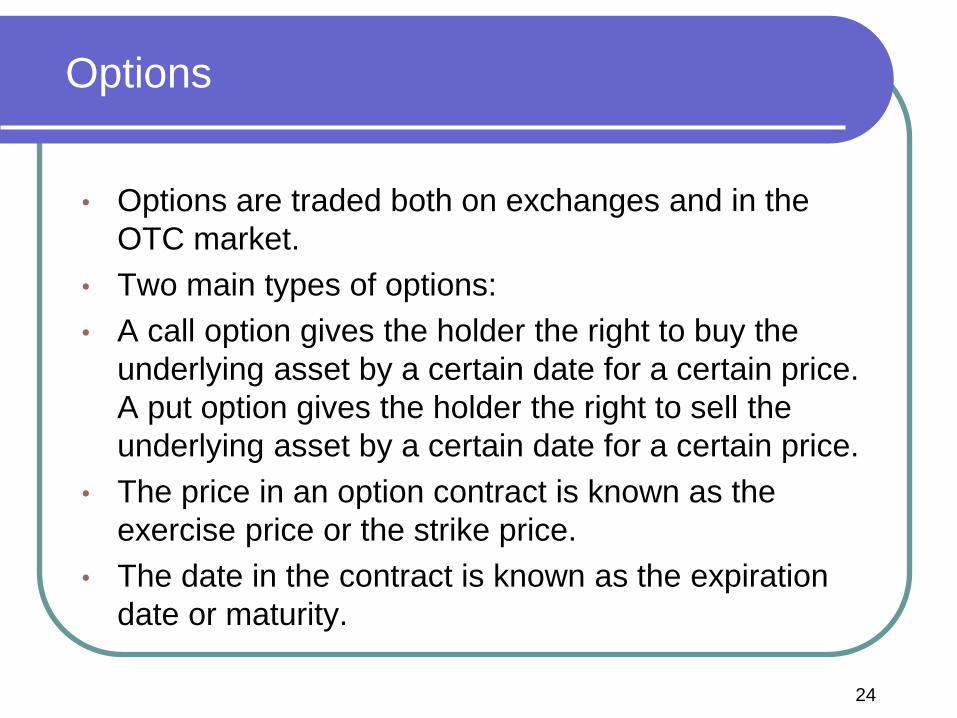

Options

• Options are traded both on exchanges and in the

OTC market.

• Two main types of options:

• A call option gives the holder the right to buy the

underlying asset by a certain date for a certain price.

A put option gives the holder the right to sell the

underlying asset by a certain date for a certain price.

• The price in an option contract is known as the

exercise price or the strike price.

• The date in the contract is known as the expiration

date or maturity.

24

Options

• American options can be exercised at any time up to

the expiration date.

• European options can be exercised only on the

expiration date itself.

• An option gives the holder the right to do something.

The holder does not have to exercise this right. This

is what distinguishes options from forwards and

futures, where the holder is obligated to buy or sell

the underlying asset.

25

Options

• There are four types of participants in options

markets:

1. Buyers of calls

2. Sellers of calls

3. Buyers of puts

4. Sellers of puts

• Buyers are referred to as having long positions;

sellers are referred to as having short positions.

• Selling an option is also known as writing the option.

26

Options vs forward contracts: Example

• What is the difference between entering into a long

forward contract when the forward price is £50 and

taking a long position in a call option with a strike

price of £50?

27

Options vs forward contracts: Example

• In the forward contract, the trader is obligated to buy

the asset for £50. (The trader does not have a

choice.)

• In the call option, the trader has an option to buy the

asset for £50. (The trader does not have to exercise

the option.)

28

Hedging using forward contracts: Example

• Suppose that on May 24, 2010 Company L which is

based in U.S., has to pay £10m on August 24, 2010 for

goods it has purchased from a British supplier.

• Company L expects that the $/£ exchange rate will be

more than 1.4500 on August 2010.

• Company L is a customer of Bank X.

• Company L wants to hedge against foreign exchange

rate risk.

29

Bid Offer

Spot 1.4407 1.4411

1-month forward 1.4408 1.4413

3-month forward 1.4410 1.4415

6-month forward 1.4416 1.4422

Hedging using forward contracts: Example

To hedge its foreign exchange risk:

Company L can write a forward contract with Bank X

and buy £10m in the 3-month forward exchange

market for 1.4415.

This would have the effect of fixing the price to be paid

to the British exporter at $14,415,000 instead of

$14,500,000 on August 24, 2010.

30

Hedging using options: Example

• Consider an investor who owns 1,000 Microsoft

shares in May 2013. The share price is $28/share.

• The investor is concerned about a possible share

price decline in the next 2 months and wants

protection (he expects to decrease to $20/share).

• The investor could buy ten July 2013 put option

contracts on Microsoft with a strike price of $27.50.

This would give the investor the right to sell a total of

1,000 shares for a price of $27.50.

• If the quoted option price is $1, this strategy costs

$1,000 but guarantees that the shares can be sold for

at least $27.50 per share during the life of the option.

31

Hedging using options: Example

• If the market price of Microsoft falls below $27.50, the

options will be exercised, so that $27,500 is realised

for the entire holding. When the cost of the options is

taken into account, the amount realised is $26,500.

• If the market price stays above $27.50, the options

are not exercised and expire worthless. However, in

this case the value of the holding is always above

$27,500 (or above $26,500 when the cost of the

options is taken into account).

32

Value of Microsoft Shares with and

without Hedging

33

20,000

25,000

30,000

35,000

40,000

20 25 30 35 40

Value of Holding ($)

Stock Price ($)

No Hedging

Hedging

Hedging: futures vs. options

Two fundamental differences in the use of forward

contracts and options for hedging:

Forward contracts are designed to neutralise risk

by fixing the price that the hedger will pay or

receive for the underlying asset.

Option contracts offer a way for investors to protect

themselves against adverse price movements in

the future while still allowing them to benefit from

favourable price movements.

Unlike forwards, options involve the payment of an

up-front fee.

34