18929648 financial derivatives

TRANSCRIPT

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 1/52

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 2/52

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 3/52

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 4/52

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 5/52

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 6/52

Excel and VBA as Modeling Tools

Even in the mid- to late 1990s, Excel was not considered a powerful enough tool forserious financial modeling, in part because the PCs available at the time had speed and

memory limitations. With advances in PCs and improvements in Excel itself, the table has

now turned completely: Excel has become the preferred tool for creating all but the largest and

most computationally intensive financial models. The advantages of Excel for financial

modeling are so obvious that it is not necessary to go into them. However, for those who have

not worked with other programs or programming languages for modeling, it is worthwhile to

point out that one of the important advantages of Excel is that with Excel you can create

excellent output with very little work. You should learn to take full advantage of Excel’s

power in this respect. If Excel is so good, then, why bother with VBA? VBA is a

programming language, and if you do not know anything about programming languages, it

will be difficult for you to appreciate the advantages of VBA at this point. Let me touch on

only a few key reasons here, and I will answer the question in greater detail when we discuss

modeling with VBA. Despite its power, Excel has many limitations, and there are many

financial models—some even relatively simple ones—that either cannot be created in Excel or

will be overly complex or cumbersome to create in Excel. What’s more, when you create a

highly complex model in Excel, it can be difficult to understand, debug, and maintain. VBA

generally offers a significant edge in all these respects.

The problem that most people have with VBA is that it is one more thing to learn, and they are

somehow afraid of trying to learn a programming language. The reality is that if you follow

the right method, learning a programming language is not particularly difficult—especially if

you selectively learn what you will really use (as we will do in this book) and not let yourself

get lost in all the other things you can do with VBA but probably never will. The truth is that

you do not need to learn all that much to be able to create very useful and powerful financial

models with VBA. What you will need is a lot of practice, which you will get as you go

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 7/52

through this book. VBA offers you the best of both worlds: you can take advantage of all the

powers of Excel including its ability to easily create excellent outputs, and supplement them

with VBA’s additional tools and flexibility

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 8/52

FINANCIAL DERIVATIVES

A derivative is a financial instrument that derives or gets it value from some real good or stock. It is in its

most basic form simply a contract between two parties to exchange value based on the action of a real good or

service. Typically, the seller receives money in exchange for an agreement to purchase or sell some good or

service at some specified future date.

The largest appeal of derivatives is that they offer some degree of leverage. Leverage is a financial term that

refers to the multiplication that happens when a small amount of money is used to control an item of much

larger value. A mortgage is the most common form of leverage. For a small amount of money and taking on

the obligation of a mortgage, a person gains control of a property of much larger value than the small amount

of money that has exchanged hands.

Derivatives offer the same sort of leverage or multiplication as a mortgage. For a small amount of money, the

investor can control a much larger value of company stock then would be possible without use of derivatives.

This can work both ways, though. If the investor purchasing the derivative is correct, then more money can be

made than if the investment had been made directly into the company itself. However, if the investor is

wrong, the losses are multiplied instead.

Derivatives made the news in 1995 when rogue trader Nick Leeson single-handedly caused the failure of the

Barings bank of England. Nick Leeson was a derivatives trader whose trades did not work out, and due to the

enormous leverage of the trades used, the losses became so large that the bank was bankrupt when the results

of his trades become due. Warren Buffet, a much revered and very successful investor, has stated in one of his

annual reports that he is very much against the use of derivatives and he expects that they will lead to eventual

failure for anyone who uses them. In spite of all this negative press, derivatives have long been a normal part

of business and investing and are likely to be so for many more years.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 9/52

Uses

Hedging

Derivatives allow risk about the value of the underlying asset to be transferred from one party to another. For

example, a wheat farmer and a miller could sign a futures contract to exchange a specified amount of cash for

a specified amount of wheat in the future. Both parties have reduced a future risk: for the wheat farmer, the

uncertainty of the price, and for the miller, the availability of wheat. However, there is still the risk that no

wheat will be available due to causes unspecified by the contract, like the weather, or that one party will

renege on the contract. Although a third party, called a clearing house, insures a futures contract, not all

derivatives are insured against counterparty risk.

From another perspective, the farmer and the miller both reduce a risk and acquire a risk when they sign the

futures contract: The farmer reduces the risk that the price of wheat will fall below the price specified in the

contract and acquires the risk that the price of wheat will rise above the price specified in the contract (thereby

losing additional income that he could have earned). The miller, on the other hand, acquires the risk that the

price of wheat will fall below the price specified in the contract (thereby paying more in the future than heotherwise would) and reduces the risk that the price of wheat will rise above the price specified in the

contract. In this sense, one party is the insurer (risk taker) for one type of risk, and the counterparty is the

insurer (risk taker) for another type of risk.

Hedging also occurs when an individual or institution buys an asset (like a commodity, a bond that has

coupon payments, a stock that pays dividends, and so on) and sells it using a futures contract. The individual

or institution has access to the asset for a specified amount of time, and then can sell it in the future at a

specified price according to the futures contract. Of course, this allows the individual or institution the benefit

of holding the asset while reducing the risk that the future selling price will deviate unexpectedly from the

market's current assessment of the future value of the asset.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 10/52

Speculation and arbitrage

Derivatives can be used to acquire risk, rather than to insure or hedge against risk. Thus, some individuals and

institutions will enter into a derivative contract to speculate on the value of the underlying asset, betting that

the party seeking insurance will be wrong about the future value of the underlying asset. Speculators will want

to be able to buy an asset in the future at a low price according to a derivative contract when the future market

price is high, or to sell an asset in the future at a high price according to a derivative contract when the future

market price is low.

Individuals and institutions may also look for arbitrage opportunities, as when the current buying price of an

asset falls below the price specified in a futures contract to sell the asset.

Speculative trading in derivatives gained a great deal of notoriety in 1995 when Nick Leeson, a trader at

Barings Bank , made poor and unauthorized investments in futures contracts. Through a combination of poor

judgment, lack of oversight by the bank's management and by regulators, and unfortunate events like the

Kobe earthquake, Leeson incurred a $1.3 billion loss that bankrupted the centuries-old institution.[1]

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 11/52

Types of derivatives

OTC and exchange-traded

Broadly speaking there are two distinct groups of derivative contracts, which are distinguished by the way

they are traded in market:

• Over-the-counter (OTC) derivatives are contracts that are traded (and privately negotiated) directly

between two parties, without going through an exchange or other intermediary. Products such as

swaps, forward rate agreements, and exotic options are almost always traded in this way. The OTC

derivative market is the largest market for derivatives, and is largely unregulated with respect to

disclosure of information between the parties, since the OTC market is made up of banks and other

highly sophisticated parties, such as hedge funds. Reporting of OTC amounts are difficult because

trades can occur in private, without activity being visible on any exchange. According to the Bank for

International Settlements, the total outstanding notional amount is $684 trillion (as of June 2008) [2]. Of

this total notional amount, 67% are interest rate contracts, 8% are credit default swaps (CDS), 9% are

foreign exchange contracts, 2% are commodity contracts, 1% are equity contracts, and 12% are other.

Because OTC derivatives are not traded on an exchange, there is no central counterparty. Therefore,

they are subject to counterparty risk, like an ordinary contract, since each counterparty relies on the

other to perform.

• Exchange-traded derivatives (ETD) are those derivatives products that are traded via specialized

derivatives exchanges or other exchanges. A derivatives exchange acts as an intermediary to all related

transactions, and takes Initial margin from both sides of the trade to act as a guarantee. The world's

largest[3] derivatives exchanges (by number of transactions) are the Korea Exchange (which lists

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 12/52

KOSPI Index Futures & Options), Eurex (which lists a wide range of European products such as

interest rate & index products), and CME Group (made up of the 2007 merger of the Chicago

Mercantile Exchange and the Chicago Board of Trade and the 2008 acquisition of the New York

Mercantile Exchange). According to BIS, the combined turnover in the world's derivatives exchanges

totalled USD 344 trillion during Q4 2005. Some types of derivative instruments also may trade on

traditional exchanges. For instance, hybrid instruments such as convertible bonds and/or convertible preferred may be listed on stock or bond exchanges. Also, warrants (or "rights") may be listed on

equity exchanges. Performance Rights, Cash xPRTs and various other instruments that essentially

consist of a complex set of options bundled into a simple package are routinely listed on equity

exchanges. Like other derivatives, these publicly traded derivatives provide investors access to

risk/reward and volatility characteristics that, while related to an underlying commodity, nonetheless

are distinctive.

Common derivative contract types

There are three major classes of derivatives:

1. Futures/Forwards are contracts to buy or sell an asset on or before a future date at a price specified

today. A futures contract differs from a forward contract in that the futures contract is a standardized

contract written by a clearing house that operates an exchange where the contract can be bought and

sold, while a forward contract is a non-standardized contract written by the parties themselves.

2. Options are contracts that give the owner the right, but not the obligation, to buy (in the case of a call

option) or sell (in the case of a put option) an asset. The price at which the sale takes place is known as

the strike price, and is specified at the time the parties enter into the option. The option contract also

specifies a maturity date. In the case of a European option, the owner has the right to require the sale

to take place on (but not before) the maturity date; in the case of an American option, the owner can

require the sale to take place at any time up to the maturity date. If the owner of the contract exercises

this right, the counterparty has the obligation to carry out the transaction.

3. Swaps are contracts to exchange cash (flows) on or before a specified future date based on the

underlying value of currencies/exchange rates, bonds/interest rates, commodities, stocks or other

assets.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 13/52

More complex derivatives can be created by combining the elements of these basic types. For example, the

holder of a swaption has the right, but not the obligation, to enter into a swap on or before a specified future

date.

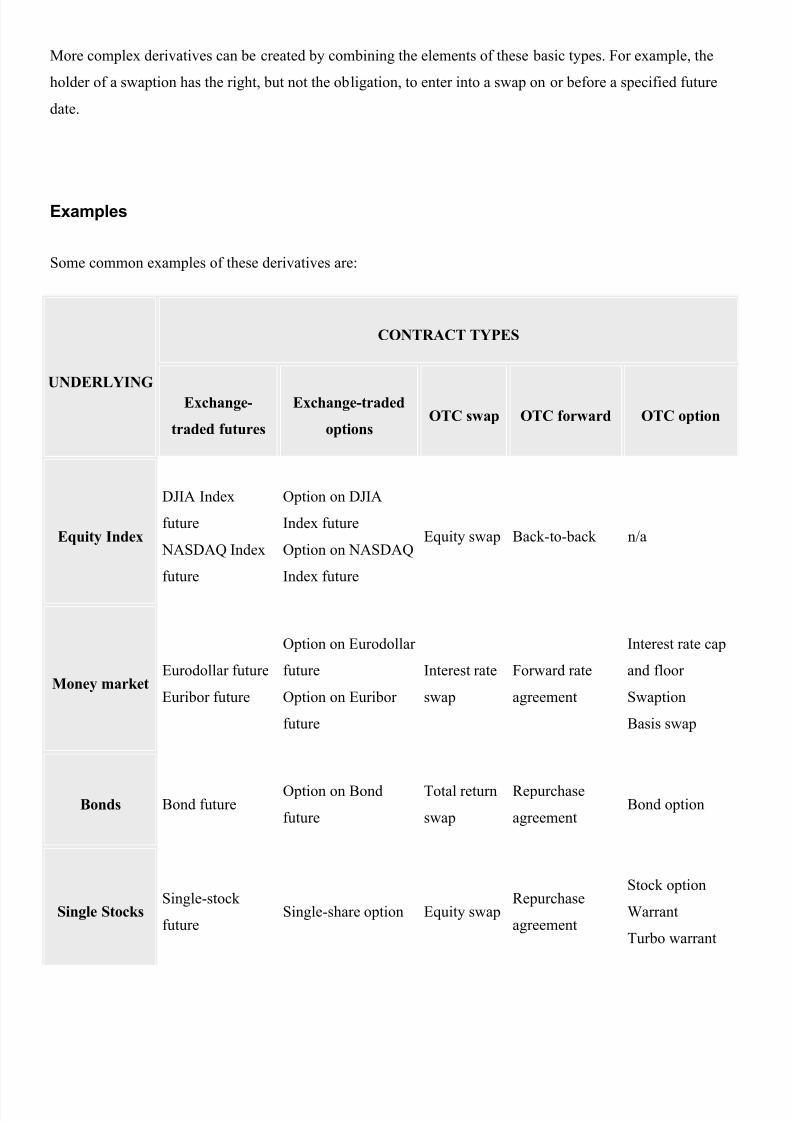

Examples

Some common examples of these derivatives are:

UNDERLYING

CONTRACT TYPES

Exchange-

traded futures

Exchange-traded

optionsOTC swap OTC forward OTC option

Equity Index

DJIA Index

future

NASDAQ Index

future

Option on DJIA

Index future

Option on NASDAQ

Index future

Equity swap Back-to-back n/a

Money marketEurodollar future

Euribor future

Option on Eurodollar

future

Option on Euribor

future

Interest rate

swap

Forward rate

agreement

Interest rate cap

and floor

Swaption

Basis swap

Bonds Bond futureOption on Bond

future

Total return

swap

Repurchase

agreementBond option

Single StocksSingle-stock

futureSingle-share option Equity swap

Repurchase

agreement

Stock option

Warrant

Turbo warrant

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 14/52

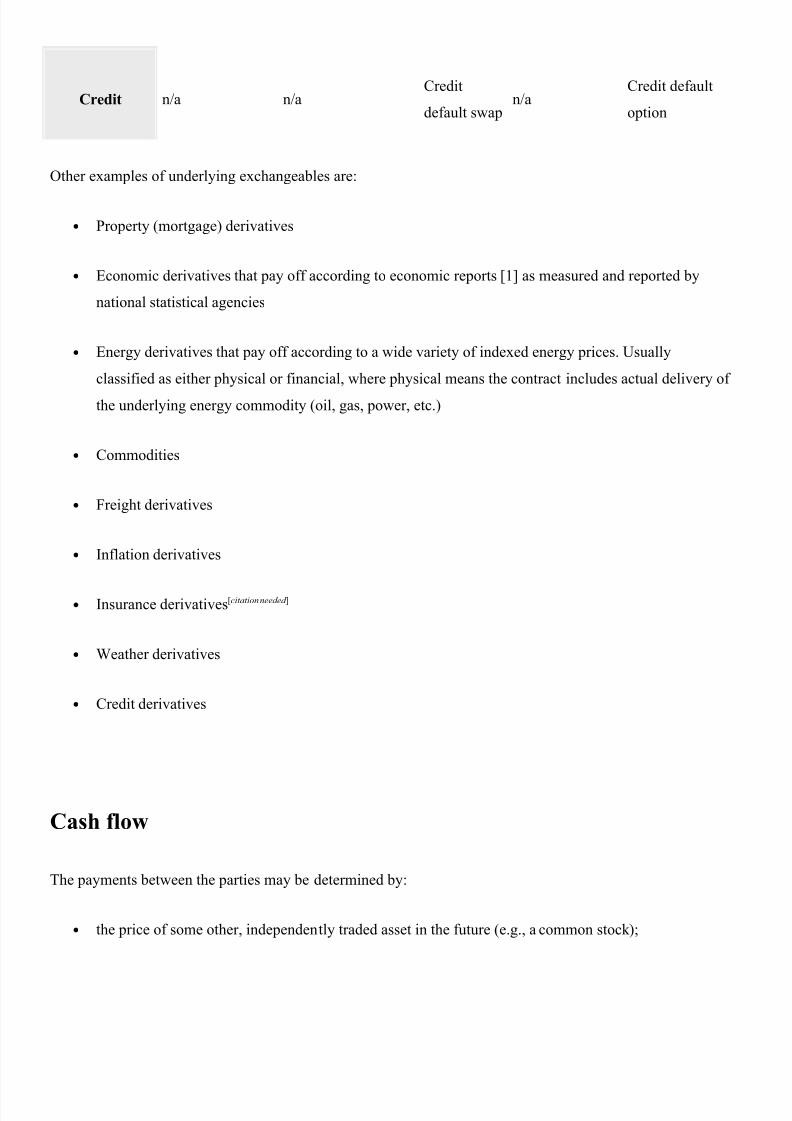

Credit n/a n/aCredit

default swapn/a

Credit default

option

Other examples of underlying exchangeables are:

• Property (mortgage) derivatives

• Economic derivatives that pay off according to economic reports [1] as measured and reported by

national statistical agencies

• Energy derivatives that pay off according to a wide variety of indexed energy prices. Usually

classified as either physical or financial, where physical means the contract includes actual delivery of

the underlying energy commodity (oil, gas, power, etc.)

• Commodities

• Freight derivatives

• Inflation derivatives

• Insurance derivatives[citation needed ]

• Weather derivatives

• Credit derivatives

Cash flow

The payments between the parties may be determined by:

• the price of some other, independently traded asset in the future (e.g., a common stock );

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 15/52

• the level of an independently determined index (e.g., a stock market index or heating-degree-days);

• the occurrence of some well-specified event (e.g., a company defaulting);

• an interest rate;

• an exchange rate;

• or some other factor.

Some derivatives are the right to buy or sell the underlying security or commodity at some point in the future

for a predetermined price. If the price of the underlying security or commodity moves into the right direction,

the owner of the derivative makes money; otherwise, they lose money or the derivative becomes worthless.

Depending on the terms of the contract, the potential gain or loss on a derivative can be much higher than if

they had traded the underlying security or commodity directly.

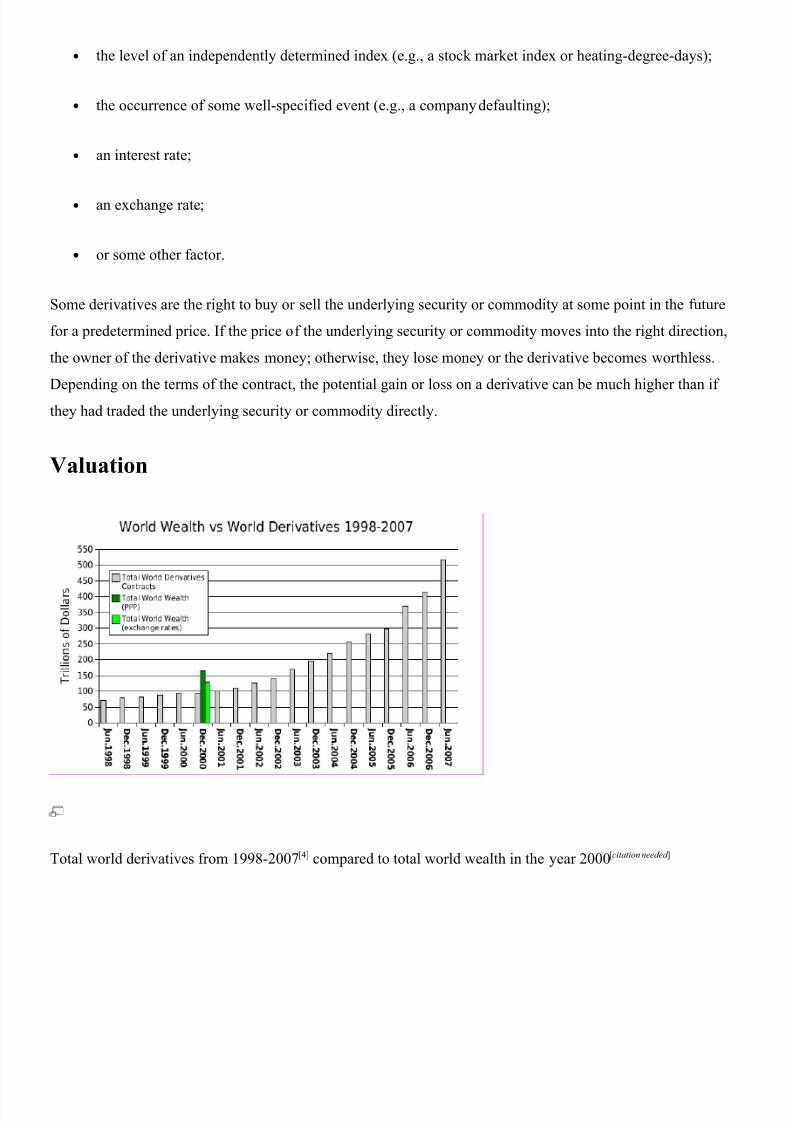

Valuation

Total world derivatives from 1998-2007[4] compared to total world wealth in the year 2000[citation needed ]

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 16/52

Market and arbitrage-free prices

Two common measures of value are:

• Market price, i.e. the price at which traders are willing to buy or sell the contract

• Arbitrage-free price, meaning that no risk-free profits can be made by trading in these contracts; see

rational pricing

Determining the market price

For exchange-traded derivatives, market price is usually transparent (often published in real time by theexchange, based on all the current bids and offers placed on that particular contract at any one time).

Complications can arise with OTC or floor-traded contracts though, as trading is handled manually, making it

difficult to automatically broadcast prices. In particular with OTC contracts, there is no central exchange to

collate and disseminate prices.

Determining the arbitrage-free price

The arbitrage-free price for a derivatives contract is complex, and there are many different variables to

consider. Arbitrage-free pricing is a central topic of financial mathematics. The stochastic process of the price

of the underlying asset is often crucial. A key equation for the theoretical valuation of options is the Black–

Scholes formula, which is based on the assumption that the cash flows from a European stock option can be

replicated by a continuous buying and selling strategy using only the stock. A simplified version of this

valuation technique is the binomial options model.

Criticisms

Derivatives are often subject to the following criticisms:

Possible large losses

See also: List of trading losses

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 17/52

The use of derivatives can result in large losses due to the use of leverage, or borrowing. Derivatives allow

investors to earn large returns from small movements in the underlying asset's price. However, investors could

lose large amounts if the price of the underlying moves against them significantly. There have been several

instances of massive losses in derivative markets, such as:

• The need to recapitalize insurer American International Group (AIG) with $85 billion of debt provided

by the US federal government [5]. An AIG subsidiary had lost more than $18 billion over the preceding

three quarters on Credit Default Swaps (CDS) it had written.[6] It was reported that the recapitalization

was necessary because further losses were foreseeable over the next few quarters.

• The loss of $7.2 Billion by Société Générale in January 2008 through mis-use of futures contracts.

• The loss of US$6.4 billion in the failed fund Amaranth Advisors, which was long natural gas in

September 2006 when the price plummeted.

• The loss of US$4.6 billion in the failed fund Long-Term Capital Management in 1998.

• The bankruptcy of Orange County, CA in 1994, the largest municipal bankruptcy in U.S. history. On

December 6, 1994, Orange County declared Chapter 9 bankruptcy, from which it emerged in June

1995. The county lost about $1.6 billion through derivatives trading. Orange County was neither

bankrupt nor insolvent at the time; however, because of the strategy the county employed it was

unable to generate the cash flows needed to maintain services. Orange County is a good example of

what happens when derivatives are used incorrectly and positions liquidated in an unplanned manner;

had they not liquidated they would not have lost any money as their positions rebounded.[citation needed ]

Potentially problematic use of interest-rate derivatives by US municipalities has continued in recent

years. See, for example:[7]

• The Nick Leeson affair in 1994

Counter-party risk

Derivatives (especially swaps) expose investors to counter-party risk .

For example, suppose a person wanting a fixed interest rate loan for his business, but finding that banks only

offer variable rates, swaps payments with another business who wants a variable rate, synthetically creating a

fixed rate for the person. However if the second business goes bankrupt, it can't pay its variable rate and so the

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 18/52

first business will lose its fixed rate and will be paying a variable rate again. If interest rates have increased, it

is possible that the first business may be adversely affected, because it may not be prepared to pay the higher

variable rate.

Different types of derivatives have different levels of risk for this effect. For example, standardized stock

options by law require the party at risk to have a certain amount deposited with the exchange, showing that

they can pay for any losses; Banks who help businesses swap variable for fixed rates on loans may do credit

checks on both parties. However in private agreements between two companies, for example, there may not

be benchmarks for performing due diligence and risk analysis.

Unsuitably high risk for small/inexperienced investors

Derivatives pose unsuitably high amounts of risk for small or inexperienced investors. Because derivatives

offer the possibility of large rewards, they offer an attraction even to individual investors. However,

speculation in derivatives often assumes a great deal of risk, requiring commensurate experience and market

knowledge, especially for the small investor, a reason why some financial planners advise against the use of

these instruments. Derivatives are complex instruments devised as a form of insurance, to transfer risk among

parties based on their willingness to assume additional risk, or hedge against it.

Large notional value

• Derivatives typically have a large notional value. As such, there is the danger that their use could

result in losses that the investor would be unable to compensate for. The possibility that this could lead

to a chain reaction ensuing in an economic crisis, has been pointed out by famed investor Warren

Buffett in Berkshire Hathaway's annual report. Buffett called them 'financial weapons of mass

destruction.' The problem with derivatives is that they control an increasingly larger notional amount

of assets and this may lead to distortions in the real capital and equities markets. Investors begin to

look at the derivatives markets to make a decision to buy or sell securities and so what was originally

meant to be a market to transfer risk now becomes a leading indicator.

Leverage of an economy's debt

Derivatives massively leverage the debt in an economy, making it ever more difficult for the underlying real

economy to service its debt obligations and curtailing real economic activity, which can cause a recession or

even depression.[8] In the view of Marriner S. Eccles, U.S. Federal Reserve Chairman from November, 1934

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 19/52

to February, 1948, too high a level of debt was one of the primary causes of the 1920s-30s Great Depression.

(See Berkshire Hathaway Annual Report for 2002)

Benefits

Nevertheless, the use of derivatives also has its benefits:

• Derivatives facilitate the buying and selling of risk , and thus have a positive impact on the economic

system. Although someone loses money while someone else gains money with a derivative, under

normal circumstances, trading in derivatives should not adversely affect the economic system because

it is not zero sum in utility.

• Former Federal Reserve Board chairman Alan Greenspan commented in 2003 that he believed that the

use of derivatives has softened the impact of the economic downturn at the beginning of the 21st

century.

Definitions

• Bilateral netting: A legally enforceable arrangement between a bank and a counter-party that creates a

single legal obligation covering all included individual contracts. This means that a bank’s obligation,

in the event of the default or insolvency of one of the parties, would be the net sum of all positive and

negative fair values of contracts included in the bilateral netting arrangement.

• Credit derivative: A contract that transfers credit risk from a protection buyer to a credit protection

seller. Credit derivative products can take many forms, such as credit default swaps, credit linked

notes and total return swaps.

• Derivative: A financial contract whose value is derived from the performance of assets, interest rates,

currency exchange rates, or indexes. Derivative transactions include a wide assortment of financial

contracts including structured debt obligations and deposits, swaps, futures, options, caps, floors,

collars, forwards and various combinations thereof.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 20/52

• Exchange-traded derivative contracts: Standardized derivative contracts (e.g. futures contracts and

options) that are transacted on an organized futures exchange.

• Gross negative fair value: The sum of the fair values of contracts where the bank owes money to its

counter-parties, without taking into account netting. This represents the maximum losses the bank’s

counter-parties would incur if the bank defaults and there is no netting of contracts, and no bank

collateral was held by the counter-parties.

• Gross positive fair value: The sum total of the fair values of contracts where the bank is owed money

by its counter-parties, without taking into account netting. This represents the maximum losses a bank

could incur if all its counter-parties default and there is no netting of contracts, and the bank holds no

counter-party collateral.

• High-risk mortgage securities: Securities where the price or expected average life is highly sensitive to

interest rate changes, as determined by the FFIEC policy statement on high-risk mortgage securities.

• Notional amount: The nominal or face amount that is used to calculate payments made on swaps and

other risk management products. This amount generally does not change hands and is thus referred to

as notional.

• Over-the-counter (OTC) derivative contracts : Privately negotiated derivative contracts that are

transacted off organized futures exchanges.

• Structured notes: Non-mortgage-backed debt securities, whose cash flow characteristics depend on

one or more indices and/or have embedded forwards or options.

• Total risk-based capital: The sum of tier 1 plus tier 2 capital. Tier 1 capital consists of common

shareholders equity, perpetual preferred shareholders equity with non-cumulative dividends, retained

earnings, and minority interests in the equity accounts of consolidated subsidiaries. Tier 2 capital

consists of subordinated debt, intermediate-term preferred stock , cumulative and long-term preferred

stock, and a portion of a bank’s allowance for loan and lease losses.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 21/52

Financial Derivatives Market and its Development in India

Financial markets are, by nature, extremely volatile and hence the risk factor is an

important concern for financial agents. To reduce this risk, the concept of derivatives

comes into the picture. Derivatives are products whose values are derived from one or more

basic variables called bases. These bases can be underlying assets (for example forex,

equity, etc), bases or reference rates. For example, wheat farmers may wish to sell their

harvest at a future date to eliminate the risk of a change in prices by that date. The

transaction in this case would be the derivative, while the spot price of wheat would be the

underlying asset.

Development of exchange-traded derivatives

Derivatives have probably been around for as long as people have been trading with one

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 22/52

another. Forward contracting dates back at least to the 12th century, and may well have

been around before then. Merchants entered into contracts with one another for future

delivery of specified amount of commodities at specified price. A primary motivation for

pre-arranging a buyer or seller for a stock of commodities in early forward contracts was to

lessen the possibility that large swings would inhibit marketing the commodity after a

harvest.

The need for a derivatives market

The derivatives market performs a number of economic functions:

1. They help in transferring risks from risk averse people to risk oriented people

2. They help in the discovery of future as well as current prices

3. They catalyze entrepreneurial activity

4. They increase the volume traded in markets because of participation of risk averse

people in greater numbers

5. They increase savings and investment in the long run

The participants in a derivatives market

• Hedgers use futures or options markets to reduce or eliminate the risk associated

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 23/52

with price of an asset.

• Speculators use futures and options contracts to get extra leverage in betting on

future movements in the price of an asset. They can increase both the potential

gains and potential losses by usage of derivatives in a speculative venture.

• Arbitrageurs are in business to take advantage of a discrepancy between prices in

two different markets. If, for example, they see the futures price of an asset getting

out of line with the cash price, they will take offsetting positions in the two markets

to lock in a profit.

Types of Derivatives

Forwards: A forward contract is a customized contract between two entities, where

settlement takes place on a specific date in the future at today’s pre-agreed price.

Futures: A futures contract is an agreement between two parties to buy or sell an asset at a

certain time in the future at a certain price. Futures contracts are special types of forward

contracts in the sense that the former are standardized exchange-traded contracts

Options: Options are of two types - calls and puts. Calls give the buyer the right but not the

obligation to buy a given quantity of the underlying asset, at a given price on or before a

given future date. Puts give the buyer the right, but not the obligation to sell a given

quantity of the underlying asset at a given price on or before a given date.

Warrants: Options generally have lives of upto one year, the majority of options traded on

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 24/52

options exchanges having a maximum maturity of nine months. Longer-dated options are

called warrants and are generally traded over-the-counter.

LEAPS: The acronym LEAPS means Long-Term Equity Anticipation Securities. These are

options having a maturity of upto three years.

Baskets: Basket options are options on portfolios of underlying assets. The underlying

asset is usually a moving average or a basket of assets. Equity index options are a form of

basket options.

Swaps: Swaps are private agreements between two parties to exchange cash flows in the

future according to a prearranged formula. They can be regarded as portfolios of forward

contracts. The two commonly used swaps are :

• Interest rate swaps: These entail swapping only the interest related cash flows

between the parties in the same currency.

• Currency swaps: These entail swapping both principal and interest between the

parties, with the cashflows in one direction being in a different currency than those

in the opposite direction.

Swaptions: Swaptions are options to buy or sell a swap that will become operative at the

expiry of the options. Thus a swaption is an option on a forward swap. Rather than have

calls and puts, the swaptions market has receiver swaptions and payer swaptions. A

receiver swaption is an option to receive fixed and pay floating. A payer swaption is an

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 25/52

option to pay fixed and receive floating.

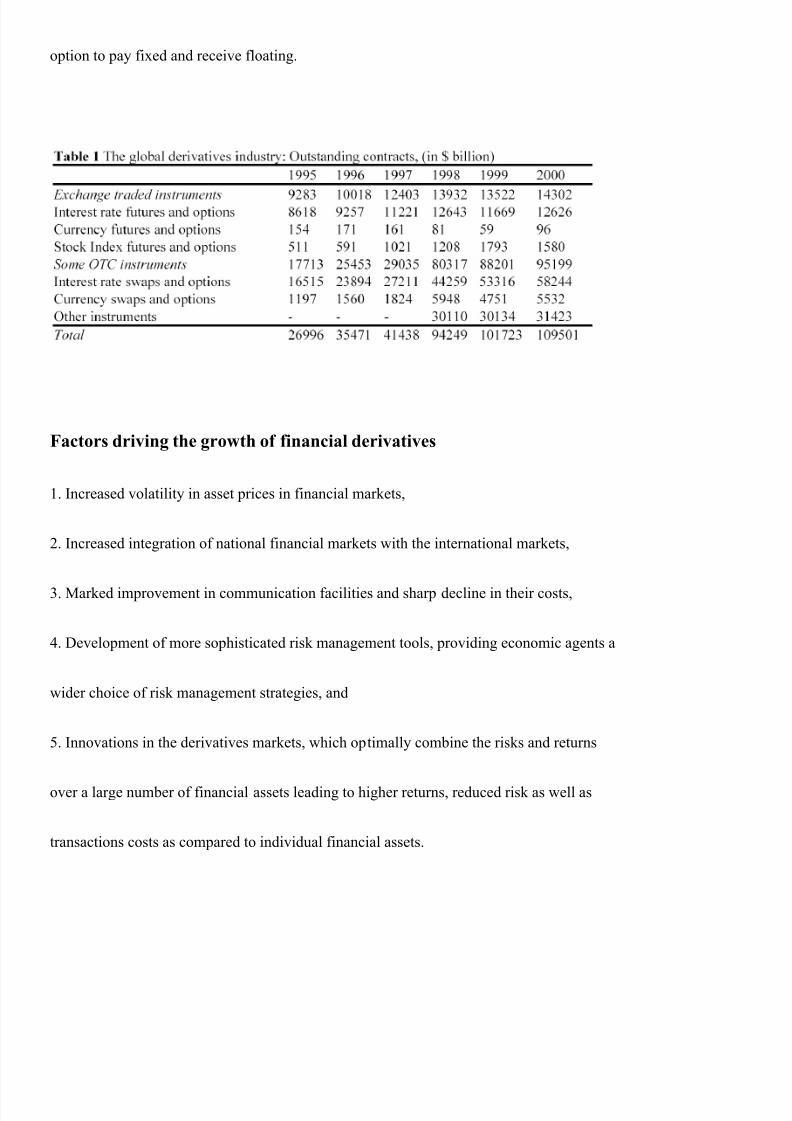

Factors driving the growth of financial derivatives

1. Increased volatility in asset prices in financial markets,

2. Increased integration of national financial markets with the international markets,

3. Marked improvement in communication facilities and sharp decline in their costs,

4. Development of more sophisticated risk management tools, providing economic agents a

wider choice of risk management strategies, and

5. Innovations in the derivatives markets, which optimally combine the risks and returns

over a large number of financial assets leading to higher returns, reduced risk as well as

transactions costs as compared to individual financial assets.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 26/52

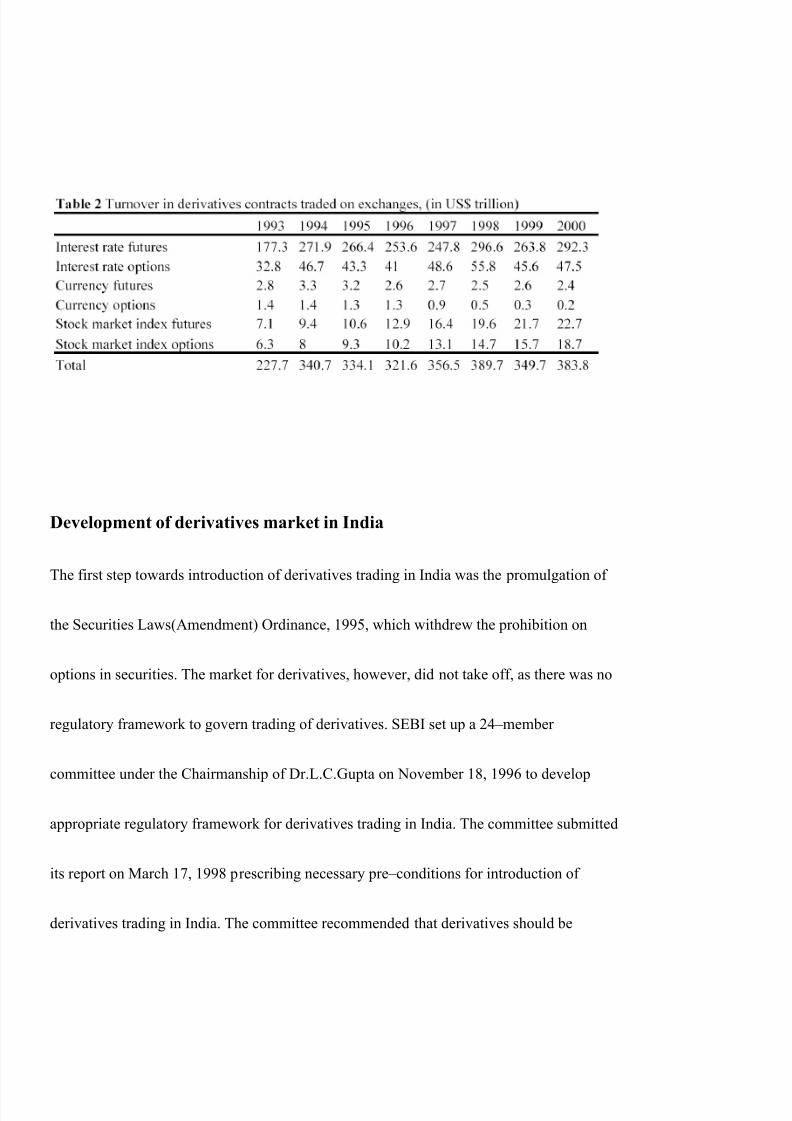

Development of derivatives market in India

The first step towards introduction of derivatives trading in India was the promulgation of

the Securities Laws(Amendment) Ordinance, 1995, which withdrew the prohibition on

options in securities. The market for derivatives, however, did not take off, as there was no

regulatory framework to govern trading of derivatives. SEBI set up a 24–member

committee under the Chairmanship of Dr.L.C.Gupta on November 18, 1996 to develop

appropriate regulatory framework for derivatives trading in India. The committee submitted

its report on March 17, 1998 prescribing necessary pre–conditions for introduction of

derivatives trading in India. The committee recommended that derivatives should be

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 27/52

declared as ‘securities’ so that regulatory framework applicable to trading of ‘securities’

could also govern trading of securities. SEBI also set up a group in June 1998 under the

Chairmanship of Prof.J.R.Varma, to recommend measures for risk containment in

derivatives market in India. The report, which was submitted in October 1998, worked out

the operational details of margining system, methodology for charging initial margins,

broker net worth, deposit requirement and real–time monitoring requirements.

The Securities Contract Regulation Act (SCRA) was amended in December 1999 to

include derivatives within the ambit of ‘securities’ and the regulatory framework was

developed for governing derivatives trading. The act also made it clear that derivatives

shall be legal and valid only if such contracts are traded on a recognized stock exchange,

thus precluding OTC derivatives. The government also rescinded in March 2000, the three–

decade old notification, which prohibited forward trading in securities.

Derivatives trading commenced in India in June 2000 after SEBI granted the final

approval to this effect in May 2001. SEBI permitted the derivative segments of two stock

exchanges, NSE and BSE, and their clearing house/corporation to commence trading and

settlement in approved derivatives contracts. To begin with, SEBI approved trading in

index futures contracts based on S&P CNX Nifty and BSE–30(Sensex) index. This was

followed by approval for trading in options based on these two indexes and options on

individual securities.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 28/52

The trading in BSE Sensex options commenced on June 4, 2001 and the trading in

options on individual securities commenced in July 2001. Futures contracts on individual

stocks were launched in November 2001. The derivatives trading on NSE commenced with

S&P CNX Nifty Index futures on June 12, 2000. The trading in index options commenced

on June 4, 2001 and trading in options on individual securities commenced on July 2, 2001.

Single stock futures were launched on November 9, 2001. The index futures and options

contract on NSE are based on S&P CNX

Trading and settlement in derivative contracts is done in accordance with the rules,

byelaws, and regulations of the respective exchanges and their clearing house/corporation

duly approved by SEBI and notified in the official gazette. Foreign Institutional Investors

(FIIs) are permitted to trade in all Exchange traded derivative products.

The following are some observations based on the trading statistics provided in the NSE

report on the futures and options (F&O):

• Single-stock futures continue to account for a sizable proportion of the F&O

segment. It constituted 70 per cent of the total turnover during June 2002. A

primary reason attributed to this phenomenon is that traders are comfortable with

single-stock futures than equity options, as the former closely resembles the

erstwhile badla system.

• On relative terms, volumes in the index options segment continues to remain poor.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 29/52

This may be due to the low volatility of the spot index. Typically, options are

considered more valuable when the volatility of the underlying (in this case, the

index) is high. A related issue is that brokers do not earn high commissions by

recommending index options to their clients, because low volatility leads to higher

waiting time for round-trips.

• Put volumes in the index options and equity options segment have increased since

January 2002. The call-put volumes in index options have decreased from 2.86 in

January 2002 to 1.32 in June. The fall in call-put volumes ratio suggests that the

traders are increasingly becoming pessimistic on the market.

• Farther month futures contracts are still not actively traded. Trading in equity

options on most stocks for even the next month was non-existent.

• Daily option price variations suggest that traders use the F&O segment as a less

risky alternative (read substitute) to generate profits from the stock price

movements. The fact that the option premiums tail intra-day stock prices is

evidence to this. Calls on Satyam fall, while puts rise when Satyam falls intra-day.

If calls and puts are not looked as just substitutes for spot trading, the intra-day

stock price variations should not have a one-to-one impact on the option premiums.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 30/52

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 31/52

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 32/52

Commodity Derivatives

Futures contracts in pepper, turmeric, gur (jaggery), hessian (jute fabric), jute sacking,

castor seed, potato, coffee, cotton, and soybean and its derivatives are traded in 18

commodity exchanges located in various parts of the country. Futures trading in other

edible oils, oilseeds and oil cakes have been permitted. Trading in futures in the new

commodities, especially in edible oils, is expected to commence in the near future. The

sugar industry is exploring the merits of trading sugar futures contracts.

The policy initiatives and the modernisation programme include extensive training,

structuring a reliable clearinghouse, establishment of a system of warehouse receipts, and

the thrust towards the establishment of a national commodity exchange. The Government

of India has constituted a committee to explore and evaluate issues pertinent to the

establishment and funding of the proposed national commodity exchange for the

nationwide trading of commodity futures contracts, and the other institutions and

institutional processes such as warehousing and clearinghouses.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 33/52

With commodity futures, delivery is best effected using warehouse receipts (which are like

dematerialised securities). Warehousing functions have enabled viable exchanges to

augment their strengths in contract design and trading. The viability of the national

commodity exchange is predicated on the reliability of the warehousing functions. The

programme for establishing a system of warehouse receipts is in progress. The Coffee

Futures Exchange India (COFEI) has operated a system of warehouse receipts since 1998.

Exchange-traded vs. OTC (Over The Counter) derivatives markets

The OTC derivatives markets have witnessed rather sharp growth over the last few years,

which has accompanied the modernization of commercial and investment banking and

globalisation of financial activities. The recent developments in information technology

have contributed to a great extent to these developments. While both exchange-traded and

OTC derivative contracts offer many benefits, the former have rigid structures compared to

the latter. It has been widely discussed that the highly leveraged institutions and their OTC

derivative positions were the main cause of turbulence in financial markets in 1998. These

episodes of turbulence revealed the risks posed to market stability originating in features of

OTC derivative instruments and markets.

The OTC derivatives markets have the following features compared to exchange-traded

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 34/52

derivatives:

1. The management of counter-party (credit) risk is decentralized and located within

individual institutions,

2. There are no formal centralized limits on individual positions, leverage, or margining,

3. There are no formal rules for risk and burden-sharing,

4. There are no formal rules or mechanisms for ensuring market stability and integrity, and

for safeguarding

the collective interests of market participants, and

5. The OTC contracts are generally not regulated by a regulatory authority and the

exchange’s self-regulatory organization, although they are affected indirectly by national

legal systems, banking supervision and market surveillance.

Accounting of Derivatives :

The Institute of Chartered Accountants of India (ICAI) has issued guidance notes on

accounting of index futures contracts from the view point of parties who enter into such

futures contracts as buyers or sellers. For other parties involved in the trading process, like

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 35/52

brokers, trading members, clearing members and clearing corporations, a trade in equity

index futures is similar to a trade in, say shares, and does not pose any peculiar accounting

problems

Taxation

The income-tax Act does not have any specific provision regarding taxability from

derivatives.The only provisions which have an indirect bearing on derivative transactions

are sections 73(1) and 43(5). Section 73(1) provides that any loss, computed in respect of a

speculative business carried on by the assessee, shall not be set off except against profits

and gains, if any, of speculative business. In the absence of a specific provision, it is

apprehended that the derivatives contracts, particularly the index futures which are

essentially cash-settled, may be construed as speculative transactions and therefore the

losses, if any, will not be eligible for set off against other income of the assessee and will

be carried forward and set off against speculative income only up to a maximum of eight

years .As a result an investor’s losses or profits out of derivatives even though they are of

hedging nature in real sense, are treated as speculative and can be set off only against

speculative income.

10 Myths About Financial Derivatives

Executive Summary

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 36/52

In our fast-changing financial services industry, coercive regulations intended to restrict banks' activities will

be unable to keep up with financial innovation. As the lines of demarcation between various types of financial

service providers continues to blur, the bureaucratic leviathan responsible for reforming banking regulation

must face the fact that fears about derivatives have proved unfounded. New regulations are unnecessary.

Indeed, access to risk-management instruments should not be feared but, with caution, embraced to help firms

manage the vicissitudes of the market.

In this paper 10 common misconceptions about financial derivatives are explored. Believing just one or two of

the myths could lead one to advocate tighter legislation and regulatory measures designed to restrict derivative

activities and market participants. A careful review of the risks and rewards derivatives offer, however,

suggests that regulatory and legislative restrictions are not the answer. To blame organizational failures solely

on derivatives is to miss the point. A better answer lies in greater reliance on market forces to control

derivative-related risk taking.

Financial derivatives have changed the face of finance by creating new ways to understand, measure, and

manage risks. Ultimately, financial derivatives should be considered part of any firm's risk-management

strategy to ensure that value-enhancing investment opportunities are pursued. The freedom to manage risk

effectively must not be taken away.

Introduction

Remember the bankruptcy of Orange County, California, and the Barings Bank due to poor investments in

financial derivatives? At that time many policymakers feared more collapsed banks, counties, and countries.

Those fears proved unfounded; prudent use, not government regulation, of derivatives headed off further

problems. Now, however, the Financial Accounting Standards Board, the Federal Reserve, and the Securities

and Exchange Commission are debating the merits of new rules for derivatives. But before adopting

regulations, policymakers need to separate myths about those financial instruments from reality.

The tremendous growth of the financial derivatives market and reports of major losses associated with

derivative products have resulted in a great deal of confusion about those complex instruments. Are

derivatives a cancerous growth that is slowly but surely destroying global financial markets? Are people who

use derivative products irresponsible because they use financial derivatives as part of their overall risk-

management strategy? Are financial derivatives the source of the next U.S. financial fiasco--a bubble on the

verge of exploding?

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 37/52

Those who oppose financial derivatives fear a financial disaster of tremendous proportions--a disaster that

could paralyze the world's financial markets and force governments to intervene to restore stability and

prevent massive economic collapse, all at taxpayers' expense. Critics believe that derivatives create risks that

are uncontrollable and not well understood. [1] Some critics liken derivatives to gene splicing: potentially

useful, but certainly very dangerous, especially if used by a neophyte or a madman without proper safeguards.

In this paper 10 myths, or common misconceptions, about financial derivatives are explored. Financial

derivatives have changed the face of finance by creating new ways to understand, measure, and manage

financial risks. Ultimately, derivatives offer organizations the opportunity to break financial risks into smaller

components and then to buy and sell those components to best meet specific risk-management objectives.

Moreover, under a market-oriented philosophy, derivatives allow for the free trading of individual risk

components, thereby improving market efficiency. Using financial derivatives should be considered a part of

any business's risk-management strategy to ensure that value-enhancing investment opportunities can be

pursued.

Myth Number 1: Derivatives Are New, Complex, High-Tech Financial Products Created by Wall Street's

Rocket Scientists

Financial derivatives are not new; they have been around for years. A description of the first known options

contract can be found in Aristotle's writings. He tells the story of Thales, a poor philosopher from Miletus

who developed a "financial device, which involves a principle of universal application." [2] People reproved

Thales, saying that his lack of wealth was proof that philosophy was a useless occupation and of no practical

value. But Thales knew what he was doing and made plans to prove to others his wisdom and intellect.

Thales had great skill in forecasting and predicted that the olive harvest would be exceptionally good the next

autumn. Confident in his prediction, he made agreements with area olive-press owners to deposit what little

money he had with them to guarantee him exclusive use of their olive presses when the harvest was ready.

Thales successfully negotiated low prices because the harvest was in the future and no one knew whether the

harvest would be plentiful or pathetic and because the olive-press owners were willing to hedge against the

possibility of a poor yield.

Aristotle's story about Thales ends as one might guess: "When the harvest-time came, and many [presses]

were wanted all at once and of a sudden, he let them out at any rate which he pleased, and made a quantity of

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 38/52

money. Thus he showed the world that philosophers can easily be rich if they like, but that their ambition is of

another sort." [3] So Thales exercised the first known options contracts some 2,500 years ago. He was not

obliged to exercise the options. If the olive harvest had not been good, Thales could have let the option

contracts expire unused and limited his loss to the original price paid for the options. But as it turned out, a

bumper crop came in, so Thales exercised the options and sold his claims on the olive presses at a high profit.

Options are just one type of derivative instrument. Derivatives, as their name implies, are contracts that are

based on or derived from some underlying asset, reference rate, or index. Most common financial derivatives,

described later, can be classified as one, or a combination, of four types: swaps, forwards, futures, and options

that are based on interest rates or currencies.

Most financial derivatives traded today are the "plain vanilla" variety--the simplest form of a financial

instrument. But variants on the basic structures have given way to more sophisticated and complex financial

derivatives that are much more difficult to measure, manage, and understand. For those instruments, the

measurement and control of risks can be far more complicated, creating the increased possibility of

unforeseen losses.

Wall Street's "rocket scientists" are continually creating new, complex, sophisticated financial derivative

products. However, those products are all built on a foundation of the four basic types of derivatives. Most of

the newest innovations are designed to hedge complex risks in an effort to reduce future uncertainties and

manage risks more effectively. But the newest innovations require a firm understanding of the tradeoff of

risks and rewards. To that end, derivatives users should establish a guiding set of principles to provide a

framework for effectively managing and controlling financial derivative activities. Those principles should

focus on the role of senior management, valuation and market risk management, credit risk measurement and

management, enforceability, operating systems and controls, and accounting and disclosure of risk-

management positions. [4]

Myth Number 2: Derivatives Are Purely Speculative, Highly Leveraged Instruments

Put another way, this myth is that "derivatives" is a fancy name for gambling. Has speculative trading of

derivative products fueled the rapid growth in their use? Are derivatives used only to speculate on the

direction of interest rates or currency exchange rates? Of course not. Indeed, the explosive use of financial

derivative products in recent years was brought about by three primary forces: more volatile markets,

deregulation, and new technologies.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 39/52

The turning point seems to have occurred in the early 1970s with the breakdown of the fixed-rate international

currency exchange regime, which was established at the 1944 conference at Bretton Woods and maintained

by the International Monetary Fund. Since then currencies have floated freely. Accompanying that

development was the gradual removal of government-established interest-rate ceilings when Regulation Q

interest-rate restrictions were phased out. Not long afterward came inflationary oil-price shocks and wild

interest-rate fluctuations. In sum, financial markets were more volatile than at any time since the GreatDepression.

Banks and other financial intermediaries responded to the new environment by developing financial risk-

management products designed to better control risk. The first were simple foreign-exchange forwards that

obligated one counterparty to buy, and the other to sell, a fixed amount of currency at an agreed date in the

future. By entering into a foreign-exchange forward contract, customers could offset the risk that large

movements in foreign-exchange rates would destroy the economic viability of their overseas projects. Thus,

derivatives were originally intended to beused to effectively hedge certain risks; and, in fact, that was the key

that unlocked their explosive development.

Beginning in the early 1980s, a host of new competitors accompanied the deregulation of financial markets,

and the arrival of powerful but inexpensive personal computers ushered in new ways to analyze information

and break down risk into component parts. To serve customers better, financial intermediaries offered an ever-

increasing number of novel products designed to more effectively manage and control financial risks. New

technologies quickened the pace of innovation and provided banks with superior methods for tracking and

simulating their own derivatives portfolios.

From the simple forward agreements, financial futures contracts were developed. Futures are similar to

forwards, except that futures are standardized by exchange clearinghouses, which facilitates anonymous

trading in a more competitive and liquid market. In addition, futures contracts are marked to market daily,

which greatly decreases counterparty risk--the risk that the other party to the transaction will be unable to

meet its obligations on the maturity date.

Around 1980 the first swap contracts were developed. A swap is another forward-based derivative that

obligates two counterparties to exchange a series of cash flows at specified settlement dates in the future.

Swaps are entered into through private negotiations to meet each firm's specific risk-management objectives.

There are two principal types of swaps: interest-rate swaps and currency swaps.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 40/52

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 41/52

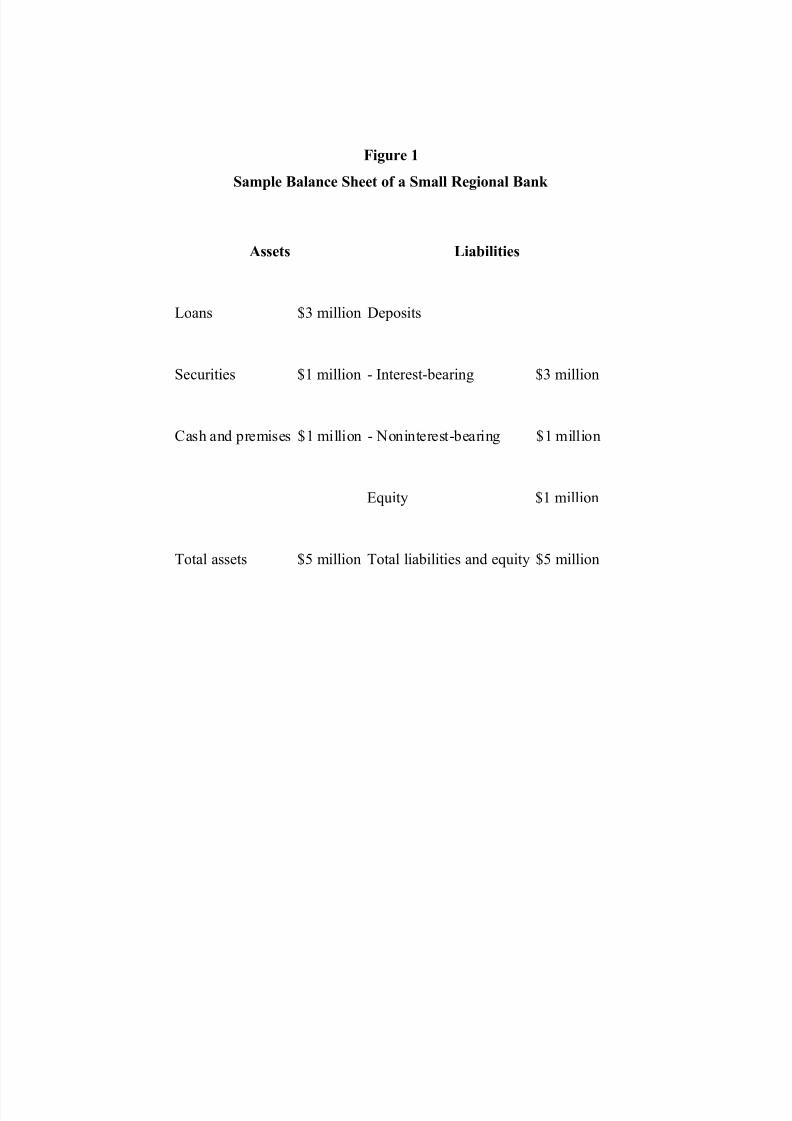

Very large organizations are the biggest users of derivative instruments. However, firms of all sizes can

benefit from using them. For example, consider a small regional bank (SRB) with total assets of $5 million

(Figure 1). [5] The SRB has a loan portfolio composed primarily of fixed-rate mortgages, a portfolio of

government securities, and interest-bearing deposits that are often repriced. Two illustrations of how SRBs

can use derivatives to hedge risks follow.

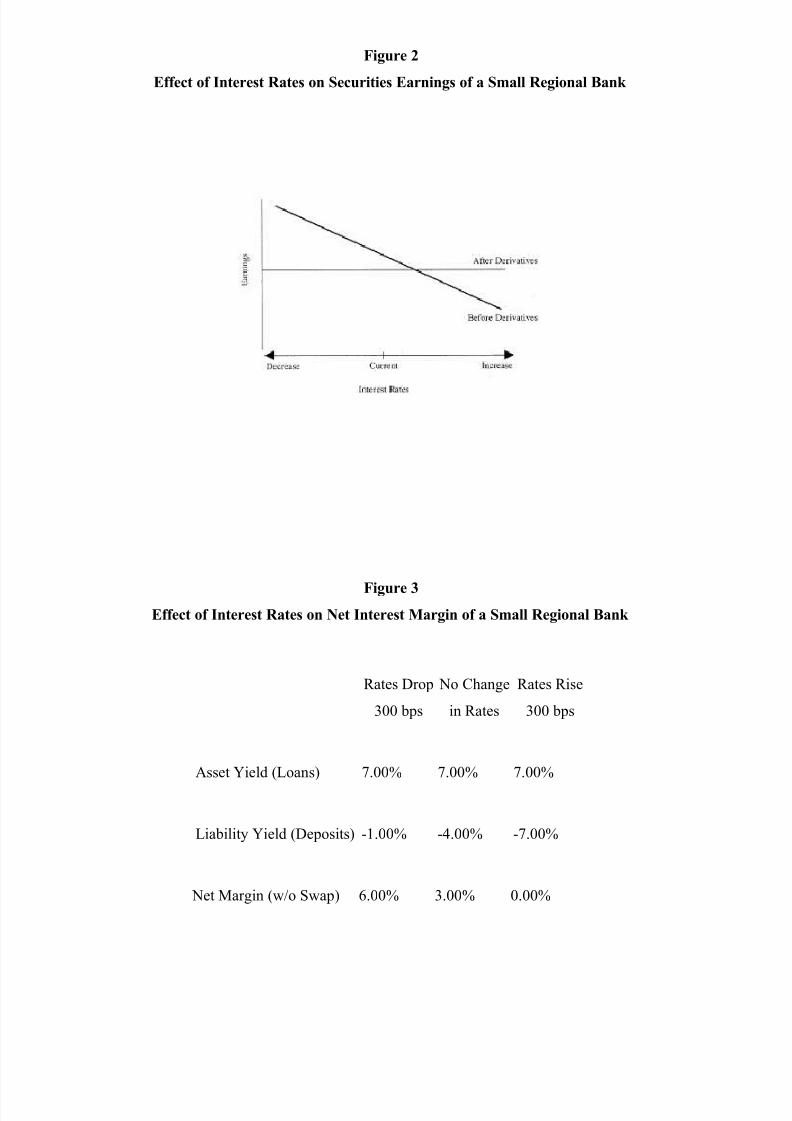

First, rising interest rates will negatively affect prices in the SRB's $1 million securities portfolio. But by

selling short a $1 million Treasury-bond futures contract, the SRB can effectively hedge against that interest-

rate risk and smooth its earnings stream in a volatile market. If interest rates went higher, the SRB would be

hurt by a drop in value of its securities portfolio, but that loss would be offset by a gain from its derivative

contract. Similarly, if interest rates fell, the bank would gain from the increase in value of its securities

portfolio but would record a loss from its derivative contract. By entering into derivatives contracts, the SRB

can lock in a guaranteed rate of return on its securities portfolio and not be as concerned about interest-rate

volatility (Figure 2).

The second illustration involves a swap contract. As in the first illustration, rising interest rates will harm the

SRB because it receives fixed cash flows on its loan portfolio and must pay variable cash flows for its

deposits. Once again, the SRB can hedge against interest-rate risk by entering into a swap contract with a

dealer to pay fixed and receive floating payments.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 42/52

Figure 1

Sample Balance Sheet of a Small Regional Bank

Assets Liabilities

Loans $3 million Deposits

Securities $1 million - Interest-bearing $3 million

Cash and premises $1 million - Noninterest-bearing $1 million

Equity $1 million

Total assets $5 million Total liabilities and equity $5 million

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 43/52

Figure 2

Effect of Interest Rates on Securities Earnings of a Small Regional Bank

Figure 3

Effect of Interest Rates on Net Interest Margin of a Small Regional Bank

Rates Drop

300 bps

No Change

in Rates

Rates Rise

300 bps

Asset Yield (Loans) 7.00% 7.00% 7.00%

Liability Yield (Deposits) -1.00% -4.00% -7.00%

Net Margin (w/o Swap) 6.00% 3.00% 0.00%

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 44/52

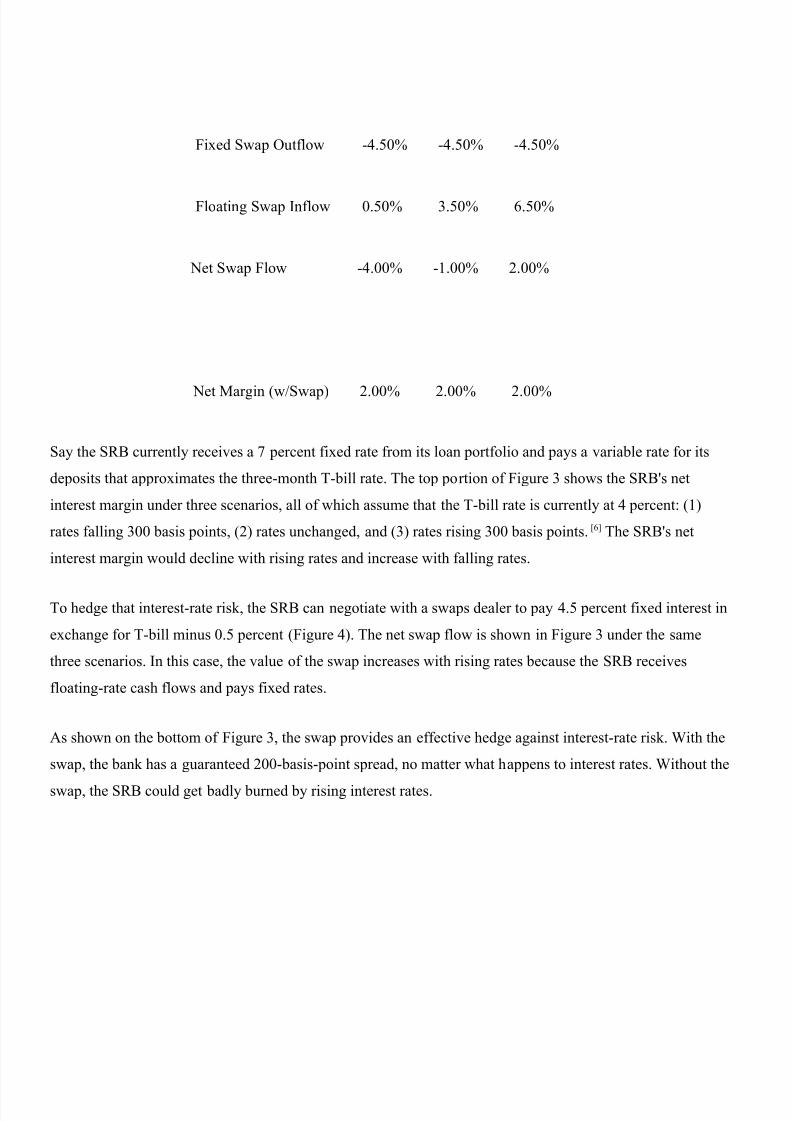

Fixed Swap Outflow -4.50% -4.50% -4.50%

Floating Swap Inflow 0.50% 3.50% 6.50%

Net Swap Flow -4.00% -1.00% 2.00%

Net Margin (w/Swap) 2.00% 2.00% 2.00%

Say the SRB currently receives a 7 percent fixed rate from its loan portfolio and pays a variable rate for its

deposits that approximates the three-month T-bill rate. The top portion of Figure 3 shows the SRB's net

interest margin under three scenarios, all of which assume that the T-bill rate is currently at 4 percent: (1)

rates falling 300 basis points, (2) rates unchanged, and (3) rates rising 300 basis points. [6] The SRB's net

interest margin would decline with rising rates and increase with falling rates.

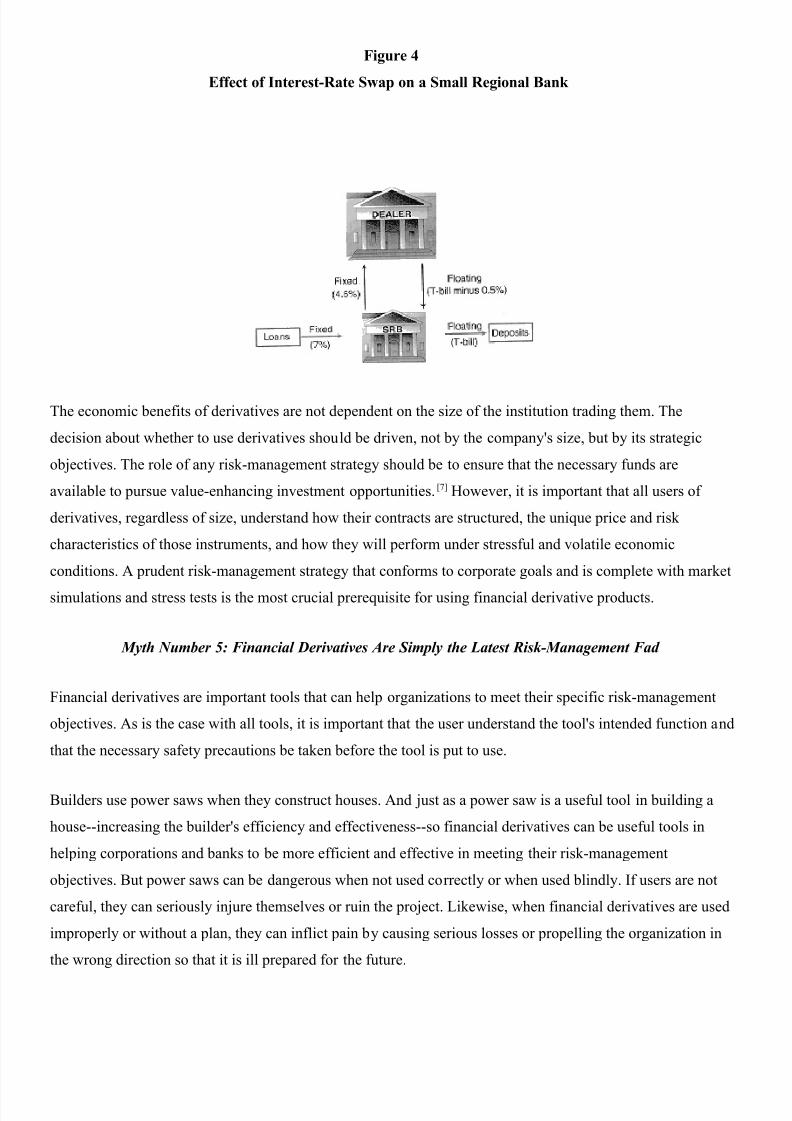

To hedge that interest-rate risk, the SRB can negotiate with a swaps dealer to pay 4.5 percent fixed interest in

exchange for T-bill minus 0.5 percent (Figure 4). The net swap flow is shown in Figure 3 under the same

three scenarios. In this case, the value of the swap increases with rising rates because the SRB receives

floating-rate cash flows and pays fixed rates.

As shown on the bottom of Figure 3, the swap provides an effective hedge against interest-rate risk. With the

swap, the bank has a guaranteed 200-basis-point spread, no matter what happens to interest rates. Without the

swap, the SRB could get badly burned by rising interest rates.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 45/52

Figure 4

Effect of Interest-Rate Swap on a Small Regional Bank

The economic benefits of derivatives are not dependent on the size of the institution trading them. The

decision about whether to use derivatives should be driven, not by the company's size, but by its strategic

objectives. The role of any risk-management strategy should be to ensure that the necessary funds are

available to pursue value-enhancing investment opportunities. [7] However, it is important that all users of

derivatives, regardless of size, understand how their contracts are structured, the unique price and risk

characteristics of those instruments, and how they will perform under stressful and volatile economic

conditions. A prudent risk-management strategy that conforms to corporate goals and is complete with market

simulations and stress tests is the most crucial prerequisite for using financial derivative products.

Myth Number 5: Financial Derivatives Are Simply the Latest Risk-Management Fad

Financial derivatives are important tools that can help organizations to meet their specific risk-management

objectives. As is the case with all tools, it is important that the user understand the tool's intended function and

that the necessary safety precautions be taken before the tool is put to use.

Builders use power saws when they construct houses. And just as a power saw is a useful tool in building a

house--increasing the builder's efficiency and effectiveness--so financial derivatives can be useful tools in

helping corporations and banks to be more efficient and effective in meeting their risk-management

objectives. But power saws can be dangerous when not used correctly or when used blindly. If users are not

careful, they can seriously injure themselves or ruin the project. Likewise, when financial derivatives are used

improperly or without a plan, they can inflict pain by causing serious losses or propelling the organization in

the wrong direction so that it is ill prepared for the future.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 46/52

When used properly, financial derivatives can help organizations to meet their risk-management objectives so

that funds are available for making worthwhile investments. Again, a firm's decision to use derivatives should

be driven by a risk-management strategy that is based on broader corporate objectives.

The most basic questions about a firm's risk-management strategy should be addressed: Which risks should be

hedged and which should remain unhedged? What kinds of derivative instruments and trading strategies are

most appropriate? How will those instruments perform if there is a large increase or decrease in interest rates?

How will those instruments perform if there are wild fluctuations in exchange rates?

Without a clearly defined risk-management strategy, use of financial derivatives can be dangerous. It can

threaten the accomplishment of a firm's long-range objectives and result in unsafe and unsound practices that

could lead to the organization's insolvency. But when used wisely, financial derivatives can increase

shareholder value by providing a means to better control a firm's risk exposures and cash flows.

Clearly, derivatives are here to stay. We are well on our way to truly global financial markets that will

continue to develop new financial innovations to improve risk-management practices. Financial derivatives

are not the latest risk-management fad; they are important tools for helping organizations to better manage

their risk exposures.

Myth Number 6: Derivatives Take Money Out of Productive Processes and Never Put Anything Back

Financial derivatives, by reducing uncertainties, make it possible for corporations to initiate productive

activities that might not otherwise be pursued. For example, an Italian company may want to build a

manufacturing facility in the United States but is concerned about the project's overall cost because of

exchange-rate volatility between the lira and the dollar. To ensure that the company will have the necessary

cash available when it is needed for investment, the Italian manufacturer should devise a prudent risk-

management strategy that is in harmony with its broader corporate objective of building a manufacturing

facility in the United States. As part of that strategy, the Italian firm should use financial derivatives to hedge

against foreign-exchange risk. Derivatives used as a hedge can improve the management of cash flows at the

individual firm level.

To ensure that productive activities are pursued, corporate finance and treasury groups should transform their

operations from mundane bean counting to activist financial risk management. They should integrate a clear

set of risk-management goals and objectives into the organization's overall corporate strategy. The ultimate

goal is to ensure that the organization has the necessary funds at its disposal to pursue investments that

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 47/52

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 48/52

around the financial system via secondary markets. Thus, many risks associated with derivatives are actually

created by the dealers' customers or by their customers' customers. Those risks have been inherent in our

nation's financial system since its inception.

Banks and other financial intermediaries should view themselves as risk managers--blending their knowledge

of global financial markets with their clients' needs to help their clients anticipate change and have the

flexibility to pursue opportunities that maximize their success. Banking is inherently a risky business. Risk

permeates much of what banks do. And, for banks to survive, they must be able to understand, measure, and

manage financial risks effectively.

The types of risks faced by corporations today have not changed; rather, they are more complex and

interrelated. The increased complexity and volatility of the financial markets have paved the way for the

growth of numerous financial innovations that can enhance returns relative to risk. But a thorough

understanding of the new financial-engineering tools and their proper integration into a firm's overall risk-

management strategy and corporate philosophy can help turn volatility into profitability.

Risk management is not about the elimination of risk; it is about the management of risk: selectively choosing

those risks an organization is comfortable with and minimizing those that it does not want. Financial

derivatives serve a useful purpose in fulfilling risk-management objectives. Through derivatives, risks from

traditional instruments can be efficiently unbundled and managed independently. Used correctly, derivatives

can save costs and increase returns.

Myth Number 9: Derivatives Link Market Participants More Tightly Together, Thereby Increasing

Systemic Risks

Financial derivative participants can be divided into two groups: end-users and dealers. As end-users, banks

use derivatives to take positions as part of their proprietary trading or for hedging as part of their asset/liability

management. As dealers, banks use derivatives by quoting bids and offers and committing capital to satisfy

customers' needs for managing risk.

In the developmental years of financial derivatives, dealers, for the most part, acted as brokers, finding

counterparties with offsetting requirements. Then dealers began to offer themselves as counterparties to

intermediate customer requirements. Once a position was taken, a dealer immediately either matched it by

entering into an opposing transaction or "warehoused" it--temporarily using the futures market to hedge

unwanted risks--until a match could be found.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 49/52

Today dealers manage portfolios of derivatives and oversee the net, or residual, risk of their overall position.

That development has changed the focus of risk management from individual transactions to portfolio

exposures and has substantially improved dealers' ability to accommodate a broad spectrum of customer

transactions. Because most active derivatives players today trade on portfolio exposures, it appears that

financial derivatives do not wind markets together any more tightly than do loans. Derivatives players do not

match every trade with an offsetting trade; instead, they continually manage the residual risk of the portfolio.If a counterparty defaults on a swap, the defaulted party does not turn around and default on some other

counterparty that offset the original transaction. Instead, a derivatives default is very similar to a loan default.

That is why it is important that derivatives players perform with due diligence in determining the financial

strength and default risks of potential counterparties.

For banking supervisors in the United States, probably the most important question today is, What could go

wrong to engender systemic risk--the danger that a failure at a single bank could cause a domino effect,

precipitating a banking crisis? Because financial derivatives allow different risk components to be isolated

and passed around the financial system, those who are willing and able to bear each risk component at the

least cost will become the risk holders. That clearly reduces the overall cost of risk bearing and enhances

economic efficiency.

Furthermore, a major shock that would jolt financial markets in the absence of derivatives would also affect

financial markets in which the use of derivatives was widespread. But because the holders of various risks

would be different, the impact would be different and presumably not as great because the holders of the risks

should be better able to absorb potential losses.

Myth Number 10: Because of the Risks Associated with Derivatives, Banking Regulators Should Ban

Their Use by Any Institution Covered by Federal Deposit Insurance

The problem is not derivatives but the perverse incentives banks have under the current system of federal

deposit guarantees. Deposit insurance and other deposit reforms were first introduced to address some of the

instabilities associated with systemic risk. Through federally guaranteed deposit insurance, the U.S.

government attempted to avoid, by increasing depositor confidence, the experience of deposit runs that

characterized banking crises before the 1930s.

The current deposit guarantee structure has, indeed, reduced the probability of large-scale bank panics, but it

has also created some new problems. Deposit insurance effectively eliminates the discipline provided by the

market mechanism that encourages banks to maintain appropriate capital levels and restrict unnecessary risk

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 50/52

taking. Therefore, banks may wish to pursue higher risk strategies because depositors have a diminished

incentive to monitor banks. Further, federal deposit insurance may actually encourage banks to use derivatives

as speculative instruments to pursue higher risk strategies, instead of to hedge, or as dealers.

Since federal deposit insurance discourages market discipline, regulators have been put in the position of

monitoring banks to ensure that they are managed in a safe and sound manner. Given the present system of

federal deposit guarantees, regulatory proposals involving financial derivatives should focus on market-

oriented reforms as opposed to laws that might eliminate the economic risk-management benefits of

derivatives. [8]

To that end, banking regulators should emphasize more disclosure of derivatives positions in financial

statements and be certain that institutions trading huge derivatives portfolios have adequate capital. In

addition, because derivatives could have implications for the stability of the financial system, it is important

that users maintain sound risk-management practices.

Regulators have issued guidelines that banks with substantial trading or derivatives activity should follow.

Those guidelines include

• active board and senior management oversight of trading activities;

• establishment of an internal risk-management audit function that is independent of the trading

function;

• thorough and timely audits to identify internal control weaknesses; and

• risk-measurement and risk-management information systems that include stress tests, simulations, and

contingency plans for adverse market movements.

It is the responsibility of a bank's senior management to ensure that risks are effectively controlled and limited

to levels that do not pose a serious threat to its capital position. Regulation is an ineffective substitute for

sound risk management at the individual firm level.

8/9/2019 18929648 Financial Derivatives

http://slidepdf.com/reader/full/18929648-financial-derivatives 51/52

Should My Company Use Derivatives?

Financial derivatives should be considered for inclusion in any corporation's risk-control arsenal. Derivatives

allow for the efficient transfer of financial risks and can help to ensure that value-enhancing opportunities will

not be ignored. Used properly, derivatives can reduce risks and increase returns.

Derivatives also have a dark side. It is important that derivatives players fully understand the complexity of

financial derivatives contracts and the accompanying risks. Users should be certain that the proper safeguards

are built into trading practices and that appropriate incentives are in place so that corporate traders do not take

unnecessary risks.

The use of financial derivatives should be integrated into an organization's overall risk-management strategy

and be in harmony with its broader corporate philosophy and objectives. There is no need to fear financial

derivatives when they are used properly and with the firm's corporate goals as guides.

What Should Regulators Do?

Believing the 10 myths presented here, indeed, believing just one or two of them, could lead one to advocate

legislative and regulatory measures to restrict the use of derivatives. [9] Derivatives-related disasters, such as

the Orange County bankruptcy and the collapse of Barings, have led to questions about the ability of

individual derivatives participants to internally manage their trading operations. In addition, concerns have