financial aid 101 presented by elizabeth ochoa

TRANSCRIPT

FINANCIAL AID 101

Presented by Elizabeth Ochoa

Federal Philosophy

Family is responsible to pay for student’s education To the extent they are financially able

Who gets to decide what “financially able” means? You or the feds?

West Valley

COA$12,617

- EFC 1,000

= Need $12,617

The FAFSA application is the foundation for any financial aid gifted

or loaned to help pay for your education.

Need Help?

Workshops Available:Every Tuesday at 11am in A&R Lobby

What is a FAFSA?

CA Dream Act Application

Application is available at: http://www.csac.ca.gov/dream_act.asp

2013-2014

April 12, 2013

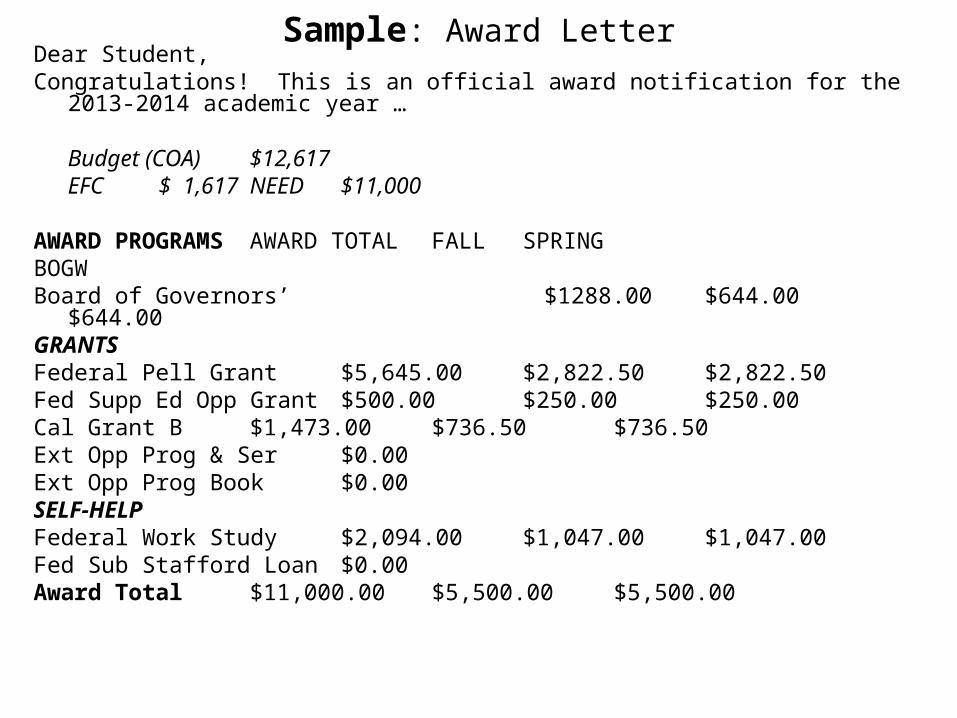

Sample: Award LetterDear Student,Congratulations! This is an official award notification for the 2013-2014

academic year …

Budget (COA) $12,617EFC $ 1,617

NEED $11,000

AWARD PROGRAMS AWARD TOTAL FALL SPRINGBOGWBoard of Governors’ $1288.00 $644.00

$644.00GRANTSFederal Pell Grant $5,645.00 $2,822.50 $2,822.50Fed Supp Ed Opp Grant $500.00 $250.00

$250.00Cal Grant B $1,473.00 $736.50

$736.50Ext Opp Prog & Ser $0.00 Ext Opp Prog Book $0.00SELF-HELPFederal Work Study $2,094.00 $1,047.00 $1,047.00Fed Sub Stafford Loan $0.00Award Total $11,000.00 $5,500.00 $5,500.00

Professional Judgment If you have a change in:

Dependency Status Income and Assets Child Support Number in Household or College Private elementary/secondary school tuition Medical or dental expenses (not covered by insurance)

*Contact your Financial Aid office for more details

Your rights and responsibilities

Right to ask: Costs and refund policies What financial help is

available To explain the various

elements in your financial aid package

Responsibility to: Know and comply with all

application deadlines Respond promptly and

provide all information Read and keep copies of all

forms Complete loan entrance

and exit counseling Repay your student loans

Know the Terminology Debit

A purchase authorized by you in which a retailer uses money electronically withdrawn from your checking account as payment for goods and services. You initiate the purchase by using your debit card, generally tied to your checking account. Does not contribute to your credit rating.

Interest

The periodic fee charged by the lender to borrow money. Interest charges are repaid in addition to the principal of the loan.

Buyer’s Remorse/Impulse Purchases

Regretted purchases usually bought in the heat of an emotional moment.

Checking Account

The most common way to pay your bills. You write a check, use a debit card or authorize a transfer of funds and that money is deducted from your checking account.

Overdraft Protection

By opting in for overdraft protection, you authorize your bank to cover charges even if you don’t have money in your account. Fees for overdraft protection transactions can be very expensive.

Credit Report

A visual summary of how you handle credit. It’s typically viewed by lenders, apartment rental managers, insurance companies and employers as a symbol of your reliability.

Credit Score

A number assigned to your credit report to indicate your overall credit worthiness on a scale from 350 (poor rating) to 850 (excellent).

Consider using the ECMC’s Financial Awareness Basics Glossary at: http://www.ecmc.org/details/financial-glossary.html

Budgeting

According to the National Center for Education Statistics (NCES), the research arm of the U.S. Department of Education, students who dropped out of postsecondary institutions cited financial reasons as the primary catalyst for leaving school.

Learning to develop and manage a budget is a key skill set that will help you achieve both short- and long-term financial goals throughout life – skills that are especially handy during college when money is typically tight.

And remember, keep your eyes on the prize.

The time you put into your budget, and the choices you make to keep your budget on track, will pay off over the long run by providing you with greater financial independence and security.

Protect against identity theft Keep your SSN, DOB, Driver’s license, passwords

and PINs confidential Do not leave your wallet in the car Never give out personal or financial information

over the phone or via e-mail Make sure Web sites are secure before providing

information Get your free credit report annually

www.annualcreditreport.com Shred all documents you no longer need Learn more at: www.ftc.gov/idtheft

QUESTIONS?