financial accounting assg

TRANSCRIPT

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 1/16

ABC 123 XYZ

MBS Student ID:

1st March 2010

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 2/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

Table of Contents

Table of Contents .......................................................................... 2

Question 1 (50 Marks) .................................................................. 3

The difference between accrual and cash accounting ..................................3

Accrual accounting as a better indicator of future cash flow ....................... 5

Limitations of accrual accounting .................................................................. 6

(1053 words) ................................................................................ 7

Question 2 (50 marks) .................................................................... 8

GYAPlc Income Statement & Balance Sheet (25 marks) ............................... 8

.................................................................................................................... 10

(553 words) ................................................................................ 13

References .................................................................................. 14

Financial Accounting – Course Assessment 1

1 March 2010 Page 2 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 3/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

Question 1 (50 Marks)The difference between accrual and cash accounting

Cash accounting records transactions based on the receipt and payment of cash, which

means that revenue is recognised when cash is received, and expenses when cash is paid (Scott

2003; Elliot and Elliot 2008). Accrual accounting on the other hand, recognizes revenue when it

is earned, and expenses when it is incurred regardless of when payment is made or received

(Scott 2003). Thus the main difference between accrual and cash accounting is “when” income

and expenses are recognised. The cash basis method recognises income when cash is “received”

and expenses when cash is “paid”. The accrual method recognises income when it is “earned” and

expenses when they are “incurred” (Scott 2003).

HHH Communications Ltd1, has the following main revenue streams; revenue from

postpaid services, sales of prepaid starter packs, sales of prepaid top up tickets and revenue

earned from carriers for international gateway services. Revenue is earned differently depending

on which revenue stream (e.g. in prepaid plans customer pays upfront for prepaid credit but may

not use services till later) and hence is recognised differently. Revenues of mobile postpaid

services and revenue earned from carriers for international gateway services are recognised at the

time of customer usage. Revenue from sales of starter packs is recognised at the point of sale to

third parties. Revenue from sales of prepaid top-up-tickets is recognised when services are

rendered.

1 For question 1, HHH Communications Ltd, a Malawin mobile telecommunicationsprovider that prepares in financial statements using accrual accounting inaccordance with the provisions of the Malawin Companies Act, 1965 and FinancialReporting Standards (“FRS”), the Malawin Accounting Standards of the CompaniesBoard (“MASB”) Approved Accounting Standards in Malawi for Entities Other thanPrivate Entities has been used as a reference.

Financial Accounting – Course Assessment 1

1 March 2010 Page 3 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 4/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

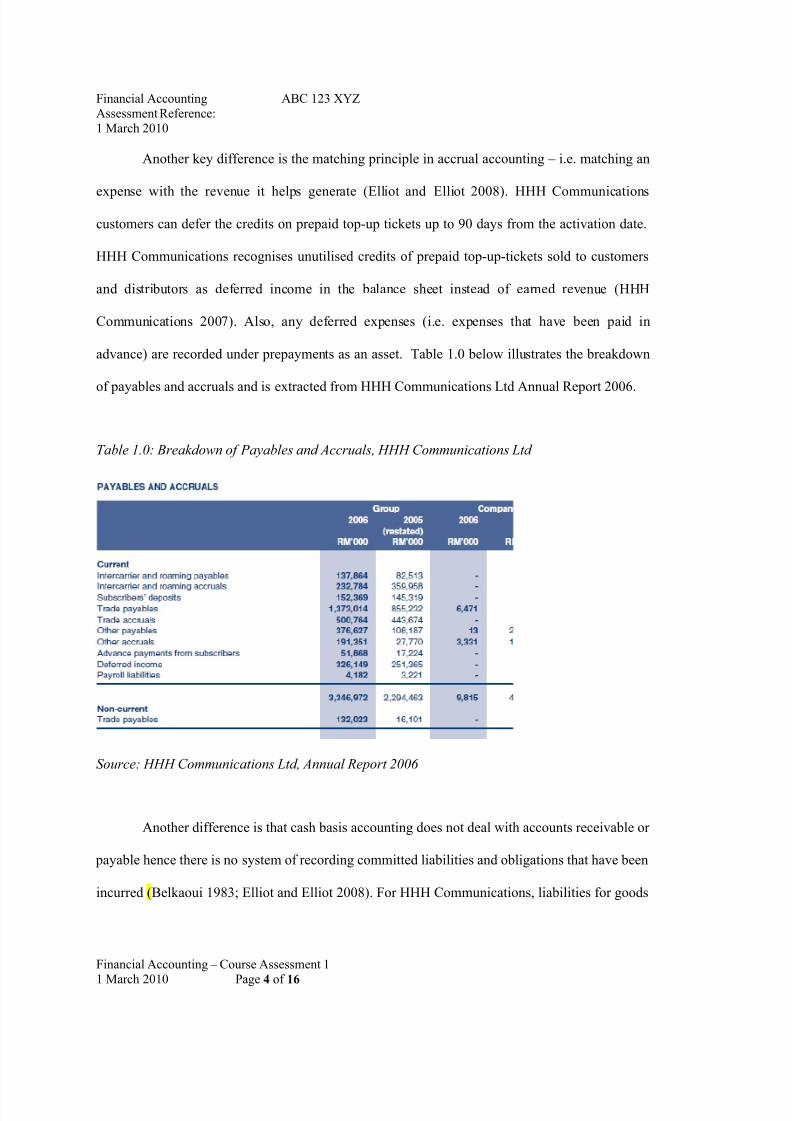

Another key difference is the matching principle in accrual accounting – i.e. matching an

expense with the revenue it helps generate (Elliot and Elliot 2008). HHH Communications

customers can defer the credits on prepaid top-up tickets up to 90 days from the activation date.

HHH Communications recognises unutilised credits of prepaid top-up-tickets sold to customers

and distributors as deferred income in the balance sheet instead of earned revenue (HHH

Communications 2007). Also, any deferred expenses (i.e. expenses that have been paid in

advance) are recorded under prepayments as an asset. Table 1.0 below illustrates the breakdown

of payables and accruals and is extracted from HHH Communications Ltd Annual Report 2006.

Table 1.0: Breakdown of Payables and Accruals, HHH Communications Ltd

Source: HHH Communications Ltd, Annual Report 2006

Another difference is that cash basis accounting does not deal with accounts receivable or

payable hence there is no system of recording committed liabilities and obligations that have been

incurred (Belkaoui 1983; Elliot and Elliot 2008). For HHH Communications, liabilities for goods

Financial Accounting – Course Assessment 1

1 March 2010 Page 4 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 5/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

received and services rendered to the company prior to the end of the financial year and which

remain unpaid are represented under payables and accruals. The credit policy provides trade

receivables with 15-120 days credit period, hence under receivables, accrued revenue are carried

at invoice amount and/or income earned less an allowance for doubtful debts.

Accrual accounting as a better indicator of future cash flow

In accrual accounting assets and liabilities are recorded and transactions are captured

irrespective of the actual inflow or outflow of cash. Thus current cash inflows and outflows are

combined with expected future cash inflows and outflows to provide a more accurate picture of a

company's current financial position and continuing ability to generate favourable cash flows

(Guinan 2009). This is illustrated in the example where the Central Government of India was

determined to switch over to an accrual system of accounting from its current cash system. As

asserted by the then Minister of Finance, Mr Chidambaram, “…because, we do not use accrual

accounting, there are many large liabilities that are hidden. For example, the pay as you go

pension system hides huge liabilities. There is no funding of the pension system and therefore the

liabilities are not calculated correctly, not provided for and not accounted for…” (Anon 2005).

In the case of HHH Communications, the unutilised credits of prepaid top-up-tickets sold

and unutilised airtime on postpaid rate plans are recognised as deferred income and recorded as a

known liability in the balance sheet ensuring that reserves are kept aside for future claims (HHH

Communications Bhd 2007). Also, accrued expenses, current and noncurrent trade payables are

also recorded to provide an indication of payment obligations not paid as yet enabling a more

indicative picture of future cash flow.

Financial Accounting – Course Assessment 1

1 March 2010 Page 5 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 6/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

In addition, because accrual accounting adopts the matching principle, it enables a more

accurate determination of net income as it matches income with the expenses incurred to produce

it. Computing income on a cash basis may misrepresent true profitability for an accounting period

when there is a time lag between the exchange of goods and services and the related cash receipt

(Greenberg, Johnson, and Ramesh 1986). In the case of HHH Communications, if revenue from

prepaid sales were captured on a cash flow basis, it may actually inflate the income figure since

this revenue would not actually be “earned” as yet although cash is received from customers.

Limitations of accrual accounting

There are limitations of accrual accounting as asset valuation and income determination

in accrual accounting can be subjective (Belkaoui 1983). Because accrual accounting records

revenue when it is earned, earnings can be managed through aggressive sales to inflate the

revenue amount for a firm. Clikeman (2003) provides an example of earnings management by

offering customers extended payment terms at the end of a period to accelerate sales or recording

generous reserves in a particularly good quarter to make it easier to meet earnings goals in a

subsequent quarter. Clikeman (2003) also states that sales can be “brought forward” from a future

period into the current period and recognised as revenue by offering discounts or more favourable

credit terms on deliveries accepted before period end. Likewise, revenue may be deferred by

delaying delivery of goods of one accounting period to the next period. Another way that reported

earnings is managed is by accelerating or postponing discretionary expenses such as maintenance,

advertising, research and development, and employee training as well as making provisions for

future expenses (Barton and Simko 2002). For instance, HHH Communications makes provisions

for liabilities and charges such as “network reconstruction”, “site rectification”, “post

Financial Accounting – Course Assessment 1

1 March 2010 Page 6 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 7/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

employment benefits” and “staff incentive scheme”. However, these provisions are based on

estimated costs and may not necessarily materialise fully in reality.

It is argued that asset valuation in accrual accounting provides opportunity for abuse and

manipulation because of different methods of depreciation and subjectivity in determining the

useful life of assets (Belkaoui 1983). For instance, management can make a firm appear more

profitable than it really is by understating depreciation expense. Richardson, Sloan, Soliman, and

Tuna (2005) citing the 2002 WorldCom case which involved billions of dollars of operating costs

that were aggressively capitalised as property, plants and equipment, assert that companies using

aggressive accrual accounting often produce unreliable earnings. Sometimes for income tax

purposes, management may want to show lower gross and operating profits by undercounting and

under valuing ending inventory Clikeman (2003).

(1053 words)

Financial Accounting – Course Assessment 1

1 March 2010 Page 7 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 8/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

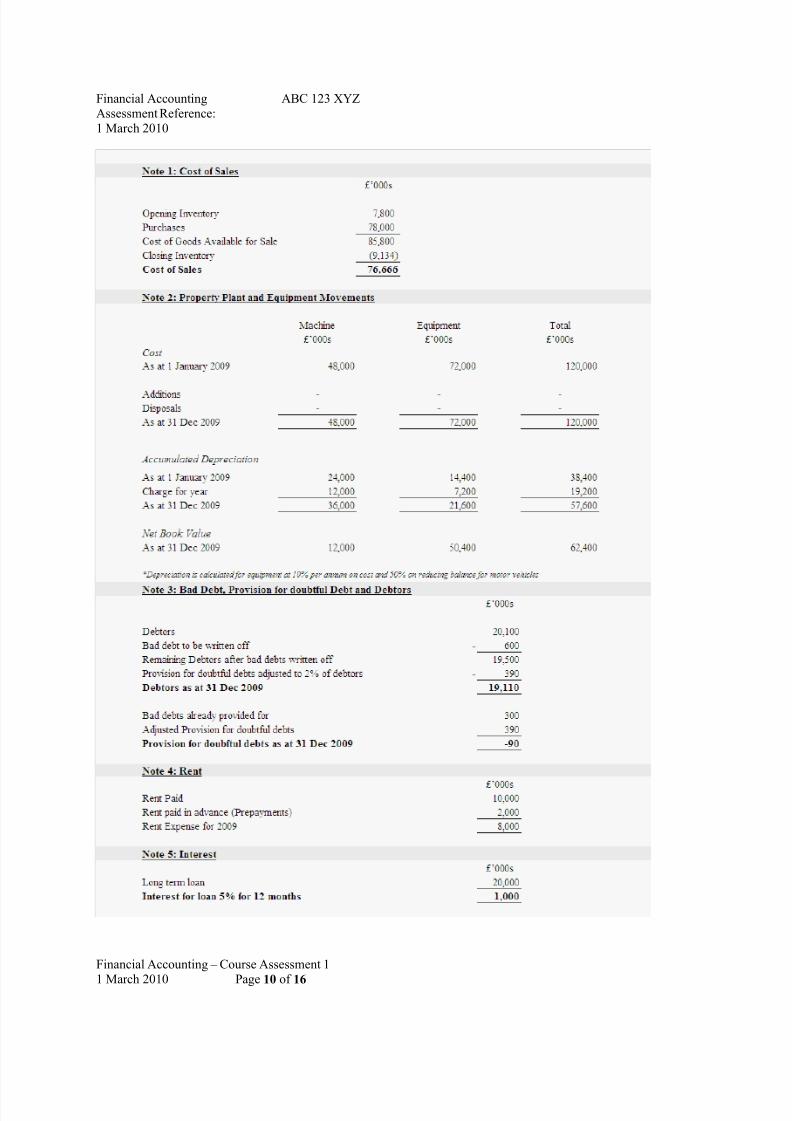

Question 2 (50 marks)

GYAPlc Income Statement & Balance Sheet (25 marks)

Financial Accounting – Course Assessment 1

1 March 2010 Page 8 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 9/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

Financial Accounting – Course Assessment 1

1 March 2010 Page 9 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 10/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

Financial Accounting – Course Assessment 1

1 March 2010 Page 10 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 11/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

a. Although IFRS is being used in many countries worldwide,

financial statements are not yet truly comparable on a global

basis. Briefly explain whether or not you agree with this

assessment and state your reasons (25 marks).

The intent of the IFRS is to enable “high quality, transparent and comparable

information” in financial reporting (Elliot and Elliot 2008; Ball 2006). More than 100 countries

have either mandated or endorsed the use of International Financial Reporting Standards (IFRSs),

while the remaining major economies have established timelines for convergence with, or

adoption of IFRS.

It can be argued that financial statements are not yet truly comparable on a global basis as

yet because although it is adopted by more than 100 countries, it has not been adopted by all

countries, amongst which is the US. Also, even though countries have embarked on “convergence

efforts” to narrow differences between the IFRS and domestic standards, the different timelines

for completion (e.g. Malawi - 2012, India -2011, US - 2015) make comparability at this stage

difficult.

In addition, political and economic reasons will result in unequal implementation of the

IFRS around the world. For instance, pressure from the French government and the domestic

banking industry on balance sheet volatility concerns resulted in the EU carve out of the fair

value accounting standard -IAS 391 and hence now allowing hedge accounting for banks’ core

1 IAS 39 - fair value accounting standard that required banks to report fair values of their financial

instruments which may result in increased volatility in their balance sheets and earnings and therefore

Financial Accounting – Course Assessment 1

1 March 2010 Page 11 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 12/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

deposits. Likewise in Malawi, all companies are subjected to IFRS 39 except for Permodalan

Nasional Ltd (PNB) which is a government owned investment arm. Hence, albeit uniformity of

international standards, countries still have the right to introduce “exceptional” standards as it

deems fit..

Moreover, the variety of IRFS adopting countries range from countries with developed

accounting and auditing professions to countries without a similarly developed institutional

background. This sheds some doubt as to whether implementation will be of equal standard in all

the 100 countries that have adopted IFRS. This may be further compounded by the lack of

enforcement since the IFSB is a standard setter and does not have an enforcement mechanism for

its standards.

Furthermore, as argued by Ball (2006), the concept that implementation of unified

standards alone will be a panacea in enabling standardised financial reporting and making

financial statements truly comparable is somewhat naïve. Ball (2006) argues that to make

financial statements truly comparable there is a need to not only achieve uniformity in accounting

standards, but also in financial reporting behaviour. This is because, aside from accounting

standards, legal and political systems, ownership structure are amongst some factors that may

interact with each other and affect quality, and hence comparability of financial reports (Ball

2006; Burgstahler and Leuz 2007; Bushman and Piotroski 2006; Ding, Hope, Jeanjean and

Stolowy 2007). For instance, a study conducted by Ball, Robin and Wu (2003) reveal that

companies’ in four East Asian countries were more likely to be part of related corporate groups

including family controlled businesses, where predominantly an “insider access” model exists

affecting investor and regulator views of the financial institutions stability.

Financial Accounting – Course Assessment 1

1 March 2010 Page 12 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 13/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

versus a public disclosure model in financial reporting. A country’s legal system also influences

the application of uniformed standards. An example would be China where all domestic

companies with foreign shareholders were mandated to adopt the IFRS. Although the adoption of

the IFRS is mandated, given China’s institutional environment where the Chinese government

and army play a strong political role in the economy and where shareholder litigation rights are

absent, Ball, Robin and Wu (2000) study reveals no increase in timeliness of economic gains or

losses reporting versus when reporting under domestic standards. Hence, it is debatable as to

whether managers in countries whose legal systems are less responsive to the interests of

shareholders will change their habits under IFRS.

Nevertheless the IFRS is definitely a step in the right direction with advantages like

standardisation of reporting formats, reducing risk and cost to investors and removing the barriers

for cross border acquisitions and divestitures amongst others.

(553 words)

Financial Accounting – Course Assessment 1

1 March 2010 Page 13 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 14/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

References

1. ANON., 2005. Centre firm on switching over to accrual accounting, Asia Africa

Intelligence Wire [online], Available at: < URL :

http://find.galegroup.com/gtx/infomark.do?&contentSet=IAC-

Documents&type=retrieve&tabID=T007&prodID=GRGM&docId=A136246438&source

=gale&srcprod=GRGM&userGroupName=sunway&version=1.0> [Accessed 19

February 2010]

2. Ball, R. (2006). International Financial Reporting Standards: pros and cons for investors.

Accounting and Busines Research, International Accounting Policy Forum, 5-27.

3. Ball, R., Robin, A. and Wu, S. (2000).Accounting standards, the institutional

environment and issuer incentives: effect on accounting conservatism in China. Asia

Pacific Journal of Accounting and Economics, 7, 71-96.

4. Ball, R. Robin, A. and Wu, S. (2003). Incentives versus standards: properties of

accounting income in four East Asian countries and implications of acceptance of IAS.

Journal of Accounting and Economic, 36, 235-270.

5. Barton, J., Simko, P.J. (2002). The balance sheet as an earnings management constraint,

The Accounting Review, December, 1-27.

6. Belkaoui, A. (1983). Accrual accounting and cash accounting: relative merits. Journal of

Business Finance and Accounting , 10 (2), 299 -312.

Financial Accounting – Course Assessment 1

1 March 2010 Page 14 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 15/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

7. Burgstahler, D., Hail, L. and Leuz, C. (2007). The importance of reporting incentives:

earnings management in European private and public Firms. The Accounting Review, 81

(2006), 983–1017.

8. Bushman, R. and Piotroski, J. (2006). Financial reporting incentives for conservative

accounting: the influence of legal and political institutions. Journal of Accounting and

Economics, 42 , 107-148.

9. Clikeman, P.M. (2003). Where auditors fear to tread: internal auditors should be

proactive in educating companies on the perils of earnings management and in searching

for signs of its use, Internal Auditor , August, 75-80.

10.Ding, Y., Hope, O., Jeanjean, T. and Stolowy, H. (2007). Differences between domestic

accounting standards and IAS: measurement, determinants and implications. Journal of

Accounting and Public Policy, 26 (1), 1-38.

11.Elliot, B. and Elliot, J. (2008). Financial accounting and reporting.12th ed. Harlow:

Pearson Education Limited.

12.Greenberg, R., Johnson, G. and Ramesh, K. (1986). Earnings versus cash flow as a

predicator of future cash flow measures. Journal of Accounting, Auditing and Finance,

Fall, 266-277.

13.Guinan, J. ed. (2009). Investopedia’s guide to wall speak. Australia: McGraw-Hill.

14.HHH Communications Ltd. (2007). 2006 Annual Report , Malawi: HHH

Communications Ltd.

Financial Accounting – Course Assessment 1

1 March 2010 Page 15 of 16

8/7/2019 FInancial Accounting Assg

http://slidepdf.com/reader/full/financial-accounting-assg 16/16

Financial Accounting ABC 123 XYZ

Assessment Reference:

1 March 2010

15.Richardson, S.A., Sloan, R. G., Soliman, M.T., Tuna, I. (2005). Accrual reliability,

earnings persistence and stock prices. Journal of Accounting and Economics, 39, 437–

485.

16.Scott, D.L. (2003). Wall Street Words: An A to Z guide to investment terms for today's

investor. Boston: Houghton Mifflin Company.

Financial Accounting – Course Assessment 1