finance and business models for community asset ownership #communityassests

TRANSCRIPT

An overview of the social investment journey

Hugh Rolo

Director of Innovation

Locality

My experience

www.thekeyfund.co.uk

www.adventurecapitalfund.org.uk

www.communityshares.org.uk

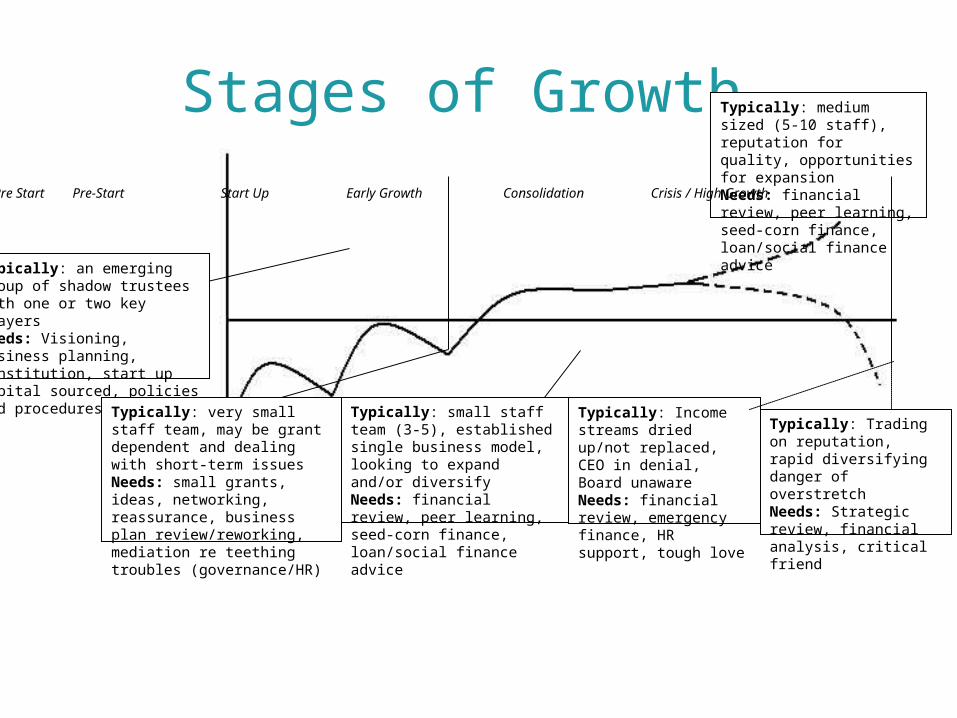

Stages of Growth

Typically: an emerging group of shadow trustees with one or two key playersNeeds: Visioning, business planning, constitution, start up capital sourced, policies and procedures

Typically: very small staff team, may be grant dependent and dealing with short-term issuesNeeds: small grants, ideas, networking, reassurance, business plan review/reworking, mediation re teething troubles (governance/HR)

Typically: small staff team (3-5), established single business model, looking to expand and/or diversifyNeeds: financial review, peer learning, seed-corn finance, loan/social finance advice

Typically: medium sized (5-10 staff), reputation for quality, opportunities for expansionNeeds: financial review, peer learning, seed-corn finance, loan/social finance advice

Typically: Income streams dried up/not replaced, CEO in denial, Board unawareNeeds: financial review, emergency finance, HR support, tough love

Typically: Trading on reputation, rapid diversifying danger of overstretchNeeds: Strategic review, financial analysis, critical friend

Pre-Pre Start Pre-Start Start Up Early Growth Consolidation Crisis / High Growth

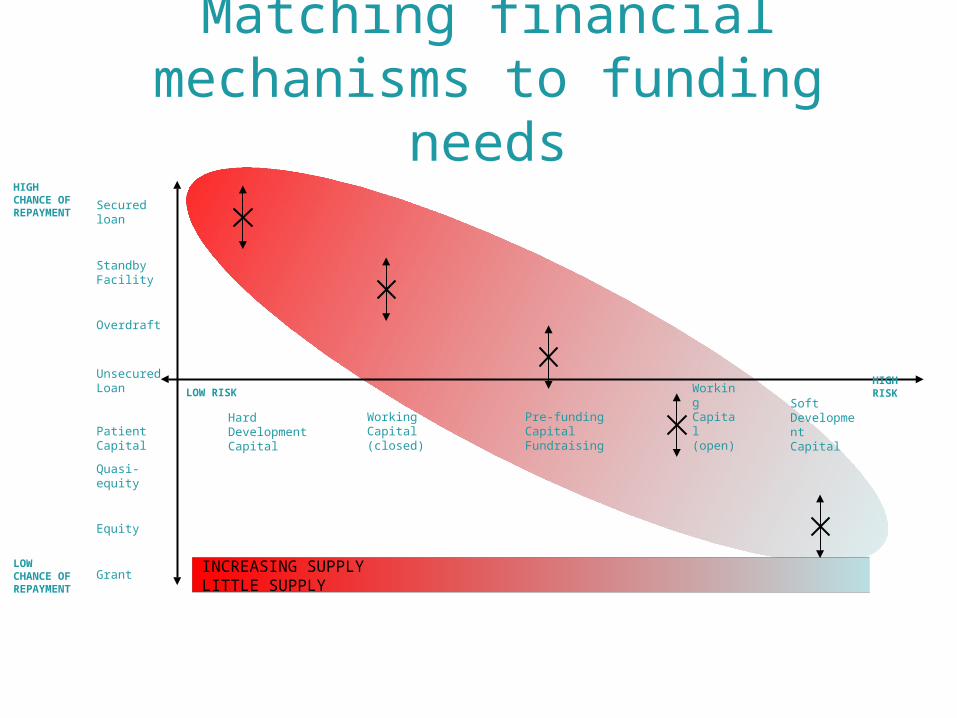

Matching financial mechanisms to funding needs

LOW RISK

Hard DevelopmentCapital

Working Capital (closed)

Pre-funding Capital Fundraising

Working Capital (open)

Soft Development Capital

HIGH RISK

INCREASING SUPPLY LITTLE SUPPLY

HIGH CHANCE OF REPAYMENT

LOW CHANCE OF REPAYMENT

Secured loan

Standby Facility

Overdraft

Unsecured Loan

Patient Capital

Quasi-equity

Equity

Grant

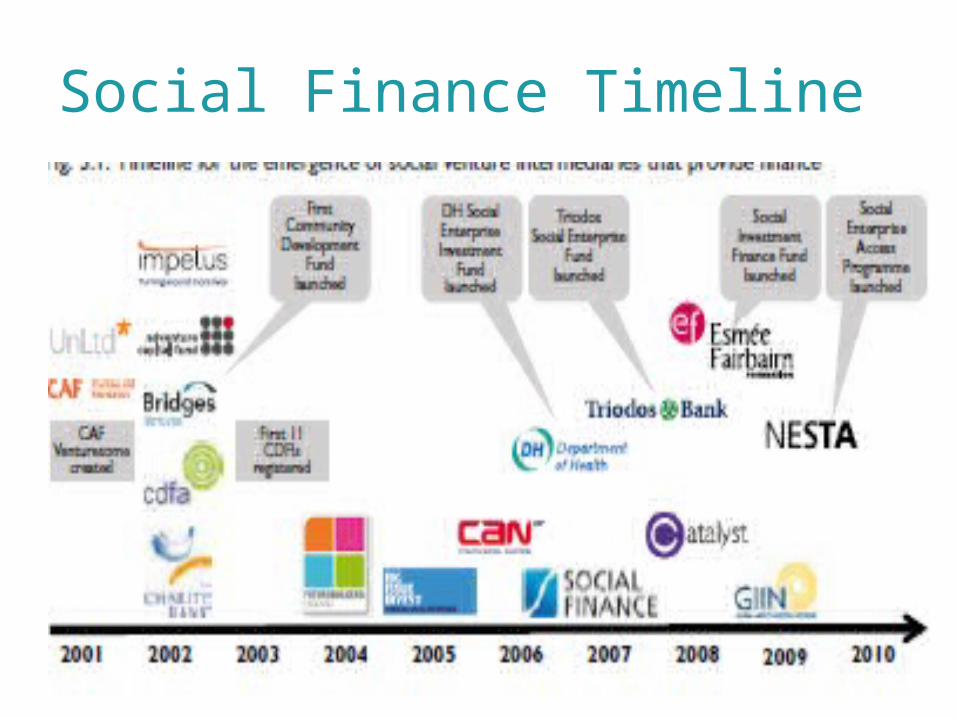

Social Finance Timeline

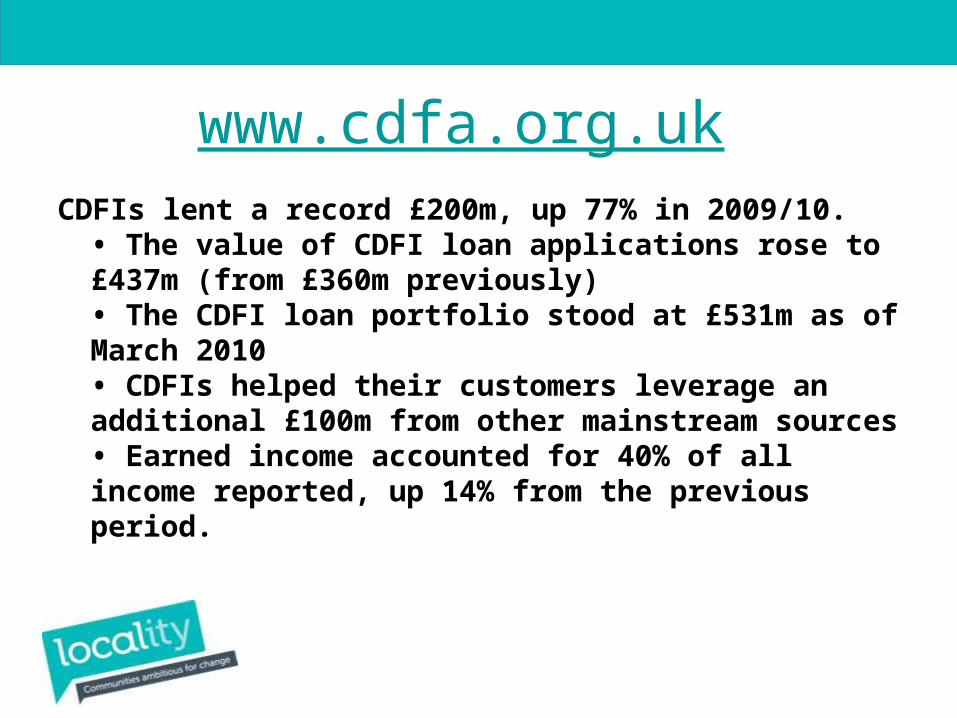

CDFIs lent a record £200m, up 77% in 2009/10. • The value of CDFI loan applications rose to £437m (from £360m previously)• The CDFI loan portfolio stood at £531m as of March 2010• CDFIs helped their customers leverage an additional £100m from other mainstream sources• Earned income accounted for 40% of all income reported, up 14% from the previous period.

www.cdfa.org.uk

Social Investment Business• Communitybuilders Fund• The Communitybuilders Fund, previously owned by the Department of Community and

Local Government is now an endowed fund, owned and administered by the Adventure Capital Fund. It supports neighbourhood-based, community-led organisations to become more sustainable through a mixture of loans, grants and business support.

• The fund is currently closed to new applications but we expect to be able to reopen within a few months.

• Social Enterprise Investment Fund• We manage the Social Enterprise Investment Fund (SEIF) with Local Partnerships, on

behalf of the Department of Health. SEIF is a fund that provides loans, grants and professional support to social enterprises involved in the delivery of health and social care services.

• The Adventure Capital Fund (ACF)• The Adventure Capital Fund is an ambitious style of funder for community enterprise. The

pioneering packages that we offer have the potential to transform neighbourhoods across the country.

• Futurebuilders England Fund• We manage the Futurebuilders England Fund on behalf of the Office for Civil Society. This

fund is a £215 million Fund that provides loan financing, often combined with grants and professional support, to third sector organisations in England that need investment to help them bid for, win and deliver public service contracts. The Futurebuilders England Fund is now currently closed for new applications.

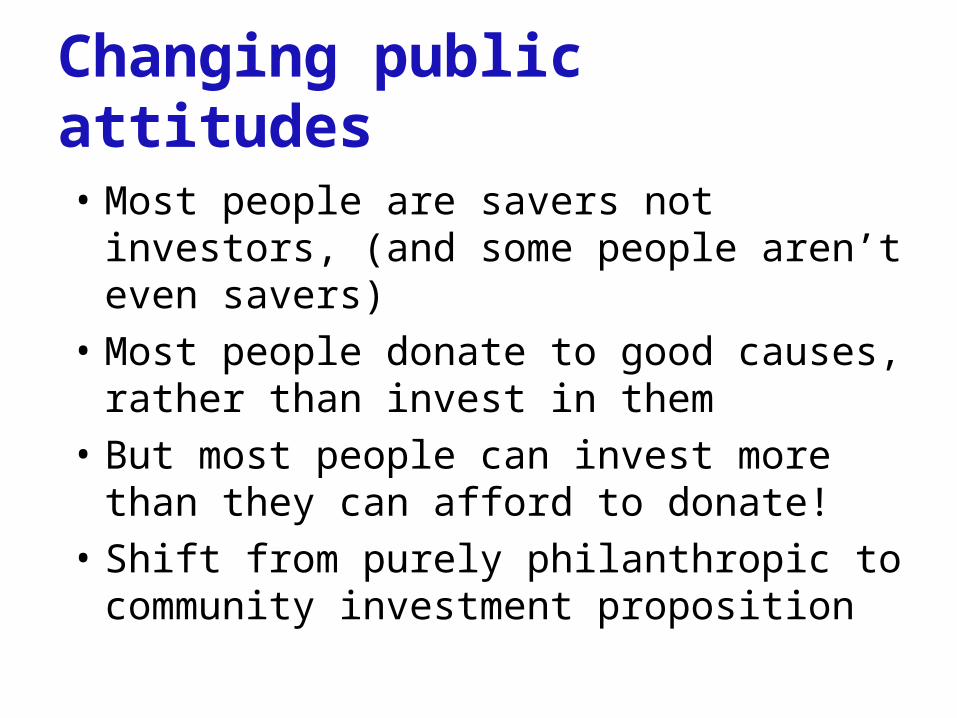

Changing public attitudes

• Most people are savers not investors, (and some people aren’t even savers)

• Most people donate to good causes, rather than invest in them

• But most people can invest more than they can afford to donate!

• Shift from purely philanthropic to community investment proposition

Growth in community share offers

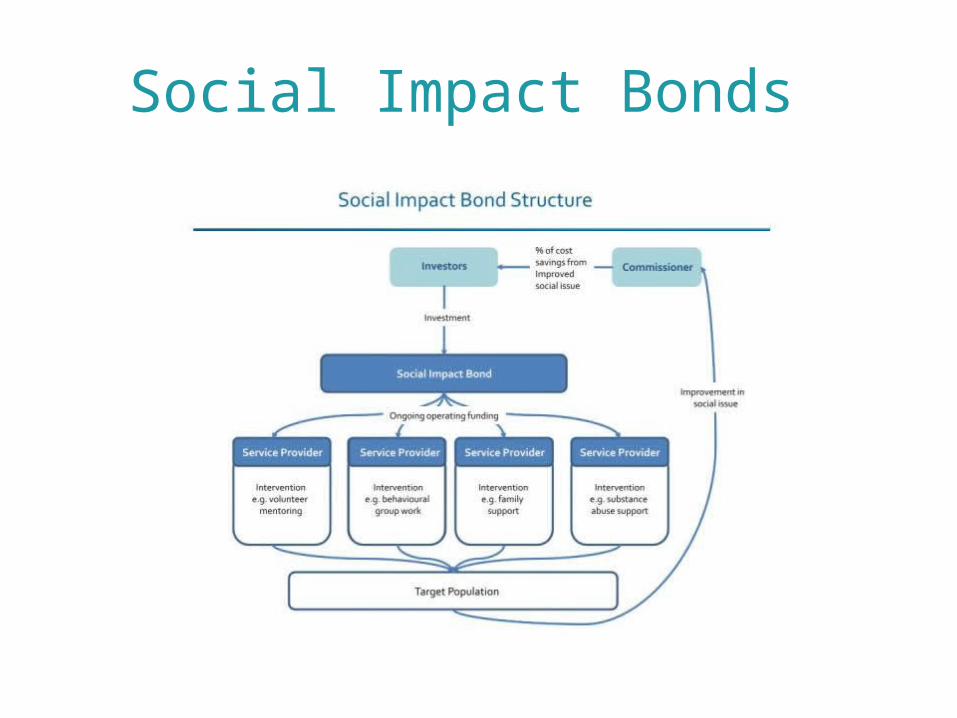

Social Impact Bonds

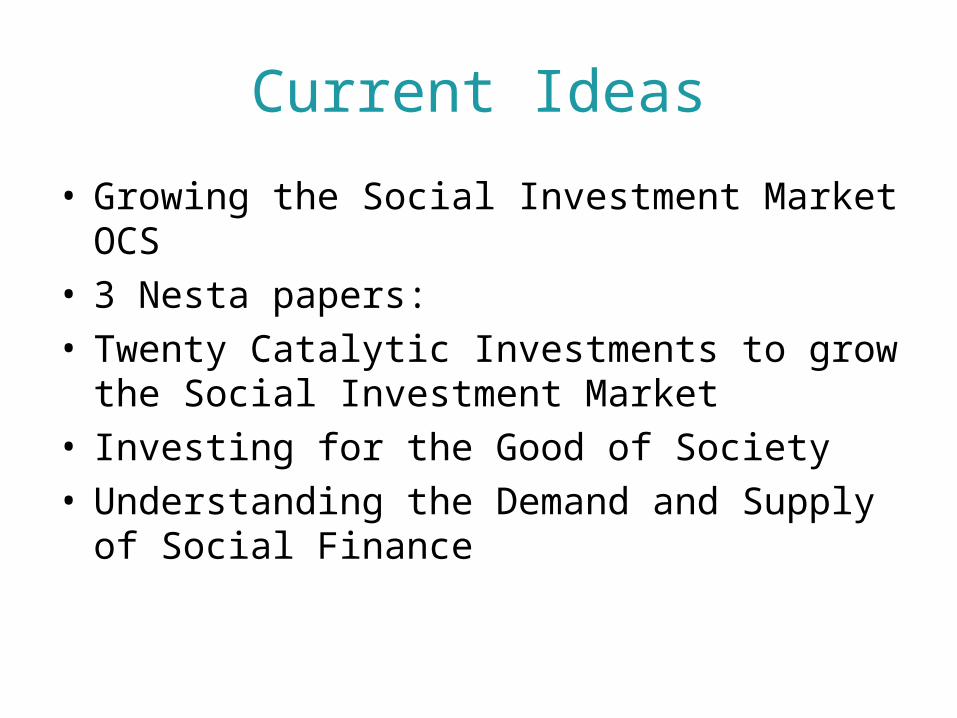

Current Ideas

• Growing the Social Investment Market OCS • 3 Nesta papers:• Twenty Catalytic Investments to grow the Social

Investment Market• Investing for the Good of Society• Understanding the Demand and Supply of Social

Finance

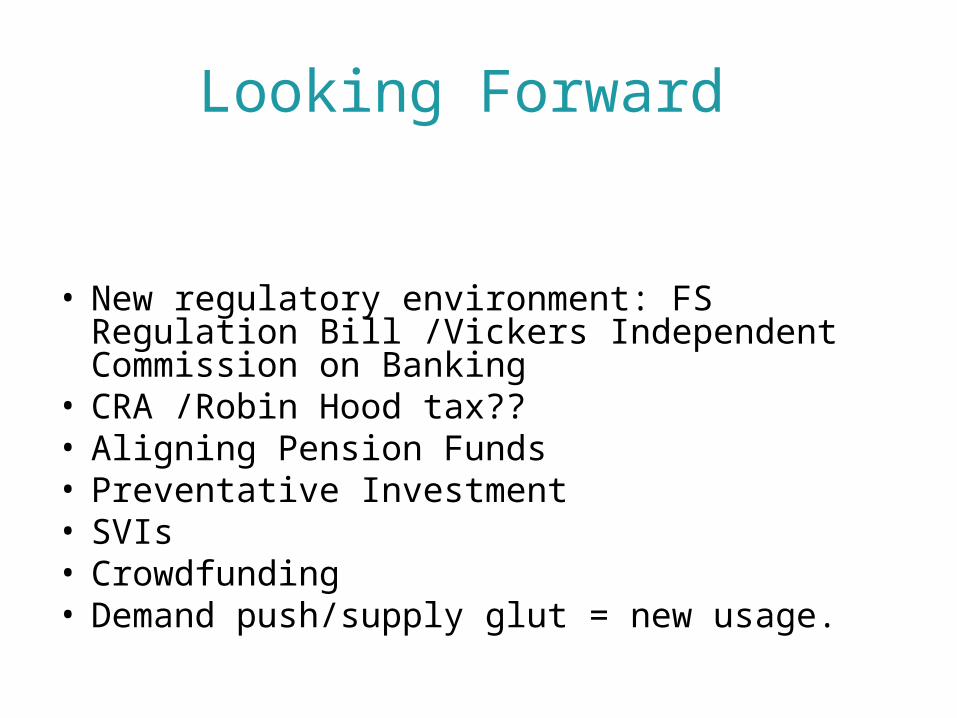

Looking Forward

• New regulatory environment: FS Regulation Bill /Vickers Independent Commission on Banking

• CRA /Robin Hood tax??• Aligning Pension Funds • Preventative Investment• SVIs • Crowdfunding • Demand push/supply glut = new usage.

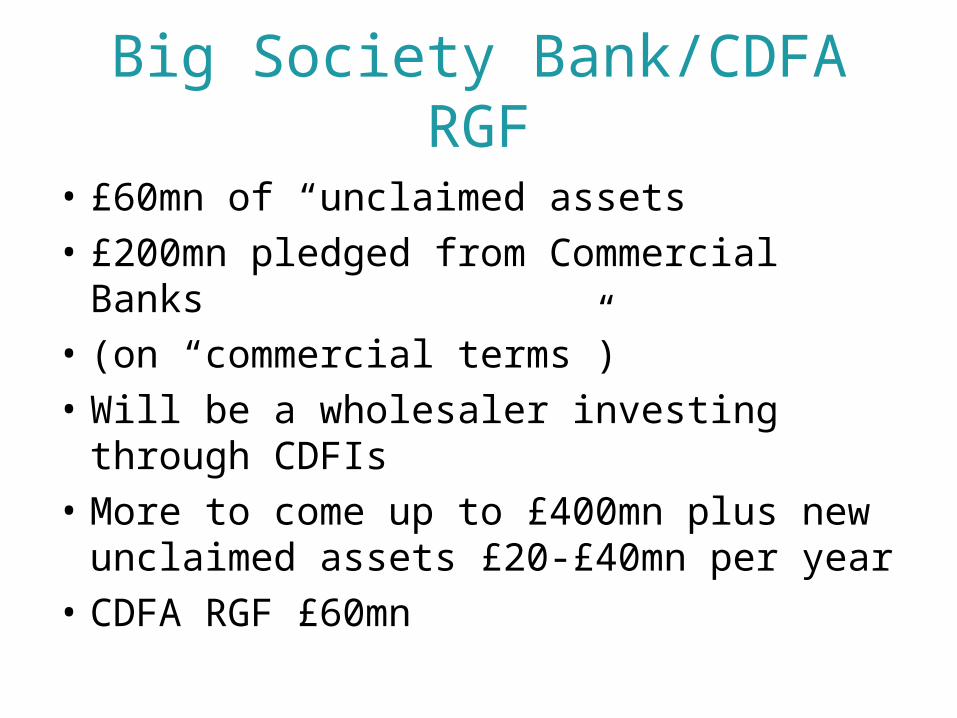

Big Society Bank/CDFA RGF

• £60mn of “unclaimed assets

• £200mn pledged from Commercial Banks

• (on “commercial terms”)

• Will be a wholesaler investing through CDFIs

• More to come up to £400mn plus new unclaimed assets £20-£40mn per year

• CDFA RGF £60mn

contact

• www.locality.org.uk

• www.communityshares.org.uk

LOCALITY CONFERENCE

in Manchester

November 1st and 2nd 2011

www.hebdenbridgetownhall.org.uk

Asset transfer and development funding: the Hebden Bridge experience

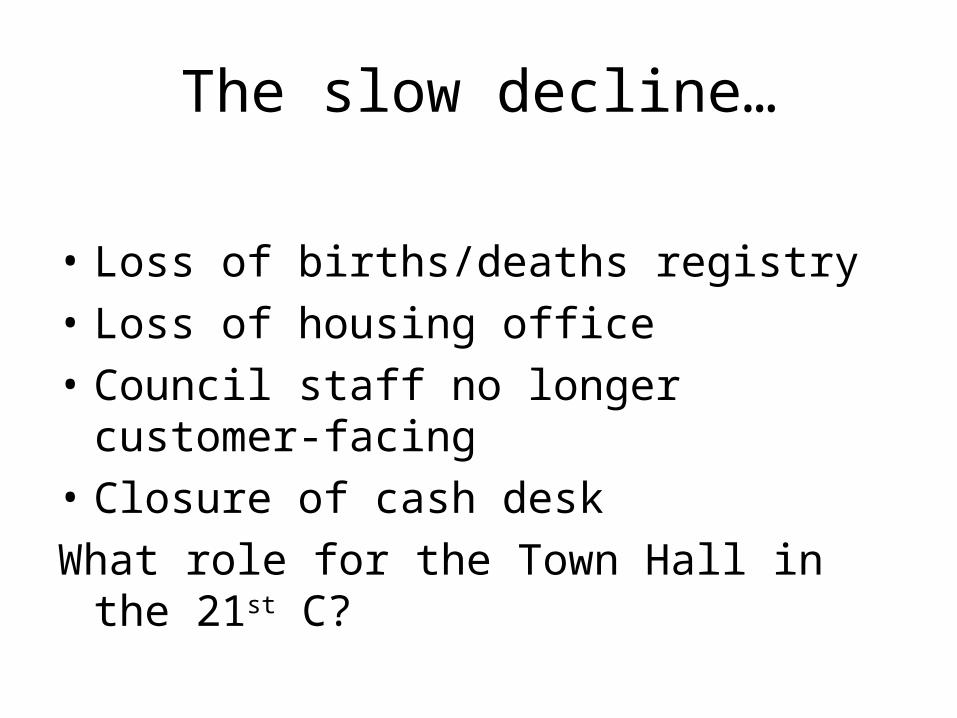

The slow decline…

• Loss of births/deaths registry

• Loss of housing office

• Council staff no longer customer-facing

• Closure of cash desk

What role for the Town Hall in the 21st C?

Community engagement

• 2004 Sale of HB adult ed building/toddler pool

• 2006 Town Hall Working party established in community• 2007 Quirk report: Making Assets Work• 2007 Community Assets programme• 2008 Establishment of HBCA, as charitable trust• 2009: Launch of Friends of the Town Hall• Summer 2009: Asset transfer submission• Dec 2009: Asset transfer agreed • April 2010 Asset transfer takes place

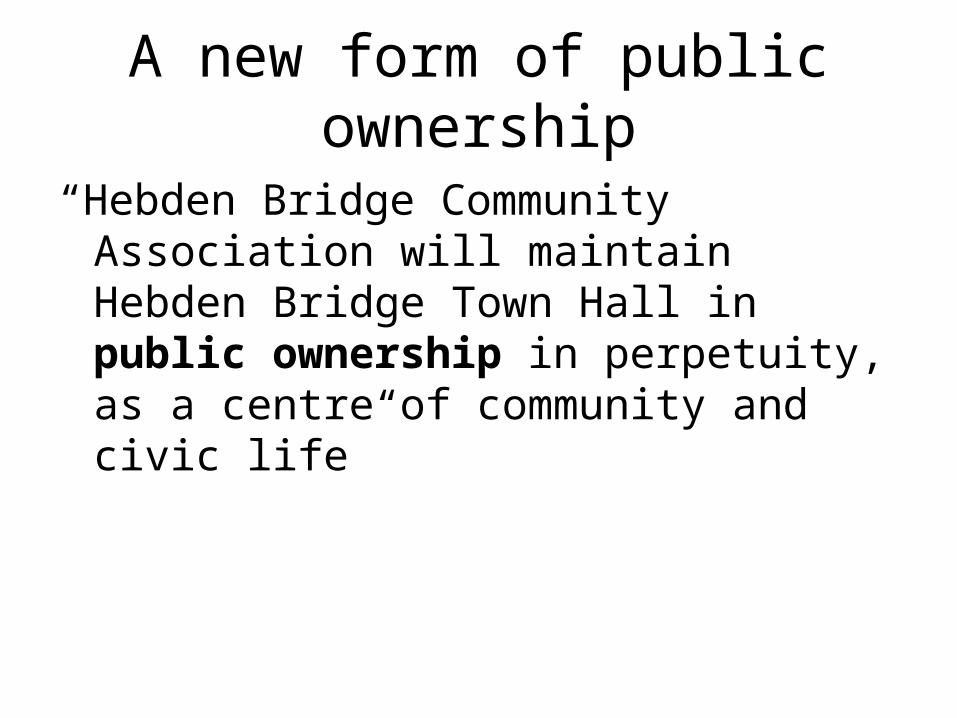

A new form of public ownership

“Hebden Bridge Community Association will maintain Hebden Bridge Town Hall in public ownership in perpetuity, as a centre of community and civic life”

A new form of public ownership

“Our concept of public ownership looks back to the earlier nineteenth century models of mutuality and common interest, as well as forward towards new 21st century models”

[Draft Community Participation and Inclusion Strategy, 2008]

A new form of public ownership

“Hebden Bridge Community Association will operate on the basis that it is demonstrably democratic and accountable”

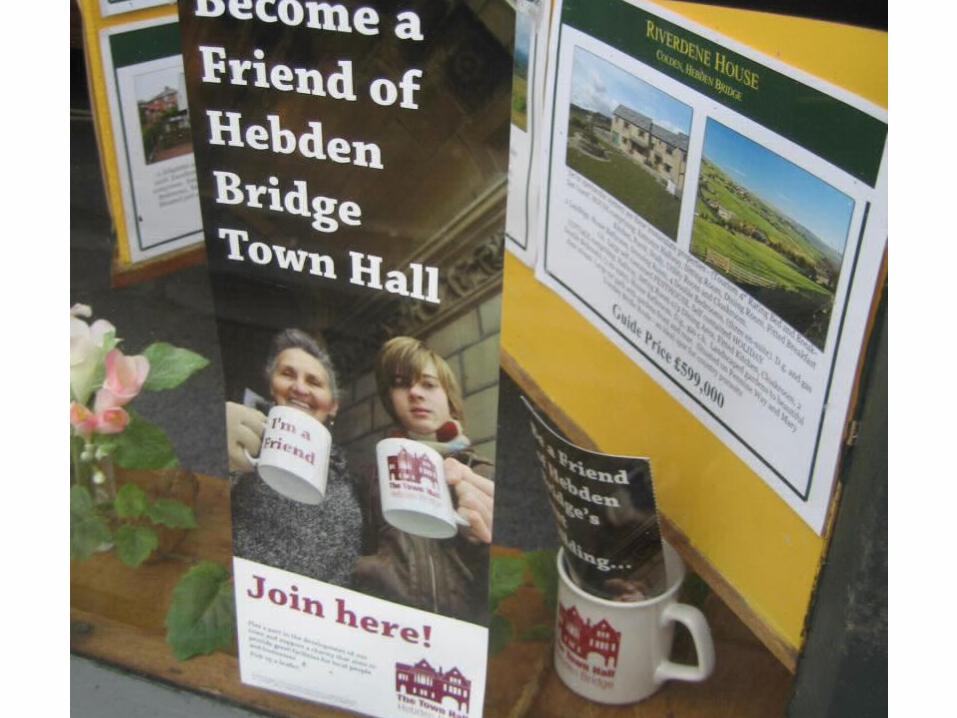

• Launch of the Friends scheme

• About 550 Friends/members at present

A new form of public ownership

Legal structure:

- Company limited by guarantee

- Registered charity

- Trustees/directors elected by members

Also considered:

- IPS Community benefit society

- CIC

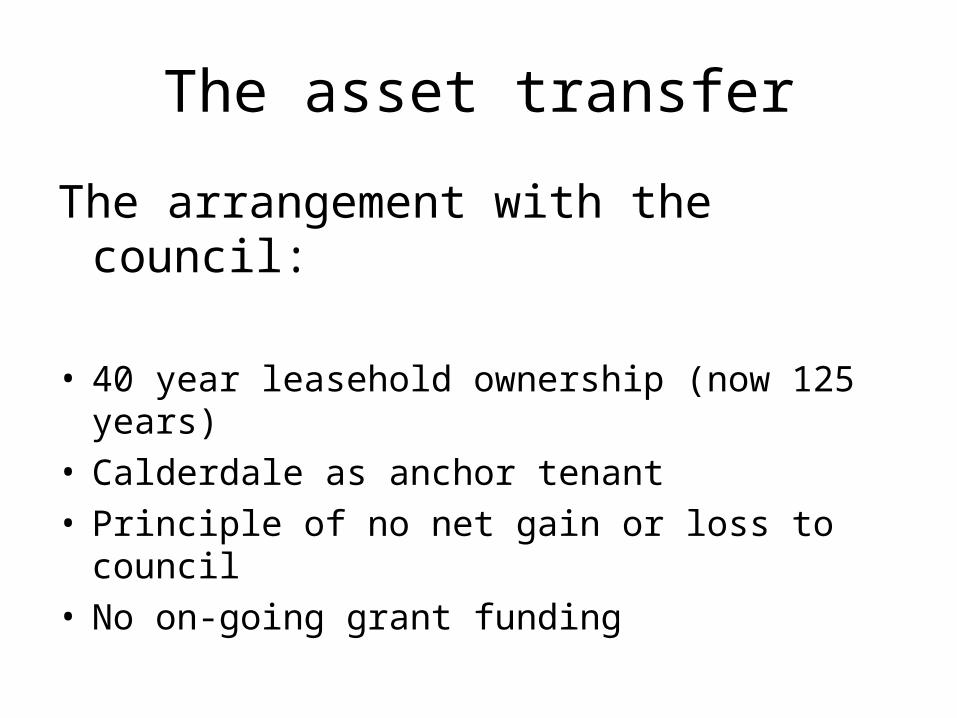

The asset transfer

The arrangement with the council:

• 40 year leasehold ownership (now 125 years)• Calderdale as anchor tenant• Principle of no net gain or loss to council• No on-going grant funding

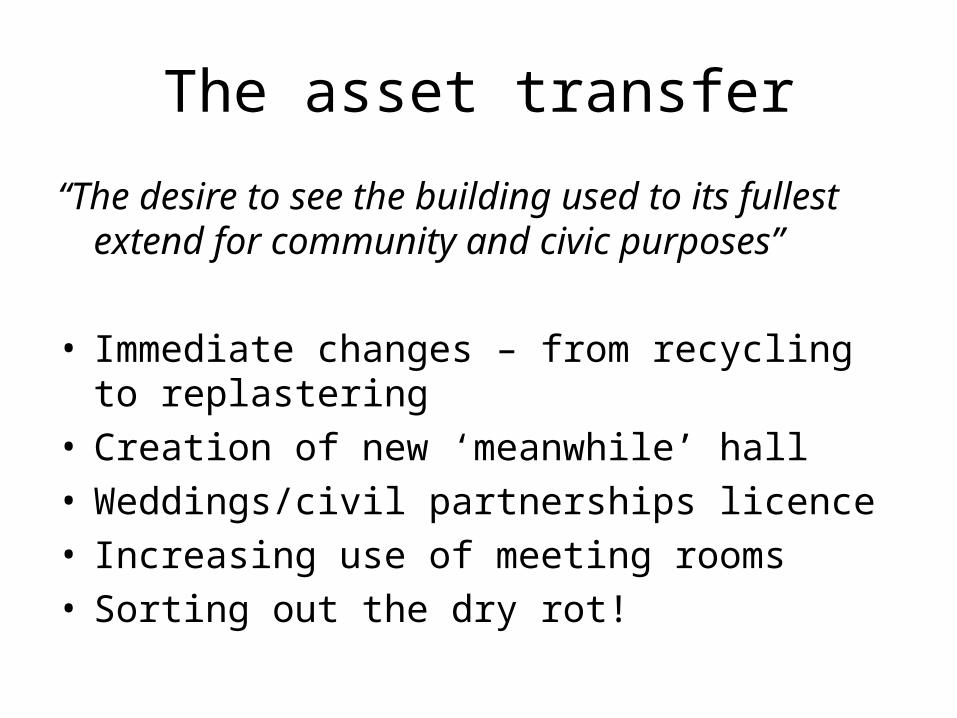

The asset transfer

“The desire to see the building used to its fullest extend for community and civic purposes”

• Immediate changes – from recycling to replastering

• Creation of new ‘meanwhile’ hall• Weddings/civil partnerships licence• Increasing use of meeting rooms• Sorting out the dry rot!

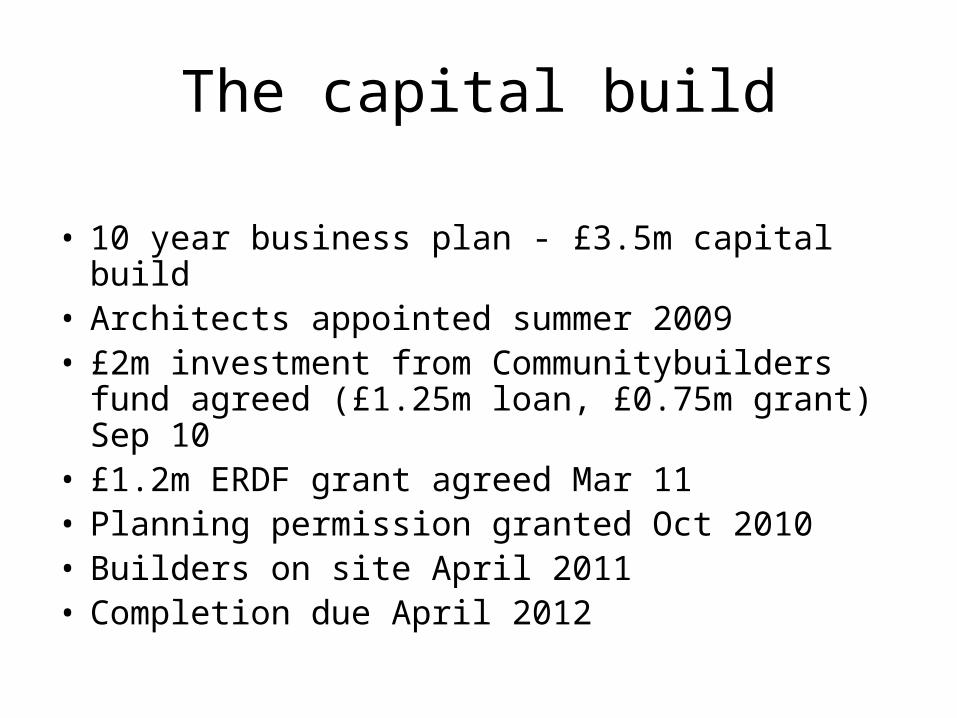

The capital build

“We are determined to ensure that the future of Hebden Bridge Town Hall is secured for the very long term”

• Working for long-term sustainability• Move away from dependency on anchor tenant• Make building DDA compliant• Provide much greater range of community facilities• Provide small enterprise facilities required

The capital build

• 10 year business plan - £3.5m capital build• Architects appointed summer 2009• £2m investment from Communitybuilders fund

agreed (£1.25m loan, £0.75m grant) Sep 10• £1.2m ERDF grant agreed Mar 11• Planning permission granted Oct 2010• Builders on site April 2011• Completion due April 2012

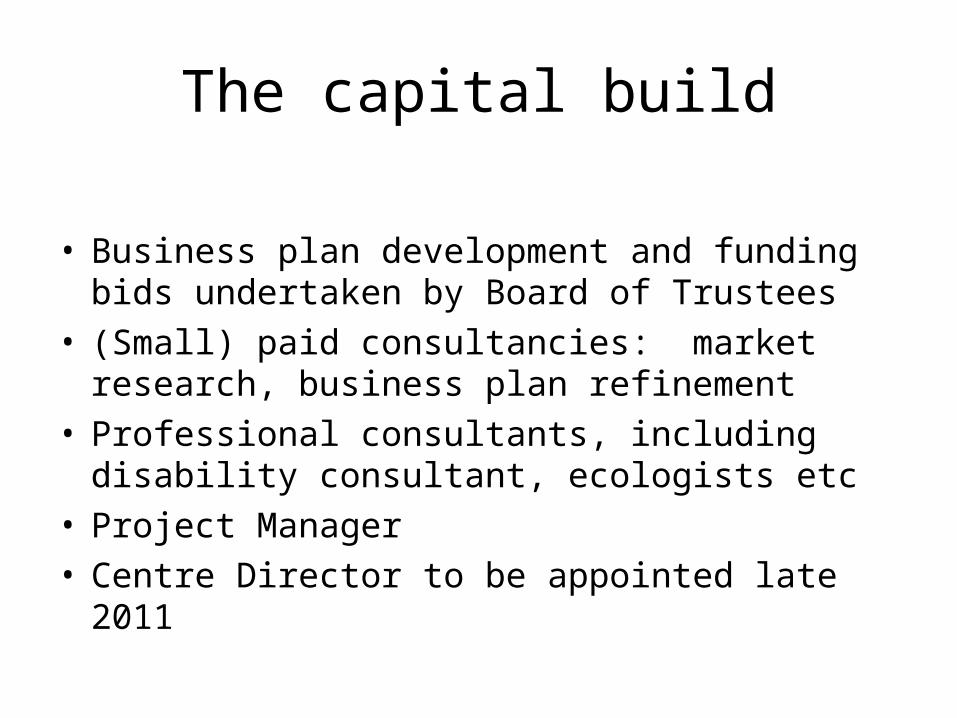

The capital build

• Business plan development and funding bids undertaken by Board of Trustees

• (Small) paid consultancies: market research, business plan refinement

• Professional consultants, including disability consultant, ecologists etc

• Project Manager• Centre Director to be appointed late 2011

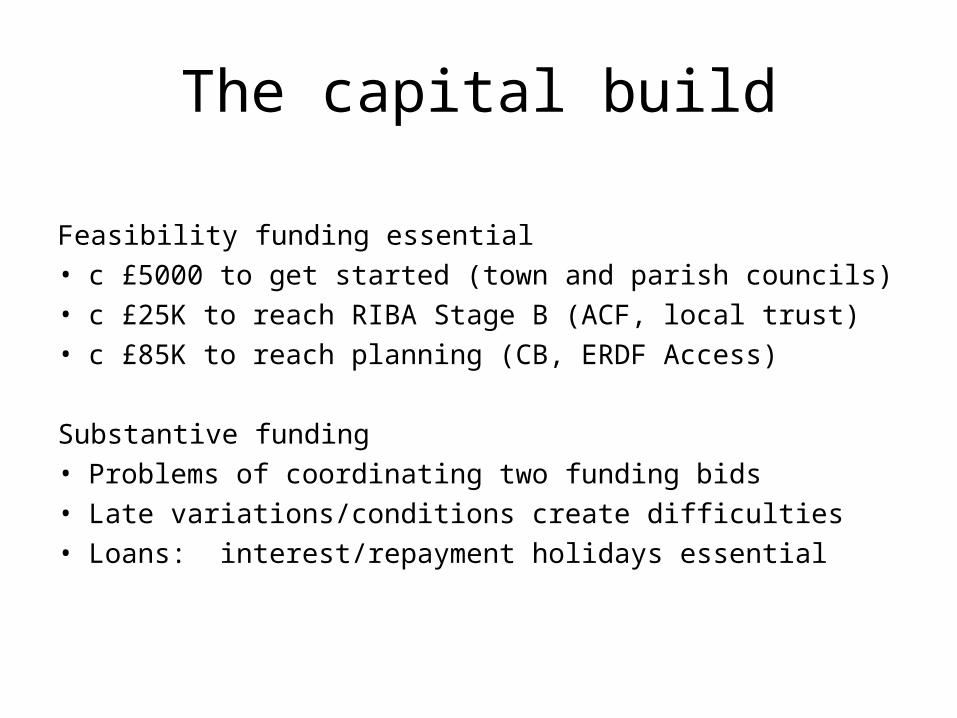

The capital build

Feasibility funding essential• c £5000 to get started (town and parish councils)• c £25K to reach RIBA Stage B (ACF, local trust)• c £85K to reach planning (CB, ERDF Access)

Substantive funding• Problems of coordinating two funding bids• Late variations/conditions create difficulties• Loans: interest/repayment holidays essential

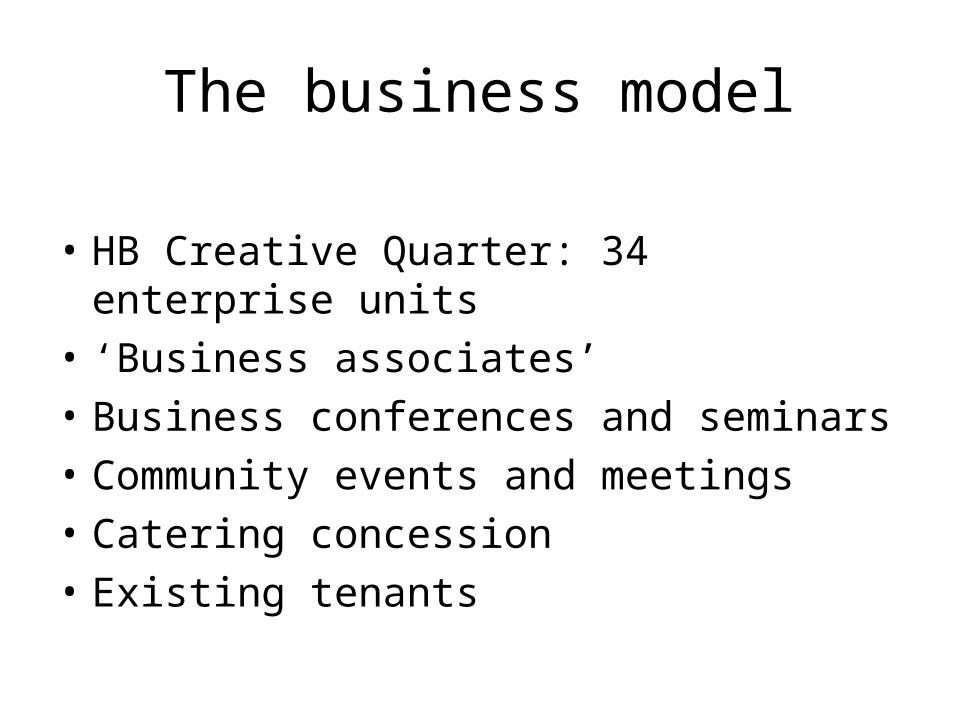

The business model

• HB Creative Quarter: 34 enterprise units

• ‘Business associates’

• Business conferences and seminars

• Community events and meetings

• Catering concession

• Existing tenants

The challenges

• Attracting business/sales

• Running an efficient operation

• Meeting funders’ criteria

• Meeting other responsibilities

• Servicing the £1.25m borrowing

Should communities really have to do this?

• Employing staff (including TUPE transfer)• VAT accounting• Health and safety• Charitable legislation• Company law• Licences etc for public buildings• Building maintenance; capital works• Cash flow… money in the bank when it’s

needed

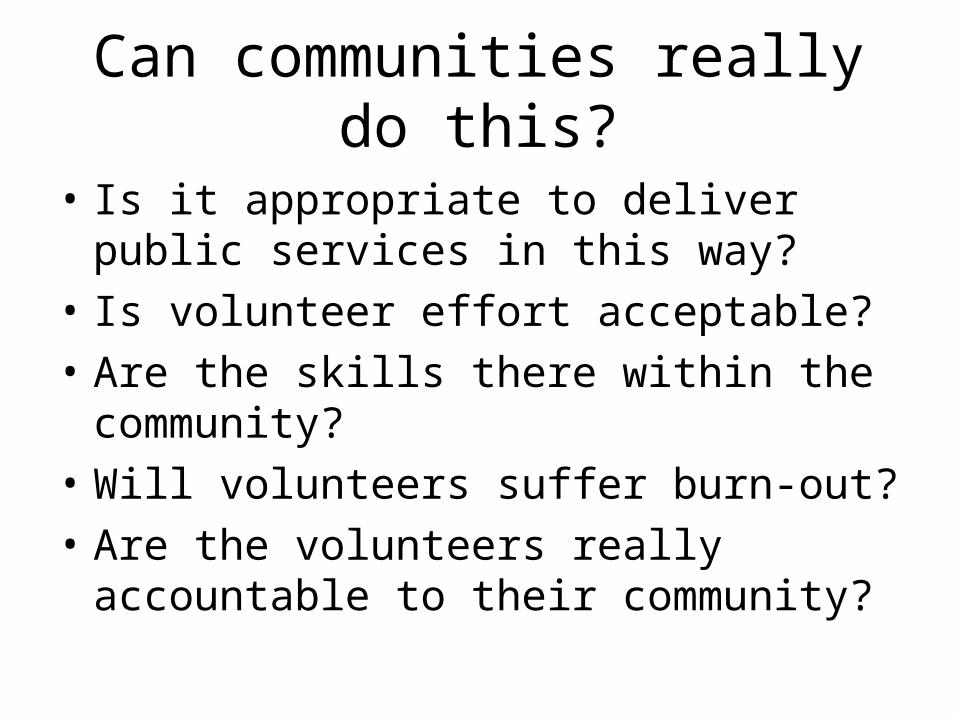

Can communities really do this?

• Is it appropriate to deliver public services in this way?

• Is volunteer effort acceptable?

• Are the skills there within the community?

• Will volunteers suffer burn-out?

• Are the volunteers really accountable to their community?

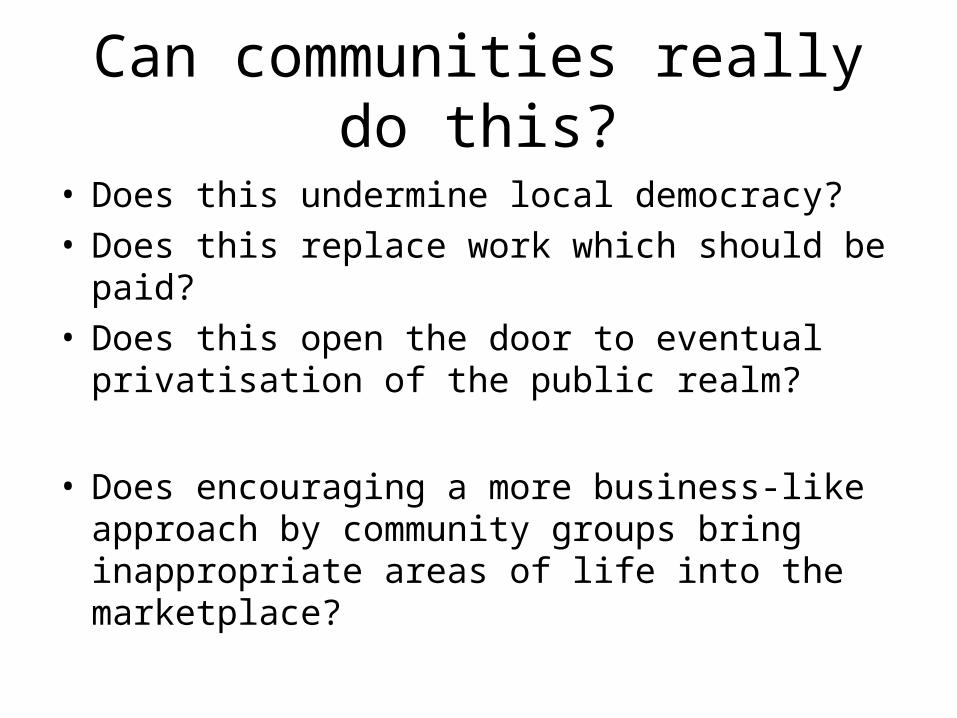

Can communities really do this?

• Does this undermine local democracy?• Does this replace work which should be paid?• Does this open the door to eventual privatisation

of the public realm?

• Does encouraging a more business-like approach by community groups bring inappropriate areas of life into the marketplace?

Moving forward

• Other public buildings potentially at risk

• Look to community’s own financial resources• Work on our democracy• Offer something back for others

Where to find out more

www.hebdenbridgetownhall.org.uk

Asset transfer and development funding: the Hebden Bridge experience

Joseph Rowntree Foundation

Seminar

4th May 2011

Tony CurtisBusiness Support

Advisor

Investment readiness and the social investment journey

•a social enterprise wholly owned by a charity (Adventure Capital Fund)

•a large scale UK social investor

•manages nearly £400m of investment

•works to help civil society organisations do more of what they do best – supporting people and communities most in need

•aims to transform the civil society sector by helping to create powerful, well capitalised and thriving organisations

The Social Investment Business

• loans / grants to third sector providers

• business support / consultancy to third sector providers including consortia & social enterprises

• services to national and local commissioners

• interim management

• training & mentoring

• sharing ideas and approaches

Our Services to Civil Society Organisations

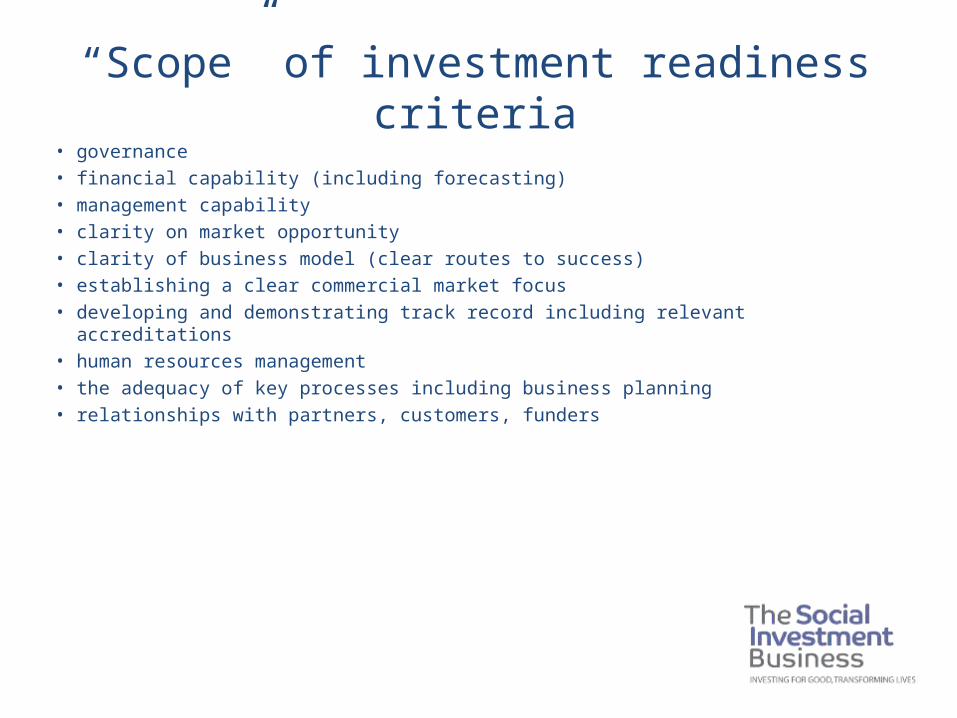

• governance• financial capability (including forecasting)• management capability• clarity on market opportunity• clarity of business model (clear routes to success)• establishing a clear commercial market focus• developing and demonstrating track record including relevant accreditations• human resources management• the adequacy of key processes including business planning• relationships with partners, customers, funders

“Scope” of investment readiness criteria

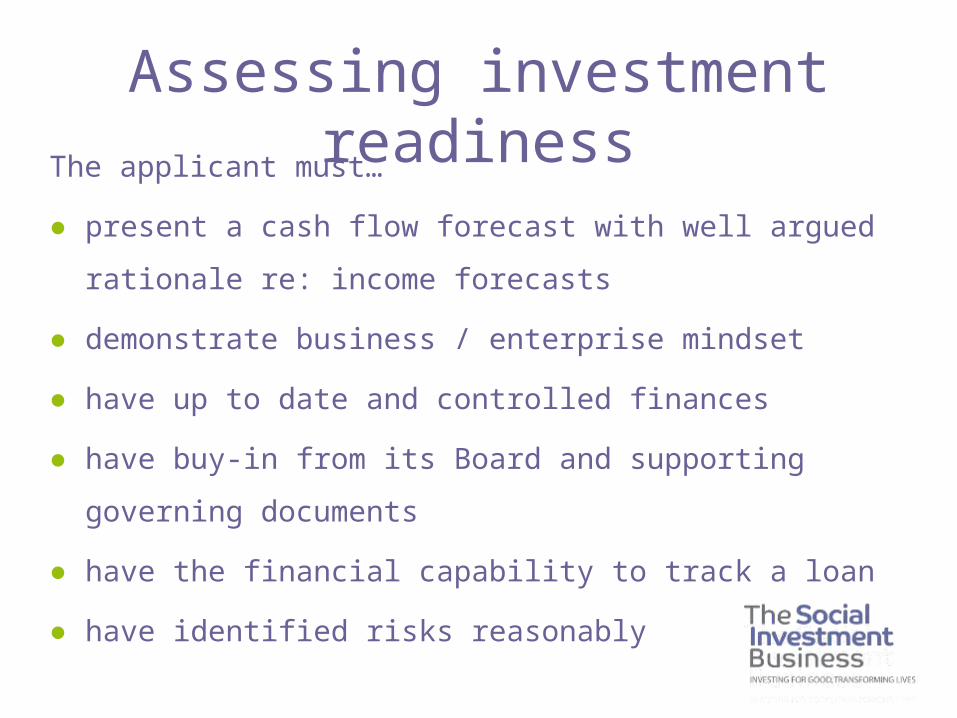

The applicant must…

● present a cash flow forecast with well argued rationale re:

income forecasts

● demonstrate business / enterprise mindset

● have up to date and controlled finances

● have buy-in from its Board and supporting governing

documents

● have the financial capability to track a loan

● have identified risks reasonably

Assessing investment readiness

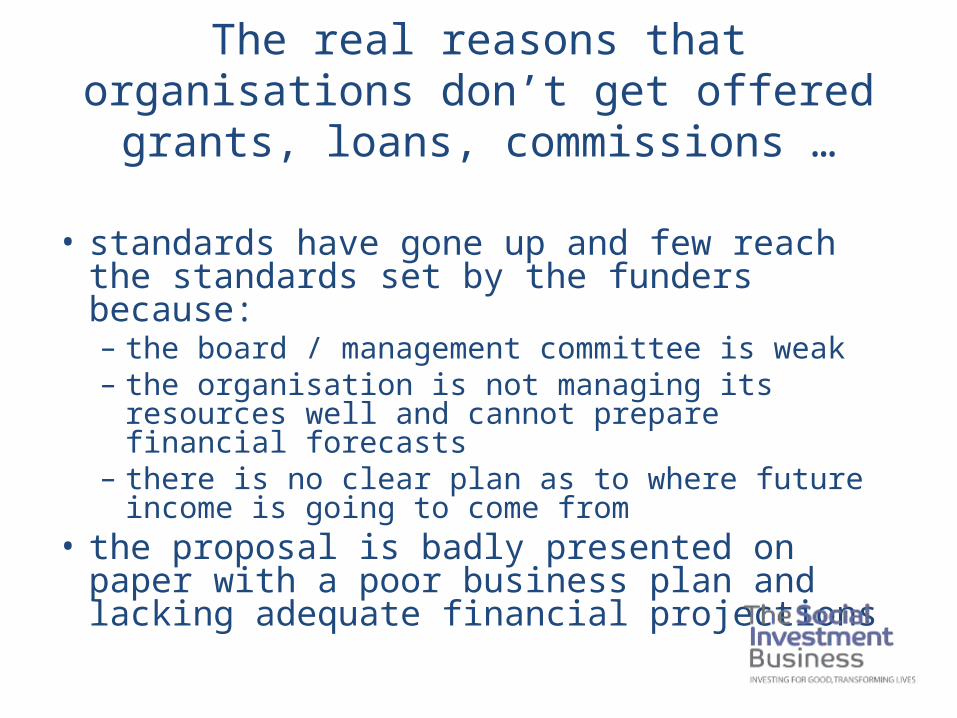

The real reasons that organisations don’t get offered grants, loans, commissions …

• standards have gone up and few reach the standards set by the funders because:– the board / management committee is weak– the organisation is not managing its resources

well and cannot prepare financial forecasts– there is no clear plan as to where future income is

going to come from • the proposal is badly presented on paper with

a poor business plan and lacking adequate financial projections

• achieving investment readiness• diversifying income streams• securing accreditations and quality marks• getting balance right – “business like” but “mission

driven”• refreshing, reviewing, upgrading and upskilling the board• articulating clearly why they are still here and still

needed

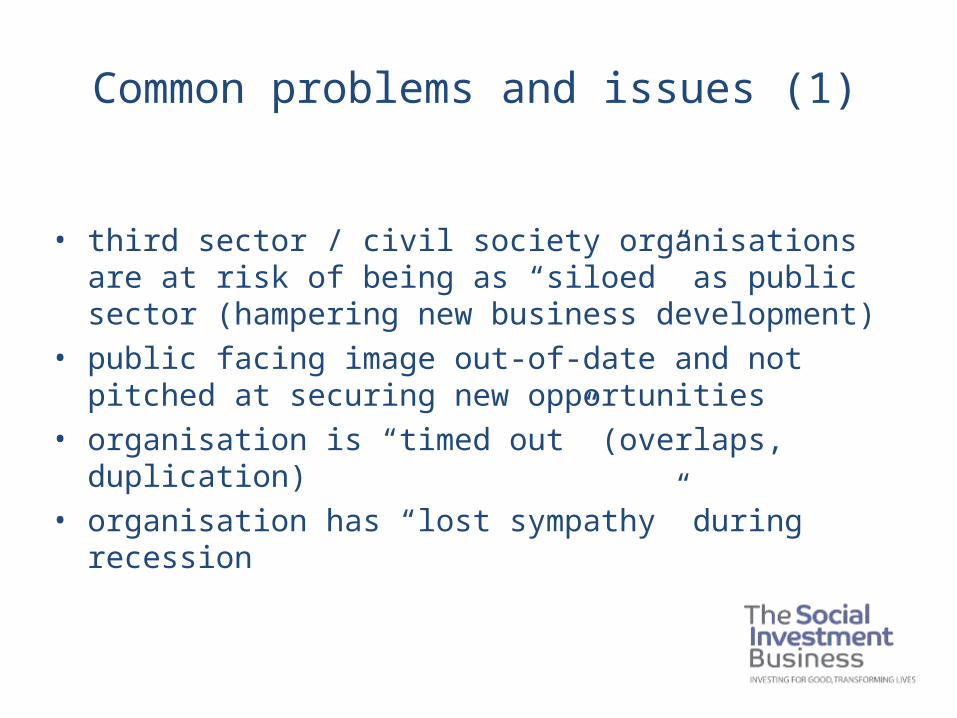

What the best organisations are doing

• third sector / civil society organisations are at risk of being as “siloed” as public sector (hampering new business development)

• public facing image out-of-date and not pitched at securing new opportunities

• organisation is “timed out” (overlaps, duplication)• organisation has “lost sympathy” during recession

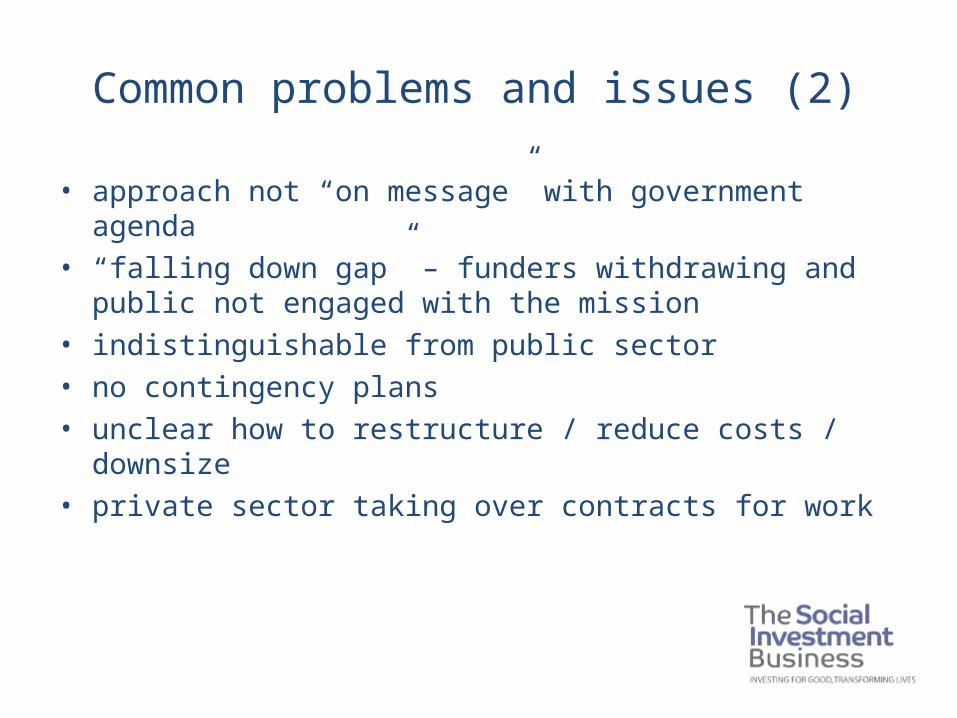

Common problems and issues (1)

• approach not “on message” with government agenda• “falling down gap” – funders withdrawing and public not

engaged with the mission• indistinguishable from public sector• no contingency plans• unclear how to restructure / reduce costs / downsize• private sector taking over contracts for work

Common problems and issues (2)

Contact details:-

www.thesocialinvestmentbusiness.org

Tel: 0191 261 5200

shineraising aspirations, creating opportunities

Risks, Challenges, Success Factors

Community Enterprise &What it Means To Take on Debt

?

Public Services Vol/Comm Social Business

Shine

Atlanta

60+

2005

Social Enterprise

“People, not spreadsheets, make things happen”

2007/8

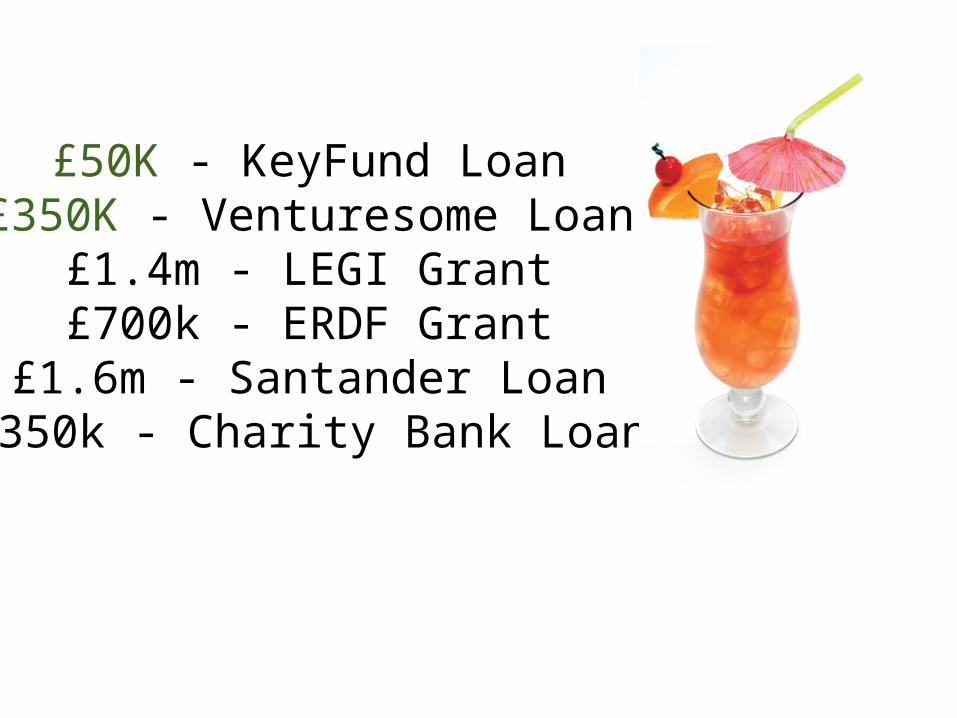

£50,000

£50K - KeyFund Loan£350K - Venturesome Loan

£1.4m - LEGI Grant£700k - ERDF Grant

£1.6m - Santander Loan£350k - Charity Bank Loan

Construction / Renovation

AutoPilot

Partial Resource

Full Team

balAnce

focus: market, cash

people

next?