final-accounts 001

TRANSCRIPT

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 1/16

Final Accounts

TARIQ HASSAN

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 2/16

Lesson objectives

By the end of the lesson, students should be

able to: -

Understand and construct a Trading Profit & LossAccount

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 3/16

Introduction

All companies or corporations must provide a

set of final accounts consisting of the

following: - Profit and Loss Account

Balance Sheet

Cash Flow Statement

Which stakeholders do you think would beinterested in a company¶s final accounts?

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 4/16

Profit & Loss Account (P&L Account)

This is a financial statement of a firms trading

over a period of time (usually a year).

There are three sections to a P&L Account. Trading Profit and Loss Account

Profit and Loss Account

Appropriation Account

Also known as Income Statements

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 5/16

Trading, Profit and LossAccount

This account represents the top of the P&L

account. It shows the difference in sales

revenue and the direct costs of trading. Itshows the gross profit of a business.

Gross Profit = Sales Revenue ± Cost of Goods Sold

Cost of sales = opening stock + purchases ± closing

stock

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 6/16

Example (figur es in $)

Trading Account for Company Y for Year Ended 31st December 2008

Sales 3600

Cost of Goods Sold

Opening Stock 1000

Purchases 2000

Closing Stock 1800

1200

Gross Profit 2400

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 7/16

Improving Gross Profit

Use cheaper suppliers

Increase the selling price

Use marketing strategies

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 8/16

Profit & Loss Account

This account shows the operating profit and

net profit of the business.

The gross profit figure is used to deduct allexpenses to calculate the operating profit.

Operating Profit= Gross Profit - Expenses

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 9/16

Examples of businessexpenses

Administration charges

Utility bills

Insurance Interest on bank loans

Marketing costs

Rent

Management salaries Stationer y costs

Transport costs

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 10/16

Example- Profit & Loss Account for Florists-

R-Us year ended 31st December 2008

$ $

Sales Revenue 450000

Cost of sales 200000

Gross Profit 250000

Less Expenses

Rent 80000

Utility bills 50000

Other overheads 30000

160000

Operating profit 90000

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 11/16

How to improve operatingprofit

Reduce rent

Heating and Lighting costs

Reviewing administration costs

The business may also have non-operating income

If the business does not have any non-operating

profit then operating profit is equal to the net profit. Interest payable/ received and Corporation Tax is

shown separately to the other expenses

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 12/16

Example$

Sales Revenue 450000

Cost of sales (200000)

Gross Profit 250000

Less Expenses (160000)

Operating profit 90000

Plus non operating

income

5000

Profit befor e inter estand tax

95000

Less Inter estpayable

(8000)

Net Profit 87000

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 13/16

Appropriation Account

This is the third part of the P&L account.

There are three parts to this account Taxation

Dividends Retained Profit

The company has no power over how much tax they pay, however they can decide how the profits are

shared out. The share of profits is decided by the directors and

approved by the AGM.

Dividends are usually paid biannually

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 14/16

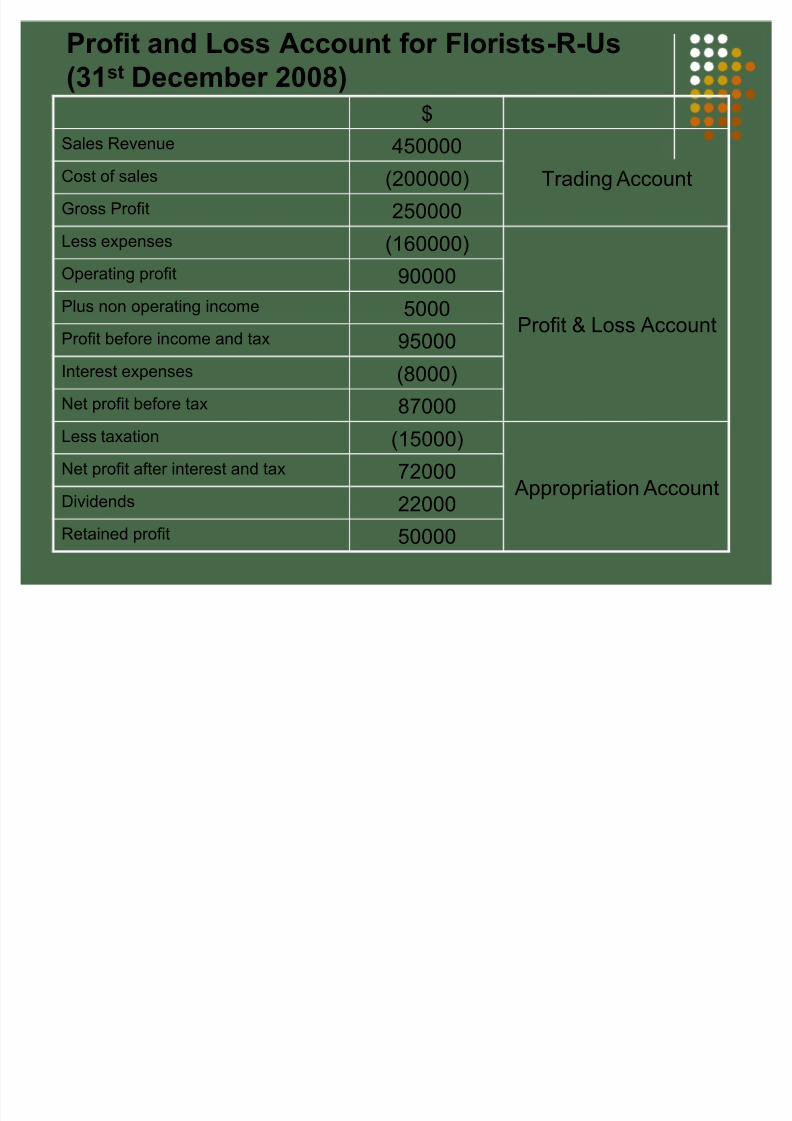

Profit and Loss Account for Florists-R-Us(31st December 2008)

$

Sales Revenue 450000

Trading AccountCost of sales (200000)

Gross Profit 250000

Less expenses (160000)

Profit & Loss Account

Operating profit 90000Plus non operating income 5000

Profit before income and tax 95000

Interest expenses (8000)

Net profit before tax

87000Less taxation (15000)

Appropriation AccountNet profit after interest and tax 72000

Dividends 22000

Retained profit 50000

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 15/16

Ahmed Educational Books LtdProfit & Loss Account for Ahmed Educational Books Ltd For Year Ended 31 December

2008

Year 2 ($000) Year 1 ($000)

Sales (a) 450

Cost of sales 200 (b)Gross Profit 300 270

Expenses 100 90

Net Profit Before Interest

& Tax

(c) 180

Interest Payable 10 0

Taxation 48 (d)

Net Profit after Interest &

Tax

142 135

Dividends 10 15

Retained Profit 132 (5)

8/7/2019 final-accounts 001

http://slidepdf.com/reader/full/final-accounts-001 16/16

Limitations of P&L accounts

Historical data rather than what will happen in

the future.

Window dressing can take place No standard format