accounts ppt (final)

TRANSCRIPT

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 1/30

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 2/30

In relation toSALES

In relation toINVESTMENT

1. Gross Profit Ratio2. Operating Expense ratio

3. Operating profit ratio

4. Net Profit ratio

1. Return on Investment2. Return on capital employed

3. Return on shareholders fund

4. Return on Total Assets

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 3/30

Mar 2010 Mar 2009 Mar 2008 Mar 2007 Mar 2006

Gross ProfitRatio 31.36 33.69 37.7 39.84 38.81

Operating

Expense ratio 64.6 62.46 58.24 60.6 61.13

Operating Profit

ratio 35.7 37.68 41.94 39.61 38.88

Net Profit Ratio 19.96 21.09 23.43 23.53 22.78

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 4/30

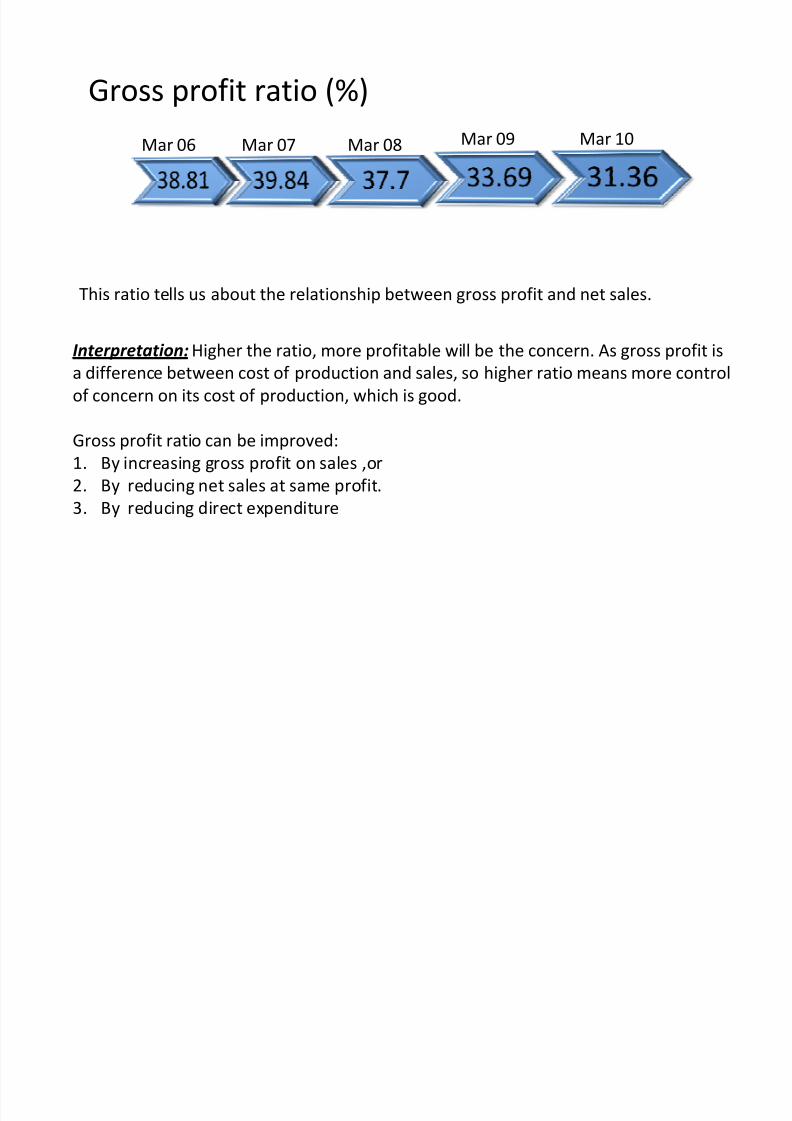

Gross profit ratio (%)

This ratio tells us about the relationship between gross profit and net sales.

Interpretation:Higher the ratio, more profitable will be the concern. As gross profit is

a difference between cost of production and sales, so higher ratio means more control

of concern on its cost of production, which is good.

Gross profit ratio can be improved:

1. By increasing gross profit on sales ,or

2. By reducing net sales at same profit.

3. By reducing direct expenditure

Mar 06 Mar 07 Mar 08 Mar 09 Mar 10

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 5/30

Gross profit ratio

From 2006 to 2007, Gross profit ratio increases

from 38.81 % to 39.84 % but after 2007 it is

continuously declining i.e. 39.84% (2007) to

31.36% (2010).

It is not a good sign of profitability means company

is losing its control over cost of production.

Companys COP is increasing every year but salesare not increasing at same rate as that of COP.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 6/30

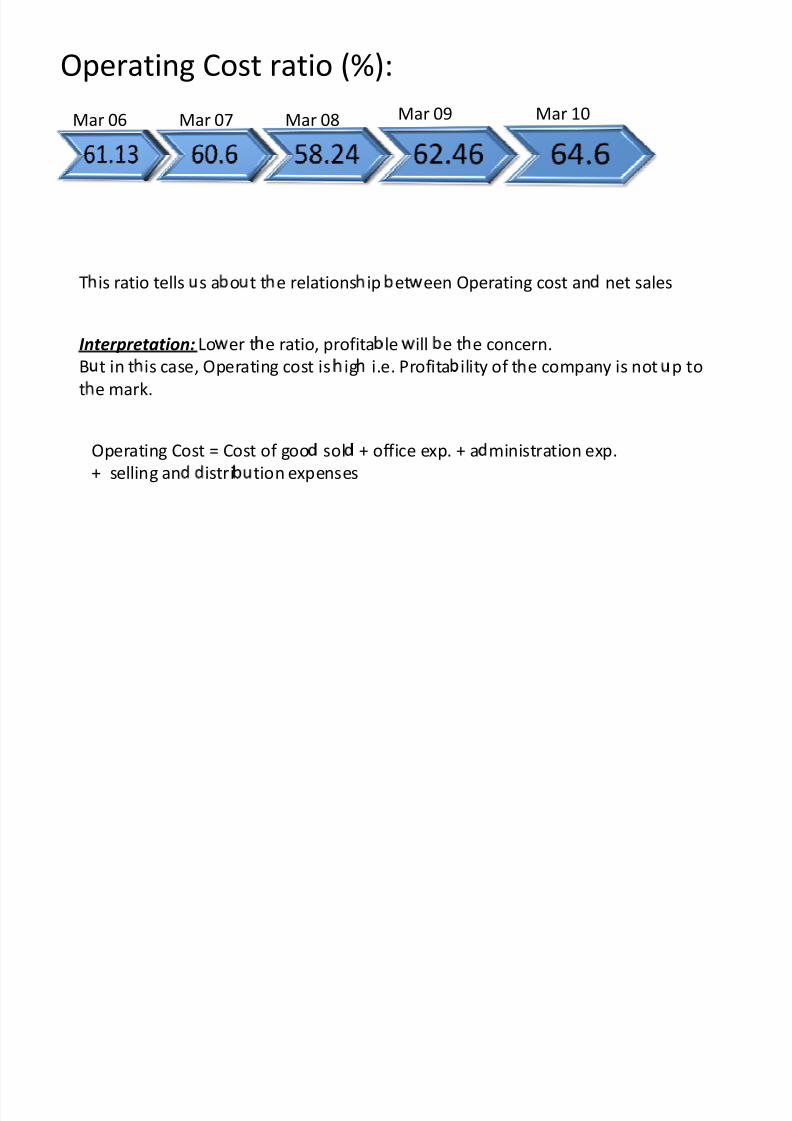

Operating Cost ratio (%):

T is ratio tells s a o t t e relations ip et een Operating cost an net sales

Interpretation: Lo er t e ratio, profita le ill e t e concern.

B t in t is case, Operating cost is ig i.e. Profita ility of t e company is not p to

t e mark.

Mar 09 Mar 10Mar 06 Mar 07 Mar 08

Operating Cost = Cost of goo sol + office exp. + a ministration exp.

+ selling an istri tion expenses

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 7/30

Operating Cost ratio

Initially Operating cost ratio was declining (2006

to 2008), but after 2008 it again startedincreasing which shows poor profitability of

the concern.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 8/30

Operating Profit ratio:

This ratio tells us about relationship between Operating profit and net sales.

Interpretation:Higher the ratio, more profitable will be the concern.

In this case, ratio initially was increasing, then started declining which shows poor

profitability of concern.

Mar 06 Mar 07 Mar 08 Mar 09 Mar 10

Operating Profit = Sales Operating cost (i.e. Cost of good sold + office exp. +

administration exp. + selling and distribution expenses)

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 9/30

Net Profit ratio (%):

This ratio shows the relationship between net profit and net sales.

Interpretation: Higher the ratio, more profitable will be the concern. Net profit

should be enough to pay dividends and make necessary appropriations.

Net profit ratio can be improved by:

Increasing gross profit Increasing sales

Reducing Indirect expenses (Office exp.+ administrative exp. + selling exp.)

ar arar 8ar 7ar 6

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 10/30

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 11/30

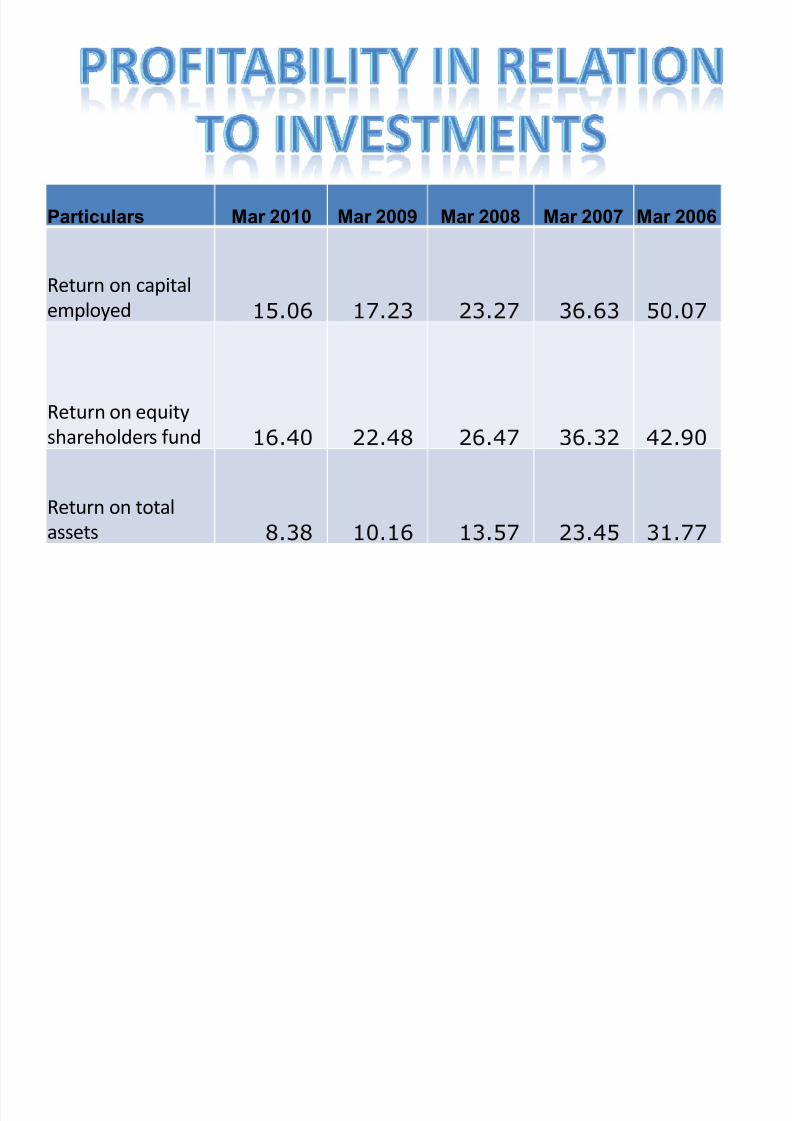

Return on capital Employed (%):

ar

ar 1ar 9ar 8ar 7

This ratio tells us about relationship between adjusted profit and capitalemployed.

Net capital employed = Fixed Assets + Current Assets Current liabilities

Adjusted Profit = Profit for the year + Non-operating expenses Non

operating Incomes.

Significance: Higher the ratio, more profitable will be the concern.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 12/30

Return on Equity shareholder funds(%):Mar 10Mar 09Mar 08Mar 07Mar 06

This ratio tells us about the relationship between Net profit (after interest,

taxes and preference share dividend) and equity share capital (Paid up).

Significance: As rate of preference share are always fixed and dividend on

equity share varies from year to year depending upon the profitability of

the concern. So equity shareholders are always interested to know what

rate of dividend they are going to get in this particular year, this ratio

provides them information about the rate of dividend they are going toget. Higher the ratio, higher will be the dividend and more satisfied the

shareholders.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 13/30

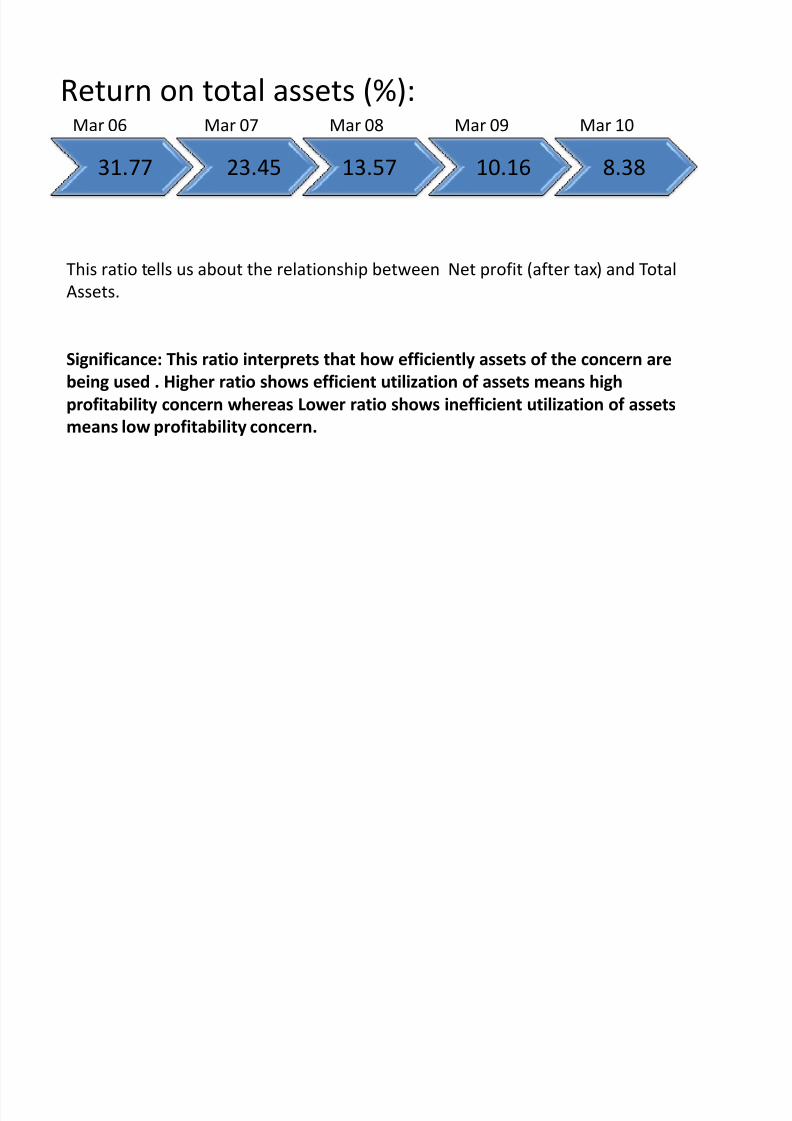

Return on total assets (%):

31.77 23.45 13.57 10.16 8.38

Mar 10Mar 09Mar 08Mar 07Mar 06

This ratio tells us about the relationship between Net profit (after tax) and TotalAssets.

Significance: This ratio interprets that how efficiently assets of the concern are

being used . Higher ratio shows efficient utilization of assets means high

profitability concern whereas Lower ratio shows inefficient utilization of assets

means low profitability concern.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 14/30

Particulars Mar 2010 Mar 2009 Mar 2008 Mar 2007 Mar 2006

Working capital turnover ratio 51.07 -226.06 1.73 7.21 -19.91

Fixed Asset ratio 1.12 1.22 1.2 1.68 1.6

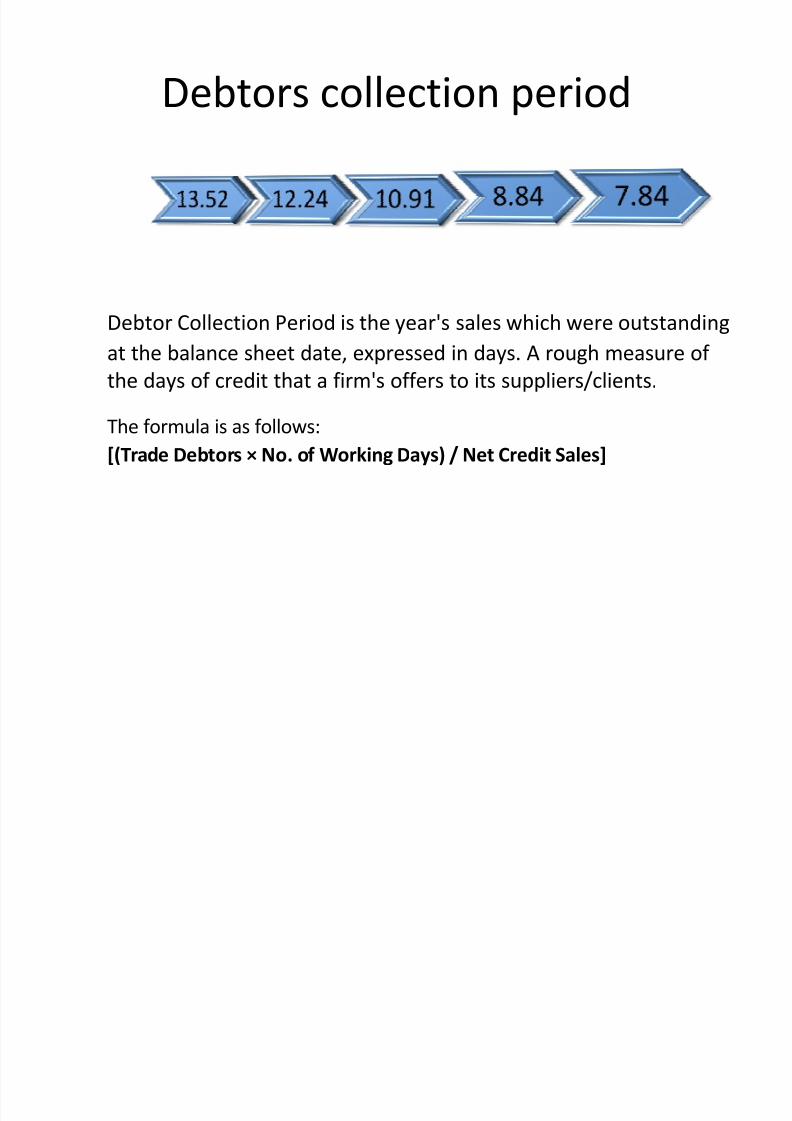

Debtors turnover ratio 46.58 41.29 33.45 29.81 26.99

Debtors collection period 7.84 8.84 10.91 12.24 13.52

Creditors turnover ratio 6.51 6.77 5.67 5.63 6.64

Creditors payment ratio 56.07 53.91 64.37 64.83 54.97

Stock turnover ratio 10.9 9.36 10.84 7.69 7.08

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 15/30

Working Capital Turnover Ratio

Following formula is used to calculate working capital

turnover ratio:

[Working Capital Turnover Ratio = Cost of Sales / NetWorking Capital]

Net working capital is found by deduction from the total of

the current assets the total of the current liabilities.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 16/30

Interpretation:

The working capital turnover ratio measure the

efficiency with which the working capital is beingused by a firm. A high ratio indicates efficient

utilization of working capital and a low ratio indicates

otherwise. But a very high working capital turnover

ratio may also mean lack of sufficient working capitalwhich is not a good situation.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 17/30

Fixed Assets Ratio

Fixed ratio is also known as sales to fixed assets ratio. This

ratio measures the efficiency and profit earning capacity of the concern.

Fixed assets ratio ratio is calculated by the following formula:

Fixed Assets Ratio = Cost of Sales / Net Fixed Assets

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 18/30

Interpretation:

Higher the ratio, greater is the intensive

utilization of fixed assets. Lower ratio means

under-utilization of fixed assets.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 19/30

Debtors turnover ratio

Debtors turnover ratio or accounts receivable turnover ratio indicates

the velocity of debt collection of a firm. In simple words it indicates the

number of times average debtors (receivable) are turned over during ayear.

[Debtors Turnover Ratio = Net Credit Sales / Average Trade Debtors]

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 20/30

Interpretation:

The higher the value of debtors turnover themore efficient is the management of debtors

or more liquid the debtors are. Similarly, lowdebtors turnover ratio implies inefficientmanagement of debtors or less liquid debtors.It is the reliable measure of the time of cashflow from credit sales

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 21/30

Debtors collection period

Debtor Collection Period is the year's sales which were outstanding

at the balance sheet date, expressed in days. A rough measure of

the days of credit that a firm's offers to its suppliers/clients.

The formula is as follows:

[(Trade Debtors × No. of Working Days) / Net Credit Sales]

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 22/30

Interpretation:This ratio measures the quality of debtors. A

short collection period implies prompt payment

by debtors. It reduces the chances of bad debts.

Similarly, a longer collection period implies too

liberal and inefficient credit collection

performance. It is difficult to provide a standard

collection period of debtors.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 23/30

Creditors Turnover ratio

This ratio is similar to the debtors turnover ratio. It compares

creditors with the total credit purchases.

It signifies the credit period enjoyed by the firm in paying

creditors. Accounts payable include both sundry creditors and

bills payable.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 24/30

I

nterpretation:A high creditors turnover ratio or a lower credit

period ratio signifies that the creditors are being

paid promptly. This situation enhances the credit

worthiness of the company. However a veryfavorable ratio to this effect also shows that the

business is not taking the full advantage of credit

facilities allowed by the creditors.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 25/30

Creditors payment ratio

This ratio tells us about the number of days or month

or week, a concern has to wait before its creditors are

paid off.

Creditor Velocity/ Payment period =

(Average trade creditors/Net credit annual

purchases)* No. of days in a year

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 26/30

Interpretation:

Lower the number of days, more efficient is the

management regarding creditors turnover. Too much

lower number of days means concern is enjoying

benefit of discount policy and ignoring the benefits of

credit policy whereas too much higher number of days

means concern is enjoying the benefits of credit policy

but ignoring the benefits of credit policy.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 27/30

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 28/30

Interpretation:

Inventory turnover ratio measures the velocity of

conversion of stock into sales. Usually a high inventoryturnover indicates efficient management of inventorybecause more frequently the stocks are sold, thelesser amount of money is required to finance the

inventory. A low inventory turnover ratio indicates aninefficient management of inventory. A low inventoryturnover implies over-investment in inventories, dullbusiness, poor quality of goods. The inventory

turnover ratio is also an index of profitability, where ahigh ratio signifies more profit, a low ratio signifieslow profit.

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 29/30

Conclusion

From above ratios, we can conclude that:

Concerns profitability is not good.

Concern is at risk

Shareholders risk is more than outsiders risk.

Efficient use of Working Capital

Under utilization of fixed assets

Enjoying credit policy from suppliers for 2months (app.)

8/7/2019 Accounts ppt (final)

http://slidepdf.com/reader/full/accounts-ppt-final 30/30