f3 advanced analytics - fincad · f3 advanced analytics see reverse > price any trade ... ♦...

TRANSCRIPT

F3 ADVANCED ANALYTICS

see reverse >

PRICE ANY TRADE♦ Vanilla or exotic ♦ Handle new trade types on-the-fly (no need to recompile) ♦ Re-usable market data and model calibrations, automatically invoked

AUTOMATIC FIRST-ORDER RISK♦ Sensitivity of price to all market data guaranteed (built into architecture) ♦ Sensitivities to market data available even if model calibration is required ♦ Uses enhanced Universal Risk Technology (fast, robust), not bumping ♦ Hedge factors ♦ DV01

GENERIC CREDIT VALUE ADJUSTMENT (CVA)♦ CVA/DVA for all trade types ♦ Calculated at trade or portfolio (netting set) level ♦ IAS 39, FAS 157 & ASC 820 Analytics♦ Unilateral & Bilateral CVA♦ Marginal CVA; Incremental CVA♦ Collateral

GENERIC VALUE-AT-RISK (VaR)♦ Historical or Monte Carlo VaR for all trade types♦ UCITs IV compliant calculation♦ Intuitive & robust MC VaR calculation♦ VaR calculation allows for unlimited paths and distribution shapes

SCENARIO ANALYSIS♦ Historical, Monte Carlo, or user-created scenarios ♦ Analysis of resulting distributions (percentiles; mean, etc.)

P&L AND PERFORMANCE ATTRIBUTION♦ For vanilla and exotic portfolios♦ Transaction-level analysis

PRICING MODELS AND ALGORITHMS

FOR ASSETS♦ Black-Scholes (Lognormal) Model♦ CEV Model ♦ Shifted Lognormal Model ♦ Normal Model (Bachelier) ♦ Heston Model♦ SABR Model♦ Vol surface construction (FX, EQ)

FOR RATES♦ Black Model (rates) ♦ Single & Multifactor Hull-White (HW) ♦ Libor Market Model (LMM/BGM) ♦ SABR Model (rates) ♦ LMM Calibration – cascade; parametric ♦ Swaption Vol Cube Construction

TECHNOLOGIES♦ Meta-model design; asset-specific models applied automatically ♦ Generic calibration engine ♦ Generic payoff replication technology (CMS; Variance; etc) ♦ Generic early exercise (callable/cancellable) ♦ Multi-rate curve building ♦ Ubiquitous time-dependency♦ Hybrid modelling: price and/or rate processes

OVE

RVI

EW

FEA12W001-1

Corporate HeadquartersCentral City, Suite 175013450 102nd AvenueSurrey, BC V3T 5X3CanadaUSA/Canada 1.800.304.0702

EMEA Sales & Client Service Center Block 4, Blackrock Business Park Carysfort Avenue, BlackrockCo Dublin, IrelandEurope 00.800.304.07020

Email [email protected]

CONTACT:

Copyright © 2012 FinancialCAD Corporation. All rights reserved. FinancialCAD® and FINCAD® are registered trademarks of FinancialCAD Corporation. Other trademarks are the property of their respective holders. This is for

informational purposes only. FINCAD MAKES NO WARRANTIES, EXPRESSED OR IMPLIED, IN THIS SUMMARY. Printed in Canada.

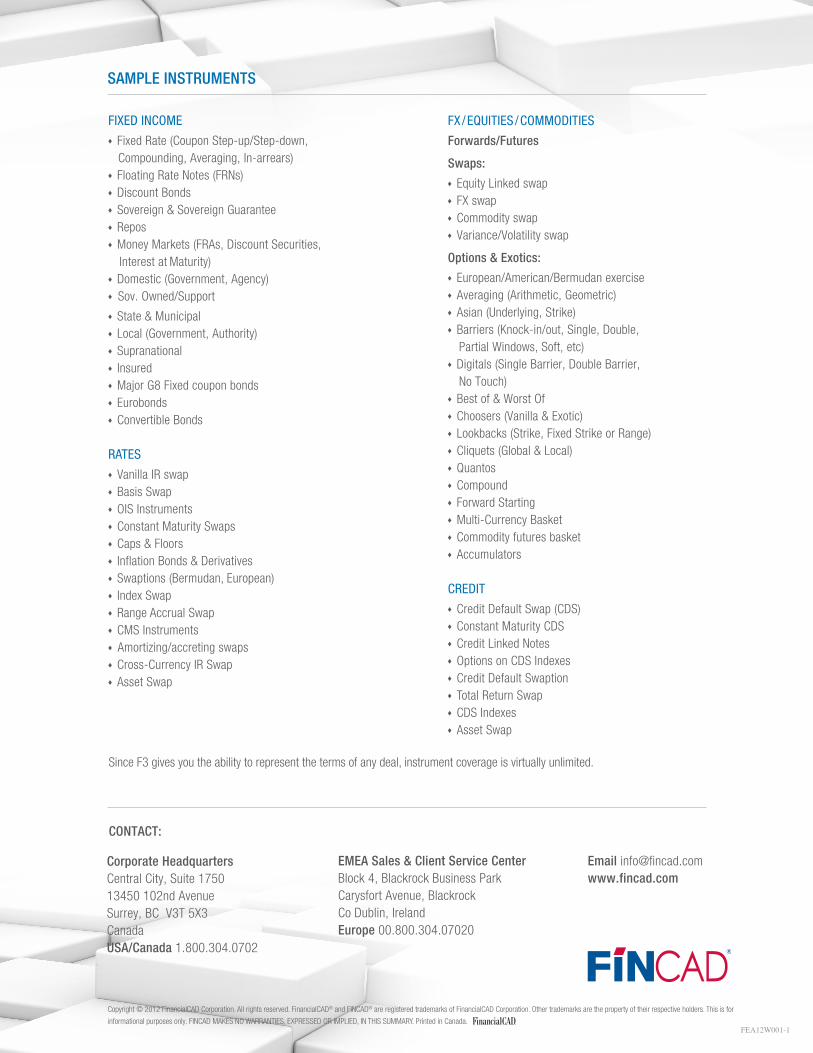

SAMPLE INSTRUMENTS

FIXED INCOME♦ Fixed Rate (Coupon Step-up/Step-down, Compounding, Averaging, In-arrears) ♦ Floating Rate Notes (FRNs) ♦ Discount Bonds ♦ Sovereign & Sovereign Guarantee ♦ Repos♦ Money Markets (FRAs, Discount Securities, Interest at Maturity)♦ Domestic (Government, Agency)♦ Sov. Owned/Support

♦ State & Municipal ♦ Local (Government, Authority) ♦ Supranational ♦ Insured ♦ Major G8 Fixed coupon bonds ♦ Eurobonds♦ Convertible Bonds

RATES♦ Vanilla IR swap ♦ Basis Swap♦ OIS Instruments♦ Constant Maturity Swaps♦ Caps & Floors♦ Inflation Bonds & Derivatives♦ Swaptions (Bermudan, European)♦ Index Swap♦ Range Accrual Swap♦ CMS Instruments♦ Amortizing/accreting swaps♦ Cross-Currency IR Swap♦ Asset Swap

FX /EQUITIES /COMMODITIES

Forwards/Futures Swaps: ♦ Equity Linked swap♦ FX swap♦ Commodity swap♦ Variance/Volatility swap

Options & Exotics:♦ European/American/Bermudan exercise♦ Averaging (Arithmetic, Geometric)♦ Asian (Underlying, Strike)♦ Barriers (Knock-in/out, Single, Double, Partial Windows, Soft, etc)♦ Digitals (Single Barrier, Double Barrier, No Touch)♦ Best of & Worst Of♦ Choosers (Vanilla & Exotic)♦ Lookbacks (Strike, Fixed Strike or Range)♦ Cliquets (Global & Local)♦ Quantos♦ Compound♦ Forward Starting♦ Multi-Currency Basket♦ Commodity futures basket♦ Accumulators

CREDIT♦ Credit Default Swap (CDS)♦ Constant Maturity CDS♦ Credit Linked Notes♦ Options on CDS Indexes♦ Credit Default Swaption♦ Total Return Swap♦ CDS Indexes♦ Asset Swap

Since F3 gives you the ability to represent the terms of any deal, instrument coverage is virtually unlimited.