ey scottish item club - united statesfile/ey-scottish-item-club-2018-forecast.pdf · in recruiting...

TRANSCRIPT

EY Scottish ITEM Club2018 ForecastPicking up pace but can Scotland accelerate faster?December 2017

EY Scottish ITEM Club

Fore

wor

dContentsForeword 1

Overview 2

Global and UK background 4

Scotland in 2017 8

Forecast for 2018 and beyond 18

City focus 22

Risks and uncertainties 31

Forecast tables 33

EY is the sole sponsor of theITEM Club, which is the onlynon-governmental economicforecasting group to use theHM Treasury model of the UKeconomy. Its forecasts areindependent of any political,economic or business bias.

This report is based on data andinformation available before 24November 2017. The EY ScottishITEM Club report is part of theEY Economics for Businessprogramme which providesknowledge, analysis and insightto help business understand theeconomic environments in whichthey operate, both in the UK andglobally. Find out more:ey.com/uk/[email protected]

Follow:go.ey.com/MarkGregory@MarkGregoryEY

Mark GregoryEY Chief Economist, UK

Mark is a business economist with over 25 years’ experience in more than 40 countries as an advisor to Governments and industry on economics, policy and regulation.

1EY Scottish ITEM Club

Fore

wor

d Mark Harvey Senior Partner EY, Scotland

Picking up momentum but how do we accelerate faster?The momentum of Scotland’s economic growth is picking up pace, navigating volatility with the consumer a key driver behind the economic growth. In 2017, GDP growth is anticipated to achieve 0.8 per cent, double what was previously predicted. This positivity is set to continue next year when GDP growth in Scotland is expected to match UK-wide growth at 1.4 per cent, as revealed in this report — EY Scottish ITEM Club 2018 Forecast.This is clearly a move in the right direction for Scotland’s economy which had begun to stagnate, but the ambitions for Scotland must be much greater than this. Particularly given that growth rates for Scotland and the whole of the UK are anticipated to diverge again during the next five years, with an annual average of 1.7 per cent growth compared with 2.0 per cent UK-wide.

This acts as a reminder that growth rates can be difficult to maintain and an enduring focus on how to grow Scotland’s economy is a priority. Driving improved performance across all seven of Scotland’s cities will be a strategic imperative to fulfil Scotland’s economic potential.

Economic and employment growth has been led by Edinburgh and Glasgow but their success is now stretching far beyond the other five cities and is set to outperform Scotland’s overall economic growth. For long-term sustainable growth Scotland cannot rely so extensively on the two biggest cities. Government and business will have to work harder and smarter together to enable Aberdeen, Dundee, Perth and Kinross, Stirling and Inverness to play a bigger role in Scotland’s growth story.

Improving productivity will be key which means stimulating business investment; addressing the skill shortages; exploiting the use of digital technologies and continuing to drive key growth sectors.

Pivotal to this is how we grow an inclusive economy where everyone can benefit, while ensuring we remain a competitive location for international investors and create an environment that promotes business growth and success.

The extended powers available to the Scottish Government provides an opportunity to shape an environment where individuals and businesses can thrive. In the Scottish Budget on the 14 December (2017), the Scottish Finance Secretary is expected to announce a further rise in the income tax paid by wealthier tax payers in Scotland compared with the rest of the UK, but will such a move be good for business, entrepreneurs and inward investment? Ideally, government should look to support more start-ups and scale-ups and help businesses grow by attracting and retaining top talent. This would in turn generate a much more dynamic and growing tax base to deliver an increase in tax revenues.

While the latest EY Scottish ITEM Club report is encouraging, it also highlights that we still face challenges, some more prevalent to Scotland such as our decrease in the number of people of working age combined with a decline in migrants. Against this backdrop let’s use the policy levers at our disposal wisely, collaborate across business and government, and grow a Scotland that plays to its strengths.

2EY Scottish ITEM Club

Overview

GDP data shows that the Scottish economy grew by 0.5% between Q2 2016 and Q2 2017, compared with a UK expansion of 1.5% over the same period. The UK has experienced a slowdown compared with 2016, partly because higher inflation has squeezed real consumer spending. The global economy has, however, performed better than many commentators predicted, despite several sources of potential uncertainty.

However, surveys show a weakening in consumer expectations in the second half of the year. Third quarter results from the Scottish Consumer Sentiment survey suggest that households have become less optimistic about prospects for the Scottish economy, with expectations of prospects for the upcoming 12 months at their lowest recorded level.

The shortfall in growth in Scotland, compared to the rest of the UK, was mainly driven by a 5.5% contraction in the construction sector, in contrast to growth of 4.1% across the UK, while subdued manufacturing growth of 0.2% was also a contributing factor. We now forecast Scottish GDP growth of 0.8% for 2017 as a whole, which is a slight downgrade on our summer forecast of 0.9%, though better than the actual 0.4% increase in 2016.

In contrast, Scotland’s business confidence remained positive in the third quarter, led by construction companies, in defiance of difficulties earlier in the year. Business sentiment is also positive within financial & business services, manufacturing and tourism. However confidence has remained negative in the retail & wholesale sector.

The expansion in onshore nominal GDP has been largely driven by household consumption, which contributed over two-thirds of the increase in Scottish GDP between the second quarters of 2016 and 2017. The continued growth of consumer expenditure was largely attributable to the falling saving ratio, which hit 6.4% in 2017, the lowest recorded rate in the past ten years.

A common theme across most sectors is a difficulty in recruiting staff, most notably in the construction and tourism sectors, which may reflect a falling-away in inward migration from the EU, following the Brexit vote.

Growth has been further supported by expansions in government spending and a slight strengthening of the net trade position, although investment fell by 3.2% over the year to the second quarter, reflecting a 14.8% fall in business investment. The improved external position partly reflected stronger exports, which rose by 8.7% in value terms, driven mostly by growth in sales to the rest of the world rather than the rest of the UK. Demand for imports rose more slowly, at 5.4%.

2017 has also seen employment growth, which has resulted in a sustained fall in the Scottish rate of unemployment, which has recently fallen to 4.0% in Q3 2017, less than half of its mid-2010 peak of 8.9%. That is despite more people looking for work, drawn-in by the increase in job opportunities.

2017

Overview

1

5

6

7

8

2

3

4

3EY Scottish ITEM Club

We forecast that Scotland will experience stronger GDP growth in 2018 than in 2017, at 1.4%, and an annual average growth rate of 1.7% a year to 2022. That is below our projection of 2.0% a year growth for the UK over the half-decade.

In addition, manufacturing looks set to improve with 1.0% growth in 2018 and an average of 1.3% a year over the next five years (in line with the UK average). Reasons include an expanding global economy, a competitive exchange rate, and productivity gains — though the last of these will be at the expense of manufacturing employment.

A key factor behind 2018’s stronger performance is household spending, which is forecast to grow in real terms by 1.1%, so up on 2017’s 0.8% increase. This reflects growth in real personal incomes, thanks to a combination of modestly higher employment, increases in average earnings and an easing in inflation through the year. House prices are forecast to grow by 3.4% in 2018, so less than in 2017. Housing affordability is better in Scotland than in the UK overall.

Overall employment growth is forecast to slow to 0.4% in 2018 and remain static in 2019. Growth will continue to be skewed towards private services, with the administrative & support services and professional, scientific & technical services sectors contributing 16,000 and 14,00 jobs respectively up to 2022, more than offsetting the net loss of 6,000 jobs elsewhere in the economy.

Our forecast does assume that some of the uncertainty over Brexit will ease during 2018, and that this will lead to increased business confidence and investment during the course of the year. Brexit nevertheless represents the biggest area of uncertainty facing Scottish companies, and indeed the Scottish economy as a whole. If there is not progress in 2018 towards a transition arrangement, then that would be likely to affect our forecast for the year.

Significantly, Scotland looks set to experience slow growth in its overall population and an absolute decline of 62,000 in its working age population over the medium term to 2022. One reason is that net inward migration is forecast to fall from 14,000 in 2017 to just 6,000 by 2022, largely reflecting Brexit. However, a larger factor is the demographic profile. Amongst the consequences, a smaller working age population, and fewer migrants, will mean a reduced supply potential compared with what it would otherwise be, and a risk of increasing skill shortages — although it also means that even with weak employment growth, the unemployment rate is likely to remain largely unchanged at an historically low 4%.

Amongst sectors, private services will continue to drive growth, predicted to contribute four-fifths of the 1.4% growth in GDP in 2018, despite accounting for just half of economic activity in 2017. The fastest growing service sectors are likely to be professional, scientific & technical activities, administrative & support services and information & communication.

Amongst Scotland’s cities, there is a noticeable gap in likely performance between the two largest and the others. Both Edinburgh and Glasgow are set to experience GDP growth of 2.1% a year over the 2017–20 period, and annual employment growth of 0.9% and 0.8% respectively. The professional and administrative support sectors will contribute significant numbers of extra jobs in both cities, while Edinburgh looks set to increase its tourism-related employment, whereas public administration jobs in the capital are projected to fall.

2018

Overview

1

5

6

7

8

2

3

4

4EY Scottish ITEM Club

Global and UK background

The global economy is delivering stable growth despite political worriesWhile there are many sources of global political anxiety at the moment, and a number of economic uncertainties, the reality is that the pace of global economic growth has picked-up during 2017, helped by rising world trade growth. We see that pattern

extending into 2018, bolstered by a likely upcoming fiscal stimulus in the US, even as the impulse from China gradually fades. That means that global GDP growth improves very slightly from 2.9% in 2017 to 3.2% in 2018, which is a slight improvement on our July forecasts of 2.6% and 2.7% respectively. If achieved, these forecasts will represent the longest period of robust global growth since the initial recovery from the Global Financial Crisis.

World GDP growth

% changes on previous year

2016 2017 2018 2019 2020 2021

US 1.5 2.2 2.6 1.8 1.5 1.5

Japan 1.0 1.6 1.7 0.9 0.0 0.9

Eurozone 1.8 2.3 2.1 1.7 1.5 1.3

UK 1.8 1.5 1.4 1.8 2.0 2.2

China 6.7 6.8 6.4 6.0 5.7 5.4

India 7.9 6.5 7.5 7.1 6.9 6.6

World 2.4 2.9 3.2 2.9 2.7 2.7

World (PPP) 3.2 3.6 3.8 3.6 3.5 3.4

Source: EY ITEM Club/Oxford Economics

Global and UK background

5EY Scottish ITEM Club

Evidence in support of this positive story includes purchasing managers’ surveys, which suggest that overall growth in advanced economies strengthened during the summer of 2017. It is true that industrial production in some of the advanced economies weakened in the period, and world trade went through a soft patch, but US industrial output was dampened by the recent hurricanes, while the more recent trade data point to a speeding-up in world growth in the second half of 2017.

Broad-based global economic strength has, however, coincided with a more hawkish tone from some central banks, including the Federal Reserve (Fed), so that we expect further US interest rate rises, including two in 2018. The Fed’s aim will be to avoid the need for more aggressive rises later. We do not expect the parallel unwinding of the central bank’s quantitative easing to have significant negative impacts on growth.

The Fed’s tougher stance, together with some challenging political developments in Europe, have led the euro to weaken against the US dollar, but we think further sustained falls in the euro are unlikely so long as the Eurozone continues to record above-trend growth, and so long as underlying inflationary pressures remain manageable.

Meanwhile a widening growth differential over advanced economies, plus firmer commodity prices, should give most emerging economies a degree of resilience to the Fed tightening, and also to the slowdown in China’s economy. Critically, the latter appears to be following a stable and managed path. We maintain our forecast of 6.8% for 2017, and although we expect somewhat lower growth of 6.4% in 2018, China only needs to grow by 6.3% a year in 2018–20 to meet its ambitious goal of doubling 2010 GDP by 2020. President Xi’s speech at the 19th Party Congress indicates no change to that ambition.

The UK economy report card not as strong as globalAgainst that global background the UK economy has experienced weak growth in 2017, partly because of a continuing squeeze on consumer purchasing power due to a rise in inflation, and partly because of uncertainties generated by Brexit and the inconclusive result of the General Election. The year has also seen growing expectations of a rise in interest rates (now implemented) and a continuing commitment from the Chancellor to achieving a balanced budget by the mid-2020s, despite the current sluggishness of the economy.

Official figures for real GDP growth in Q3 were marginally higher than expected, at 0.4% quarter-on-quarter, but still below historical trends. Manufacturing output picked up somewhat and retail spending was probably helped by foreign and domestic tourist spending, but the construction sector was a significant drag on the economy.

Survey evidence, such as the Purchasing Managers’ Indices for the services, manufacturing and construction sectors combined, suggests that Q4 has seen a similar overall pattern to the third quarter. In particular, businesses look to have been cautious over investment commitments. We therefore estimate that 2017 as a whole has seen real GDP growth of 1.5%: unchanged from our July projection, but noticeably lower than 2016’s outturn of 1.8%.

A tight labour market in 2017 but subdued wages growth Despite slow economic growth, the UK labour market has continued to tighten. Employment in Q3 2017 was 279,000 up on a year earlier, at 32.1 million (though 14,000 down on Q2) while unemployment was 182,000 lower than a year earlier (and 59,000 down on Q2).

At 4.3% the UK unemployment rate in Q3 was the lowest since 1975, and also below the 4.5% unemployment rate that the Bank of England (BoE) considers to be the ‘equilibrium’ level, below which the BoE suggests there is a danger of accelerating inflation. Despite that, there is little evidence of average earnings being driven up: both regular pay and total pay (including bonuses and the like) were 2.2% higher in nominal terms in Q3 2017 than they were in the same period a year earlier, which was little changed from the increases reported for Q2.

-800-600-400-2000

4006008001,000

4.04.55.05.56.06.57.07.58.08.59.0

Year-on year change in employment (RHS)LFS unemployment rate (LHS)

Source: EY ITEM Club/Haver Analytics

%

UK: Labour market indicators000s

200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172005 2006

Global and UK background

6EY Scottish ITEM Club

Continuing employment growth is, however, coming at the expense of productivity. It appears that the ongoing cheapness of labour is pricing workers into jobs. Faced with a mixture of skill shortages and longer-term uncertainty employers are meeting increases in demand primarily by taking on more workers, rather than by committing to potentially costly and lengthy capital investments. Meanwhile employees are in general also behaving cautiously, and are refraining from taking advantage of the tight labour market to push for large pay increases. That is despite higher inflation, which has continued to be driven-up by the lingering impact of sterling’s sharp drop, following the Brexit vote in 2016.

UK inflation should ease as the economy strengthens in 2018 and beyondLooking forward, consumer price inflation is set to rise to just above 3% in the near term, partly due to firmer oil and energy prices. However, these effects will not last, and inflation should ease as 2018 progresses, helped by the recent strengthening in sterling. We project 2% consumer price inflation in Q4 2018. That should permit an increase in real wages, though with real consumer spending growth nevertheless remaining subdued: indeed slower in 2018 than in 2017 (1.1% compared with 1.5%).

Source: EY ITEM Club

UK: Average earnings and inflation

*National accounts measure

-3-2-101234567

2004 2006 2008 2010 2012 2014 2016 2018 2020

Average earnings* CPI inflation

% year

Forecast

Partly as a result, GDP growth is projected to be 1.4% in 2018, a slight upgrade on our July forecast of 1.3% expansion but still slightly below growth in 2017. However, that weakening masks a gradual increase in pace during the year, from a very slow start.

This profile is partly based on the assumption that progress is made during the course of 2018 with respect to the terms of the UK’s exit from the European Union, and in particular that an agreement is struck on a transition agreement. That should boost business confidence during the year, and hence support a gradual pick-up in investment. Contrarily, if an agreement is not arrived at, then there will be a risk of a slump in business confidence.

Another important consideration with respect to 2018 is the likely profile of the UK’s overseas trade. There were hopes that in 2017 exports would make a significant contribution to UK growth, helped by a very competitive pound and improvements in overseas markets. The evidence of this has been muted, perhaps because companies used the weaker pound to boost their profit margins rather than price more competitively in international markets. Even so, net trade has made a more positive contribution to UK GDP growth in 2017 than in 2016, and the current account deficit has fallen from 5.9% of GDP to 4.4%. We expect further improvements in 2018.

Source: EY ITEM Club

UK: Current account

IDP = interest, profit and dividends

-12-10-8-6-4-20246

2004 2006 2008 2010 2012 2014 2016 2018 2020

Services Goods IPD Net transfers Current account

% of GDP

Forecast

Meanwhile the squeeze on consumers should ease appreciably during the course of 2018 as inflation falls through the year, and as wages increase a little more strongly, reflecting the easing of the public sector pay cap that the Chancellor has already announced. However, the upside for consumer spending is likely to be limited by slower employment growth.

Global and UK background

7EY Scottish ITEM Club

Source: EY ITEM Club

UK: Contributions to GDP growth

-5-4-3-2-101234

2004 2006 2008 2010 2012 2014 2016 2018 2020

Domestic demand Net exports GDP growth

% year

Forecast

Medium-term growth below trendOur medium-term projections for the UK are unchanged, having been lifted in July when we concluded that the weakened position of the Government following June’s general election was likely to result in a more business-friendly Brexit, as well as in a modestly looser fiscal stance, notwithstanding the Chancellor’s continuing commitment to achieving a balanced budget.

On that basis, and assuming that the UK does indeed avoid a ‘cliff edge’ exit from the European Union (EU) in March 2019, the economy should benefit from improving business investment over the medium term. We project that GDP growth strengthens to 1.8% in 2019, 2.0% in 2020 and 2.2% in 2021. These are unchanged from our July forecasts, but remain below the UK’s long-run average growth rates.

Global and UK background

8EY Scottish ITEM Club

Scotland in 2017

Growth in 2017’s first half was led by the service sectorOfficial figures from the Scottish Government suggest that Scotland’s onshore GDP in Q2 2017 was 0.5% higher than in Q2 2016. This compares with a UK expansion of 1.5% over the same period.

The Scottish National Accounts data suggest that in value terms, Scotland’s onshore GDP grew by 2.8% between Q2 2016 and Q2 2017, comprising a combination of the 0.5% volume expansion referred to above, and an implied rise of 2.4% in the corresponding measure of prices.

That increase is slower than the equivalent rise in the value of UK-wide GDP, which was 3.7% over the same period. However, if Scotland’s geographic share of oil and gas production is included in the calculation then the total value of Scottish GDP growth in the year to Q2 was also 3.7%: so fully in line with the UK increase, and the highest Scottish growth rate recorded since 2014.

As far as the on-shore economy is concerned the service sector has been the key driver of growth, with an increase of 1.3% between Q2 2016 and Q2 2017 — although that was below the UK gain of 1.8%. Both mainly public and mainly private services grew at the same rate.

Within mainly private services the transport & communications sector generated an impressive 2.9% increase between Q2 2016 and Q2 2017, while professional services and ‘other’ sectors also provided considerable momentum. Financial services also contributed to the overall increase, but less so than in 2016. Real estate was another modest net contributor.

In contrast, the accommodation & food and retail sectors saw output falls over the year to Q2 2017. Government & other services increased by 1.3%, so higher than the equivalent UK growth of 1.1%.

Source: Scottish Government/EY ITEM Club

Scotland: private service sector growth

Transport & communications

Retail

Real estate

Professional services

Other

Financial services

Accommodation & food

Private services

-6 -4 -2 0 2 4 6 8 10 12

2015 2016 2017

% annual change (year to Q2)

Scotland in 2017

9EY Scottish ITEM Club

Scotland’s manufacturers performed particularly poorly in Q2, with growth of just 0.2% compared with the same period in 2016, reflecting in part a weakening from the level attained in the first quarter (which had been a more respectable 1.3% up on a year earlier). That said, even the Q2 figure is a significant improvement on earlier years: manufacturing output declined 2.0% in 2015 and a further 5.2% in 2016. And even in Q2 2017 there were notably positive contributions to GDP growth from the chemicals, metals & machinery and other manufacturing goods elements, which all out-performed the preceding years. However, positive growth in these sectors was largely offset by declines in transport equipment and textiles production, both at faster rates than previously, and also by contractions in food & drink and electronics.

As at the UK level, it seems likely that the decline that occurred in the exchange rate following the Brexit vote has been mainly used by companies to increase their margins, rather than to raise sales volumes.

Source: Scottish Government/EY ITEM Club

Scotland: manufacturing sector growth

Textiles

Transport equipment

Other manufacturing

Metals & machinery

Food & drink

Electronics

Chemicals

Manufacturing

-14 -12 -10 -8 -6 -4 -2 0 2 4 6 8

2015 2016 2017

% annual change (year to Q2)

Scotland’s worst performing sector in Q2 was construction, which saw output volumes fall by 5.5% compared with the same quarter a year earlier. The sector achieved a recent peak in the final quarter of 2015 and has been trending downwards since then, partly because of sluggish overall GDP growth, public sector spending limits and weak business confidence, but also just the result of a number of major projects coming to completion. The sector saw rapid growth throughout 2014 and 2015. Even so, the latest contraction contrasts with the situation in the UK as a whole, in which construction was the fastest growing sector: up 4.1% in the year from Q2 2016 to Q2 2017.

Increases in consumer spending have also supported growthThe 2.8% expansion in onshore nominal GDP between Q2 2016 and Q2 2017, referred to above, was mainly driven by household consumption. This increased by 3.1%, or 0.3 percentage points above the total. Indeed, consumer spending contributed over two-thirds (71%) of the increase in Scotland’s nominal GDP over the year.

An important reason for that is a decline in the saving ratio, which fell to 6.4% in the second quarter, continuing a trend apparent since the recent highpoint of 14.7% in the last quarter of 2010. Scotland’s saving rate is generally above the UK average, but the gap has now almost closed.

Source: Scottish Government/ONS

Consumer savings have continued to fall

0

2

4

6

8

10

12

14

16

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Scotland UK

Saving ratio (%)

A second factor helping consumer spending has been continuing growth in employment. Total employment, including those of retirement age, increased by 46,000 between the three months ending September 2016 and the three months ending September 2017, reaching a total of 2.65 million. The employment rate rose to 60.1% of the population aged 16 and over, or 75.2% if those aged over 64 are excluded.

Less helpful has been growth in average earnings. Provisional data for April 2017 indicate that, at £28,400 a year, average earnings in Scotland were £400 (or 1.4 percentage points) below the UK average. More importantly to spending growth, nominal earnings were only 1.5% higher than a year earlier, underperforming the UK average of 2.0%. Furthermore, growth in nominal wages fell below CPI inflation in Q2 2017 (2.7%), indicating that wages in real terms fell.

Scotland in 2017

10EY Scottish ITEM Club

Unemployment has continued to fallAfter peaking at 8.9% in mid-2010 the unemployment rate — those who are without a job but who are actively seeking employment — has fallen to under half of this rate (4.0%) in the three months to September 2017. The main explanation is of course the rise in employment. However, the relationship is not one-for-one. Employment of people aged 16-64 rose by 53,000 between the three months to September 2016 and the same period in 2017, but unemployment of people in that age group declined by much

less — just 21,000. The reason is that more people entered the labour market looking for work, not least because there were more jobs available. So the proportion inactive (neither in work not looking for a job) fell, while the proportion who were active (in work or looking for it) rose.

This is a welcome recovery in the activity rate. Historically this has tended to be higher in Scotland than at the UK level, and it was on a clear rising trend from late 2012 to the start of 2016, when it peaked at 79.3%. But in early 2017 the rate began to fall sharply, moving well below the UK level. In the three months ending September 2017 it was back in line with the UK rate, at 78.4% for those of working age.

Economic activity rate recovering in 2017

74

75

76

77

78

79

80

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Scotland UK

Economic activity rate (%)

Source: ONS

As unemployment continues to fall

Source: ONS

0

1

2

3

4

5

6

7

8

9

10

2008 2009 2010 2011 2012 2013 2014 2015 2016Scotland UK

Unemployment rate (%)

Scotland in 2017

11EY Scottish ITEM Club

House building has risen but business investment has fallenOne factor helpful to Scottish households is that a continuing modest expansion in housebuilding investment has contributed to Scotland maintaining better housing affordability than elsewhere in the UK. At 4.8% the increase in the value of housebuilding in Scotland in the year to Q2 2017 was larger than the average for the UK (3.8%). Evidence from Nationwide suggests that the resultant ratio of first-time buyer house prices to mean gross annual earnings was 3.3 for Scotland in the third quarter of 2017, compared with a UK average of 5.4 and a high of 10.1 for London.

Lowest house price to earnings ratio in the UK

Source: Nationwide

3.33.4

3.73.94.04.1

4.64.8

5.46.16.3

7.210.1

ScotlandNorth

Yorkshire & HumberNorth West

Northern IrelandWales

East MidlandsWest Midlands

East AngliaSouth West

Outer South EastOuter Met

London

0 2 4 6 8 10 12

Ratio of first time buyer house price to earnings (Q3 2017)

Unfortunately, the 4.8% increase in the value of housebuilding in Scotland in the year to Q2 2017 contrasts sharply with a large contraction in Scotland’s business investment, which fell by 14.8% relative to the second quarter of 2016, despite a 4.2% increase across the UK over the same period. Scotland did see growth in government investment over this period which, at 14.6%, was markedly faster than the 1.7% rise across the UK as a whole. Nevertheless, the combined impact of all three types of investment was a 3.2% fall in value terms in the amount of gross capital formation in Scotland, between Q2 2016 and Q2 2017.

Weak business investment offset by housebuildingand the public sector

Source: Scottish Government/EY ITEM Club

-20-15-10

-505

1015202530

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Business Investment Government investment

Dwellings investment

% change per annum

Improving external position, driven by international exportsA factor that has been more favourable than investment to Scottish GDP growth is a slight strengthening in the nation’s net trading position. This reflects stronger growth in export values (8.7%) than import values (5.4%) in the year to the second quarter of 2017, with the former driven mostly by growth in sales to the rest of the world (11%). The share of exports to the UK was 60.3% in the second quarter of 2017, a fall of 0.8 percentage points on the same period in the previous year, reflecting the weakness in demand in the UK generally.

Exports by destination and net trade position

Source: Scottish Government/EY ITEM Club

0%

2%

4%

6%

8%

10%

12%

2008 2009 2010 2011 2012 2013 2014 2015 2016 20170

5,000

10,000

15,000

20,000

25,000

To rUK (LHS) To rWorld (LHS)

Trade deficit (% of GDP) (RHS)

Exports (£m) Net trade position (% of GDP)

Scotland in 2017

12EY Scottish ITEM Club

Scottish manufacturing exports grew strongly between the second quarters of 2016 and 2017, reflecting strong performances from the petroleum and engineering & allied industries sub-sectors, in which the values of exports increased by 36% and 14% respectively. Growth was also positive for the wood, paper & printing and textiles sub-sectors, which grew by 6.3% and 5.6% respectively, although these sectors contributed only a minority (6%) of Scotland’s manufacturing exports in Q2 2017 and hence made only a small contribution to the overall increase. In contrast, food & drink, which generated over a third (35%) of manufacturing exports in Q2 2017, saw no change over this period. Meanwhile the metals and non-metallic products sectors both saw exports fall over this period, by 7.9% and 4.8% respectively.

Manufacturing exports continue to rise

Source: Scottish Government/EY ITEM Club

-15

-10

-5

0

5

10

15

2008 2009 2010 2011 2012 2013 2014 2015 2016 201760708090

100110120130140

Export volumes (% y/y) (RHS) Index (2008Q1=100) (LHS)

Manufacturing export volumes to rUK and rWorld (2008Q1=100)% change

per annum

More recently, consumer confidence has weakenedFor the second half of 2017 we are largely reliant on survey evidence. Unfortunately, that suggests that consumer confidence has been weakening, probably because of continued uncertainty with respect to Brexit, the squeeze that has occurred to real incomes because of higher inflation, worries over austerity measures, and of course the advent of rising interest rates.

Third quarter results from the Scottish Consumer Sentiment survey indicate that although the net balance of consumers’ responses was still positive when asked about economic performance over the past 12 months, it was less so than in recent quarters. Furthermore, when asked about their expectations for the forthcoming 12 months, the net balance of consumers’ responses was very negative: indeed, at its lowest ever recorded level.

Household confidence continues to fall

Source: Scottish Government

2013 2014 2015 2016 2017-50-40-30-20-10

010203040

Scottish economy (last 12 months) Household finances (last 12 months)

Scottish economy (next 12 months) Household finances (next 12 months)

Better-worse (%)

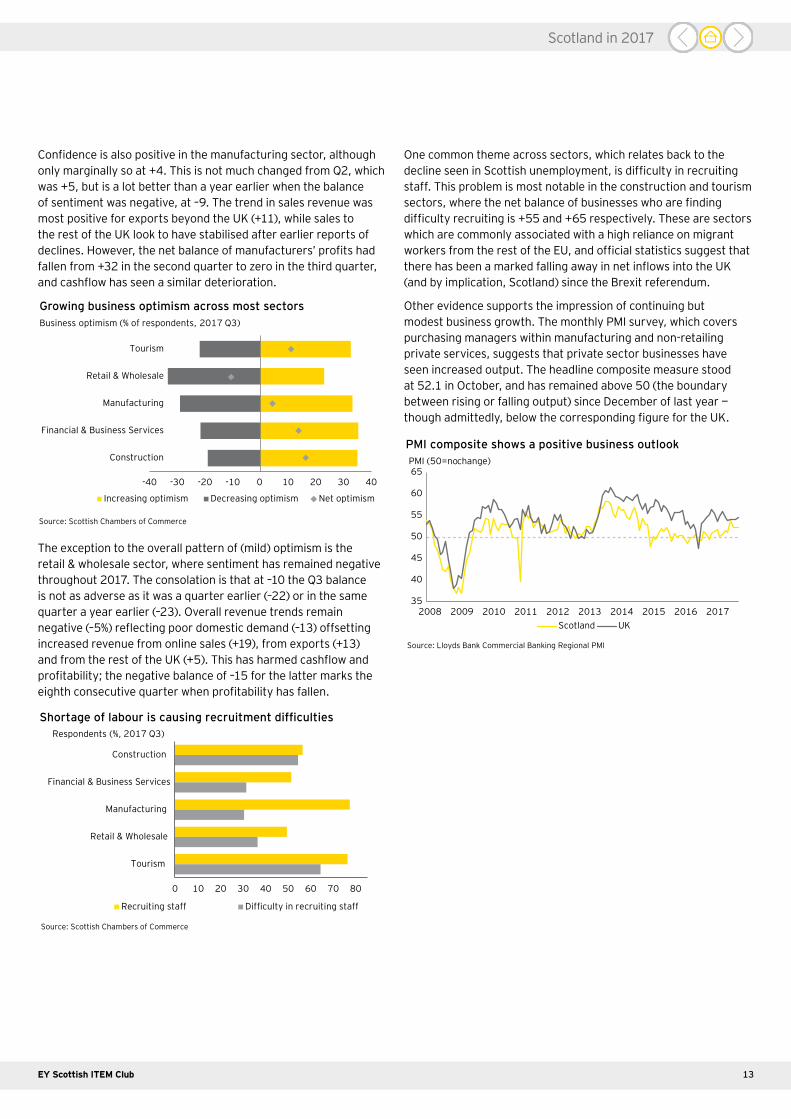

Whereas business confidence remains positive overallIn contrast, the latest Scottish Chambers of Commerce (SCC) Quarterly Economic Indicator for the third quarter shows improving optimism across most sectors.

Net optimism was highest in the construction sector, where the balance of businesses more rather than less optimistic was +16. This was the highest recorded since Q2 2016, and suggests that companies feel that their very weak performance earlier in 2017, discussed above, may be coming to an end.

That said, the more detailed evidence for the sector does suggest some reasons for caution. Construction companies’ sales revenues were also positive overall, but with a balance of +3, markedly less so than in both the previous quarter (+18) and the same quarter a year earlier (+23). It seems that growth in domestic Scottish revenue has been partially offset by weakening sales to the rest of the UK.

The survey also identifies positive balances for contracts gained, most notably in the private sector, and especially an increasing amount of work-in-progress, so that capacity utilisation remains high at 83%. Cashflow, however, has deteriorated, and 27% of construction companies report that they have applied for credit.

In other sectors, financial and business services and tourism are also displaying confidence, with overall net levels of business optimism at +14 and +11 respectively. The former report similar sales performances from the domestic Scottish market, the rest of the UK, exports and online sales, whereas for tourism online sales are the strongest (+23) and domestic Scottish sales the weakest (+2) — a clear reflection of how that market is changing through time.

Scotland in 2017

13EY Scottish ITEM Club

Confidence is also positive in the manufacturing sector, although only marginally so at +4. This is not much changed from Q2, which was +5, but is a lot better than a year earlier when the balance of sentiment was negative, at –9. The trend in sales revenue was most positive for exports beyond the UK (+11), while sales to the rest of the UK look to have stabilised after earlier reports of declines. However, the net balance of manufacturers’ profits had fallen from +32 in the second quarter to zero in the third quarter, and cashflow has seen a similar deterioration.

Growing business optimism across most sectors

Source: Scottish Chambers of Commerce

Construction

Financial & Business Services

Manufacturing

Retail & Wholesale

Tourism

-40 -30 -20 -10 0 10 20 30 40

Increasing optimism Decreasing optimism Net optimism

Business optimism (% of respondents, 2017 Q3)

The exception to the overall pattern of (mild) optimism is the retail & wholesale sector, where sentiment has remained negative throughout 2017. The consolation is that at –10 the Q3 balance is not as adverse as it was a quarter earlier (–22) or in the same quarter a year earlier (–23). Overall revenue trends remain negative (–5%) reflecting poor domestic demand (–13) offsetting increased revenue from online sales (+19), from exports (+13) and from the rest of the UK (+5). This has harmed cashflow and profitability; the negative balance of –15 for the latter marks the eighth consecutive quarter when profitability has fallen.

Construction

Financial & Business Services

Manufacturing

Retail & Wholesale

Tourism

0 10 20 30 40 50 60 70 80

Recruiting staff Difficulty in recruiting staff

Source: Scottish Chambers of Commerce

Respondents (%, 2017 Q3)

Shortage of labour is causing recruitment difficulties

One common theme across sectors, which relates back to the decline seen in Scottish unemployment, is difficulty in recruiting staff. This problem is most notable in the construction and tourism sectors, where the net balance of businesses who are finding difficulty recruiting is +55 and +65 respectively. These are sectors which are commonly associated with a high reliance on migrant workers from the rest of the EU, and official statistics suggest that there has been a marked falling away in net inflows into the UK (and by implication, Scotland) since the Brexit referendum.

Other evidence supports the impression of continuing but modest business growth. The monthly PMI survey, which covers purchasing managers within manufacturing and non-retailing private services, suggests that private sector businesses have seen increased output. The headline composite measure stood at 52.1 in October, and has remained above 50 (the boundary between rising or falling output) since December of last year — though admittedly, below the corresponding figure for the UK.

35

40

45

50

55

60

65

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Scotland UK

PMI composite shows a positive business outlookPMI (50=nochange)

Source: Lloyds Bank Commercial Banking Regional PMI

Scotland in 2017

14EY Scottish ITEM Club

2017 growth as a whole: slightly stronger than in 2016Based on the evidence, we estimate that overall, Scottish GDP in 2017 is likely to be 0.8% higher in real terms than it was in 2016. This is a welcome improvement on the 0.4% growth of 2016 itself, but is clearly much below historical trends, and is likely to be leaving considerable spare capacity in the economy — though as

noted above, with a reasonably tight labour market. Households’ real disposable incomes are also estimated to be 0.4% up on 2016, but by reducing their net savings (achieved in part by increases in borrowing) consumers will have increased their spending by slightly more: we estimate 0.8%. However, the latter is well-down on 2016’s increase of 2.5%. The Scottish economy has thus experienced a difficult but not a disastrous year, against a global economic background which has proved to be slightly less challenging than perhaps seemed likely a year ago.

That growth has provided modest support to public financesContinuing (albeit modest) economic growth in Scotland has been having a beneficial impact on public finances, especially since devolved tax-raising powers have been taken up in the form of the Land and Buildings Transactions Tax, the Scottish Landfill Tax, and more recently the Scottish Rate of Income Tax.

As evidence of that, the latest edition of Government Expenditure and Revenue Scotland (GERS) shows that the Scottish public sector deficit has fallen, from £14.5bn in 2015/16 to £13.3bn in 2016/17 (including Scotland’s geographic share of North Sea

taxes). Even so, at 8.3% of GDP, that is three times higher than the equivalent figure for the UK. The difference reflects a combination of lower revenues per person and higher government spending.

The main revenues are income taxes, National Insurance contributions and VAT. Corporation taxes are rather smaller, while North Sea revenues, even if based on a geographical rather than a population share of the total, are now very small at £208 million out of a £58 billion Scottish total.

Within that total, devolved tax revenues accounted for £10 billion in 2016/17, up from £5 billion in 2015/16. The introduction of the Scottish Rate of Income Tax accounted for the bulk of this increase, and future growth in employment and wages, as well as other forms of personal income, will similarly impact on the overall Scottish tax-take, going forward.

Currently devolved taxes (£bn)

Tax 2012–13 2013–14 2014–15 2015–16 2016–17

Council tax 1.9 2.0 2.0 2.0 2.1

Non-domestic rates 2.3 2.4 2.5 2.6 2.7

Land and buildings transaction tax (devolved from 2015–16)

– – – 0.4 0.5

Scottish landfill tax (devolved from 2015–16)

– – – 0.1 0.1

Scottish Rate of Income Tax Liabilities (devolved from 2016–17)

– – – – 4.6

Total devolved taxes 4.3 4.3 4.5 5.2 10.0

Source: Scottish Government

Scotland in 2017

15EY Scottish ITEM Club

Scotland’s Growth SectorsAs we noted above, Scotland’s recent growth has varied across sectors, with services generally out-pacing manufacturing, and some marked variations within those broad categories.

In its Economic Strategy 2015 the Scottish Government identified six Growth Sectors in which it believed Scotland has a distinct comparative advantage, implying that these might be expected to generate particularly favourable growth performance.

Food & Drink

Financial & Business Services

Life Sciences

Energy (incl. Renewables)

Sustainable Tourism

Creative Industries

Rest of the Economy

Source: Scottish Government

Share of employment, 2015 (%)

Growth Sectors account for 30% of jobs

3% 7%1%4%

12%

4%70%

Food & Drink

Financial & Business Services

Life Sciences

Energy (incl. Renewables)

Sustainable Tourism

Creative Industries

Rest of the Economy

Source: Scottish Government

Share of employment, 2015 (%)

And 37% of businesses

2%

14%

3%

9%

9%63%

The Scottish Government has recently published estimates for the scale of these six sectors, and for their growth over the period 2010–15.1 These estimates suggest that in 2015 the six accounted for 546,000 jobs in Scotland across over 65,000 businesses. The largest of the six in employment terms was sustainable tourism, which the data suggested provided 212,000 jobs in 2015 (or

11.7% of all jobs in Scotland), whereas the financial & business services sector was estimated to account for nearly 26,000 businesses, 14.4% of Scotland’s total, but only 7.0% of jobs — a reflection of the large number of independent advisers such as accountants and lawyers.

1. Scottish Government, Growth Sector Statistics Database (Scottish Government, 2017).

Scotland in 2017

The six were:

1. Food & drink (including agriculture & fisheries)

2. Creative industries (including digital)

3. Sustainable tourism

4. Energy (including renewables)

5. Financial & business services

6. Life sciences

16EY Scottish ITEM Club

According to the Scottish Government figures, employment growth in these sectors was strong in the 2010–15 period. Of the 142,000 jobs added to the Scottish economy over the period, 59,800 (or 42.2%) were in the six Growth Sectors. However, the relative performance between the Growth Sectors in terms of job creation was mixed. Sustainable tourism, the largest employer, grew fastest at a rate of 4% per annum, contributing 63% of all additional jobs within the Growth Sectors. In contrast, the food & drink sector saw employment fall by 1,500 (or 0.6% per annum) over this period.

In addition, productivity — the average output per worker — was relatively high across most of the Growth Sectors, according to the Scottish Government data. In 2015 values were highest in the energy sector, at over five times the level of the rest of the economy. Only one of the six had lower productivity than average: sustainable tourism, where the average output per worker (£30,200 in current prices) in 2015 was under half that of the rest of the Scottish economy (£80,100).

Unfortunately, the Scottish Government data suggests that while most of the Growth Sectors have high levels of productivity, they have tended to under-perform in terms of productivity growth. Across the period 2010–15 only the creative industries and financial & business services sectors significantly out-performed the rest of the economy, with productivity values increasing at 8.4% and 2.8% a year respectively, while food & drink saw productivity growth that only marginally exceeded that of the rest of the economy. The weakest performance was observed for the energy sector, where productivity values actually fell, by 8.2% a year over this period.

However, as the Scottish Government themselves note, there are several limitations to their dataset. The evidence is taken from the Scottish Annual Business Survey, which provides the level of detail needed to identify ‘life sciences’ and ‘creative industries’, but which is only currently available until 2015. Furthermore, that dataset does not cover financial services, so that the sector described as ‘financial & business services’ is actually just the latter. Meanwhile, the data for ‘sustainable tourism’ includes all tourism activity, while references to ‘the rest of the economy’ exclude parts of agriculture and public sectors.

859095

100105110115120125

2010 2011 2012 2013 2014 2015Food & Drink Financial & Business ServicesLife Sciences Energy (incl. Renewables)Sustainable Tourism Creative IndustriesRest of the Economy

Source: Scottish Government/EY ITEM Club

Employment (2010=100)Job creation has historically been mixed

436

209

125

98

86

80

30

Energy (incl. Renewables)

Food & Drink

Life Sciences

Creative Industries

Financial & Business Services

Rest of the Economy

Sustainable Tourism

0 100 200 300 400 500Source: Scottish Government/EY ITEM Club

2015 Output per worker(£000s, current prices)

Growth Sectors tend to be relatively productive

40

60

80

100

120

140

160

2010 2011 2012 2013 2014 2015Food & Drink Financial & Business ServicesLife Sciences Energy (incl. Renewables)Sustainable Tourism Creative IndustriesRest of the Economy

Source: Scottish Government/EY ITEM Club

Productivity Index (2010=100)

Productivity growth below or in line with the rest of the economy

Scotland in 2017

17EY Scottish ITEM Club

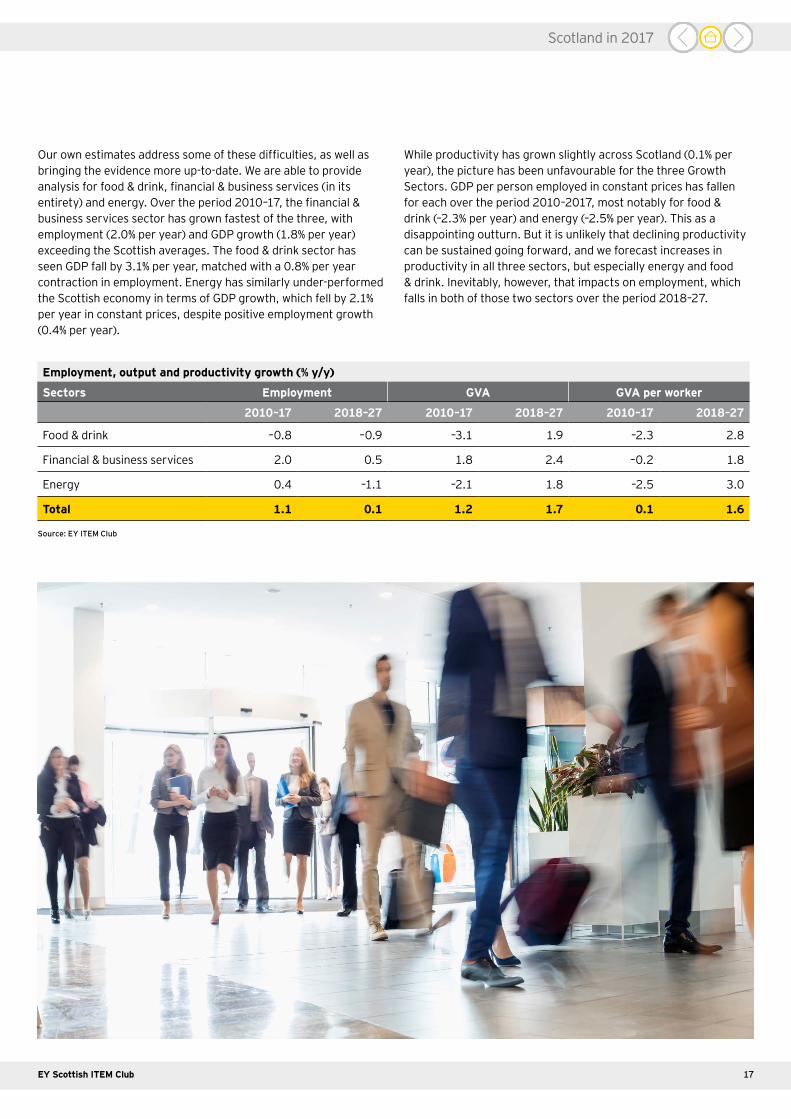

Our own estimates address some of these difficulties, as well as bringing the evidence more up-to-date. We are able to provide analysis for food & drink, financial & business services (in its entirety) and energy. Over the period 2010–17, the financial & business services sector has grown fastest of the three, with employment (2.0% per year) and GDP growth (1.8% per year) exceeding the Scottish averages. The food & drink sector has seen GDP fall by 3.1% per year, matched with a 0.8% per year contraction in employment. Energy has similarly under-performed the Scottish economy in terms of GDP growth, which fell by 2.1% per year in constant prices, despite positive employment growth (0.4% per year).

While productivity has grown slightly across Scotland (0.1% per year), the picture has been unfavourable for the three Growth Sectors. GDP per person employed in constant prices has fallen for each over the period 2010–2017, most notably for food & drink (–2.3% per year) and energy (–2.5% per year). This as a disappointing outturn. But it is unlikely that declining productivity can be sustained going forward, and we forecast increases in productivity in all three sectors, but especially energy and food & drink. Inevitably, however, that impacts on employment, which falls in both of those two sectors over the period 2018–27.

Employment, output and productivity growth (% y/y)

Sectors Employment GVA GVA per worker

2010–17 2018–27 2010–17 2018–27 2010–17 2018–27

Food & drink –0.8 –0.9 –3.1 1.9 –2.3 2.8

Financial & business services 2.0 0.5 1.8 2.4 –0.2 1.8

Energy 0.4 –1.1 –2.1 1.8 –2.5 3.0

Total 1.1 0.1 1.2 1.7 0.1 1.6

Source: EY ITEM Club

Scotland in 2017

18EY Scottish ITEM Club

Forecast for 2018 and beyond

Scotland’s growth will continue to lag the UK’sAlthough forecast to rise steadily over the next three years, economic growth in Scotland will continue to lag behind the UK’s. In 2018 GDP growth is predicted to be 1.4%, increasing to 1.6% in 2019. And for the period to 2022 the annual growth rate is set to average 1.7%, compared with a UK average of 2.0% a year. This represents a slight upgrade on our Summer forecast, which estimated growth over the period to 2022 at 1.3% per year in Scotland and 1.6% across the UK.

A key factor behind 2018’s stronger performance is household spending, which is forecast to grow in real terms by 1.1%, so up

on 2017’s 0.8% increase. This means that spending grows at the same rate as in the UK as a whole, although in that case the 1.1% rise represents a slowdown (1.5% in 2017). The explanation for this lies in a rise in the saving ratio in the UK that is not replicated in Scotland, which in turn is associated with a larger number of over-extended high earners at the UK level deciding to restrain their spending and borrowing in the face of rising interest rates and anxieties over the future path of house prices.

Where the latter are concerned, our forecast is that house price increases will slow in Scotland to 3.4% in 2018 after 4.7% in 2017, and again to 3.1% in 2019. Average annual growth over the next five years ahead is forecast to be 2.5% a year, so below the UK rate of 3.0%; that will, however, mean that housing affordability in Scotland will continue to look better than in other parts of the UK.

The ITEM Club forecast for the Scottish Economy, November 2017

% changes on previous year unless otherwise stated

GVA Personal disposable

income

Consumers’ expenditure

Population 000s

Employment 000s

Unemployment rate %

(Claimant Count)

Working-age migration

000s

2016 0.4 –0.5 2.5 5,405 2,749 5.2 29

2017 0.8 0.4 0.8 5,420 2,821 3.9 11

2018 1.4 1.1 1.1 5,436 2,833 4.0 13

2019 1.6 1.2 1.2 5,449 2,834 4.2 10

2020 1.7 1.1 1.5 5,459 2,837 4.1 7

Source: EY ITEM Club

Forecast for 2018 and beyond

19EY Scottish ITEM Club

Private services will continue to drive growth. Across Scotland, these sectors will contribute four-fifths of GVA growth in 2018, despite representing just half of economic activity. The fastest growing service sectors are forecast to be professional, scientific & technical activities, administrative & support services and information & communication. All of this resembles the pattern for the UK: indeed, the latter is even more reliant on private services for growth than is Scotland.

Public services account for over a fifth (22%) of GVA in 2017, so rather more than the UK as a whole. Overall this has a negative impact on Scottish growth, going forward. Both education and health & social work are forecast to continue modest growth, while public administration & defence activity is forecast to decline, and at a faster rate than for the UK as a whole (–1.5%, compared with –1.2%, in 2018, and –0.5% and –0.2% respectively up to 2022).

One important area of improvement is manufacturing, which is forecast to grow by 1.0% in both 2018 and 2019 after contracting

in 2015 and 2016. Over the next five years manufacturing growth is forecast to pick up to 1.3% a year, in line with the UK average. The continuing expansion in world trade and a competitive exchange rate are two reasons, alongside increases in productivity, which we forecast will rise in the manufacturing sector by 2.8% a year up to 2022 (with the result that employment in the manufacturing sector falls from 187,000 in 2017 to 173,000 in 2022).

Inevitably our forecast for Scottish manufacturing relies on our assumption, discussed in a previous section, that when the UK leaves the EU in early 2019 there will be a transitional arrangement in place, followed by a free trade agreement between the UK and the EU. Clearly if that were not to happen and if Scottish manufacturers were to face tariffs on exports to the EU, then that would alter, and probably weaken, the outlook for the sector.

Public administration & defenceEducation

Agriculture, forestry & fishingHuman health & social work

Other service activitiesTransportation & storage

Arts, entertainment & recreationConstruction

Financial & insuranceManufacturing

Water supplyElectricity, gas, steam & air

Accommodation & food serviceWholesale & retail trade

Real estate activitiesInformation & communication

Administrative & supportProfessional, scientific & technical

Mining & quarrying

-2 -1 0 1 2 3 4 5

ScotlandUKScottish economy

Source: EY ITEM Club

Forecast GVA growth rates by sector: 2018 (%)

Forecast for 2018 and beyond

20EY Scottish ITEM Club

ManufacturingPublic administration & defence

Water supplyElectricity, gas, steam & air

Financial & insuranceAgriculture, forestry & fishing

Mining & quarryingEducation

Transportation & storageHuman health & social work

Other service activitiesWholesale & retail trade

Real estate activitiesAccommodation & food service

Information & communicationArts, entertainment & recreation

ConstructionProfessional, scientific & technical

Administrative & support

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

ScotlandUKScottish Economy

Source: EY ITEM Club

As employment growth weakensAlthough in 2017 employment growth in Scotland was double the UK rate (2.6% compared with 1.3%), the employment outlook over the decade ahead is weaker for Scotland. Employment growth is forecast to slow to 0.4% in 2018 and remain static in 2019. Growth is then expected to resume but remain lacklustre, at 0.1% a year to 2022, which will result in only 23,000 additional jobs over the period. And as UK employment growth slows overall, Scotland

gradually falls behind, with the result that, despite supporting 8.1% of the UK’s jobs in 2017, Scotland contributes just 3.5% of UK jobs growth over the coming half-decade.

Within that, over the forthcoming five years, employment growth will continue to be skewed towards Scotland’s private services. This is largely underpinned by annual growth of 1.5% a year in administrative & support services and 1.4% in professional, scientific & technical services. These sectors will contribute 16,000 and 14,000 jobs growth respectively up to 2022, which more than offset the net loss of 6,000 jobs elsewhere in the economy.

Forecast employment growth by sector: 2017–2022 (% y/y)

Forecast for 2018 and beyond

21EY Scottish ITEM Club

1516

13

10 119

476 456 434396 377

341

050100150200250300350400450500550

2017 2018 2019 2020 2021 202202468

10121416182022

Migration (Scotland) Natural change (Scotland) Population change (Scotland)Migration (UK) Natural change (UK) Population change (UK)

Source: EY ITEM Club

Scottish population growth (y/y, 000s) UK population growth (y/y, 000s)

Components of population change

Furthermore, and arguably of more significance from an economic point-of-view, the working age population is forecast to contract by 62,000 in Scotland over the same period, or 0.4% a year, compared with modest growth of 0.2% a year across the UK. Here, the decline in inward migration is of greater significance, since migrants tend to be of working age and hence improve the economy’s supply potential by raising skills availability. A decline in the working age population will tend to have a downward impact on Scottish GDP growth, offsetting some of the benefits of productivity gains. A contracting working age population nevertheless means that even with weak employment growth, Scotland’s unemployment rate is likely to remain largely unchanged at 4% by 2022.

Lower net migration dampens population growthAn important element of our forecast is the likelihood of reduced inward migration, once the UK exits the EU. Net inward migration into Scotland is forecast to fall from 14,000 a year in 2017 to just 6,000 a year by 2022. Despite that, net migration will contribute over four-fifths (81%) of overall population growth across Scotland over the next five years, compared to under half across the UK (41%). The reason is differences in the rate of natural change (the balance between birth and deaths), reflecting an older age-profile in Scotland. When these two factors are combined, we forecast that the population of Scotland will grow by just 0.2% a year over the period to 2022, equivalent to an additional 58,000 residents, which compares unfavourably with 0.6% a year growth across the UK as a whole.

Forecast for 2018 and beyond

22EY Scottish ITEM Club

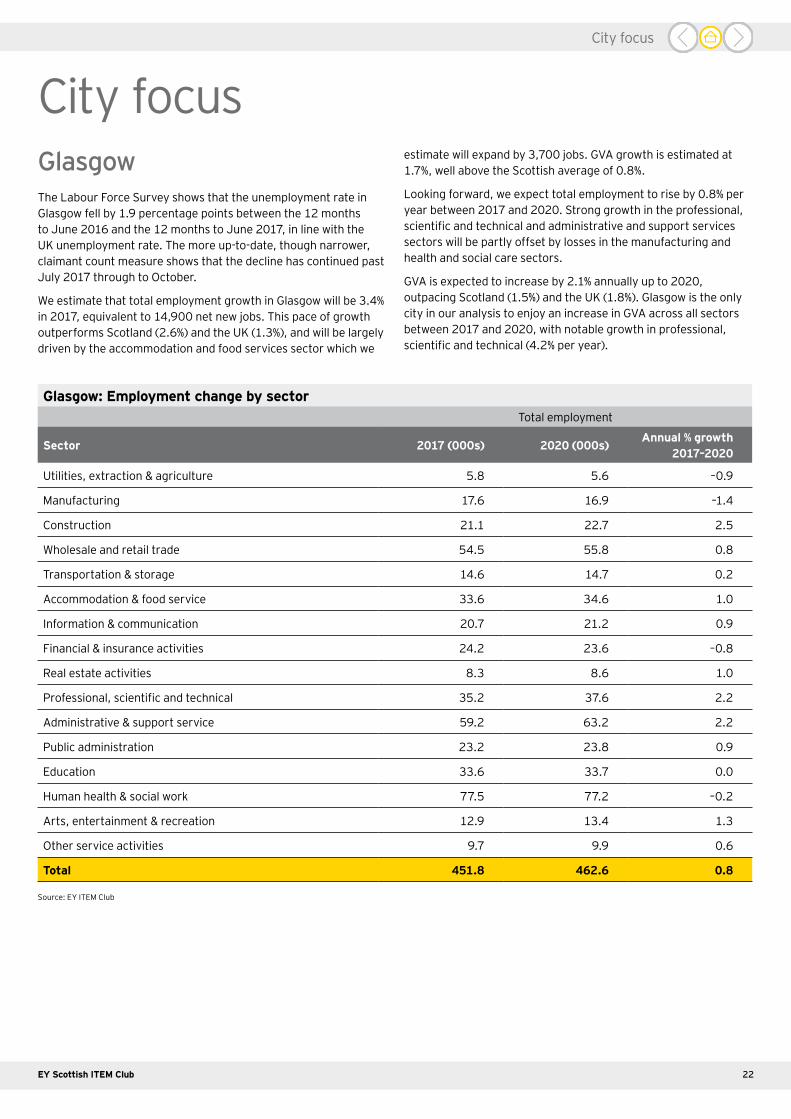

City focusGlasgowThe Labour Force Survey shows that the unemployment rate in Glasgow fell by 1.9 percentage points between the 12 months to June 2016 and the 12 months to June 2017, in line with the UK unemployment rate. The more up-to-date, though narrower, claimant count measure shows that the decline has continued past July 2017 through to October.

We estimate that total employment growth in Glasgow will be 3.4% in 2017, equivalent to 14,900 net new jobs. This pace of growth outperforms Scotland (2.6%) and the UK (1.3%), and will be largely driven by the accommodation and food services sector which we

estimate will expand by 3,700 jobs. GVA growth is estimated at 1.7%, well above the Scottish average of 0.8%.

Looking forward, we expect total employment to rise by 0.8% per year between 2017 and 2020. Strong growth in the professional, scientific and technical and administrative and support services sectors will be partly offset by losses in the manufacturing and health and social care sectors.

GVA is expected to increase by 2.1% annually up to 2020, outpacing Scotland (1.5%) and the UK (1.8%). Glasgow is the only city in our analysis to enjoy an increase in GVA across all sectors between 2017 and 2020, with notable growth in professional, scientific and technical (4.2% per year).

Glasgow: Employment change by sectorTotal employment

Sector 2017 (000s) 2020 (000s)Annual % growth

2017–2020

Utilities, extraction & agriculture 5.8 5.6 –0.9

Manufacturing 17.6 16.9 –1.4

Construction 21.1 22.7 2.5

Wholesale and retail trade 54.5 55.8 0.8

Transportation & storage 14.6 14.7 0.2

Accommodation & food service 33.6 34.6 1.0

Information & communication 20.7 21.2 0.9

Financial & insurance activities 24.2 23.6 –0.8

Real estate activities 8.3 8.6 1.0

Professional, scientific and technical 35.2 37.6 2.2

Administrative & support service 59.2 63.2 2.2

Public administration 23.2 23.8 0.9

Education 33.6 33.7 0.0

Human health & social work 77.5 77.2 –0.2

Arts, entertainment & recreation 12.9 13.4 1.3

Other service activities 9.7 9.9 0.6

Total 451.8 462.6 0.8

City focus

Source: EY ITEM Club

23EY Scottish ITEM Club

EdinburghThe Labour Force Survey shows that the unemployment rate in Edinburgh fell by 2.2 percentage points between the 12 months to June 2016 and the 12 months to June 2017. The more up-to-date, though narrower, claimant count measure shows that the decline has continued in the four months to October 2017.

We estimate that Edinburgh’s total employment is to grow by 4.3%, equivalent to 15,100 net new jobs in 2017 and thus will outperform Scotland (2.6%) and the UK (1.3%). The city has the highest pace of employment growth of all cities in this analysis.

The strongest performing sector will be accommodation and food services, increasing by 4,400 and potentially benefitting from a weaker pound boosting tourism. GVA growth will also outpace Scotland and the UK, with an increase of 2.1% expected in 2017.

Total employment in Edinburgh is forecast to grow by 0.9% per year between 2017 and 2020. Tourism will play a large part in this growth, as the hospitality and cultural sectors are experience the largest increases offsetting falls in construction and public administration. GVA growth is expected to average 2.1% per year between 2017 and 2020, outperforming Scotland (1.5%) and the UK (1.8%).

Edinburgh: Employment change by sectorTotal employment

Sector 2017 (000s) 2020 (000s)Annual % growth

2017–2020

Utilities, extraction & agriculture 4.5 4.4 –0.8

Manufacturing 7.9 7.6 –1.4

Construction 11.2 12.0 2.4

Wholesale and retail trade 41.2 42.9 1.4

Transportation & storage 14.3 14.6 0.8

Accommodation & food service 35.8 37.5 1.5

Information & communication 20.6 21.1 0.9

Financial & insurance activities 38.7 37.4 –1.1

Real estate activities 5.5 5.7 1.4

Professional, scientific and technical 33.7 36.4 2.6

Administrative & support service 27.0 29.1 2.5

Public administration 20.7 19.8 –1.5

Education 32.9 33.5 0.6

Human health & social work 51.4 52.1 0.5

Arts, entertainment & recreation 13.7 14.6 2.2

Other service activities 10.9 11.2 0.8

Total 370.0 380.0 0.9

City focus

Source: EY ITEM Club

24EY Scottish ITEM Club

AberdeenThe Labour Force Survey shows that the unemployment rate in Aberdeen rose by 0.9 percentage points between the 12 months to June 2016 and the 12 months to June 2017. However, the more up-to-date, though narrower, claimant count measure shows that unemployment has declined consistently between July and October 2017.

Aberdeen continues to struggle for momentum in 2017 following a two-year period of low oil prices, although the declines in total employment are lessening. We estimate that the city will experience a 0.1% contraction in employment in 2017, compared

to growth in both Scotland (2.6%) and the UK (1.3%). Similarly, we expect Aberdeen is to experience a contraction in GVA of 1.0% in 2017.

The labour market outlook remains weak, with total employment failing to show any improvement throughout 2017 to 2020. While employment in the utilities, extraction and agriculture and construction sectors are expected to see some gains, public spending cuts will translate into job losses in public administration and health and social work. Despite muted employment growth, GVA growth is expected to average 1.5% per year between 2017 and 2020, in line with growth in Scotland but still lagging behind the UK (1.8% per year).

Aberdeen: Employment change by sectorTotal employment

Sector 2017 (000s) 2020 (000s)Annual % growth

2017–2020

Utilities, extraction & agriculture 24.5 25.3 1.0

Manufacturing 10.9 10.6 –1.2

Construction 7.0 7.1 0.9

Wholesale and retail trade 21.3 21.5 0.2

Transportation & storage 10.2 10.1 –0.3

Accommodation & food service 15.0 15.2 0.3

Information & communication 4.0 4.1 0.6

Financial & insurance activities 1.6 1.6 –0.5

Real estate activities 2.0 2.0 –0.5

Professional, scientific and technical 23.1 23.5 0.6

Administrative & support service 13.9 14.2 0.6

Public administration 8.5 7.9 –2.4

Education 10.1 9.9 –0.6

Human health & social work 27.0 26.4 –0.7

Arts, entertainment & recreation 3.8 3.9 0.8

Other service activities 3.2 3.2 –0.3

Total 186.2 186.3 0.0

City focus

Source: EY ITEM Club

25EY Scottish ITEM Club

DundeeThe Labour Force Survey shows that the unemployment rate in Dundee fell by 4.5 percentage points between the 12 months to June 2016 and the 12 months to June 2017. The more up-to-date, though narrower, claimant count measure shows that the decline has continued, although more slowly, past July 2017.

Total employment within Dundee is expected to increase by 1.9% in 2017, equivalent to 1,500 net new jobs. While this pace of growth lags behind Scotland (2.6%), it outperforms the UK (1.3%). Growth will be mainly concentrated in accommodation and food services and information and communication sectors as the gaming cluster

in the area continues to develop. GVA is expected to grow at a slower pace of 0.4%, falling behind both Scotland and the UK.

Looking ahead, total employment growth in Dundee is expected to slow to just 0.2% per year between 2017 and 2020. Notable job losses in the health and social care and manufacturing sectors will offset the gains made elsewhere.

However, the pace of GVA growth is expected to pick up between 2017 and 2020, rising to 1.5% per year in line with Scotland. Strong growth is expected in the public administration sector as the new social security agency is due to open in the city and be fully operational by 2021.

Dundee: Employment change by sectorTotal employment

Sector 2017 (000s) 2020 (000s)Annual % growth

2017–2020

Utilities, extraction & agriculture 0.8 0.8 –0.9

Manufacturing 5.0 4.8 –1.4

Construction 3.9 4.1 1.5

Wholesale and retail trade 13.2 13.3 0.2

Transportation & storage 2.0 2.0 –0.3

Accommodation & food service 8.2 8.3 0.4

Information & communication 3.6 3.7 0.8

Financial & insurance activities 1.3 1.3 –0.8

Real estate activities 1.2 1.2 0.0

Professional, scientific and technical 4.0 4.1 1.3

Administrative & support service 3.7 3.8 1.3

Public administration 5.5 6.1 3.2

Education 8.6 8.5 –0.5

Human health & social work 17.0 16.6 –0.7

Arts, entertainment & recreation 2.4 2.4 0.8

Other service activities 2.2 2.2 –0.1

Total 82.6 83.2 0.2

City focus

Source: EY ITEM Club

26EY Scottish ITEM Club

Perth and KinrossThe Labour Force Survey shows that the unemployment rate in Perth and Kinross fell by 0.5 percentage points between the 12 months to June 2016 and the 12 months to June 2017. The more up-to-date, though narrower, claimant count measure shows the decline has continued past July 2017.

Total employment in Perth and Kinross is expected to rise by 2,500 jobs in 2017, equivalent to 3.3% growth, and outpacing Scotland and the UK. Gains in the agriculture and accommodation and food service sectors underpin such gains. Overall GVA growth for 2017 is estimated to average 0.4%.

Despite strong growth in 2017, employment opportunities are forecast to be muted between 2017 and 2020. Government spending cuts are likely to cause job losses in the public sector, while further contractions in the manufacturing and utilities, extraction and agriculture sectors curtailing growth.

Nevertheless, GVA is set to grow on average by 1.5% annually between 2017 and 2020, in line with the pace of growth in Scotland, although behind the UK (1.8%). At a sectoral level, professional, scientific and technical and information and communications are expected to enjoy the fastest rates of output growth, and will offset the expected decline in public administration.

Perth & Kinross: Employment change by sectorTotal employment

Sector 2017 (000s) 2020 (000s)Annual % growth

2017–2020

Utilities, extraction & agriculture 9.6 9.4 –0.9

Manufacturing 3.8 3.7 –1.3

Construction 5.8 6.1 1.5

Wholesale and retail trade 11.8 11.8 0.1

Transportation & storage 2.6 2.6 –0.3

Accommodation & food service 9.4 9.4 0.2

Information & communication 0.9 0.9 0.8

Financial & insurance activities 1.6 1.6 –0.6

Real estate activities 1.2 1.2 0.4

Professional, scientific and technical 4.3 4.5 1.5

Administrative & support service 4.7 4.9 1.7

Public administration 3.6 3.3 –2.1

Education 5.6 5.6 –0.3

Human health & social work 8.5 8.4 –0.5

Arts, entertainment & recreation 2.8 2.9 0.9

Other service activities 2.0 2.0 –0.4

Total 78.3 78.4 0.0

City focus

Source: EY ITEM Club

27EY Scottish ITEM Club

StirlingThe Labour Force Survey shows that the unemployment rate in Stirling fell by 0.9 percentage points between the 12 months to June 2016 and the 12 months to June 2017. However, the more up-to-date, though narrower, claimant count measure shows that unemployment increased marginally between July and October 2017.

Total employment in Stirling is expected to grow by 3.6% in 2017, creating 1,900 net new jobs, and outperforming Scotland and the UK. Growth is being driven by the accommodation and food

services, and wholesale and retail sectors, which are expected to create 700 and 300 new jobs respectively.

Despite strong growth expected in 2017, employment growth is expected to average only 0.3% annually between 2017 and 2020.

In contrast to the weak employment outlook, GVA is expected to remain positive throughout the forecast period, rising 1.6% annually between 2017 and 2020. GVA growth in Stirling is expected to outperform Scotland and just fall behind the UK (1.8%). Professional, scientific and technical and administrative and support services are expected to enjoy the fastest rates of growth, offsetting declines in public administration.

Stirling: Employment change by sectorTotal employment

Sector 2017 (000s) 2020 (000s)Annual % growth

2017–2020

Utilities, extraction & agriculture 2.0 1.9 –0.9

Manufacturing 3.0 2.8 –1.5

Construction 3.4 3.6 2.1

Wholesale and retail trade 8.6 8.7 0.5

Transportation & storage 1.5 1.5 –0.1

Accommodation & food service 5.7 5.8 0.7

Information & communication 2.0 2.0 0.6

Financial & insurance activities 3.0 2.9 –0.9

Real estate activities 0.8 0.8 0.7

Professional, scientific and technical 3.3 3.5 1.8

Administrative & support service 4.3 4.5 1.8

Public administration 2.6 2.5 –1.9

Education 5.0 5.0 –0.1

Human health & social work 5.3 5.3 –0.3

Arts, entertainment & recreation 1.9 2.0 1.1

Other service activities 1.3 1.3 –0.1

Total 53.7 54.2 0.3

City focus

Source: EY ITEM Club

28EY Scottish ITEM Club

InvernessClaimant count data show that unemployment in Inverness has fallen consistently throughout January to October 2017.

Total employment growth in Inverness is expected to grow by 1,300 jobs throughout 2017, an increase of 2.6%. This pace of growth aligns with growth in Scotland, and outperforms the UK (1.3%). Growth is driven by the accommodation and food, transport and storage, and wholesale and retail sectors. GVA growth in 2017 is expected to average 0.7%, below Scotland (0.8%) and the UK (1.5%).

Despite strong employment growth throughout 2017, employment within Inverness is forecast to contract by 0.1% per year between 2017 and 2020. Job losses in the health and social care sector alongside public administration contractions caused by fiscal tightening underpin the decline.

Despite the weak labour market outlook, GVA growth is expected to average 1.3% per year between 2017 and 2020, below both the Scottish (1.5%) and the UK (1.8%) averages. The professional, scientific and technical and information and communications sectors are expected to be the fastest growing sectors, partly offsetting the losses forecast in public administration and education.

Inverness: Employment change by sectorTotal employment

Sector 2017 (000s) 2020 (000s)Annual % growth

2017–2020

Utilities, extraction & agriculture 1.2 1.2 –0.7

Manufacturing 1.9 1.8 –1.4

Construction 3.3 3.5 1.7

Wholesale and retail trade 9.2 9.2 –0.1

Transportation & storage 3.0 3.0 –0.5

Accommodation & food service 3.7 3.7 0.2

Information & communication 1.6 1.7 0.8

Financial & insurance activities 0.5 0.5 –0.9

Real estate activities 0.5 0.5 0.3

Professional, scientific and technical 3.0 3.2 1.4

Administrative & support service 2.5 2.6 1.5

Public administration 2.7 2.6 –2.1

Education 2.1 2.1 –0.5

Human health & social work 13.3 13.1 –0.6

Arts, entertainment & recreation 1.3 1.3 0.6

Other service activities 1.5 1.5 –0.5

Total 51.5 51.4 –0.1

City focus

Source: EY ITEM Club

29EY Scottish ITEM Club

Region and city outlook: Scotland compared to the rest of the UK

0.5 1 1.5GVA % cagr

Source: EY ITEM Club

20 2.5

North East

Yorkshire & Humberside

North West

East Midlands

West Midlands

East

South East

London

South West

Wales

Scotland

2017–20 2014–17

Source: EY ITEM Club

Jobs ‘0000 50 100 150 200 250 300 350

North East

Yorkshire & Humberside

North West

East Midlands

West Midlands

East

South East

London

South West

Wales

Scotland

2017–20 2014–17

GVA growth 2014–17 and 2017–20

Employment Growth 2014–17 and 2017–20

City focus

30EY Scottish ITEM Club

Cities with Scotland included 2017-20 GVA

Cities with Scotland Employment

–1

0

1

2

3

4

5

6

2014-17 2017-20

Tees

ide

Sund

erla

nd

New

cast

le

Hul

l

Leed

s

Shef

field

Live

rpoo

l

Man

ches

ter

Birm

ingh

am

Oxf

ord

Pom

pey

Milt

on K

eyne

s

Luto

n

Read

ing

Sout

ham

pton

Sout

h Co

ast

Tham

es V

alle

y

Bris

tol

Lond

on

Exet

er

Corn

wal

l

Card

iff

Cam

brid

ge

E A

nglia

Stirl

ing

Pert

h

Inve

rnes

s

Glas

gow

Edin

burg

h

Dund

ee

Abe

rdee

n

GVA

% c

agr

Source: EY ITEM Club

-4

-3

-2

-1

0

1

2

3

4

5

6

2014-17 2017-20

Tees

ide

Sund

erla

nd

New

cast

le

Hul

l

Leed

s

Shef

field

Live

rpoo

l

Man

ches

ter

Birm

ingh

am

Oxf

ord

Pom

pey

Milt

on K

eyne

s

Luto

n

Read

ing

Sout

ham

pton

Sout

h Co

ast

Tham

es V

alle

y

Bris

tol

Lond

on

Exet

er

Corn

wal

l

Card

iff

Cam

brid

ge

E A

nglia

Stirl

ing

Pert

h

Inve

rnes

s

Glas

gow

Edin

burg

h

Dund

ee

Abe

rdee

n

GVA

% c

agr

Source: EY ITEM Club

City GVA growth 2014–17 and 2017–20

City Employment Growth 2014–17 and 2017–20

City focus

31EY Scottish ITEM Club

Risks and uncertainties

The main area of uncertainty affecting the Scottish economy remains Brexit. Recent months have seen only limited progress towards agreement between the UK Government and the EU, despite Theresa May’s speech in Florence on 22 September. The Prime Minister stated that the UK wants a transition (or ‘implementation’) arrangement, during which current trading rules would essentially continue, market access remain unchanged, the UK would continue to make payments to the EU budget, and there would be continued freedom of movement of people (albeit with EU visitors to the UK being registered as they arrive). The rulings of the European Court of Justice would also be taken into consideration by UK courts.

However, UK government ministers appear divided on what a transition agreement might mean in practice and especially how long it should last, while the EU is unwilling to make a commitment until there has been more progress on the size of the ‘divorce bill’, the future of the Irish border, and citizens’ rights. There is also great uncertainty about what trade deals, if any, the UK might be able to strike with third nations, and how quickly, and what the impact of those on domestic producers, including those in Scotland, might be.

As a result, several business organisations have called for greater clarity from the Government, arguing that the danger of a ‘cliff edge’ exit for the UK from the EU at the end of March 2019 is impacting on business decisions, particularly regarding investment. The evidence presented in this report on declining investment by Scottish businesses seems to support that judgement. The risk is that these anxieties will get worse before they get better (if indeed they do get better).