europe an international benchmark of private banks advisory services

TRANSCRIPT

$CompanySe ctorNa me$ Europe Sector research360 _SR

keplercheuvreux.com

F

Full report

Europe

09 March 2016

X X

An international benchmark of Private Banks Advisory services What’s it all about? Most European private banks are undergoing a small revolution: new regulatory constraints, fresh competition from robo-advisers, new expectations from an increasingly international and younger clientele, new technologies, etc. In this context, many private banks have launched strategic projects to adapt their product range, segment their clients, as well as to price or digitise their services. Advisory services are at the heart of these challenges, and many banks would like to develop and structure this field, since they see it as a promising bridge business in a context where discretionary mandates are becoming less profitable. Our December 2015 survey sampled 160 private banking professionals across Europe. The objective was to take stock of the practices at European private banks, based on our participants’ answers as well as testimony from more than 50 private banks (CEOs, Heads of Research, CIOs, Heads of Advisory, etc.), robo-advisers, regulators, consultants and Kepler Cheuvreux’s experts. Indeed, there are numerous studies on Wealth Management in the Street. Our differentiating approach has been to give the floor to the players.

keplercheuvreux.com 2

About Kepler Cheuvreux

Kepler Cheuvreux is a leading independent European financial services group specialised in advisory services and intermediation. Headquartered in Paris, the group employs around 550 people. This multi-local company is also present in Amsterdam, Boston, Frankfurt, Geneva, London, Madrid, Milan, New York, Paris, San Francisco, Stockholm, Vienna and Zurich. Kepler Cheuvreux’s activities are organised around four main business lines: Equities, Debt & Derivatives, Corporate Finance and Investment Solutions. www.keplercheuvreux.com

About our SmartAdvisory Services

Our approach is to help private banks to:

Optimise their cost base and outsource some time-consuming tasks (e.g. production of research sheets).

Develop advisory services with a flexible cost basis, before revenues are generated.

Gain market share as well as offer investment products that could interest clients and are complementary to their current line-up.

Answer their clients’ investment idea requests with access to our own Advisory Desk.

Our SmartAdvisory services offering aimed at Private Banks includes:

Production of research sheets for equities/bonds (based on our research universe and data). The content, format and branding are customisable. These sheets can be produced in English or local languages, for private bankers only or sent to retail clients. Kepler Cheuvreux covers almost 700 stocks and 150 bond issuers.

Access to the Kepler Cheuvreux’s Advisory Desk to provide/push investment ideas and to help private bankers answer any requests from their clients.

Structured products.

Bond portfolio review/optimisation.

Our team:

Sarah Ablin Strategic Project Manager +33 1 70 81 58 13 [email protected]

Audrey Germain Junior Cross Asset Sales +33 1 70 81 57 20 [email protected]

Frederic Jardry Cross Asset Sales +33 1 53 65 35 58 [email protected]

Bénédicte Thibord Global Head of SmartConnect Services +33 1 53 65 36 58 [email protected]

keplercheuvreux.com 3

About the Author

The survey was carried out by Bénédicte Thibord, Global Head of SmartConnect Services, with the help of Grégoire Prengère and Audrey Germain.

Bénédicte Thibord has been Global Head of SmartConnect services at Kepler Cheuvreux since 2013 and was previously Head of Corporate Access and Marketing at CA Cheuvreux from 2008 to 2013. She has also been in charge of the new service offering dedicated to Private Banks, SmartAdvisory, since April 2015. Previously, she worked for ten years at PricewaterhouseCoopers as a banks/insurance auditor, then as a capital markets consultant. She holds a Master's in banking, finance and insurance from University of Paris Dauphine, as well as a Certified European Financial Analyst diploma from the French Society of Financial Analysts (SFAF). She has been teaching a course in financial communication at the French business school HEC for the last 12 years.

Thank you

We would like to thank the following people for their contribution to the present study. Indeed, there are numerous studies on Wealth Management in the Street. Our differentiating approach has been to give the floor to the players.

Private banks

Edouard Crestin-Billet, Partner, 1875 Finance

Marco Aldo Vicentini, Head of Advisory department, Banca Cesare Ponti

Manlio Unfer, Director, Group Head of Private Banking, Banque Havilland

François Oesch, Chief Investment Officer, Banque Heritage SA

Fabrizio Croce, Senior Equity Analyst Financials, Bank J. Safra Sarasin AG

Marie-José Billy, Wealth manager, Banca Leonardo

Gaetano Zanon, CFA, CQF, Managing Director, Banque Morval

Martial Godet, Head of Advisory & Execution services, BNP Paribas Wealth Management

Antoine Denis, CAIA, Head of Advisory, Bordier & Cie

Julien Collin, Head of Markets & Investment Solutions, CA Indosuez Wealth Management

Roberto Cerratti, Vice President, Head of Investment Consulting, Private Banking & Wealth

Management Switzerland, Credit Suisse

Klaus Niedermeier, Head of Research, Deutsche Apotheker- und Ärztebank

Muriel Tailhades, Chief Investment Officer, Edmond de Rothschild (France)

Dominique Carrel-Billiard, CEO, Financière de l’Echiquier

Sébastien Collard, Head of Portfolio Management, ING Luxembourg Private Banking

Silvia Bocchiotti, Investment Director, LCL Banque Privée

Catherine Reichlin, Head of Research, Mirabaud

Dirk Gojny, Investment professional, National Bank

Philippe Bourquin, Financial Adviser, NBK Banque Privée (Suisse)

Alessandra Gaudio, CIO, Swiss Life Banque Privée

Manuela d’Onofrio, Head of Global Investments & Marketing, Unicredit SpA

Head of Investment Research and Communications, Dutch Private Bank (anonymous)

Head of Advisory, Luxembourg Private Bank (anonymous)

Senior Portfolio Advisor, Swiss Private Bank (anonymous)

Head of Advisory, Swiss Private Bank (anonymous)

keplercheuvreux.com 4

Other stakeholders

Jérôme Charpentier, Senior Manager, Alaincy

Valérie Baudson, CEO, Amundi ETF Indexing & Smart Beta

Philippe Guillot, Executive Directoir, Markets Director, Autorité des Marchés Financiers

Clément Jeanneau, Blockchain France

Caroline Arnould, Head of Sales, Crédit Agricole Titres

Hugues Le Bret, Founder and chairman, Financière des Paiements Electroniques – Compte

Nickel

Meyer Azogui, President, Cyrus Conseil

Daniel Pion, Associate Head of Retail banking sector, Deloitte

Kimberly Urisich, Director, Wealth and Asset Management, Ernst & Young

Leonard de Tilly, CEO, Fundshop

Alexandre Gaillard, CEO & Founder, InvestGlass

Michel Dumont, Founder & CEO, Leyders Associates

Romain Girard, Partner, Progress - IIC Partners

Olivier Paquier, Head of SPDR ETFs France, Monaco, Spain/Portugal, SPDR

The European Banking Federation

Mourtaza Asad-Syed, Founder & CEO, Yomoni

Kepler Cheuvreux

Alfredo Alonso, Equity Research Analyst

Mats Anderson, Equity Research Analyst

Sebastien Barthelemi, Head of Credit Research

Anna-Maria Benassi, Head of Italian Equity Research

Pierre Boucheny, Head of French Equity Research

Robert Buller, Global Head of Account Management

Peter Casanova, Equity Research Analyst

Romain Chassard, Managing Partner, Investment Solutions

Jacques-Henri Gaulard, Head of Banking Sector Research

Mathieu Labille, Deputy Global Head of Research

François Mallet, Senior Managing Director, Global Head of Strategic cooperation

Nicolas Miara-Godet, Head of Investment Solutions

Thomas Neuhold, Equity Research Analyst

Benoît Petrarque, Equity Research Analyst

Christopher Potts, Head of Economy & Strategy

Filippo Prini, Equity Research Analyst

Patrick Raffard, Head of Credit Innovation

Eric Rettien, Head of Retail Services

Stéphane Rio, Global Head of Debt & Derivatives

Nicolas Tremel, Economy & Strategy Analyst

Romain Turquem, Head of Marketing, Investment Solutions

keplercheuvreux.com 5

Contents

Introduction by Jacques-Henri Gaulard, Head of Banking Sector Research, Kepler Cheuvreux ......... 6

Main highlights ............................................................................................................................ 7

MiFID II and Robo-advisers: back to the future ............................................................................ 12

MiFID II Story ..................................................................................................................................... 12

Who’s afraid of robo-advisers? ......................................................................................................... 15

Client segmentation, advisory and service pricing ....................................................................... 20

The importance of advisory services in strategic plans .................................................................... 20

The client segmentation story ........................................................................................................... 23

All about advisory teams ................................................................................................................... 25

Private banks’ investment services: the usual suspects ................................................................... 28

In the mood for Advisory & Research .......................................................................................... 33

Everything you always wanted to know about research organisation and distribution* but were

afraid to ask ....................................................................................................................................... 33

Anatomy of research documentation ............................................................................................... 34

Digitalisation: modern times ....................................................................................................... 36

Once upon a time in private banks ................................................................................................... 36

For a few dollars more… .................................................................................................................... 37

Appendices ................................................................................................................................ 42

Survey sample and methodology ...................................................................................................... 43

Sample details ................................................................................................................................... 45

Disclaimers ........................................................................................................................................ 46

keplercheuvreux.com 6

Introduction by Jacques-Henri Gaulard, Head of Banking Sector Research,

Kepler Cheuvreux Private banking is a phenomenally resilient industry. How many times have we heard that it is in

structural decline over the last twenty years? I would not even dare to count.

Having analysed private banks since 1997 as well as having worked at one, I can assure you that

there has not been a single year without the announcement of major consolidations, a collapse in

margins, the end to an industry overly dependent on banking secrecy, or worse. However, the HNWI

(High Net Worth Individual) market keeps growing. According to the 2014 McKinsey Global Wealth

Management Survey, the wealth management market represented more than USD50trn in 2013, and

was expected to post a CAGR of 8% between now and 2018E. It is worth noting that such growth has

been consistent for as long as the wealth management market has been tracked, in the early 2000s.

Not bad for a dying industry.

Such resilience is all the more remarkable as the private banking market has not exactly been a bed

of roses since 2009. Banking secrecy has all but disappeared, requests for information exchange from

cash-strapped governments have proliferated, and a persistently low interest rate environment has

not helped client performance. Despite this unfavourable environment, the industry is still standing.

Of course, it had to adapt. The end of banking secrecy triggered a major strategic reassessment.

"Private banking" became increasingly the less associated politically "wealth management", margins

fell sharply, costs had to be reduced, investment processes had to be streamlined, and private

banking became more institutionalised. At the same time, big retail banks started to extract a

"private banking" client base from their domestic networks, and digitalisation started to become

more important in client interaction, while regulatory demands were becoming more taxing.

When I read Kepler Cheuvreux’s survey “Private Banks: The Advisory awakens”, I was quite taken

by its conclusions. Private banks have worked hard to remain relevant. They have embraced

digitalisation and regulation to improve their client experiences and make them as personalised and

as seamless as before the crisis, but to be able to do this, they had to overhaul their processes, their

investment policies and compliance.

From where I sit, the use of research documents is an increasingly common practice used to pass

along investment ideas in an advisory context. Having also worked for many brokers in my career, I

can safely say that Kepler Cheuvreux’s research product is both thorough and differentiated. With

our base of extremely well-informed local analysts, Kepler Cheuvreux is able to go where no other

broker has gone before (to continue the SciFi metaphor our SmartConnect team is now famous for!)

and deliver investment ideas that are both relevant and original.

We are very excited to be able to participate in the evolution of the private banking industry, and

embrace its phenomenal resilience. Enjoy the read - and the ride!

keplercheuvreux.com 7

Main highlights Most European private banks are undergoing a small revolution: new regulatory constraints, fresh competition from robo-advisers, new expectations from an increasingly international and younger clientele, new technologies, etc.

In this context, many private banks have launched strategic projects to adapt their product range, segment their clients, as well as to price or digitise their services. Advisory management is at the heart of these challenges, and many banks would like to develop and structure this field, since they see it as a promising bridge business in a context where discretionary mandates are becoming less profitable.

Our December 2015 survey sampled 160 private banking professionals across Europe. The objective was to take stock of the practices at European private banks, based on our participants’ answers as well as testimony from more than 50 private banks (CEOs, Heads of Research, CIOs, Heads of Advisory, etc.), robo-advisers, regulators, consultants and Kepler Cheuvreux’s experts.

MiFID II and Robo-advisers: back to the future - More than 40% of respondents are worried about the potential impacts of MiFID II

and close to one-quarter think that this could create new business opportunities for private banks. It should also be noted that one out of five respondents is involved in internal MiFID II projects, while less than 15% either do not know about MiFID II or are not concerned by it.

- The emergence of robo-advisers is being closely watched by private banks: more than half of them are either in a “wait-and-see” position (34%) or already consider these players to be serious competition (23%). Meanwhile, only one person out of six does not feel threatened. We would also note that one-quarter of the sample has little or no knowledge of these new players.

Client segmentation, advisory and service pricing - While one-third of private banks from the sample currently consider advisory

services to be very important, more than two-thirds have integrated these services into their strategic projects for 2016 and/or the medium term.

- Today, access policies for private banks’ advisory services are very heterogeneous and tend to be only loosely structured. Few banks have formalised their policies, and in a number of cases, these policies remain at the discretion of private bankers, depending on their relationships with clients.

- For instance, two-thirds of the private banks in the sample propose some customised investment ideas to their mass affluent clients and roughly 40% provide them with access with their advisory desks (equities/bonds). One in three also propose some tailor-made structured products.

Top financial products preferred by private banking clients:

- European stocks - Corporate high-yield bonds - Corporate investment grade bonds - US stocks - Structured products and Delta one certificates - Subordinated financials

keplercheuvreux.com 8

In the mood for advisory and research - The size of the advisory teams varies greatly and is very correlated to the size of the

Private Banks. Most frequently, their missions include: 1) Selection of investment ideas (notably in case of no brokerage activities or buy-side analyst teams in the Group), 2) Internal support to Private bankers/CRMs for clients bespoke investment requests, 3) Production of research materials (sheets, newsletter, etc.). 55% of surveyed advisory teams have regular contacts with clients independently to CRMs.

- For the purpose of their advisory services, two-thirds of private banks (62%) in our sample intend to reinforce their client research documentation in terms of investment ideas, mainly due to new regulatory constraints (44%) as well as to meet clients’ requests (18%).

- Of the respondents who produce internal research reports, only 23% claim to be satisfied with the quality of the research.

- Around 45% of private banks produce these sheets only for internal use; 55% also distribute them to their clients.

Digitalisation: modern times

- Most of the private banks surveyed expect the deployment of digital tools to allow productivity gains (56%) particularly for “mass affluent” clients (24%).

- Today, practices in terms of digital setup vary by private bank: the most common set-up is a website which offers clients direct access to their portfolio. But it is worth noting that over 25% of the private banks surveyed have not developed any digital set-up

- The main difficulties and barriers to service digitalisation are, according to the private banks surveyed, linked to client data security (30%), cultural reasons, to convince people internally first and then clients (21%), implicated financial budgets (18%) and a lack of internal technical expertise in terms of digitalisation (15%).

Key information in research documents:

- Investment case - Financial data - Company profile - Recommendation

Our latest banking sector report

What’s it all about?

The landscape of banking is changing at a whirlwind pace, and French banks are not immune to it. For the first time since 1995, we believe that all major players will have to significantly amend their business models to face the challenges of technology, energy transition and regulation. Because of these factors going beyond the usual investment horizon (from 2018 for IFRS 9 to 2035 for the energy transition), we believe there are a lot of uncertainties pertaining to the profitability of the sector, its dividend payment capacity and ultimately its share price performance. As a result, for now we have a very pragmatic, short-term view of French bank stocks.

keplercheuvreux.com 9

“The market is dominated by some of the large banks together with local stockbrokers which offer a more personalized advisory without offering a product range considered to be private banking elsewhere, i.e. a low level of sophistication. Some of these stockbrokers have disappeared in recent years because of the overall pressure on investment banking products. Outside the large banks private banking offering the afore mention stockbrokers have been replaced by internet brokers which in turn are transforming into savings portals to cater to larger customer groups and get greater leverage on investments. As such they are in practice leaving private banking. It means that the platforms offering a more traditional private banking offering are increasingly within some of the larger banks in the region which have the resources to keep up with technological change to get economies in this particular business line. ”

Research Corner: Our analysts’ views on Private Banks

“The private banking industry is currently facing a transformation process driven by regulatory and internet driven changes increasing transparency and comparability of services and costs. Another big challenge in the Austrian private banking market is the fact that substantial assets will be inherited by the next generation. Establishing good relationships with the succeeding generation, providing individual, fairly priced solutions and using electronic channels are important factors in order to secure competitiveness. “

Thomas Neuhold Head of Austrian Equity Research

“Spain’s private banking industry remains mostly in hands of Spanish retail banks as a separate business unit, with low levels of sophistication and, in many cases, scarce differentiation versus common retail banking services. In the meantime, only a few specialised competitors have been able to maintain relevant market shares. That said, private banking now faces a significant transformation process, striving for offering a more personalised service, in an environment with historically low interest rates and volatility making clients to become more risk-adverse.”

Alfredo Alonso Equity Research Analyst

Mats Anderson Equity Research Analyst

“Swiss Banks have lost a part of their special attractiveness and are faced with structurally lower revenue margin and constantly growing non-value chain linked cost. We argued in summer 2014 that “Happy Days are over (Report on Swiss wealth managers) and we are firmly convinced these “happy days are not coming back”. This forces the wealth management players to redesign the product factory and find new models.”

Peter Casanova, CFA Equity Research Analyst

“Private banks in the Benelux are mostly part of larger banking operations and are able to benefit from Internet and mobile banking applications developed for the retail clients. Smaller stand alone private banks will struggle with substantial higher IT costs going forward. It is urgent for the Benelux private banks to improve their low ROE of below 10% on average. “

Benoit Petrarque Equity Research Analyst

“In Italy the total assets referred to the private banking world (clients with net available wealth in excess of EUR0.5m) posted relevant growth rates in the last years reaching the outstanding EUR750bn (latest available data) which compares with the EUR4tnt of financial wealth at national level. This is a market still dominated by large banks (with Intesa San Paolo, Unicredit and Ubi commanding a 35% market share), whereas the most active players are becoming the networks of financial advisors, exploiting the leakage of professionals from the traditional banks. We believe that the two most relevant trends in play are: the recruitment of the financial advisors (with the related benefits and costs) and the tailor-made services offered to the clients to retain a pricing premium compared with the cheap solutions (ETF, ETP and passive management).“

Annamaria Benassi | Head of Italian Equity Research Filippo Prini | Equity Research Analyst

Jacques-Henri Gaulard Head of Banking sector Research

keplercheuvreux.com 10

“

CEOs/CIOs Corner

“Market segmentation is squeezed by two opposing forces: regulation, which leads us to select high net worth clients to amortise increasing costs and digitalisation including productivity gains with mass-affluent clients. These challenges are leading some players to shift their strategies too frequently. This is a shame, as building relationships with client based on trust and confidence takes time. An entrepreneurial model, which is more agile by nature, allows for greater adaptation to this ongoing paradigm. There could be an intermediate model between major financial institutions that are more focused on reputational risks and solvency margins than clients and independent ‘boutiques’ that cannot always finance their independence.”

Meyer Azogui, President, Cyrus Conseil

“The private banking sector is undergoing profound changes due to the combined forces of regulatory changes, digitalisation and central banks' low interest rate policies. In short, these forces are leading to the end of complacency and the rise of transparency and convenience. A constant imperative remains the delivery of investment performance for clients and the management of portfolio volatility. Adapting to a new world of lower margins and higher compliance costs requires changes to one's business model. No single formula should prevail as the key to success is eventually going to be proper segmentation of customer targets with matching products and services.”

Dominique Carrel-Billiard, CEO Financière de l’Echiquier

“In spite of new regulatory constraints, clients needs are not changing; the quality of relationships and performance remain the two most important requirements. Because of low return on assets and high market volatility, the generation of steady returns over time is still the main financial objective of our clients. To satisfy this objective, asset managers have to invest on different bases. Exposure to market risk has a significant weight on portfolio performances. Dynamic, tactical allocation and sustainable return depend on the strength of the investment process. “

Edouard Crestin-Billet, Partner, 1875 Finance

“For the first time, the annual client growth of new entrants is poised to exceed traditional players. Fintechs are experiencing good momentum, thanks to real-time information and recommendation simplification. Indeed, it appears that account management and payment methods have been successful. However, it would probably be harder to convince investors to manage their savings through Fintech services, as they are looking for advice.”

Hugues Le Bret, Founder and Chairman of Financière des Paiements Electroniques, Compte

Nickel

”

“In the context of low interest rates and new regulations, private banks must innovate in terms of investment products and more specifically in advisory services. This is an important challenge that should bring more changes in the next few years than those seen in the last twenty.”

Muriel Tailhades, Chief Investment Officer, Edmond de Rothschild (France)

keplercheuvreux.com 11

“

CEOs/CIOs Corner

“Regulation and digitalisation are the two game-changers for wealth management in this new environment. We should innovate and adapt our discretionary and advisory services. This implies new channels of communication, more transparency and more added value.”

Silvia Bocchiotti, Investment Director, LCL Banque Privée

“Wealth management is universally at a turning point, which will probably change the well-established landscape and create opportunities. The key ingredient is always the same: know your clients. But the recipes are changing, rapidly: how to target, reach and keep clients; what is for them the real value proposition; and how to be profitable in a world with lower margins, higher regulation and fiercer competition. Leveraging ‘big data’, content and technology (aggregators, seamless digitisation ‘back to front to client’) to be more targeted, valuable, consistent in our offer to our clients will create a virtuous circle of net new assets, revenue growth and cost efficiency.”

Alessandra Gaudio, CIO, Swiss Life Banque Privée

“The development of strong advisory competences is clearly front-of-mind across the European wealth management landscape. In the face of changing industry dynamics, the need to provide true added-value throughout the investment advice cycle will be key in nurturing existing client relationships as well as developing new ones.”

Gaetano Zanon, CFA, Managing Director, Banque Morval

“The players who want to succeed in adapting their business models to the new standards of lower margins and higher costs will have to strike a delicate balance between cost control and the need to deliver a high level of service. This is particularly true for advisory activity, where economies of scale often contrast with the personalised nature of the service. Quality of service, as one of the only few real differentiators in our industry, is the single most complex critical success factor to implement effectively, as it not only involves mechanical (or technical) aspects but also the more subjective perception clients have of it. Hence, the challenge is finding the right mix between more cost-efficient automated solutions and the old-school, tailor-made approach.”

Manlio Unfer, Director, Group Head of Private Banking, Banque Havilland

”

“Private banking in Luxembourg is focusing on its expertise and should attain the status of international hub it deserves. Luxembourg is developing new tools and new services based on transparency, (digital) information quality and efficient services for clients. We combine our strengths and competences to leverage on our best innovative ideas, operational procedures and talent.”

Sébastien Collard, Head of Portfolio Management, ING

Luxembourg Private Banking

Regulation, information, and digitalization are driving the imagination of Private Banks. Providing Wealth Management services in this “new normal” investment backdrop is a daily challenge as the industry strives to deliver a state of the art investment offering. Investment advisors can be compared to trapeze artists working without a net. Evolving in a zero interest rate environment does not allow room for a single mistake, and innovation is key to meeting our clients’ expectations

François Oesch, Chief Investment Officer, Banque Heritage SA

keplercheuvreux.com 12

MiFID II and Robo-advisers: back to the future

MiFID II Story

More than 40% of respondents are worried about the potential impacts of MiFID II, and close to one-

quarter (22%) think that this could create new business opportunities for private banks. It should also

be noted that one in five respondents is involved in internal MiFID II projects, while less than 15%

either do not know about MiFID II (5%) or are not concerned about it (9%).

Chart 1: MiFID II

I am very concerned 44%

I don't know about MiFID 2

5%

It will not affect me 9%

It will create new business

opportunities 22%

I am involved in the internal project

20%

MiFID II: Where do we stand? “The entire regulatory process incorporating how the regulators enact incoming rules and how we interact with the industry is changing. MiFID I was voted on in 2004 and implemented in 2007, and then there was the financial crisis of 2008, which led to further talks resulting in MiFID II, which was voted on in 2014 and is due for implementation in either 2017 or 2018. Regulation exists to define a floor and a ceiling on what firms can do, must do, and could do. We look at firms’ actions from every angle, and we see that, in the context of regulation, they can either be doing too much or too little, and what we want is a regulatory environment where everybody can work and trade together in a balanced ecosystem.”

Philippe Guillot, Executive Director, Markets Director, Autorité des Marchés Financiers

“Publication of the Delegated Acts by the EC has been delayed. Initially they were due to be published in July, 2015 and now some commentators are speculating that they will arrive only by end H1, 2016. Publication so late has made the ability to adhere to the original Jan 2017 implementation date impractical. Therefore, the implementation has been delayed to January, 2018 (although that date still has to be ratified by the European Parliament). Post publication of the Delegated Acts both the European Parliament and European Council have 3 months (with a possible extension of 3 further months) to raise further objections. The main reason of the delay has been intense lobbying in the background by the Treasuries of member governments. In particular, there was a letter from UK, French & German Treasuries on 25th August which sought clarity and changes to several sections of the Delegated Acts. “

Robert Buller, Global Head of Account Management, Kepler Cheuvreux

keplercheuvreux.com 13

MiFID II: what operational impacts for Private Wealth Managers?

“The separation of Execution and Research under MiFID II means that Research can be paid for in one of three ways: 1) from the asset manager’s P&L; 2) through Commission-Sharing Agreements (CSAs); and 3) through ‘hard dollars’ (a daily charge against the NAV of the fund). The majority of large sophisticated Institutional asset managers are likely to choose payment for Research via CSAs. However, our feedback from meetings with private wealth managers that manage non-discretionary portfolios is that they are leaning strongly towards payment for Research from their own P&Ls due to the complexity of creating a research budget for each underlying private client.”

Robert Buller, Global Head of Account Management, Kepler Cheuvreux

“For private banking, MiFID is not only a question of reinforcing policies and procedures, stricter KYC due diligence and recording investment advice - which will already be a headache to implement (ex- annual checking of client financial capacity to bear losses, recording, etc.); it also presents key structural business questions that need to be addressed. For instance, private banks will have to reshape their offer (dependent advisory service, added-value RTO, etc.) if they want to preserve their current inducement-based economic model. To a greater extent, client access to investment products and advisory services will need to be tailored to client profiles, bearing in mind each fund’s target market. It will require a complete review of the current catalog of products available for clients with, additionally, more transparency on fees paid by clients.

In a nutshell, given the deep change and critical decisions ahead for private banks to be MiFID-compliant, the one-year delay is not an excuse to freeze MIF adaptation plans but a welcome grace period to hopefully be ready on time.”

Jérôme Charpentier, Senior Manager, Alaincy

“The postponement of the introduction of MiFID II gives the banking sector additional time to adopt its business model to a new and much more transparent environment. Together with the challenge of more regulation and increasing competition from fintechs, banks need to focus on tailor-made solutions for clients that fit costumer needs exactly.”

Dirk Gojny, Investment professional, National-Bank

keplercheuvreux.com 14

MiFID II, Wealth managers & Retail Execution

25% of French retail market

share

7 million orders processed each

year

EUR22 billions in cash

throughout the year

Leader in France for

execution services aimed at retail clients (Retail & Private Banks)

Why make this offer appealing to retail or private banks?

1. It gives them access to optimised execution services for their clients

2. It helps them improve the quality of their retail execution services by providing additional features for their clients (the “cancel and replace” option, management of IPOs and corporate actions, etc.).

3. It allows them to outsource retail execution services to reduce the cost of their existing setup: Kepler Cheuvreux provides both the crossing and netting of orders, generating substantial gains for large flows. In Q3 2015, Kepler Cheuvreux improved retail clients’ orders by 0.68bps compared to Euronext.

Eric Rettien Head of Retail Services

Kepler Cheuvreux

“When it comes to transforming private bankers’ model portfolios, recommendations and best investment ideas into tangible transactions for their clients, Kepler Cheuvreux has a wide range of high-performing solutions. With more than 20% of French retail & private bank market share and traded volume up to EUR2bn per day in 2015, Kepler Cheuvreux is a leading player for execution services. Our technical architecture provides secure, widely available and continuous access to European, North American and Asian markets. We are keen to foster competition between the trading venues and to promote technological innovation to reduce implicit and explicit transaction costs. To achieve this, we have developed a unique multi-venue offer for private banking clients. Thanks to enhanced technology via our Smart Order Router, Kepler Cheuvreux is able to capture best prices on primary and alternative markets (Euronext, Chi-X, Turquoise, BATS, Blink MTF, etc.).”

Eric Rettien, Head of Retail Services, Kepler Cheuvreux

keplercheuvreux.com 15

Who’s afraid of robo-advisers?

The emergence of robo-advisers is being closely watched by private banks: more than one-third of

them are either in a “wait-and-see” position (34%) or already consider these players to be serious

competitors (23%). Meanwhile, only one person in six does not feel threatened by them (14%). We

would also note that one-quarter of the sample has little or no knowledge of these new players.

Chart 2: Robo-advisers

“The emergence of a new group of digital wealth management firms offering automated

investment advice services has quickly become one of the most frequently debated topics in the

industry. Comparisons are being made to the travel industry of the 1990s, when the travel agent

model lost ground to online services such as Expedia, and some media outlets and analysts are

predicting that the emerging start-ups will revolutionise how wealth management advice is

provided. Yet others have discounted and labelled this “robo-advisor” movement as unproven

and believe its solutions are no match for human personalised investment advice.”

Source: Advice goes virtual report, Ernst & Young

keplercheuvreux.com 16

1 Digital entrants use a combination of simplified client experience, lower fees and increased transparency to offer automated advice direct to consumers.

These firms have created direct-to-consumer models to provide the basic elements of wealth management advice, minimising the traditional reliance on human advisors and ultimately changing the fundamental economics and scalability of underserved segments. They have done so by combining the basic components of a wealth management offering with simple user interfaces, seamlessly integrated and automated technology, lower pricing with greater transparency, and client-relevant digital content.

2 The new models have the potential to make advice for the mass market* feasible at last.

The changes in economics and scalability enable these players to reach client segments that have traditionally been out of reach for wealth managers. The firms have made it possible to bring investment advice to the masses and unlock the significant potential of those underserved segments.

3 The changes digital firms have introduced are here to stay, so traditional players need to determine if and how they want to approach them.

The current market share of these firms is marginal (concentrated mainly at the lower end of the market), and their underlying business models are still untested in down markets. However, we believe their steps to streamline clients’ online experience, provide greater transparency and improve the economics for the mass segments are irreversible. While traditional firms will continue to focus on the wealthier segments, those that also want to compete for the lower end of the market and/or improve their clients’ digital experience will need to determine if and how to adjust their offerings accordingly. All in all, this offers new opportunities for expansion while challenging some of the aspects of the traditional advice model.

DIGITAL WEALTH MANAGERS

VS. TRADITIONAL WEALTH MANAGEMENT FIRMS

Fully automated Advisor-assisted

Business model

Software-based delivery of customised and automated investment advice

Phone-based financial advisor (FA) accessible through digital channels to offer personal advice

Face-to-face advice mainly through branch networks offering comprehensive wealth management

Typical investor

Millennial, tech-savvy, price-sensitive; wants to match market returns and pay low fees

Mass market and mass affluent* clients who value human guidance and technology

Affluent, high net worth*** and ultra-high net worth**** clients who value guidance from a trusted FA

Value proposition

Convenient and easy-to-use, low-cost online platform offered directly to consumers

Digital platform combined with advisor relationship; affordable pricing for fully diversified portfolio

Dedicated FA with full range of investment choices and comprehensive wealth planning

Fee structure A 0.25-0.50% fee on assets managed; minimums may apply

A 0.30-0.90% fee on assets managed; monthly fees per planning programme; minimums may apply

A 0.75-1.5%+ fee on assets managed; minimums may apply, varies by investment type

Investment process overview

Risk profile, target asset allocation, managed investment account, automated rebalancing, easy access

Virtual FA meeting, financial planning, risk profile, target asset allocation, managed investment account, automated rebalancing, easy access, periodic reviews

In-person meeting with dedicated advisor, financial planning, investment proposal, target asset allocation, brokerage and managed accounts, automated rebalancing, in-person access and reviews

Investment vehicles

Exchange-traded funds (ETFs), direct indexing**

ETFs, stocks

Stocks, bonds, ETFs, mutual funds, options, alternative investments, commodities, structured products

Source: Advice goes virtual report, Ernst & Young

*US households with between USD250,000 and USD1m in financial assets **Wealthfront offers direct indexing to accounts with over USD500,000 in assets through individual stock selection ***US households with between USD1m and USD10m in financial assets ****US households with greater than USD10m in financial assets

keplercheuvreux.com 17

“

“Would you be ready to meet a robot as your doctor if you felt sick? My answer is yes, as it would reduce the human error factor. The same will apply to the private banking activity, at least the pure investment side. It will take ten years to become mainstream but we will get there.”

Philippe Bourquin, Financial Adviser, NBK Banque Privée (Suisse)

“On a risk-adjusted basis, the banking sector’s cost base is still stellar, as the sector has learned nothing from the first wave of the crisis in 2008. A rebase of wages by at least one-third would be necessary. Redundancies would be the easiest way to cope with cost overruns, and fintech enables this to be done in an unprecedented way in terms of speed and efficiency. Only very well capitalised banks will be able to stand the pace, and the gap with static incumbents will widen. We believe that by far the biggest misunderstood variable in the fintech equation is the dramatic social implications, in particular for cities such as London, which is highly dependent on the financial services industry.”

Fabrizio Croce, Senior Equity Analyst Financials, Bank J. Safra Sarasin AG

“Digitalisation is a topic that is very high up on our daily agenda. It obviously relates to all aspects of our work and includes the entire relationship with the client. From a product point of view, we like to keep things very simple. Our focus in this respect is more on different portfolio strategies. As for robo-advisors, we have created a subsidiary that actively experiments with their use in client relationships.”

Klaus Niedermeier, Head of Research, Deutsche Apotheker- und Ärztebank

“Private banking is about listening, trust, and relationships. While technology can help, it cannot fully replace human beings.”

Marie-Jose Billy, Banque Leonardo

“After nearly 15 years of institutional use of ETFs, we are observing constant growth among retail investors. Indeed, ETFs offer a simple and low-cost access to a concept that is gaining in popularity each year: passive management. Moreover, the change in the regulatory framework in Europe (RDR, MiFID II, etc.) is clearly opening up new opportunities for retail platforms and IFAs for ETF providers.”

Olivier Paquier, Head of SPDR ETFs France, Monaco, Spain & Portugal, State Street Global Advisors

”

What they think about robo-advisers…

keplercheuvreux.com 18

Robo-adviser corner “

”

At Yomoni, we believe that investors’ habits evolve with technology, especially where the wealthiest investors are concerned. While the basic assumption is often generational (“only young people are digital natives”), this is not the case. Indeed, online life insurance has been well-received by older people, who are major players on the savings markets. At Yomoni, this behaviour is observed in our clientele. Indeed, we can divide our clientele into two categories: young workers less than 35 years old who have not yet bought property and older, more experienced people who spontaneously subscribe to our online service. Ultimately, all these investors are now looking for easy access and functional application rather than a price engine search tool. Nowadays, banks are having trouble providing valuable services for wealth below 200-300,000 euros. Financial advisers serve more than 500 customers, and it is impossible to stand by all of them. Most of the time, financial advice boils down to mass campaigns of products from an innumerable range of incomprehensible sources. Instead, the automation of customer follow-up at Yomoni provides a simple service adapted to each customer profile. While advisors can follow clients only one day every four years, “robots” can monitor them anytime. However, during the onboarding process, human support is unparalleled. During our underwriting process, we observed that most of our clients interact with our online advisors before investing. Fintechs are facing a problem with recognition that is hampering massive subscription, but time seems to be on our side. Also, some underline that French consumers are not familiar with riskier investments (e.g. stocks), although we doubt it. In our opinion, French outdated tax scheme prevents household to build a truly diversified asset allocation, including stocks and corporate bonds, for instance.. Indeed, France is probably the only industrialised country to provide a tax advantage (or subsidy) to short-term non-risky saving products such as “Livret A”.

Mourtaza Asad-Syed, CEO, Yomoni

"When you only have 30 seconds to convince someone, how do you ensure that your financial products are going to be suitable for distribution, and your storytelling convincing? Advisory is not just a contract - advisory could be discretionary mandates and direct access to trading rooms. Advisory is engaging the client with a meaningful story while respecting appropriateness and suitability. The biggest challenge with MiFID II and PSD2 (Payment Services Directive 2) will be client data ownership, and trust decentralisation. While institutions have a monopoly on trust, new API (Application Programming Interface) challenges might change the deal. How will banks articulate their value added around client servicing? Mass customisation and a collaborative economy are key to our new way of consuming services. Clients are thirsty for empowerment, which might leave banks on the road? or not… this will depend on institutions’ capacity to satisfy clients’ needs.”

Alexandre Gaillard, CEO & Founder, InvestGlass

“As a Fintech involved in the financial products distribution channel (robo-advisor), we believe that technology is changing the interaction between clients and distributors. Retail investors are switching from “clients looking for the best product” behaviour to “users looking for the best service”. Innovation is now client-oriented and aims at simplifying access to sophisticated investment strategies. Collaboration between Fintechs and Financial Institutions will allow best practices from both worlds to be offered: competitive products and individualised service.”

Leonard de Tilly, CEO, Fundshop

keplercheuvreux.com 19

The Deloitte report “Wealth management and private banking: connecting with clients and

reinventing the value proposition” provides interesting insights on how clients use different

interaction channels. For complex transactions, face-to-face meetings are still perceived to be

extremely important.

The overall importance of different interaction channels

Source: “Wealth Management and Private Banking – Connecting with clients and reinventing the value proposition”, Deloitte

Inherited

High Net Worth

Emerging Markets

Entrepreneurial

Mass affluent

Developed markets

1

2

3

Reputation / premium brand

Quality of relationship with banker

Investment performance

1

2

3

Reputation / premium brand

Proximity of relationship office

Quality of relationship with banker

1

2

3

Large array of products & services available

Investment performance

Proximity of relationship office

1

2

3

Quality of relationship with bankers

Large array of products & services available

Ease of dealing with the bank

1

2

3

Compliance with regulatory requirements

Large array of products & services available

Global coverage

1

2

3

Global coverage

Full wealth management and private banking proposition

Compliance with regulatory

keplercheuvreux.com 20

Client segmentation, advisory and service pricing

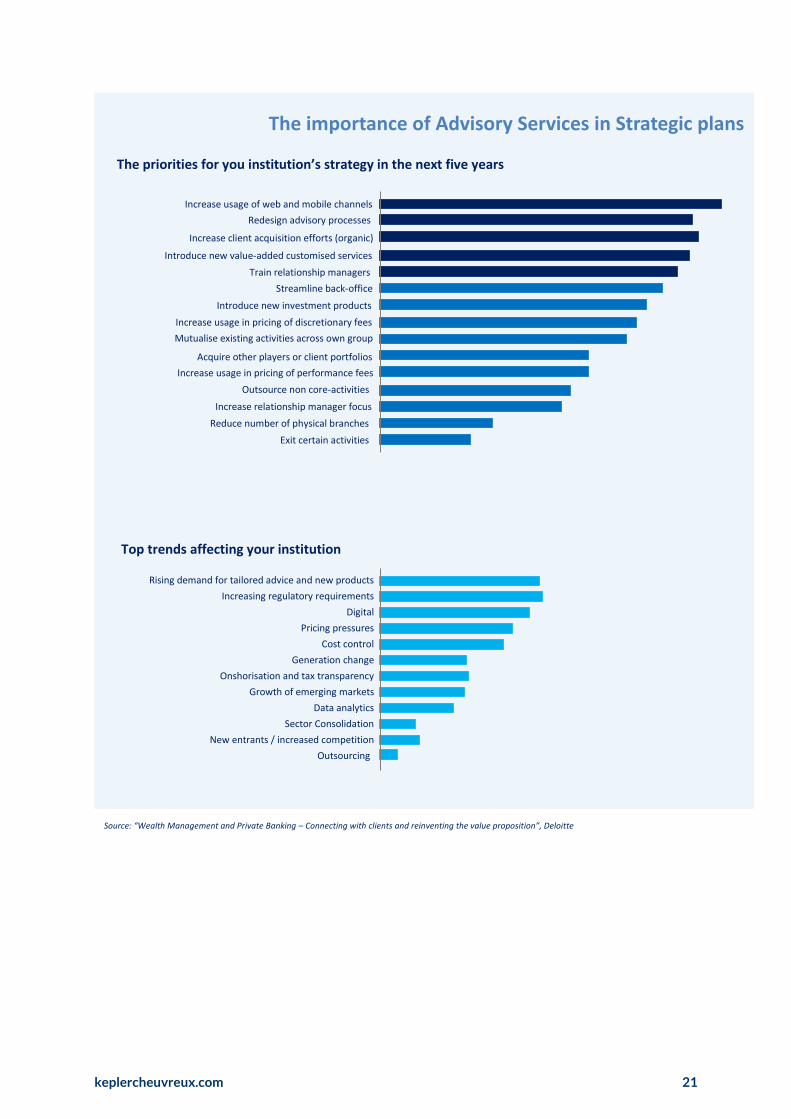

The importance of advisory services in strategic plans

One-third of private banks from the sample consider advisory services to be very important today;

however, roughly two-thirds have integrated these services into their strategic projects for 2016

(58%) and/or the medium term (60%).

Chart 3: Advisory services development horizon

From 1 to 3 (3 being the most)

16,3%

9,3% 14,0%

47%

33%

21%

37%

58% 60%

0% 0% 5%

Today 2016 plan Medium term guidance

1 2 3 I don't know

”

“

"Private banks have four main drivers: low interest rates, increasing regulatory constraints, low margins, market and client volatility. What are the operational consequences for private banks? To reduce their cost base; to reinforce their teams with expert profiles - real estate, advisory desks, financial specialists, private bankers and to adopt technological tools and Fintech practices.”

Michel Dumont, Founder & CEO, Leyders Associates

“Executive search in private banking is strongly correlated with new regulation and transparency rules and impacted by economic uncertainties. Private bankers have to bring more value to clients with higher-quality assets, who are deeply cautious and skilled. Therefore, they need new profiles to reinforce mainly three functions: 1) senior bankers with strong sales skills and networks within UHNWI & HNWI segments; 2) compliance and risks officers; and 3) M&A and tax together with relationship skills through advisory desks or internal advisors (for smaller institutions). We also notice a strong and recent growth of executive search in all these fields in Luxembourg. Additional digital skills are not yet required at this stage, but this could well change in the future.”

Romain Girard, Partner, Progress - IIC Partners

What headhunters think

keplercheuvreux.com 21

The priorities for you institution’s strategy in the next five years

The importance of Advisory Services in Strategic plans

Top trends affecting your institution

Source: “Wealth Management and Private Banking – Connecting with clients and reinventing the value proposition”, Deloitte

Increase usage of web and mobile channels Redesign advisory processes

Increase client acquisition efforts (organic) Introduce new value-added customised services

Train relationship managers Streamline back-office

Introduce new investment products Increase usage in pricing of discretionary fees Mutualise existing activities across own group

Acquire other players or client portfolios Increase usage in pricing of performance fees

Outsource non core-activities Increase relationship manager focus

Reduce number of physical branches Exit certain activities

Rising demand for tailored advice and new products Increasing regulatory requirements

Digital Pricing pressures

Cost control Generation change

Onshorisation and tax transparency Growth of emerging markets

Data analytics Sector Consolidation

New entrants / increased competition Outsourcing

keplercheuvreux.com 22

The importance of Advisory Services in Strategic plans

Expected pricing usage in the next 5 years

↗ Increase

→ Stay the same

↘ Decrease

Advisory fees (e.g., per hour spent, per structure designed)

92% 0% 8%

All in one model (one fee combining all of the above)

82% 0% 18%

Performance fees (e.g., on annual portfolio performance)

75% 17% 8%

Management fees (e.g., on assets under discretionary mandate)

60% 35% 5%

Custody fees (e.g., on assets held in custody)

35% 29% 35%

Transaction fees (e.g., by order executed)

17% 33% 50%

How much do clients invest today?

Source: “Wealth Management and Private Banking – Connecting with clients and reinventing the value proposition”, Deloitte

keplercheuvreux.com 23

The client segmentation story

The minimum portfolio size required by private banks depends on the institution: one-third requires

EUR200k-500k, and one-third asks for EUR500k-1m. We would note that less than 10% of private

banks from our sample give access to their services to clients with portfolios of less than

EUR200,000. In 11% of cases, their policies are discretionary. Nearly one on five (17%) requires a

minimum of EUR2bn to get access to private bank services.

Chart 4: Access to the Private Bank (in EUR ‘000s)

The Ernst & Young “Advice goes virtual” survey provides interesting and complementary insights into

the relative weight of each client category.

Discretionary 11%

<200 8%

200-500 31%

500-1000 33%

>2000 17%

Financial assets per household and market segment

Mass Market

Mass Affluent

High net worth

individuals

Ultra-high net worth individuals

US$3,8t US$7,0t

US$14,4t

US$5,7t

$ $ $

$ $

$ $

Financial Assets per HH

# of HH

< US$250k < US$250k-US$1m < US$1m-US$10m >US$10m

103m HH 14m HH 5.6m HH 0.2m HH

Source: estimates based on the Federal Reserve 2013 Survey of Consumer Finance, “Advice goes virtual”, Ernst & Young

keplercheuvreux.com 24

The minimum portfolio size required by private banks for advisory services is also very

heterogeneous, albeit with two main groups: EUR500,000-1m (35%) and over EUR2m (35%). In only

one-tenth of cases (9%), access to these services is open to clients whose portfolios are less than

EUR200,000; for 6% of banks, the policy is discretionary.

Chart 5: Access to the advisory services (in EUR ‘000s)

Indeed, our survey has highlighted one key market trend: Advisory Desk access policies are loosely

structured: few banks have formalised them precisely, and in a number of cases, it remains at the

discretion of private bankers/CRMs, depending on their relationships with clients.

For instance, two-thirds of the private banks in the sample propose some customised investment

ideas to their mass affluent clients and 43% provide them with access to their advisory desks

(equities/bonds). One in three (37%) also proposes some tailor-made structured products.

Chart 6: Services to mass-affluent clients

Discretionary 6%

<200 9%

200-500 15%

500-1000 35%

>2000 35%

66%

43%

37%

Customised investment ideas Access to your Advisory desk Tailor-made structured products

keplercheuvreux.com 25

All about advisory teams

The size of the advisory teams varies greatly and is very correlated to the size of the Private Banks.

Most frequently, their missions include:

- Selection of investment ideas (notably in case of no brokerage activities or buy-side analyst

teams in the Group).

- Internal support to Private bankers/CRMs for clients bespoke investment requests.

- Production of research materials (sheets, newsletters, etc.).

55% of surveyed advisory teams have regular contacts with clients independently to private

bankers/CRMs.

Chart 7: Advisory teams’ contacts with clients

Regular contact with clients

55%

Client contacts upon CRM's request only

45%

keplercheuvreux.com 26

“The banking industry is undergoing a massive transformation. Lower margins, stricter regulatory requirements and higher client expectations are shaping a new world private banks have to face. Digitalisation and new advisory models are among the responses to this changing world. The introduction of a “pay-for-advisory” model was a big challenge for us, but turned out to be a big success. There is demand for high-quality, customised, comprehensive and proactive financial advice, and clients are ready to pay for it.”

Roberto Cerratti, Vice President, Head of Investment Consulting, Private Banking & Wealth Management

Switzerland, Credit Suisse

Advisory desk corner

“CA Indosuez Wealth Management Advisory team fosters a dedicated approach to serve UHNWIs. It is made up of 50 multicultural and polyglot professionals with expert knowledge of different asset classes and their derivative instruments on the world’s main markets. The Advisory team also publishes regular market comments and investment recommendations. In addition, CA Indosuez Wealth Management is developing various digital means for our clients to have direct access to our research and is currently working on an innovative, highly personalised, asset allocation tool.”

Julien Collin, Head of Markets & Investment Solutions, CA Indosuez Wealth Management

“Improving the client experience is the key challenge for Private Banks. The value proposition will have to combine high-quality Advisory services worth paying for and a variety of distribution channels adapted to clients' needs. In that respect, recent regulations which increase the knowledge of clients' needs and reinforce the monitoring of risks create opportunities to engage with clients, should increase the proximity between clients and their banks, and finally improve performance.”

Martial Godet, Head of Advisory & Execution Services, BNP Paribas Wealth Management

“The commoditisation of financial market access makes customer loyalty management more difficult. Banks have to improve their skills, enhance services and create a new business model (advisory) to offer a tailor-made service that can add value in regard to digital and mass finance, and introduce clients to a more sophisticated financial environment.”

Senior Portfolio Advisor, Swiss Private Bank (anonymous) ”

“

keplercheuvreux.com 27

“

”

Advisory desk corner

“In an increasingly digitalised world, it is ever more important to become a client’s trusted advisor. Finance has always been based on trust and we are committed to building on personalised relationships. We believe in giving clients direct access to experienced people who are able to provide customised solutions and respect clients’ lifestyles rather than compete with machines. We aim to partner up with clients and steer them towards predefined objectives.”

Catherine Reichlin, Head of Research, Mirabaud

“The way we have set up our advisory desk is similar to the tailor-made partnership we have with our clients. Depending on needs, we may support clients directly or through RM, providing them with solutions to specific requests or helping them build their portfolio with a broader view.”

Antoine Denis, CAIA, Head of Advisory, Bordier & Cie

“Aligning the value proposition with the revenue drivers is becoming key for banks. Advisory is always described as a key topic, but surprisingly many players are now in a position where "advisory clients" are not charged for advice but through transaction fees. One of our challenges will be to shift from a commoditisation of financial services to a model where financial advice is fairly assessed and paid by clients throughout the value chain.”

Head of Advisory, Swiss Private Bank (anonymous)

“We are here to fully understand our clients’ needs and adapt our product whether it should help advisory desks when they talk directly to customers or as a support to private bankers. Our offer is large enough, as it includes equities but also bonds and structured products. Our advisory desk should be extremely reactive and the unique entry point for any requests our clients may have.”

François Mallet, Senior Managing Director, Global Head of Strategic Cooperation Kepler Cheuvreux

“The increasing volatility of financial markets due to rising uncertainties, the lack of trading bond liquidity due to regulators’ constraints on banks’ market-making demand to lengthen the investment horizon (Buy & Hold approach) of the Strategic Asset Allocation while idiosyncratic opportunities may be picked up through Tactical AA for more risk-oriented clients. We are devoting great efforts to making our clients more aware of the new “higher risk, less return” investment environment.”

Manuela d’Onofrio, Head of Global investments, Global marketing, Unicredit SpA

keplercheuvreux.com 28

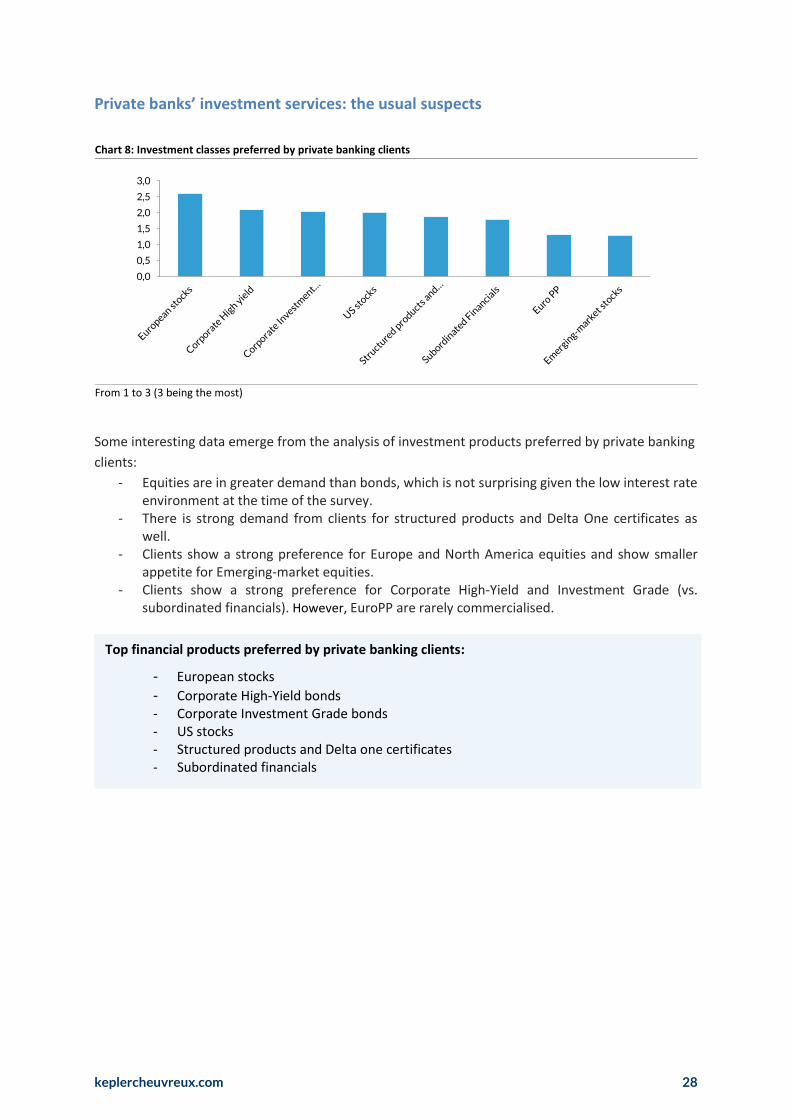

Private banks’ investment services: the usual suspects

Chart 8: Investment classes preferred by private banking clients

From 1 to 3 (3 being the most)

Some interesting data emerge from the analysis of investment products preferred by private banking

clients:

- Equities are in greater demand than bonds, which is not surprising given the low interest rate environment at the time of the survey.

- There is strong demand from clients for structured products and Delta One certificates as well.

- Clients show a strong preference for Europe and North America equities and show smaller appetite for Emerging-market equities.

- Clients show a strong preference for Corporate High-Yield and Investment Grade (vs. subordinated financials). However, EuroPP are rarely commercialised.

0,0

0,5

1,0

1,5

2,0

2,5

3,0

Top financial products preferred by private banking clients:

- European stocks

- Corporate High-Yield bonds - Corporate Investment Grade bonds - US stocks - Structured products and Delta one certificates - Subordinated financials

keplercheuvreux.com 29

Equity stock-picking: relative outperformance

1st

European equity broker

1 billion euros of equities traded

daily

1st

equity research coverage in

Europe

“With a team of 100 analysts, Kepler Cheuvreux Research is independent, fundamental and innovative. Our multi-local set-up offers a unique and compelling advisory proposition. Based on a strict methodology, recognised expertise and very wide coverage of Continental European indexes, the research is mainly known for the quality of its in-depth reports, the originality of its products and the relevance of its recommendations, as the very good ranking published every year by Extel shows, where Kepler Cheuvreux appears to be in a leading position at the European level.”

Matthieu Labille, Deputy Global Head Research, Kepler Cheuvreux

8 Country Top Picks selected List

2

European selected lists of 10

stocks (Large and SMID Cap)

Our best convictions available for

nearly 25 sectors

KEY FIGURES :

“The investment year 2015 in Europe’s equity space illustrates very well the difference between the vision of an equity market as an index or as a collection of individual stocks. In 2015 over 50% of European stocks rose by 10% or more. The leading pan-European equity indices advanced by only 5-7% because the region’s largest most global companies have experienced the greatest stress. Accordingly, most stock-pickers out-performed the index buyers, as demonstrated by the outstanding record of Kepler Cheuvreux’s own recommended list.”

Christopher Potts, Head of Economics & Strategy, Kepler Cheuvreux

95

105

115

125

135

145

155

12/13 04/14 08/14 12/14 04/15 08/15 12/15

Kepler Cheuvreux Large Caps Selected List

Stoxx 200 Large

90

110

130

150

170

190

12/13 04/14 08/14 12/14 04/15 08/15 12/15

Kepler Cheuvreux SMID Caps Delected List

Stoxx Smid 200

Around 100 analysts

Nearly 700 stocks followed by

Equity Research department

Relative outperformance of 29.7% since December 2013 Relative outperformance of 35.8% since December 2013

keplercheuvreux.com 30

Kepler Cheuvreux Credit Research at a glance

“Kepler Cheuvreux offers extensive expertise in Credit Research advisory with dedicated research products for private banks (Selected Lists, portfolio construction, research sheets, etc.) based on a wide coverage of over 150 issuers (investment and speculative grade) and 12 sectors (corporate and financial).

“The zero yield environment has created the need for private bankers to find some more complex Fixed Income solutions to address their clients who wish to get steady returns on their portfolios. The bond market is much more diversified than the equity world: plenty of issuers, different seniorities, different ratings. This complexity can only be addressed by specialists. Kepler Cheuvreux offers private bankers the comfort of bespoke fixed income advisory for the bond portfolio construction and the follow up. “

Patrick Raffard, Head of Credit Innovation & Development, Kepler Cheuvreux

Kepler Cheuvreux credit research, supported by nearly a hundred equity analysts, makes its own assessment of the issuer’s credit quality based on our credit adjustments (in line with rating agencies’ methodologies). After reviewing the prospectus of each bond, Kepler Cheuvreux credit research comes up with a relative valuation and a recommendation based on fundamental and relative values. We have also developed expertise in niche areas such as non-rated issuers, hybrid corporate bonds, and financial subordinated bonds.”

Sébastien Barthelemi, Head of Credit Research, Kepler Cheuvreux

”

Today, it is more and more difficult to find liquidity on credit market. Our Debt & Derivative team allow investors to benefit from all the expertise and experience based on an independent research. In addition to our traditional services, we had developed an electronic platform Electryon. This platform allows investors to access to a wide range of bonds for less. Electryon is offering innovative solutions that meet liquidity constraints of private banks.

Stéphane Rio, Global Head of Debt & Derivatives, Kepler Cheuvreux

“

keplercheuvreux.com 31

According to the private banks in our sample, when seeking investment solutions their clients tend to

focus on Capital-protected products. They are still relatively unfamiliar with proprietary

indices/SmartBeta products and these offers are often less commercialised.

Chart 9: Structured products preferred by private banking clients

From 1 to 3 (3 being the most)

42%

18%

33%

40%

36% 33%

38%

27%

13%

38%

22%

11% 11% 11% 11%

24%

Delta one certificates Capital protected products Non capital Guaranteedproducts

Proprietary indexes (smartbeta and other systematic

stretagies)

1 2 3 I don't know

Ranking of structured products preferred by private banking clients

- Capital-protected products

- Non-capital guaranteed products

- Delta one certificates

- Proprietary indexes (Smart Beta and other systematic strategies)

"In this highly challenging environment, private banks and retail networks are looking to partner with Asset Managers committed to offering comprehensive solutions and services beyond selling products. Amundi, with its longstanding experience in serving such players worldwide, is well positioned and fully equipped to offer advisory, meaningful servicing and tailor-made tools to its clients and partners , with a permanent focus on innovation and cost efficiency. ETFs, index-based structured products and allocation models are one of the main trends we are currently noticing and implementing for our clients and partners.”

Valérie Baudson, CEO Amundi ETF, Indexing & Smart Beta

keplercheuvreux.com 32

Investment Solutions Corner

“Kepler Cheuvreux has developed a unique model focused on four areas of expertise: independent research, tailor-made engineering, open architecture and customised execution and follow-up. Our recent rankings and product development illustrate our commitment to providing our clients with the best service.“

Romain Chassard, Managing partner, Investment Solutions, Kepler Cheuvreux

“

”

Third best providers of structured product in France

“The results of our “Private Banks: the advisory awakens” survey confirm the appetite for structured products but also the need to educate stakeholders both internally (CRMs) and externally (clients). We address this issue by providing concise overviews and training documents, client-oriented or internal communications, and by holding events (with our specialists both internally and for our clients).”

Romain Turquem, Head of marketing, Investment Solutions, Kepler Cheuvreux

Third Best Provider of Structured Products!

• Quantitative criteria, with the most frequently mentioned providers, and,

• Qualitative criteria, the professionals judges the relevance of the product, the commercial availability and the aftersales quality.

From left to right: Nicolas Miara-Godet, Paul Baignières, Jeremy Sayada and Romain Turquem. | 1 Derivatives Capital is a brand of Kepler Cheuvreux used for distribution of Investment Solutions in France.

The French magazine, “Gestion de Fortune”, has rewarded “Derivatives Capital Kepler Cheuvreux”1 as the third

best provider of structured products (after Société Générale and BNP Paribas). This ranking combines:

“ The Private Banking segment is a major focus in the development of the business line Investment Solutions. Today, more and more Private Banks trust us to design their structured product offers. They especially appreciate our independence, our tailor-made approach and our differentiating products. Two of our latest product launches illustrate this well. One uses the recommendations of Kepler Cheuvreux Research equity through a targeted investment theme: "low cost" in Europe. The other is based on a Eurozone equity index, launched in partnership with MSCI, improving performance and/or protection of the offered product.”

Nicolas Miara-Godet, Head of Investment Solutions, Kepler Cheuvreux

keplercheuvreux.com 33

In the mood for Advisory & Research

Everything you always wanted to know about research organisation and

distribution* but were afraid to ask

The internal organisation of research sheets is quite varied across private banks: more than 40% are

produced by internal asset management teams, and one-third are compiled by advisory teams.

Access to external providers differs by asset class: between 17%-18% for funds and bonds, and 24%

for equities. Very rarely (2-5% of cases) do private bankers or CRM teams produce sheets.

Chart 10: Research sheet production

31%

37% 36% 40%

43% 44%

24%

17% 18%

4% 3% 3%

Equities Bonds Funds

Advisory desk Asset management team External provider CRMs

- 2-3 pages document summarizing the key points on a stock or bond issuer

- Content based on our research universe and database (investment case, financial data…)

- Customizable format and branding - Simplified/adapted wording to private

bankers/CRMs and clients

Kepler Cheuvreux’s research sheets

“Our research department, supported by a team of 100 analysts, covers nearly 700 stocks making Kepler Cheuvreux one of the largest research brokerage houses in Europe. Our research sheets are based on Kepler Cheuvreux’s high quality research, and give private bankers access to all of our expertise in terms of analysis and valuation tools.”

Pierre Boucheny, Head of French Equity Research, Kepler Cheuvreux “As private bankers, qualitative and large universe research is crucial. We were looking to expand our research universe for mid and large French capitalisation (such as SBF120), and Kepler Cheuvreux developed a pertinent and flexible solution that was compatible with our IT systems and our processes.”

Head of Investment Advisory, France (anonymous)

keplercheuvreux.com 34

Anatomy of research documentation

Of the respondents who produce internal research reports, only 23% claim to be satisfied with the

quality of the research.

Chart 11: Satisfaction with research

From 1 to 3 (3 being the most)

Two-thirds of private banks (62%) in our sample intend to reinforce their client research

documentation in terms of investment ideas, mainly due to new regulatory constraints (44%) as well

as to meet clients’ requests (18%).

Chart 12: Research documentation

20%

46%

23%

11%

1 2 3 I don't know

Yes, because of regulatory constraints

44%

Yes, because of clients requests

18%

No 38%

keplercheuvreux.com 35

Practices regarding the documentation of internal/client investment ideas are also fairly

homogeneous across asset classes (equities, bonds, funds); however, their use continues to differ:

- 40%-45% of private banks produce these sheets only for internal use (45% for Equities and Bonds, 40% for Funds).

- 55%-60% also distribute them to their clients (55% for Equities and Bonds, 40% for Funds).

Chart 13: Investment research distribution per asset class

Unsurprisingly, the sample considers investment case, financial data, company profile and

recommendation to be the most important information in research sheets.

45% 45%

39%

55% 55%

61%

Equities Bonds Funds

Internal use only Client distribution

Key information in research documents:

- Investment case - Financial data - Company profile - Recommendation - SWOT analysis - Target price - Bond analysis - Stock graph

keplercheuvreux.com 36

Digitalisation: modern times

Once upon a time in private banks

For private banks, the most common digital set-up is a website that gives clients access to their portfolio. Only 15% propose also some online transactions (portfolio changes, electronic order routing trading). It is very rare for smart information flow based on the client profile/portfolio or chat and video conference systems between clients and advisors to be incorporated into the private banks’ digital set-up. It is worth noting that over 25% of the private banks in our survey had not developed any digital set-up.

Chart 14: Digital services provided by the private banks

29% 27%

15%

5%

1%

Access to portfolio No digital set-up Online transactions(portfolio changes,

electronic ordertrading)

Chat, video conference(client/advisor)

Smart information flowbased on client

profile/portfolio

keplercheuvreux.com 37

“ “The challenge for private banks is to strike the right balance between digitalisation and the personal touch. The client experience will on the one hand be based on personal care, knowing your client and his/her needs, and on the other hand making sure he/she can reach his/her information in the easiest way possible. So service and communication that are custom-made to meet the individual needs of each client is the way to go.”

Head of Investment Research & Communication, Dutch Private bank (anonymous)

“Probably the banking sector as a whole is facing a phase of discontinuity due to unprecedented technological innovation, the prospect of a profound change in the way of using banking services and pressure on revenue margins. Even Private Banking must face this challenging environment and the priority seems to be the smart utilisation of technology to increase efficiency in service delivery, and to increase the added value for clients. However, these two aims must be reconciled with a "warm" and tailored relationship between banker and customer.”