eu constraints on recent and expected changes … · eu constraints on recent and expected changes...

TRANSCRIPT

EU CONSTRAINTS ON RECENT

AND EXPECTED CHANGES IN

SPAIN

María Teresa Soler Roch

Preliminary remarks

(Report on Tax Reform)• EU constraints. Key principles:

– Fiscal consolidation (sound public finance)

– Main role of income taxation (corporate

and individual)

– Reduction of selective tax incentives

AGRESSIVE TAX PLANNING

AND CORPORATE TAX

Anti-avoidance(subject -to-tax,

GAAR, Parent/Subsidiary

Directive). Tax incentives

Recommendation (2012/772/UE)

Subject to tax clause:

“Where this Convention provides that

an item of income shall be taxable only

in one of the contracting States, the

other contracting State shall be

precluded from taxing such item only if

this item is subject to tax in the first

contracting State”

DTCs and Spanish provisions

• Spanish DTCs:

– No rule of that kind

– Tax sparing clauses in some DTCs

• Domestic provisions

– Exemption/Foreign tax credit

– General rule: effective payment of the

foreign tax (ECJ decision 8 December

2011, C-157/10 BBVA )

Recommendation 2012/772/UE:

proposal of GAAR• “An artificial arrangement or an artificial

series of arrangements which has been

put in place for the essential purpose of

avoiding taxation and leads to a tax

benefit shall be ignored. National

authorities shall treat these

arrangements for tax purposes by

reference to their economic substance”

GAARS in Spanish GTA (Ley

General Tributaria)• Substance over form (article 13)

• Anti-avoidance (article 15): artificial

transactions, tax benefit as main

purpose

• Sham transactions (article 16)

• Procedural aspects

• EU GAAR, a better option?

Parent/subsidiary proposal 2013

• COM (2013) 814 final, amending

2011/96/EU

– Article 4.1.a): “refrain from taxing such

profits to the extent that such profits are

not deductible by the subsidiary of the

parent company”

Spanish provisions

• Participation exemption (article 22 CTA)

– 5% threshold - Business activity

– Taxation at source - No tax haven

• Tax Reform Report. Proposal 43:

– 10% tax at source – B.activity not required

• Future scenario?

– BEPS Action 2 (hybrids)

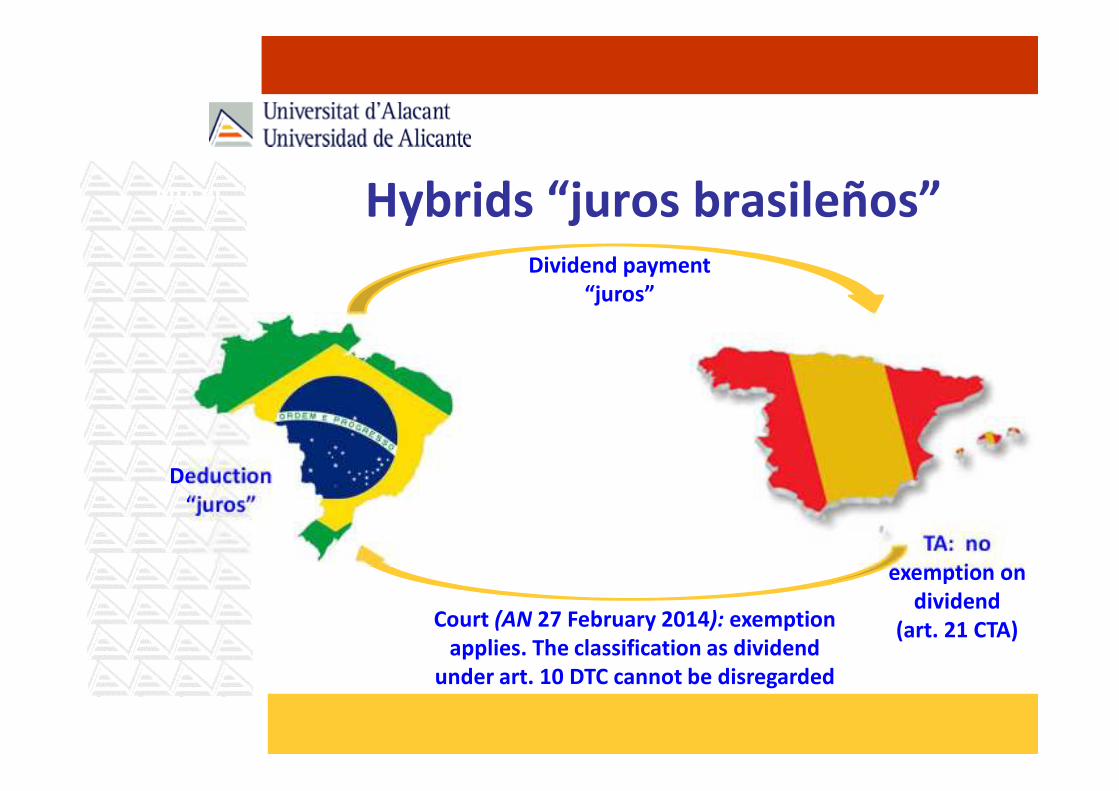

Hybrids “juros brasileños”Dividend payment

“juros”

Court (AN 27 February 2014): exemption

applies. The classification as dividend

under art. 10 DTC cannot be disregarded

TA: no

exemption on

dividend

(art. 21 CTA)

Deduction

“juros”

BRAZIL

SPAIN

Parent/Subsidiary proposal 2013

• Commission (2013) 814 final

– Article 1.2 “This Directive shall not preclude

the application of domestic or agreement-

based provisions required for the

prevention of tax evasion”

– New article 1 a “Member States shall

withdraw the benefit of this directive in the

case of an artificial arrangement…..” (GAAR

Recommendation 2012)

Parent/Subsidiary

Spanish provisions• Specific provision (article 14.1.h) NRTA)

– Look-through approach (no exemption at

source if more than 50% non EU residents)

• Court decision: Audiencia Nacional 25

November 2010

– Exception: valid economic purpose,

effective business activity

– Compatible with PSD GAAR proposal?

Tax incentives

• Legitimate tax policy option vs. Potential

risks of unlawful State Aids and harmful

tax competition

• Tax Reform Report. Proposal 45:

– No tax incentives (tax credit such as: R&D&I

or environment investments, new jobs or

reinvestment of extraordinary profits)

– What about the patent box regime?

Profit shifting

P. B. regimeInput incentive

STATE A

Company X STATE B

Company X/Y

R&D activity R&D result

INDIVIDUAL TAXATION

Inheritance Tax

(non residents) and Pensions

(temporary residents)

Inheritance tax on non residents:

EU constraints• Commission proposals (tackling tax

obstacles, relief of double taxation)

• ECJ doctrine (cases Barbier, Geurts-

Votgen, Jäger, Eckelkamp, Arens-Sikken,

Block, Mattner, Halley, Ivon Welte)

– Discrimination in comparable situations

– Restriction on free movement of capital

EXAMPLE

• Deceased resident in the region of

Valencia (Spain) all assets in Spain

• Heirs (on equal footing) residents in

Valencia, Madrid and Brussels.

– Tax allowance (tax base):100.00 (R in

Valencia and Madrid), 15.956’87 (R in

Brussels)

– 75% tax debt reduction: only R in Valencia

Inheritance tax and non

residents: Spanish provisions• Problem raised by regional legislation

• ECJ pending decision : Commision vs.

Spain (C-127/2012)

• High Supreme Court (4209/2011 Const.

Court on IHT provisions Valencia)

• Report on the Tax Reform. Proposal 57:

same exemption in all Spanish territory

Pensions (temporary residents)

• The exclusive rule in article 18 OECD MC

– Alternative proposals in the Commentary

– Recent exceptions (DTC Germany-Spain)

• Tax Reform Report. Proposal 32:

– Foreign retired residents: pensions taxed at

the lowest Income Tax rate

– Tax competition and profit shifting?

STATE AIDS

Pending issues (Implementation

of recovery procedure)

Recovery of unlawful aids:

EU provisions• Procedural regulation (659/1999,

794/2004). Article 14.3:

– “Recovery shall be effected without delay

and in accordance with the procedures

under the national law of the member State

concerned, provided that they allow the

inmediate and effective execution of the

Commission’s decision”

ECJ decision 13 May 2014

(C-184/11 Commission vs. Spain)• (Grand Chamber): Spain has failed to

fulfil its obligations under art.206.1 TFUE

– Spain has been the subject of a number of

judgements of the kind (failure in inmediate

an effective recovery)

– Delay for recovery (more than 5 years)

– Penalty: lump sum (not reduced because of

regional infringement)

Recovery of unlawful aids

Spanish provisions• Main issues

– Legal certainty and legitimate expectations

(risk of retrospectivity)

– Statute of limitation (possible solutions)

• Procedure (Member States autonomy)

– In the case of tax benefits: lack of ad hoc

provisions

– Next modification of the GTA?