ethics in professional fields of practice the … · ethics in professional fields of practice the...

TRANSCRIPT

ETHICS IN PROFESSIONAL FIELDS OF PRACTICE

THE TAX PRACTITIONERWEBINAR 2. 25 August 2017

Presented by Adv Werner Bouwer

AGENDA

AGENDA

PRESENTATION 1 - THE THINKING…

WELCOME & INTRODUCTION

PREVIOUS SESSION RECAP

INFLUENCE OF CULTURE ON ETHICAL DECISION MAKING PROCESS

COMPLIANCE & THE LAW

RATIONALISATION

WHAT TO DO WHEN CONFRONTED WITH TAX EVASION … THE LAW

INFLUENCE OF CULTURE ON ETHICAL DECISION MAKING

‘… compliance is there to reinforce

culture and it also demonstrates why

those who advocate a paper

compliance program are wrong. It is

the doing compliance, not simply

having it on paper, that makes it all

work.’ Tom Fox – 10 Feb ‘17

DEFINITION OF CULTURE:It is the “pattern of responses discovered,

developed or invented during the group’s history of

handling problems …

These responses are considered the correct way to

perceive, feel, think and act … Culture determines

what is acceptable or unacceptable, … right or

wrong, …’

Thank You for Being Late, Thomas Friedman

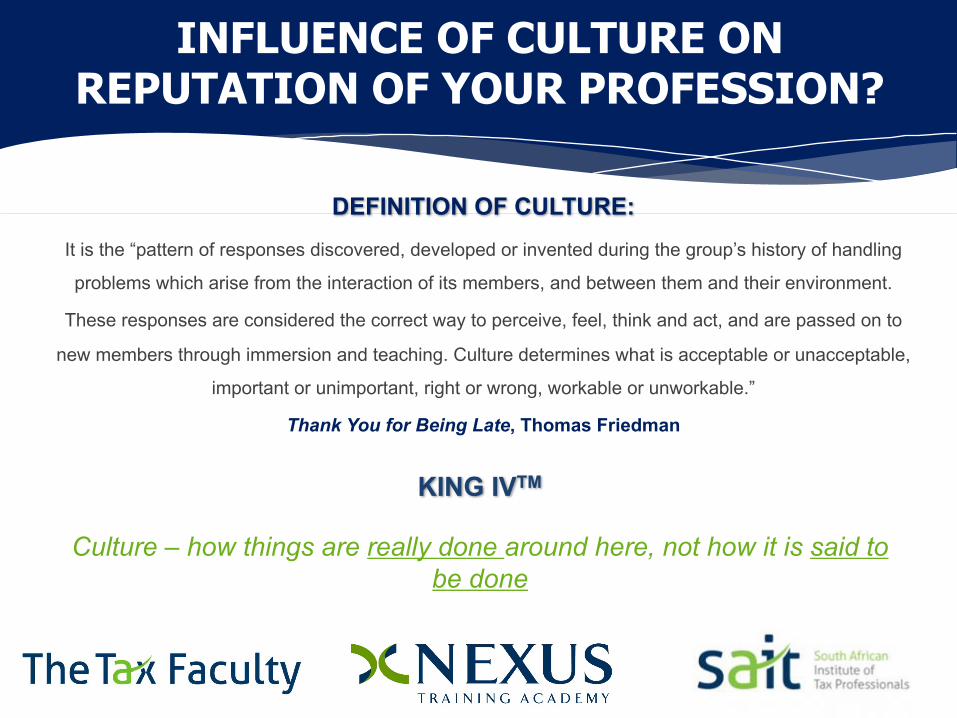

INFLUENCE OF CULTURE ON REPUTATION OF YOUR PROFESSION?

DEFINITION OF CULTURE:It is the “pattern of responses discovered, developed or invented during the group’s history of handling

problems which arise from the interaction of its members, and between them and their environment.

These responses are considered the correct way to perceive, feel, think and act, and are passed on to

new members through immersion and teaching. Culture determines what is acceptable or unacceptable,

important or unimportant, right or wrong, workable or unworkable.”

Thank You for Being Late, Thomas Friedman

KING IVTM

Culture – how things are really done around here, not how it is said to be done

RELATIONSHIP BETWEEN LAW & CULTURE

‘… compliance is there to reinforce culture and it also demonstrates why those who advocate a paper

compliance program are wrong. It is the doing compliance, not simply having it on paper, that makes it all

work.’ Tom Fox – 10 Feb ‘17

MFMA has the strongest criminal measures against malfeasance. Yet, municipalities have the most qualified

audit reports. Very little prosecutions ito MFMA, after 14 years.

PFMA: Took the NPA approximately 15 years of endless reports on billions of irregular expenditure year on

year; to muster the courage for the 1st prosecution.

PRECCA is one of the strongest pieces of anti-corruption legislation in the world. Yet, after 13 years, there

are not one name reflected on the Register of Tender Defaulters …

With the World Bank audits, we get full marks for having the rules on AML. Yet, we flunk the walk the talk

test.

RELATIONSHIP BETWEEN LAW & CULTURE

The ‘Rule of Law’ concept does not refer

to whether the law itself exists. Its

existence is merely the 1st step.

Rule of Law means how that what there

is, is applied.

The fearless but fair application of the law -

Is the ‘doing’ part setting the example

Is the ‘pattern of responses discovered,

developed or invented’

Determines what the public perceives

are right or wrong.

That is why ethical pioneers are all ad idem -The law’s existence does not help – if no-one does nothing, there ‘is nothing’ (SCOPA Chair)

Biggest barrier to root out corruption is the sense of impunity of some (Madonsela)

RATIONALISATION IS A SLIPPERY SLIDE

Easy to think – but everybody is doing it.

Easy to point and blame ….Some questions …

1.3 The member also has duties to the country and the

fiscus, notably of compliance with the law and the honest presentation of taxpayer client’s

affairs.

WHAT TO DO WHEN CONFRONTED WITH TAX EVASION? REPORTING DUTY?

1.7 Members must comply with statutory duties of legal disclosure where they have proof or

suspicions of criminal activity.

4.17 Members must maintain the confidentiality of their employer and clients and should not

disclose information to a third party without an employer or client’s permission, unless there is

a legal obligation to do so.

235. Criminal offences relating to evasion of tax.(1) A person who with intent to evade or to assist another person to evade tax or to obtain an undue refund

under a tax Act—

a) makes or causes or allows to be made any false statement or entry in a return or other document, or signs

a statement, return or other document so submitted without reasonable grounds for believing the same to

be true;

b) gives a false answer, whether orally or in writing, to a request for information made under this Act

c) prepares, maintains or authorises the preparation or maintenance of false books of account or other

records or falsifies or authorises the falsification of books of account or other records;

d) makes use of, or authorises the use of, fraud or contrivance; or

e) makes any false statement for the purposes of obtaining any refund of or exemption from tax,

is guilty of an offence and, upon conviction, is subject to a fine or to imprisonment for a period not exceeding

five years.

THE TAA – S 235 (1)

THE TAA – S 235 (3)

(3) A senior SARS official may lay a complaint with the South

African Police Service or the National Prosecuting Authority

regarding an offence contemplated in subsection (1).

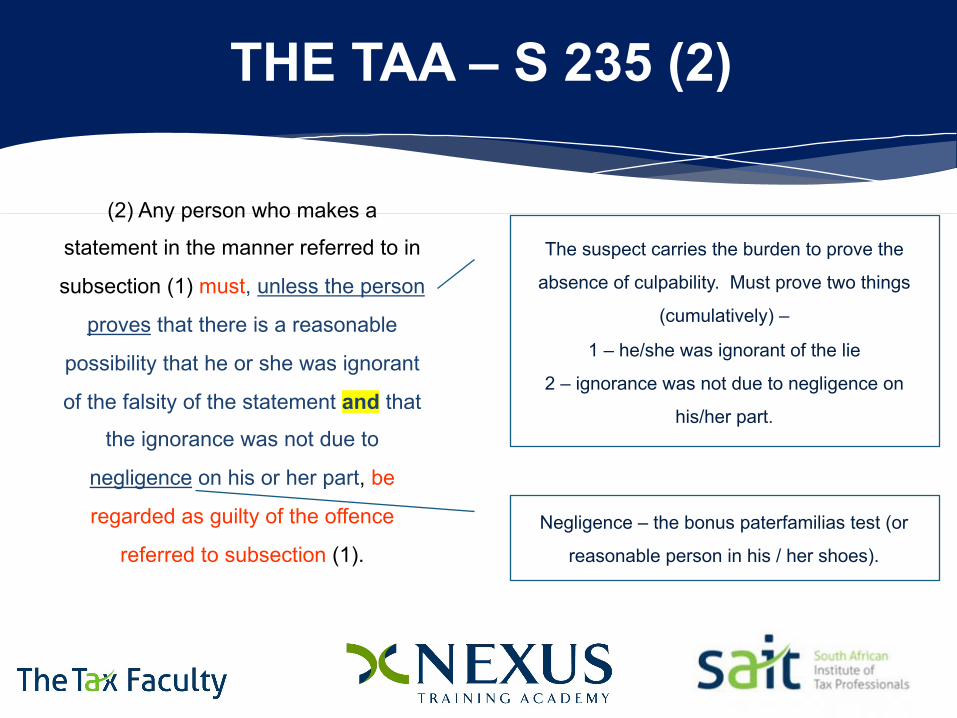

(2) Any person who makes a

statement in the manner referred to in

subsection (1) must, unless the person

proves that there is a reasonable

possibility that he or she was ignorant

of the falsity of the statement and that

the ignorance was not due to

negligence on his or her part, be

regarded as guilty of the offence

referred to subsection (1).

THE TAA – S 235 (2)

The suspect carries the burden to prove the

absence of culpability. Must prove two things

(cumulatively) –

1 – he/she was ignorant of the lie

2 – ignorance was not due to negligence on

his/her part.

Negligence – the bonus paterfamilias test (or

reasonable person in his / her shoes).

4.5 Members must not knowingly be associated with reports,

returns, communications or other information where he/she

believes that the information:

4.5.1 contains a materially false or misleading statement;

4.5.2 contains statements or information furnished

recklessly;

4.5.3 omits or obscures information required to be included

where such omission or obscurity would be misleading.

When a tax ‘registered practitioner’ becomes aware that the

above has occurred he must cease to represent the taxpayer

concerned if the taxpayer does not remedy the situation.

WHAT TO DO WHEN CONFRONTED WITH TAX EVASION? OTHER?

4.12 This Code explain the position of

members if a client refuses to act in

accordance with the member’s advice,

for example where the client has

unreasonably delayed either the

production of information needed for the

preparation of returns or accounts or full

disclosure of irregularities. The member

should consider whether to continue to

act for the client but should note the

recommendations contained in the

Code regarding termination of

relationships with the client.

4.11 A member should deal

with taxation work only on

the basis that the client is

prepared to make full

disclosure to him. Such

disclosures are governed by

confidentiality as an implied

contractual term.

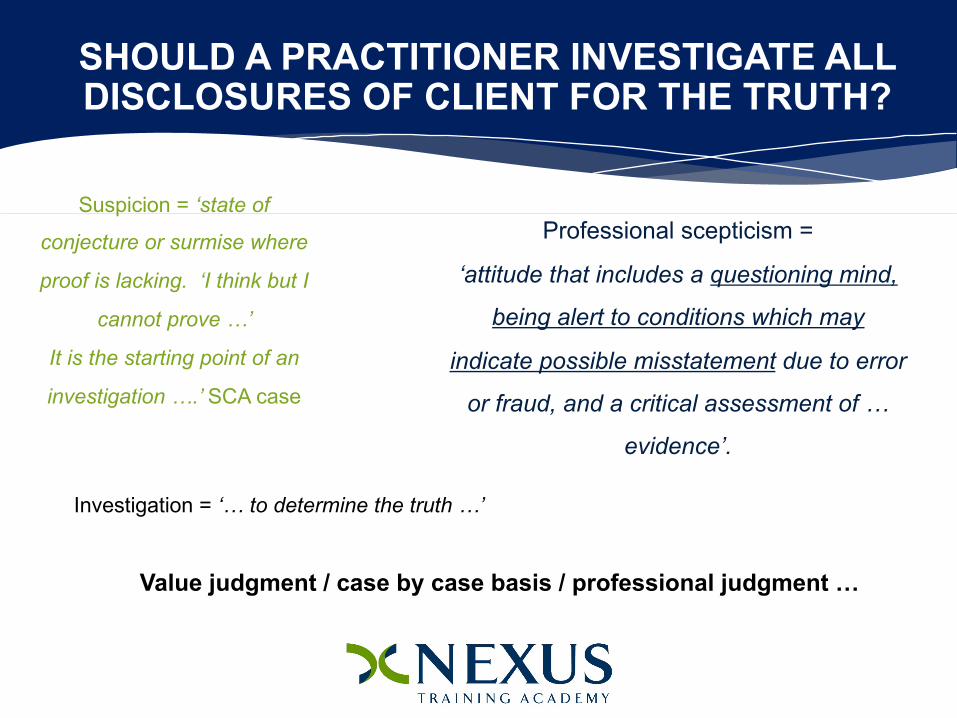

SHOULD A PRACTITIONER INVESTIGATE ALL DISCLOSURES OF CLIENT FOR THE TRUTH?

4.26 Members must keep proper working papers and

files of professional work done to support, for

example, the tax return, opinion and other advice

given. Members must comply with the SA Tax

Standards. It is also compulsory to perform a critical

evaluation and apply professional scepticism to the

information submitted to the member. For example, a

member should scrutinise the bank statements of

client taxpayers’ for completeness of income declared.

SHOULD A PRACTITIONER INVESTIGATE ALL DISCLOSURES OF CLIENT FOR THE TRUTH?

Suspicion = ‘state of

conjecture or surmise where

proof is lacking. ‘I think but I

cannot prove …’

It is the starting point of an

investigation ….’ SCA case

Professional scepticism =

‘attitude that includes a questioning mind,

being alert to conditions which may

indicate possible misstatement due to error

or fraud, and a critical assessment of …

evidence’.

Value judgment / case by case basis / professional judgment …

Investigation = ‘… to determine the truth …’

4.36 Members must consider the money

laundering statutory reporting

requirements. Where members become

aware of tax irregularities, they must

consider that under the money

laundering legislation, fiscal offences can

amount to money laundering and act

appropriately.

4.38 A member who has knowledge of

or reasonable grounds for suspecting

money laundering must consider

whether he has an obligation to make

a report to the appropriate authorities.

THE PRACTITIONER & ML

SUSPICIOUS AND UNUSUAL TRANSACTIONS (SECTION 29)

S 29 – Suspicious and Unusual (STR) Any person who carries on, is in charge, manages or is employed

at a business What they suspect, or ought reasonably to have suspected

Inter alia transaction that

> has no apparent business or lawful purpose

> will facilitate the transfer of unlawful proceeds

> is conducted to avoid a reporting duty

> is relevant in respect of investigation of offence ito TAA.

S 28 – Cash - CTRWho? Accountable

& Reporting Institutions

Any CTR above R25 000

Any series of CTRs individually below

R25 000, but forms the same

series, and collectively

exceeds R25k

Werner BouwerDirector: Nexus Forensics & Nexus Training Academy

SASSETA accredited Facilitator & ModeratorMobile: 082 419 1262Tel: +27 12 664 5568Fax: +27 12 664 0307

e-mail: [email protected]

www.nexusforensics.co.za