estimation of the conditional tail index in presence of...

TRANSCRIPT

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Estimation of the conditional tail index in presenceof random covariates

Laurent Gardes (Universite de Strasbourg)Joint work with Gilles STUPFLER (Universite d’Aix-Marseille)

7th International Conference of the ERCIM WG on Computational andMethodological Statistics

1/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Outline

1. The problem

2. The estimator

3. Asymptotic properties

4. A simulation study

5. Conclusion and forthcoming studies

2/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

The problem

Let (X1,Y1), . . . , (Xn,Yn) be n independent copies of a random pair (X ,Y )such that X takes its values in Rd , d ≥ 1 and that Y given X = x hasconditional survival function

F (y |x) = y−1/γ(x)L(y |x), y > 0,

where L(·|x) is a slowly varying function at infinity.

We address the problem of estimating the function x 7→ γ(x), which iscalled the conditional tail-index of the random pair (X ,Y ).

3/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Some applications

• the estimation of high risk in finance;

• the description of the upper tail of the claim size distribution forreinsurers;

• study of extreme rainfalls in hydrology.

4/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Some existing methods

• Fixed design case (the Xi ’s are nonrandom):• Regression model: Smith (1989), Davison and Smith (1990);• Semi-parametric approach: Hall and Tajvidi (2000);• Local polynomials: Davison and Ramesh (2000);• Splines: Chavez-Demoulin and Davison (2005);• Moving window: Gardes and Girard (2008);• Nearest neighbor: Gardes and Girard (2010).

• Random design case:• Maximum likelihood: Wang and Tsai (2009);• Conditional quantile estimators: Daouia et al. (2011, 2013);• Threshold and kernel regression: Goegebeur et al. (2013).

5/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

A first idea

• Let Y1,n ≤ . . . ≤ Yn,n be the ordered statistics.

• The covariate associated with the ordered statistic Yn−i+1,n will bedenoted by X ∗i .

• For k ∈ 1, . . . , n, let Mk(x , h) is the number of covariates amongX ∗1 , . . . ,X

∗k which lie in the ball B(x , h) with center x and radius

h = h(n)→ 0.

6/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

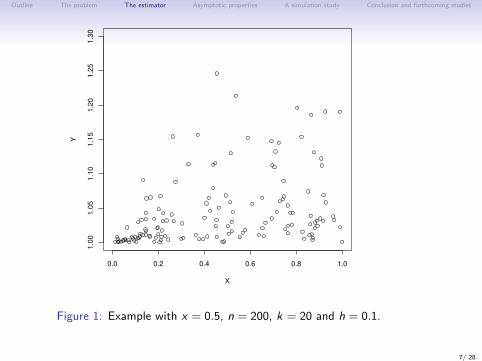

Figure 1: Example with x = 0.5, n = 200, k = 20 and h = 0.1.

7/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

Figure 1: Example with x = 0.5, n = 200, k = 20 and h = 0.1.

7/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

Figure 1: Example with x = 0.5, n = 200, k = 20 and h = 0.1.

7/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

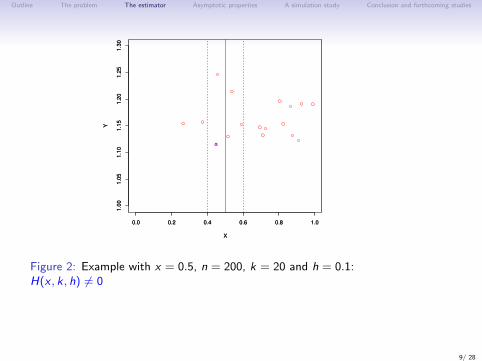

Figure 1: Example with x = 0.5, n = 200, k = 20 and h = 0.1:Mk(x , h) = 5.

7/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

A straightforward adaptation of Hill’s estimator is:

H(x , k, h) =1

Mk(x , h)− 1

k−1∑i=1

logYn−i+1,n

Yn−k+1,n1l‖X∗i −x‖∨‖X∗k −x‖≤h

if Mk(x , h) > 1 and H(x , k , h) = 0 otherwise, where 1l· is the indicator

function and ‖ · ‖ is a norm on Rd .

Problem: the behavior of H(x , k , h) as a function of k is very erratic.

8/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

x

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

Figure 2: Example with x = 0.5, n = 200, k = 20 and h = 0.1:H(x , k, h) 6= 0

9/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

x

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

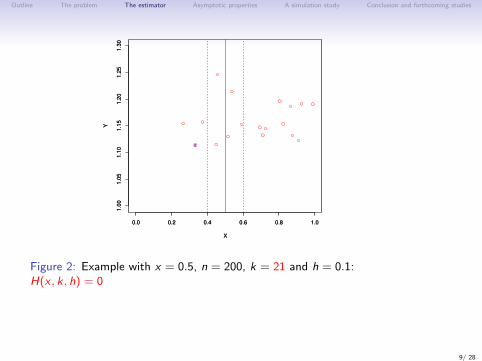

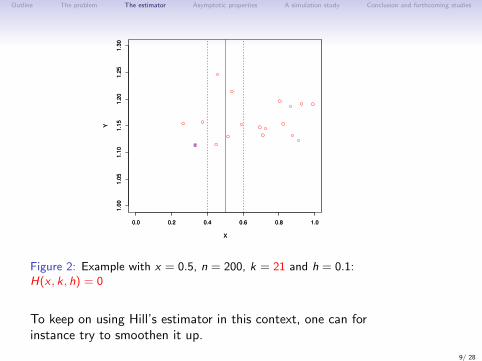

Figure 2: Example with x = 0.5, n = 200, k = 21 and h = 0.1:H(x , k, h) = 0

9/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

x

0.0 0.2 0.4 0.6 0.8 1.0

1.0

01

.05

1.1

01

.15

1.2

01

.25

1.3

0

X

Y

Figure 2: Example with x = 0.5, n = 200, k = 21 and h = 0.1:H(x , k, h) = 0

To keep on using Hill’s estimator in this context, one can forinstance try to smoothen it up.

9/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

A smoothed local Hill estimator

We propose to estimate the conditional tail index by an average on j of thestatistics H(x , j , h):

γa(x , kx , h) =1

kx − kx,a + 1

n∑j=2

H(x , j , h)1lkx,a≤Mj (x,h)≤kx

where

• a ∈ [0, 1) is a tuning parameter;

• kx = kx(n)→∞ is a positive sequence belonging to the interval[2/(1− a), n];

• kx,a = b(1− a)kxc where bzc is the integer part of z .

The parameter a controls the number of statistics H(x , j , h) appearing inthe estimator γa.

10/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Uniform consistency

From now on, it is assumed that X has a probability density function fwhose support is a subset S of Rd (d ≥ 1) having nonempty interior.

We wish to state the uniform consistency of our estimator on a compactsubset Ω of Rd which is contained in the interior of S . We first introducesome regularity assumptions:

(A1) It holds that

• The function γ is positive and continuous on S ;

• The function f is positive and Holder continuous on S ;

• For all x ∈ S , the function F (·|x) is continuous and decreasing.

11/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

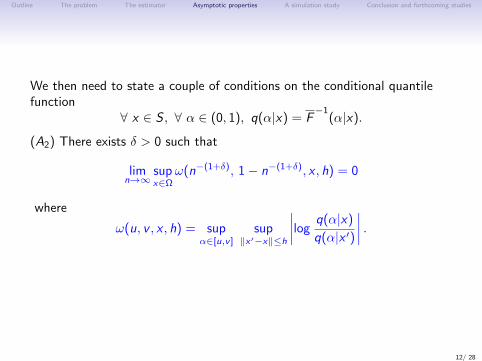

We then need to state a couple of conditions on the conditional quantilefunction

∀ x ∈ S , ∀ α ∈ (0, 1), q(α|x) = F−1

(α|x).

(A2) There exists δ > 0 such that

limn→∞

supx∈Ω

ω(n−(1+δ), 1− n−(1+δ), x , h) = 0

where

ω(u, v , x , h) = supα∈[u,v ]

sup‖x′−x‖≤h

∣∣∣∣logq(α|x)

q(α|x ′)

∣∣∣∣ .

12/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Finally, note that in our context, it holds that

∀ x ∈ S , ∀ α ∈ (0, 1), q(α|x) = α−γ(x)`(α−1|x)

where `(·|x) is a slowly varying function at infinity.

(A3) For all x ∈ S and t ≥ 1,

`(t|x) = c(x) exp

(∫ t

1

∆(u|x)

udu

),

where c(x) > 0 and ∆(·|x) is an ultimately monotonic function convergingto 0 at infinity.

13/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

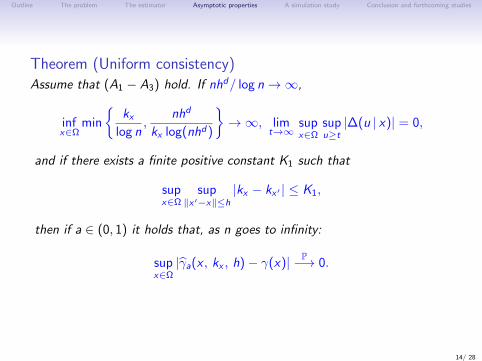

Theorem (Uniform consistency)Assume that (A1 − A3) hold. If nhd/ log n→∞,

infx∈Ω

min

kx

log n,

nhd

kx log(nhd)

→∞, lim

t→∞supx∈Ω

supu≥t|∆(u | x)| = 0,

and if there exists a finite positive constant K1 such that

supx∈Ω

sup‖x′−x‖≤h

|kx − kx′ | ≤ K1,

then if a ∈ (0, 1) it holds that, as n goes to infinity:

supx∈Ω|γa(x , kx , h)− γ(x)| P−→ 0.

14/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

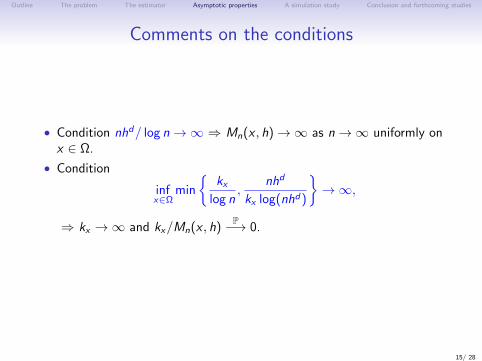

Comments on the conditions

• Condition nhd/ log n→∞ ⇒ Mn(x , h)→∞ as n→∞ uniformly onx ∈ Ω.

• Condition

infx∈Ω

min

kx

log n,

nhd

kx log(nhd)

→∞,

⇒ kx →∞ and kx/Mn(x , h)P−→ 0.

15/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

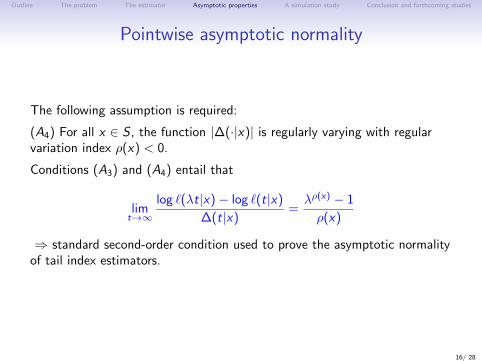

Pointwise asymptotic normality

The following assumption is required:

(A4) For all x ∈ S , the function |∆(·|x)| is regularly varying with regularvariation index ρ(x) < 0.

Conditions (A3) and (A4) entail that

limt→∞

log `(λt|x)− log `(t|x)

∆(t|x)=λρ(x) − 1

ρ(x)

⇒ standard second-order condition used to prove the asymptotic normalityof tail index estimators.

16/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Theorem (Pointwise asymptotic normality)Assume that (A1), (A3) and (A4) hold. Pick x in the interior of S.Conditionally to the event Mn(x , h) = mx, if

• mx →∞ and kx/mx → 0;

• k1/2x ω(m−1−δ

x , 1−m−1−δx , x , h)→ 0;

• k1/2x ∆(mx/kx |x)→ ξ(x) ∈ R

then for a ∈ [0, 1) one has:

k1/2x (γa(x , kx , h)− γ(x))

d−→ N(ξ(x)AB(a, x)

1− ρ(x), γ2(x)AV(a)

)where if a ∈ (0, 1):

AB(a, x) =1− (1− a)1−ρ(x)

a(1− ρ(x)), AV(a) =

2(a + (1− a) log(1− a))

a2

and if a = 0: AB(0, x) = AV(0) = 1.

17/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

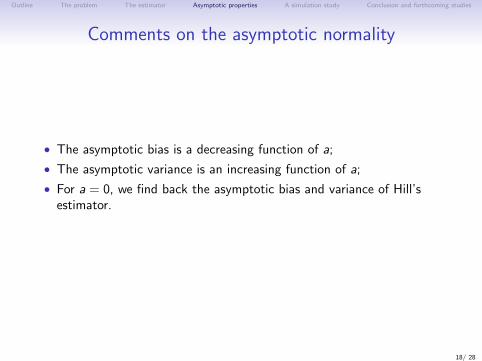

Comments on the asymptotic normality

• The asymptotic bias is a decreasing function of a;

• The asymptotic variance is an increasing function of a;

• For a = 0, we find back the asymptotic bias and variance of Hill’sestimator.

18/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

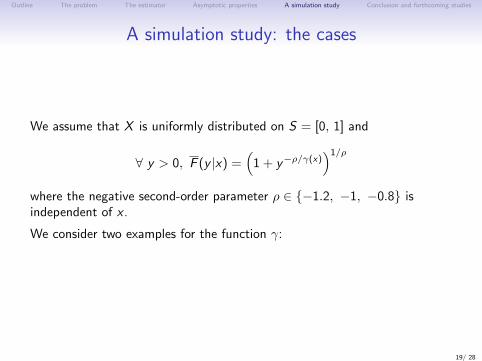

A simulation study: the cases

We assume that X is uniformly distributed on S = [0, 1] and

∀ y > 0, F (y |x) =(

1 + y−ρ/γ(x))1/ρ

where the negative second-order parameter ρ ∈ −1.2, −1, −0.8 isindependent of x .

We consider two examples for the function γ:

19/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

0.0 0.2 0.4 0.6 0.8 1.0

0.2

00

.25

0.3

00

.35

0.4

00

.45

0.5

0

x

γ 1(x

)

0.0 0.2 0.4 0.6 0.8 1.0

0.2

00

.25

0.3

00

.35

0.4

00

.45

0.5

0

x

γ 2(x

)

Figure 3: Functions γ1 (left) and γ2 (right)

Aim: in each case, to estimate the conditional tail-index on a grid of pointsx1, . . . , xM of [0, 1].

20/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Choice of the parameters

We take a = 3/7: this value of a provides reasonable performances in alarge range of situations.

⇒ it remains to choose:

• the bandwidth h;

• the number of upper order statistics kxi , for 1 ≤ i ≤ M.

Let h1, . . . , hP be a grid of possible values of h. For 1 ≤ i ≤ M,1 ≤ j ≤ P and k ∈ [2/(1− a),Mn(xi , hj)], we set

γi,j(k) = γa(xi , k , hj).

Our selection procedure is carried out in two steps.

21/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

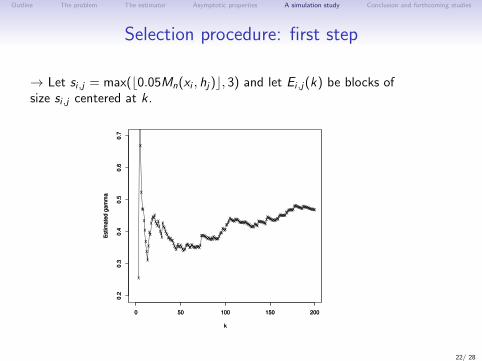

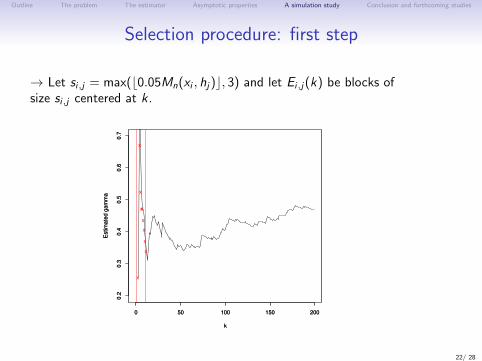

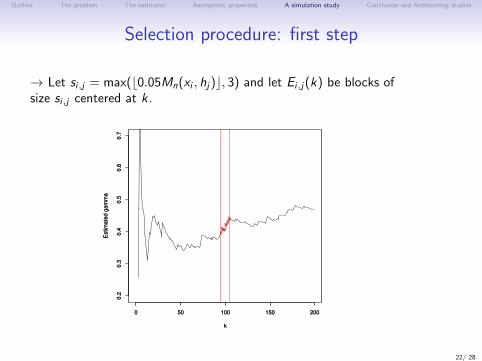

Selection procedure: first step

For every i ∈ 1, . . . ,M and j ∈ 1, . . . ,P, we make a preliminarychoice of kxi for a given hj .

22/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: first step

→ Let si,j = max(b0.05Mn(xi , hj)c, 3) and let Ei,j(k) be blocks ofsize si,j centered at k .

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

x

x

x

xx

x

x

x

x

x

x

xx

xxxxx

xxxxxxxx

xxxxxxxxxxxx

xxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxx

xxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxx

xxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxx

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

estim

ate

d g

am

ma

22/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: first step

→ Let si,j = max(b0.05Mn(xi , hj)c, 3) and let Ei,j(k) be blocks ofsize si,j centered at k .

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

x

x

x

xx

x

x

x

x

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

22/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: first step

→ Let si,j = max(b0.05Mn(xi , hj)c, 3) and let Ei,j(k) be blocks ofsize si,j centered at k .

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

xxxxxxxxxxx

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

22/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: first step

→ Let si,j = max(b0.05Mn(xi , hj)c, 3) and let Ei,j(k) be blocks ofsize si,j centered at k .

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

xxxxx

xxxxxx

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

22/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: first step

→ Let Ei,j(k∗) be the block where the estimated gammas hasminimal variance.

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

xxxxxxxxxxx

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

22/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

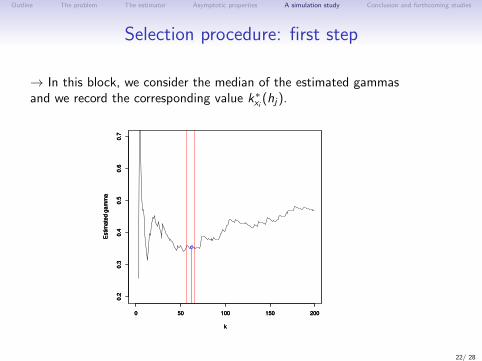

Selection procedure: first step

→ In this block, we consider the median of the estimated gammas

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

x

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

o

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

22/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

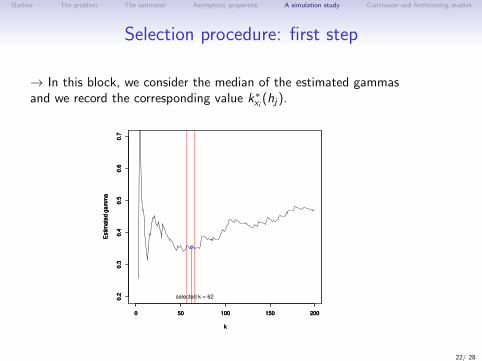

Selection procedure: first step

→ In this block, we consider the median of the estimated gammasand we record the corresponding value k∗xi (hj).

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

o

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

22/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: first step

→ In this block, we consider the median of the estimated gammasand we record the corresponding value k∗xi (hj).

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

o

0 50 100 150 200

0.2

0.3

0.4

0.5

0.6

0.7

k

Estim

ate

d g

am

ma

selected k = 62

22/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: second step

We now choose the parameter h.

23/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: second step

→ For every i ∈ 1, . . . ,M, we plot the estimator γi,j(k∗xi (hj)) as afunction of hj , j ∈ 1, . . . ,P

0.05 0.10 0.15 0.20 0.25

0.4

0.5

0.6

0.7

0.8

0.9

h

Estim

ate

d g

am

ma

23/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: second step

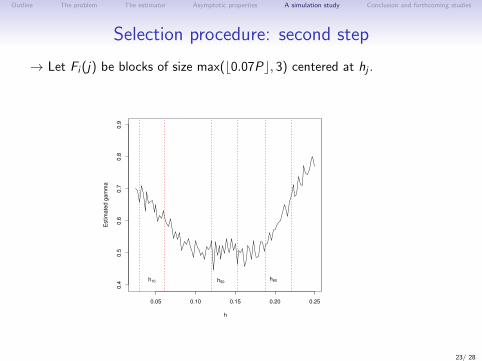

→ Let Fi (j) be blocks of size max(b0.07Pc, 3) centered at hj .

0.05 0.10 0.15 0.20 0.25

0.4

0.5

0.6

0.7

0.8

0.9

h

Estim

ate

d g

am

ma

h10 h50h80

23/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: second step

→ Compute the standard deviation σi (j) of each block Fi (j) and letσ(j) be the mean of the σi (j), 1 ≤ i ≤ M.

0.05 0.10 0.15 0.20 0.25

0.4

0.5

0.6

0.7

0.8

0.9

h

Estim

ate

d g

am

ma

h10 h50h80

σi(10)

σi(50)

σi(50)

23/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: second step

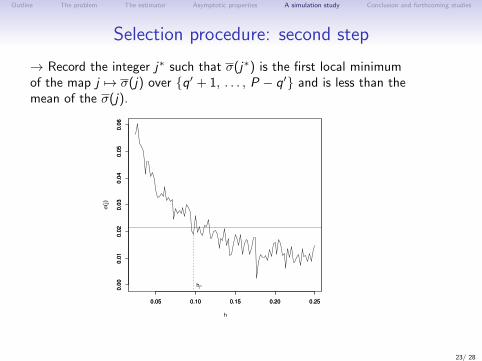

→ Record the integer j∗ such that σ(j∗) is the first local minimumof the map j 7→ σ(j) over q′ + 1, . . . , P − q′ and is less than themean of the σ(j).

0.05 0.10 0.15 0.20 0.25

0.0

00

.01

0.0

20

.03

0.0

40

.05

0.0

6

h

σ(j

)

0.05 0.10 0.15 0.20 0.25

0.0

00

.01

0.0

20

.03

0.0

40

.05

0.0

6

hjx

23/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Selection procedure: second step

Conclusion We then choose h∗ = hj∗ and k∗xi = k∗xi (hj∗).

23/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

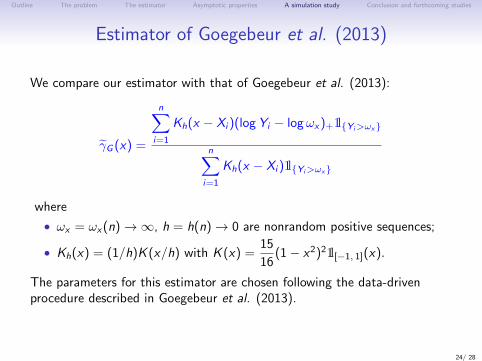

Estimator of Goegebeur et al. (2013)

We compare our estimator with that of Goegebeur et al. (2013):

γG (x) =

n∑i=1

Kh(x − Xi )(log Yi − logωx)+1lYi>ωx

n∑i=1

Kh(x − Xi )1lYi>ωx

where

• ωx = ωx(n)→∞, h = h(n)→ 0 are nonrandom positive sequences;

• Kh(x) = (1/h)K (x/h) with K (x) =15

16(1− x2)21l[−1, 1](x).

The parameters for this estimator are chosen following the data-drivenprocedure described in Goegebeur et al. (2013).

24/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Methodology

• 100 samples with size n = 1000 of random copies of the pair (X , Y )are generated;

• The estimation is carried out on a grid of M = 35 evenly spaced pointsin [0, 1];

• Selection procedure: P = 100 evenly spaced values of h ranging from0.025 to 0.25 are tested.

MSEs (over the 100 samples) are computed for both estimators.

25/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

SituationEstimator γG Smoothed Hill

of Goegebeur et al. estimator γaγ = γ1

ρ = −0.8 0.0241 0.0115

ρ = −1 0.0157 0.00753

ρ = −1.2 0.00972 0.00512

γ = γ2

ρ = −0.8 0.0321 0.0164

ρ = −1 0.0198 0.0102

ρ = −1.2 0.0148 0.00724

Table 1: MSEs associated to the estimators in all cases.

Both estimations worsen as |ρ| decreases. Remark that the smoothed Hillestimator γa performs better than the estimator γG of Goegebeur et al.(2013) in all the considered situations.

26/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

Conclusion and forthcoming studies

• A new estimator of the conditional tail index was proposed with aprocedure to select the hyper-parameters.

• Its uniform consistency was established.

Future developments include trying to obtain the asymptotic distribution ofthe uniform error

supx∈Ω|γa(x , kx , h)− γ(x)| .

27/ 28

Outline The problem The estimator Asymptotic properties A simulation study Conclusion and forthcoming studies

References

Gardes, L., Stupfler, G. (2014). Estimation of the conditional tail indexusing a smoothed local Hill estimator, Extremes 17(1), 45–75.

Goegebeur, Y., Guillou, A., Schorgen, A. (2014). Nonparametric regressionestimation of conditional tails – the random covariate case, Statistics,48(4), 732–755.

28/ 28