estimating - dr. ahmed h. elyamanydrahmedelyamany.weebly.com/.../2.estimating.pdf · functions of...

TRANSCRIPT

ESTIMATINGAhmed Elyamany, PhD, AVS

Estimate Definitions

• An estimate is a quantitative assessment of a likely outcome.

• It should always include some indication of accuracy (e.g., + or - x percent).

Functions of Estimating

• Could Assess cost of construction from the conceptual design phase (Owner, Designer & Sometimes Contractor ). Feedback to• Conceptual Design for Alternative Architecture

• Feasibility of the Project

• Project / Company Alignment of Objectives, Constraints, Strategic Goals and Policies

• Provide the basis for bidding & contracting (Contractor)

• Provide a baseline for cost control and post project evaluation (Owner & Contractor)

�3

Estimate development phases

• Project initiation phase:• Project initiation estimate

• Feasibility phase:• Option analysis estimate

• Procurement strategy phase:• Concept estimate

• Preliminary and detailed design phase :• Preliminary design estimate

• Detailed design estimate

• Construction procurement phase:• Budget cost estimate

• Construction phase:• Budget cost updates

Project Initiation Estimate

• Project initiation estimate is produced during the Project initiation phase, normally as part of a Project initiation report.

• This estimate provides budgets for forward programming.

• Major risks must be identified and their impact on the out-turn cost shall be assessed and included in the estimate.

Option Analysis estimate

• Option analysis estimate is prepared during the concept phase and compare project options.

• Such estimate is based on a preliminary brief, limited general and site information, and the scope of work.

• All possible risks must be identified and included in the estimate.

Preliminary Design Estimate

• Preliminary design estimate is prepared based on an advanced design.

• It provides a check on the position between the approved scope/budget and the Project estimate

• Occurs immediately prior to the detailed design stage.

Detailed Design Estimate

• Detailed design estimate includes all components of a project prepared prior to seeking construction funding and the tendering of the physical works.

• It is based on detailed design documentation, which includes final design drawings, specifications, the schedule of prices, and all consent conditions.

Budget Cost Estimate

• Budget cost estimate is prepared during the tender evaluation period and updated (at least) quarterly during the construction phase until project completion.

• It is based on the tendered price of selected tender and is used to confirm that construction funding allocations are sufficient.

• It should include change orders provided during the construction stage.

Estimating Methods

• Global estimate

• Unit Rate estimate

• First Principle estimate

• Expert opinion

• Trend analysis

Global Estimate / Unit

method• Global estimating is an approximate method of estimating that

involves using global composite rates.

• With this method, the Project consists of one or a few estimating elements on which the estimate is prepared.

• Examples include: • Bridge costs per square meter of deck area; • Road costs per kilometer.

• Used when little is known about the Project.

• This estimate requires using historical data.

• Analyze the unit costs of a number of completed projects of the same type

Global Estimate / Unit method

• Level 1

• It is an estimate prepared from the description of the project scope

where there is little or no design.

• Accuracy falls between +40 and ‐10 %.

• Level 2 • It is an estimate prepared upon completion of preliminary design.

• Accuracy falls between +25 and ‐5 %.

• Level 3 • It is an estimate prepared upon completion of the final design.

• Accuracy falls between +10 and ‐3 %.

Global Estimate / Unit method

• Generally prepared by:• The owner as part of economic feasibility analysis or by

• The designer for selecting the design alternatives

• The contractor for negotiated work between owner and a contractor.

• Requires cost information from previous projects of similar type and size is essential.

• From the cost records of previous projects, the estimator can develop unit costs to forecast the cost of future projects.

Global Estimate / Unit method

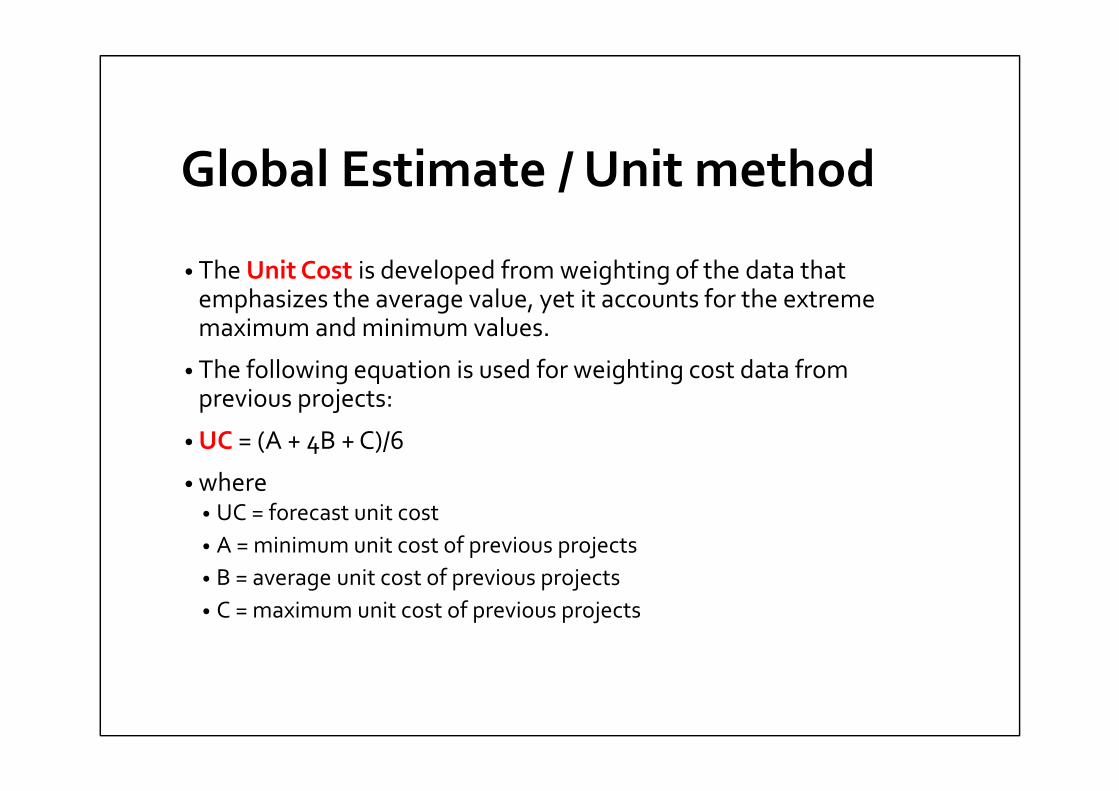

• The Unit Cost is developed from weighting of the data that emphasizes the average value, yet it accounts for the extreme maximum and minimum values.

• The following equation is used for weighting cost data from previous projects:

• UC = (A + 4B + C)/6

• where • UC = forecast unit cost

• A = minimum unit cost of previous projects

• B = average unit cost of previous projects

• C = maximum unit cost of previous projects

Global Estimate / Unit method

• Adjustment of Unit Cost• The cost information of previously completed projects must be adjusted

for the following before applying the cost for the proposed project

• Time,

• Location,

• Size

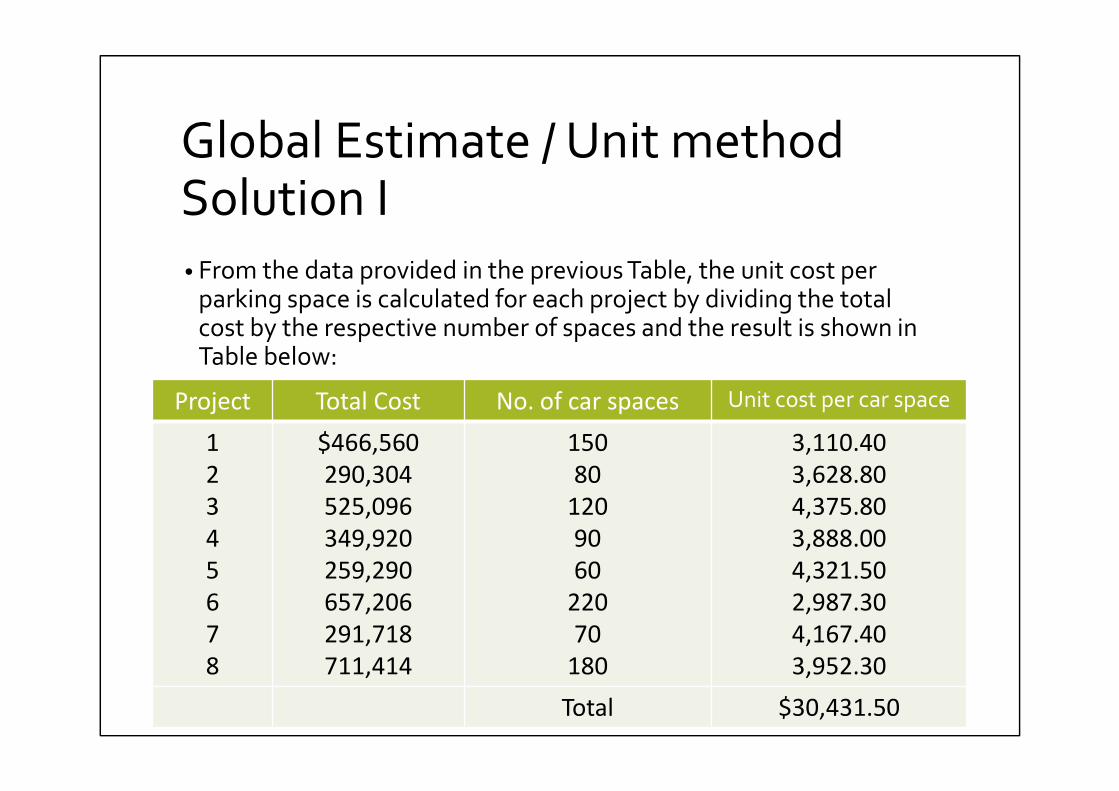

Global Estimate / Unit methodExample I• Cost data from eight previously constructed parking garage projects is

shown below.

• Use the weighted unit cost to determine the conceptual cost estimate for a proposed parking garage that is to contain 135 parking spaces.

Project Total Cost No. of car spaces

1

2

3

4

5

6

7

8

$466,560

290,304

525,096

349,920

259,290

657,206

291,718

711,414

150

80

120

90

60

220

70

180

Global Estimate / Unit methodSolution I

• From the data provided in the previous Table, the unit cost per parking space is calculated for each project by dividing the total cost by the respective number of spaces and the result is shown in Table below:

Project Total Cost No. of car spaces Unit cost per car space

1

2

3

4

5

6

7

8

$466,560

290,304

525,096

349,920

259,290

657,206

291,718

711,414

150

80

120

90

60

220

70

180

3,110.40

3,628.80

4,375.80

3,888.00

4,321.50

2,987.30

4,167.40

3,952.30

Total $30,431.50

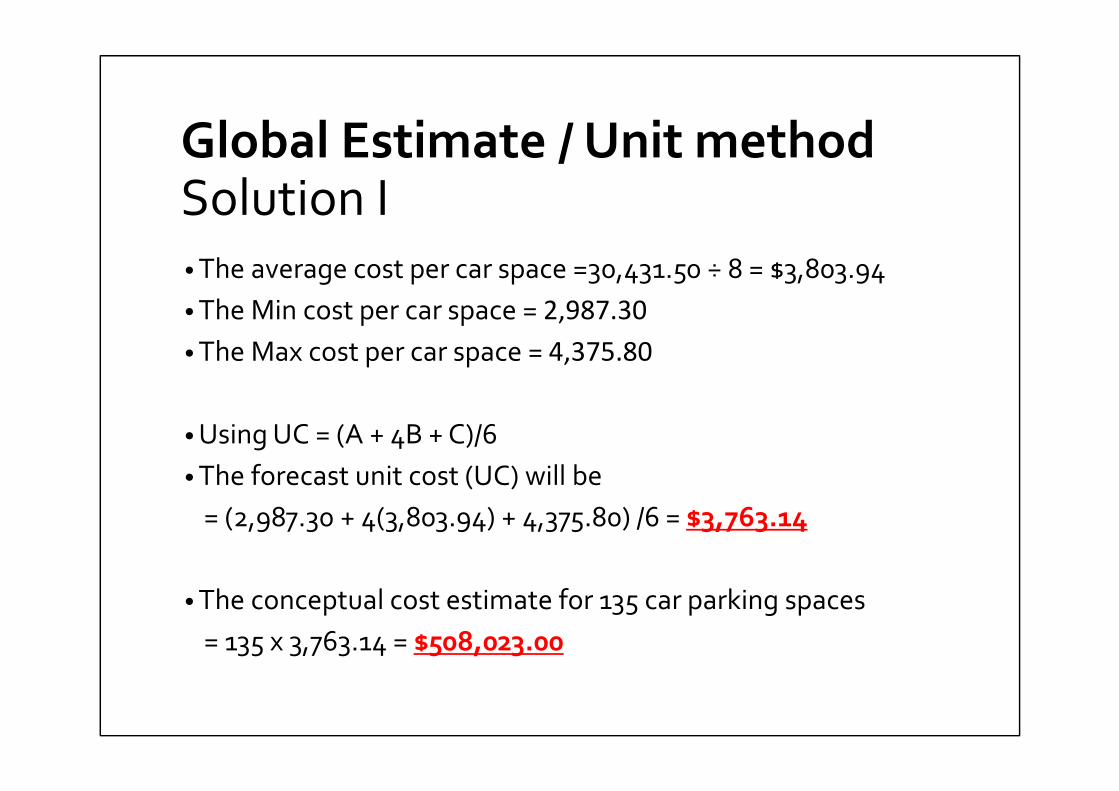

Global Estimate / Unit methodSolution I• The average cost per car space =30,431.50 ÷ 8 = $3,803.94

• The Min cost per car space = 2,987.30

• The Max cost per car space = 4,375.80

• Using UC = (A + 4B + C)/6

• The forecast unit cost (UC) will be

= (2,987.30 + 4(3,803.94) + 4,375.80) /6 = $3,763.14

• The conceptual cost estimate for 135 car parking spaces

= 135 x 3,763.14 = $508,023.00

Unit Rate Estimate

• Unit rate estimates are based on the historical bid price

• Aided by sound engineering judgment, which can be used for estimating the cost of each element of the project by multiplying the quantity of work with historical unit rates.

• Total project cost will be determined by the sum of all elemental costs.

Cost‐Based Estimating

• A cost-based approach, aided by sound engineering judgment, is the most ultimate of the estimate techniques and uses information down to the lowest level of detail available.

• Utilized by Contractors to price projects.

• Accuracy of the estimate depends on the accuracy of available information.

Expert Opinion / Spot Estimate

• Data is collected from the specialist

• This technique may be used for activities for which there is no other sound basis and is most appropriate in the early stages of a project .

• These cost estimates should include:• A list of the experts consulted,

• Their relevant experience,

• The basis of their opinion.

Trend Analysis

• This estimating technique is used for in-progress, current work.

• A trend is first established by comparing originally planned costs against actual costs for work performed to date.

• Derived cost indices are then used to adjust the estimate of work not yet completed.

• This technique can be used to update cost estimates developed using other techniques.

Cost‐Based‐Unit‐Rate Estimate

• Uses historical bid price down to the lowest level of detail available

23

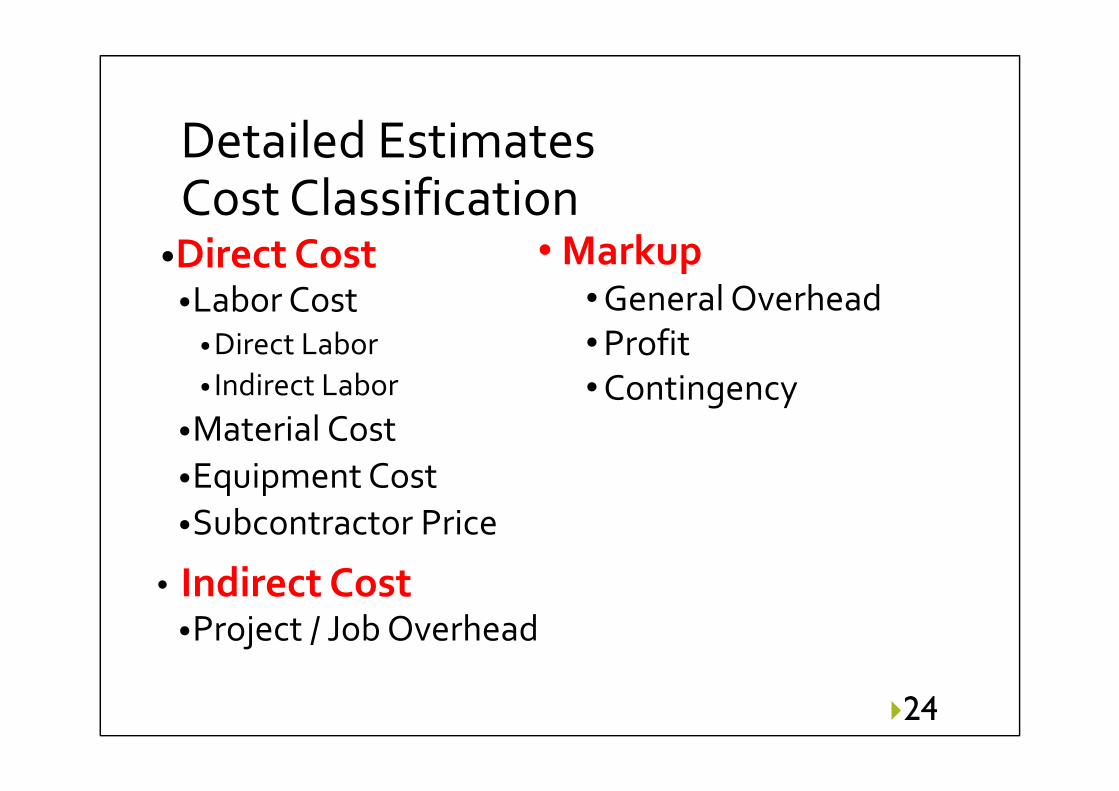

Detailed EstimatesCost Classification

•Direct Cost•Labor Cost

• Direct Labor

• Indirect Labor

•Material Cost

•Equipment Cost

•Subcontractor Price

• Indirect Cost•Project / Job Overhead

�24

• Markup• General Overhead

• Profit

• Contingency

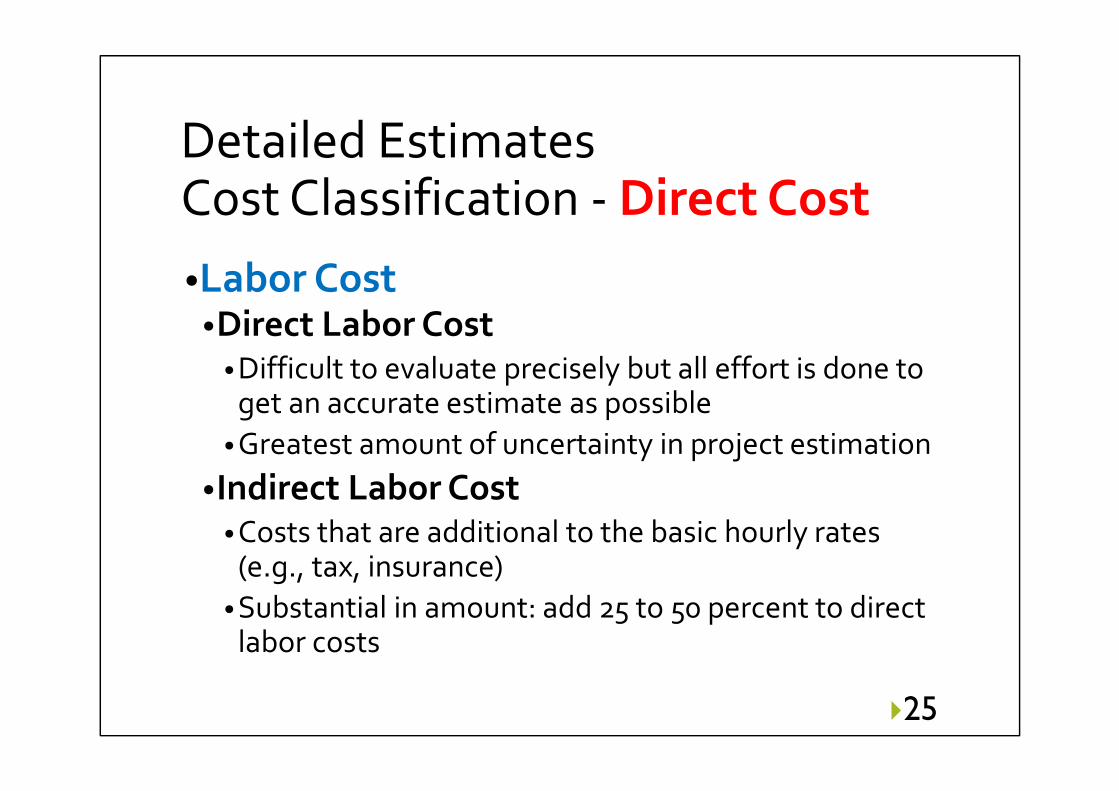

Detailed EstimatesCost Classification - Direct Cost

•Labor Cost•Direct Labor Cost

• Difficult to evaluate precisely but all effort is done to get an accurate estimate as possible

• Greatest amount of uncertainty in project estimation

•Indirect Labor Cost• Costs that are additional to the basic hourly rates

(e.g., tax, insurance)

• Substantial in amount: add 25 to 50 percent to direct labor costs

�25

Detailed EstimatesCost Classification - Direct Cost

•Material Cost• All materials that are utilized in the finished structure.

•Equipment Cost• Costs Includes: ownership, lease or rental expenses, and

operating costs

•Subcontractor Price• Includes quotations from all subcontractors working on

the project

• Quotations submitted by the subcontractor usually require extensive review by the general contractor’s estimator to determine what they include & do not include

�26

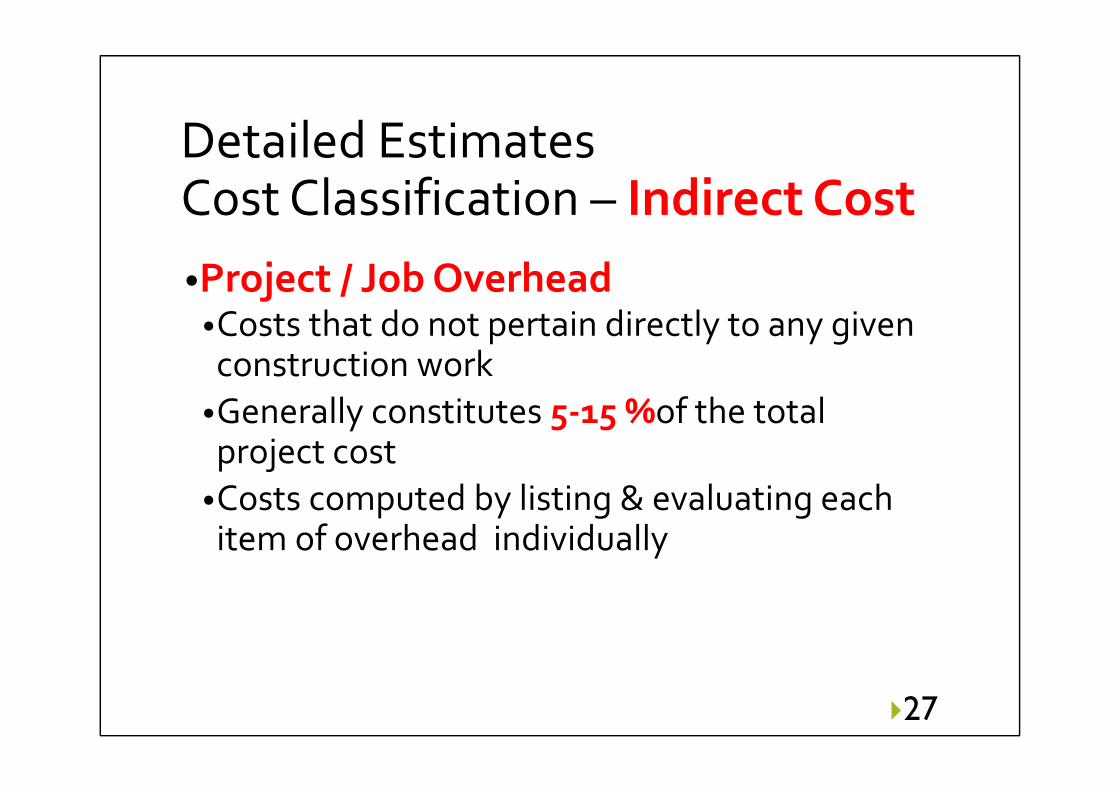

Detailed EstimatesCost Classification – Indirect Cost

•Project / Job Overhead•Costs that do not pertain directly to any given construction work

•Generally constitutes 5‐15 %of the total project cost

•Costs computed by listing & evaluating each item of overhead individually

�27

Detailed EstimatesCost Classification – Indirect Cost

�28

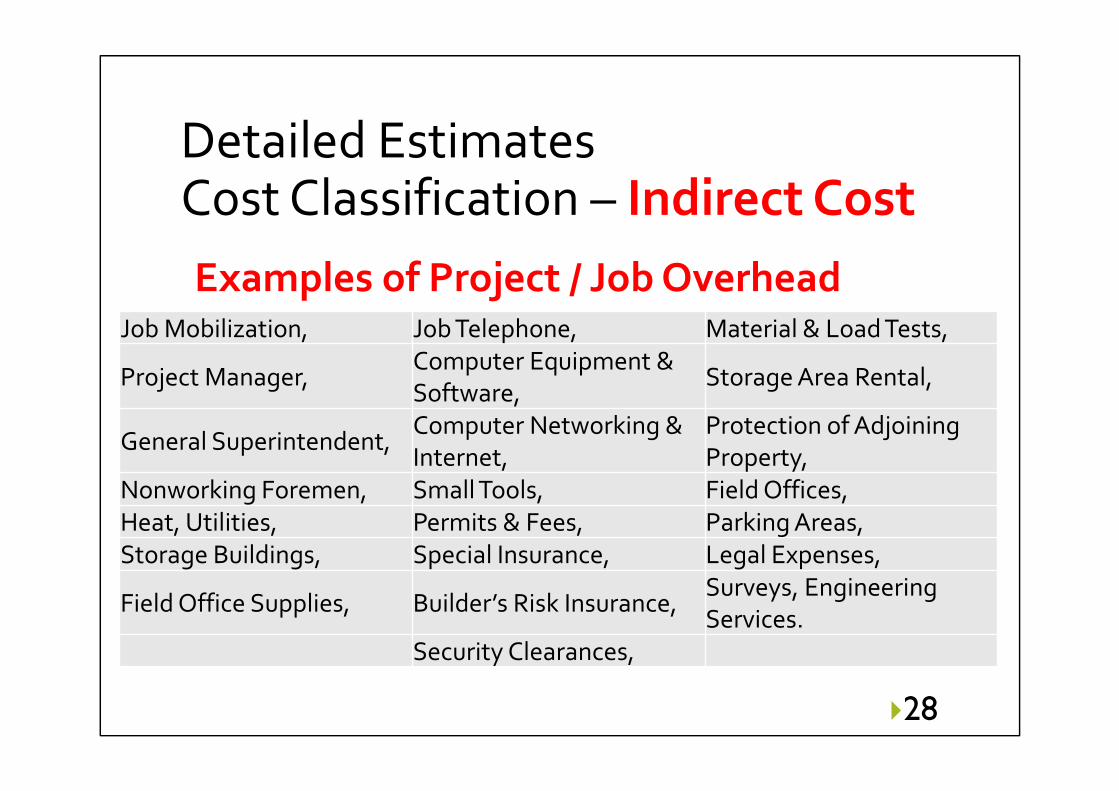

Examples of Project / Job OverheadJob Mobilization, Job Telephone, Material & Load Tests,

Project Manager, Computer Equipment &

Software, Storage Area Rental,

General Superintendent, Computer Networking &

Internet,

Protection of Adjoining

Property,

Nonworking Foremen, Small Tools, Field Offices,

Heat, Utilities, Permits & Fees, Parking Areas,

Storage Buildings, Special Insurance, Legal Expenses,

Field Office Supplies, Builder’s Risk Insurance, Surveys, Engineering

Services.

Security Clearances,

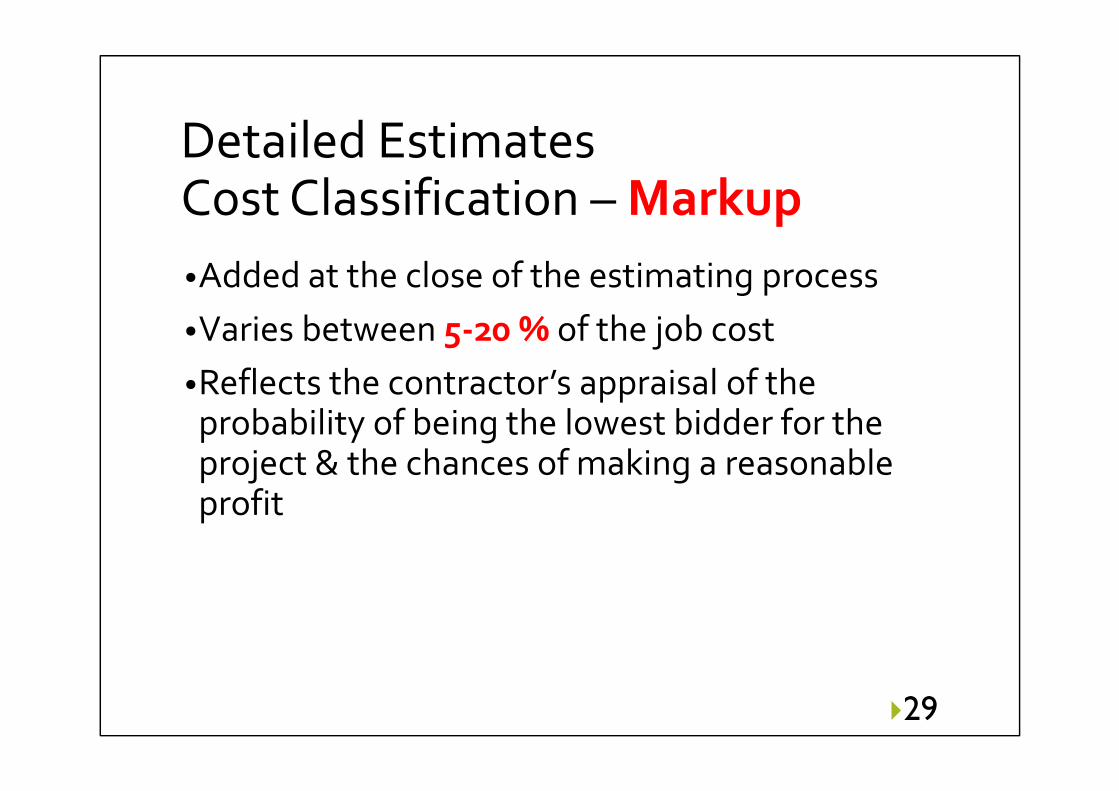

Detailed EstimatesCost Classification – Markup

•Added at the close of the estimating process

•Varies between 5‐20 % of the job cost

•Reflects the contractor’s appraisal of the probability of being the lowest bidder for the project & the chances of making a reasonable profit

�29

Detailed EstimatesCost Classification – Markup

Factors considered when deciding on a job markup include:

•Project size & complexity,

•Provisions of the contract documents,

•Difficulties inherent in the work,

•Identities of the owner & architect/engineer

�30

Detailed EstimatesCost Classification – Markup

Include allowance for:

•General / Office Overhead• Includes costs to support the overall company construction

program

• Normally included in the bid as a percentage of the total estimated job cost

• Examples of General / Office Overhead include:

�31

office rent furniture travel

office insurance telephone & internet association dues

heat, legal expenses salaries of executives

electricity donations salaries of office employees

office supplies advertising

Detailed EstimatesCost Classification – Markup

Include allowance for:

•Profit

•Contingency

�32

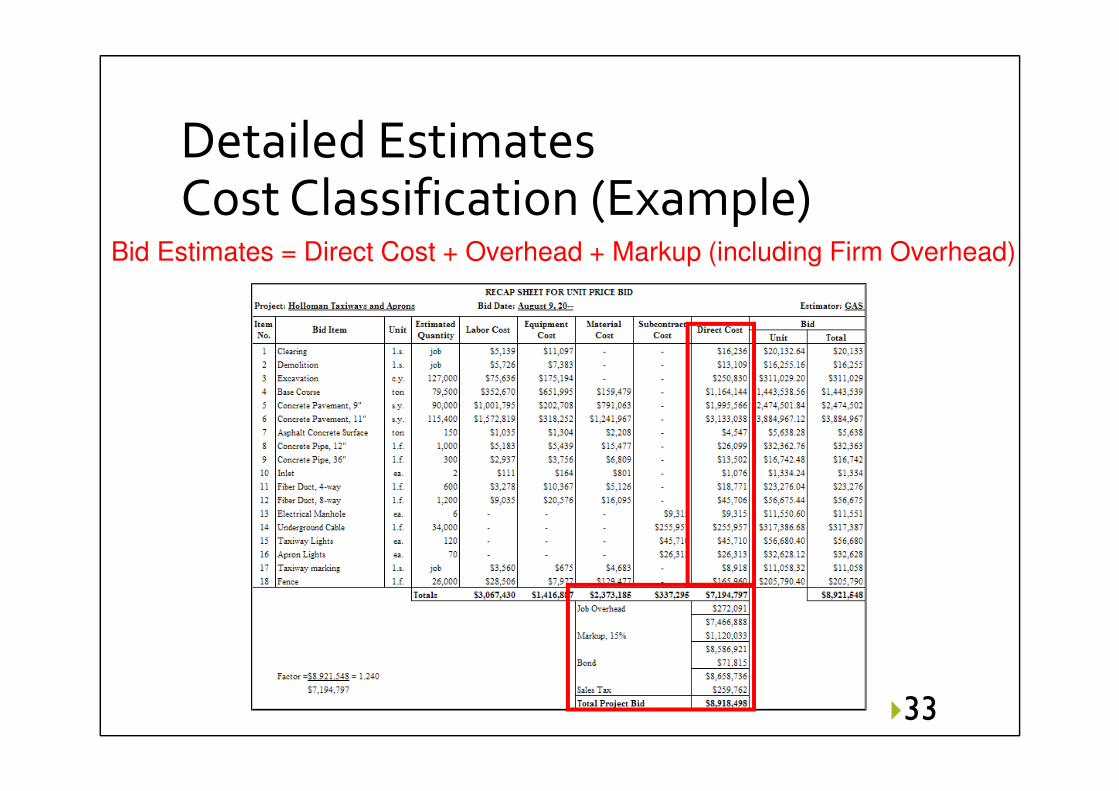

Detailed EstimatesCost Classification (Example)

�33

Bid Estimates = Direct Cost + Overhead + Markup (including Firm Overhead)

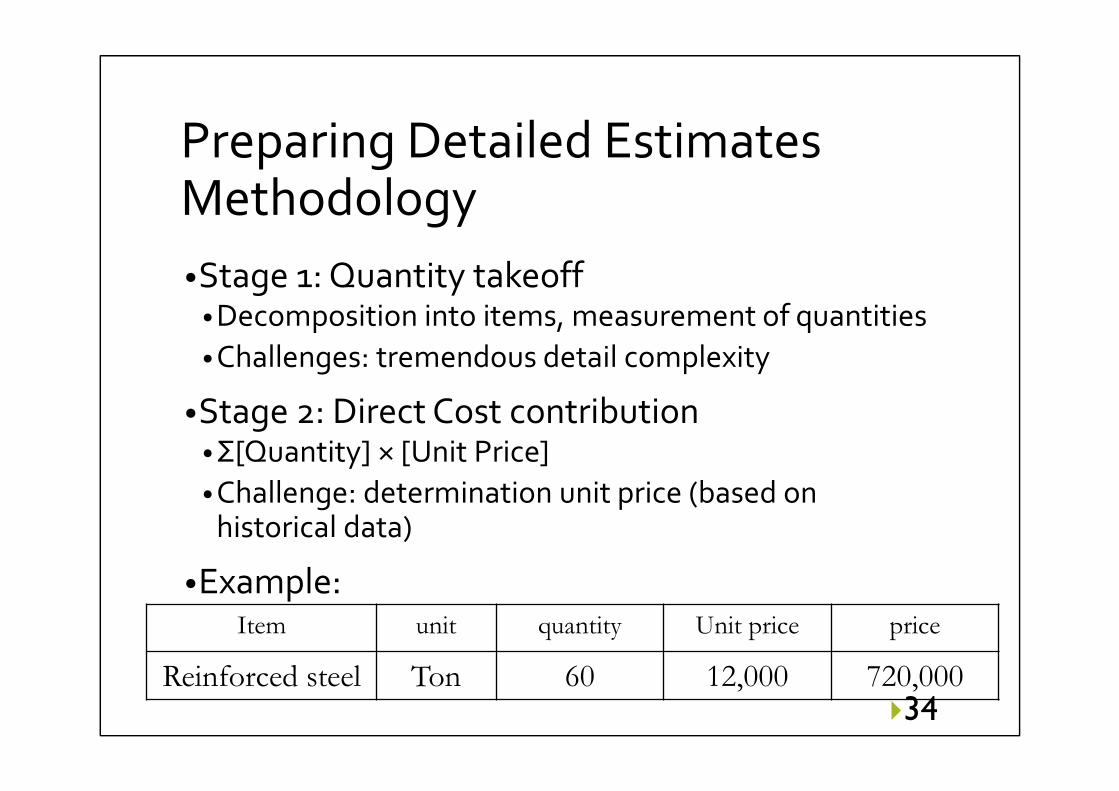

Preparing Detailed EstimatesMethodology

•Stage 1: Quantity takeoff• Decomposition into items, measurement of quantities

• Challenges: tremendous detail complexity

•Stage 2: Direct Cost contribution• Σ[Quantity] × [Unit Price]

• Challenge: determination unit price (based on historical data)

•Example:

�34

Item unit quantity Unit price price

Reinforced steel Ton 60 12,000 720,000

Estimate PreparationProject Study

• Drawings

• Specifications

• Contract conditions

• Meeting with the owner and architect

• Site visit

35

Quantity Takeoff

• Once the estimating tasks are identified, categorized, and organized, the team begins the quantity takeoff, which is the foundation to the estimate.

• The purpose of a quantity takeoff is to determine accurately the quantity of construction work.

36

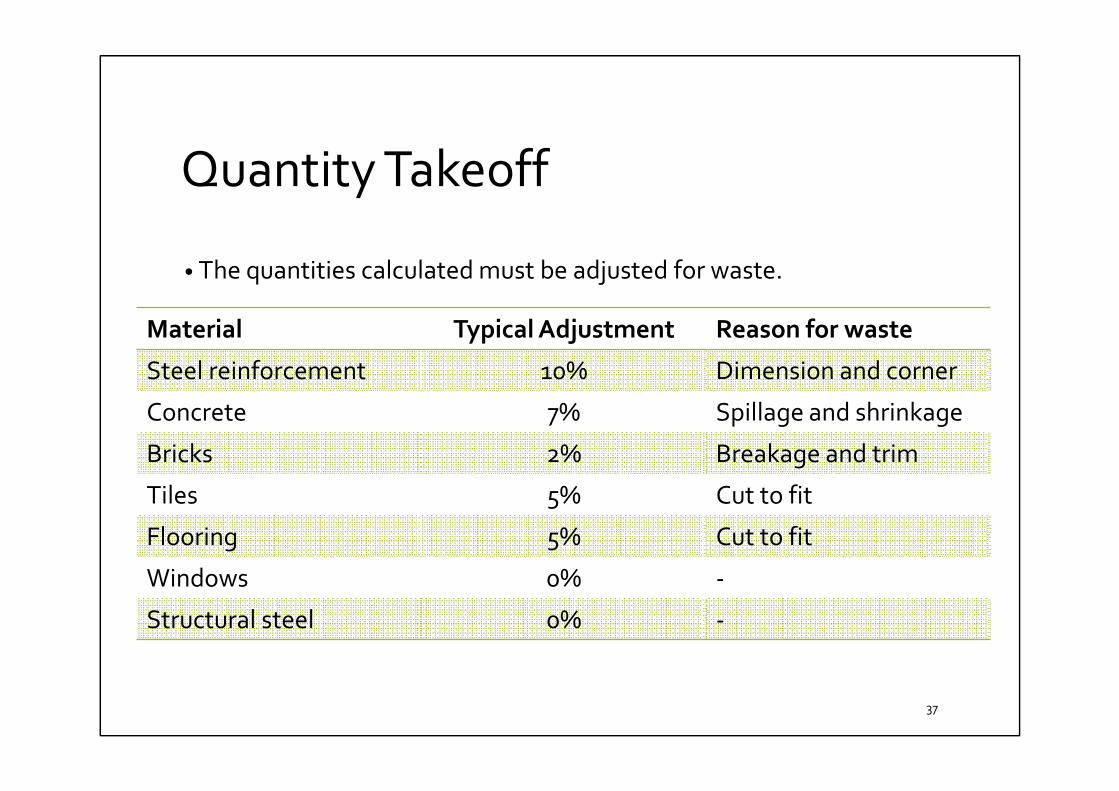

Quantity Takeoff

• The quantities calculated must be adjusted for waste.

37

Material Typical Adjustment Reason for waste

Steel reinforcement 10% Dimension and corner

Concrete 7% Spillage and shrinkage

Bricks 2% Breakage and trim

Tiles 5% Cut to fit

Flooring 5% Cut to fit

Windows 0% -

Structural steel 0% -

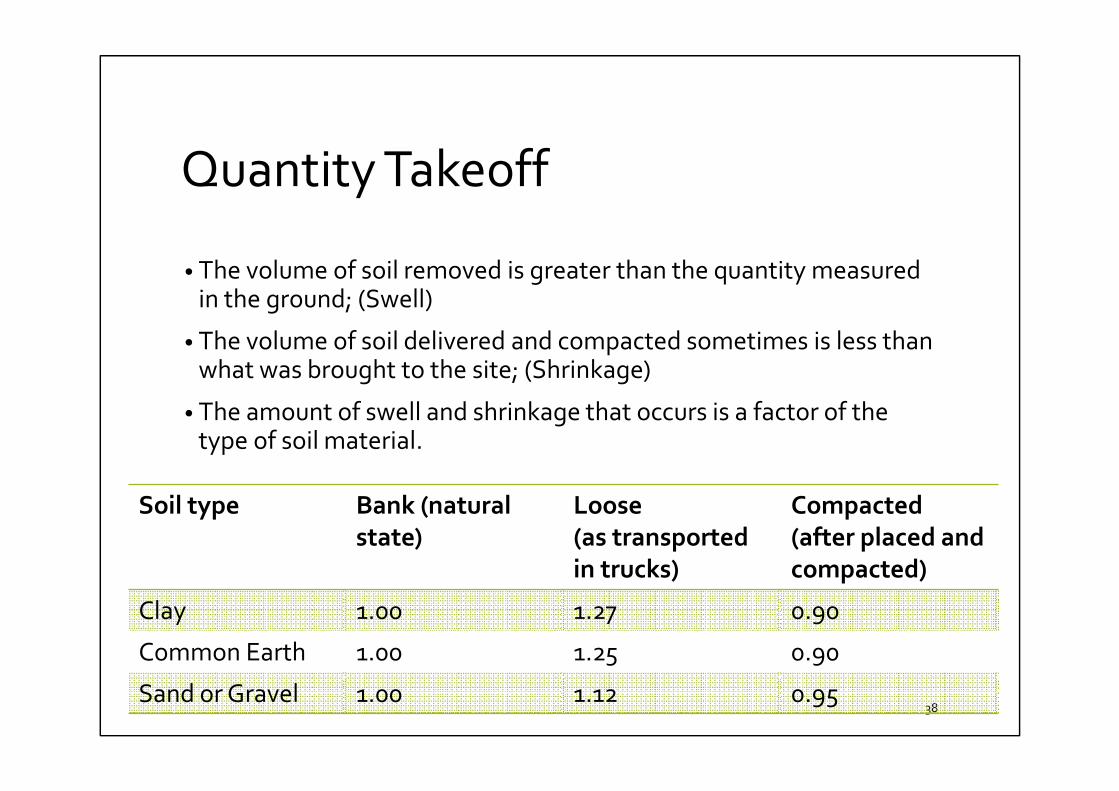

Quantity Takeoff

• The volume of soil removed is greater than the quantity measured in the ground; (Swell)

• The volume of soil delivered and compacted sometimes is less than what was brought to the site; (Shrinkage)

• The amount of swell and shrinkage that occurs is a factor of the type of soil material.

38

Soil type Bank (natural

state)

Loose

(as transported

in trucks)

Compacted

(after placed and

compacted)

Clay 1.00 1.27 0.90

Common Earth 1.00 1.25 0.90

Sand or Gravel 1.00 1.12 0.95

Site Visit

• General description.

• Soil.

• Topography.

• Transportations.

• Utilities.

• Labors.

• Safety arrangements.

• Temporary buildings.

• Neighbors.

39

Cost of Labor

• People are the most important resource on a project.

• The cost to hire a labor includes the straight-time wage plus any overtime pay, worker’s insurance, social security tax, liability, and health insurance.

• Straight time wage normally applies to work done during the 40-hr work week, 8 hrs/day and 5 days/week.

• For work in excess of 8 hr/day or 40 hr/week, the straight-time wage rate is generally increased to 1.5 to 2 times the straight-time rate.

Detailed Estimates Labor Costs

• Categorized Bid Estimate (not overall unit prices)

• Unit Labor Cost = HC / LP ($/unit)• HC = Hourly Labor cost ($/hours)

• LP = Labor Productivity (units/hour)

• Total Labor Cost = Q * HC/LP• Q = Total quantity of work

�41

Detailed Estimates Labor Cost - Prices Related

• Components• Wages (varies by area, seniority, …)

• Insurance (varies w/contractor record, work type)

• Social security benefits

• health benefits

• Wage premiums (e.g., overtime, shift-work differentials, hazardous work)

�42

Detailed Estimates Labor Cost - Productivity

• Difficult but critical• High importance of qualitative factors (environment, morale, fatigue,

learning, etc)

• The primary means to control labor costs

• Historical data available• Firm updated database

• Department of Labor, professional organizations, state governments

�43

Detailed Estimates Productivity Considerations

• Considerations• Location of jobsite (local skill base, hiring & firing)

• Learning curves

• Work schedule (overtime, shift work)

• Weather

• Environment

• Location on jobsite, noise, closeness to materials

• Management style (e.g., incentive)

• Worksite rules

�44

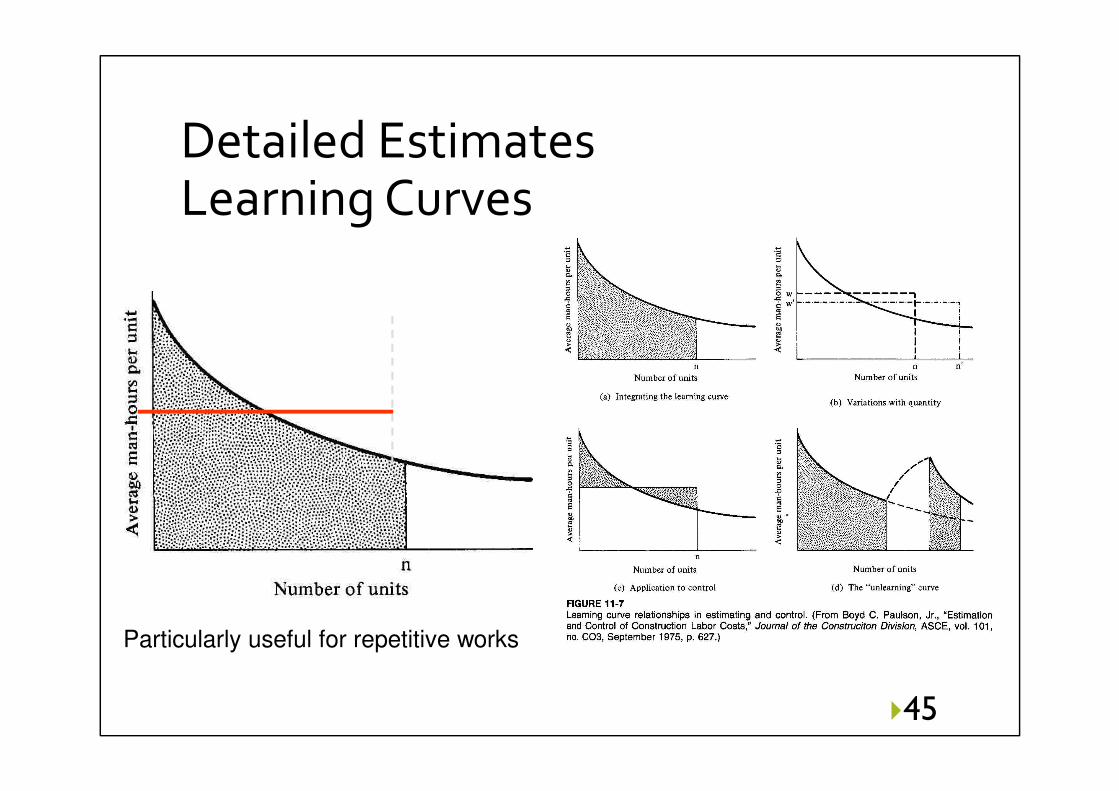

Detailed Estimates Learning Curves

�45

Particularly useful for repetitive works

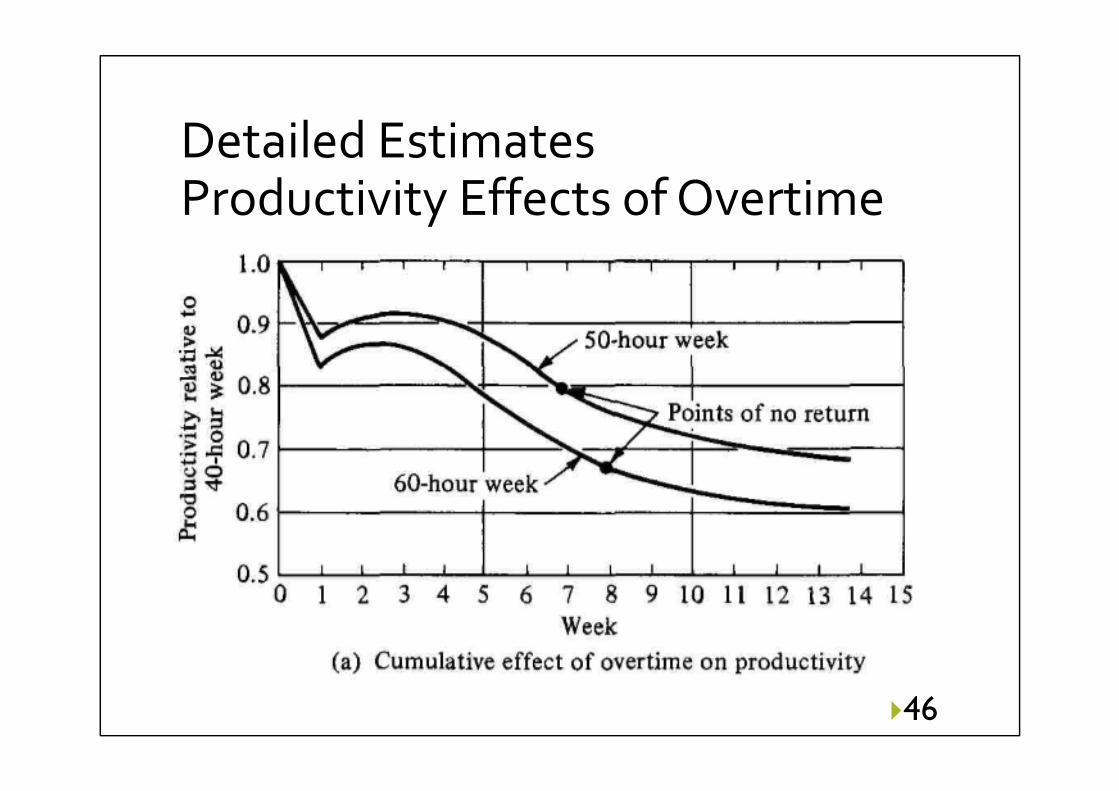

Detailed Estimates Productivity Effects of Overtime

�46

Cost of Equipment

• All projects involve use of construction equipment to some extent.

• Construction equipment can be purchased or rented. • Purchased when used extensively

• Rented when used sparingly.

• When equipment is purchased, it is necessary to determine:• (a) ownership cost

• (b) operating cost

Ownership costInvestment on money

• 1. Investment on money

• The money to purchase the equipment will be borrowed from a lender, or it will be taken from the reserve funds of the purchaser.

• So, either the lender will charge an interest for the borrowed money, or the buyer will lose any interest income on the money taken out of his reserve funds.

• Therefore, the interest expense or the loss of the interest income, is part of the ownership cost.

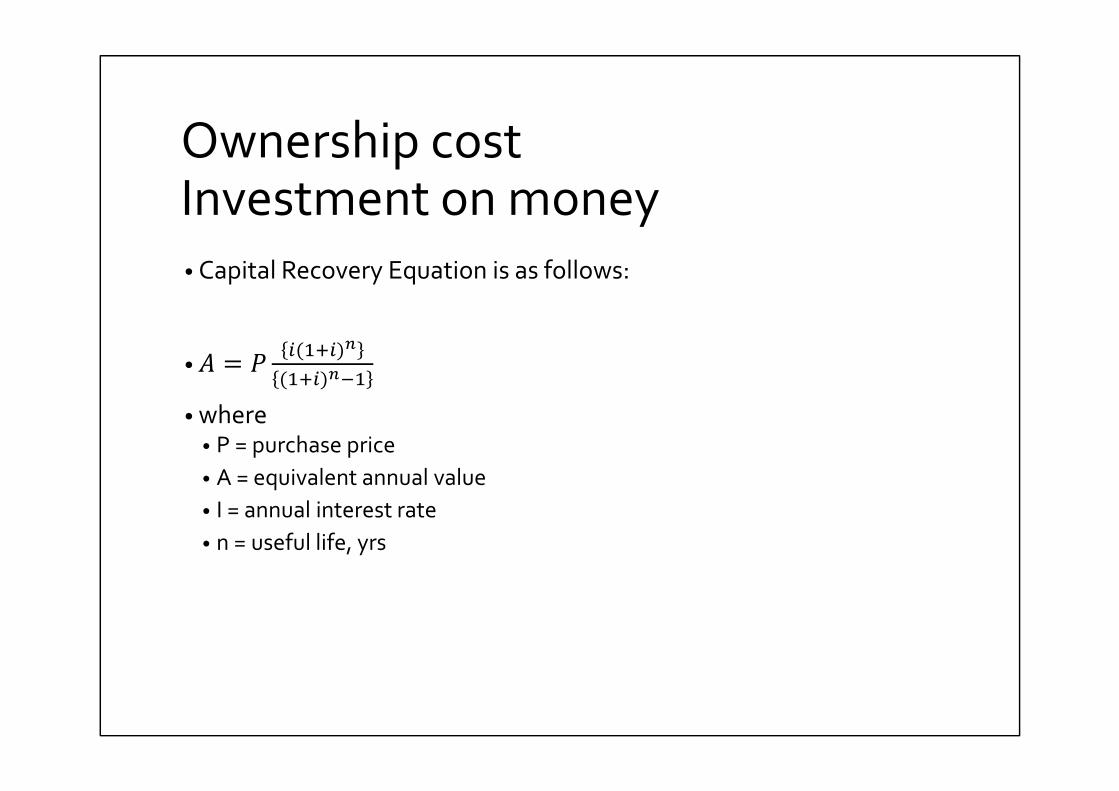

Ownership costInvestment on money

• Capital Recovery Equation is as follows:

•� = ��(���)

(���)�

• where • P = purchase price

• A = equivalent annual value

• I = annual interest rate

• n = useful life, yrs

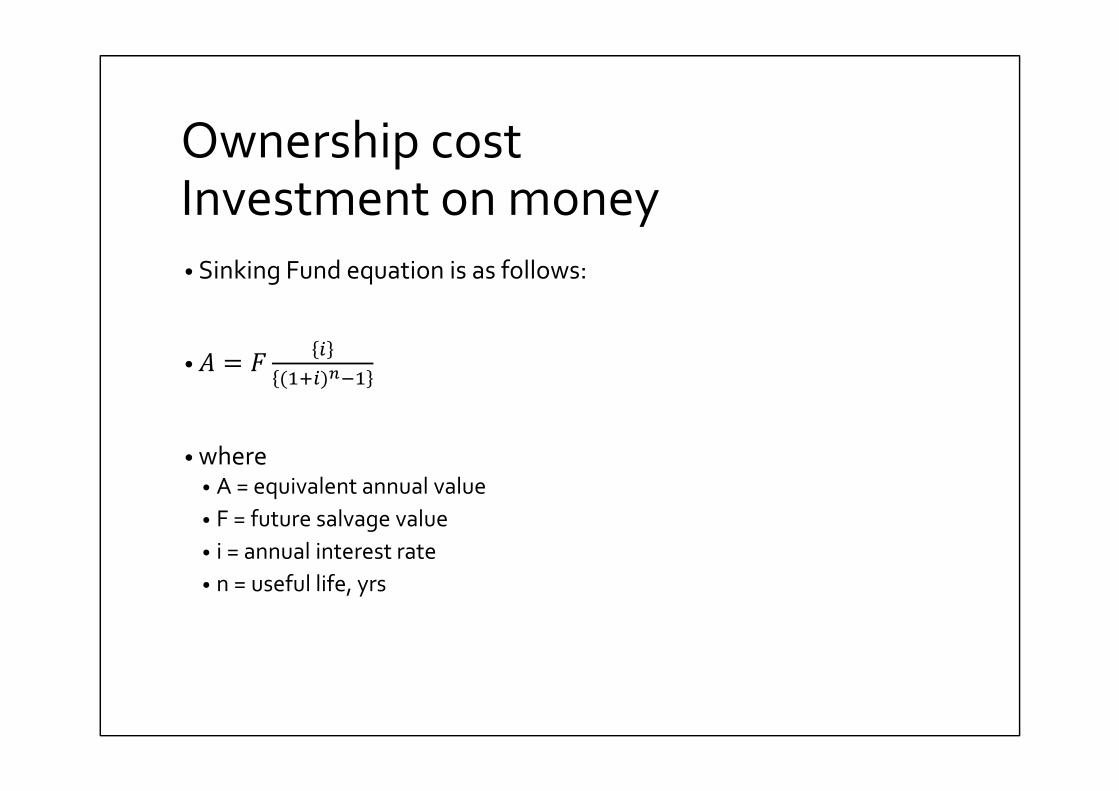

Ownership costInvestment on money

• Sinking Fund equation is as follows:

•� = ��

(���)�

• where • A = equivalent annual value

• F = future salvage value

• i = annual interest rate

• n = useful life, yrs

Ownership costInvestment on money

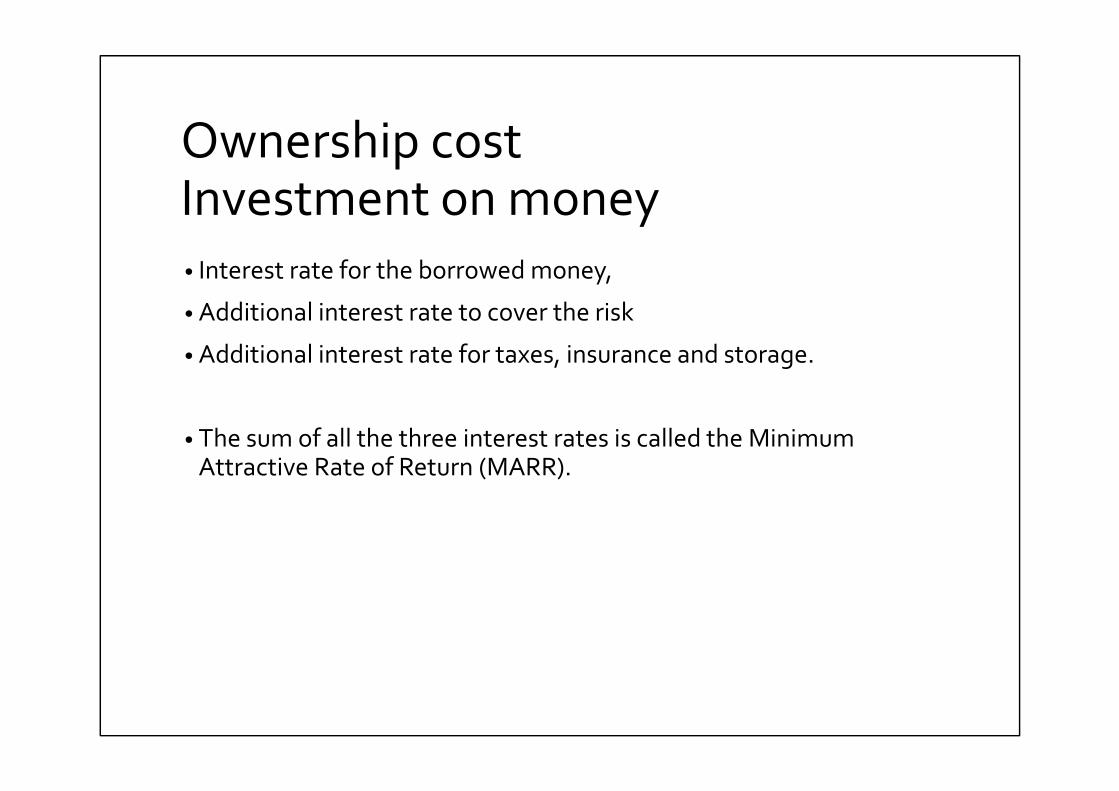

• Interest rate for the borrowed money,

• Additional interest rate to cover the risk

• Additional interest rate for taxes, insurance and storage.

• The sum of all the three interest rates is called the Minimum Attractive Rate of Return (MARR).

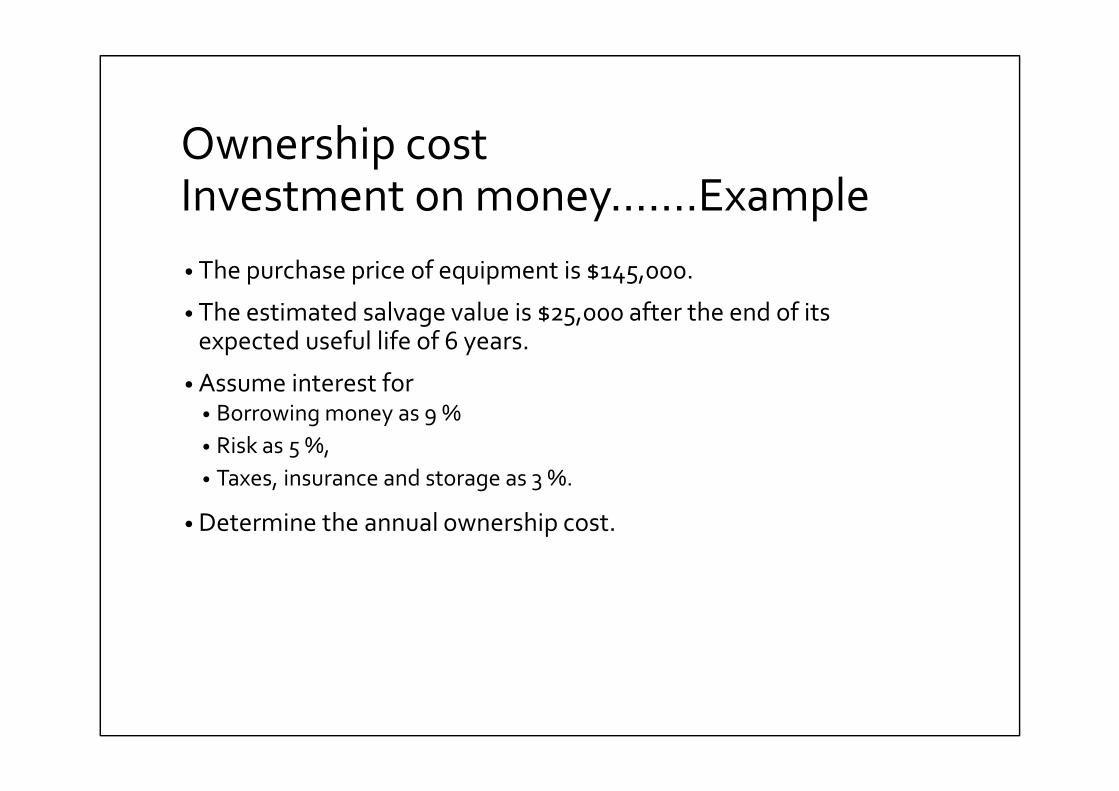

Ownership costInvestment on money…….Example

• The purchase price of equipment is $145,000.

• The estimated salvage value is $25,000 after the end of its expected useful life of 6 years.

• Assume interest for • Borrowing money as 9 %

• Risk as 5 %,

• Taxes, insurance and storage as 3 %.

• Determine the annual ownership cost.

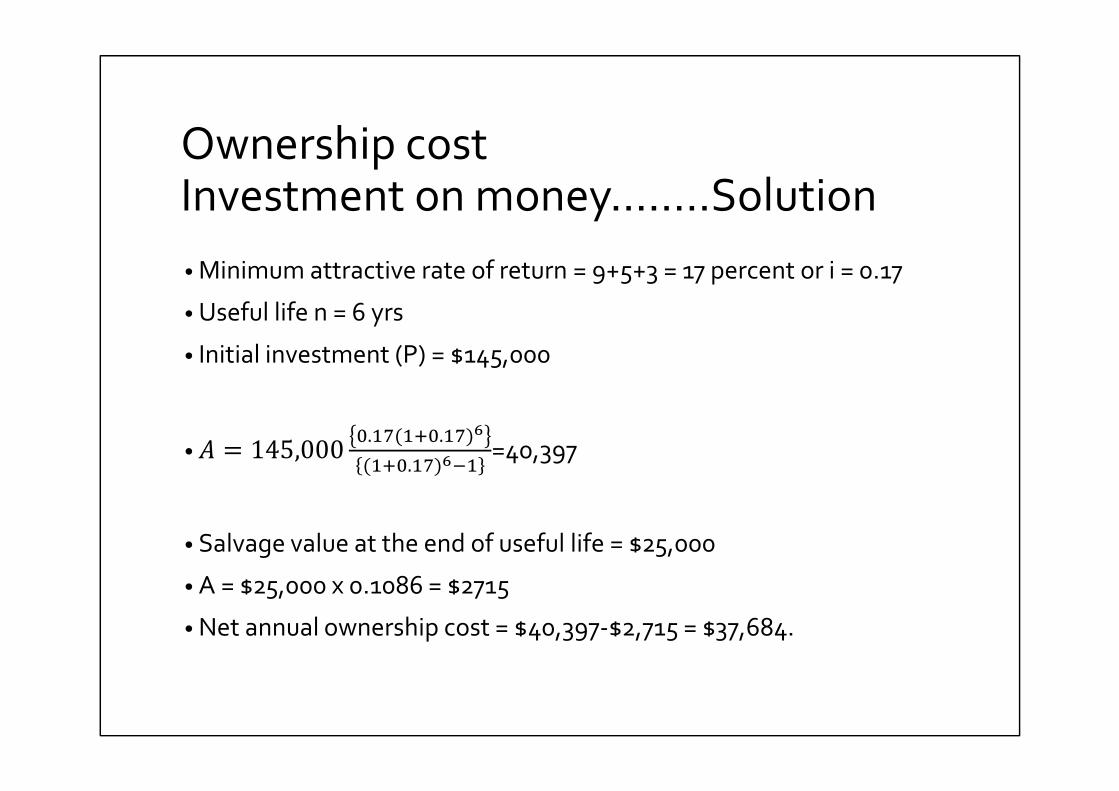

Ownership costInvestment on money……..Solution

• Minimum attractive rate of return = 9+5+3 = 17 percent or i = 0.17

• Useful life n = 6 yrs

• Initial investment (P) = $145,000

•� = 145,000�.��(���.��)�

(���.��)��=40,397

• Salvage value at the end of useful life = $25,000

• A = $25,000 x 0.1086 = $2715

• Net annual ownership cost = $40,397-$2,715 = $37,684.

Ownership cost

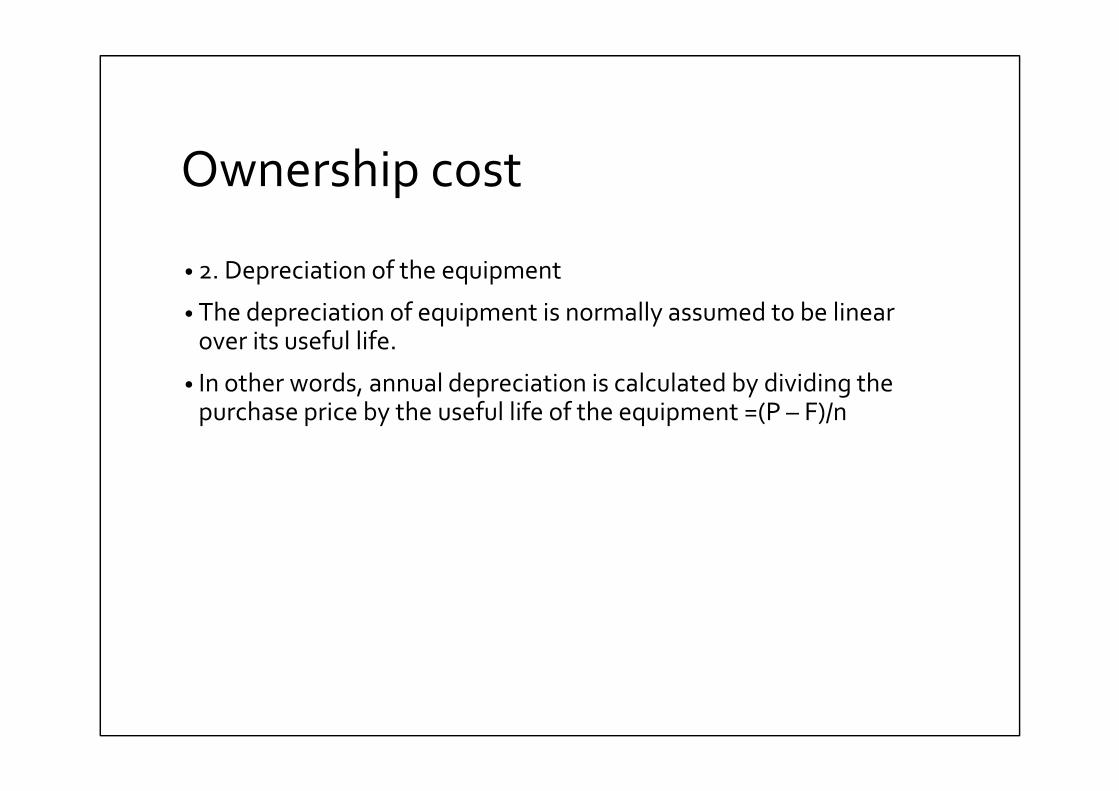

• 2. Depreciation of the equipment

• The depreciation of equipment is normally assumed to be linear over its useful life.

• In other words, annual depreciation is calculated by dividing the purchase price by the useful life of the equipment =(P – F)/n

Ownership cost

• 3. Taxes

• 4. Insurance

• 5. Storage when not used.

• For above items, an equivalent interest rate is added to the interest rate on the borrowed money.

Operating CostCost of fuel• Construction equipment require fuel for operating

• The fuel may be gasoline or diesel.

• The equipment is seldom used for 60 minutes in an hour.

• Most machines normally operate for 45 minutes in an hour.

• Moreover, the machine is not operated at its full capacity all the time.

• It may work at its full power only during heavy load conditions.

• At normal temperature and pressure;• Gasoline engine will consume approximately 0.06 gallons of fuel for each

actual horse- power developed.

• Diesel engine will consume approximately 0.04 gallons of fuel for each horse-power developed.

Operating CostCost of fuel………..Example

• A shovel is used in a digging operation.

• Its rated horse-power is 160.

• During an operating cycle of 20 seconds, the engine is operated at full power while filling the bucket in tough ground, requiring 5 seconds.

• During the balance of the cycle, the engine is operated at 50 percent of its rated power and the shovel is operated only for 45 minutes in an hour.

• Calculate the diesel required per hour.

Operating CostCost of fuel……….. Solution

• Engine factor:

• Filling the bucket: (5/20) x 100% = 0.250

• Rest of cycle: (15/20) x 50% = 0.375

• Engine factor = 0.625

• Time factor = 45/60 = 0.750

• Operating factor = 0.625 x 0.750 = 0.470

• Fuel required = 0.47 x 160 x 0.04 = 3.0 gallons/hour

Operating Cost Cost of lubricating oil

• The quantity of lubricating oil required by an engine will vary with the size of the engine, the capacity of the crankcase, the conditions of the pistons, and the number of hours between oil changes.

• The quantity of oil consumed can be estimated by means of the following equation:

• Q = {(hp x 0.6 x 0.006)/7.4} + c/t

• where • Q = quantity of oil required, gal/hr

• hp = rated horsepower of the engine

• c = capacity of crankcase, gal

• t = hrs between oil changes,

• 0.6 = operating factor

Operating Cost Cost of lubricating oil …….. Example

• A shovel fitted with a 100-hp motor is used in a digging operation.

• The capacity of crankcase is 4 gal and oil has to be changed every 100 hours of operation.

• Assuming an operating factor of 0.6, calculate the lubricating oil required for the engine.

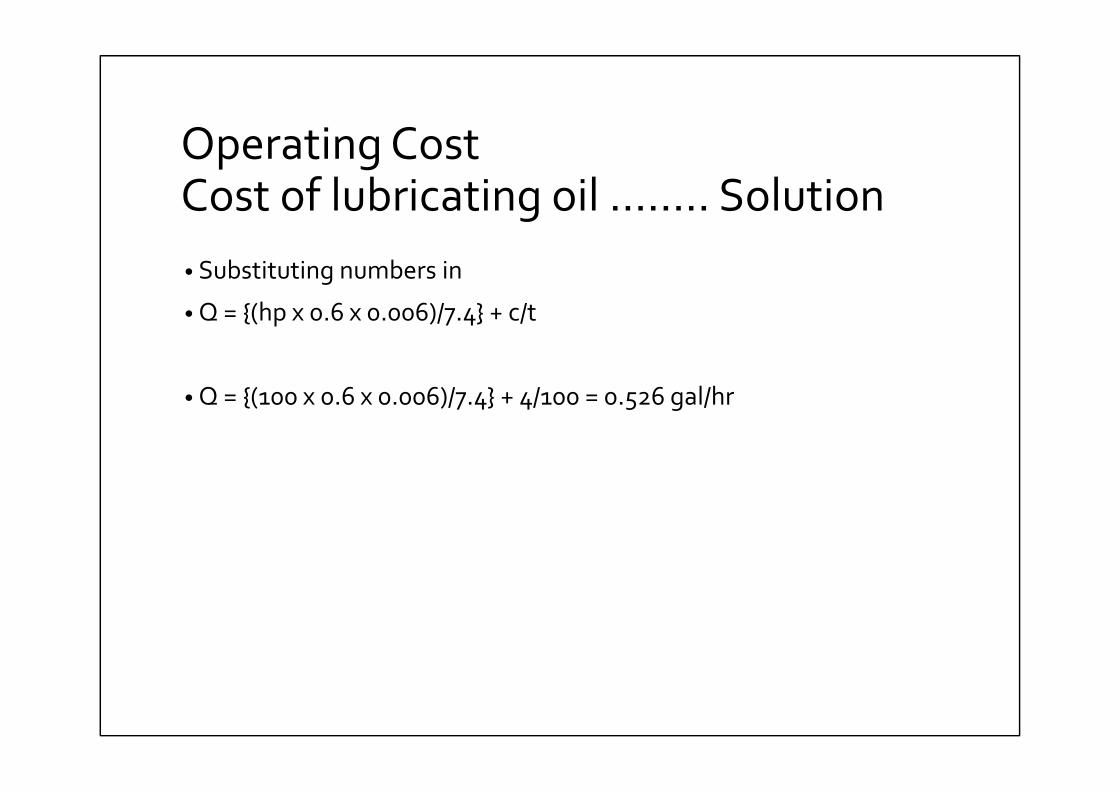

Operating Cost Cost of lubricating oil …….. Solution

• Substituting numbers in

• Q = {(hp x 0.6 x 0.006)/7.4} + c/t

• Q = {(100 x 0.6 x 0.006)/7.4} + 4/100 = 0.526 gal/hr

Operating Cost Cost of maintenance and repairs

• The annual cost of maintenance and repairs is often expressed as a percentage of the purchase price or as a percentage of the straight-line depreciation costs (P – F)/n

HANDLING & TRANSPORTING MATERIAL• Construction materials have to be transported from the storage

yard of the material supplier to the job site and from the stockpiles on the jobsite to the location where the material will be permanently installed.

• This involves a cost that must be included in the estimate for the project.

• The time required by a truck for transport of materials is divided into the following four elements:

• 1. Load.

• 2. Haul, loaded.

• 3. Unload.

• 4. Return, empty.

Cycle Time for Transporting Material

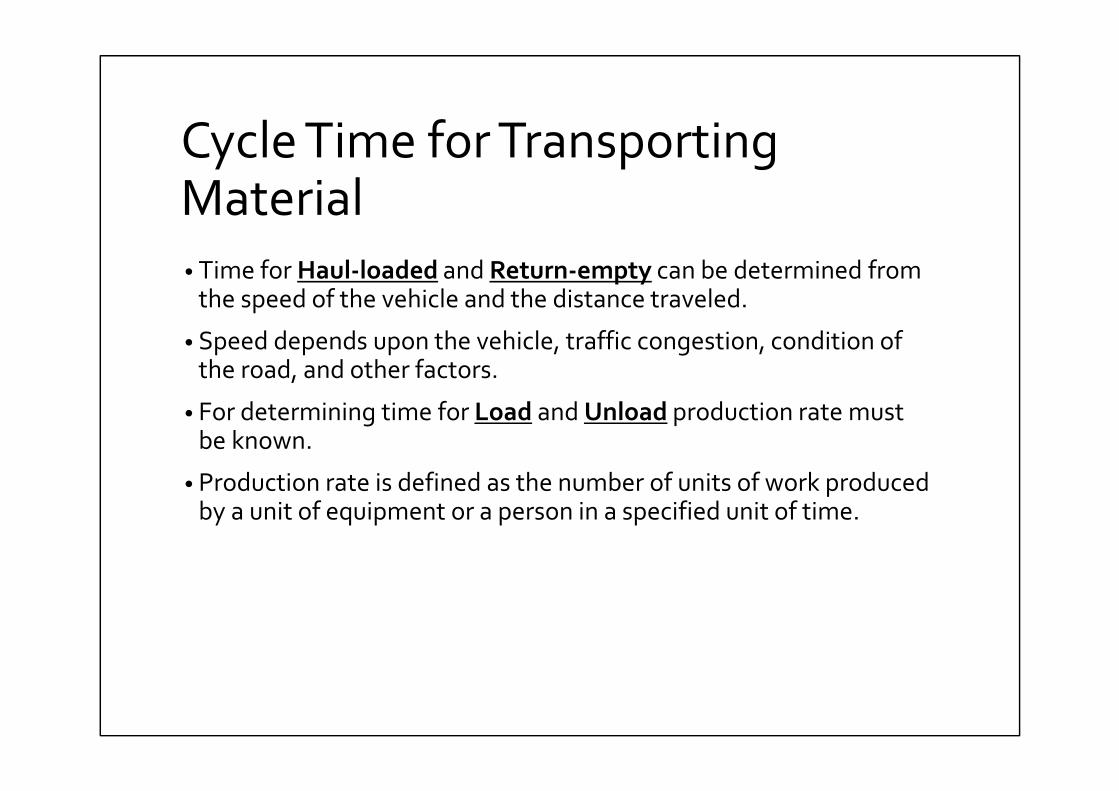

• Time for Haul‐loaded and Return‐empty can be determined from the speed of the vehicle and the distance traveled.

• Speed depends upon the vehicle, traffic congestion, condition of the road, and other factors.

• For determining time for Load and Unload production rate must be known.

• Production rate is defined as the number of units of work produced by a unit of equipment or a person in a specified unit of time.

Cycle Time for Transporting Material

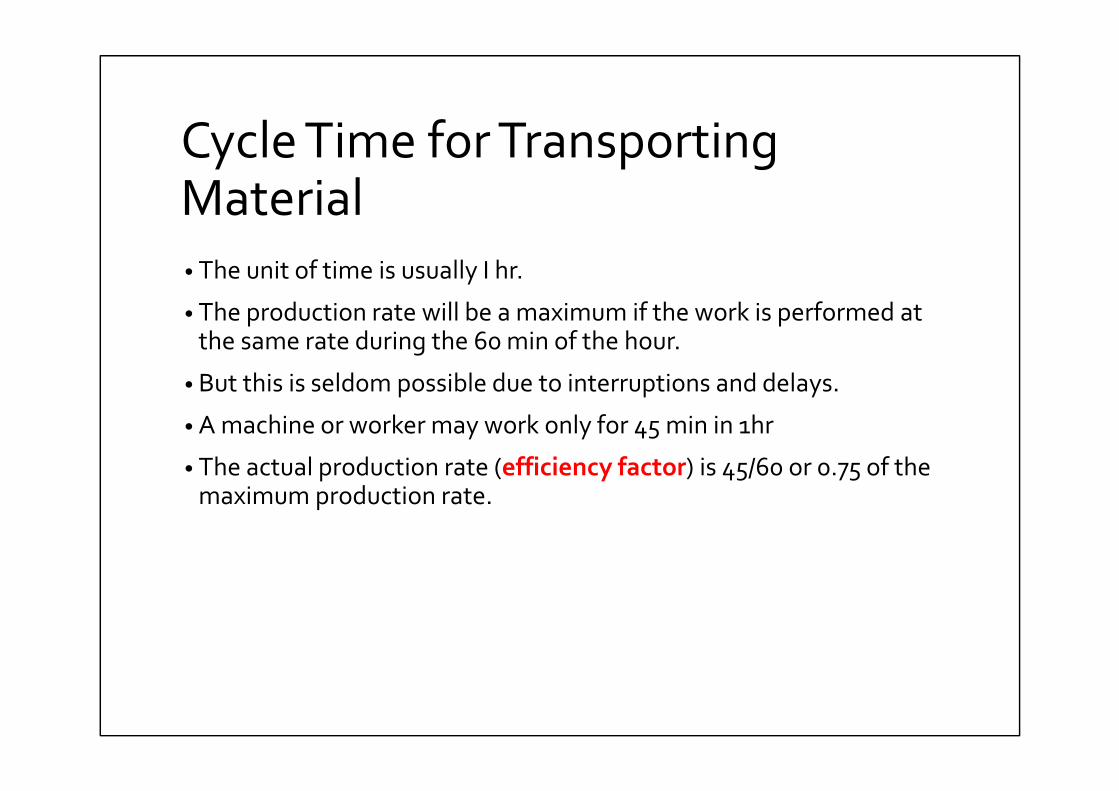

• The unit of time is usually I hr.

• The production rate will be a maximum if the work is performed at the same rate during the 60 min of the hour.

• But this is seldom possible due to interruptions and delays.

• A machine or worker may work only for 45 min in 1hr

• The actual production rate (efficiency factor) is 45/60 or 0.75 of the maximum production rate.

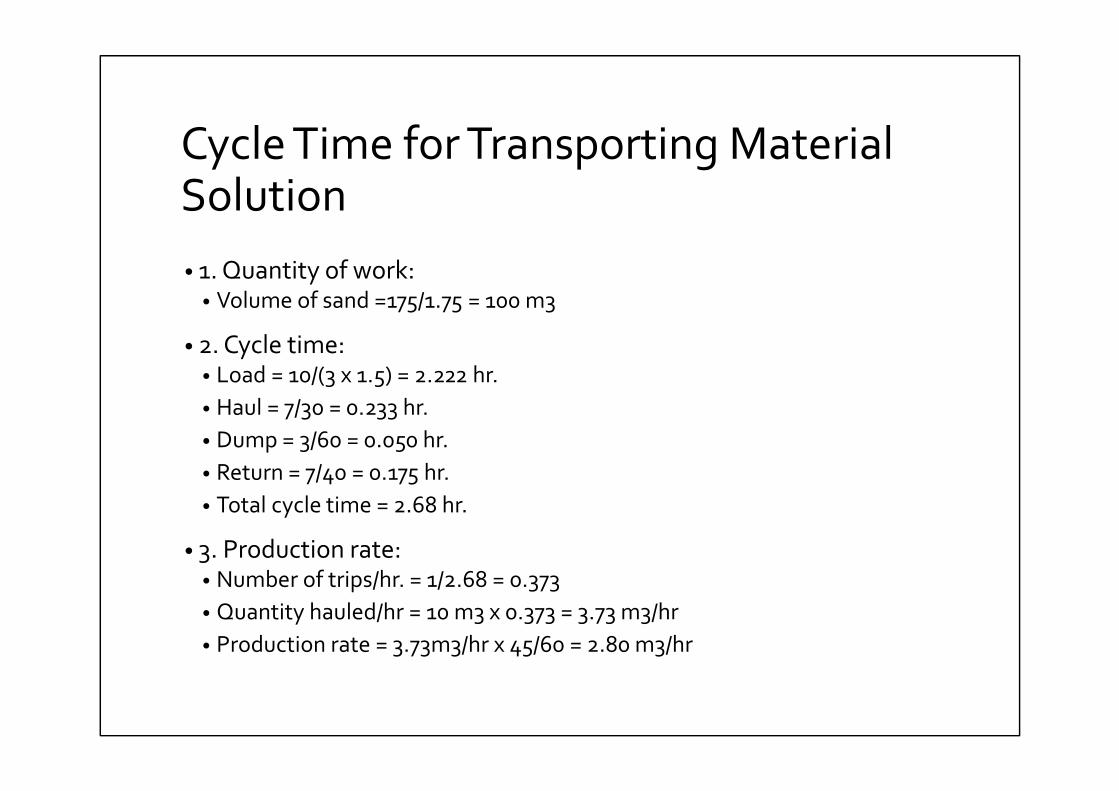

Cycle Time for Transporting MaterialExample 1

• 175 tons of sand with a density of 1.75 ton/m3 must be transported 7 km using a 10m3 dump truck.

• Two laborers and a driver each will load the truck at a rate of 1.5 m3/hr.

• The haul speed is 30 km/h and return speed is 40 km/h.

• It takes 3 min to unload the truck.

• The cost of the truck is $25/hr, the driver is $18/hr, and the laborer is $15/hr.

• Determine the total time, total cost, and the cost/unit of transporting the sand if the actual working time is 45 min in one hr.

Cycle Time for Transporting MaterialSolution

• 1. Quantity of work:• Volume of sand =175/1.75 = 100 m3

• 2. Cycle time:• Load = 10/(3 x 1.5) = 2.222 hr.

• Haul = 7/30 = 0.233 hr.

• Dump = 3/60 = 0.050 hr.

• Return = 7/40 = 0.175 hr.

• Total cycle time = 2.68 hr.

• 3. Production rate:• Number of trips/hr. = 1/2.68 = 0.373

• Quantity hauled/hr = 10 m3 x 0.373 = 3.73 m3/hr

• Production rate = 3.73m3/hr x 45/60 = 2.80 m3/hr

Cycle Time for Transporting MaterialSolution

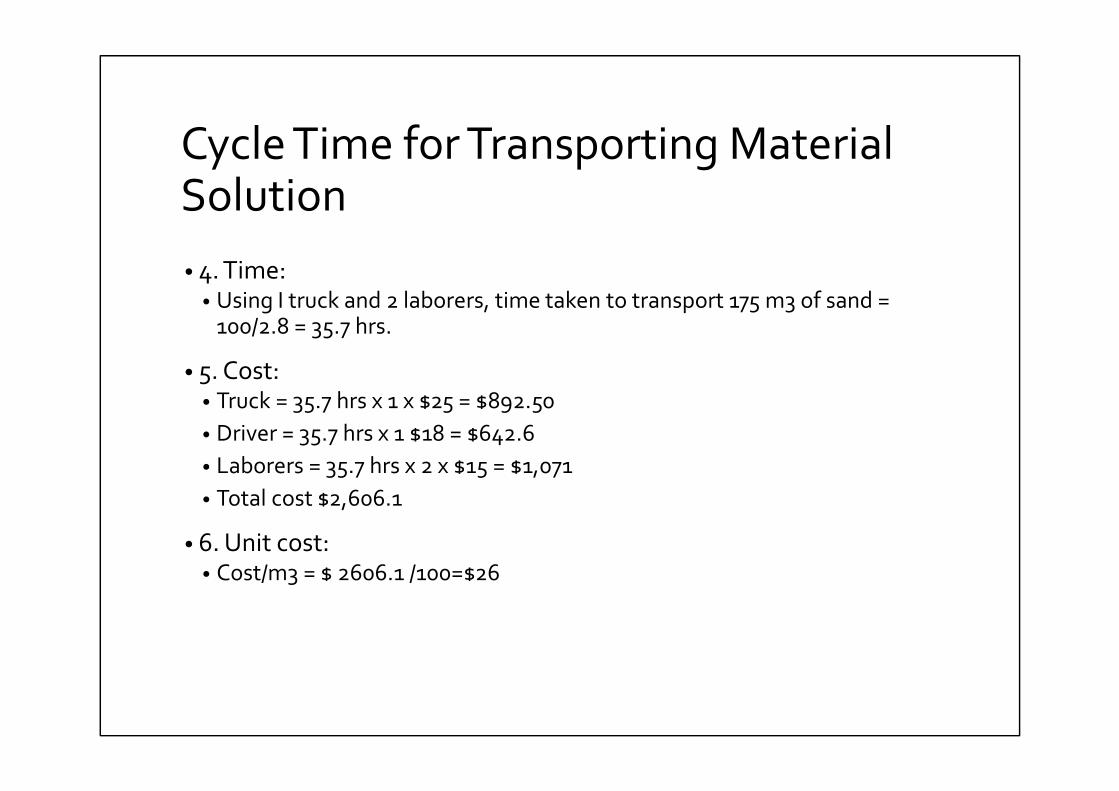

• 4. Time:• Using I truck and 2 laborers, time taken to transport 175 m3 of sand =

100/2.8 = 35.7 hrs.

• 5. Cost:• Truck = 35.7 hrs x 1 x $25 = $892.50

• Driver = 35.7 hrs x 1 $18 = $642.6

• Laborers = 35.7 hrs x 2 x $15 = $1,071

• Total cost $2,606.1

• 6. Unit cost:• Cost/m3 = $ 2606.1 /100=$26

Cycle Time for Transporting MaterialSolution

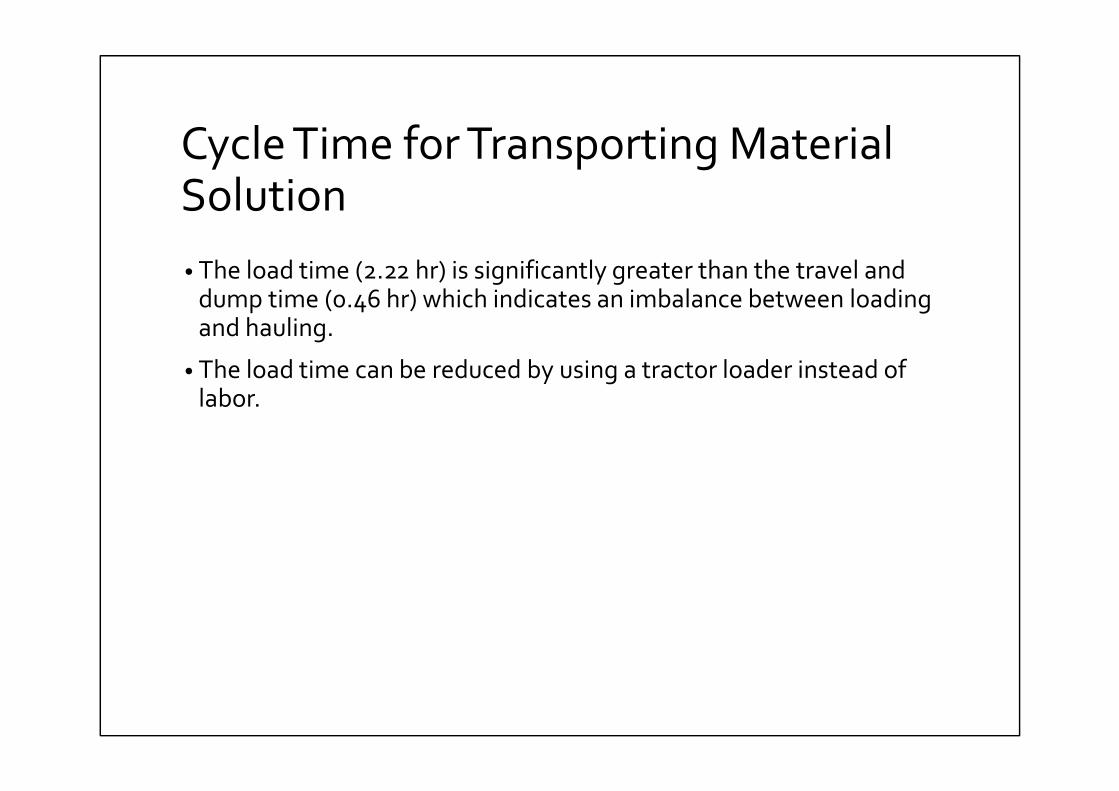

• The load time (2.22 hr) is significantly greater than the travel and dump time (0.46 hr) which indicates an imbalance between loading and hauling.

• The load time can be reduced by using a tractor loader instead of labor.

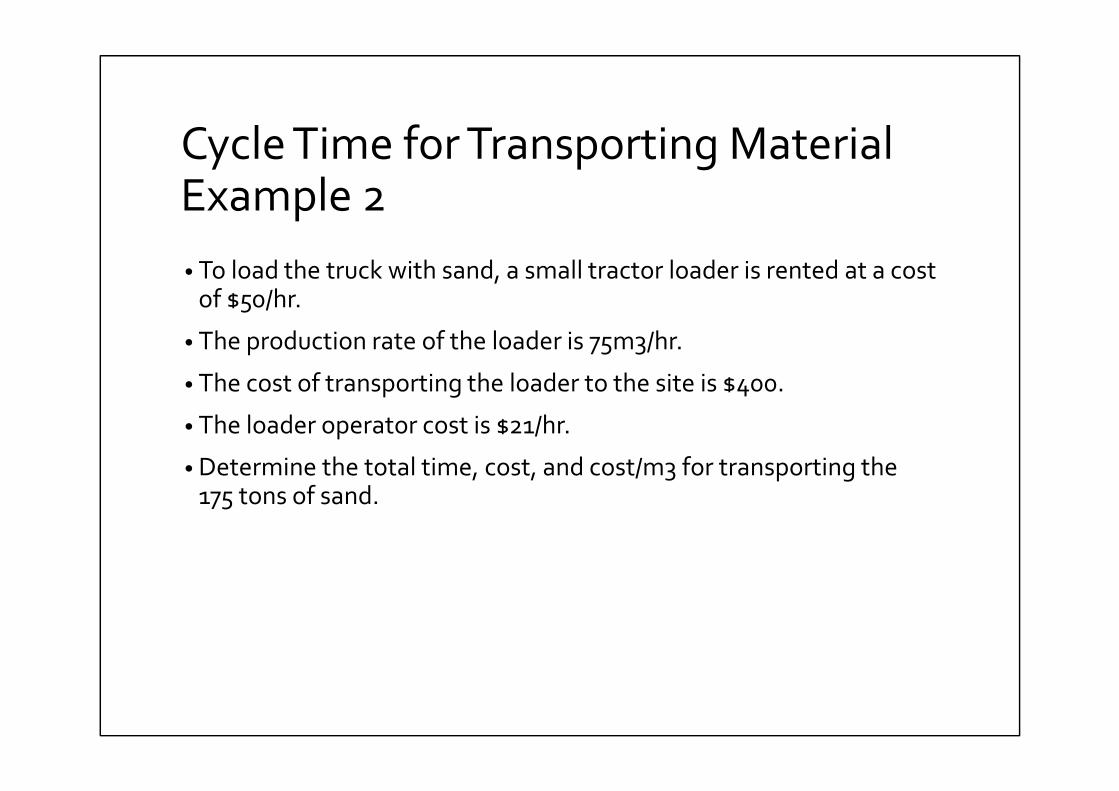

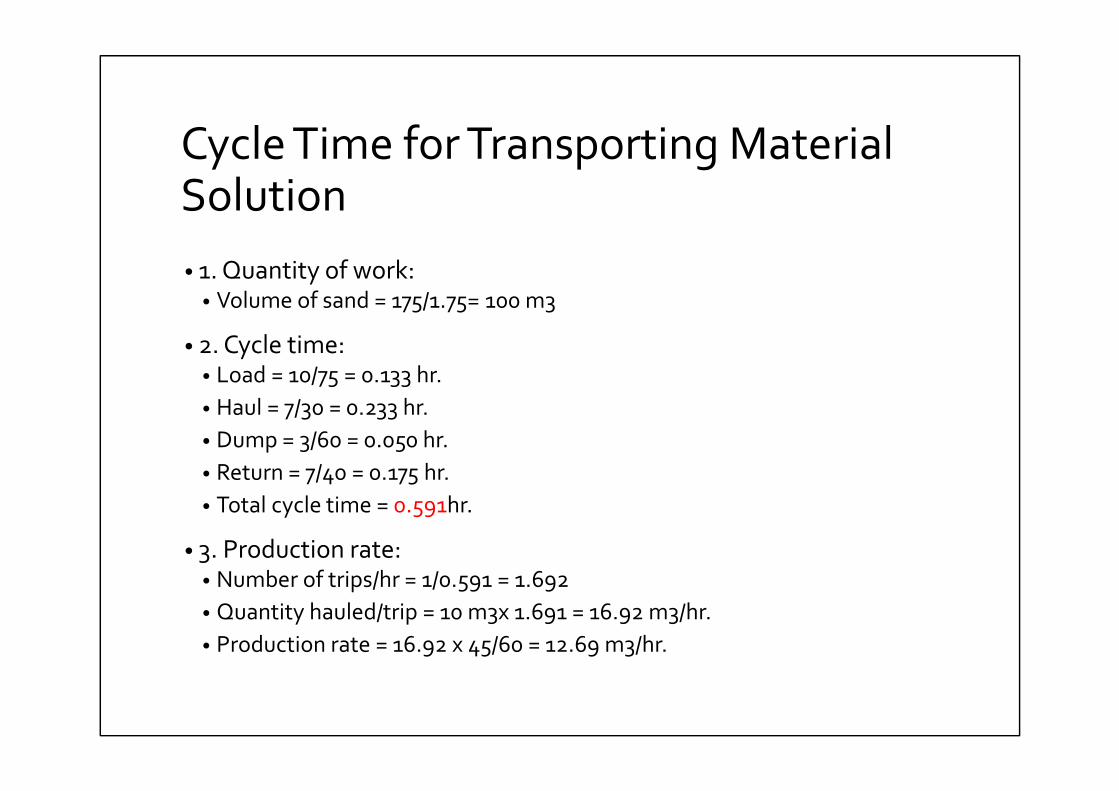

Cycle Time for Transporting MaterialExample 2

• To load the truck with sand, a small tractor loader is rented at a cost of $50/hr.

• The production rate of the loader is 75m3/hr.

• The cost of transporting the loader to the site is $400.

• The loader operator cost is $21/hr.

• Determine the total time, cost, and cost/m3 for transporting the 175 tons of sand.

Cycle Time for Transporting MaterialSolution

• 1. Quantity of work:• Volume of sand = 175/1.75= 100 m3

• 2. Cycle time:• Load = 10/75 = 0.133 hr.

• Haul = 7/30 = 0.233 hr.

• Dump = 3/60 = 0.050 hr.

• Return = 7/40 = 0.175 hr.

• Total cycle time = 0.591hr.

• 3. Production rate:• Number of trips/hr = 1/0.591 = 1.692

• Quantity hauled/trip = 10 m3x 1.691 = 16.92 m3/hr.

• Production rate = 16.92 x 45/60 = 12.69 m3/hr.

Cycle Time for Transporting MaterialSolution

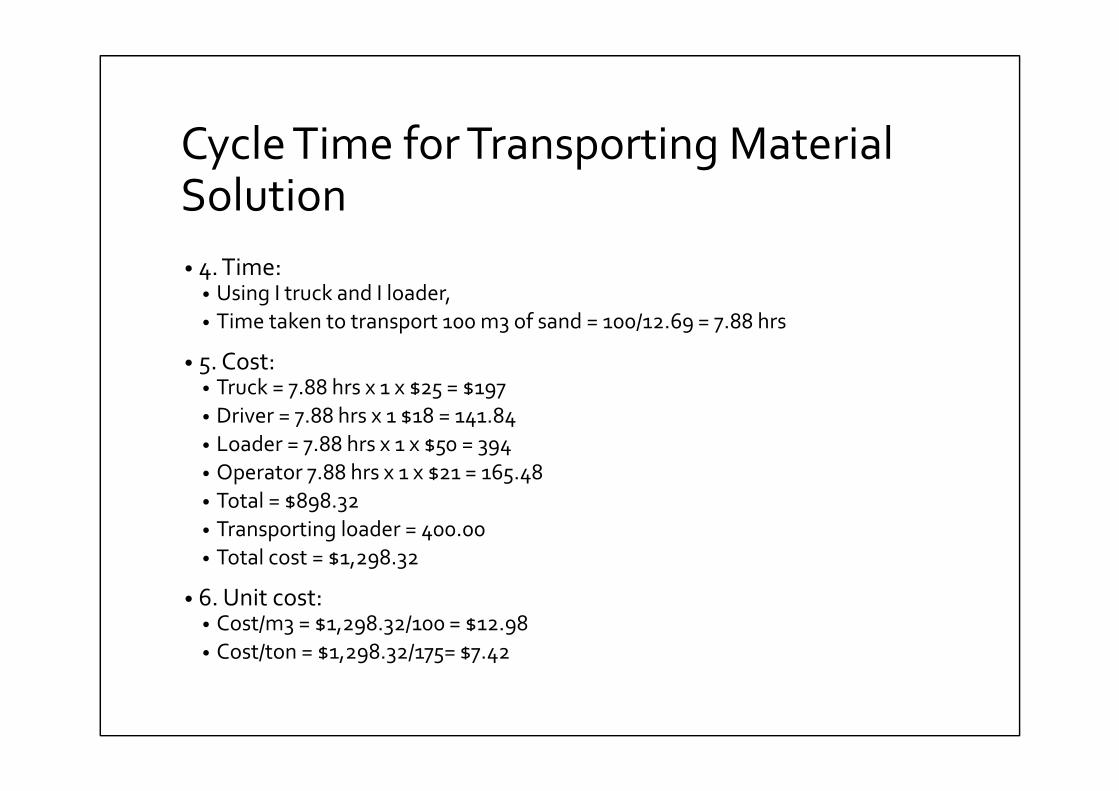

• 4. Time:• Using I truck and I loader,

• Time taken to transport 100 m3 of sand = 100/12.69 = 7.88 hrs

• 5. Cost:• Truck = 7.88 hrs x 1 x $25 = $197

• Driver = 7.88 hrs x 1 $18 = 141.84

• Loader = 7.88 hrs x 1 x $50 = 394

• Operator 7.88 hrs x 1 x $21 = 165.48

• Total = $898.32

• Transporting loader = 400.00

• Total cost = $1,298.32

• 6. Unit cost:• Cost/m3 = $1,298.32/100 = $12.98

• Cost/ton = $1,298.32/175= $7.42

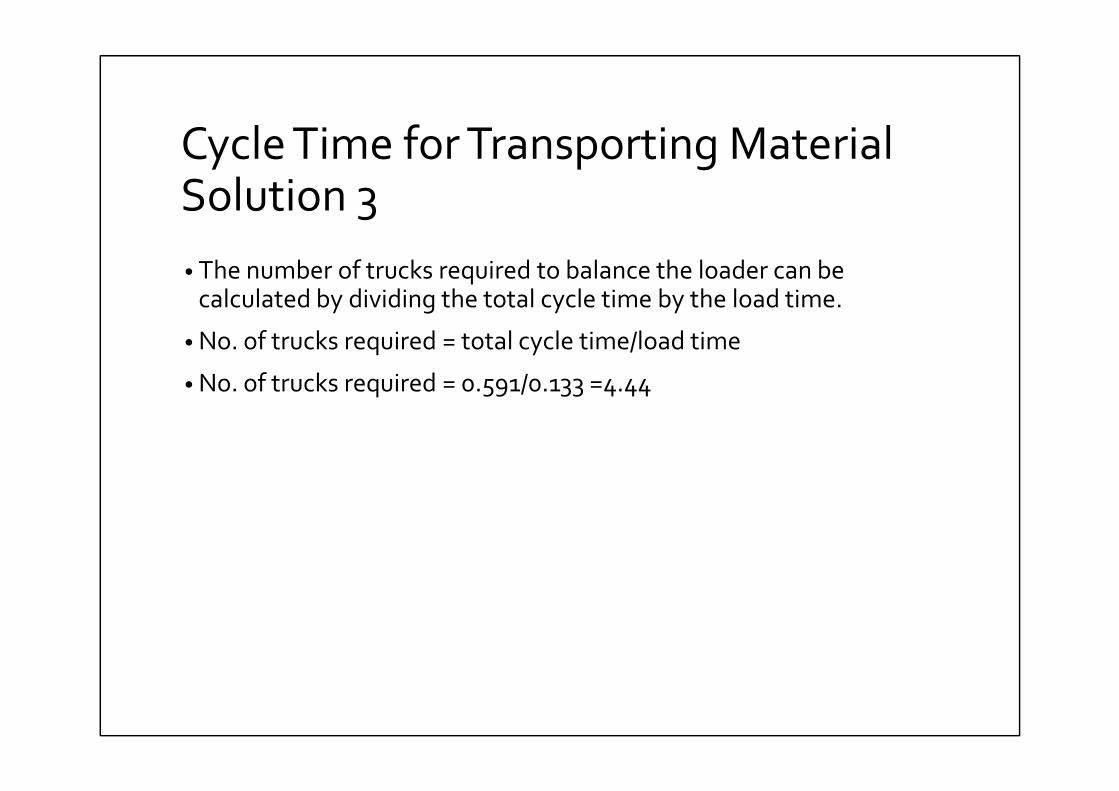

Cycle Time for Transporting MaterialExample 3

• Using the data in Example 2, determine the economical number of trucks such that the load time and transport time balance.

• Also determine the cost/unit for transporting the material.

Cycle Time for Transporting MaterialSolution 3

• The number of trucks required to balance the loader can be calculated by dividing the total cycle time by the load time.

• No. of trucks required = total cycle time/load time

• No. of trucks required = 0.591/0.133 =4.44

Cycle Time for Transporting MaterialSolution 3 - Alternative 1

• Using 4 trucks, there are fewer trucks than needed and hence the production rate is governed by the truck production rate.

• Quantity hauled by one truck = 16.92 m3/hr

• Quantity hauled by 4 trucks = 4 x 16.92 = 67.68 m3/hr

• Time to transport 100 m3 of sand = 100/67.68 = 1.48 hrs

• Cost: • Loader = 1.48 hrs x$ 50 = $74.00• Loader operator = 1.48 hrs x $21 = 30.08• Trucks = 1.48 hrs x 4 x $25 = 148.00• Truck drivers = 1.48 hrs x 4 x $18 = 106.56• Total labor and equipment = 358.64• Transporting loader = 400.00• Total cost = $758.64

• Cost/m3 = $758.64/100 = $7.59

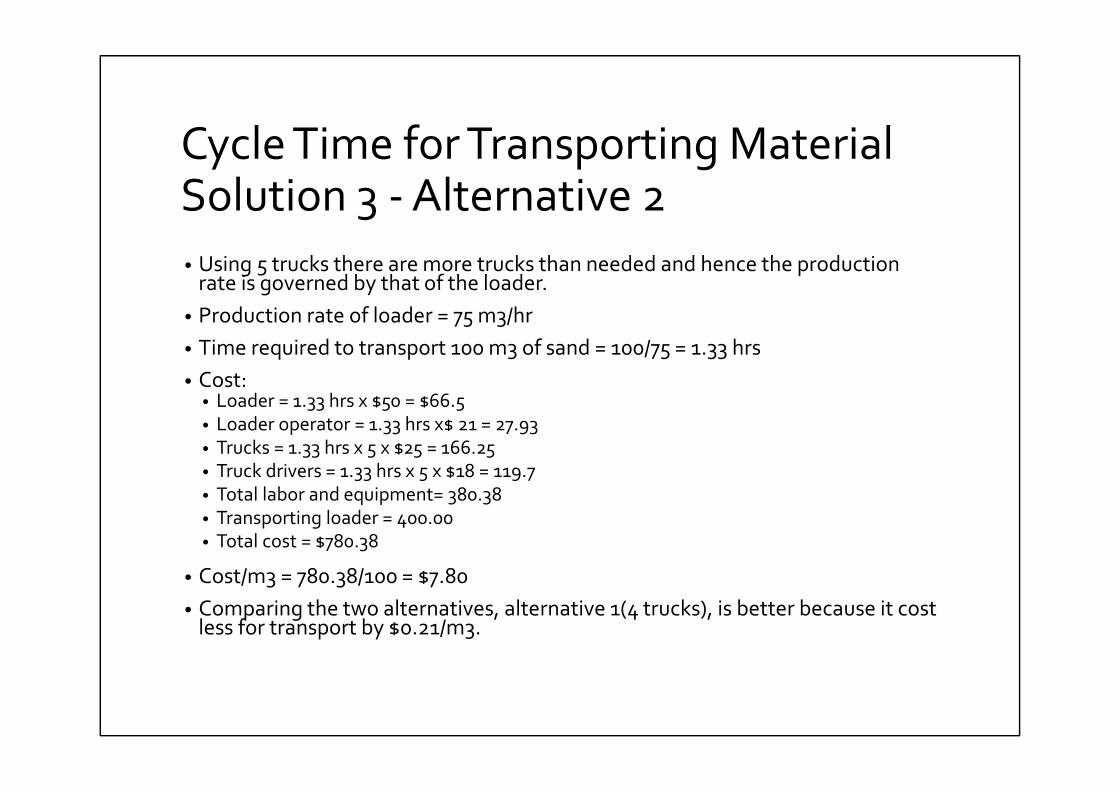

Cycle Time for Transporting MaterialSolution 3 - Alternative 2

• Using 5 trucks there are more trucks than needed and hence the production rate is governed by that of the loader.

• Production rate of loader = 75 m3/hr

• Time required to transport 100 m3 of sand = 100/75 = 1.33 hrs

• Cost: • Loader = 1.33 hrs x $50 = $66.5• Loader operator = 1.33 hrs x$ 21 = 27.93• Trucks = 1.33 hrs x 5 x $25 = 166.25• Truck drivers = 1.33 hrs x 5 x $18 = 119.7• Total labor and equipment= 380.38• Transporting loader = 400.00• Total cost = $780.38

• Cost/m3 = 780.38/100 = $7.80

• Comparing the two alternatives, alternative 1(4 trucks), is better because it cost less for transport by $0.21/m3.

THANKS