ernesto ochoa director, marketing - tennessee gas pipeline

TRANSCRIPT

The Big Picture

Dramatic supply growth continues

Marcellus, Utica, Permian, Eagle Ford….. Unconventional = the “new” conventional?

Gas demand continues growth trajectory US economy : power gen residential / industrial Exports : LNG; Mexico

Infrastructure impetus New sources new plumbing supply to market Mexico Energy Reform

2

3

U.S. becomes net exporter Industrial demand growth

Less Canadian Exports to U.S. More U.S. Exports to Mexico Continued supply increases

Gas-fired generation increases

Source: ICF International and Kinder Morgan Analysis

+9.6 Bcfd Res +1.9 Bcfd

+20.1 Bcfd +1.5 Bcfd -2.0 Bcfd

+7.7 Bcfd Ind +3.1 Bcfd

Current Key Trends

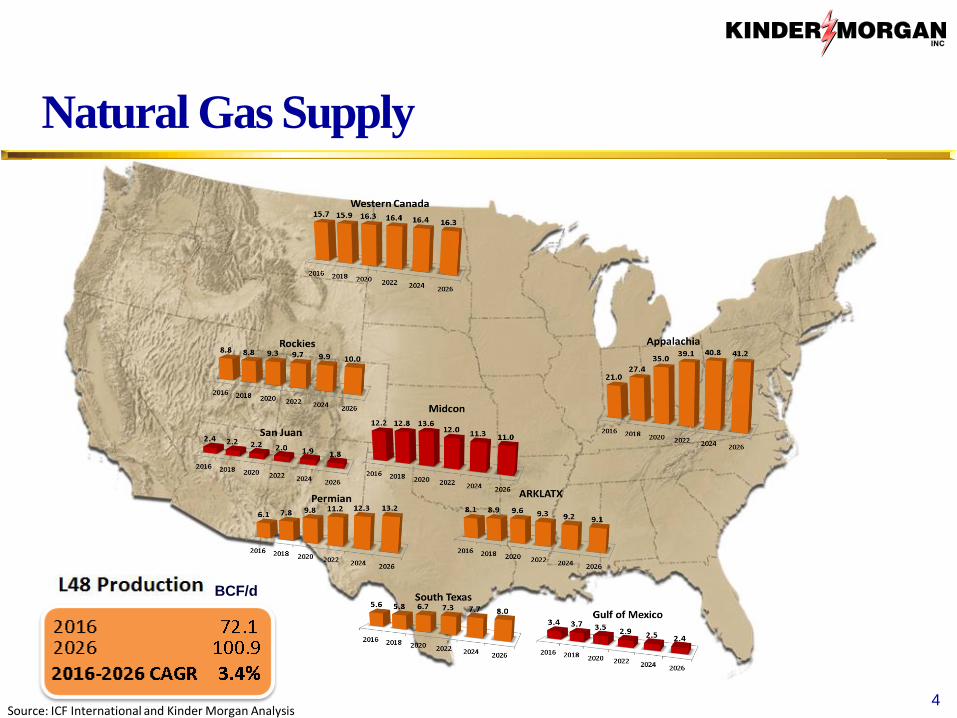

Natural Gas Supply

4

BCF/d

Source: ICF International and Kinder Morgan Analysis

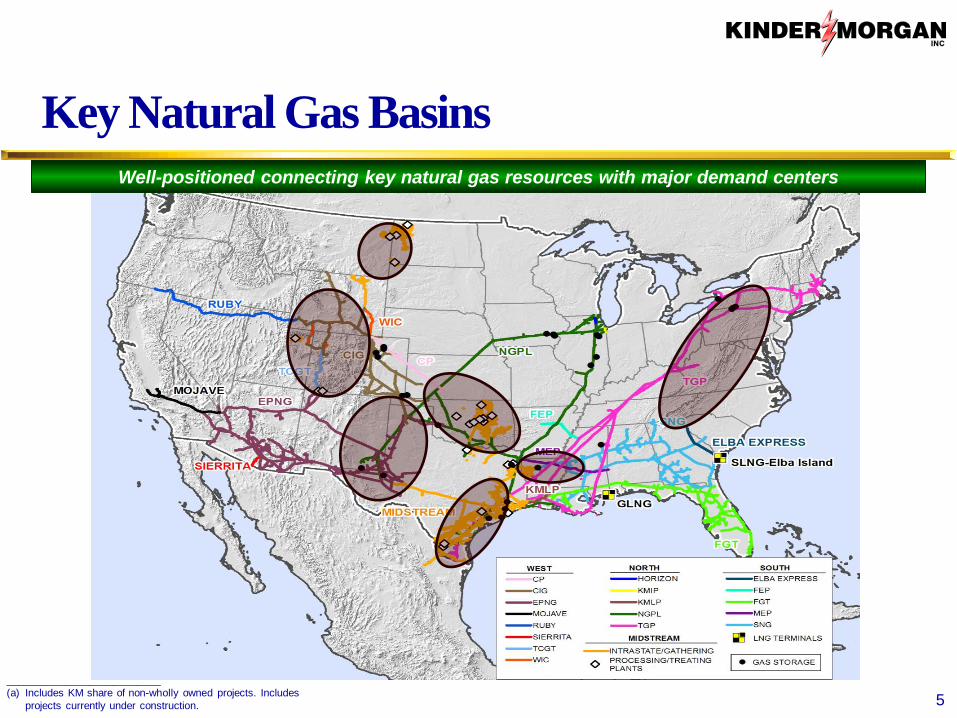

Key Natural Gas Basins

Well-positioned connecting key natural gas resources with major demand centers

__________________________

(a) Includes KM share of non-wholly owned projects. Includes

projects currently under construction. 5

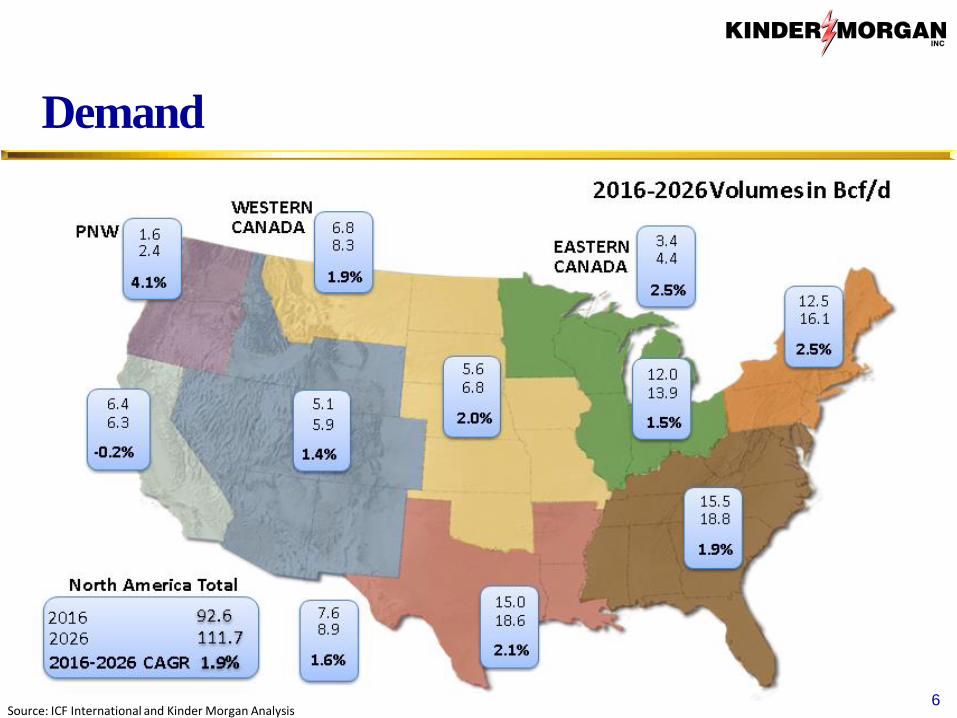

Demand

6 Source: ICF International and Kinder Morgan Analysis

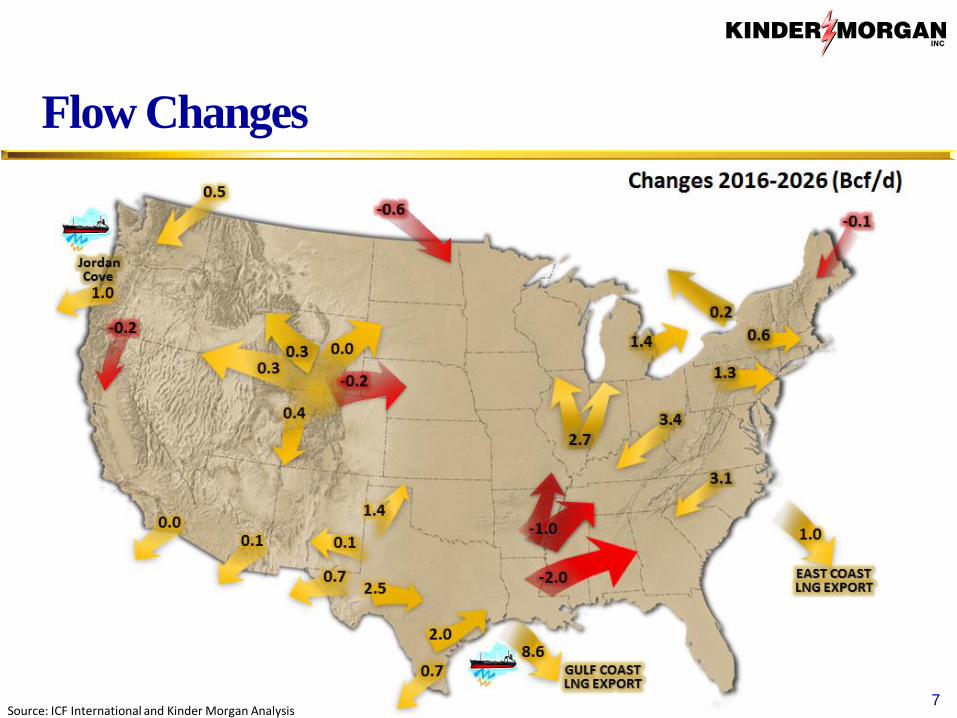

Flow Changes

7 Source: ICF International and Kinder Morgan Analysis

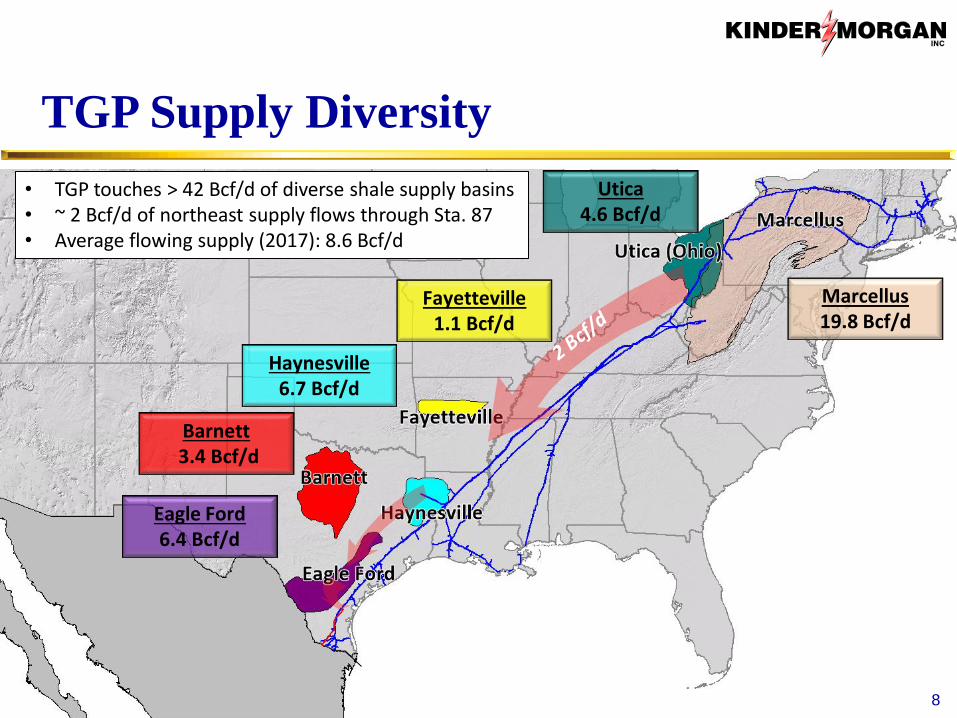

TGP Supply Diversity

8

Marcellus 19.8 Bcf/d

Haynesville 6.7 Bcf/d

Eagle Ford 6.4 Bcf/d

Fayetteville 1.1 Bcf/d

Utica 4.6 Bcf/d

Barnett 3.4 Bcf/d

• TGP touches > 42 Bcf/d of diverse shale supply basins • ~ 2 Bcf/d of northeast supply flows through Sta. 87 • Average flowing supply (2017): 8.6 Bcf/d

Changing TGP Operations

• Designed to deliver TX/LA supply rate-able to Northeast markets

• High utilization of 100 line, high seasonal utilization of 200 and 300 lines

• Consistent imports on the Niagara Spur • Maintenance typically performed in summer

months May – Oct

2007 2017

• Marcellus receipts > 3.4 Bcf/d serving Northeast markets, new power generation with record power burn

• Lower utilization of 100 line long-haul, high utilization of 200 & 300 lines, 300 line westbound from Station 315

• Consistent exports on Niagara Spur & to Mexico • Maintenance performed whenever possible due to power

plant load and Marcellus supply

100 Line

800 Line

500 Line

200 Line

300 Line 300 Line

100 Line 500 Line

800 Line

200 Line

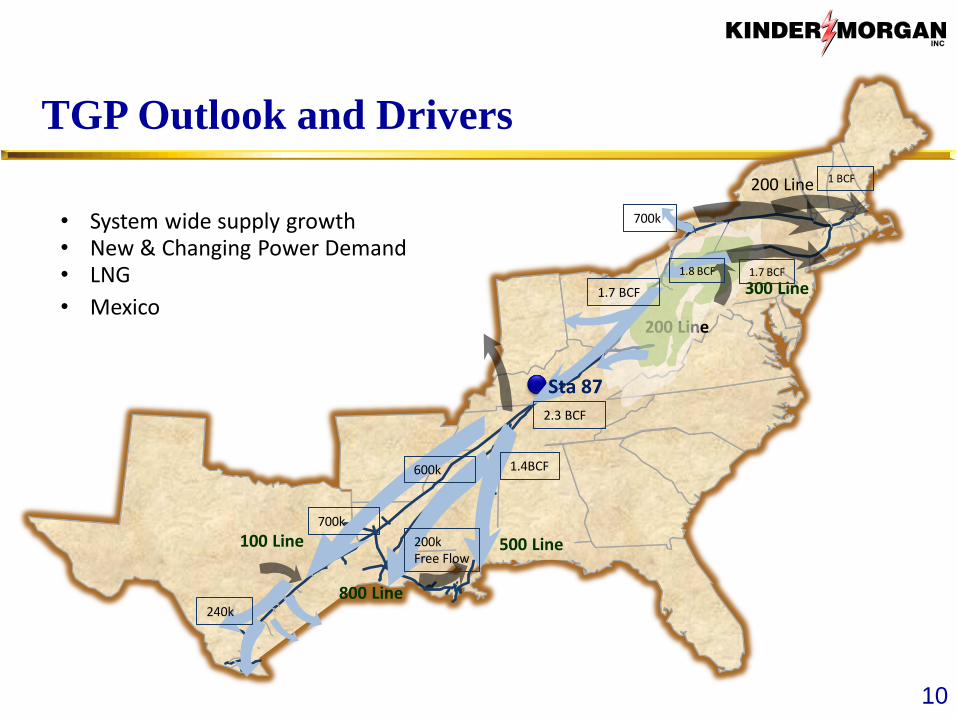

TGP Outlook and Drivers

10

500 Line

200 Line

300 Line

100 Line

200 Line

800 Line

• System wide supply growth • New & Changing Power Demand • LNG

• Mexico

1.4BCF

200k Free Flow

2.3 BCF

700k

1.7 BCF

700k

240k

1.8 BCF 1.7 BCF

1 BCF

600k

Sta 87

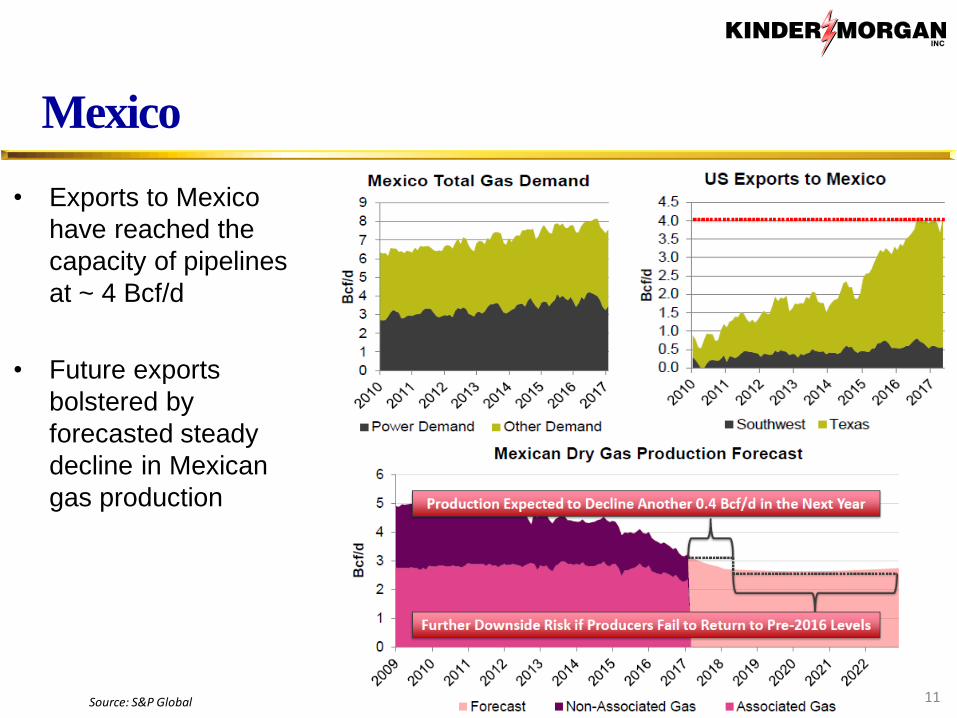

Mexico

11

• Exports to Mexico

have reached the

capacity of pipelines

at ~ 4 Bcf/d

• Future exports

bolstered by

forecasted steady

decline in Mexican

gas production

Source: S&P Global

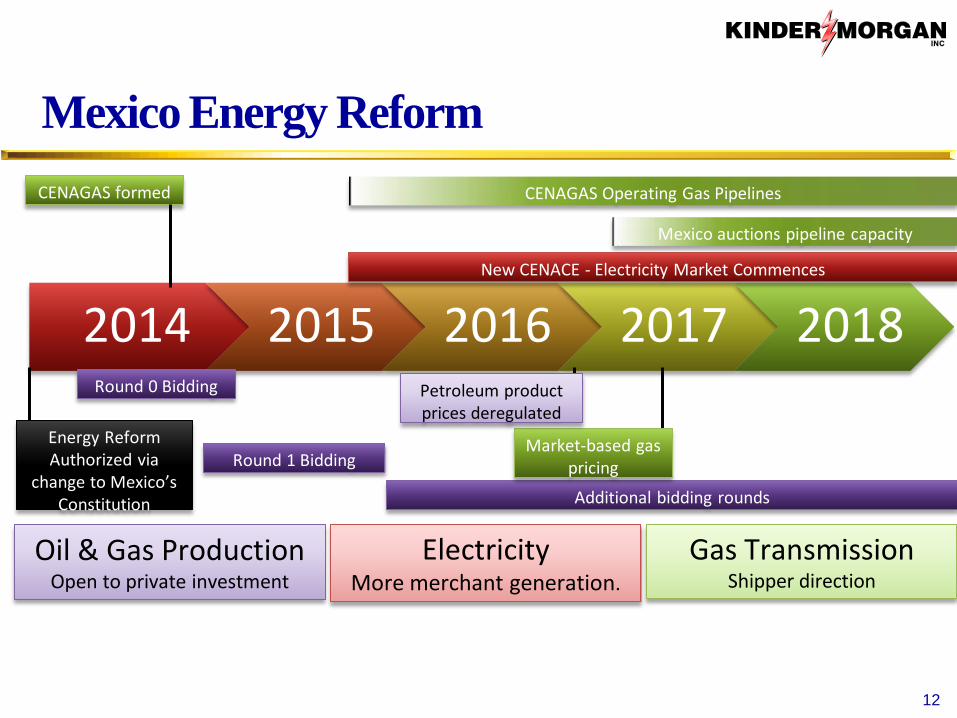

Mexico Energy Reform

12

Oil & Gas Production Open to private investment

Electricity More merchant generation.

Gas Transmission Shipper direction

2014 2015 2016 2017 2018 New CENACE - Electricity Market Commences

CENAGAS formed

Round 0 Bidding

Round 1 Bidding

Additional bidding rounds

CENAGAS Operating Gas Pipelines

Energy Reform Authorized via

change to Mexico’s Constitution

Market-based gas pricing

Petroleum product prices deregulated

Mexico auctions pipeline capacity

Thank You