equity analyst india equity analyst bhaskar basu, cfa ... · india equity strategy challenges...

TRANSCRIPT

India | Equity Strategy

India 21 November 2016

India Equity StrategyChallenges Beyond Cash Crunch

EQU

ITY STRATEG

Y IND

IAGovindarajan Chellappa *Equity Analyst

+91 22 4224 6111 [email protected] Jasani §

Equity Analyst+65 6551 3962 [email protected]

Piyush Nahar *Equity Analyst

+91 22 4224 6113 [email protected] Karfa *

Equity Analyst+91 22 4224 6118 [email protected]

Bhaskar Basu, CFA *Equity Analyst

+91 22 4224 6130 [email protected] Mathur *

Equity Analyst+91 22 4224 6115 [email protected]

Avinash Singh, CFA *Equity Associate

+91 22 4224 6183 [email protected] Sen *

Equity Analyst+91 22 4224 6122 [email protected]

Vaibhav Dhasmana *Equity Analyst

+91 22 4224 6126 [email protected] Quadros *

Equity Analyst+91 22 4224 6116 [email protected]

Ankit Fitkariwala *Equity Analyst

+91 22 4224 6125 [email protected] Venkatesan *

Equity Associate+91 22 4224 6123 [email protected]

Ranjeet Jaiswal *Equity Associate

+91 22 4224 6114 [email protected] Murkya *

Equity Analyst+91 224224 6112 [email protected]

Anurag Mantry *Equity Associate

+91 22 4224 6129 [email protected]

* Jefferies India Private Limited § Jefferies Singapore Limited

MCI (P) 047/07/2016

^Prior trading day's closing price unlessotherwise noted.

Key Takeaway

The fight against corruption will extend beyond demonetization. However,the implications for the listed universe isn’t too rosy, at least in the near-term. Wealth destruction and risk aversion mean growth will slow, primarilyin consumer discretionary. Banks will hurt more from growth slowdown andasset quality issues than they benefit from higher CASA and rate cuts. Low endconsumption might be the lone bright spot. We set a new Nifty target of 7500.

The politics of anti-corruption: We see the recent demonetization move as part of aprocess to fight corruption and unaccounted wealth in which several more moves will come.Together with GST (which now runs risk of delay), these measures will accumulate to createa reasonable deterrence to further generation of black money. It is clear that PM Modi willgo to the electorate in the next elections on the anti-corruption plank. Having said that,PM Modi is taking a massive political risk, alienating powerful sections of his core supportbase (traders) and possibly members in his own party but that is unlikely to deter him fromcontinuing on this path. The risk is that of an escalating ladder of tax measures if significantblack money is not discovered and extinguished through the current round.

Will impact longer than you think: The scale of black economy and unaccountedwealth is huge but unquantified. And the government’s efforts to bring it down areunprecedented. There would undoubtedly be a downward shift in wealth, real (cash thatbecomes useless) and perceived (land price). The ability and confidence of black economyparticipants to continue business as usual ought to be severely dented. So will their riskappetite and willingness to spend. The slowdown in the black economy will impact thewhite economy as well as they are inextricably linked. We expect activity levels in rest ofFY17 and FY18 to lower than what it would have been otherwise. The employment scenario,alarming already, will probably worsen, at least temporarily. Consumer discretionary willbe hurt the most and the extent of slowdown will likely be linked directly to the price pointof the item.

On the positive side: Contraction in money supply would help the already benigninflation outlook. We see a strong possibility of 50-100bps rate cuts over next 12 months.Bond markets have already anticipated such a move. Lower rates are unlikely to spur higherconsumption growth or capex cycle in the short-term in times of such high uncertaintyand excess capacity. Banks, especially those with strong retail liability franchise (read publicsector banks) could possibly benefit from higher CASA but will face headwinds from slowcredit growth as well as possible asset quality issues, especially in consumer lending (thoughin near-term, willful defaulters could use their ill-gotten wealth to pay up).

Government finances could benefit from higher tax collections as complianceimproves. We think there are several legal impediments to Reserve Bank paying out the“windfall gains” from exit of black cash from the system. It is almost imperative that thegovernment uses any gains to expand its spending to boost the economy but its optionsare limited. Increased capex is likely but the government does not have the institutionalcapacity to rapidly increase construction of roads or rail. Therefore some form of transfer toconsumers, either through tax slab changes (limited impact) or direct transfers in some formor the other (to the poor) is likely. We think low end consumption would benefit in FY18.

All things considered, we expect big challenges to growth in FY17 and FY18. The marketisn’t cheap and the well owned sectors (discretionary, NBFCs) face the most headwinds fromgovernment action. We downgrade financials to neutral and discretionary to underweightand upgrade consumer staples to overweight. IT continues to be our other key overweight.Top down, we now expect index earnings to grow 8% (cons. at 13%) in FY17E and 15%(cons. 20%) in FY18E. We expect Nifty to trade near 7500, at its historic earnings multiple.

Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 18 to 22 of this report.

Key charts

Exhibit 1: Upgrade staples & telecom, downgrade discretionary & financials

Sector recommendations

Current Earlier

Overweight Consumer staples Financials

Industrials Industrials

IT IT

Utilities Utilities

Neutral Financials Consumer staples

Telecom Consumer discretionary

Energy Energy

Underweight Pharma Pharma

Consumer discretionary Telecom

Source: Jefferies

Exhibit 2: Top picks

Company Ticker CMP TP Rating Jeff PE (x) Jeff PB (x)

(In INR) (In INR) FY17E FY18E FY19E FY17E FY18E FY19E

Hindustan Unilever Ltd HUVR IN 803 1,000 BUY 37.5 31.2 27.2 42.7 41.7 40.6

ITC ITC IN 228 298.6 BUY 25.6 23.1 20.5 7.1 6.3 5.6

Infosys INFO IN 920 1,280 BUY 14.5 12.9 11.3 3.0 2.7 2.3

Tata Consultancy Services TCS IN 2125 2,700 BUY 15.9 14.2 12.4 4.6 3.8 3.1

HDFC Bank HDFCB IN 1211 1,410 BUY 21.5 18.1 14.5 3.8 3.2 2.7

State Bank of India* SBIN IN 276 320 BUY 16.9 12.9 9.1 1.6 1.3 1.1

Larsen & Toubro LT IN 1370 1,750 BUY 22.8 20.5 16.8 2.7 2.5 2.3

Tata Motors TTMT IN 471 606 BUY 9.8 8.2 7.8 1.6 1.4 1.1

NTPC NTPC IN 159 195 BUY 12.9 11.2 9.5 1.4 1.3 1.2

Bharat Petroleum Corp BPCL IN 643 714 BUY 9.5 8.2 8.0 2.5 2.1 1.8

Source: Jefferies estimates, company data *(Parent)

Equity Strategy

India

21 November 2016

page 2 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Exhibit 3: Changes in JEF growth estimates across consumer-facing sectors (%)

New Old

FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E

NBFCs

MMFS 12.6 9.3 15.0 15.8 12.6 12.9 15.1 15.8

SHTF 17.1 10.5 13.9 14.4 17.1 16.7 16.3 14.8

Bajaj Finance 43.9 32.0 30.8 29.2 43.9 32.8 31.3 28.7

Capital First 73.8 53.2 48.1 40.4 73.8 58.3 43.7 40.7

LICHF 15.2 13.3 12.1 13.1 15.2 15.5 15.5 15.7

Banking sector

System loan growth 10.3 6.0 9.0 15.0 10.3 12.0 15.0 15.0

Autos

Hero

Motorcycles (1.3) 5.3 8.4 6.8 (1.3) 8.1 7.2 7.4

Scooters 8.9 20.7 15.4 12.1 8.9 26.4 15.4 15.4

Bajaj

Motorcycles 7.2 12.0 8.0 8.0 7.2 15.0 8.0 8.0

Maruti

Cars 9.5 3.6 10.1 12.0 9.5 5.6 14.6 12.1

UVs 28.9 74.1 19.2 14.5 28.9 74.3 18.1 14.5

Mahindra - UVs

UV 7.5 7.0 5.6 10.9 7.5 8.8 10.4 13.9

Tractors (8.8) 20.0 5.0 7.0 (8.8) 18.0 7.0 7.0

Consumer Durables

Voltas - Unitary Cooling 2.0 17.0 19.0 18.0 2.0 24.0 21.0 20.0

Consumer Staples

Hindustan Unilever

Soaps (3.5) 5.0 15.0 15.0 (3.5) 5.0 7.0 7.0

Detergents 3.9 5.0 15.0 15.0 3.9 5.0 7.0 7.0

Personal Products 7.5 3.0 12.0 12.0 7.5 3.0 12.0 12.0

Tea 6.6 2.0 7.0 7.0 6.6 2.0 7.0 7.0

Market Index

NIFTY EPS* 8 15 13 20

Source: Jefferies estimates, company data *Old represents current consensus estimates

Equity Strategy

India

21 November 2016

page 3 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Demonetization The government’s decision to demonetize 86% of currency in circulation (Rs15.4tr in

Rs.500 and Rs.1000 notes) came with the surprise element that is a precondition for such

a move to succeed. What could have possibly determined the timing of the decision? With

all the information we have now, it seems clear that the decision to demonetize was taken

a long while ago, though the exact timing could have been a factor of extraneous

considerations – need to maintain secrecy and political calendar. The currency in

circulation (CIC) has grown at an abnormal pace since late last year. Various reasons have

been cited for this but none of them seem convincing on their own individual merit.

Exhibit 4: Spurt in currency in circulation…

Source: Jefferies estimates, RBI

Exhibit 5: …and as a % of GDP

Source: Jefferies estimates, RBI

However, the prerequisites for secrecy have also meant delay in issuance of notes that

replace the stock of outgoing notes. The reasons for introduction of notes with Rs2000

denomination are unclear but it is possible that these will also be demonetized at some

point in the not too distant future. Based on the current printing capacity of the mints, we

estimate that it will take at least 5 months before the notes that are required for normal

functioning of the economy are fully replenished. Getting notes printed in another

country could be an option but we don’t know if that’s a route the government would

choose to take.

5%

10%

15%

20%

Currency growth Nominal GDP at market price growth (yoy)

75%

80%

85%

90%

11%

12%

13%

Currency-to-trailing 4Q GDP M3-to-trailing 4Q GDP(RHS)

Decision to render 86% currency in

circulation as illegal tender not taken

overnight

Reintroduction of new currency to

take over 5 months at least, we think

Equity Strategy

India

21 November 2016

page 4 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Exhibit 6: Estimated time taken to replace stock of currency ~6 months

Existing stock of currency

Currency denomination Volume (million pieces)

on 31-Mar-16

Estimated volume

on 07-Nov-16

Comments

500 15,707 16,972 The value of currency in circulation grew by 8% between 31-

Mar-16 and 04-Nov-16

1000 6,326 6,836

Replacement stock of Currency

Currency denomination Volume (million pieces)

to be printed

Comments

500 16,972 Assumed all 500 notes to be replaced with 500 notes only

2000 3,418 All 1000 notes to be replaced with 2000 value notes

Total notes to be printed 20,390

Printing logistics

Annual capacity (million pieces)

2 presses owned by RBI 16,000

2 Presses owned by the government 9,000

Total Capacity 25,000

Capacity utilisation 120%

Replacement assumptions

Notes not returning 30% Assumed 30% of both 500 and 1000 notes do not come back.

Estimates notes to be printed 14,273

Time required 5.7 months

Source: Jefferies estimates, Government of India, RBI

There could be some semblance of normalcy much before that period as trade channels

adjust credit terms and move partly to non-cash modes of payment. Nevertheless, the

logistical issues disrupting the economy would likely extend well into the March quarter.

Hopes of a quick transition to card based payments and e-wallets need to be tempered by

the penetration of cards and point of sales machines. On last count, there were 1.46m

POS machines across the country. For reference, India has about 6m retail outlets and a

large number of wholesale markets and mandis (agriculture markets).

Exhibit 7: Impressive growth in cards and POS but not enough

Source: RBI

296351

414

575686

739661

854

1,0661,127

1,3861,462

0

200

400

600

800

1,000

1,200

1,400

1,600

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Aug-16

Total cards (in million) PoS terminals (in thousands)-RHS

Massive adoption of non-cash

payment systems still far away

Equity Strategy

India

21 November 2016

page 5 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

The big imponderable right now is what proportion of the Rs15.4tr is permanently

destroyed. Various estimates put the extent of unaccounted wealth held in form of cash

between Rs3tn to Rs5tn. Undoubtedly, holders of hidden wealth would try to find ways to

beat the system. Small amounts of unaccounted money would be shown as part of

current year’s income or in revised returns of previous years. Some would convert part of

the unaccounted cash through purchase of precious metals (gold import is less than

Rs0.3tn per month) or deposit in other people’s accounts (upto Rs250k invites no

scrutiny). But these will not be enough to “legalise” the entire amount, especially since

the government is plugging loopholes on a daily basis. There are already news reports of

the government departments having sent tax notices to jewellers and unusual depositors

in the last few days.

Accounting norms – not so clear

What the RBI does with the cash that isn’t exchanged or deposited is yet another

imponderable. There doesn’t seem to be a straightforward answer to this question. The

RBI act provides no guidance to how the board of directors should treat an event like this.

All that is says is that the RBI shall pay the profits to the central government after

deducting certain expenses. Could the RBI pass the lower resulting liability through its

P&L and show it as a profit? We aren’t sure of the accounting norms.

“After making provision for bad and doubtful debts, depreciation in assets, contributions

to staff and superannuation funds [and for all other matters for which provision is to be

made by or under this Act or which] are usually provided for by bankers, the balance of

the profits shall be paid to the Central Government” – Reserve Bank of India Act, 1934

“After making provision for bad and doubtful debts, depreciation in assets, contributions to

staff and superannuation funds [and for all other matters for which provision is to be made

by or under this Act or which] are usually provided for by bankers, the balance of the profits

shall be paid to the Central Government” – Reserve Bank of India Act, 1934

Moreover, there could be legal challenges to the RBI treating the currency that isn’t

returned by March 31st 2017 as currency that is extinguished. After all, the currency note

is a promissory note to perpetuity. What gains could RBI possibly record while making

enough provisions for notes that come up for exchange at a later date?

We think the RBI could choose to do a combination of all choices – transfer part of the

gains to the government but retain most of the gains to increase its normal reserves. If the

transfer requires a change in RBI act, the government can easily do so presenting it as a

money bill. Politically, it wouldn’t be a difficult task to do, especially if the resulted flow is

used for some kind of pro-poor policy.

Economic cost in the short-term is all pervasive.

There is almost no sector that would not see a significant drop in activity during the

period of transition of at least 2 quarters. We see double digit declines in most domestic

consumer facing businesses through rest of the year and significant elongation of working

capital cycles. Banks and NBFCs might face higher delinquencies, albeit most of which

would be temporary in nature. The markets are unlikely to be too bothered about these

short-term issues. The real question is the impact on demand and asset quality beyond

the transition period.

Key question remains what portion

of the Rs15.4tr rendered illegal will

not come back

Another moot point is how this

reduced RBI liability from lesser

deposit of old currency, if any, will

be utilised by the RBI or the govt.

The RBI might only transfer a part of

the potential gains to the govt., we

think

All sectors to be impacted for at least

2 quarters in our view

Equity Strategy

India

21 November 2016

page 6 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Part of series of moves The demonetization move is part of the series of the moves that the government has been

making since it assumed power in May 2014. There have been several legislative and

administrative actions and it is clear that this will continue.

Exhibit 8: List of bills passed by the government which mitigate corruption in some form

Year Topic Bill Description Status

2016 Aadhaar The Aadhaar (Targeted Delivery

of Financial and Other Subsidies,

Benefits and Services) Bill, 2016

- To provide targeted delivery of subsidies and services to citizens by assigning them

unique identity (Aadhaar) numbers

Passed

2015 Banking

&

Financial

Services

The Insolvency and Bankruptcy

Code, 2015

- Aimed at creation of time-bound processes for insolvency resolution of companies and

individuals, targeting completion within 180 days

- In case of lack of resolution of insolvency, the creditors may sell the assets of the

borrowers to recover the debt.

Passed

2015 Black

money

The Benami Transactions

(Prohibition) (Amendment) Bill,

2015

- To prohibit benami transactions (cases where the property is not being held by the

person who has paid for it to evade taxes, or is held under a fictitious name) and provide

for confiscation of such properties

- Amends the Benami Transactions Act, 1988

Passed

2015 Black

money

The Undisclosed Foreign Income

and Assets (Imposition of Tax)

Bill, 2015

- To enact a comprehensive new law on black money focusing on such wealth which has

been parked outside the country

- Provides for separate taxation, outside the Income Tax Act, of any undisclosed foreign

income and assets

- Window for one-time declaration of undisclosed income and assets given – to be taxed at

30%, with 30% penalty on top

- Charges for undeclared income outside the window: 30% tax, 90% penalty

Passed

2015 Black

money

Amendments vide Finance Act,

2015

- To Prevention of Money-laundering Act (PMLA), 2002: Amendment of the definition of

proceeds of crime to enable attachment and confiscation of equivalent asset in India where

the foreign asset cannot be confiscated

- To Foreign Exchange Management Act (FEMA), 1999: Amendment to provide for seizure

and confiscation of value equivalent situated in India, in cases where foreign exchange,

foreign security or immovable property situated outside India have been acquired in

contravention of Section 4 of FEMA

Passed

2015 Mining The Coal Mines (Special

Provision) Bill, 2015

- Aims to make transparent the process of allocation or auction of coal mines

- Introduced to replace the associated Ordinance issued by the Government after the

cancellation of 204 coal blocks by the Supreme Court in 2014

Passed

2014 Taxation The Constitution (122nd

Amendment) (GST) Bill, 2014

- The Constitution amendment bill to enable introduction of the goods and services tax

(GST)

Passed

2014 Judicial The Constitution (121st

Amendment) Bill, 2014

- To make the process of appointments to higher judicial posts and transfer of High Court

judges more participatory, transparent and objective

Passed

2014 Financial

Markets

The Securities Laws

(Amendment) Bill, 2014

- To empower Securities and Exchange Board of India (SEBI), the securities market

regulator, to effectively pursue fraudulent investment schemes by calling for relevant

information and records from any person

- Also provides guidelines for the formation of special fast trial courts

Passed

Source: Jefferies estimates, Government of India

The incumbent govt. has taken

numerous initiatives against black

money & corruption

Equity Strategy

India

21 November 2016

page 7 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Exhibit 9: Non-legislative initiatives taken by the Modi government to combat black money

Year Initiative Description

2016 Existing Rs500 and Rs1,000

notes not eligible as legal tender

- Move announced on November 8 at 8PM, effective midnight

- Replacement of such extant notes with new notes of denominations Rs500 and Rs2,000

2016 Income Declaration Scheme - 4-month window for resident Indians to declare undisclosed assets; tax rate 45%; immunity from prosecution

- Charges for undeclared income outside the window: effective penalty up to 200%; imprisonment up to 7 years

- ~Rs653 bn disclosed, with ~Rs294 bn being the government collection, out of which half accrues this fiscal

2016 Enhanced enforcement measures - Finding of tax evasion cases to the tune of ~Rs500bn in indirect taxes and Rs210bn in undisclosed income (till

May, 2016) in ~2 years

- Smuggled goods worth ~Rs40bn seized in ~2 years, 32% higher than in previous comparable 2-year period

- Prosecution launched in 1,466 cases in ~2 years (higher by 25% versus previous comparable 2-year period)

- The SIT directed the ED to take necessary action against 788 companies (up to July, 2016) for not bringing back

export realisations of over Rs1bn within the required window, thereby illicitly parking funds abroad.

2016 Widening of ambit of goods

subject to tax collection at

source (TCS)

- TCS of 1% on any purchase in cash of value exceeding Rs0.2mn (excluding bullion and jewellery) versus a

select list of goods earlier

- TCS of 1% on purchase of motor vehicles exceeding Rs1mn in value

2015 Mandatory PAN requirements - Purchase/ sale of any goods or services exceeding Rs.0.2mn in value per transaction (including jewellery) versus

no requirement earlier

- Hotel, restaurant and foreign travel expenses exceeding Rs50,000 versus Rs25,000 earlier

- Cash payments aggregating over Rs.50,000 in a year versus no requirement earlier

2015 Foreign Black money compliance

window

- 3-month window to declare undisclosed foreign assets to be taxed at 30%, with 30% penalty on top; immunity

from prosecution

- Charges for undeclared income outside the window: 30% tax, 90% penalty; imprisonment for up to 10 years

- Rs41.5 bn disclosed in 638 cases; government collection ~Rs25bn

2015

on-

wards

Negotiations with other nations - India signed DTAAs (Double Taxation Avoidance Agreements) with a number of countries such Cyprus,

Mauritius and South Korea to limit round-tripping of money into capital markets by adopting source-based

taxation of capital gains and other measures.

- India joined the Multilateral Competent Authority Agreement (MCAA) on Automatic Exchange of Financial

Account Information, the aim of which is to have exchange of information on an automatic basis from 2017 as

per Common Reporting Standards (CRS).

- India entered into an Automatic Exchange of Information (AEOI) with Switzerland in a spirit of mutual

friendship and cooperation, and is negotiating similar agreements with other countries to combat tax evasion.

2014 Special Investigation Team (SIT)

on black money

- An SIT under a retired Supreme Court judge formed to:

- probe black money parked abroad, and

- to come up with various recommendations to curb formulation and movement of black money

Source: Jefferies estimates, Government of India

Having opened up its efforts on assets held abroad and black wealth held in cash, the next

logical step would be an attack on hidden wealth held in the form of gold and real estate

and a tighter regulatory control on anonymous equity investments coming through

participatory notes. The political and economic cost of efforts to uncover hidden wealth in

the form of gold is low but administratively, a lot harder to track down. The jewellers

association has confirmed that the government has sent tax notices to over 600 jewellers

this month and clearly sees the need to track efforts of hoarders to hide wealth in form of

precious metal. We expect more action on this front in the coming months.

Handling real estate, on the other hand, is a completely different ball game. The

government has armed itself with a reasonably harsh law (Benami property act).

However, the cost of going after hidden wealth in the form of land is huge. Firstly, land

titles are very unclear and hugely disputed. Very few states have digitized land records.

Potential next targets could be gold,

real estate and anonymous equity

investments

Equity Strategy

India

21 November 2016

page 8 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Secondly, the amounts involved are massive relative to the size of the economy. As it is,

we expect prices and transactions in properties to fall post the demonetization drive. That

would worsen significantly if the government were to go after illegal wealth in land. The

attendant negative wealth effect would hurt the economy in a vastly higher magnitude

than any of the other measures. The biggest challenge, however, is the impact such a

move will have on health of the financial sector. We don’t think the banking system can

handle rapid erosion in value of real estate prices. We expect (and hope) that the

government takes a more calibrated approach to handling hidden wealth in real estate. It

probably will, as political costs are likely to be high as well.

The key issue isn’t whether the government indeed does all of the above. The mere threat

of further action against black income and wealth (as the PM has already warned in his

political rallies), will likely induce behavioural changes of those in the black economy.

Politics of black money Black economy somehow seems to enthral Indian voters in a manner that is

unprecedented in any other large democracy. It is seen as the single most reason holding

India back from its inevitable greatness. The narrative around the 2014 election was

primarily around corruption and black money and we think the current government

under PM Modi has already made up its mind to make this the key election issue in 2019

as well.

Without a question, the government has taken a massive risk in undertaking an exercise of

this scale, affecting every citizen in a not so favourable manner, in the hope that the sense

of retributive justice against the corrupt will yield political dividends. And it seems to be

working. The government has been adept at making what is essentially an economic

event in recovering unpaid taxes into a political rallying point against corruption. Our

reading of the current voter sentiment is that it is mostly favourable towards the recent

moves against black wealth and income, despite temporary hardship that most citizens

have had to face. Of course, sentiment could change if the hardship lasts too long. The

overwhelming public mood against corruption has turned the demonetization process

into a public movement. Protest rallies organized by opposition parties seem to have

generated lukewarm response. Those protesting most loudly are being seen as the ones

with most to hide. Modi and the chief ministers of Bihar (Nitish Kumar) and Orissa (Navin

Patnaik) seem to be the ones emerging stronger in the process. Some political

realignment seems possible.

Behavioural changes How does the consumption behaviour and risk appetite of those with black wealth

change this beyond this period of disruption? That’s the key question in investors’ minds.

It ought to be increasingly clear to everyone, including to those with hidden income and

wealth, that this government is likely to take the fight against black wealth to the finish

and is willing to absorb political and economic costs in the process. In fact, the risk is that

the government will unleash harsher measures with every failed attempt in uncovering

black money. That being the case, assuming business as usual scenario would be

erroneous. The series of measures unveiled and to be unveiled creates a permanent

deterrent to generation and storage of black wealth. Our base case is that there would be

considerable wealth destruction – directly (obsolescence of cash on hand) and indirectly

(fall in real estate prices and ability to transact in that market).

It is well accepted that black wealth and income is a key source of demand for land, high

end luxury items (expensive watches, for e.g.) and jewellery. But the linkages go far

deeper. If black component of economic activity is indeed 20-25% of GDP, as various

agencies’ reports seem to suggest, the linkages with the white economy will be far wider.

People with black wealth/income also have tax paid income and disclosed wealth. How

A crackdown on real estate could

have huge ramifications for the

financial sector

Massive political risk, but sentiment

by and large seems positive

Impact on mind-set for creation of

black wealth might be permanent

Equity Strategy

India

21 November 2016

page 9 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

the tax paid money is spent will necessarily be influenced by the extent of non-disclosed

income. It is well possible that someone with hidden wealth uses his tax paid income to

access finance to buy a car. If the certainty of that hidden income or wealth were to

suddenly disappear, it would most certainly change his willingness to buy the car or at

least change the kind of car he buys. It would therefore be erroneous to assume that the

impact would be limited to sectors where purchases were being made directly with

hidden income. Thus, to assume that the lasting impact of the anti-hidden wealth

measures hurt only real estate (and associated home improvement) demand and not

demand for other consumer durables would be taking an overoptimistic view of the

situation. We expect a general fall in risk appetite and willingness to spend (even with

disclosed income).

Black vs Informal economy

There is a risk of confusing cash and informal economy with black economy. Indian

economy is largely informal, with over 84% of employment being informal. By law,

agriculture is not taxed, either directly or indirectly. Farmers do not even need to file their

returns. This poses a serious policy challenge for the government – how does it

differentiate undisclosed income/wealth from wealth/income that need not be disclosed?

Moving to cashless transfers and transactions is certainly one way but that is some time

off. In the current political environment, it is probably imperative for the government to

assuage the fears of rural populace with some fiscal measures.

Exhibit 10: Contract employees account for all increase in organized

enterprises

in mn Informal Formal Total

FY00

Unorganised 341.3 1.4 342.6

Organised 20.5 33.7 54.1

Total 361.8 35.1 396.7

FY05

Unorganised 393.5 1.4 394.9

Organised 29.1 33.4 62.6

Total 422.6 34.8 457.5

FY10

Unorganised 385.1 2.3 387.3

Organised 42.1 30.7 72.9

Total 427.2 33 460.2

Source: NSSO, Planning commission

Difficult to distinguish between

undisclosed wealth and wealth not

needed to be disclosed

The impact of the move could be

huge not just for real estate, but for

the entire discretionary consumption

basket

Equity Strategy

India

21 November 2016

page 10 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Fiscal and monetary implications India’s employment situation dictates that, in absence of external shock or massive

expansion in fiscal deficit, inflation should stay contained. And that is our base case.

Exhibit 11: Inflation estimated to remain below 5%

Source: Jefferies estimates, CMIE

Monetary implications

The demonetization process is likely to reduce currency in circulation, at least in the near-

term. This will likely enhance the already benign inflation outlook. This would give room

for the RBI to cut rates further, though the bond markets have already anticipated such an

eventuality. We expect 50-100bps cut in policy rates in the next one year. Further move in

market rates would also be dictated by foreign inflows/outflows. It is pertinent to note

that the difference between India’s real rate and the US’s real rate has not narrowed

meaningfully yet.

Exhibit 12: While the Indian bond yields have fallen…

Source: Bloomberg

Exhibit 13: … gap vs US rates has not fallen materially

Source: Bloomberg

Fiscal implications

Forecasting fiscal account changes for the next year is a lot more challenging. It is likely

that there would be better compliance in direct personal tax administration. There could

be meaningful increases in both FY17 as well as FY18. However, corporate tax collection

and indirect tax collection could suffer on account of slowdown in activity. Furthermore,

the transition to a GST regime makes such a calculation even more challenging.

As we argued earlier, fiscal support to boost the economy has become almost

unavoidable. The extent and nature of the fiscal boost would depend on how much gains

the government realizes from demonetization. Having said that, it is almost certain that

0

1

2

3

4

5

6

7

8

9

10

Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

CPI (%)

Projection

4

5

6

7

8

9

10

May-14 Nov-14 May-15 Nov-15 May-16 Nov-16

India 10YR Bond Yield (%)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

May-14 Nov-14 May-15 Nov-15 May-16 Nov-16

Gap between India and US real 10yr yield (%)

Our base case – inflation under

control (below 5%)

Expect RBI to cut rates by 50-100bps

Forecasting fiscal implications tough;

positive – compliance, negative –

economic activity slowdown

Equity Strategy

India

21 November 2016

page 11 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

the fiscal support would be directed towards the low end consumers, to mitigate the

impact of the hardships faced from the transition as well as to effect an immediate

multiplier impact. Increased spending in infrastructure is likely. But capex spend runs the

challenge of lack of institutional ability to meaningfully spend that money in a hurry. It is

hardly fathomable that the government would be in a position to increase road

construction activity by 30-40% in a short period. Instead, it is more likely that the

government would choose to boost subsidies for low cost rural housing and farm

insurance scheme. There are press reports about the government transferring any windfall

gains from demonetization directly into the accounts of Jan Dhan account holders. This is

not improbable given its potent political messaging of transferring wealth from the

corrupt to the poor (part of the government’s poll rhetoric in 2014).

While tax collections could be challenged in the immediate short-term, the combination

of anti-black money measures and GST would bring in more entities and persons into to

the tax net, both direct and indirect. As the systems stabilise and information exchange

between various tax systems improves, avoiding tax would be increasingly hard. That

argues for lower tax rates on those who already pay taxes. It is hard to imagine a cut in

personal income tax rates, as is being expected by some. India has amongst the lowest tax

rates amongst emerging economies. An increase in tax slab limits is more likely – we

expect the lowest slab limit to increase from Rs250,000 to Rs300,000 in the coming

budget. The government has already committed to bringing corporate tax rate to 25%

from 30% over the next 3 years.

Sectoral impact Over the next 18-24 months, we see the following impact of the anti-corruption moves

on the economy

Significant slowdown in real estate prices and transaction (except low cost

housing, should it get government support)

A further worsening of the already poor jobs scenario

Fall in consumer sentiment, impacting high end discretionary spending

Muted increase in capacity utilisation and growth outlook, delaying the private

sector capex further

Slowdown in credit growth compared to what it would have been otherwise

Improvement in low end consumption

Autos

In the short-term, we see a sharp deceleration in demand across all categories due to lack

of currency to transact. Most auto companies have strong balance sheet, so they could

help the rest in the supply chains by offering better credit terms. That would mitigate

distribution issues to a certain extent. However, demand, especially in the case of two-

wheelers would be severely impacted in the short-term. Anecdotal evidence suggests a

very high drop in sales of two-wheelers and spare parts and 10-20% drop in retail sales of

cars.

The medium term (1-2 years) impact is likely to be quite different. We see a sharp

slowdown in high priced cars, moderate slowdown in mid-priced cars and mild

slowdown in small cars and two-wheelers from FY18. Commercial vehicles would grow

slower than what it would have otherwise due to slower economic activity. Tractor

demand could slow too. Pricing power will likely be absent across all categories.

Companies could gain from better spare parts sales as unorganized competition

diminishes.

Hard to imagine tax rate cuts –

personal rates already low, corporate

rates committed to be raised

Short-term – sharp fall in demand

across categories

Medium-term – impact more for

high-end and less for small cars and

2-wheelers

Expect fiscal boost to support

economy, especially for lower-end

customers through housing and

insurance schemes

Equity Strategy

India

21 November 2016

page 12 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Consumer staples

Short-term disruption would be short-lived due to the nature of demand. We expect

recovery from March quarter itself. Some categories which are more discretionary in

nature might see slower recovery.

Medium term (1-2 years), consumer staples benefit from three drivers. We see fiscal

stimulus aimed at low end consumers. Secondly, the listed companies will benefit at the

expense of unorganized competitors due to anti-corruption moves as well as

implementation of GST.

Industrials

In the short-term, capex activity could see disruptions due to cash crunch in the system.

However, this is likely to affect cash flows more than actual construction.

With diminished growth outlook, weaker sentiment and low capacity utilisation, private

sector capex would likely be further postponed. Lower rates are unlikely to help demand

revival much in this scenario but could help stretched balance sheets improve.

Government capital expenditure could see increase but unlikely to be meaningfully large.

On balance, medium term outlook is likely unchanged.

Financials

Banks would likely see a sharp upsurge in deposits in the current quarter and next but we

expect most of the incremental deposits to be withdrawn as notes become available. The

lasting benefit of higher CASA would be marginal. On the other hand, credit growth in

FY18 would likely be slower than what it would have been otherwise. Lower rates could

help boost value of investments. Delinquencies could see upside risks, especially in the

hitherto unaffected consumer lending segment.

Non-banking financial companies with excessive focus on consumer lending and loan

against property could see diminished growth outlook as well as deterioration in asset

quality.

A shift in transactions from cash to cashless and in savings/storage from physical

assets/cash to financial savings would boost banks’ competitiveness and balance sheets in

the long-term. Immense opportunities exist for banks and financial institutions that

innovate and adapt to new emerging technologies.

Real estate

In the short-term, we expect a sharp fall in transaction volume and value of land and

houses. While transactions could recover gradually, especially boosted by lower rates,

prices are likely to be under pressure for an extended period. Registered value of land and

houses (on which stamp duty is paid) could converge to market rates, eliminating a key

source of hidden wealth creation. Low cost housing could possibly see some meaningful

support from the government.

White goods

Medium term demand is likely to be lower than what it would have been otherwise.

However, considering the low penetration and low price points, it could start normalising

before too long. Moreover, large companies with strong balance sheets could possibly

gain share due to GST.

Cement

Fall in real estate construction would likely be offset by increase in construction of low

cost housing. Infrastructure construction could also accelerate marginally. On balance,

demand outlook likely unchanged. The sector could also benefit from implementation of

GST.

Immediate impact to be brief; sector

to benefit over medium term

Largely neutral due to moving parts

Consumer lending and LAP focussed

NBFCs under risk

Value of land under pressure;

number of transactions could rise

Medium term to be impacted, but

tailwinds from penetration and GST

Largely unchanged – many moving

parts

Loan growth expectation reset lower

Equity Strategy

India

21 November 2016

page 13 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Market conclusion We think the markets’ earnings expectations for FY17E and FY18E would have to be reset

meaningfully post the recent events. Any exercise in earnings estimates at this point is

fraught with risks of predicting too many inscrutable behavioural changes and

unpredictable variables but the risks to the numbers are clearly on the downside.

Exhibit 14: Current EPS estimates for MSCI…

Source: Factset

Exhibit 15: …and Nifty

Source: Jefferies estimates, Bloomberg

Prior to the recent events, the pace of earnings downgrades had slowed considerably and

there was room for belief that finally we are entering a phase of reality matching forecasts.

In the following chart, we show the changes in forecasts for the current year and

immediate following year for each quarter. As can be seen, the pace of downgrades

remained high in 2015 and 1QCY16 but has slowed since.

Exhibit 16: Downgrades in market EPS forecasts had slowed in recent

quarters

Source: Factset

Growth forecasts for FY17E/CY16E are clearly at risk due to the short-term cash shortage

disruption. Risks to absolute earnings numbers for FY18E/CY17E are also on the

downside, though growth numbers might not look too bad on the lowered base.

The main downside risks to the market come from the duration of cash crunch. As we

argued, cash in circulation would probably take 6-8 months to normalise. Beyond that,

risks on the downside come from behavioural changes of those who have so far benefited

from hidden wealth and income. Certain sectors, such as real estate and consumer

3.8%

12.7%

18.5%

0%

5%

10%

15%

20%

CY15 CY15E CY17E

MSCI

4.0%

13.1%

19.9%

0%

5%

10%

15%

20%

FY16 FY17E FY18E

Nifty

(12)

(10)

(8)

(6)

(4)

(2)

0

2

4

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

MSCI India EPS Change (%) QoQ

F1 F2

Index earnings estimates under

downside risk

Pace of earnings downgrades had

slowed recently

Equity Strategy

India

21 November 2016

page 14 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

discretionary would likely see lasting impact with its attendant impact on financials

through lower credit growth and asset quality issues.

We see very limited upside risks to current earnings forecasts. If any, one could argue that

the long-term earnings growth of the listed universe benefits from the formalisation of the

economy, share gains for organized players, more equitable tax incidence and lower cost

of capital. That would impact earnings multiples rather than actual forecasts made by

analysts.

After the recent correction, market multiple is marginally above its long-term average on

current inflated consensus forecast.

Exhibit 17: MSCI India trades at a marginal premium to average

Source: Factset

Top down, we expect Nifty earnings to grow c8% in FY17E and c15% in FY18E – that

would imply a cut of c4.5% in Fy17E EPS forecast and c8.4% cut in FY18E EPS forecast. We

set a Nifty target of 7500 in 6 months, assuming market trades at its long-term average

multiple.

Changes to model portfolio In our previous note, “Jobless Growth - Apparel Exports to the Rescue?”, we had

downgraded Consumer discretionary from Overweight to Neutral and upgraded Staples

from Underweight to Neutral. We take this one step forward and downgrade discretionary

to Underweight and upgrade Staples to Overweight. We also downgrade Financials to

Neutral and upgrade Telecom to Neutral.

The changes in portfolios of institutional investors tell a very interesting story. There has

been a consistent increase in allocation to consumer discretionary and financials at the

expense of IT and staples in portfolios of both foreign and domestic institutions.

Exhibit 18: Sectoral allocation of FII portfolio

Mar-13 Mar-14 Mar-15 Mar-16 Sep-16

Consumer Discretionary 9.6 10.6 11.0 11.2 12.3

Consumer Staples 10.8 9.5 8.1 8.3 7.6

Energy 8.0 7.7 6.0 6.9 7.0

Financials 30.9 28.1 30.7 29.2 32.8

Health Care 6.6 6.8 8.3 8.7 7.4

Industrials 5.5 6.5 7.2 6.4 6.3

Information Technology 13.7 16.0 14.6 15.7 11.9

Materials 7.5 7.7 6.7 6.8 8.4

Real Estate 1.4 1.1 0.9 0.7 0.7

Telecommunication Services 2.7 2.7 3.3 3.0 2.4

Utilities 3.4 3.4 3.2 3.2 3.1

Source: Jefferies estimates, company data

8

10

12

14

16

18

20

22

24

26

Nov-04 Nov-06 Nov-08 Nov-10 Nov-12 Nov-14 Nov-16

MSCI India 12M Fwd PE Avg

We see downside risks to earnings

due to impact across sectors

Our Nifty earnings estimates – c8%

in FY17, c15% in FY18, implying cuts

to consensus of over 4% and 8%

respectively

Strong trend of portfolio allocation

shifting to discretionary and

financials and out of IT and staples

Equity Strategy

India

21 November 2016

page 15 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

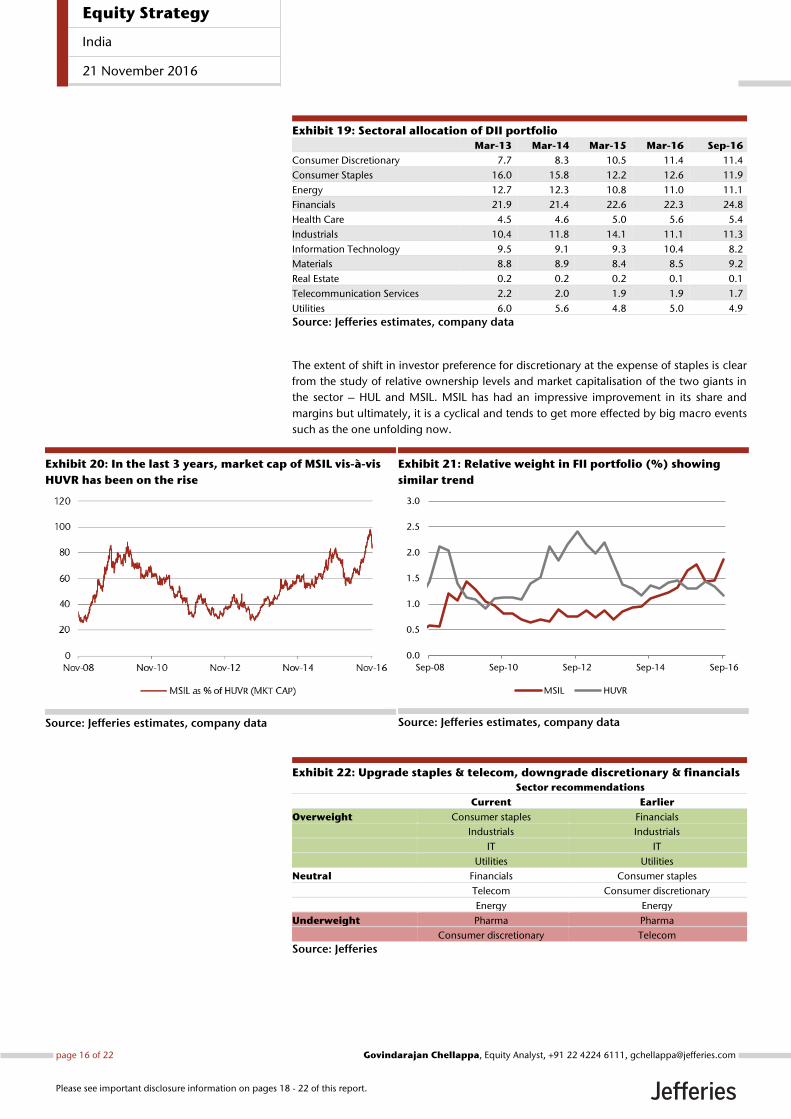

Exhibit 19: Sectoral allocation of DII portfolio

Mar-13 Mar-14 Mar-15 Mar-16 Sep-16

Consumer Discretionary 7.7 8.3 10.5 11.4 11.4

Consumer Staples 16.0 15.8 12.2 12.6 11.9

Energy 12.7 12.3 10.8 11.0 11.1

Financials 21.9 21.4 22.6 22.3 24.8

Health Care 4.5 4.6 5.0 5.6 5.4

Industrials 10.4 11.8 14.1 11.1 11.3

Information Technology 9.5 9.1 9.3 10.4 8.2

Materials 8.8 8.9 8.4 8.5 9.2

Real Estate 0.2 0.2 0.2 0.1 0.1

Telecommunication Services 2.2 2.0 1.9 1.9 1.7

Utilities 6.0 5.6 4.8 5.0 4.9

Source: Jefferies estimates, company data

The extent of shift in investor preference for discretionary at the expense of staples is clear

from the study of relative ownership levels and market capitalisation of the two giants in

the sector – HUL and MSIL. MSIL has had an impressive improvement in its share and

margins but ultimately, it is a cyclical and tends to get more effected by big macro events

such as the one unfolding now.

Exhibit 20: In the last 3 years, market cap of MSIL vis-à-vis

HUVR has been on the rise

Source: Jefferies estimates, company data

Exhibit 21: Relative weight in FII portfolio (%) showing

similar trend

Source: Jefferies estimates, company data

Exhibit 22: Upgrade staples & telecom, downgrade discretionary & financials

Sector recommendations

Current Earlier

Overweight Consumer staples Financials

Industrials Industrials

IT IT

Utilities Utilities

Neutral Financials Consumer staples

Telecom Consumer discretionary

Energy Energy

Underweight Pharma Pharma

Consumer discretionary Telecom

Source: Jefferies

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Sep-08 Sep-10 Sep-12 Sep-14 Sep-16

MSIL HUVR

Equity Strategy

India

21 November 2016

page 16 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Exhibit 23: Top picks

Company Ticker CMP TP Rating Jeff PE (x) Jeff PB (x)

(In INR) (In INR) FY17E FY18E FY19E FY17E FY18E FY19E

Hindustan Unilever Ltd HUVR IN 803 1,000 BUY 37.5 31.2 27.2 42.7 41.7 40.6

ITC ITC IN 228 298.6 BUY 25.6 23.1 20.5 7.1 6.3 5.6

Infosys INFO IN 920 1,280 BUY 14.5 12.9 11.3 3.0 2.7 2.3

Tata Consultancy Services TCS IN 2125 2,700 BUY 15.9 14.2 12.4 4.6 3.8 3.1

HDFC Bank HDFCB IN 1211 1,410 BUY 21.5 18.1 14.5 3.8 3.2 2.7

State Bank of India* SBIN IN 276 320 BUY 16.9 12.9 9.1 1.6 1.3 1.1

Larsen & Toubro LT IN 1370 1,750 BUY 22.8 20.5 16.8 2.7 2.5 2.3

Tata Motors TTMT IN 471 606 BUY 9.8 8.2 7.8 1.6 1.4 1.1

NTPC NTPC IN 159 195 BUY 12.9 11.2 9.5 1.4 1.3 1.2

Bharat Petroleum Corp BPCL IN 643 714 BUY 9.5 8.2 8.0 2.5 2.1 1.8

Source: Jefferies estimates, company data *(Parent)

Exhibit 24: Changes in JEF growth estimates across consumer-facing sectors (%)

New Old

FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E

NBFCs

MMFS 12.6 9.3 15.0 15.8 12.6 12.9 15.1 15.8

SHTF 17.1 10.5 13.9 14.4 17.1 16.7 16.3 14.8

Bajaj Finance 43.9 32.0 30.8 29.2 43.9 32.8 31.3 28.7

Capital First 73.8 53.2 48.1 40.4 73.8 58.3 43.7 40.7

LICHF 15.2 13.3 12.1 13.1 15.2 15.5 15.5 15.7

Banking sector

System loan growth 10.3 6.0 9.0 15.0 10.3 12.0 15.0 15.0

Autos

Hero

Motorcycles (1.3) 5.3 8.4 6.8 (1.3) 8.1 7.2 7.4

Scooters 8.9 20.7 15.4 12.1 8.9 26.4 15.4 15.4

Bajaj

Motorcycles 7.2 12.0 8.0 8.0 7.2 15.0 8.0 8.0

Maruti

Cars 9.5 3.6 10.1 12.0 9.5 5.6 14.6 12.1

UVs 28.9 74.1 19.2 14.5 28.9 74.3 18.1 14.5

Mahindra - UVs

UV 7.5 7.0 5.6 10.9 7.5 8.8 10.4 13.9

Tractors (8.8) 20.0 5.0 7.0 (8.8) 18.0 7.0 7.0

Consumer Durables

Voltas - Unitary Cooling 2.0 17.0 19.0 18.0 2.0 24.0 21.0 20.0

Consumer Staples

Hindustan Unilever

Soaps (3.5) 5.0 15.0 15.0 (3.5) 5.0 7.0 7.0

Detergents 3.9 5.0 15.0 15.0 3.9 5.0 7.0 7.0

Personal Products 7.5 3.0 12.0 12.0 7.5 3.0 12.0 12.0

Tea 6.6 2.0 7.0 7.0 6.6 2.0 7.0 7.0

Market Index

NIFTY EPS* 8 15 13 20

Source: Jefferies estimates, company data *Old represents current consensus estimates

Equity Strategy

India

21 November 2016

page 17 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Analyst Certification:I, Govindarajan Chellappa, certify that all of the views expressed in this research report accurately reflect my personal views about the subjectsecurity(ies) and subject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specificrecommendations or views expressed in this research report.I, Nilesh Jasani, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.I, Piyush Nahar, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.I, Nilanjan Karfa, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.I, Bhaskar Basu, CFA, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.I, Nitin Mathur, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.I, Avinash Singh, CFA, certify that all of the views expressed in this research report accurately reflect my personal views about the subjectsecurity(ies) and subject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specificrecommendations or views expressed in this research report.I, Arya Sen, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) and subjectcompany(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or viewsexpressed in this research report.I, Vaibhav Dhasmana, certify that all of the views expressed in this research report accurately reflect my personal views about the subjectsecurity(ies) and subject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specificrecommendations or views expressed in this research report.I, Lavina Quadros, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.I, Ankit Fitkariwala, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.I, Poornaa Venkatesan, certify that all of the views expressed in this research report accurately reflect my personal views about the subjectsecurity(ies) and subject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specificrecommendations or views expressed in this research report.I, Ranjeet Jaiswal, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.I, Rahul Murkya, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.I, Anurag Mantry, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.Registration of non-US analysts: Govindarajan Chellappa is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and isnot registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, andtherefore may not be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, publicappearances and trading securities held by a research analyst.Registration of non-US analysts: Nilesh Jasani is employed by Jefferies Singapore Limited, a non-US affiliate of Jefferies LLC and is not registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, and therefore maynot be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, public appearancesand trading securities held by a research analyst.Registration of non-US analysts: Piyush Nahar is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is not registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, and therefore maynot be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, public appearancesand trading securities held by a research analyst.Registration of non-US analysts: Nilanjan Karfa is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is not registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, and therefore maynot be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, public appearancesand trading securities held by a research analyst.Registration of non-US analysts: Bhaskar Basu, CFA is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is notregistered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, andtherefore may not be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, publicappearances and trading securities held by a research analyst.Registration of non-US analysts: Nitin Mathur is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is not registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, and therefore maynot be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, public appearancesand trading securities held by a research analyst.

Equity Strategy

India

21 November 2016

page 18 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Registration of non-US analysts: Avinash Singh, CFA is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is notregistered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, andtherefore may not be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, publicappearances and trading securities held by a research analyst.Registration of non-US analysts: Arya Sen is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is not registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, and therefore maynot be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, public appearancesand trading securities held by a research analyst.Registration of non-US analysts: Vaibhav Dhasmana is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is notregistered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, andtherefore may not be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, publicappearances and trading securities held by a research analyst.Registration of non-US analysts: Lavina Quadros is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is notregistered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, andtherefore may not be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, publicappearances and trading securities held by a research analyst.Registration of non-US analysts: Ankit Fitkariwala is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is notregistered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, andtherefore may not be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, publicappearances and trading securities held by a research analyst.Registration of non-US analysts: Poornaa Venkatesan is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is notregistered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, andtherefore may not be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, publicappearances and trading securities held by a research analyst.Registration of non-US analysts: Ranjeet Jaiswal is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is not registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, and therefore maynot be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, public appearancesand trading securities held by a research analyst.Registration of non-US analysts: Rahul Murkya is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is not registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, and therefore maynot be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, public appearancesand trading securities held by a research analyst.Registration of non-US analysts: Anurag Mantry is employed by Jefferies India Private Limited, a non-US affiliate of Jefferies LLC and is notregistered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC, a FINRA member firm, andtherefore may not be subject to the NASD Rule 2241 and Incorporated NYSE Rule 472 restrictions on communications with a subject company, publicappearances and trading securities held by a research analyst.As is the case with all Jefferies employees, the analyst(s) responsible for the coverage of the financial instruments discussed in this report receivescompensation based in part on the overall performance of the firm, including investment banking income. We seek to update our research asappropriate, but various regulations may prevent us from doing so. Aside from certain industry reports published on a periodic basis, the large majorityof reports are published at irregular intervals as appropriate in the analyst's judgement.

Investment Recommendation Record(Article 3(1)e and Article 7 of MAR)

Recommendation Published , 20:30 ET. November 20, 2016Recommendation Distributed , 20:40 ET. November 20, 2016

Company Specific DisclosuresFor Important Disclosure information on companies recommended in this report, please visit our website at https://javatar.bluematrix.com/sellside/Disclosures.action or call 212.284.2300.

Explanation of Jefferies RatingsBuy - Describes securities that we expect to provide a total return (price appreciation plus yield) of 15% or more within a 12-month period.Hold - Describes securities that we expect to provide a total return (price appreciation plus yield) of plus 15% or minus 10% within a 12-month period.Underperform - Describes securities that we expect to provide a total return (price appreciation plus yield) of minus 10% or less within a 12-monthperiod.The expected total return (price appreciation plus yield) for Buy rated securities with an average security price consistently below $10 is 20% or morewithin a 12-month period as these companies are typically more volatile than the overall stock market. For Hold rated securities with an averagesecurity price consistently below $10, the expected total return (price appreciation plus yield) is plus or minus 20% within a 12-month period. ForUnderperform rated securities with an average security price consistently below $10, the expected total return (price appreciation plus yield) is minus20% or less within a 12-month period.NR - The investment rating and price target have been temporarily suspended. Such suspensions are in compliance with applicable regulations and/or Jefferies policies.CS - Coverage Suspended. Jefferies has suspended coverage of this company.NC - Not covered. Jefferies does not cover this company.Restricted - Describes issuers where, in conjunction with Jefferies engagement in certain transactions, company policy or applicable securitiesregulations prohibit certain types of communications, including investment recommendations.Monitor - Describes securities whose company fundamentals and financials are being monitored, and for which no financial projections or opinionson the investment merits of the company are provided.

Equity Strategy

India

21 November 2016

page 19 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.

Valuation MethodologyJefferies' methodology for assigning ratings may include the following: market capitalization, maturity, growth/value, volatility and expected totalreturn over the next 12 months. The price targets are based on several methodologies, which may include, but are not restricted to, analyses of marketrisk, growth rate, revenue stream, discounted cash flow (DCF), EBITDA, EPS, cash flow (CF), free cash flow (FCF), EV/EBITDA, P/E, PE/growth, P/CF,P/FCF, premium (discount)/average group EV/EBITDA, premium (discount)/average group P/E, sum of the parts, net asset value, dividend returns,and return on equity (ROE) over the next 12 months.

Jefferies Franchise PicksJefferies Franchise Picks include stock selections from among the best stock ideas from our equity analysts over a 12 month period. Stock selectionis based on fundamental analysis and may take into account other factors such as analyst conviction, differentiated analysis, a favorable risk/rewardratio and investment themes that Jefferies analysts are recommending. Jefferies Franchise Picks will include only Buy rated stocks and the numbercan vary depending on analyst recommendations for inclusion. Stocks will be added as new opportunities arise and removed when the reason forinclusion changes, the stock has met its desired return, if it is no longer rated Buy and/or if it triggers a stop loss. Stocks having 120 day volatility inthe bottom quartile of S&P stocks will continue to have a 15% stop loss, and the remainder will have a 20% stop. Franchise Picks are not intendedto represent a recommended portfolio of stocks and is not sector based, but we may note where we believe a Pick falls within an investment stylesuch as growth or value.

Risks which may impede the achievement of our Price TargetThis report was prepared for general circulation and does not provide investment recommendations specific to individual investors. As such, thefinancial instruments discussed in this report may not be suitable for all investors and investors must make their own investment decisions basedupon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Past performance ofthe financial instruments recommended in this report should not be taken as an indication or guarantee of future results. The price, value of, andincome from, any of the financial instruments mentioned in this report can rise as well as fall and may be affected by changes in economic, financialand political factors. If a financial instrument is denominated in a currency other than the investor's home currency, a change in exchange rates mayadversely affect the price of, value of, or income derived from the financial instrument described in this report. In addition, investors in securities suchas ADRs, whose values are affected by the currency of the underlying security, effectively assume currency risk.

Other Companies Mentioned in This Report• Bajaj Auto Limited (BJAUT IN: INR2,574.80, HOLD)• Bajaj Finance Limited (BAF IN: INR878.40, UNDERPERFORM)• Bharat Petroleum Corporation Limited (BPCL IN: INR642.55, BUY)• Capital First Limited (CAFL IN: INR525.70, UNDERPERFORM)• HDFC Bank (HDFCB IN: INR1,211.40, BUY)• Hero MotoCorp (HMCL IN: INR2,935.40, BUY)• Hindustan Unilever (HUVR IN: INR802.85, BUY)• Housing Development Finance Corp. Ltd. (HDFC IN: INR1,249.80, HOLD)• Infosys (INFO IN: INR920.00, BUY)• ITC Limited (ITC IN: INR227.85, BUY)• Larsen & Toubro (LT IN: INR1,370.45, BUY)• LIC Housing Finance Limited (LICHF IN: INR518.40, BUY)• Mahindra & Mahindra Limited (MM IN: INR1,239.85, UNDERPERFORM)• Mahindra and Mahindra Financial Services Limited (MMFS IN: INR272.65, HOLD)• Maruti Suzuki India Limited (MSIL IN: INR4,950.90, UNDERPERFORM)• NTPC (NTPC IN: INR159.05, BUY)• Shriram Transport Finance Company Limited (SHTF IN: INR831.75, HOLD)• State Bank of India (SBIN IN: INR275.80, BUY)• Tata Consultancy Services (TCS IN: INR2,125.10, BUY)• Tata Motors (TTMT IN: INR471.25, BUY)• Voltas Limited (VOLT IN: INR292.70, BUY)

For Important Disclosure information on companies recommended in this report, please visit our website at https://javatar.bluematrix.com/sellside/Disclosures.action or call 212.284.2300.

Distribution of RatingsIB Serv./Past 12 Mos.

Rating Count Percent Count Percent

BUY 1106 52.15% 325 29.39%HOLD 858 40.45% 168 19.58%UNDERPERFORM 157 7.40% 17 10.83%

Equity Strategy

India

21 November 2016

page 20 of 22 , Equity Analyst, +91 22 4224 6111, [email protected] Chellappa

Please see important disclosure information on pages 18 - 22 of this report.