entrepreneurship i class #3 financing the venture

Post on 18-Dec-2015

217 views

TRANSCRIPT

Entrepreneurship I

Class #3

Financing the Venture

CCarryer Consulting

9/19/01 2

• Cash is king• Cash flow is queen

9/19/01 3

Timing

• When do you look for cash?– More cash vs. less cash– Cash sooner vs. later– Less risky cash vs. more risky

• At least 6 months to raise capital• Balance between cash needs and

dilution

9/19/01 4

Funding Sources

Banks

Angels

VCSweat Grants

Friends&Family Partnerships

9/19/01 5

Types of Financing

• Debt• Equity• Variations – convertible debt• Advances on product sales• Technical development (partner)

9/19/01 6

First Step

• Credit cards• Family loans/investment• Partnerships

– customers– suppliers– joint venture– corporate

9/19/01 7

Stages

• Startup capital• Seed funding – often angels (individuals)• Early stage financing (VC):

– First round – series A– Development stage – second round, series B– Expansion stage – third round, series C– Growth stage – Series D, mezzanine

financing

• Private placements• Public offerings – IPO

9/19/01 8

Stock classes

• Common stock• Preferred stock• Convertible debenture• Loan with warrants

9/19/01 9

Venture Capital

5-10x return

1 out of 10 are hits

Invest at least $2mm

Change the world, disruptive technologies

Industry focus

Physical location is important

Hard to get

Business plan and presentationFounder/management is key

Large = $500mm

9/19/01 10

VC funds• Cash pooled by pension & endowment

funds and wealthy individuals• Expect returns of 50-60% on high risk

investments• About 7% of these investments account

for 60% of the profits• One third results in partial or total loss• Each project must represent a home run

9/19/01 11

VC continued

• Large markets > $100 mm• Companies worth $1b in sales• Dominated by popular industry (software,

internet, bio)• Arthur Rock limits his investments to

those that can “change the world”• VC dollars have quintupled from $.5b in

1990 to $12b in 1997 to $100b in 2000• $8.2b invested in 2nd qtr 2001 (669

companies)

9/19/01 12

• More than 30% decline from lass year• Silicon Valley is #1 in number of deals and dollars

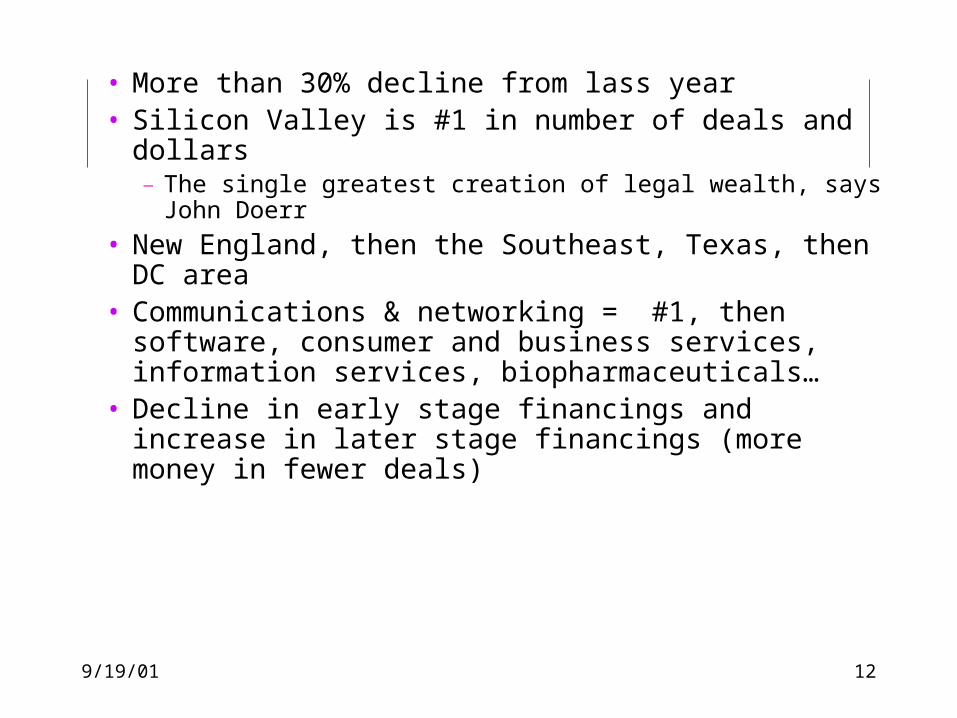

– The single greatest creation of legal wealth, says John Doerr

• New England, then the Southeast, Texas, then DC area

• Communications & networking = #1, then software, consumer and business services, information services, biopharmaceuticals…

• Decline in early stage financings and increase in later stage financings (more money in fewer deals)

9/19/01 13

Pittsburgh VC

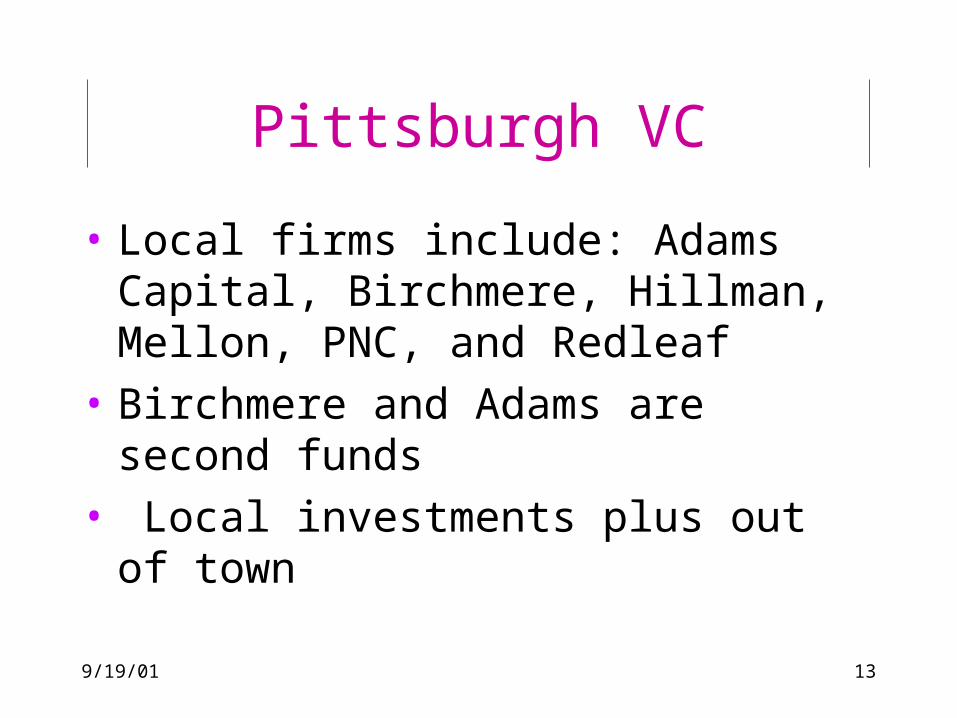

• Local firms include: Adams Capital, Birchmere, Hillman, Mellon, PNC, and Redleaf

• Birchmere and Adams are second funds

• Local investments plus out of town

9/19/01 14

Challenges with VC Funding

• VC money is hard to get• Early stage money is even harder• Must have an introduction• Importance is founders not the idea• Good business plan• Solid strategy for entering the market

and growth• Not usually seed capital• Investments of ~ $2m

9/19/01 15

Remember...

• Value added• The earlier you get VC funding, the

more you give away– Management team experience– Risk– Reward

9/19/01 16

Angels

• Private offering is viable alternative• 30-40% of companies end up getting

private equity funding• $5-10b invested annually in 20-30K

companies• $20-50K is typical• Many are entrepreneurs who want to

help and invest in other entrepreneurs

9/19/01 17

More on Angels

• Individuals and syndicates – Private investors group– Band of angels

• May take considerable equity• May try to dominate venture• Don’t like it if you miss profit/sales

goals

9/19/01 18

Remember...

• Finding angels can be hard• Tremendous value added

– knowledge of markets and technologies

– contacts– strategies

• Fees of investment bankers & attorneys may need to be paid regardless of success

9/19/01 19

Mind set

Operational

Breakeven

Hi value

Crack team

Check growth

Cash vs profitsCredit

Bootstrapping

9/19/01 20

Bootstrapping

• Different mind set – resource utilization

• Get operational quickly• Quick breakeven, cash generating

projects• Short term focus vs. long term

growth• Offer high value products or services

9/19/01 21

Bootstrapping continued

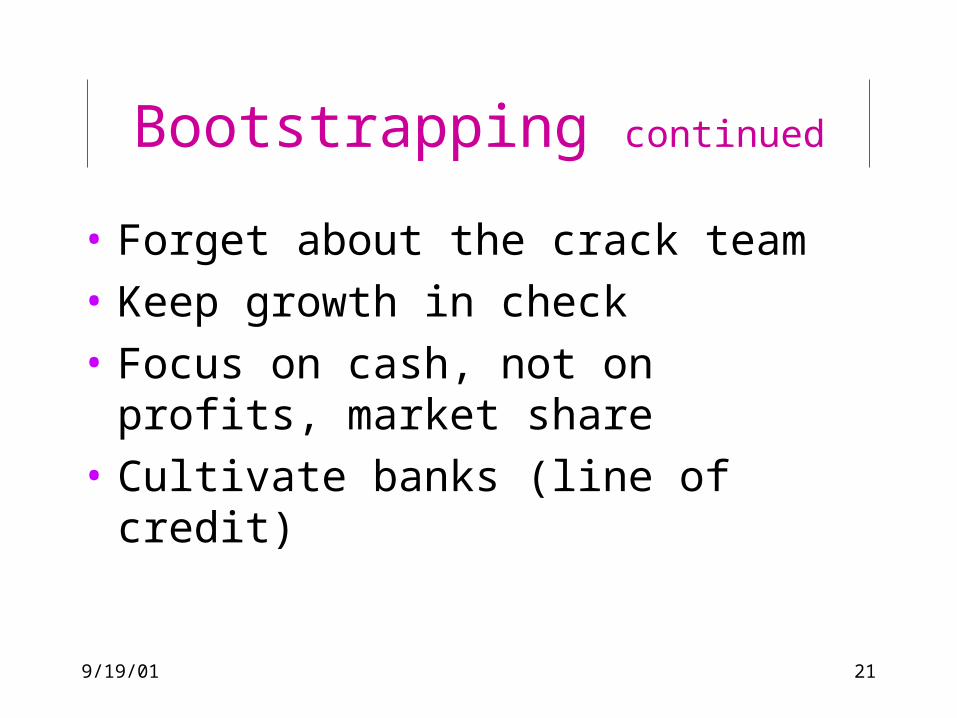

• Forget about the crack team• Keep growth in check • Focus on cash, not on profits,

market share• Cultivate banks (line of credit)

9/19/01 22

Exit Strategies

Sale or merger

IPO

Transfer of ownership

9/19/01 23

So,

• There’s a lot of good ideas• There’s a lot of money• There’s more money than good

ideas• There’s only a few great

opportunities• Those get financed