emmanuel saez berkeleysaez/course131/taxsavings.pdf · emmanuel saez berkeley 1. ... incidence...

TRANSCRIPT

131: Public Economics

Taxes on Capital and Savings

Emmanuel Saez

Berkeley

1

MOTIVATION

1) Capital income is about 25% of national income (labor

income is 75%) but distribution of capital income is much

more unequal than labor income

Capital income inequality is due to differences in savings be-

havior but also inheritances received

⇒ Equity suggests it should be taxed more than labor

2) Capital Accumulation correlated strongly with growth [al-

though causality link is not obvious] and capital accumulation

might be sensitive to the net-of-tax return.

⇒ Efficiency cost of capital taxation might be high.

2

MOTIVATION

3) Capital more mobile internationally than labor

Key distinction is residence vs. source base capital taxation:

Residence: Capital income tax based on residence of owner

of capital.

Most individual income tax systems are residence based (with

credits for taxes paid abroad)

Incidence falls on the owner ⇒ can only escape tax through

tax evasion (tax heavens) or changing residence (mobility)

Tax evasion through tax heavens is a very serious concern

(Zucman QJE’13)

3

Source: Capital income tax based on location of capital (cor-

porate income tax except US)

Incidence is then partly shifted to labor if capital is mobile.

Example: Open economy with fully mobile capital and source

taxation: net-of-tax rate of return is fixed by the international

rate of return r∗ so that (1 − τ)f ′(k) = r∗ where k is capital

stock per person

4) Capital taxation is extremely complex and provides many

tax avoidance opportunities

FACTS ABOUT WEALTH AND CAPITAL INCOME

Definition: Capital Income = Returns from Wealth Holdings

Aggregate US Personal Wealth = 3.5*GDP = $ 50 Tr

Tangible assets: residential real estate (land+buildings) [in-come = rents] and unincorporated business + farm assets[income = profits]

Financial assets: corporate stock [income = dividends + re-tained earnings], fixed claim assets (corporate and govt bonds,bank accounts) [income = interest]

Liabilities: Mortgage debt, Student loans, Consumer creditdebt

Substantial amount of financial wealth is held indirectly through:pension funds [DB+DC], mutual funds, insurance reserves

4

Private wealth / national income ratios, 1970-2010

100%

200%

300%

400%

500%

600%

700%

800%

1970 1975 1980 1985 1990 1995 2000 2005 2010Authors' computations using country national accounts. Private wealth = non-financial assets + financial assets - financial liabilities (household & non-profit sectors)

USA Japan

Germany France

UK Italy

Canada Australia

Source: Piketty and Zucman '13

Private wealth / national income ratios 1870-2010

100%

200%

300%

400%

500%

600%

700%

800%

1870 1890 1910 1930 1950 1970 1990 2010Authors' computations using country national accounts. Private wealth = non-financial assets + financial assets - financial liabilities (household & non-profit sectors)

USA

Europe

Source: Piketty and Zucman '13

The changing nature of national wealth, France 1700-2010

0%

100%

200%

300%

400%

500%

600%

700%

800%

1700 1750 1780 1810 1850 1880 1910 1920 1950 1970 1990 2010National wealth = agricultural land + housing + other domestic capital goods + net foreign assets

(% n

atio

nal i

ncom

e)

Net foreign assets

Other domestic capital

Housing

Agricultural land

Source: Piketty, Handbook chapter, 2014

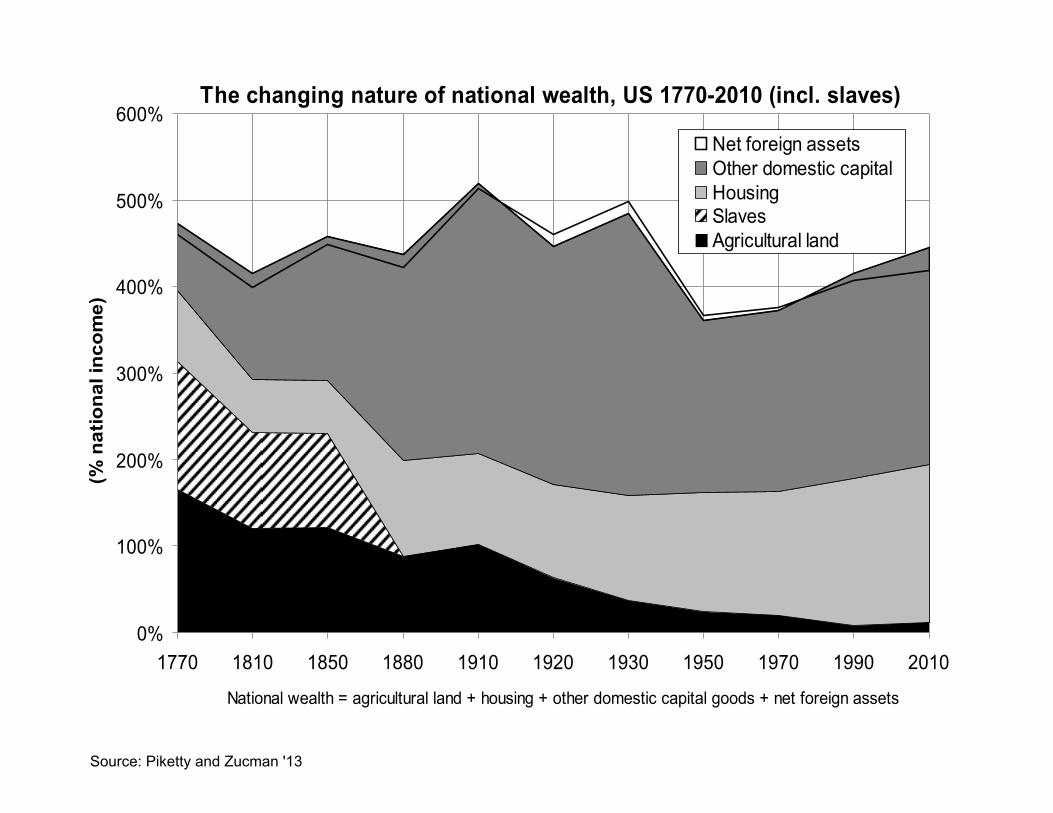

The changing nature of national wealth, US 1770-2010 (incl. slaves)

0%

100%

200%

300%

400%

500%

600%

1770 1810 1850 1880 1910 1920 1930 1950 1970 1990 2010

National wealth = agricultural land + housing + other domestic capital goods + net foreign assets

(% n

atio

nal i

ncom

e)

Net foreign assetsOther domestic capitalHousingSlavesAgricultural land

Source: Piketty and Zucman '13

FACTS ABOUT WEALTH AND CAPITAL INCOME

Wealth = W , Return = r, Capital Income = rW

Wt = Wt−1 + rtWt−1 + Et + It − Ct

where Wt is wealth at age t, Ct is consumption, Et labor in-

come earnings (net of taxes), rt is the average (net) rate of

return on investments and It net inheritances (gifts received

and bequests - gifts given).

Differences in Wealth and Capital income due to:

1) Age

2) past earnings, and past saving behavior Et − Ct [life cycle wealth]

3) Net Inheritances received It [transfer wealth]

4) Rates of return rt

6

WEALTH DISTRIBUTION

Wealth inequality is very large

US Household Wealth is divided 1/3,1/3,1/3 for the top 1%,the next 9%, and the bottom 90% [bottom 1/3 householdshold almost no wealth]

Financial wealth is more unequally distributed than (net) realestate wealth

Share of real estate wealth falls at the top of the wealth dis-tribution

Growth of private pensions [such as 401(k) plans] has “de-mocratized” stock ownership in the US

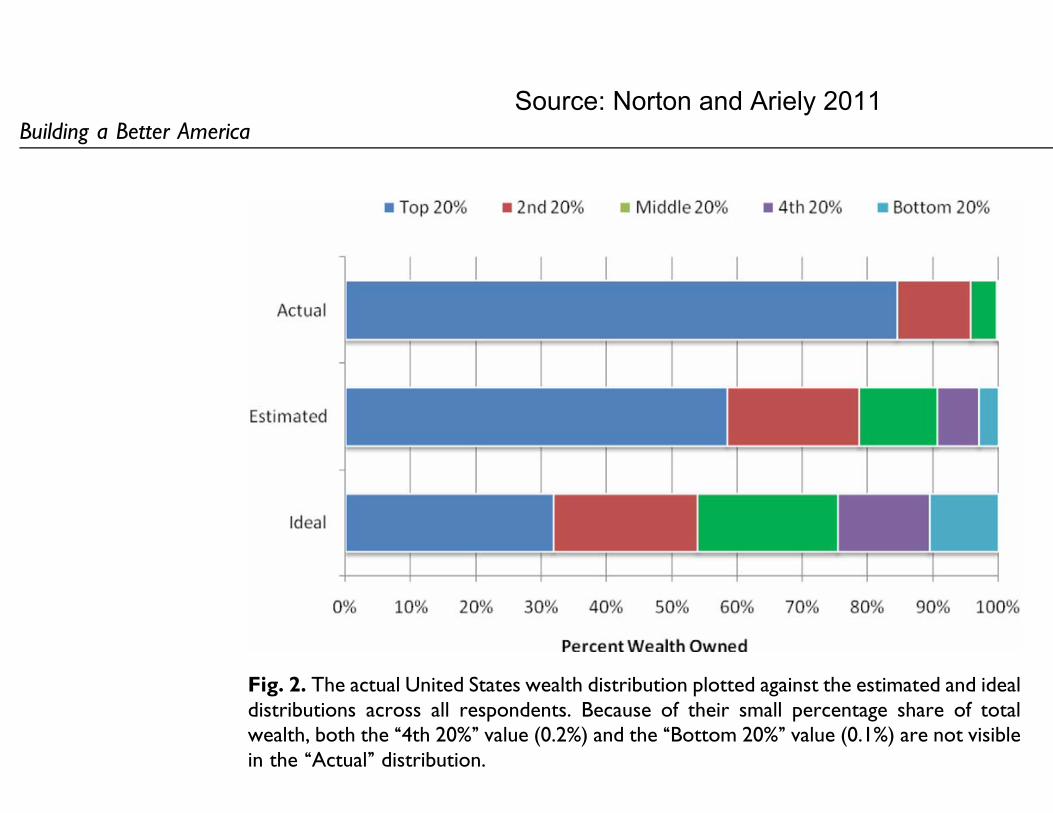

US public underestimates extent of wealth inequality and thinksthe ideal wealth distribution should be a lot less unequal [Norton-Ariely ’11]

7

agreed that such redistribution should take the form of moving

wealth from the top quintile to the bottom three quintiles. In

short, although Americans tend to be relatively more

favorable toward economic inequality than members of other

countries (Osberg & Smeeding, 2006), Americans’ consensus

about the ideal distribution of wealth within the United States

Fig. 3. The actual United States wealth distribution plotted against the estimated and idealdistributions of respondents of different income levels, political affiliations, and genders.Because of their small percentage share of total wealth, both the ‘‘4th 20%’’ value (0.2%)and the ‘‘Bottom 20%’’ value (0.1%) are not visible in the ‘‘Actual’’ distribution.

Fig. 2. The actual United States wealth distribution plotted against the estimated and idealdistributions across all respondents. Because of their small percentage share of totalwealth, both the ‘‘4th 20%’’ value (0.2%) and the ‘‘Bottom 20%’’ value (0.1%) are not visiblein the ‘‘Actual’’ distribution.

Building a Better America 11

at Harvard Libraries on February 3, 2011pps.sagepub.comDownloaded from

Source: Norton and Ariely 2011

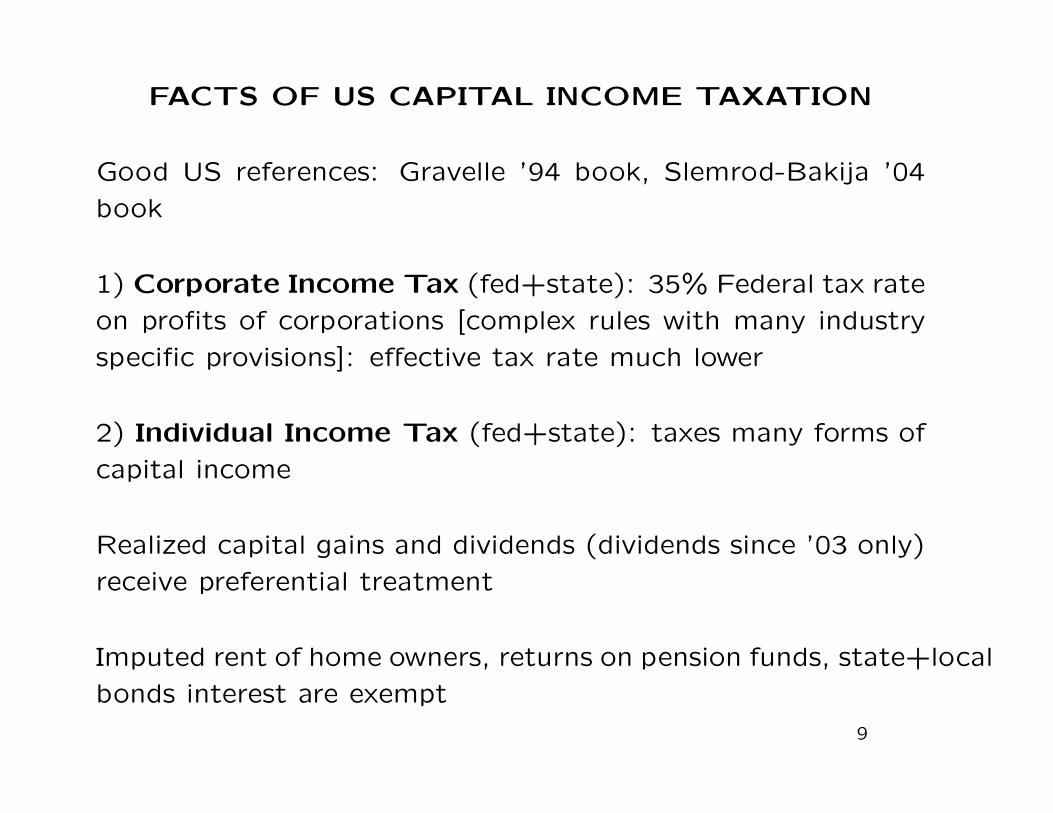

FACTS OF US CAPITAL INCOME TAXATION

Good US references: Gravelle ’94 book, Slemrod-Bakija ’04

book

1) Corporate Income Tax (fed+state): 35% Federal tax rate

on profits of corporations [complex rules with many industry

specific provisions]: effective tax rate much lower

2) Individual Income Tax (fed+state): taxes many forms of

capital income

Realized capital gains and dividends (dividends since ’03 only)

receive preferential treatment

Imputed rent of home owners, returns on pension funds, state+local

bonds interest are exempt

9

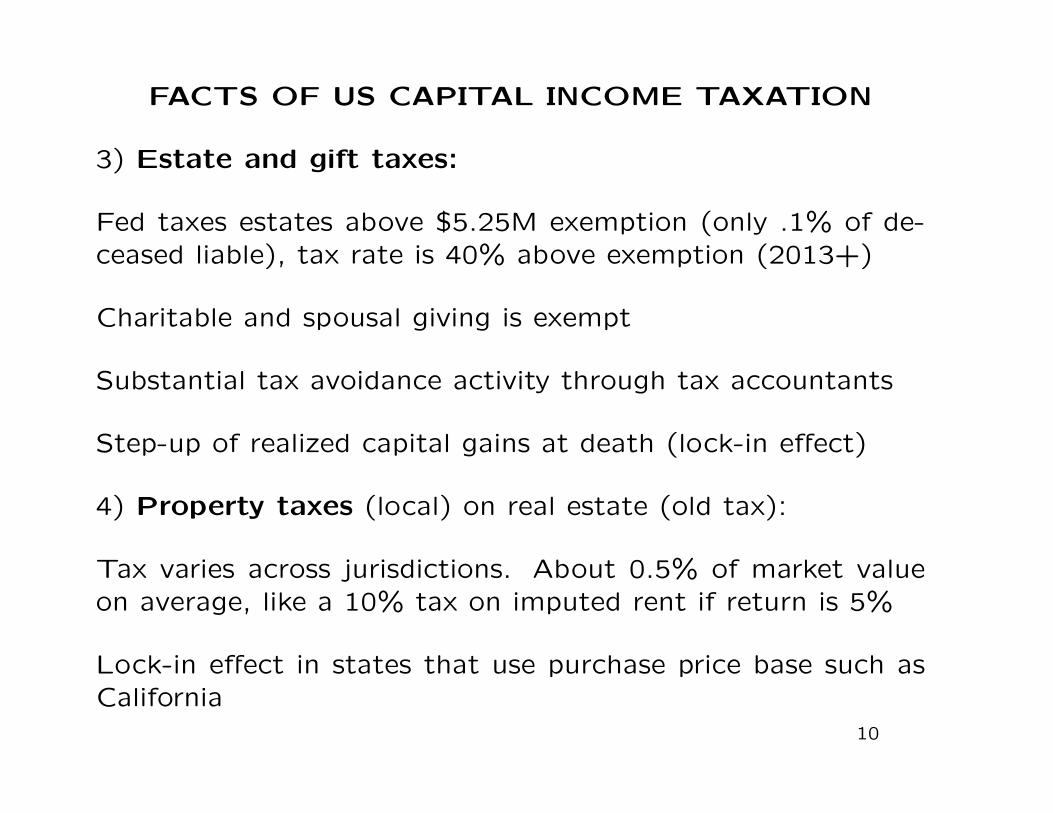

FACTS OF US CAPITAL INCOME TAXATION

3) Estate and gift taxes:

Fed taxes estates above $5.25M exemption (only .1% of de-ceased liable), tax rate is 40% above exemption (2013+)

Charitable and spousal giving is exempt

Substantial tax avoidance activity through tax accountants

Step-up of realized capital gains at death (lock-in effect)

4) Property taxes (local) on real estate (old tax):

Tax varies across jurisdictions. About 0.5% of market valueon average, like a 10% tax on imputed rent if return is 5%

Lock-in effect in states that use purchase price base such asCalifornia

10

LIFE CYCLE VS. INHERITED WEALTH

Economists divide existing wealth into 2 categories:

1) Life-cycle wealth is wealth due to savings earlier in yourlife (e.g., pension contributions, paying down a home mort-gage, etc.)

2) Inherited wealth is wealth due to inheritances received(e.g., receiving a house or a trust fund from parents)

Distinction matters for taxation because individuals are re-sponsible for life-cycle wealth but not inherited wealth [meri-tocracy vs. aristocracy]

Inherited wealth used to be very large in the past, becamesmall in post-World War II period, but is growing in recentdecades (especially in Europe)

11

Figure S11.3. The share of inherited wealth in aggregate wealth, France 1850-2100 (2010-2100: g=1,7%, r=3,0%)

30%

40%

50%

60%

70%

80%

90%

100%

1850 1870 1890 1910 1930 1950 1970 1990 2010 2030 2050 2070 2090

Partially capitalized inheritance(PPVR definition)

Non-capitalized inheritance(Modigliani)

Source: Piketty, Handbook chapter, 2014

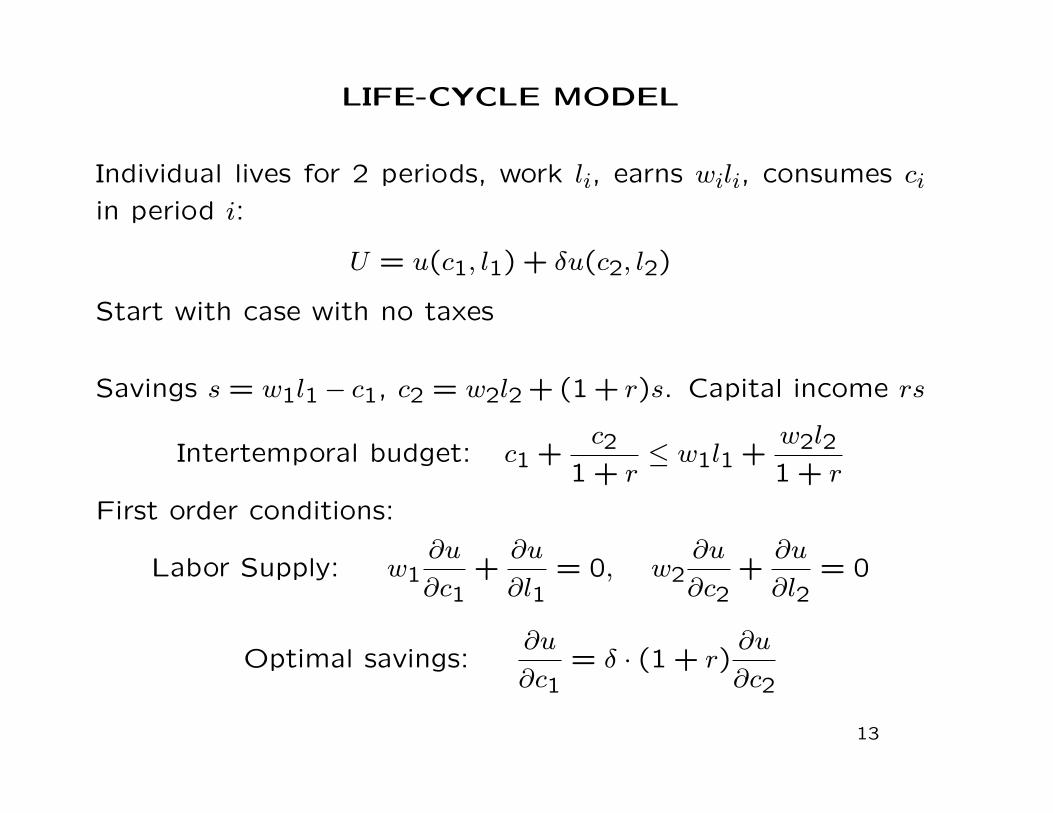

LIFE-CYCLE MODEL

Individual lives for 2 periods, work li, earns wili, consumes ciin period i:

U = u(c1, l1) + δu(c2, l2)

Start with case with no taxes

Savings s = w1l1− c1, c2 = w2l2 + (1 + r)s. Capital income rs

Intertemporal budget: c1 +c2

1 + r≤ w1l1 +

w2l21 + r

First order conditions:

Labor Supply: w1∂u

∂c1+

∂u

∂l1= 0, w2

∂u

∂c2+

∂u

∂l2= 0

Optimal savings:∂u

∂c1= δ · (1 + r)

∂u

∂c2

13

TAXES IN LIFE-CYCLE MODEL

Budget with consumption tax tc:

(1 + tc)[c1 + c2/(1 + r)] ≤ w1l1 + w2l2/(1 + r)

Budget with labor income tax τL:

c1 + c2/(1 + r) ≤ (1− τL)[w1l1 + w2l2/(1 + r)]

Consumption and labor income tax are equivalent if

1 + tc = 1/(1− τL)

Both taxes distort only labor supply and not savings

Labor Supply: wi(1− τL)∂u

∂ci+∂u

∂li= 0

14

TAXES IN LIFE-CYCLE MODEL

Budget with capital income tax τK:

c1 + c2/(1 + r(1− τK)) ≤ w1l1 + w2l1/(1 + r(1− τK))

τK distorts only savings choice (and not labor supply)

Optimal savings:∂u

∂c1= δ · (1 + r(1− τK))

∂u

∂c2

Budget with comprehensive income tax τ :

c1 + c2/(1 + r(1− τ)) ≤ (1− τ)[w1l1 + w2l2/(1 + r(1− τ))]

τ distorts both labor supply and savings

τ imposes “double” tax: (1) tax on earnings, (2) tax on sav-

ings

15

EFFECT OF CAPITAL TAX ON SAVINGS

Consider simpler model (fixed earnings and in period 1 only)

maxc1,c2

u(c1) + δu(c2) subject to c1 +c2

1 + r(1− τK)≤ w

Suppose τK increases and hence 1/[1 + r(1− τK)] ↑

1) Substitution effect: price of c2 ↑ ⇒ c2 ↓, c1 ↑ ⇒ savings

s = w1 − c1 ↓.

2) Income effect: Price of c2 ↑ ⇒ consumer is poorer and both

c1 and c2 ↓ ⇒ save more

Total net effect is theoretically ambiguous ⇒ τK has ambigu-

ous effects on s

16

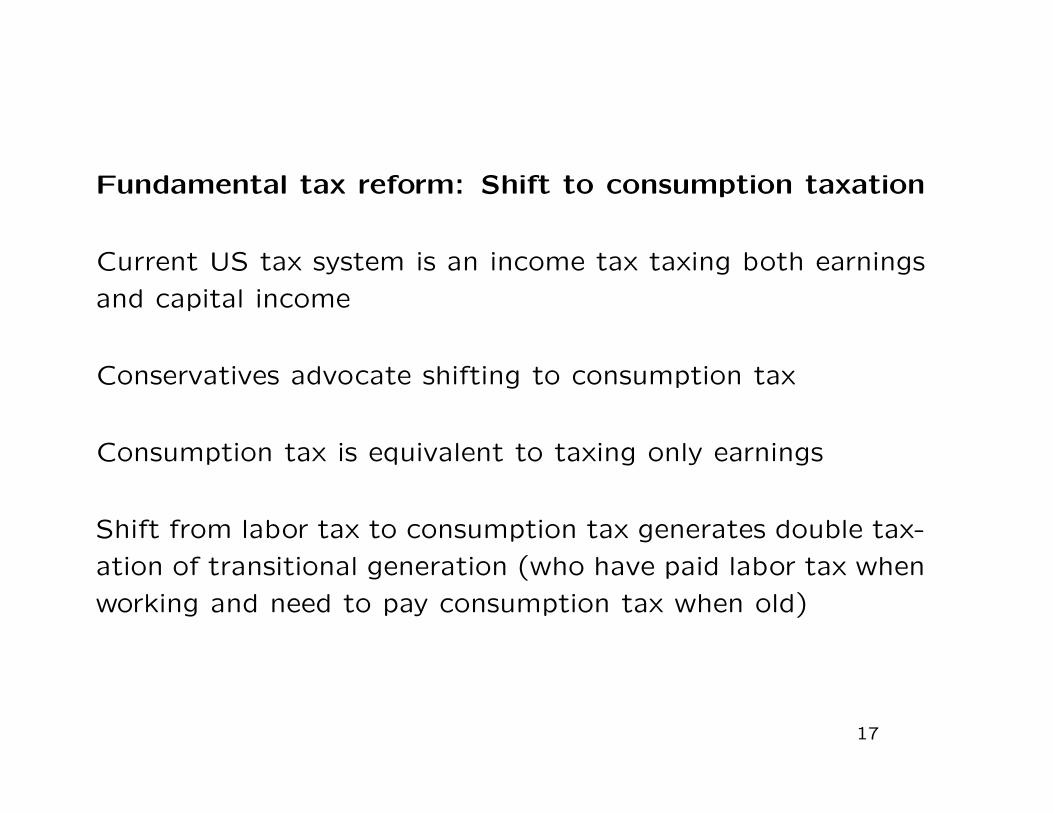

Fundamental tax reform: Shift to consumption taxation

Current US tax system is an income tax taxing both earnings

and capital income

Conservatives advocate shifting to consumption tax

Consumption tax is equivalent to taxing only earnings

Shift from labor tax to consumption tax generates double tax-

ation of transitional generation (who have paid labor tax when

working and need to pay consumption tax when old)

17

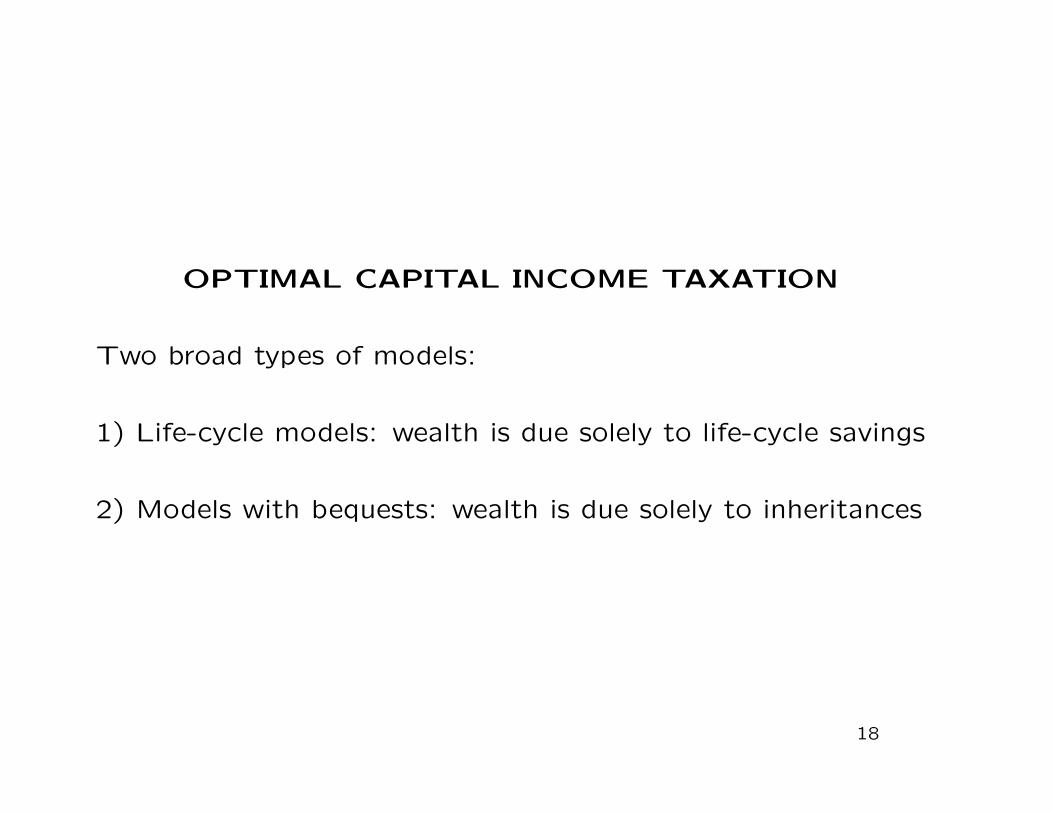

OPTIMAL CAPITAL INCOME TAXATION

Two broad types of models:

1) Life-cycle models: wealth is due solely to life-cycle savings

2) Models with bequests: wealth is due solely to inheritances

18

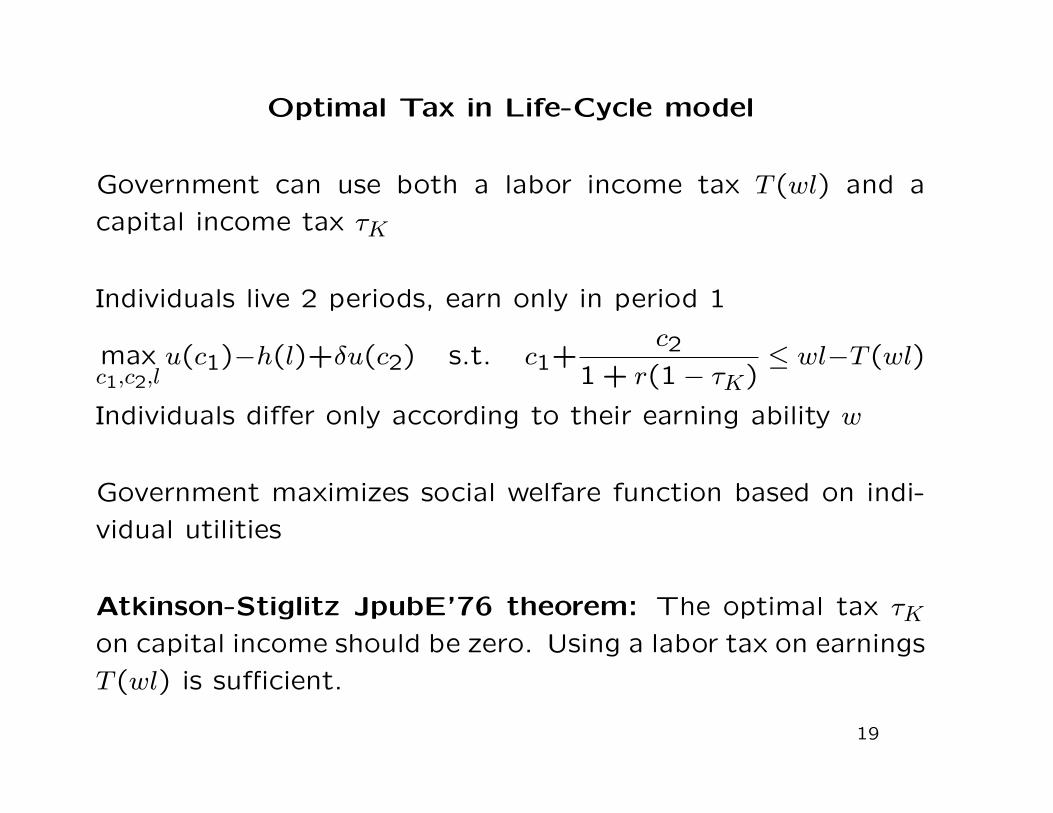

Optimal Tax in Life-Cycle model

Government can use both a labor income tax T (wl) and a

capital income tax τK

Individuals live 2 periods, earn only in period 1

maxc1,c2,l

u(c1)−h(l)+δu(c2) s.t. c1+c2

1 + r(1− τK)≤ wl−T (wl)

Individuals differ only according to their earning ability w

Government maximizes social welfare function based on indi-

vidual utilities

Atkinson-Stiglitz JpubE’76 theorem: The optimal tax τKon capital income should be zero. Using a labor tax on earnings

T (wl) is sufficient.

19

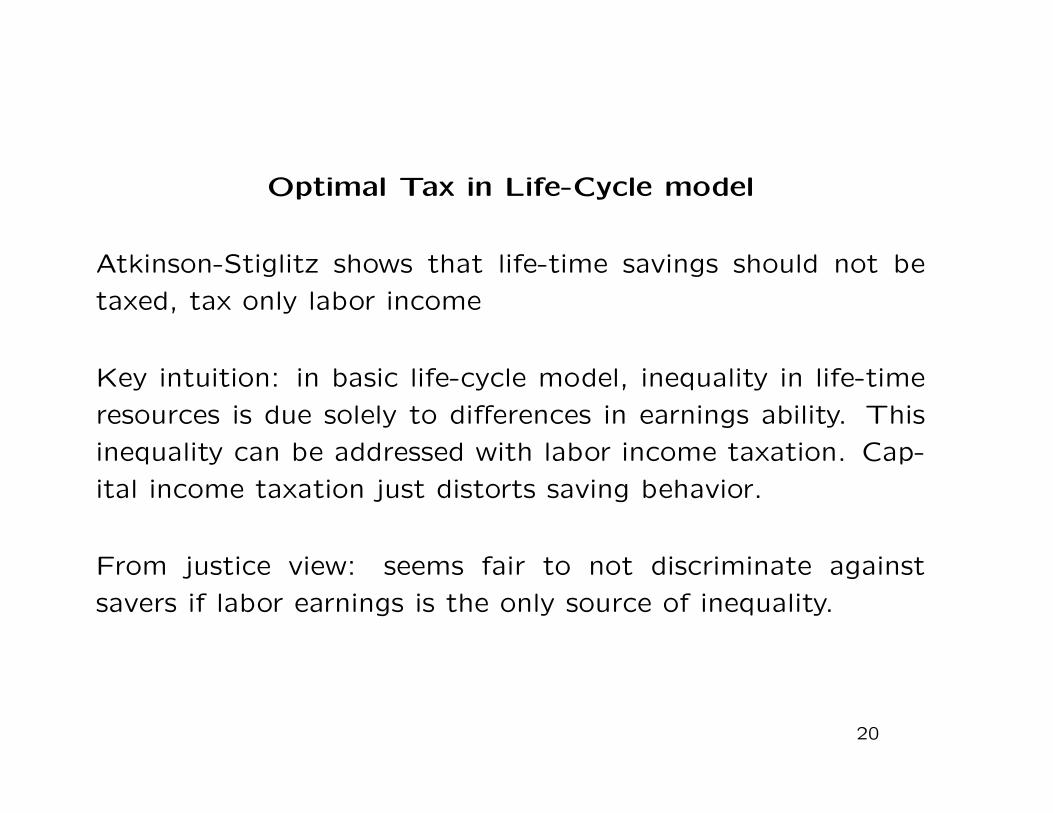

Optimal Tax in Life-Cycle model

Atkinson-Stiglitz shows that life-time savings should not be

taxed, tax only labor income

Key intuition: in basic life-cycle model, inequality in life-time

resources is due solely to differences in earnings ability. This

inequality can be addressed with labor income taxation. Cap-

ital income taxation just distorts saving behavior.

From justice view: seems fair to not discriminate against

savers if labor earnings is the only source of inequality.

20

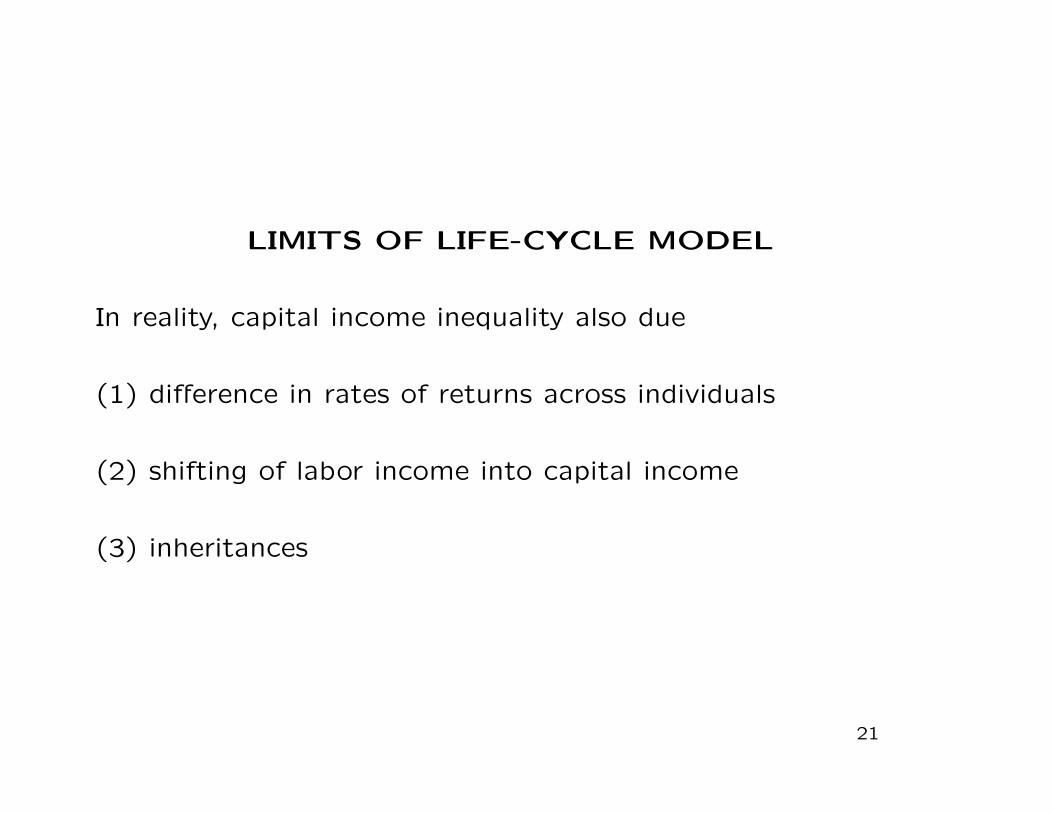

LIMITS OF LIFE-CYCLE MODEL

In reality, capital income inequality also due

(1) difference in rates of returns across individuals

(2) shifting of labor income into capital income

(3) inheritances

21

SHIFTING OF LABOR / CAPITAL INCOME

In practice, difficult to distinguish between capital and laborincome [e.g., small business profits, professional traders]

Differential tax treatment can induce shifting

(1) Carried interest in the US: hedge fund and private equityfund managers receive fraction of profits of assets they managefor clients. Those profits are really labor income but are taxedas realized capital gains

(2) Finnish Dual income tax system: taxes separately capitalincome at preferred rates since 1993: Pirttila and Selin SJE’11show that it induced shifting from labor to capital incomeespecially among self-employed

With income shifting, taxing capital income becomes desirableto avoid shifting

22

Taxation of Inheritances: Welfare Effects

Definitions: donor is the person giving, donee is the person

receiving

Inheritances and inter-vivos transfers raise difficult issues:

(1) Inequality in inheritances contributes to economic inequal-

ity: seems fair to redistribute from those who received inheri-

tances to those who did not

(2) However, it seems unfair to double tax the donors who

worked hard to pass on wealth to children

⇒ Double welfare effect: inheritance tax hurts donor (if donor

altruistic to donee) and donee (which receives less) [Kaplow,

’01]

23

Taxation of Inheritances: Behavioral Responses

Potential behavioral response effects of inheritance tax:

(1) reduces wealth accumulation of altruistic donors (and hencetax base) [no very good empirical evidence, Slemrod-Kopczuk01]

(2) reduces labor supply of altruistic donors (less motivatedto work if cannot pass wealth to kids) [no good evidence]

(3) induces donees to work more through income effects (Carnegieeffect, decent evidence from Holtz-Eakin,Joulfaian,Rosen QJE’93)

Critical to understand why there are inheritances to decide onoptimal inheritance tax policy. 4 main models of bequests:(a) accidental, (b) bequests in the utility, (c) manipulativebequest motive

24

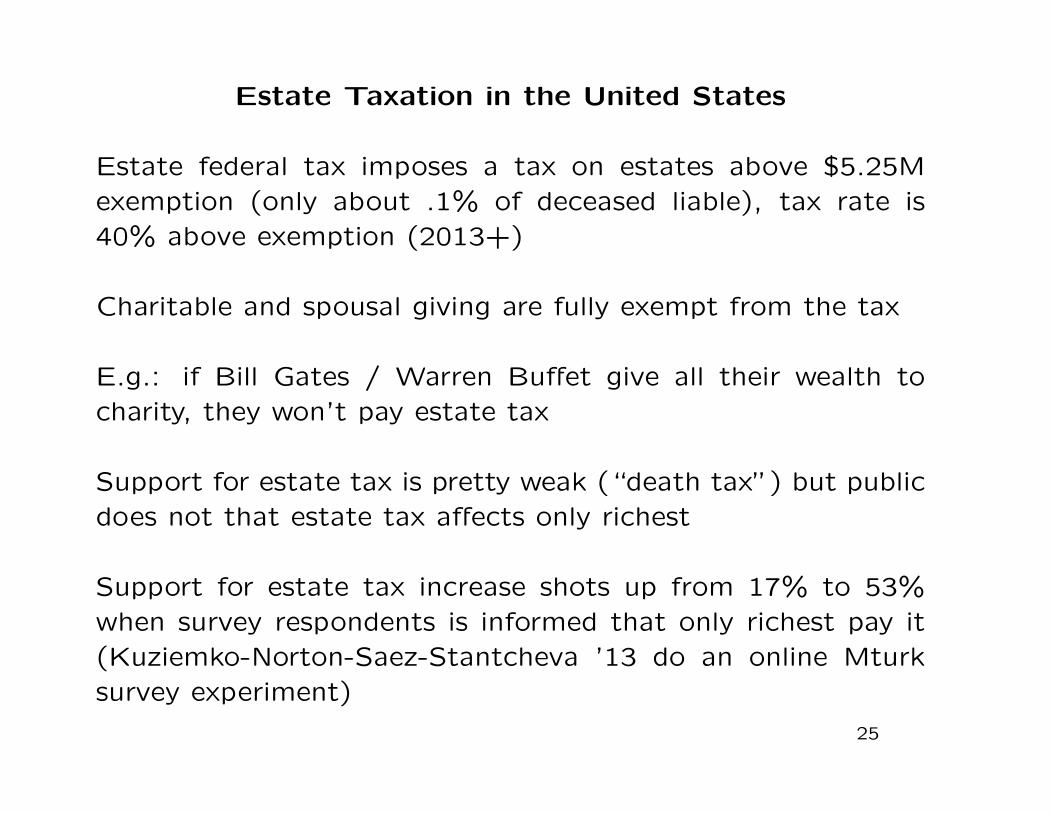

Estate Taxation in the United States

Estate federal tax imposes a tax on estates above $5.25Mexemption (only about .1% of deceased liable), tax rate is40% above exemption (2013+)

Charitable and spousal giving are fully exempt from the tax

E.g.: if Bill Gates / Warren Buffet give all their wealth tocharity, they won’t pay estate tax

Support for estate tax is pretty weak (“death tax”) but publicdoes not that estate tax affects only richest

Support for estate tax increase shots up from 17% to 53%when survey respondents is informed that only richest pay it(Kuziemko-Norton-Saez-Stantcheva ’13 do an online Mturksurvey experiment)

25

Treatment example: Information about the Estate Tax

14

ACCIDENTAL BEQUESTS

People die with a stock of wealth they intended to spend onthemselves: Such bequests arise because of imperfect annuitymarkets

Annuity is an insurance contract converting lumpsum amountinto a stream of payments till end of life [insurance againstrisk of living too long]

Annuity markets are imperfect because of adverse selection[Finkelstein-Poterba EJ’02, JPE’04] or behavioral reasons [in-ertia, lack of planning]

Public retirement programs [and defined benefit private pen-sions] are in general annuities

Newer defined contribution private pensions [401(k)s in theUS] are in general not annuitized

27

ACCIDENTAL BEQUESTS

Bequest taxation has no distortionary effect on behavior ofdonor and can only increase labor supply of donees (throughincome effects) ⇒ strong case for taxing bequests heavily

Kopczuk JPE ’03 makes the point that estate tax plays therole of a subsitute annuity:

Estate tax paid by those who die early, and not by those whodie late ⇒ Implicit insurance against risk of living too long

Wealth loving: Same tax policy conclusion arises if donorshave wealth in their utility function [social status or power,Carroll ’98]

Surveys show that bequest motives are not the main driver ofwealth accumulation (Kopczuk-Lupton ’07)

28

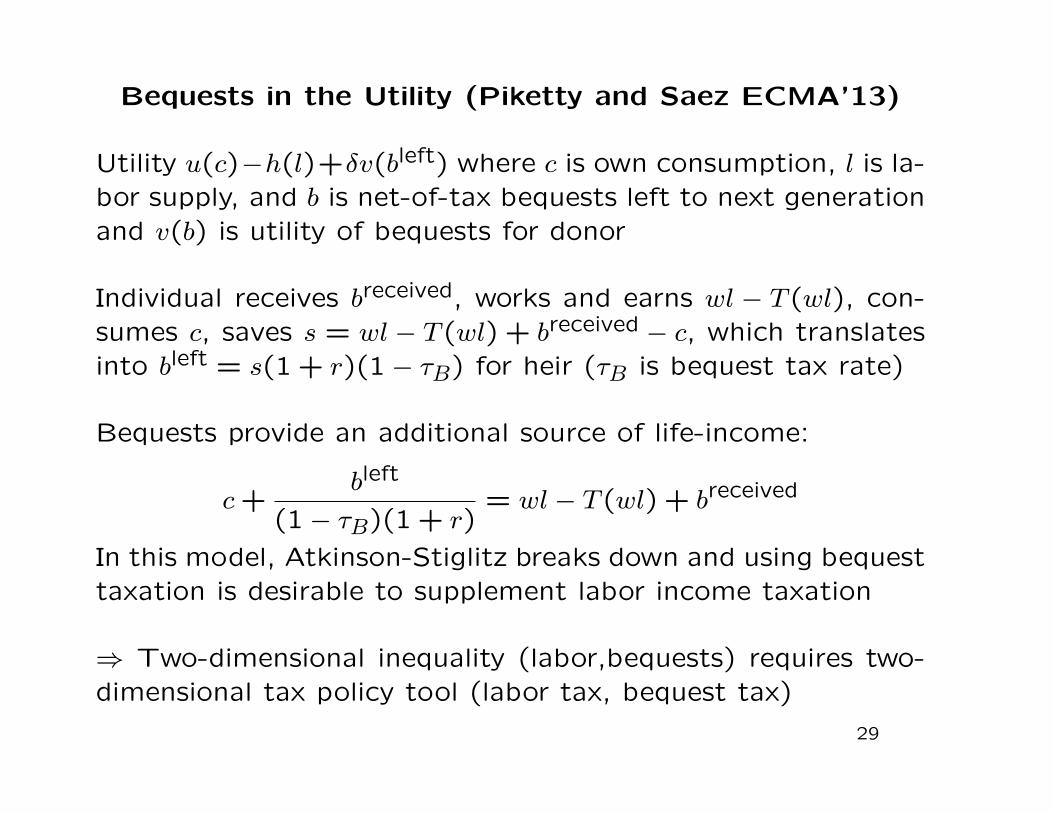

Bequests in the Utility (Piketty and Saez ECMA’13)

Utility u(c)−h(l)+δv(bleft) where c is own consumption, l is la-bor supply, and b is net-of-tax bequests left to next generationand v(b) is utility of bequests for donor

Individual receives breceived, works and earns wl − T (wl), con-sumes c, saves s = wl − T (wl) + breceived − c, which translatesinto bleft = s(1 + r)(1− τB) for heir (τB is bequest tax rate)

Bequests provide an additional source of life-income:

c+bleft

(1− τB)(1 + r)= wl− T (wl) + breceived

In this model, Atkinson-Stiglitz breaks down and using bequesttaxation is desirable to supplement labor income taxation

⇒ Two-dimensional inequality (labor,bequests) requires two-dimensional tax policy tool (labor tax, bequest tax)

29

MANIPULATIVE BEQUESTS

Parents use potential bequest to extract favors from children

Empirical Evidence: Bernheim-Shleifer-Summers JPE ’85 show

that number of visits of children to parents is correlated with

bequeathable wealth but not annuitized wealth of parents

Visitsi = α+β Bequeathable Wealthi+γ Annuitized wealthi+εi

They find β > 0 and γ = 0 (but causality not clear)

⇒ Bequest becomes one additional form of labor income for

donee and one consumption good for donor

⇒ Inheritances should be counted and taxed as labor income

for donees

30

SOCIAL-FAMILY PRESSURE BEQUESTS

Parents may not want to leave bequests but feel compelledto by pressure of heirs or society: bargaining between parentsand children

With estate tax, parents do not feel like they need to give asmuch ⇒ parents are made better-off by the estate tax ⇒ Casefor estate taxation stronger

Empirical evidence:

Aura JpubE’05: reform of private pension annuities in the USin 1984 requiring both spouses signatures when worker decidesto get a single annuity or couple annuity: reform increasessharply couple annuities choice

Equal division of estates [Wilhelm AER’96, McGarry]: estatesare very often divided equally but gifts are not

31

REFERENCES

Atkinson, A.B. and J. Stiglitz “The design of tax structure: Direct versusindirect taxation”, Journal of Public Economics, Vol. 6, 1976, 55-75.(web)

Aura, S. “Does the Balance of Power Within a Family Matter? The Caseof the Retirement Equity Act”, Journal of Public Economics, Vol. 89,2005, 1699-1717. (web)

Bernheim, B. D., A. Shleifer, and L. Summers “The Strategic BequestMotive”, Journal of Political Economy, Vol. 93, 1985, 1045-76. (web)

Carroll, C. “Why Do the Rich Save So Much?”, NBER Working Paper No.6549, 1998. (web)

Christiansen, Vidar and Matti Tuomala “On taxing capital income withincome shifting”, International Tax and Public Finance, Vol. 15, 2008,527-545. (web)

DeLong, J.B. “Bequests: An Historical Perspective,” in A. Munnell, ed.,The Role and Impact of Gifts and Estates, Brookings Institution, 2003(web)

Diamond, Peter and Emmanuel Saez “The Case for a Progressive Tax:From Basic Research to Policy Recommendations”, Journal of EconomicPerspectives, 25(4), Fall 2011, 165-190. (web)

32

Finkelstein A. and J. Poterba, “Adverse Selection in Insurance Markets:Policyholder Evidence from the U.K. Annuity Market”, Journal of PoliticalEconomy, Vol. 112, 2004, 183-208. (web)

Finkelstein A. and J. Poterba, “Selection Effects in the United KingdomIndividual Annuities Market”, The Economic Journal, Vol. 112, 2002,28-50. (web)

Gordon, R.H. and J. Slemrod “Are “Real” Responses to Taxes SimplyIncome Shifting Between Corporate and Personal Tax Bases?,” NBERWorking Paper, No. 6576, 1998. (web)

Holtz-Eakin, D., D. Joulfaian and H.S. Rosen “The Carnegie Conjecture:Some Empirical Evidence”, Quarterly Journal of Economics Vol. 108, May1993, pp.288-307. (web)

Kaplow, L. “A Framework for Assessing Estate and Gift Taxation”, inGale, William G., James R. Hines Jr., and Joel Slemrod (eds.) Rethinkingestate and gift taxation Washington, D.C.: Brookings Institution Press,2001. (web)

Kopczuk, W. “The Trick Is to Live: Is the Estate Tax Social Security forthe Rich?”, The Journal of Political Economy, Vol. 111, 2003, 1318-1341.(web)

Kopczuk, Wojciech and Joseph Lupton 2007. “To Leave or Not to Leave:The Distribution of Bequest Motives,” Review of Economic Studies, 74(1),207-235. (web)

Kopczuk, Wojciech and Emmanuel Saez “Top Wealth Shares in the UnitedStates, 1916-2000: Evidence from Estate Tax Returns”, National TaxJournal, 57(2), Part 2, June 2004, 445-487. (web)

Kopczuk, Wojciech and Joel Slemrod, “The Impact of the Estate Tax onthe Wealth Accumulation and Avoidance Behavior of Donors”, in WilliamG. Gale, James R. Hines Jr., and Joel B. Slemrod (eds.), Rethinking Estateand Gift Taxation, Washington, DC: Brookings Institution Press, 2001,299-343. (web)

Kuziemko, Ilyana, Michael I. Norton, Emmanuel Saez, and Stefanie Stantcheva“How Elastic are Preferences for Redistribution? Evidence from Random-ized Survey Experiments,” NBER Working Paper No. 18865, 2013. (web)

Modigliani, F. “The Role of Intergenerational Transfers and Lifecyle Sav-ings in the Accumulation of Wealth”, Journal of Economic Perspectives,Vol. 2, 1988, 15-40. (web)

Norton, M. and D. Ariely “Building a Better America–One Wealth Quintileat a Time”, Perspectives on Psychological Science 2011 6(9). (web)

Piketty, T. “On the Long-Run Evolution of Inheritance: France 1820-2050”, Quarterly Journal of Economics, 126(3), 2011, 1071-1131. (web)

Piketty, T. “Wealth and Inheritance in the Long-Run”, Handbook of In-come Distribution, Volume 2, Elsevier-North Holland, in preparation (slidesApril 2013) (web)

Piketty, T. and G. Zucman “Capital is Back: Wealth-Income Ratios inRich Countries, 1870-2010”, in preparation (slides March 2013) (web)

Pirttila, Jukka and Hakan Selin, “Income shifting within a dual income taxsystem: evidence from the Finnish tax reform,” Scandinavian Journal ofEconomics, 113(1), 120-144, 2011. (web)

Wilhelm, Mark O. “Bequest Behavior and the Effect of Heirs’ Earnings:Testing the Altruistic Model of Bequests,” American Economic Review,86(4), 1996, 874-892. (web)

Zucman, G. “The Missing Wealth of Nations: Are Europe and the US NetDebtors or Net Creditors”, forthcoming Quarterly Journal of Economics,2013. (web)